Abstract

Environmental, social, and governance (ESG) activities, along with green innovation, have become crucial strategies for achieving sustainable development in business. However, the relationship between ESG activities and green innovation remains inconclusive in the current literature. This study aims to clarify this relationship by addressing three key questions: (1) whether ESG activities are linked to green innovation, (2) the mechanisms through which these activities influence green innovation, and (3) the conditions that enhance their effectiveness. Therefore, we integrated the Input-Process-Outcome(IPO) model with leadership theory and collected empirical data through a questionnaire survey of 299 small and medium-sized Chinese manufacturers. The results indicate that each of ESG activities has a positive impact on green innovation, with the social and governance(SG) aspects partially mediated by employees’ cognition, Furthermore, the moderated mediation analysis shows that the strength of this mediation varies depending on the leadership style of the CEO. These findings highlight the critical roles of employees’ cognition and CEO leadership in fostering green innovation through ESG activities, providing new insights into effective management for sustainable development.

Introduction

In the era of high-quality economic development, achieving sustainable business practices has become imperative for maintaining competitive advantage and fulfilling corporate social responsibility (Dyllick & Hockerts, 2002; Kramer & Porter, 2006; Mohy-ud-Din, 2024). In this context, environmental, social, and governance (ESG) activities and green innovation are viewed as crucial strategies for advancing sustainable development in business (Hojnik & Ruzzier, 2016; Y. Liu et al., 2022; D. Wang et al., 2022) Investors show interest in ESG investments for several reasons. Firstly, by prioritizing ESG investments, ethical investment practices are actively encouraged. Secondly, ESG investments are increasingly acknowledged for their ability to enhance the performance of managed portfolios, mitigate portfolio risks, and bolster returns. In addition, ESG initiatives aim to balance economic success with social and environmental responsibility, while green innovation focuses on reducing environmental impacts through new products, processes, and practices (Y. Liu et al., 2022). however, while prior studies have examined ESG activities and green innovation separately, few have focused on their direct relationship (H. Liu & Lyu, 2022; Tan & Zhu, 2022; H. Zhang et al., 2024). Consequently, the potential synergy between ESG activities and green innovation remains under-explored, presenting an important research gap in understanding how ESG initiatives contribute to sustainable innovation.

This study seeks to address this gap by examining the relationship between ESG activities and green innovation, identifying the mechanisms and conditions that enhance this connection Specifically, we incorporate employees’ cognition as a mediating variable and CEO leadership style as a moderating variable. These factors are crucial but often overlooked elements in the ESG activities—green innovation relationship. Cognitive theories suggest that employee perception shapes their engagement in organizational objectives, including sustainability initiatives (Schunk & DiBenedetto, 2020). While the role of executive cognition in sustainability decisions has been widely acknowledged (Kim et al., 2012), limited research has considered how employees’ cognition-especially in regard to ESG activities-affects green innovation. Examining this perspective contributes to a more comprehensive understanding of how organizational behavior and employee engagement facilitate sustainable practices. Moreover, we investigate the moderating role of CEO leadership. Different leadership styles can significantly impact corporate decision-making, activities and strategies, including the adoption and success of ESG and innovation. CEOs are instrumental in setting an organization’s direction and influencing how ESG objectives are perceived and implemented, thus affecting the overall success of green innovation (Zhu & Huang, 2023). By considering the variation in leadership styles, this study adds depth to the understanding of the boundary conditions under which ESG initiatives foster green innovation.

The focus on small and medium-sized manufacturing enterprises in China as the sample for this study is intentional. In contrast to larger firms, small- and medium-sized enterprises (SMEs) possess unique advantages in innovation capacity, although they have to face constraints of financial resources and higher costs. They can leverage their flexibility, cost efficiency, and legitimacy to excel in green innovation (Ahinful & Tauringana, 2019). In addition, China’s policy landscape further emphasizes the importance of green development, as evidenced by its commitment to achieving carbon peak by 2030 and carbon neutrality by 2060, as outlined in the “Report to the 20th National Congress of the Communist Party of China.” This unique context not only heightens the relevance of ESG and green innovation but also positions China as a critical setting for understanding sustainable business practices.

This study integrates the Input-Process-Output (IPO) model, the stakeholder theory, and the leadership theory to build a robust framework for analyzing the ESG activities-green innovation relationship. The IPO model supports an understanding of how inputs(ESG activities) are transformed through processes (employees’ cognition) to yield outputs (green innovation; McGrath, 1964). Stakeholder theory further underscores the importance of addressing stakeholder needs, such as those of employees and shareholders, in sustainable practices (Freeman, 1984). Leadership theory, on the other hand, offers insight into how CEO characteristics influence organizational priorities and decision-making. By addressing these theoretical gaps and incorporating employees’ cognition and CEO leadership into the analysis, This study provides both theoretical and practical insights for firms seeking to promote green innovation through ESG activities. Our findings aim to guide companies in formulating and executing ESG activities more effectively, shaping employees’ cognition actively, and thereby advancing green innovation and bolstering their sustainable development.

Theoretical Background

IPO Model

This study employs the IPO model to examine the relationships among ESG activities, employees’ cognition, and green innovation. The IPO model was first proposed by McGrath (1964). The IPO model is a foundational framework for analyzing team performance, especially in contexts involving multi-level interactions (Bunderson & Sutcliffe, 2003; Edmondson, 1999). According to McGrath (1964), The model categorizes components as input refer to the factors affecting team member interactions, including individual factors, team factors, and organizational and environmental factors; the process, as a critical link in the model, refers to the interactions between team members to ensure that the task is completed, and describes how the inputs are transformed into outputs; output includes team performance and members’ response. In our study, ESG activities serve as inputs that influence employees’ cognition (the process), ultimately leading to green innovation outcomes. This structure allows for a systematic understanding of how ESG activities foster an environment conducive to sustainable innovation.

Sustainable Development (Input Factors)

To evaluate sustainable development practices, we adopt the ESG framework as a measure of corporate commitment to sustainability. Sustainable development, according to the triple bottom line (TBL) perspective (Elkington, 1998) identifies economic, environmental, and social pillars as fundamental aspects of sustainable management. These dimensions form the basis for evaluating a firm’s sustainable management performance (Konrad et al., 2006). Further, from a stakeholder-centered perspective, sustainable management involves business activities aimed at enhancing communication with stakeholders, achieving economic benefits, and ensuring environmental and social soundness to ensure corporate development (Saam, 2015). Finally, from a management performance perspective, sustainable management encompasses activities that create shareholder value over a long term by capitalizing on opportunities arising from economic, environmental, and social development while managing associated risks (Stead & Stead, 2015).

In all these perspectives, sustainable management revolves around stakeholders, who maintain direct or indirect relationships with a firm’s activities. Companies must acknowledge the needs and interests of diverse stakeholders and systematically incorporate them into their management practices to achieve sustainable growth (T.-T. Li et al., 2021; Young et al., 2005). In summary, ESG activities, as a new dimension of sustainable development, signifying a company’s responsibility toward society, environment, and governance while pursuing economic value. Environmental factors address the company’s impact on ecological systems, Social factors emphasize its relationships with employees, customers, and communities, and Governance focuses on corporate policies, ethics, and transparency. This study addresses the lack of empirical evidence on how ESG activities act as inputs that contribute to green innovation, especially through internal mechanisms such as employees’ cognition.

Employees’ Cognition (Process)

Employees’ cognition represents a key process to connect ESG activities and green innovation. According to cognitive theory, an individual’s behaviors arise from the interaction between internal cognitive systems and external stimuli (D. Wang et al., 2022; Wood & Bandura, 1989). Cognition is foundational for interpreting external information and making decisions, which, in turn, drive organizational behavior (Schunk & DiBenedetto, 2020). In a corporate setting, employees’ understanding and perception of ESG efforts are crucial for translating these activities into innovation outcomes. This study uniquely highlights employees’ cognition as a neglected but essential factor in sustainable development, providing a psychological pathway through which ESG initiatives can influence green innovation.

Green Innovation (Output Factors)

Green innovation, characterized by novelty and value, facilitates achieving management and competitive objectives while preserving resources and the environment (Franceschini et al., 2016; Song et al., 2019), that is, green innovation embodies a series of innovative endeavors that promote sustainable environment by reducing pollution and securing competitive advantages through technological enhancements and novel administrative practices (Song et al., 2019). Through technological advancements and novel management practices, green innovation not only fosters environmental benefits but also provides companies with a competitive edge. Thus, according to D. Zhang et al. (2019), we define green innovation as the generation of novel ideas, products, services, processes, or management systems related to energy efficiency, pollution prevention, waste recycling, green product design, and eco-friendly logistics services. This study extends the green innovation literature by examining how ESG activities can stimulate such innovation, especially in the presence of supportive employee cognition and CEO leadership.

Stakeholder Theory

Stakeholder theory serves as a lens for understanding the influence of various stakeholders on ESG activities and green innovation. Firms are motivated to engage with both internal and external stakeholders to adapt to changing environments and capitalize on opportunities (Barnea & Rubin, 2010; Sepasi et al., 2021). This process can be understood through the lenses of legitimacy and stakeholder theory (Deegan, 2014). The legitimacy and stakeholder theories are system-oriented, focusing on a firm’s connection to its environment and emphasizing adaptation to specific aspects such as social contracts or stakeholder requirements (Scott, 2008). According to the stakeholder theory, stakeholders are defined as a group with the authority to participate in decision-making within the realm of management activities. A company is driven to efficiently cultivate relationships with various stakeholders on an ethical foundation to create value (Gray et al., 1996; Phillips et al., 2019). Through this framework, our study examines how firms can leverage stakeholder relationships to foster green innovation as a pathway to sustainable development.

Hypotheses

The Relationship Between Environmental, Social, Governance Activities, and Green Innovation

Prior research has pointed out the importance of ESG dimensions—environmental, social, and governance—in shaping firms’ sustainability strategies, but the distinct impact of each on green innovation remains under-explored (Cho et al., 2013; Hart, 1995). This study hypothesizes a positive relationship between each ESG dimension and green innovation.

First, we explore the impact of environmental activities on green innovation. Through engaging in environmental activities, including the efficient use of capital, technology, and resources, enterprises can comply with institutional pressures, reduce costs (Hart, 1995), minimize exposure to risks (Cho et al., 2013), and access eco-friendly business prospects (L. Wang et al., 2014). That is, environmental activities play a crucial role in cost reduction and enhancing the capacity to seize new business opportunities (Singh et al., 2020). In conclusion, by engaging in environmental activities, firms reduce costs, mitigate risks, and capitalize on eco-friendly opportunities (Singh et al., 2020; L. Wang et al., 2014), thereby enhancing their ability to innovate sustainably. Thus, the following hypothesis is established:

Hypothesis 1-1. Environmental activities have a positive relationship with green innovation.

Second, we explore the impact of social activities on green innovation. Through social activities, as a fundamental component of corporate strategy, enterprises can communicate with external and internal stakeholders effectively, comply with laws and regulations (Brammer & Millington, 2008; Phillips et al., 2019), and form a crucial foundation for gaining competitive advantages (Dressler & Paunović, 2019). That is, based on the stakeholder theory, social activities foster stakeholder engagement, reduce regulatory risks, and enhance brand reputation, which together contribute to sustainable competitive advantage, thereby promoting green innovation. We thus propose the following hypothesis:

Hypothesis 1-2. Social activities have a positive relationship with financial performance.

Lastly, we explore the impact of governance activities on green innovation. Corporate governance refers to the mechanism that oversees and regulates the overall management processes of a company, including resource procurement, resource allocation, and profit distribution (Allegrini & Greco, 2013). Weak corporate governance tends to erode corporate profitability and value (Balachandran & Faff, 2015), while governance that is transparent and equitable empowers companies to generate stable profits and enhance their performance (Alsayegh et al., 2020; Esteban-Sanchez et al., 2017). According to the signaling theory, this can solve the problem of information asymmetry, enhance transparency, optimize resource utilization, attract investment capital, and increase investor confidence. It is important for promoting long-term investment and high-risk green innovation. That is, transparent governance enhances trust and reduces information asymmetry, making it easier to attract investment and support for green initiatives. Thus, the following hypothesis is established:

Hypothesis 1-3. Governance activities have a positive relationship with green innovation.

The Mediating Role of Employees’ Cognition

We explore the effect of employees’ cognition on the relationship between ESG activities and green innovation in this section. The cognition of ESG activities among employees within a company refers to the extent to which employees perceive and acknowledge the ESG strategy and commitment (Nekhili et al., 2021). It is important to cultivate employees’ cognition of ESG activities and foster proactive participation, so as to gain legitimacy from employees in the implementation of ESG management strategies and decision-making processes.

By engaging in environmental initiatives, enterprises can heighten their employee’s environmental awareness. Similarly, through social activities, employees can tangibly experience enterprises’ contributions to society and themselves and thus can enhance their satisfaction with and loyalty to enterprises. Governance activities play a pivotal role in building a positive image and reputation through transparent information disclosure, thereby enhancing employees’ confidence (Barnea & Rubin, 2010). Consequently, through ESG activities, enterprises can improve employees’ cognition by enhancing environmental awareness, employee satisfaction and loyalty, and confidence to support long-term, less immediately profitable, and potentially challenging green innovations. Following the IPO model, promoting ESG activities within enterprises can improve employees’ cognition, subsequently promoting green innovation. Accordingly, the following hypotheses are established:

Hypothesis 2-1. Employees’ cognition mediates the positive relationship between environmental activities and green innovation.

Hypothesis 2-2. Employees’ cognition mediates the positive relationship between social activities and green innovation.

Hypothesis 2-3. Employees’ cognition mediates the positive relationship between governance activities and green innovation.

The Moderated Mediation Effect of CEO Leadership

In the previous section, we explore the importance of employees’ cognition. In this section, to refine the analysis of the ESG-green innovation relationship, this study explores the moderating effect of two distinct CEO leadership styles: transformational and transactional. According to Burns and Stalker (1961), leadership stands as a cornerstone for effective management and innovation, and the choice of leadership style exerts a profound impact on an enterprise’s development. The leadership theory classifies leadership in various ways, with transformational and transactional leadership being prominent categories. These styles, while conceptually distinct, can coexist within an organization, as leaders may adopt multiple styles to address varying employee needs and organizational objectives (Bass, 2008). Specifically, a CEO may use transactional leadership to ensure task completion and reward performance, while simultaneously employing transformational leadership to inspire employees toward higher-order goals. These leadership styles exhibit contrasting effects on employees’ behavior and attitude (Ko, 2011). Transactional leadership is a leadership approach where leaders establish reciprocity through an exchange relationship that primarily revolves around fulfilling the external needs of team members (Bass, 2008). In essence, transactional leadership is built upon interdependent exchanges, where leaders provide desired rewards, and team members, in turn, deliver desired outcomes. Transactional leadership may reinforce employees’ focus on immediate goals, aligning their efforts with the company’s green innovation objectives. Transformational leadership, in contrast, represents a dynamic process of mutual motivation and empowerment, where the leader inspires intrinsic motivation among team members to fulfill their higher-order needs (Bass, 2008). This leadership style can amplify employees’ commitment to green innovation by reinforcing the strategic importance of ESG activities.

This dual approach is relevant in the context of ESG and green innovation, where transformational leadership can inspire employees toward long-term environmental goals, while transactional leadership provides the necessary support and incentives to achieve short-term milestones. Hence, this study proposes that both leadership styles can influence the mediation effect of employees’ cognition on the ESG-green innovation relationship, with each style providing complementary benefits in the context of green innovation. In this context, this study explores the impact of the two different leadership styles. Consequently, the following hypotheses are established:

Hypothesis 3-1. The effect of environmental activities and green innovation through employees’ cognition is stronger with higher levels of transactional leadership.

Hypothesis 3-2. The effect of social activities and green innovation through employees’ cognition is stronger with higher levels of transactional leadership.

Hypothesis 3-3. The effect of governance activities and green innovation through employees’ cognition is stronger with higher levels of transactional leadership.

Hypothesis 4-1. The effect of environmental activities and green innovation through employees’ cognition is stronger with higher levels of transformational leadership.

Hypothesis 4-2. The effect of social activities and green innovation through employees’ cognition is stronger with higher levels of transformational leadership.

Hypothesis 4-3. The effect of governance activities and green innovation through employees’ cognition is stronger with higher levels of transformational leadership.

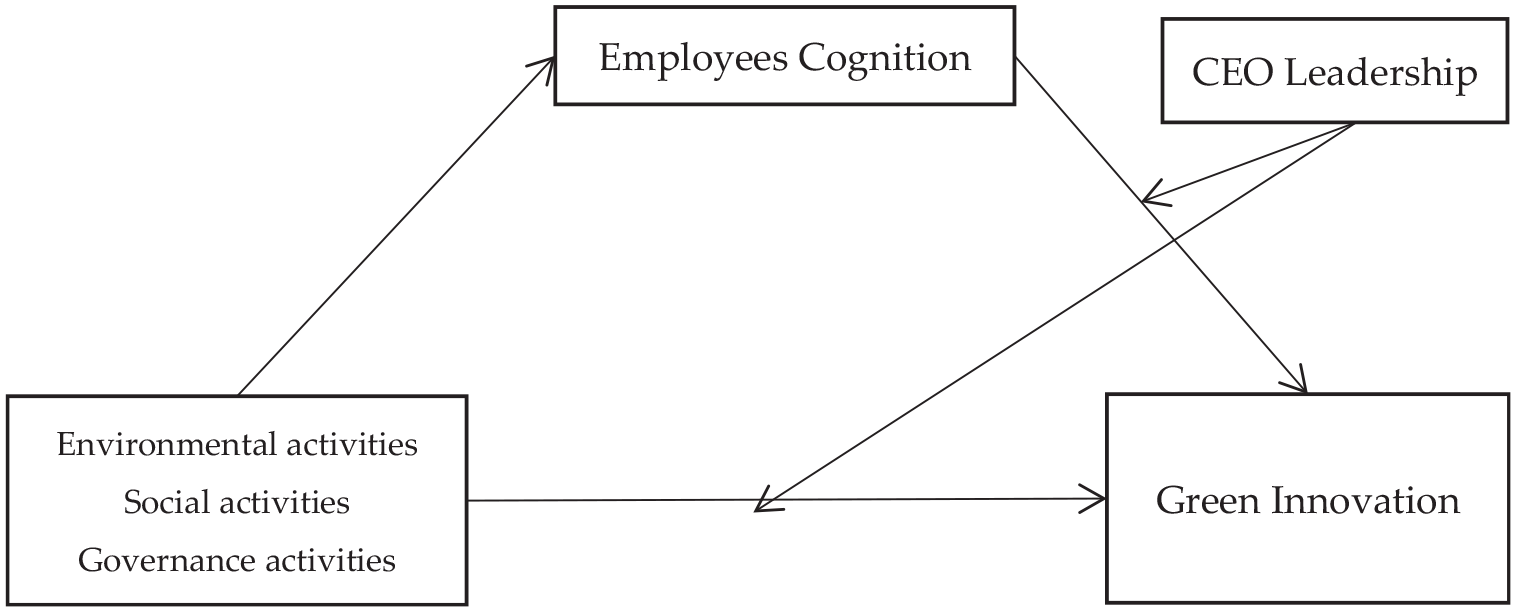

The research model depicting these hypotheses is illustrated in Figure 1. The causal relationships between ESG activities, employees’ cognition, and green innovation are drawn upon the IPO model and stakeholder theory, while the moderating influence of CEO leadership on these relationships is rooted in the leadership theory.

Research model.

Methodology

Sample and Data Collection

This study focuses on small and medium-sized enterprises (SMEs) within ESG-sensitive industries, specifically apparel/textile, machinery/equipment, chemicals, computer/communication, and food/beverage. These industries are significantly impacted by ESG demands due to their environmental footprint, regulatory scrutiny, and high stakeholder expectations (Eccles et al., 2014; Kramer & Porter, 2006). For instance, the apparel/textile industry faces challenges in sustainable sourcing and labor practices, while the chemicals and machinery/equipment sectors are under pressure to minimize environmental pollution and resource consumption. The computer/communication and food/beverage industries, meanwhile, are experiencing growing demands for transparency and sustainable supply chains. These factors justify the selection of these industries, as they represent sectors where ESG practices are critical for regulatory compliance and maintaining a competitive advantage (Y. Liu et al., 2022). According to Industrial Development Statistics of the National Economic Development Report provided by the Bureau of Statistics of China, we selected the SMEs operating in these industries(Y. Liu et al., 2022). From these industries, we identified 2,060 firms as our initial target population, excluding the enterprises with incorrect contact information and those with less than 4 years of operational history.

Firstly, we designed the questionnaire based on relevant literature. Then, we conducted a pretest of the questionnaire with four senior SME executives in the relevant industries to gauge the clarity and appropriateness of the questions. We revised the questionnaire based on their feedback. Then, we carried out a pilot test of the revised questionnaire with 10 senior SME executives to evaluate their responses, and made further adjustments based on their feedback in relevant industries. Finally, we distributed the final questionnaire via email, sending reminders at 2-week intervals. As a result, we received a total of 332 responses, with 299 responses usable, yielding an effective response rate of 14.5%.

Measurement

We measured all constructs using multiple items, and for each construct, we computed a composite score by calculating the means of the items.

Dependent, Independent, Mediating, and Moderating Variables

Respondents were asked to indicate the extent of their agreement or disagreement (1 = “strongly disagree” to 7 = “strongly agree”) with the items on a seven-point Likert scale. Green innovation was measured using a scale adapted from Chu et al. (2018). To measure the level of enterprises’ ESG activities, we modified a scale based on various sources, including Elkington (1998), Petti and Zhang (2011), Shubham et al. (2018), and the ESG evaluation guidelines of the Korea Corporate Governance Service (Baron & Kenny, 1986; Hess et al., 2002). Employees’ sustainability cognition was measured using a scale adapted from Rui and Lu (2021) and Gadenne et al. (2009). Furthermore, CEO leadership, divided into transformational and transactional leadership, was measured using a scale adapted from Avolio et al. (1999) and Manzoor et al. (2019).

Control Variables

To account for other factors that may influence green innovation, we included industry type, firm size, firm age, and research and development (R&D) intensity as the control variables in our model. The industry type, known to have an impact on firms’ direction (Rothaermel & Alexandre, 2009), was controlled using dummy-coded industries. Larger firms with more resources may have a higher investment capacity for their ESG activities than smaller firms with fewer resources (Rothaermel & Alexandre, 2009). Thus, the firm size was controlled for and measured by the number of employees. Firm age indicates accumulated knowledge and experience. Compared with younger firms, older firms can accumulate more knowledge and experience to improve their innovation (Lavie et al., 2010). Thus, we controlled for the firm age effect measured by the number of years of operation. R&D intensity, measured as R&D expenses as a percentage of sales, can influence firm green innovation, so we controlled for R&D intensity in our study (Y. Liu et al., 2019).

Analyses and Results

Analyses Method

We used AMOS 25 to conduct a confirmatory factor analysis and used PROCESS Macro for SPSS v. 3.14 to examine the indirect effects in our mediation and moderated mediation models. Since AMOS cannot model interactions of continuous latent variables, we utilized the bootstrap confidence interval (CI) approach to calculate the lower limit confidence interval (LLCI) and upper limit confidence interval (ULCI) of a 95% bootstrap CI for indirect effects based on 5,000 bootstrap samples (Hayes, 2022; Preacher & Hayes, 2008).

Reliability and Validity of the Measurement

This study executes a confirmatory factor analysis to evaluate the reliability and validity of the measurements (Bentler & Chou, 1987; Fornell & Larcker, 1981). We first assessed construct reliability using composite reliability (CR) and Cronbach’s alpha. As shown in Table 1, the results indicate a high level of reliability, exceeding the recommended minimum value of 0.7 for both CR and Cronbach’s alpha (Hayes, 2022). We conducted convergent and discriminant validity tests to assess our constructs’ dimensionality. In Table 1, all items are loaded on their intended factors, with factor loading exceeding the cutoff value of 0.5 and the average variance extracted (AVE ) exceeding the threshold of 0.4 for each scale. These results support the 7-factor solution with an adequate level of convergent validity (Nunnally, 1967). The discriminant validity of our constructs was further confirmed using multiple factors analysis, thus affirming satisfactory discriminant validity for all the factors (Nunnally, 1967). Finally, as shown in Table 1, the goodness-of-fit results for our CFA model reveal an acceptable level of fit, with χ2 = 906.185, df = 573, p < .001, χ2/df = 1.570, CFI = 0.948, TLI = 0.943, and RMSEA = 0.044.

Reliability and Validity.

Note.χ2 = 906.185, df = 573, p < .001, χ2/df = 1.581, CFI = 0.948, TLI = 0.943, RMSEA = 0.044.

t-values for n = 299; SE = standard error; CR = composite reliability; AVE = average variance extracted.

p < .001.

Common Method Bias

Due to relying on a single respondent to measure the variables, we checked and controlled for common method bias. First, we utilized a question randomization option to mitigate potential common method bias. Second, we examined potential bias by conducting Harman’s one-factor test with an unrotated factor solution. The analysis yielded a total of seven factors with an eigenvalue of 1.0 or higher, explaining 35.31% of the variance, which is well below the maximum threshold of 50%).

To capture the common variance among all observed variables, a common latent factor (CLF) test is performed by introducing a new latent variable to our CFA model. This ensured that all observed items were related to the model. We then compared the standardized regression weights of all items for the models with and without CLF. The differences were smaller than 0.2, confirming that common method bias did not affect the validity of this study.

Hypotheses Test

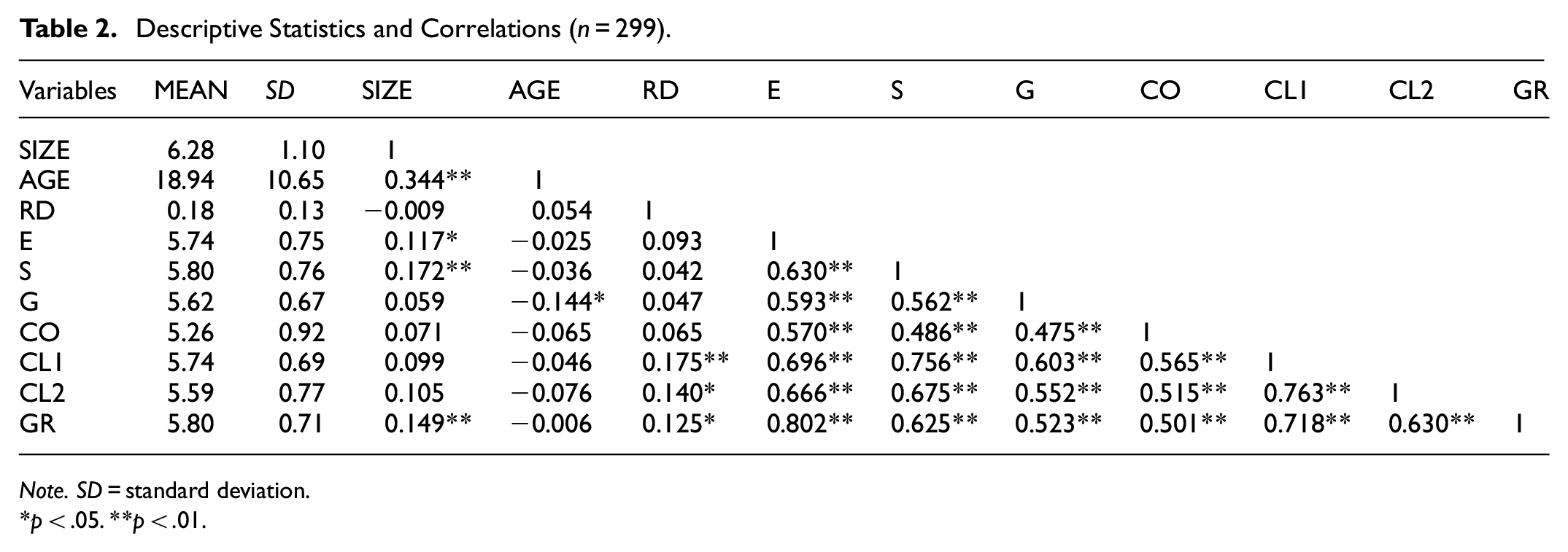

Descriptive Statistics and Correlations

We present the standard deviations, mean, and correlations among the variables in Table 2. As expected, all correlations among the variables are significant and positive, consistent with the presumed direction of the relationships outlined in our hypotheses. Specifically, the correlations in the direct relationships between variables are higher than the indirect ones. Examination of the variance inflation factor (VIF) scores revealed no instances of multicollinearity. The maximum VIF score is 5.25, which is below the rule-of-thumb cutoff point of 10.

Descriptive Statistics and Correlations (n = 299).

Note. SD = standard deviation.

p < .05. **p < .01.

Analyses

Hierarchical Multiple Regression Analysis

Models 13 in Table 3 provide the results of the multiple regression analysis, examining the total effect of ESG activities on green innovation, while considering all control variables. As anticipated, the coefficients for environmental (β = .790, p < .001), social (β = .618, p < .001), and governance (β = .514, p < .001) activities are all positively significant, supporting Hypotheses 1-1, 1-2, and 1-3. Then, comparisons of standardized regression coefficients indicate that environmental activities have the greatest influence on green innovation, followed by social and governance activities.

Hierarchical Multiple Regression (n = 299).

Note. Table provides parameter estimates and standard errors. Due to limitations of space, industry dummies impact on dependent variables are not presented.

p < .05. **p < .01. ***p < .001.

Based on the Baron and Kenny’s causal step approach. Model 4-6 reveals that environmental (β = .551, p < .001), social (β = .478, p < .001), and governance (β = .465, p < .001) activities all have a significantly positive impact on employees’ cognition. The relative magnitude of the effects on employees’ cognition is ranked as environmental, social, and governance activities. As a final step for mediation analysis, Model 13 shows that the effect of employees’ cognition on green innovation is not significant, Models 14-15 show the significant effect between social and governance activities on green innovation, thus supporting Hypotheses 2-2 and 2-3.

Statistical Inference Test for Mediation Effects

The causal step approach does not formally quantify the indirect effect or require inferential testing. To estimate indirect effects statistically in our mediation models, we computed the LLCI (Low Limit Confidence Interval) and ULCI (Upper Limit Confidence Interval) of a 95% bootstrap CI for indirect effects, based on 5,000 bootstrap samples.

The results of the bootstrap significance test are reported in Table 4. The total, direct, and indirect effects of social and governance activities on green innovation are significantly positive, whereas the indirect effects of environmental activities are not significant. These results align with the results of hierarchical multiple regression analysis, thereby supporting Hypotheses 2-2 and 2-3. Consequently, pursuing a high level of social and governance activities positively affects employees’ cognition, which, in turn, leads to superior green innovation.

Bootstrap Significance Test for Mediating Effects.

Note. All the control variables are included; Bootstrap samples: 5,000.

Moderated Mediation Analysis

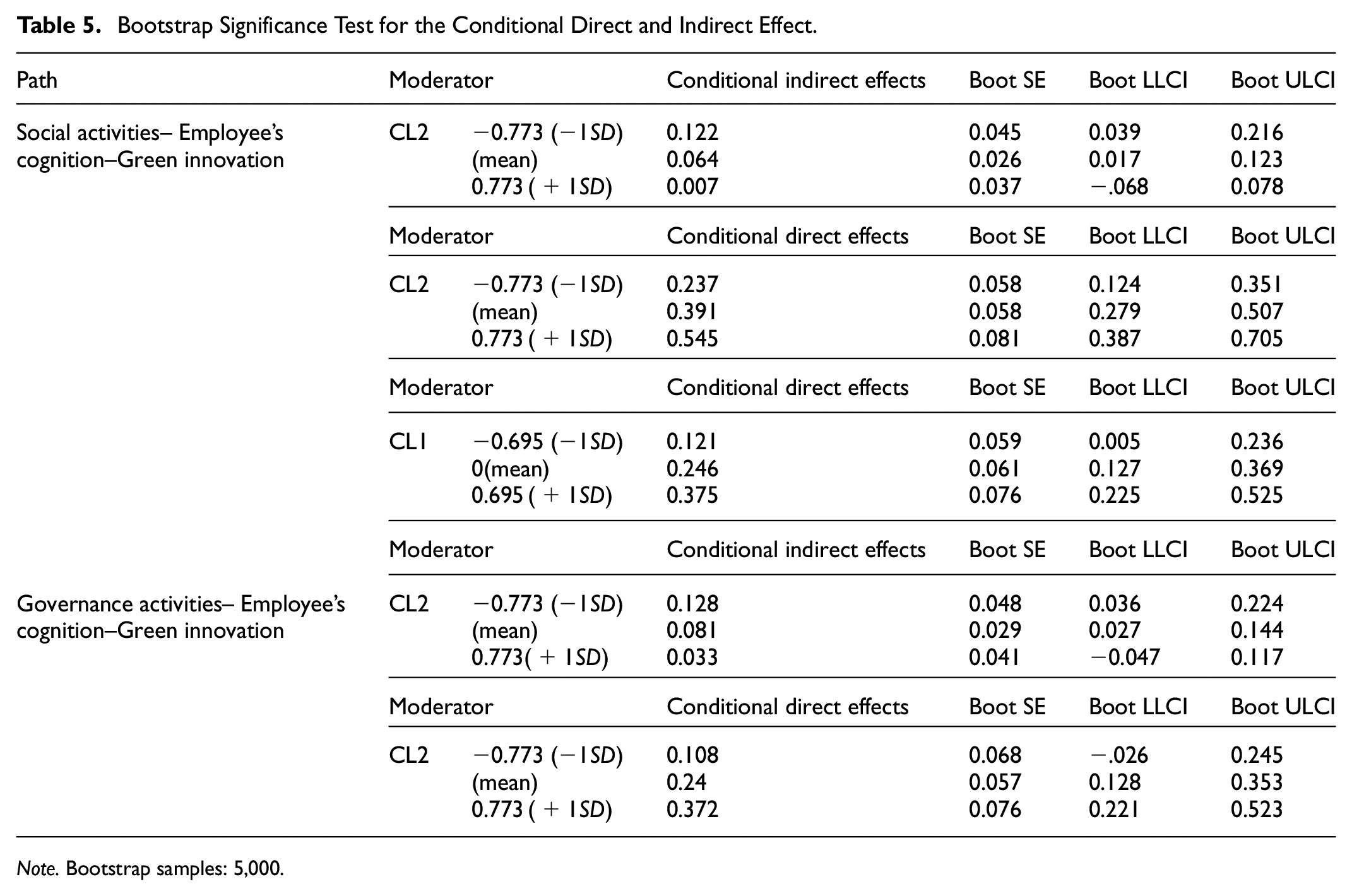

Hypothesis 3 suggests that the positive effect of ESG activities on green innovation through employees’ cognition varies depending on the type of leadership, necessitating a moderated mediation analysis. If only one mediator exists in a model, the indirect effect is the product of two effects. Evidence of moderation of the indirect effect exists if one of the paths defining the indirect effect is moderated by a formal statistical test, and the other effect is statistically significant because the indirect effect is a product of two paths, one of which is moderated. However, we need to test whether the indirect effect is statistically dependent on a moderator. Therefore, a follow-up inferential test is required to determine whether the conditional indirect effect differs from zero at specified values of a moderator, ascertaining where the indirect effect is significant in the distribution of the moderator, and where it is not.

Following Preacher and Hayes “s statistical approach, we first examined how the positive effect of ESG activities on employees” cognition (mediator) varies depending on the type of leadership. As shown in Models 7 to 12 of Table 3, first, the interaction terms of “Social activities × transformational Leadership” (b = 0.156, p < .001), “Social activities × transactional leadership” (b = 0.143, p < .001) and “Governance activities × transactional leadership” (b = 0.130, p < .01) have a significantly positive impact on employees’ cognition, thus significantly improving the model fits.

Additionally, we test for the conditional indirect and direct effects at various values of moderators (+1 SD, mean, −1SD) by estimating the conditional effects at those values. The indirect effects of both social and governance activities on green innovation are significantly positive at the two specified values of the moderators shown in Table 5. In particular, the conditional indirect effect of social activities is stronger for the firms scoring low (−1 SD) in transactional leadership (b = 0.122; CI[0.039, 0.216]). The conditional direct effect of social activities is stronger for the firms scoring high (+1SD) in transactional leadership (b = 0.545. CI [0.387, 0.705]) and transformational leadership (b = 0.375; CI = 0.225–0.525).

Bootstrap Significance Test for the Conditional Direct and Indirect Effect.

Note. Bootstrap samples: 5,000.

Similarly, the conditional direct effect of governance activities on green innovation is more pronounced for those with high in transactional leadership (b = 0.372; CI[0.221, 0.523]). However, the conditional indirect effect of governance activities on green innovation is stronger for the firms scoring low (−1 SD) in transactional leadership (b = 0.128; CI [0.036, 0.224]). Based on the two-step approach to moderated mediation, Hypotheses 3-2, 4-2, and 4-3 are supported, while Hypotheses 3-1, 3-3, and 4-1 are not. These results suggest that the firms pursuing high levels of environmental activities can promote green innovation directly. Even among the firms pursuing high levels of social and governance activities, those exposed to stronger transactional leadership are likely to yield better employee cognition, which subsequently leads to superior green innovation.

Conclusion

Discussion

Sustainable development has become a global concern. Firms are pursuing sustainable management through ESG activities to foster green innovation. Based on the data from 299 SMEs in China, we reveal that each ESG activity significantly promotes green innovation. Furthermore, our mediation analysis demonstrates that employees’ cognition mediates the link between social and governance activities and green innovation. This implies that social and governance activities can play a significant role in promoting green innovation by positively influencing employees’ cognition and attitudes toward sustainability. Specifically, when companies actively engage in social and governance initiatives—such as fostering an inclusive work environment, maintaining ethical standards, and enhancing corporate transparency—they can heighten employees’ environmental awareness and commitment to sustainable practices. This mediating effect of employee cognition suggests that the direct link observed in previous studies between firms’ environmental or ESG activities and green innovation may, in fact, be partially explained by this internal cognitive shift among employees rather than being a purely direct effect. This study aims to provide supporting evidence for this mediating role, emphasizing that the indirect pathway through employee cognition is a critical mechanism through which social and governance activities foster green innovation. Environmental activities have the most significant impact on green innovation and employees’ cognition. However, environmental activities cannot impact green innovation through improvement of employee’s cognition. This finding implies that environmental initiatives, by their nature, may inherently drive innovation, perhaps due to more direct and visible impacts on production processes and resource use.

The study’s moderated mediation analysis indicates that CEO leadership styles play a critical role in shaping the ESG-green innovation relationship. Specifically, the positive impact of social and governance activities on green innovation, mediated through employees’ cognition, is intensified under transactional leadership, which emphasizes contingent rewards and clear expectations. Interestingly, transactional leadership demonstrated a stronger moderated mediation effect compared to transformational leadership, underscoring the effectiveness of structured incentives and explicit goal-setting over inspirational approaches in the context of SMEs. This finding aligns with the hypothesis that employees respond more effectively to transactional leadership in contexts where clear outcomes and short-term gains are emphasized. Although both leadership styles can coexist, this study suggests that, for green innovation, transactional leadership may have a more immediate impact within ESG-focused environments.

Implication

First, this study emphasizes the importance of integrating ESG concepts into management processes and shaping employees’ cognition to achieve green innovation. It provides a theoretical foundation for subsequent studies that analyze firms’ strategies with the IPO model. This study contributes to the integration of the Input-Process-Output (IPO) model with leadership theory, illustrating how the combined framework can offer insights into the ESG-green innovation link. Future research may apply this model in different contexts, examining how diverse organizational processes and leadership styles influence sustainability outcomes across industries. Additionally, addressing the low AVE (average variance extracted) for latent variables remains crucial. Although the AVE was slightly below the conventional threshold, factor loadings and composite reliability indicate that hypothetical testing is appropriate, particularly as the constructs used in the model are well-supported in existing literature. Second, in the current economic and social transformation phase, firms can gain investments to promote research and development (R&D), adopt green technologies, and mitigate principal-agent risks by enhancing their ESG activities. This study emphasizes the importance of employees’ cognition in this process, particularly for SMEs.

Additionally, transactional leadership has more influence on business currently. For practitioners, integrating ESG principles within management practices is essential for fostering green innovation. This study highlights that firms should actively cultivate employees’ cognition of ESG efforts, especially in social and governance dimensions, to drive green innovation. Given the stronger impact of transactional leadership, managers in SMEs may consider incorporating reward systems and explicit performance expectations aligned with ESG objectives to optimize innovation outcomes. Finally, governments should enhance ESG evaluation systems and information disclosure mechanisms by improving ESG information disclosure mechanisms. The findings suggest that policymakers should support enhanced ESG information disclosure and establish evaluation frameworks that promote transparency. Improved ESG metrics allow stakeholders to make informed decisions, thereby facilitating sustainable investment and supporting high-quality economic and social development. This can help stakeholders make informed decisions and support the overall goal of high-quality economic and social development.

Limitations and Future Research

Despite its academic and practical implications, this study has several limitations that should be considered in future research. First, generalization of results should be done cautiously due to the limitation of samples. This research was conducted on SME manufacturers in Beijing, China, and the specific social, cultural, and industrial factors that may have influenced the outcomes. Future studies can expand the analysis model to include other countries, regions, and other industry firms to address this limitation. Then, there is a potential issue of reverse causality, as green innovation may also drive sustainable management activities. However, due to survey data and the time lag between variables, controlling for reverse causality was challenging. This study relied on cross-sectional survey data, limiting the ability to control for causality. Future research could employ longitudinal or secondary panel data to address this potential reverse causality, providing a more dynamic view of the ESG-innovation relationship. Finally, future studies should explore whether the coexistence of transformational and transactional leadership styles has a synergistic effect on ESG-related outcomes, given that each style may support different aspects of green innovation. Addressing these areas will deepen understanding of how ESG activities, leadership styles, and employee engagement collectively shape sustainable development practices.

Footnotes

Acknowledgements

All authors have seen and approved the manuscript. None of the authors has a financial or personal relationship with other people or organizations that could inappropriately influence or bias the content of the research and No competing interests are at stake.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author upon reasonable request. Some parts of the data may not be publicly accessible.