Abstract

This study explores the driving factors for attracting Foreign Direct Investment (FDI) inflow in the Saudi Arabian economy in two stages. First, it applies a general to specific approach to form a model reflecting theoretical and anecdotal evidence of the Saudi Arabian economy. Second, we analyse time series data over the years 1984 to 2018. applying Autoregressive Distributed Lags (ARDL) approach, incorporating several structural breaks. This study explores Saudi membership of the World Trade Organization (WTO) and institutional quality, identifying them as promising factors in fostering FDI inflows in the economy. Our empirical investigation demonstrates that the Saudi economy experienced a higher inflow of FDI during the global financial crisis (GFC) due to economic stability. Trade openness is found to be conducive to promote FDI inflow. This study provides several policy implications.

Introduction

The government of Saudi Arabia aspires to lessen the reliance on hydrocarbon economy by diversifying the economy in its Vision 2030. An important instrument proposed to accelerate this process is foreign direct investment (FDI) inflow, which directly benefits recipient economies in several ways. A substantial body of literature argues that FDI is an effective instrument to boost economic growth and development for many countries (e.g., Al-Mamun & Sohag, 2015; Aziz & Mishra, 2016; Boğa, 2019; Joshua, Rotimi et al., 2020). In addition, FDI inflow is an important factor to amplify public welfare by increasing employment opportunities and labor expertise (Boğa, 2019). Importantly, FDI functions as a channel to promote transmission of advanced technologies to the country which eventually in return enhance economic growth (Aziz & Mishra, 2016; Boğa, 2019). Another key advantage of FDI is that it promotes global market competitiveness, which eventually fosters productivity in the domestic economy.

The dynamics of FDI inflow in the Saudi economy follow a particular equation due to its specific national characteristics. Significant oil revenues allow the government to contribute to a larger portion of the economy, which functions to narrow the economic base into a few major industries. The economy also experienced negative FDI inflow until 2004. Given the importance of FDI for the economy, the country adopted several policies, including World Trade Organization (WTO) membership. After WTO accession in December 2005, the economy experienced high inflows of FDI, even during the global financial crisis (GFC) of 2008 to 2009, while many developed countries experienced sluggish inflows. Accession to the WTO has direct and indirect impacts on FDI. Direct impacts include facilitating international corporations’ investments in WTO member states, with lower trade barriers, including tariffs, import quotas, and regulations. Indirect impacts include enhanced political globalization, which eventually enhances political institutions in the domestic countries. Given the plausible role of WTO membership on the Saudi economy, this study measures its dynamic impact on FDI inflow.

Prior literature argues that there is a link connecting FDI with institutional quality, whereby high-quality institutions reflect government solidity (Mina, 2012; Mohamed & Sidiropoulos, 2010). Conversely, political instability causes a country unattractive, negatively affect the business environment (Büthe & Milner, 2008), which could deactivate economic processes (Schneider & Frey, 1985). Many empirical studies prove that political instability has a detrimental impact to foreign direct investment (Schneider & Frey, 1985). Ali et al. (2010) show that quality of institution is a vital factor attracting FDI inflow, especially regarding economic institutions (e.g., property rights and contract enforcement). Bayraktar (2015) and Moran et al. (2018) argue that an improvement in the “ease of doing business” indicator is becoming a key factor in attracting more FDI to developing countries. Interestingly, the Saudi economy has proved to be a haven for FDI inflow, with the country enjoying higher inflows of FDI in the aftermath of the GFC due to its political and economic stability. Given the proven role of institutional quality, this study incorporates its role along with GFC to explain FDI inflow.

This study contributes to the economic literature in several ways. It extends the study by Aziz and Mishra (2016) to contextualize several exogenous structural breaks in the FDI inflow equation. Primarily, this study forms an appropriate empirical model through a general to a specific approach, reflecting the anecdotal evidence from economic analysts. Eventually, we form our model comprising economic and political variables by highlighting a plausible explanation defining FDI inflow in Saudi Arabia, which is reinforced by the national development agenda. Second, we incorporate the role of WTO membership along with institutional quality to explain the FDI inflow. We utilize a holistic measure of institutional quality suggested by international country risk guide. Third, the structural break is counted in our model, particularly the global financial crisis dummy.

Our findings are robust by considering short-run and long-run behavior under error correction framework. Our findings provide a new insight that WTO accession and higher institutional quality promote FDI inflow, even during the GFC. Trade openness galvanizes FDI inflow in the long run. The impact of financial development appears to be inclusive in explaining FDI inflow in Saudi Economy. This study provides several policy implications.

Section 2 reviews relevant literature to derive the tested hypotheses pertaining to institutional quality, WTO accession, and the GFC and FDI. Section 3 explains the rationale for studying Saudi Arabia. Section 4 presents the data and methods used, followed by presentation of the results in Section 5. Section 6 concludes the paper and identifies some policy implications.

Literature Review

Though not without its critiques, FDI is essentially seen as an effective tool to foster economic growth in many countries, particularly developing economies, as its inflows promote local economies in several ways. First, FDI is considered to be one of the most high-powered instruments to reduce poverty. To this end, FDI inflow enhances public welfare by increasing job opportunities and labor development (Boğa, 2019). Second, FDI functions as an essential method for mobilizing advanced technologies toward host countries from source countries, thereby promoting technological development and economic growth in the latter (Aziz & Mishra, 2016; Boğa, 2019). Nevertheless, maintaining economic openness and attracting foreign investments does not automatically guarantee FDI, which also seeks out economic stability in receiving countries. Benefiting from FDI requires a sound implementation plan and supporting investment policies. A growing number of studies stress the need to explore key determinants of FDI inflows in specific countries. Prior literature argues that various factors attract FDI inflow, including natural resources, cheap labor costs, favorable exchange rates, market size, business environment, institutional quality, governance, and economic freedom; such factors are country-specific rather than general.

Institutional Quality and FDI Inflow

Institutional quality plays an important role in attracting FDI inflow. Institutional reforms attract foreign investors by ensuring protection and reducing political and governmental stability risks (Mina, 2012; Mohamed & Sidiropoulos, 2010). Ali et al. (2010) and Buchanan et al. (2012) document that governance infrastructure emphatically influences FDI inflow in a positive way. A recent empirical study by Borojo and Yushi (2020) shows that the betterment in governance quality and business atmosphere in African economies significantly attracts Chinese FDI flow to African countries. Institution instability and poor business environments create instability, rendering a certain environment unpredictable, hence inhibiting FDI flow (Büthe & Milner, 2008; Globerman & Shapiro, 2003). Aziz and Mishra (2016) analyzed the main economic, endowment, and institutional determinants of FDI inflows to Arab countries. The findings confirm that governance quality indicators, political stability, investment profile, and anti-corruption are important determinants in host countries to attract FDI inflows. Political instability makes a country less attractive, and creates an unpredictable environment (Büthe & Milner, 2008; Loree & Guisinger, 1995; Woodward & Rolfe, 1993), which end up deranging economic processes (Schneider & Frey, 1985). Okada (2013) documents that the joint effects of financial deepening and institutional quality spur capital inflows. Similarly, using data for Africa during 1970 to 1990, Naudé and Krugell (2007) scrutinized the determinants of FDI inflows and showed that institutional quality (in terms of the rule of law, and government/political stability) is a key determinant of FDI. In the analysis of developing economies, Root and Ahmed (1979) and Schneider and Frey (1985) observed that FDI is notably deterred by political instability, and more recent studies affirm this. Zangina and Hassan (2020) demonstrate that corruption hinders FDI inflow, and corruption control has asymmetric effects on FDI inflow to Nigeria. Joshua, Adedoyin et al. (2020), Joshua, Rotimi et al. (2020) document that the effect of FDI is more noticeable across emerging economies compared to developed economies. Ameer et al. (2020) argue that poor institutional quality is detrimental to private capital formation for emerging economies, and extensive anecdotal evidence shows that poor institutional quality often hinders the investment process.

From a developed-country FDI investor perspective, Wheeler and Mody (1992) analyzed US firms’ data and found that corruption in host countries is detrimental to FDI decisions. As mentioned previously, economic institutional quality is a particularly potent FDI indicator (Ali et al., 2010), and the “ease of doing business” is a robust tool to increase FDI inflows to developing economies (Bayraktar, 2015; Moran et al., 2018). Consequently, this study investigates institutional quality’s role in explaining FDI inflow.

Accession to the WTO and FDI

Accession to the WTO can have many impacts on national economies. Direct impacts include lower trade barriers with other members, including import quotas and tariffs, and the harmonization of many regulations with other states. Indirect outcomes include enhanced political globalization, and one of the aims of the WTO itself is to promote democratic transition by the development of political institutions in domestic countries. Institutional quality is commonly understood in general terms pertaining to democratization, representation, and civil society, and in terms of corruption eradication, in a more specifically economic context. WTO accession is posited to improve the business atmosphere, institutional quality, and governmental transparency, reducing corruption in national economies. Allee and Scalera (2012) state that accession to WTO and other international organizations, such as the International Monetary Fund (IMF), might have wide indirect effects—such as on domestic political institutions within joiners—in several ways, like reducing corruption and increasing transparency. As for the determinants of FDI inflows to Arab states, Aziz and Mishra (2016) observe that WTO and Euro-Mediterranean Union (EMU) membership are supportive toward economic growth through international trade activities and increased FDI inflows to Arab economies. Similarly, Alfalih and Bel Hadj (2020) study determinants of FDI in Saudi Arabia in the short- and long-run with reference to its features as a preeminent global oil exporter, documenting that FDI inflows are encouraged by policy implementation for improved law and order, and several macroeconomic factors (including trade openness). Rose (2004) scrutinized the impacts of non-membership of WTO on bilateral trade flows, assessing the impact of various international trade agreements on trade flows, including the WTO and Generalized System of Preferences (GSP) in the case of developed to developing countries. The findings observe a positive impact of WTO membership on trade flows by considering the distinct effects of individual preferential trade agreements (PTAs).

Wang (2003) evaluates the impact of China’s WTO accession on patterns of world trade and economic growth, providing a relatively comprehensive assessment based on the actual market access commitments of China and Taiwan. Wang (2003) highlights that the Chinese economy gained efficiency from WTO accession, and it and many partner countries gained economic benefits, including developed nations, Asian newly industrialized economies, and less developed countries. A similar study by Büthe and Milner (2008) also assessed the impact of multilateral trade agreement on FDI inflows, arguing that international institutions influence FDI by facilitating foreign investors’ access to local markets. The study documents that international trade agreements considerably increase flows of FDI into developing countries. Prior literature argues that Russian membership in WTO provides several trade benefits to tertiary sectors by enhancing trade liberalization. WTO accession induced trade liberalization in Russia, consequently elevating macroeconomic performance through international competitive markets. WTO membership particularly spurs the services sectors more profoundly through the integration to global markets, as in banking, education, tourism, and so on (Camacho & Rodríguez, 2007; Camacho & Rodriguez, 2010; Pilat & Wölfl, 2005). Pertaining to the plausible role of WTO accession to the economy, we are motivated to measure its role in influencing FDI inflow in the context of Saudi economy.

Global Financial Crisis and FDI

Some distinct advantages of Saudi Arabia enabled the economy to enjoy higher inflow of FDI even during the period of GFC. Brach and Loewe (2010) argue that high energy prices during this period were particularly beneficial to the Arab World. Anecdotal evidence suggests that the major Arab oil and gas producing countries, including Algeria, Kuwait, Libya, Oman, Qatar, Saudi Arabia, and the UAE, experienced higher growth through augmenting the value of their foreign assets invested in international capital markets. The International Monetary Fund (IMF, 2009b) reports that GDP increased by 7.7 % and 6.5% in 2005 and 2007 respectively on an average in those countries. In addition, economies of Arab countries showed a better resilience toward to GFC due to higher remittance inflow. For instance, Arab households received about USD104 per capita as a form of remittance in 2008, compared to USD54 per capita for all developing nations (Ratha & Mohapatra, 2009). Besides, the Arab world enjoyed higher inflow of international tourists during over the year of 2002 to 2008, and tourism sector significantly contributes to macroeconomic performance in those countries. Statistics shows that tourism contributes annual per capita income of USD68, USD4, USD9, USD50, and USD96 in Arab countries, Sub-Saharan Africa, South Asia, East Asia, and Latin America (World Bank, 2009). Moreover, Arab countries also accrue a substantial amount of total global development assistance, and received considerable foreign assets of more than USD2500 per capita in 2006, compared to less than USD1500 for the rest of the developing world (Heshmati et al., 2017). Arab countries therefore fared relatively better than the global average during the GFC (IMF, 2009a).

The Middle East and North Africa (MENA) region possess some unique characteristics in terms of FDI inflows, including high oscillation and a high degree of concentration at the national and sector levels. A higher inflow of FDI over 2000 to 2008 was determined by structural and institutional improvements in the region even during the GFC. Most foreign investment is engrossed by a small number of MENA countries at the country level, especially Saudi Arabia, Turkey, and the UAE, which have received 60% of the region’s total FDI flows since 2000, followed by Egypt, Lebanon, Morocco, and Qatar (United Nations Conference on Trade and Development [UNCTAD], 2018).

Abdel-Latif (2019) highlights that MENA countries apparently gained several benefits from the flow of FDI, and their share remains stable compared to other regions. It should be noted that MENA was also vulnerable to the negative effects of the GFC on FDI flows, like other regions, but they adopted several astute recovery measures. The study further argues that the instability of the Arab Spring and contemporaneous events hurt FDI inflow in 2011. These findings are significant for policymakers who intend to assess the role of unexpected political shocks in impeding FDI flows. Prolonged political shocks reduce investor confidence, creating redundant turbulences in macroeconomic fundamentals, negatively affecting development plans and FDI flows. Therefore, policymakers should develop timely and suitable policy responses to political shocks, given their negative impacts on FDI flows.

Likewise, Ucal et al. (2010) investigated the impact of the global financial crisis on FDI inflows in the context of 148 developing countries, concluding that FDI inflow dropped by 15% in the sample countries due to the GFC in 2007 and 2008. Apparently, the impact of GFC lasted for an even a longer time horizon, as UNCTAD (2013) revealed that FDI inflow collapsed by 18% in 2012 compared to 2011. This section strongly endorses the role of GFC as an exogenous shock toward FDI flows, thus we incorporate its role to explain our empirical model.

Why Saudi Arabia?

The economy of Saudi Arabia is one of the top twenty economies in the world. Mainly dependent on oil exports, the Saudi Arabia has the second-largest proven petroleum reserves, and is one of the top exporters of petroleum in the world. According to the World Bank’s (2020) Doing Business Report, Saudi Arabia ranked 62nd out of 190 economies, up by 30 places from 2019. It launched its national development plan, Vision 2030, in 2016. This ambitious project aims to develop the Saudi economy and decrease the country’s reliance on oil. Its most important economic goals are to increase the private sector’s contribution to GDP from 40 to 65%, and raise the share of non-oil exports in non-oil GDP from 16% to 50%. The government has made attracting greater foreign investment a cornerstone of the national agenda, seeking to diversify the economy of the world’s top oil exporter away from a reliance on crude revenues. Vision 2030 provides important opportunities for foreign investors in the sectors of education, housing, energy, and health, among others. Also, the country authorized the acquisition of 100% of assets by foreign investors in retail and wholesale trading, removing traditional protectionist quotas placed on foreign investments in these sectors.

The government also tries to attract FDI in sectors like entertainment, which has great future potential. According to Jadwa Investment, Saudi Arabia spent around SAR100 billion on tourism in 2016, of which 31 billion SAR went to entertainment, indicating the growing demand for tourism and entertainment by the population that is estimated to reach 40 million people by 2030. Also, other sectors like renewable energy have seen FDI in line with the government’s economic diversification goal, and new projects outside the oil and gas sector.

As mentioned previously, FDI generally brings benefits and skills to host countries, which in the Saudi case include managerial skills, technological know-how, new jobs opportunities, capacity building, and creating a sound competitive environment to diversify non-oil exports to achieve the goals of Vision 2030. Figure 1 shows FDI net inflow as per cent of GDP and the growth of the real GDP. Historically, FDI in Saudi Arabia has increased a great deal since 2005, with accelerated interest and investment since WTO accession in that year, which substantially improved foreign investment climate in the Kingdom. According to the World Investment Report, the increased in FDI inflow into Saudi Arabia in 2008 was mainly driven by real estate, petrochemicals, refining, construction and trade. Until September 2008, FDI inflows were still supported by the continuous rise in oil prices, robust economic growth and the proliferation of mega development projects (UNCTAD, 2009). However, the slowdown of global credit markets has had a severe impact on the financing of development projects, which cut FDI inflows in 2009. According to the UNCTAD, as a result of the global financial crisis, Saudi Arabia’s share in total FDI inflows to West Asia collapsed from 53% in 2009 to 27% in 2015, and a mere 6% in 2017 (UNCTAD, 2018).

KSA GDP and FDI inflow.

Due to fluctuating FDI flows in recent years, and generally poor performance since 2011, the Kingdom passed many regulatory reforms and unprecedented legal changes with the aim of consolidating Saudi Arabia as one of the world’s ten most competitive countries and attractive markets for investing. According to a Royal Decree released in February, 2020, Saudi Arabia changed the General Authority of Investment to the Ministry of Investment, which highlighted the importance of attracting both domestic and foreign investors and expanding their investments, in order to achieve sustainable national economic growth.

Many economies emphasize promoting FDI inflow as a key driver of socio-economic development policy. In this study, we scrutinize the impact of realistic axioms of FDI inflow in Saudi Arabia. FDI inflow is regarded an imperative source of production variables (e.g., capital, technology, trade surplus, knowledge, network, and value systems), which are factors of paramount importance for the development of developing or emerging nations.

Data and Methods

Data and Sources

The paper seeks to determine key factors that can explain FDI dynamics. This study utilizes annual time series data from 1984 to 2018. The relevant data are obtained from various sources, including the Saudi Arabia Monetary Authority (SAMA), World Bank, and PRS Group. The dependent variable is Foreign Direct Investment (FDI) inflow share of GDP. We consider several variables; by applying a general to a specific model, this study considers the variables shown in Table 1. Based on several empirical studies and anecdotal evidence, the following core detriments of FDI have been taken. For stance, governance quality improves the domestic country’s investment climate (Ameer et al., 2021). Besides, Al-Mamun and Sohag (2015) argue that financial development (FD) is the channel through which the FDI flow takes place; hence the role of FD should be considered to derive FDI function. Likewise, trade openness is directly associated with FDI as trade protection or embargo impedes FDI flows. Allee and Scalera (2012) state that accession to WTO and other international organizations, such as the International Monetary Fund (IMF), might have wide indirect effects—such as domestic political institutions within joiners—in several ways, like reducing corruption and increasing transparency. Lastly, since the Saudi economy enjoyed a robust inflow of FDI during GFC, thus this study consider its role.

Definition and Sources of Variables.

Empirical Method

This study applies the Autoregressive Distributed Lag (ARDL) model to estimate our time-series data from 1984 to 2018. Before we employed this estimation, we conducted a unit root test (specifically, Dickey–Fuller-Generalized Least Squared (DF-GLS) test), to determine the order of integration of the respective variables. Although the ARDL approach is robust under the mixed order of integration, we apply the unit root test to validate its application.

Mahran and Al Meshall (2014) argue that the ARDL model is an efficient and consistent framework to deal with small samples. This approach is usually appropriate for studying macroeconomic variables. The ARDL framework is given in equation 1:

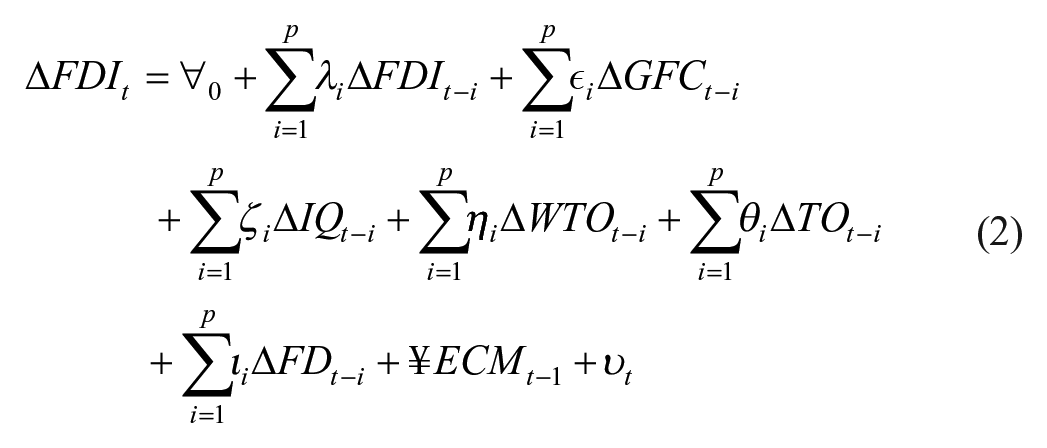

Where ∀0 is constant and υt is residuals. Variables with summation signs indicate autoregressive terms. In equation (2), the vector of μ indicates the long-term coefficients. First, we estimate equation (1) under ordinary least squares (OLS) framework. We performed Wald joint significance test on lagged variables to determine the cointegration. The null hypotheses for equation (1) is H0: μ1 = μ2. . . = μ8= 0, assuming no co-integration relations among the variables. Contrarily, the alternative hypotheses H1: μ1 ≠ μ2. . . ≠ μ8≠ 0 indicates the co-integrating relations among DV and list of IVs.

After conducting Wald test, we evaluate the calculated F-statistic with critical values provided by Pesaran et al. (2001), who indicate that if the calculated F-statistic surpasses the upper bound of the critical value, we accept the alternative hypothesis, and conclude that there is co-integration (a long-term relationship) among the variables. Conversely, if the calculated F-statistic is below the lower bound of the critical values variables, we accept the null hypothesis, and conclude that there is no co-integration (no long-term relationship) among the variables. If the calculated F-statistic lies between the lower and upper bounds of the critical values, this indicates an inconclusive result. Once a long-term relationship is identified, we estimate long-run coefficients and eventually short-term coefficients along with error correction coefficient, as shown in equation (2).

There are several post-diagnostic tests to valid the estimators. Pesaran et al. (2001) suggest applying “cumulative sum of recursive residuals (CUSUM)” and a “cumulative sum of squares of recursive residual (CUSUMSQ)” on the residual to check the stability. CUSUM and CUSUMSQ diagrams help identify stability when estimated values lie between the lower and upper critical bounds at the 5% significance level. Post-estimation diagnostic tests also confirm whether estimators are robust in terms of heteroscedasticity, serial correlation, model specification, and normality issues.

Results

Descriptive Statistics

Table 2 presents basic summary statistics for all variables in the model. It is important to note that some of the included variables are dummy variables. A number of the reported statistics may not provide significant information about the dummy variable at hand. WTO or GFC has been included in Table 2 to provide addition information on quantitative variables.

Summary Statistics.

The descriptive statistics in Table 2 appear to be reasonable individual-level statistics for the variables. Average FDI inflow in Saudi Arabia was 1.5% of GDP over the last 35 years, financially developed by 0.4 units. Its exposure to international trade was 72.7% of its GDP, and its quality of institutions scored 2.1 out of 10 over the last 35 years.

The standard deviation of FDI is fairly large at 2.5% of GDP, considering that the maximum FDI inflow is 8.5. This indicates there is substantial variation in FDI observations around the mean. The standard deviation of FD is smaller at 0.1, indicating the variation in the financial development index is less than in FDI inflow. At 10.3, TO has a significantly small standard deviation, given its maximum value of 96.1. IQ is fairly small at 0.2 units.

FD, TO, and ICRG variables are normally distributed according to the reported Jarque-Bera normality statistics, while FDI follows a particularly non-normal distribution. This variable has reported skew and kurtosis of 1.3 and 4, respectively, which are not normally distributed values of 0 and 3. Possible corrective actions may be taken for FDI which are not normally distributed, including transforming the variable into logarithmic form, or accounting for significant outliers within the series.

Table 3 presents the correlation matrix, including the level of significance (p-value). It reveals a strong and significant positive correlation between FDI–GFC. Likewise, the correlation between FDI and IQ appears to be positive and significant. Importantly, positive and significant correlations can be seen between FDI–WTO membership, FDI–TO, and FDI–FD. Variance inflation factor (VIF) scores confirm that our model does not encounter with any several multi-collinearity problem.

Correlation Matrix and VIF.

As predicted in the theoretical section of the paper, FDI is expected to be positively correlated with all variables determining FDI, and the correlations shown in Table 4 support this. Of these variables, FDI has the highest correlation with GFC (correlation coefficient: .6) and the lowest correlation with the FD (correlation coefficient: .2). WTO and FD might present multicollinearity problems if they are both included as explanatory variables (correlation coefficient: .8). This issue can be corrected by introducing an interaction term between FDI and FD; however, the model may lose some explanatory power if this interaction term is accounted for in this manner. We also apply Dickey–Fuller generalized least squared (DF-GLS) approach to identify the order of integration of our series, due to its consistency in the presence of heterogeneity and outlier observations (Begum et al., 2015; Elliott et al., 1992). Table 4 indicates that all variables are non-stationary but become stationary after taking first difference.

Unit-root Result by DF-GLS.

Note. *** and ** indicate 5%, and 10% significance level.

Main Results

The model follows a general to specific approach. The specific model focuses on four important variables: trade openness (TO), financial development (FD), institutional quality (IQ), and WTO membership. The coefficient of error correction is negative and significant, which confirms the long-run equilibrium of our model (Table 5). Precisely, the mode adjusts 75% per year toward the long-run equilibrium. The post diagnostic tests confirm that estimated parameters are robust, as no issues were found regrading heteroscedasticity, normality, serial correlation, and model specification. The coefficient of TO is found to be positive and significant, implying that TO fosters FDI inflow in the long run. Nevertheless, the coefficient of FD appears to be positive but insignificant in explaining FDI inflow in the long run. The striking finding is that IQ promotes FDI inflow in the long run, which echoes many prior studies (Aziz, 2018; Uddin et al., 2019).

FDI Inflow—Role of WTO Membership.

Note. Bound Test F-Stat = 5.566a; ARDL(1,1,0,0,1)

indicates 1% significance level.

Our findings echo the fact that institutional quality plays an important role in attracting FDI inflow. Our result supports the contentions of Mohamed and Sidiropoulos (2010) and Mina (2012), who argue that the institutional reforms attract foreign investors by providing protection and reducing uncertainty of government stability. Our finding is line with Borojo and Yushi (2020), who found that the governance infrastructure positively influences FDI inflow. Our results coincide with the proposition of Aziz and Mishra (2016), who document that greater quality of economic and institution increased FDI inflows to Arab countries. Our empirical results confirm that institutional quality indicators (e.g., government stability, investment profile, and anti-corruption) are important factors in host countries in facilitating FDI inflows. Political and governmental instability make a country less attractive because it creates an unreliable business environment (Büthe & Milner, 2008; Loree & Guisinger, 1995; Woodward & Rolfe, 1993), which could deactivate economic processes and thus deter investment (Schneider & Frey, 1985).

The coefficient of WTO is positive and significant, indicating that WTO accession benefits the economy by promoting FDI inflow, as supported by Figure 2. This confirms our argument that WTO accession can have manifold impacts. First, the direct impact facilitates international corporate investment in all WTO member countries, due to lower trade barriers, including tariffs, import quotas, and regulations. Indirect impacts include political institutional development in host countries. This affirms Allee and Scalera’s (2012) argument that WTO accession reduces corruption and increases transparency. Our empirical findings also demonstrate that both IQ and WTO membership spur FDI inflow in the short run. Our model is stable, as all diagnostic tests accept our simulation. Figures 3 and 4 show that our model is stable.

FDI inflow and its determinants.

Plot of cumulative sum of recursive residuals for FDI inflow—role of WTO membership.

Plot of cumulative sum of squares of recursive residuals for FDI inflow—role of WTO membership.

At this stage, we estimate our model incorporating the role of the GFC dummy. Our second model appears to be consistent with the baseline one, but its convergence speed is higher. The coefficient of ECM is −.83, implying that the model reached long-run equilibrium with a rate of 83% per year (Table 6). Figures 5 and 6 show that our model is stable. Interestingly, the coefficient of GFC is positive and significant, indicating that the GFC promoted FDI inflow. This finding affirms anecdotal evidence suggesting that the Saudi economy experienced a high inflow of FDI during the crisis period. A few characteristics of the MENA oil-producing economies (Algeria, Kuwait, Libya, Oman, Qatar, Saudi Arabia, and UAE) allowed them to achieve many benefits during the period 2002–2008, while many other regions suffered, mainly due to high oil prices and increasing value of foreign assets invested in international capital markets, as discussed previously, with GDP increasing by 7.7 and 6.5 per cent in 2005 and 2007, respectively (Brach & Loewe, 2010; IMF, 2009b).

FDI Inflow During GFC.

Note. Bound Test F-Stat = 8.2154a; ARDL(1,1,0,0,1)

indicates 1% significance level.

Plot of cumulative sum of recursive residuals for FDI inflow—during GFC.

Plot of cumulative sum of squares of recursive residuals for FDI inflow—during GFC.

Conclusions and Policy Implications

Given the importance of FDI inflow in promoting macroeconomic performance, this study explores key determinants to explain such inflow into the Saudi economy. The general-to-specific approach helps to develop a realistic model comprising economic and political factors. To this end, we analyse time series data by applying ARDL approach under structural break framework to derive several interesting findings. First, we recognized that trade openness is the driving factor spurring FDI inflow. In addition, local institutional quality and WTO accession are important variables fostering FDI inflow into the Saudi economy in both the short and long run. Interestingly, the economy experienced a higher inflow of FDI during the GFC, implying that the Saudi economy is relatively stable and robust against global economic shocks.

Our empirical findings provide several policy implications. A positive role of trade openness indicates that the country can promote FDI inflow by lowering trade barriers in the form of different customs duties and taxes. Moreover, institutional quality appears to be positive and significant, implying that the overall institutional quality has to be improved, including market competitiveness, business freedom, political globalization, bureaucratic quality, investment profile, and so on. FDI is believed to be an important driver for enhancing competitiveness, innovation, labor productivity, and economic diversification, eventually promoting economic growth; hence, governments should undertake various measures to attract FDI inflow, by ensuring a favorable business environment, including by facilitating a comprehensive legislative structure and improving bureaucratic quality. In addition, the country should extend more bilateral and multilateral agreements with various potential states in terms of trade and financial integrations.

Our study considers the composite factor of institutional quality instead of decomposed components of it, which requires a thorough study focusing on each component of IQ for enhancing the understanding regarding FD-institution nexus. Future studies can explore the role of decomposed components of IQ in explaining FDI inflow in the Saudi economy.

Footnotes

Author Note

Nahla Samargandi is now affiliated to K.A.CARE Energy Research and Innovation Center, King Abdulaziz University, Jeddah, Saudi Arabia.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors acknowledge the support provided by King Abdullah City for Atomic and Renewable Energy (K.A.CARE), under K.A.CARE-King Abdulaziz University Collaboration Program.