Abstract

To assess the impact of sustainability assessment tools on the sustainability of the business and measure the impact of these tools and the business’s sustainability on the business’s reputation and brand. Scoring the sustainability level according to each criterion of each sustainability assessment tool, run AMOS software to measure the impact of each assessment tool on the sustainability and reputation of the business. This article aims to present and discuss the art of sustainability assessment using integrated assessment tools, including life cycle assessment, data-based assessment of sustainability reports, impact assessment with stakeholders and from stakeholders to make recommendations for further development, consistent with ontology, epistemology, and methodology of aspects of sustainability science. By using integrated tools to assess a business’s sustainability, it is possible to ensure that its activities match the needs and expectations of its stakeholders. This can help build trust and goodwill with the community and contribute to the long-term and sustainable success of the business.

Plain language summary

The article examines how different sustainability assessment tools influence a business’s overall sustainability and evaluates the effect of these tools, along with the business’s sustainability practices, on its reputation and brand image.

The study involves scoring the sustainability level based on specific criteria associated with each assessment tool and utilizing AMOS software to analyze the impact of each tool on the business’s sustainability and reputation.

The article seeks to explore and discuss the practice of sustainability assessment by employing a range of integrated tools, such as life cycle assessment, data-driven analysis of sustainability reports, and impact assessments involving stakeholders. These discussions aim to provide recommendations for future developments in line with the ontological, epistemological, and methodological dimensions of sustainability science. Using a combination of tools to assess a business’s sustainability ensures alignment with stakeholder needs and expectations, thereby fostering trust, building positive community relationships, and supporting the business’s long-term sustainable success. First, it demonstrates that Life Cycle Costing (LCC) has the highest impact on sustainability evaluation, surpassing traditional tools like Life Cycle Assessment (LCA) and Sustainability Reporting. This challenges previous assumptions that environmental metrics alone are sufficient for assessing corporate sustainability. Second, the study reveals that corporate sustainability serves as the strongest intermediary factor influencing business reputation, emphasizing the need for businesses to align sustainability practices with financial and operational strategies.

Keywords

Introduction

Much has been written about why companies engage in sustainability practices. Several studies have addressed the question, “How can companies and do integrate sustainability assessment, management accounting, management control, and reporting?” assessing sustainability based on information on sustainability reports. However, corporate sustainability requires integrated measurement and management of sustainability issues rather than separate applications of different organizational tools. This article researches and considers the assessment of corporate sustainability integrated based on the device’s Sustainability Reporting Standards, Life-Cycle Costing (LCC), Life Cycle Assessment (LCA), Social Impact Assessment, and Sustainable Supply Chain Management. At the same time, study the impact of sustainability assessment on the business’s brand. Key findings show that concepts of Sustainability Reporting Standards, Environmental Management Systems (EMS), Life Cycle Assessment (LCA), Social Impact Assessment, and Sustainable Supply Chain Management are defined and used in different ways but mainly handled separately. Based on these findings, this paper proposes a comprehensive, integrated framework for assessing sustainability based on information on sustainability reports and business activities impact on the environment and society. Previous studies only assessed the effect of the subject, and this study integrates the integrated result of the subject enterprise and its environmental and social stakeholders. From a scientific perspective, the proposed framework is the first attempt to integrate these isolated concepts. It can help researchers and practitioners better understand the relationship between the five concepts and how they can be linked to developing an integrated sustainability assessment.

There are several business sustainability assessment tools available that companies can use to evaluate their sustainability performance. Some commonly used tools are Sustainability Reporting Standards, Environmental Management Systems (EMS), Life Cycle Assessment (LCA), Carbon Footprinting, Social Impact Assessment, Sustainable Supply Chain Management…With the tool of Sustainability Reporting Standards, the Global Reporting Initiative (GRI) provides widely recognized sustainability reporting standards that companies can use to measure and report on their sustainability performance. An environmental Management System (EMS) is a framework that helps companies manage and reduce their environmental impact. ISO 14001 is a widely recognized EMS standard. A Life Cycle Assessment (LCA) is a method used to evaluate the environmental impact of a product or service throughout its entire life cycle (Finkbeiner & Hoffmann, 2006).

Using tools such as Sustainability Reporting Standards, Life-Cycle Costing (LCC), Life Cycle Assessment (LCA), Social Impact Assessment, and Sustainable Supply Chain Management is essential for evaluating business sustainability, particularly in Vietnam. Sustainability Reporting Standards (such as GRI and SASB) provide a structured framework for Vietnamese enterprises to communicate their Environmental, Social, and Governance (ESG) performance transparently. This is vital for building trust with international investors and partners who increasingly demand robust ESG disclosures, enabling Vietnamese businesses to compete globally. Tools like LCC and LCA help Vietnamese businesses identify and quantify the environmental and economic impacts of their operations throughout a product’s life cycle. This is particularly important in Vietnam, where rapid industrialization has led to increased resource consumption and environmental degradation. By optimizing resource use and minimizing waste, businesses can achieve cost savings while enhancing environmental sustainability. There have been several studies examining the relationship between sustainability performance and firm value, showing that companies with strong sustainability activities tend to outperform their industry peers financially over the long term (Gao et al., 2024). There is a comprehensive review of the academic literature on corporate sustainability, identifying key trends, challenges, and opportunities for future research on corporate sustainability activities (Rodrigues & Franco, 2019). There is a study of different approaches to assessing corporate sustainability performance, discussing the effectiveness of different metrics and reporting standards in capturing comprehensive sustainability outcomes (Nicolăescu et al., 2015). However, there have been no studies that assess corporate sustainability through tools such as Sustainability Reporting Standards, Life-Cycle Costing (LCC), Life Cycle Assessment (LCA), Social Impact Assessment, and Sustainable Supply Chain Management and simultaneously study their impact on the business’s brand. This article studies the assessment of business sustainability based on tools such as Life-Cycle Assessment (LCA), Life-Cycle Costing (LCC), and Societal Life-Cycle Assessment (SLCA).

Using aggregate tools to assess corporate sustainability makes theoretical contributions to the field by recognizing the multi-dimensionality and complexity of sustainability, promoting systems thinking and integration, enabling benchmarking and transparency, and contributing to developing sustainability standards and practices (Visentin et al., 2020).

This article is divided into four parts:

- An overview of the sustainability assessment tools used

- Theoretical framework of business sustainability assessment tools

- Impact assessment tools and business sustainability assessment

- Methodology of research and results of research

- Discussions and conclusions

Literature Review

A life cycle assessment (LCA) is the detailed analysis of a product’s complete life cycle concerning sustainability. Each part of a product’s life cycle is cataloged from the extraction of raw materials to production, its inputs, transport, use, and what happens to a product after use.

Environmental Life Cycle Assessment (LCA) has multiplied in the past three decades. Today, LCA is widely applied and used as a support tool for performance-based policies and regulations, especially concerning bioenergy. Via Decades ago, LCA expanded to include life cycle costs (LCCs) and society LCA (SLCA), based on a three-pillar or “three bottom line” sustainability model. With these developments, LCA has expanded from a mere environment to a more comprehensive life cycle sustainability assessment (LCSA; Larsen et al., 2022).

LCSA has received increasing attention over the years, and at the same time, its meaning and content are not always clear enough. Padilla-Rivera et al. (2023) has distinguished the exact three dimensions that the LCSA is expanding when compared to the environmental LCA: (1) expanding impact, LCSA = LCA + LCC + SLCA; (2) expand the level of analysis, product-questions, and analysis about the industry and the economy as a whole; and (3) deepening, including beyond technological relationships, such as physical, economic, and behavioral relationship. From this analysis, it is clear that much of the LCSA study has so far focused on the “expansion of impacts” aspect. The most challenging is frequently cited concerning the need for more real-life examples of LCSA, practical how to communicate LCSA results, and additional data and methods, especially for SLCA indicators and comprehensive uncertainty assessment. He concluded that the three most important challenges that need to be addressed are a development first, Quantitative and valuable indicators for SLCA, lifecycle-based approaches to assessing scenarios for a sustainable future, and practical ways to deal with uncertainties and recovery effects (Padilla-Rivera et al., 2023).

Bini and Bellucci (2020) introduces the goals and interests driving companies to report on their sustainability practices and provides an overview of the development history development of sustainability reporting in recent decades. Following the presentation of the challenges in sustainability reporting comes a critical review of approaches to overcoming these problems. The authors propose a dual approach combining an inside-out strategic approach to measuring and managing performance with an outside-in approach to applying external requirements and concluding with consequences for sustainable communications (Bini & Bellucci, 2020).

Alaloul et al. (2021) suggested that life cycle cost (LCC) is related to the system engineering process because economic considerations are essential in the system creation process. LCC involves assessing all future costs associated with the life of a system. The main goal of this author is to discuss the usefulness of LCC as a method to enhance sustainability for business owners and improve their decision-making base (Alaloul et al., 2021). Guinée argues that there are many approaches to studying production and consumption’s environmental and sustainability aspects. Some of these are at the conceptual level, for example, industrial ecology, ecological design, and cleaner manufacturing. Other approaches are based on quantitative models, for example, life cycle assessments, material flow calculations, and strategic environmental assessments. These authors focus on developing a framework that can combine different models for ecological analysis, with the option of broader scope including economic and social aspects, thus including The three pillars of sustainability (Guinée et al., 2022). Through the lens of Industry 4.0 and technology concepts the article aims to contribute knowledge on assessing the impact of additive manufacturing technology on sustainable business models (I. Costa et al., 2022). Their ideas are implemented through a proposed framework, as well as models and scales that can be used to identify these impacts. Impacts are assessed by considering the social, environmental, and economic effects of additive manufacturing on business models, and for all three, a balanced scorecard structure is established. Schilling summarizes the research on quantitative models for transitional supply chains, thereby contributing to further proof of environmental and social impact assessment. He argues that while different types of models apply, it is clear that the social aspect of sustainability is not considered. Regarding the environment, approaches based on life cycle assessment and impact criteria dominate. In terms of modeling, there are three main approaches: balanced modeling, multi-criteria decision-making, and hierarchical analytical procedures (Schilling & Seuring, 2023). By considering the total cost of a product, a business can identify opportunities to reduce waste, improve efficiency, and minimize negative environmental impacts. This can enhance the business’s reputation as a responsible and sustainable organization. Sustainable supply chain management ensures suppliers and partners adhere to sustainability standards and practices. By implementing sustainable supply chain management practices, a business can reduce environmental and social risks, improve supply chain efficiency, and enhance its reputation as a responsible and sustainable organization (İncekara, 2022).

Theoretical Framework and Hypotheses

Theoretical Framework

Two of the most fundamental theories underpinning business sustainability assessment tools are the Triple Bottom Line (TBL) and Stakeholder Theory. Both frameworks are critical in shaping how organizations evaluate and measure sustainability performance, providing a comprehensive view that extends beyond traditional financial metrics to include social and environmental dimensions.

Triple Bottom Line (TBL) Theory

The Triple Bottom Line theory, introduced by John Elkington in the mid-1990s, posits that businesses should commit to measuring their performance not just in terms of economic value, but also in social and environmental value. The TBL framework is often summarized as the “three Ps”: People, Planet, and Profit. People refers to the social aspect, which includes fair labor practices, community engagement, employee well-being, and human rights. Planet addresses the environmental aspect, encompassing resource usage, waste management, carbon footprint, and overall impact on natural ecosystems. Profit represents the traditional economic dimension, which focuses on financial performance, profitability, and market growth. TBL theory significantly impacts business sustainability assessment tools by expanding the scope of performance evaluation. Traditional business metrics primarily focused on financial success, but TBL requires organizations to integrate social and environmental indicators into their assessment frameworks. This shift necessitates the development of tools that can quantitatively and qualitatively measure performance across all three dimensions. Sustainability reporting frameworks such as the Global Reporting Initiative (GRI) and the Integrated Reporting Framework (IR) are directly influenced by TBL theory. These frameworks guide organizations to report on a broad range of sustainability indicators, from carbon emissions and energy consumption to employee turnover rates and community impact initiatives. The influence of TBL has led to the creation of multi-dimensional assessment tools, like the Dow Jones Sustainability Index (DJSI) and the Corporate Sustainability Assessment (CSA), which evaluate companies based on their environmental, social, and governance (ESG) practices. Moreover, TBL theory encourages organizations to adopt a long-term perspective on value creation, understanding that sustainable practices often yield benefits that are not immediately apparent in short-term financial metrics but are critical for long-term resilience and success. This holistic view drives businesses to innovate in areas such as sustainable product development, supply chain management, and corporate social responsibility (CSR) initiatives (Żak, 2015).

Stakeholder Theory

Stakeholder Theory, proposed by R. Edward Freeman in the 1980s, emphasizes the importance of all stakeholders in a company’s operations, not just its shareholders. Stakeholders include employees, customers, suppliers, communities, governments, and even the environment. The theory posits that businesses should create value for all stakeholders, as opposed to solely focusing on maximizing shareholder returns. Stakeholder Theory has a profound impact on business sustainability assessment tools by expanding the criteria for measuring performance. The theory suggests that the success of a business should be evaluated based on its ability to meet the needs and expectations of a diverse range of stakeholders. This multi-stakeholder focus has led to the development of tools that integrate stakeholder engagement metrics into sustainability performance assessments. For example, the Sustainability Accounting Standards Board (SASB) and the Task Force on Climate-related Financial Disclosures (TCFD) are influenced by Stakeholder Theory. These standards require companies to disclose information on how they manage risks and opportunities related to sustainability issues, particularly those that affect stakeholders. They emphasize transparent communication about sustainability practices and performance, ensuring that companies account for the interests and concerns of all their stakeholders. Furthermore, tools like the B Impact Assessment, used by B Corporations, reflect the principles of Stakeholder Theory. The B Impact Assessment evaluates a company’s social and environmental performance across a range of impact areas, such as governance, workers, community, environment, and customers. This tool helps organizations understand their impact on various stakeholders and develop strategies to enhance their sustainability performance (Mahajan et al., 2023).

Impact Assessment Tools and Business Sustainability Assessment

Life-Cycle Assessment (LCA)

Life Cycle Assessment (LCA) is a method used to evaluate the environmental impact of a product or service throughout its entire life cycle, including raw material extraction, production, transportation, use, and disposal. On the other hand, corporate sustainability assessment is a broader evaluation of a company’s sustainability performance, which includes social, economic, and environmental dimensions. Using the Life-Cycle Assessment (LCA) to assess corporate sustainability involves evaluating the environmental impacts associated with the entire life cycle of a product, service, or process, from raw material extraction to end-of-life disposal. The LCA is a standardized methodology that can quantify business activity’s environmental impacts by considering the movement’s resource inputs, energy consumption, emissions, and waste generation. Using the LCA to assess corporate sustainability is identifying the environmental hotspots, or areas of significant environmental impact, associated with the business activity. This information can be used to prioritize areas for improvement and develop sustainability strategies that reduce the environmental footprint of the business activity. By considering the entire life cycle of the activity, the LCA provides a comprehensive assessment of the environmental impacts associated with the activity and enables companies to identify opportunities for improvement throughout the supply chain. Using the LCA to assess corporate sustainability is becoming increasingly crucial as stakeholders, including customers, investors, and regulators, demand more transparency and accountability in business practices. Companies that use the LCA to assess their sustainability performance can demonstrate their commitment to sustainability and respond to stakeholder demands for more sustainable business practices (Ferrari et al., 2021).

H1: The quality of the use of LCA has a positive and direct impact on the assessment of business sustainability

H2: Using LCA to assess a business’s sustainability has a direct and positive impact on a business’ brand

Life-Cycle Costing (LCC)

Life-Cycle Costing (LCC) is a financial analysis technique that considers the total cost of ownership of a product or service throughout its entire life cycle. LCC considers the initial purchase price and the costs associated with production, maintenance, disposal, and end-of-life management. By considering a product or service’s entire life cycle costs, LCC can provide a more accurate assessment of corporate financial sustainability (Fathollahi & Coupe, 2021). LCC helps to identify areas where a business can reduce costs, increase efficiency, and improve its environmental and social impact. LCC also encourages firms to consider the long-term effects of their decisions on the environment and society. By factoring in the costs of waste disposal, emissions, and other environmental and social impacts, LCC can help businesses make more informed decisions that support sustainability. In summary, Life-Cycle Costing can significantly impact the assessment of business sustainability by providing a comprehensive financial analysis that considers the long-term costs and benefits of a product or service over its entire life cycle. This can help businesses make more informed decisions that support sustainability, reduce costs, and improve their environmental and social impact. Using Life-Cycle Costing (LCC) to assess sustainability can positively impact a business’s brand and reputation, especially if the results demonstrate a commitment to sustainability (Kambanou, 2020).

H3: The quality of the use of LCC has a positive and direct impact on the assessment of business sustainability

H4: Using LCC to assess sustainability can have a positive effect on the brand and reputation of a business

Sustainability Reporting Standards

Using Sustainability Reporting Standards to assess sustainability can have a positive impact on corporate sustainability in several ways (Gold & Md. Taib, 2020):

Firstly, measuring and reporting sustainability performance using a set of established standards can help a business identify areas where it can improve its sustainability practices. This can lead to implementing more sustainable procedures, such as reducing greenhouse gas emissions or improving water efficiency, which can reduce the environmental impact of the business and improve its long-term sustainability. Secondly, using Sustainability Reporting Standards to assess sustainability can help a business to demonstrate its commitment to sustainability to stakeholders such as customers, investors, and employees. This can enhance the business’s reputation, attract new customers and investors interested in sustainability, and help retain employees committed to working for a socially responsible organization. Thirdly, using Sustainability Reporting Standards can help a business comply with regulations and industry standards related to sustainability. This can reduce the risk of non-compliance penalties and reputational damage arising from non-compliance. Overall, using Sustainability Reporting Standards to assess sustainability can help a business improve its sustainability practices, enhance its reputation, and reduce compliance risks, all of which can contribute to the company’s long-term sustainability. Furthermore, sustainability reporting can help businesses to differentiate themselves from their competitors by demonstrating their sustainability performance and practices. This can be particularly important in industries where sustainability is increasingly important to customers and investors. Using Sustainability Reporting Standards to assess sustainability can positively impact a business’s reputation and brand by enhancing its credibility, transparency, and differentiation and demonstrating its commitment to sustainability.

H5: Using Sustainability Reporting Standards to assess sustainability can help a business to improve its sustainability

H6: Using Sustainability Reporting Standards to assess sustainability can have a positive impact on a business’s reputation and brand

Social Impact Assessment (SIA)

Using a Social Impact Assessment (SIA) can affect corporate sustainability. The SIA is a tool used to assess a project or business initiative’s potential social and environmental impacts and identify strategies to manage those impacts. By conducting an SIA, a business can better understand how its activities may affect the local community and environment and take steps to mitigate and enhance negative impacts. Here are some ways in which using an SIA to assess sustainability can affect the brand and reputation of a business: Conducting an SIA can increase transparency around a business’s activities, including the potential social and environmental impacts. This can help build trust with stakeholders, such as customers, investors, and regulators, enhancing the business’s reputation. Conducting an SIA can establish a business’s commitment to corporate social responsibility (CSR) by assessing the potential impacts of its activities on society and the environment and identifying strategies to manage those impacts. This can enhance the business’s reputation as a responsible corporate citizen. By conducting an SIA and communicating the findings to stakeholders, a business can differentiate itself from competitors that may not be as transparent or committed to sustainability. This can help to enhance the business’s reputation as a leader in sustainability. An SIA can help a business to identify and manage potential adverse effects of its activities on stakeholders, such as employees, customers, and the local community. The company can create positive social and environmental outcomes, enhancing its reputation and brand image. However, a business needs to conduct an SIA and act on its findings and recommendations to truly enhance its brand and reputation as a sustainable business. If a company is seen as running an SIA without taking meaningful action, it could harm its brand and standing instead of enhancing it (Martinez & Komendantova, 2020).

H7: SIA can positively impact the corporate sustainability

H8: SIA enhances the business’ brand and reputation.

Sustainable Supply Chain Management (SSCM)

Using Sustainable Supply Chain Management (SSCM) to assess how sustainability affects corporate sustainability can be a valuable tool for identifying and managing the social and environmental impacts of a business’s supply chain activities. By adopting SSCM practices, a company can assess the sustainability of its supply chain and identify strategies to enhance its sustainability performance, which can positively impact the business’s sustainability as a whole. Here are some ways in which using SSCM to assess how sustainability affects corporate sustainability can be beneficial: Adopting SSCM practices can help a business identify potential social and environmental risks within its supply chain that could negatively impact the company’s sustainability. By doing so, the business can take proactive measures to manage these risks, such as developing supplier codes of conduct or implementing sustainable sourcing policies. By adopting SSCM practices, a business can improve the strength of its supply chain by identifying and addressing potential vulnerabilities, such as dependence on single suppliers or locations. This can help to mitigate the risk of supply chain disruptions due to social or environmental factors, which can negatively impact the sustainability of the business. Adopting SSCM practices can improve the importance of a business as a responsible corporate citizen by demonstrating its commitment to sustainability throughout its supply chain. This can help to attract socially and environmentally conscious customers, employees, and investors, which can positively impact the sustainability of the business. Adopting SSCM practices can help a business to identify opportunities for improving efficiency within its supply chain, such as reducing waste or improving energy efficiency. This can lead to cost savings and enhance the overall sustainability of the business. Overall, adopting SSCM practices to assess sustainability can be a powerful tool for enhancing the brand and reputation of a business. However, a company needs to adopt SSCM practices and act on its findings and recommendations to truly improve its brand and reputation as a sustainable business. If a business is seen as adopting SSCM practices without taking meaningful action, it could harm its brand and standing instead of enhancing it (D’Eusanio et al., 2019).

H9: SSCM to assess how sustainability positively affects the corporate sustainability

H10: SSCM practices to assess sustainability can be a powerful tool for enhancing the brand and reputation of a business.

Corporate Sustainability

Corporate sustainability can have a significant impact on its brand and reputation. Consumers, employees, investors, and other stakeholders increasingly expect businesses to demonstrate their commitment to sustainability in today’s socially and environmentally conscious marketplace. Here are some ways in which corporate sustainability can affect its brand and reputation (Alam & Islam, 2021):

Adopting sustainable practices throughout a business’s operations and supply chain can improve its brand value by demonstrating its commitment to social and environmental responsibility. Consumers are becoming increasingly aware of sustainability issues and are more likely to support brands prioritizing sustainability. A sustainable business can build a positive reputation as a responsible corporate citizen that cares about the social and environmental impacts of its operations and supply chain activities. This can help to attract socially and environmentally conscious customers, employees, and investors and enhance the business’s reputation. A sustainable business can engage and inspire its stakeholders, including customers, employees, and investors, looking for businesses that share their values. This can help to build a loyal customer base, attract top talent, and secure investment. A business that prioritizes sustainability can minimize risk by identifying and managing potential social and environmental risks within its operations and supply chain. This can enhance the resilience of the business and protect it from reputational damage. Many governments are introducing rules to reduce the environmental impact on businesses. A sustainable business that complies with these regulations can build a positive reputation as a responsible corporate citizen while avoiding the risks and penalties associated with non-compliance.

Overall, corporate sustainability can profoundly impact its brand and reputation. By adopting sustainable practices throughout its operations and supply chain, a business can enhance its brand value, importance, stakeholder engagement, resilience, and compliance with regulations, while mitigating risk and protecting itself from reputational damage.

H11: Corporate sustainability can have a profound impact on its brand and reputation

Methodology of Research

Sample

The paper uses a combination of qualitative and quantitative methods to study business sustainability assessment tools and analyze their impact on corporate sustainability and reputation. Using AMOS and SPSS statistical software, this research identified and measured the impact of sustainability assessment tools on the sustainability performance of each company. The paper uses structural equation modeling (SEM) to analyze the data. Based on the empirical rules of Gupta and Gupta (2020) and Ajibike et al. (2021) for estimation, the minimum sample size required for this study is n > 8 × number of variables = 8 × 18 = 144. Hence, we selected the sample size as n = 192.

The 192 enterprises in the research sample are listed on the Vietnam Stock Exchange (according to the website cophieu68.vn). The enterprises in the research sample are manufacturing enterprises with the following characteristics: the production process goes through many processing stages, has a supply chain, and the production process has a significant impact on the environment. These characteristics are consistent with the sustainability assessment tools used in the article (Table 1).

Structure of Surveyed Enterprises.

Source. Author’s classification.

Research Model

Model of research.

Several studies use methods to assess sustainability in different ways (e.g., Bjørn et al., 2020; Lindfors, 2021) or data taken from financial statements (D. Costa et al., 2019). We use a scale based on Likert scale from 1 to 5 scored from sustainability reports or annual reports, combining the views of Visentin et al. (2020). This scale has the advantage of allowing an aggregate assessment of the information published in the reports of companies—and the evaluation criteria of each method.

The dependent variable Corporate sustainability is affected by five independent variables: Sustainability Reporting Standards, Life-Cycle Costing (LCC), Life Cycle Assessment (LCA), Social Impact Assessment, and Sustainable Supply Chain Management. At the same time, the independent variable corporate reputation is affected by six variables: Sustainability Reporting Standards, Life-Cycle Costing (LCC), Life Cycle Assessment (LCA), Social Impact Assessment, Sustainable Supply Chain Management, and Corporate Sustainability.

Using these dependent variables has been studied by some authors such as Flannelly et al. (2020), Candel and Daugbjerg (2020), and Mattes and Roheger (2020).

We study two aspects: (1) measuring the influence of independent variables (Sustainability Reporting Standards, Life-Cycle Costing [LCC], Life Cycle Assessment [LCA], Social Impact Assessment, and Sustainable Supply Chain Management) on corporate sustainability; (2) Measure the influence of independent variables (Sustainability Reporting Standards, Life-Cycle Costing [LCC], Life Cycle Assessment [LCA], Social Impact Assessment, and Sustainable Supply Chain Management) and intermediate variables (corporate sustainability) to the second dependent variable corporate reputation.

Research data is taken from survey questionnaires with a Likert scale of 5 for 192 manufacturing enterprises in six industry groups listed on the Vietnam Stock Exchange (HOSE).

Collect Data

Survey Tools and Measures

We used a survey instrument to collect data to test the hypotheses. The content of the survey forms includes (1) Introducing the research objectives and introductory and screening questions; (2) a Questionnaire measuring the impact of sustainability assessment tools on the level of sustainability and brand of the business; (3) The last part is a thank you note.

The measurement of variables was adapted from previous corporate sustainability studies. We select scales with high reliability and then evaluate the appropriateness of the selected scales. We used the Vietnamese Questionnaire for the survey, which was then translated into English when synthesizing the results. We conducted nine in-depth interviews with experts and 23 interviews with businesses. After these interviews, we revised some of the content in the Questionnaire to better suit reality. The content of the Questionnaire is evaluated on a 5-point Likert scale, from 1 being “Strongly disagree” to 5 beings “Strongly agree.”

Collect Data and Samples

Data were collected from March to June 2023 using survey methods. We went directly to businesses (35 businesses), and for the remaining businesses we sent survey forms via email. We only take one survey form for each enterprise. The person surveyed can be a member of the Board of Directors or a functional department head such as the Accounting Department or the Operations Department. Respondents who agree to participate in the survey are provided with the means and support to conduct the survey objectively and accurately. All volunteered respondents were informed about the study objectives, and information about those surveyed was kept confidential. An incentive grant of 50,000 VND (about 2 USD) was given to each surveyor. After more than 2 months of surveying, with 254 surveys distributed, we have collected 215 surveys. After filtering incomplete responses, we were left with 192 questionnaires (for each business, we only managed about one vote for analysis).

Data Analysis Methods

We used IBM SPSS 25 and IBM AMOS 25 software to analyze research data. SPSS 25 software is used to analyze Cronbach Alpha, Kaiser-Meyer-Olkin coefficient Measures the adequacy of sampling, Total Variance Interpreted shows the percentage of variation of observed variables, Pattern Matrix for consideration convergence of factors. AMOS 25 software was used for confirmatory factor analysis (CFA), method variance coefficient, Regression Weights, Standardized Regression Weights, and structural equation modeling (SEM) analysis.

Measurement and structural models are evaluated using indices such as Chi-square ratio and degrees of freedom (χ2/df), goodness-of-fit index (GFI), and root mean square error of approximation (RMSEA).

Using AMOS software with Structural Equation Modeling (SEM) is the most appropriate choice for this article. SEM is a powerful statistical technique that allows for the modeling of complex relationships between multiple dependent and independent variables. In this article, the assessment of business sustainability involves several interrelated factors, such as the impact of different sustainability tools (e.g., Life Cycle Costing, Life Cycle Assessment, Sustainability Reporting Standards, Social Impact Assessment, and Sustainable Supply Chain Management) on the overall sustainability performance and reputation of the business. SEM, through AMOS, can simultaneously assess these multiple relationships, providing a comprehensive understanding of how each tool influences sustainability outcomes. The article deals with constructs such as “business sustainability” and “corporate reputation,” which are latent variables that cannot be measured directly but are inferred through observed indicators (like specific sustainability metrics or stakeholder perceptions). SEM in AMOS is well-suited for analyzing latent constructs because it incorporates both measurement models (confirmatory factor analysis) and structural models, ensuring that the relationships between observed variables and their underlying latent constructs are accurately estimated.

Results of Research

Table 2: After running the rotation matrix, the coefficient KMO = 0.872 > 0.5, sig = .000 < .05, so the model is satisfactory; Table 3: there are seven groups of factors that converge and have cumulative loadings at 66.749% > 50%, which showed that the independent variables explained 66.794% of the dependent variable.

KMO and Bartlett’s Test.

Source. Analysis results from statistical software SPSS.

Total Variance Explained.

Source. Analysis results from statistical software SPSS.

Note. Extraction Method: Principal Axis Factoring.

When factors are correlated, sums of squared loadings cannot be added to obtain a total variance.

From Tables 4 and 5, we see: The results of assessing the sustainability of enterprises by the LCC tool gave the highest impact with an average score of 3.65, followed by the SIA tool with the second highest result at 3.64, LCA is 3.46, SCR is 3.39, SSC is 3.34

Descriptive Statistics.

Source. Analysis results from statistical software SPSS.

Note. SRS = Sustainability Reporting Standards; LCC = Life-Cycle Costing; LCA = Life Cycle Assessment; SIA = Social Impact Assessment; SSC = Sustainable Supply Chain Management; CS = corporate sustainability; CR = corporate reputation.

Mean of Tools.

Source. Analysis results from statistical software SPSS.

Pattern Matrix rotation matrix is used to analyze factor confirmatory in AMOS software, to see whether the elements are convergent and discriminant (Table 6).

Pattern Matrix. a

Source. Analysis results from statistical software SPSS.

Note. Extraction Method: Principal Axis Factoring. Rotation Method: Promax with Kaiser Normalization.

Rotation converged in seven iterations.

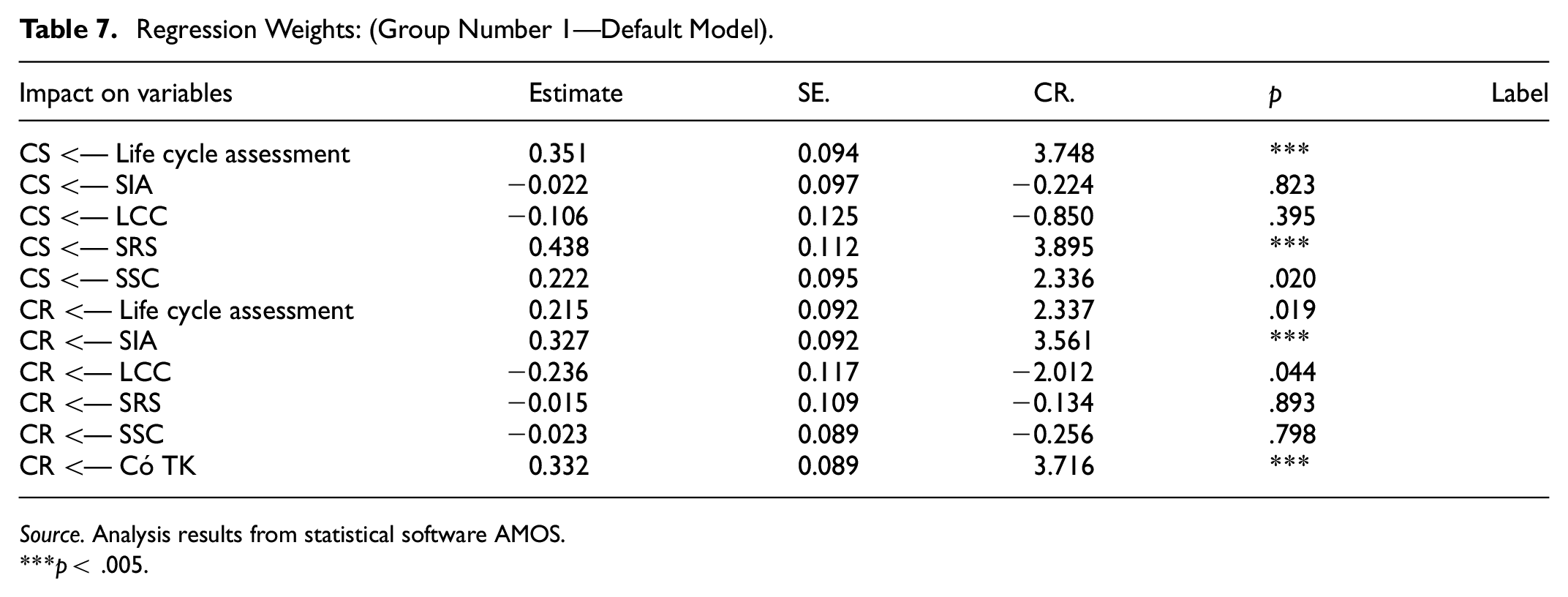

Regression Weights results (Table 7) show that: independent variables SRS, LCA, and SSC have an impact on CS (sig < .05). Hypotheses H1, H5, and H9 are accepted. The independent variables LCC and SIA do not affect CS (sig > .05). Hypotheses H3 and H7 are rejected. Similarly, variables LCA, SIA, LCC, and CS impact CR (sig < .05). Hypotheses H4, H6, H8, H11 are accepted. The independent variable SRS and SSC do not affect CR (sig > .05). Hypothesis H2 and H10 are rejected.

Regression Weights: (Group Number 1—Default Model).

Source. Analysis results from statistical software AMOS.

p < .005.

Table 8 shows the impact of the independent variables (sustainability assessment tools) on the business’s sustainability, reputation, and brand.

Standardized Regression Weights: (Group Number 1—Default Model).

Source. Analysis results from statistical software AMOS.

Impact on CS: The independent variable SRS has the most substantial effect with 0.366, followed by LCA (0.338) and SSC (0.216); LCC and SIA have no impact.

Impact on CR: The intermediate variable CS has the most substantial effect with 0.378, followed by SIA (0.360), LCA (0.235), and LCC (0.226). SRS and SSC have no impact.

The summary results of the influences of factors on the CS and the CR of business are as follows (Figure 2):

The influences of factors on the CS and the CR of the business.

This figure shows the results of the quantitative model, the impact of the independent variables on the dependent variables, and the impact of the dependent variable CS on the dependent variable CR.

Discussions, Recommendations and Conclusions

Discussions

The research findings of this article reveal several notable similarities and differences when compared to other studies on assessing business sustainability. A key conclusion of this article is that the Life Cycle Costing (LCC) tool yields the highest average value among the evaluated assessment tools. However, this does not imply that sustainability assessment outcomes are solely dependent on this method. The findings suggest that while LCC provides the most substantial results as a sustainability assessment tool for businesses, achieving optimal sustainability outcomes requires the integration of multiple tools and frameworks, active stakeholder engagement, and consideration of systemic impacts. These findings align with the studies of Hariram et al. (2023), which emphasize that no single tool can comprehensively assess sustainability; instead, a combination of tools and frameworks is necessary to effectively address the diverse dimensions of sustainability.

This research also highlights some significant differences compared to other studies. For instance, the works of Chygryn et al. (2020) argue that sustainability reporting, particularly through standards like the Global Reporting Initiative (GRI) and the Sustainability Accounting Standards Board (SASB), is essential for advancing corporate sustainability by providing structured and transparent communication of Environmental, Social, and Governance (ESG) performance. While this article acknowledges the critical role of sustainability reporting, it demonstrates that the LCC tool yields higher results among the tools evaluated, suggesting that LCC may have a more pronounced impact when applied as a business sustainability assessment tool.

Similarly, the study by Kumar et al. (2022) underscores the benefits of Life Cycle Assessment (LCA) in identifying environmental hotspots and fostering sustainable practices. This research corroborates that LCA plays a significant role in influencing sustainability assessment outcomes. Both studies agree that LCA enables businesses to identify areas for improvement and make informed decisions related to product design, procurement, and manufacturing. However, this article highlights that the impact of LCA is secondary to that of LCC, offering a more nuanced perspective on which tools may drive the most significant changes in specific contexts.

A key finding of this research challenges the conclusions of Kazakova and Lee (2022) regarding Sustainable Supply Chain Management (SSCM). While their study asserts that SSCM plays a direct and substantial role in sustainability outcomes, this research suggests that its impact, although positive, may be less significant than that of Life Cycle Costing (LCC) or Life Cycle Assessment (LCA) in certain contexts. The assumption that SSCM alone can drive corporate sustainability fails to acknowledge the complexity of sustainability integration across industries. This research, instead, supports the argument of Riad et al. (2024), who emphasize that SSCM is most effective when combined with broader sustainability frameworks rather than being treated as a standalone mechanism for corporate resilience.

Furthermore, this study critically evaluates the role of Social Impact Assessment (SIA), revealing that it does not significantly influence business sustainability outcomes. This directly contradicts the findings of Yildiz Çankaya and Sezen (2019), who argue that SIA is essential for assessing a company’s social contributions. However, such claims often overlook the inconsistencies in how SIA is applied across different industries and regulatory environments. Unlike their broad, theoretical assumptions, this study presents empirical evidence showing that while SIA may enhance corporate reputation, its direct impact on business sustainability remains negligible. This aligns with the recent work of Johnson (2024), who highlight that ESG performance—when measured through quantifiable metrics—yields more tangible financial and reputational benefits than generic social impact assessments.

This research also deepens the discussion on how different assessment tools influence corporate sustainability and their intermediary role in shaping corporate reputation. The findings confirm that corporate sustainability itself acts as the strongest mediator in influencing sustainability outcomes, followed by social impact assessment, LCA, and LCC. These results resonate with the argument of Hariram et al. (2023), who stress that corporate sustainability is not merely a reflection of responsible business practices but also a strategic alignment with stakeholder expectations. However, unlike earlier studies that treat these tools as equally impactful, this research demonstrates that some frameworks yield substantially stronger results than others, further questioning the overemphasis on tools like SSCM and SIA.

Additionally, this study critically examines the use of sustainability reporting and assessment tools such as LCA and SSCM. While previous studies, including Kumar et al. (2022), highlight LCA as a crucial tool for identifying environmental impacts and promoting sustainable alternatives, this research underscores that LCA’s effectiveness is highly dependent on its integration with financial and operational strategies. Similarly, Chen and Gupta argue that sustainability practices are most effective when aligned with circular economy strategies, a perspective that further supports this research’s emphasis on comprehensive, cross-functional sustainability assessments.

Despite some alignment with previous findings, this research diverges significantly in its evaluation of LCC. While Chygryn et al. (2020) emphasize sustainability reporting as the primary driver of corporate responsibility, this study presents compelling evidence that LCC outperforms other tools when used for sustainability assessment. This contradicts the prevailing assumption that transparency in reporting equates to sustainability impact. Instead, this research suggests that financial-based assessments, like LCC, offer a more concrete pathway for companies to implement measurable and cost-effective sustainability strategies.

Furthermore, while prior research, including Yildiz Çankaya and Sezen (2019), has positioned SIA as an essential component of corporate sustainability, this study exposes the limitations of such claims. The assertion that SIA directly enhances sustainability performance appears to be based more on theoretical frameworks than on empirical evidence. The findings here align more closely with Johnson and Lee (2024), who demonstrate that ESG-driven financial incentives produce stronger sustainability commitments than social impact assessments alone.

In summary, this research presents a more nuanced and empirical perspective on sustainability assessment, challenging overly generalized conclusions from earlier studies. The evidence underscores the necessity of integrating multiple tools and frameworks, as no single assessment method can comprehensively capture the complexities of sustainability. This study also highlights that the impact of each tool varies significantly based on its application within a company’s strategic framework. These findings reinforce the conclusions of Riad et al. (2024), who argue that sustainability assessment should be approached through an integrated, adaptive lens rather than a one-size-fits-all model. Ultimately, this research provides a stronger foundation for companies seeking to enhance sustainability outcomes through a combination of financial, environmental, and operational strategies.

Recommendations

To achieve a comprehensive and effective sustainability assessment, businesses should integrate multiple tools and frameworks that address diverse dimensions of sustainability, rather than relying solely on one method such as Life Cycle Costing (LCC) or Social Impact Assessment (SIA). This multi-faceted approach will enable enterprises to gain a broader evaluation of their environmental, social, and economic performance and enhance the accuracy and relevance of their assessments. Combining various tools, such as Sustainability Reporting Standards, Life Cycle Assessment (LCA), and Sustainable Supply Chain Management (SSCM), will provide deeper insights into potential areas for improvement, facilitate benchmarking against peers, and enhance stakeholder engagement by demonstrating a commitment to transparency and accountability.

Businesses should prioritize the development of a sustainability-oriented culture that encourages continuous learning, improvement, and engagement across all levels of the organization. This includes educating employees about the importance of sustainability, fostering innovation in sustainable practices, and aligning business strategies with long-term sustainability goals. Moreover, companies should ensure that sustainability data is of high quality, reliable, and consistent to support meaningful assessments and decision-making.

Engaging stakeholders is also crucial to driving meaningful sustainability improvements. Enterprises should actively communicate their sustainability performance, goals, and progress to stakeholders through transparent and regular reporting, using recognized standards like GRI or SASB. This fosters trust, enhances corporate reputation, and attracts socially responsible investors and customers.

Finally, businesses should adapt their sustainability assessments to evolving standards and emerging trends. Staying updated with global sustainability frameworks, regulations, and best practices will enable companies to remain competitive, mitigate risks, and capitalize on new opportunities for sustainable growth. Integrating findings from sustainability assessments into core business strategies, policies, and actions is essential to creating a resilient, responsible, and future-ready organization.

Conclusions

There are views that just one method of assessing an enterprise’s sustainability level is enough. However, employing multiple sustainability assessment tools in an enterprise offers a broader evaluation, increased accuracy, tailored assessments, benchmarking opportunities, stakeholder engagement, identification of blind spots, and adaptability to evolving standards. These benefits contribute to a more robust and effective sustainability management approach, improving environmental, social, and economic performance.

The product life cycle assessment (LCA) approach provides an essential starting point for global sustainability reporting, including future emerging trends in this context. A business can enhance its reputation as a responsible and sustainable organization by implementing sustainability practices. This can help build stakeholder trust, improve brand value, and drive long-term business success. The Sustainability report standards tool offers a robust framework, comprehensive assessment, benchmarking opportunities, stakeholder engagement, and improved communication. These factors contribute to meaningful and impactful sustainability assessments, enabling enterprises to drive positive change, enhance their reputation, and contribute to a more sustainable future.

It’s essential to recognize that life cycle costing and social impact assessment tools provide valuable insights and potential for driving sustainability improvements. However, realizing their impact requires a holistic approach that includes integration into business processes, fostering a sustainability-oriented culture, engaging stakeholders, ensuring data quality, and taking appropriate actions based on the findings.

Overall, corporate sustainability strongly impacts corporate reputation due to values alignment, meeting stakeholder expectations, risk mitigation, competitive advantage, long-term value creation, and transparency. Embracing sustainability practices not only benefits the environment and society but also enhances the overall perception of the company, leading to improved reputation and stakeholder support.

It’s important to note that the impact of sustainability report standards and sustainable supply chain management on corporate reputation may vary depending on how effectively they are implemented, communicated, and integrated into the organization’s overall sustainability strategy. To maximize the positive impact on reputation, companies should prioritize genuine sustainability efforts, ensure transparency, engage stakeholders, and consistently demonstrate their commitment to responsible practices throughout the supply chain.

While these factors may influence the perceived impact of sustainability report standards and sustainable supply chain management on corporate reputation, it is essential to recognize that adopting and implementing these practices can still contribute positively to a company’s reputation over the long term. The specific circumstances and actions of the enterprise will ultimately determine the actual impact on reputation.

Research Limitations and Future Research Directions

The study’s limitations may significantly influence the interpretation of results, particularly given the cultural and economic context of Vietnam. One key constraint is the reliance on specific sustainability assessment tools, which may not fully capture industry-specific sustainability dimensions. This could lead to an incomplete or skewed evaluation, as certain sectors may emphasize environmental factors while others prioritize social or economic aspects.

Another concern is the subjectivity in the scoring method, where the selection of criteria and weight allocation may reflect implicit biases. This subjectivity could be exacerbated in Vietnam, where regulatory inconsistencies and varying levels of corporate transparency may influence how sustainability is reported and assessed. Additionally, the use of AMOS software, while effective for structural modeling, may overlook external macroeconomic factors and informal business practices, which are common in Vietnam’s rapidly evolving market.

Future research should integrate a broader range of sustainability assessment tools, incorporating sector-specific and emerging global standards. Alternative statistical models could provide a more nuanced analysis of sustainability impacts, while longitudinal studies would help track changes over time. Furthermore, considering regional and cultural variations in sustainability expectations would enhance the applicability of findings across diverse economic landscapes.

Future research should focus on addressing the sector-specific applicability of sustainability assessment tools in Vietnam. Given the diversity of industries—from manufacturing to services and agriculture—different sectors may prioritize sustainability dimensions differently. For instance, the manufacturing sector may benefit from enhanced Life Cycle Costing (LCC) models, integrating real-time environmental impact tracking using Internet of Things (IoT) sensors. Conversely, the financial and service sectors may require advanced ESG performance models, incorporating machine learning algorithms to assess long-term sustainability risks.

Another crucial avenue for research is the role of digital transformation in sustainability assessments. Emerging technologies such as blockchain for supply chain transparency and artificial intelligence-driven sustainability reporting could revolutionize how companies in Vietnam evaluate and communicate their sustainability performance. Investigating how these technologies influence the accuracy, efficiency, and adoption of sustainability assessments would provide critical insights for both policymakers and businesses.

Additionally, future studies should examine how Vietnam’s regulatory landscape and cultural attitudes toward sustainability shape corporate behavior. For instance, state-owned enterprises (SOEs) may respond differently to sustainability pressures compared to private enterprises or foreign-invested firms. Research could explore how government incentives or policy changes influence the adoption of sustainability frameworks across these different business models.

Finally, longitudinal studies are essential to track how sustainability initiatives impact corporate performance over multiple years. This would help determine whether early adopters of integrated sustainability tools experience measurable long-term benefits in financial stability, market competitiveness, and stakeholder trust.

Footnotes

Ethical Considerations

This article does not contain any studies with human participants performed by any of the authors.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.