Abstract

The importance of being a pioneer in a market is one of the major topics in the field of strategic management. While being a pioneer in the market can offer distinct advantages, the strategic importance of being a fast second mover cannot be overstated. This study explores the concept of fast following within the realm of catch-up strategy, highlighting significant factors of corporate governance that can help accelerate the speed of catching up. Drawing from theoretical frameworks and empirical evidence from the pharmaceutical industry of South Korea, this study intends to reveal how ownership concentration can impact the catch-up speed of the second mover and discusses the role of the CEO’s experience and education in this relationship. The findings of the study demonstrate that firms with higher ownership concentration tend to enter markets at a faster pace, supporting theories that concentrated ownership facilitates streamlined decision-making and quicker responses to market opportunities. Additionally, CEO education and tenure significantly moderate this relationship. Firms led by long-tenured and highly educated CEOs benefit from enhanced decision-making agility, enabling faster market entry.

Introduction

To bridge the gap between first movers and late comers, a catch-up strategy emerges as an essential approach that aims to accelerate progress and foster sustainable development. The idea of “catching up” has become a popular topic of interest in academic literature since the early 1950s (Mathews, 2006a). A catch-up strategy has been seen as a planned and targeted technique employed by developing and post-war European countries to speed up their growth and lessen disproportions in key areas including infrastructure, technology, economy, and education (Abramovitz, 1986; Souzanchi Kashani et al., 2022). It acknowledges the importance of learning lessons from the successes and experiences of developed nations, allowing late comers to achieve quick growth and development by adopting existing proven strategies (Kuo et al., 2018). Later development in this field exceeded the idea including catch-up strategies for firms (Capone et al., 2021; Malerba & Lee, 2021). However, the effectiveness of catch-up strategies—especially in terms of timing and speed of entry—remains underexplored, particularly in industries where the dynamics of first-mover and second-mover advantages can be complex and highly context-dependent.

Research has long shown that first-mover firms can secure key benefits such as brand recognition, market share, customer loyalty, superior production process, and technological leadership (Lieberman & Montgomery, 1988, 1998; Xie et al., 2021). Even considering these advantages, recent studies are analyzing the idea that late entry in some cases may be more beneficial than first entry. Second movers may benefit from reduced risks, lower entry costs, and improved market knowledge through window of opportunity (Li et al., 2023; Mathews, 2002). Through a thorough understanding of customer preferences, pain points, and unfulfilled demands, the second mover can tailor their offerings and value proposition to better resonate with the target market.

Existing research has explored catch-up dynamics, identifying factors that get influenced when firms choose to catch-up, such as market saturation, technological advancements, and industry life cycles (Ethiraj & Zhu, 2008; Giachetti & Li Pira, 2022). In the realm of technology and economic development, literature has evolved significantly, analyzing technology as a multifaceted capability spanning firm, sector, and national levels (Fagerberg, 1987; Souzanchi Kashani et al., 2022). Early studies, particularly on the newly industrializing economies of East Asia, have provided insights into the technological catch-up processes, emphasizing the role of systemic factors and firm-level capabilities (Mathews, 2006b). However, while these discussions have grown in breadth, certain gaps in understanding remain, especially regarding the nuanced mechanisms of catch-up speed and its determinants. Schoenecker and Cooper (1998) emphasized the strategic importance of competitive market entry timing while highlighting the lack of empirical exploration into its drivers. According to Robinson et al. (1992), there is evidence to support the “comparative advantage hypothesis,” which states that enterprises choose their market entry timing approach based on particular resources and capabilities. While resource and capability factors are central to research on the determinants of catch-up speed, the specific governmental factors influencing the speed of catch-up lack empirical depth. Furthermore, the current body of research often neglects how latecomer firms strategically adapt to resource limitations in smaller markets, such as South Korea.

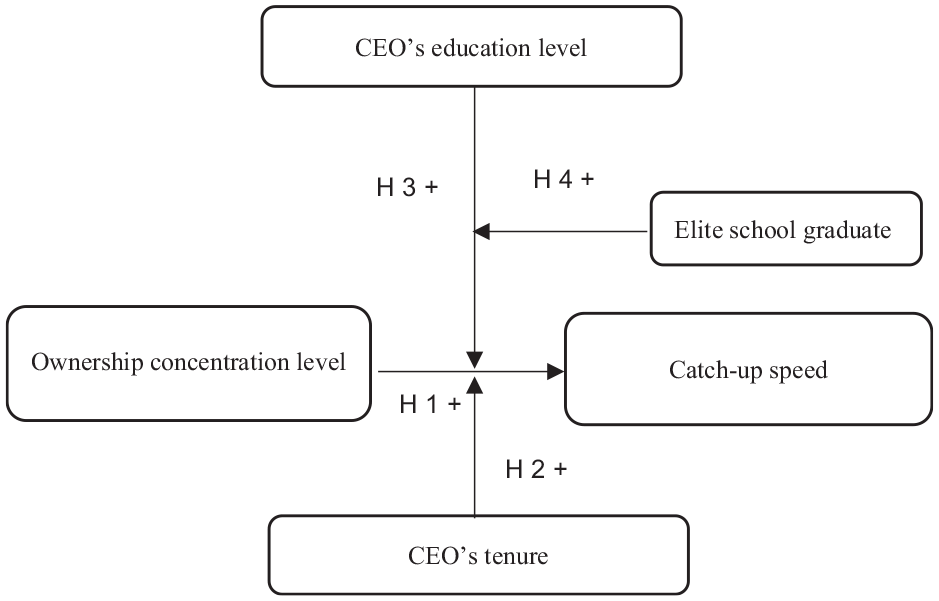

Building on these ideas, this study analyzes catch-up speed from the perspective of factors influencing it, specifically focusing on corporate governance. The study explores the role of ownership structure in shaping the decisions of catch-up timing, through the approach where firms seek to duplicate successful practices of industry leaders. It posits that ownership concentration influences catch-up speed by affecting decision-making agility and strategic focus. Additionally, leadership factors, such as CEO tenure and education, are hypothesized to moderate the relationship between ownership concentration and catch-up speed. Evidence suggests that CEO traits significantly impact risk-taking, innovation, and adaptability in dynamic markets (Farag & Mallin, 2018; Jaggia & Thosar, 2022; Kish-Gephart & Campbell, 2015).

This study uses data from pharmaceutical companies in South Korea, a context where the second-mover strategy is often more advantageous compared to multinational competitors due to capital and resource limitations (Mathews, 2002). To test the hypotheses, the study employs ordinary least squares (OLS) moderated regression analysis, which allows for examining both the direct effects of ownership concentration on catch-up speed and the moderating effects of CEO characteristics, such as tenure and education. The findings from this study offer actionable implications for firms attempting to develop their competitive positioning in dynamic markets. As noted by Hawk et al. (2013), firms with strong intrinsic speed capabilities can better time their entry and adjust to changing market conditions.

The article is structured as follows. Section 2 defines the theoretical frameworks underpinning the research, namely catch-up speed and ownership concentration, highlighting their relevance to the field of research. Section 3 proposes the hypotheses and overall, the research model. Section 4 explains the research method, including data collection and analysis. And the last two sections discuss the results and conclusions of the study.

Background & Literature Review

Understanding Catch-Up Speed and Factors Influencing It

A catch-up strategy refers to a set of deliberate actions and policies pursued by a country or firm to accelerate its economic growth and narrow the gap with more advanced economies or competitors (Malerba & Lee, 2021; Mathews, 2006a). It is often employed by countries or firms that are considered “late comers” or lagging in terms of technological advancements, industrial development, productivity, or overall economic performance. Catch-up strategies typically aim to leverage various resources, capabilities, and opportunities to enhance competitiveness, increase productivity, and accelerate economic growth (Buckley et al., 2020; Saghafi et al., 2020).

From its early conceptualization to its practical implementation, the evolution of catch-up strategy highlights the dynamic nature of business and the continuous quest for advancement. The idea of a catch-up strategy can be traced back to the Industrial Revolution when late-comer countries sought to close the economic gap with early industrialized nations. The focus in these studies was primarily on the developing countries (Abramovitz, 1986; Amsden, 1992) and their development strategies. Early catch-up strategies frequently centered on copying effective models and importing technology and knowledge to promote industrialization (Buckley et al., 2020). Later, the studies started to emerge and include not just countries but industries (Kuo et al., 2018) and firms (Capone et al., 2021; Mathews, 2002).

From the evolutionary perspective, the early studies defined the catch-up strategy from the perspective of imitating the leader. Fagerberg and Godinho (2005) defined the catch-up strategy as the ability of a late comer to narrow the gap between productivity and income compared to a leader. The notion of catch-up strategy transformed from imitation to innovation-driven methods as the world of business changed. Late-comer businesses started to understand that innovation and specialized skills were more important for competitiveness and long-term success than simple replication (K. Lee, 2019; K. Lee & Lim, 2001). The development of knowledge-based economies, technological developments, and the growing significance of intellectual property rights all contributed to this change.

The question of whether fast technology imitation, which refers to the act of improvement of existing technologies, products, or services developed by others by including new features (Zheng Zhou, 2006), is influencing the firm performance is an active topic of research study in the research field. Early studies on this discussed early imitation as a profitable alternative to moving first (M. L. Katz & Shapiro, 1986; Teece, 1986). One of the famous supporters of this idea is Drucker. According to Drucker (1985), early imitators can learn from first mover’s mistakes and avoid them by improving their own products.

Some studies addressed this question from the perspective of a first mover, by explaining the risks of fast imitation responses from rivals. The timing effect and durability of first mover are empirically tested by H. Lee et al. (2000), and their findings indicate that the faster a firm launches a new product, the higher the abnormal returns; however, the faster a firm imitates, the bigger the negative abnormal returns for the first mover. Lieberman and Montgomery (1988) explore the concept of first-mover advantages and discuss how second-movers can overcome these advantages through fast entry strategies. It highlights the importance of timing and speed in capturing market share and achieving superior firm performance. In their study on the development of the research of first-mover advantage Lieberman and Montgomery (1998) addressed this question again. The authors propose that firms with strengths in new product development may choose pioneering strategies, while those with marketing and manufacturing strengths may prefer to enter later after uncertainties are resolved. However, the timing of entry may not always be a managerial choice, as firms with weaker innovative capabilities may be forced into late-entry positions. Late entrants can succeed if they possess valuable resources or capabilities lacking by pioneers and can even acquire pioneers to combine resources and skills. Empirical studies have shown that a firm’s resources play a crucial role in entry timing (Rodríguez-Pinto et al., 2007; Schoenecker & Cooper, 1998), but understanding is still limited.

Different perspectives for the study of the importance of catch-up speed can be seen through the comparison between fast followers and latecomers. Unlike latecomer companies, which enter established markets after initial pioneers, fast followers strategically time their market entry to capitalize on and improve proven technologies, consumer preferences, and market demand. Latecomer companies, on the other hand, enter the market after the initial wave of innovation has occurred (Li et al., 2023). By embracing innovation and taking calculated risks, second movers position themselves as forward-thinking and adaptable companies. This not only helps them compete in the present and create barriers for latecomers but also builds resilience for the future, as they are better equipped to respond to changes in market dynamics, regulatory requirements, and consumer preferences.

The analysis of factors that influence this catch-up speed in strategic management research has received little academic interest. The majority of studies see market entry timing as a factor itself and concentrate on the connection between entry timing and firm performance (Schoenecker & Cooper, 1998). According to Shamsie et al. (2004), factors that influence market entry timing can be divided into three broad categories. First, the category includes factor conditions that the company faces at market entry. Entry conditions for late movers are dependent on the remaining market opportunities when they choose to enter. Second, organizational resources that a company possesses may influence market entry timing. The probability and timing of entry are shaped by the firm’s current resources and capabilities, dictating its strengths and weaknesses in the market (Robinson et al., 1992). Lastly, late entrant success is also determined by the performance of its products compared to those of competitors available in the market (G. S. Carpenter & Nakamoto, 1990). Different studies analyze catch-up speed in different contexts, and for this study, we will refer to the catch-up speed as the rate at which the second mover brings its product to market.

Ownership Concentration and Its Importance

The distribution of ownership rights among shareholders in a firm is commonly referred to as ownership concentration (Demsetz & Villalonga, 2001). It can vary from widely dispersed ownership, where no single shareholder holds a significant stake, to concentrated ownership, where a few shareholders or a single shareholder hold a substantial portion of the company’s shares. Firm ownership concentration is often viewed as a corporate governance mechanism aimed at mitigating agency problems, particularly the principal-agent problem, in corporations with dispersed ownership structures (Jensen & Meckling, 1976).

Recent research studies on ownership concentration have delved into several critical areas, reflecting its significant influence on corporate governance and firm behaviors. These studies explore how ownership concentration impacts overall firm performance (Iwasaki & Mizobata, 2020; Wu et al., 2020), corporate financial policies, including risk management, capital structure, and dividend policies (Asadi & Ramezankhani, 2022; Kirimi, 2024).

While theoretical literature has extensively explored the effects of concentration on product position and variety within markets (George, 2007; Saghi-Zedek, 2016), empirical evidence on the question of market entry speed remains scarce. The study of Li et al. (2010) examines the relationship between ownership concentration and product innovation in China and the findings of the study suggest a nuanced relationship between ownership concentration, product innovation, and learning orientation within firms. Specifically, the results indicate that ownership concentration exhibits an inverse U-shaped relationship with both product innovation and learning orientation. The study conducted by Thomas et al. (2009) delves into the relationship between ownership structure and new product development (NPD) within the affiliates of transnational corporations (TNCs) operating in China. The findings of the study shed light on the differential effects of ownership structures on NPD within TNC affiliates in China. According to the results of empirical testing, wholly- owned subsidiaries, where the parent company maintains full ownership control, exhibit greater autonomy, and flexibility in implementing NPD strategies. These subsidiaries may benefit from direct access to corporate resources, technology, and knowledge, enabling them to pursue ambitious and innovative NPD initiatives.

Concentrated ownership within companies can serve as a powerful motivator for innovation, providing additional support in terms of funds, technology, human resources, and managerial capabilities (Fernández & Nieto, 2005). However, despite the potential benefits of concentrated ownership for innovation, company managers may exhibit a tendency toward caution when pursuing innovative projects, citing high costs and risks as constraints (Zhang et al., 2018). In this context, shareholder involvement plays a crucial role in influencing management decisions related to innovation investment. Studies suggest that concentrated ownership can help minimize agency problems by aligning the interests of shareholders and managers (Gillan & Starks, 2000). Controlling shareholders, with a significant stake in the company, are more likely to scrutinize management decisions and advocate for strategies that prioritize innovation and long-term value creation.

Moreover, research indicates that concentrated ownership positively influences company performance. One of the early mentions of this can be seen in the thesis of Berle and Means (1932). The authors analyze the changing nature of the corporation and its implications for the ownership and control of large-scale enterprises. They highlight the increasing concentration of economic power in the hands of managers, leading to potential agency problems and conflicts of interest between managers and shareholders. The main implication of this study is a positive correlation between ownership concentration and profit rates. Compared to this, a later study on corporate ownership structure (Demsetz & Lehn, 1985) argues that shareholders consciously choose to alter ownership structure, understanding the consequences of loosening control over management. The higher cost and reduced profit associated with diffuse ownership should be offset by other profit-enhancing aspects. The authors present empirical evidence from a profit rate equation analysis, using alternative measures of ownership concentration. The results show no significant relationship between ownership concentration and accounting profit rate, contradicting the Berle-Means thesis.

In this aspect, this study suggests a new topic for discussion in ownership structure literature: the question of how ownership concentration can influence the speed of market entry specifically for companies that do pursue a catch-up strategy.

Hypotheses Development

Ownership Concentration and Catch-Up Speed

As was mentioned above, market entry timing is especially important for rapidly evolving industries such as pharmaceuticals. The pharmaceutical industry is a complex and highly regulated sector that focuses on the research, development, production, and marketing of drugs and medications (Chung et al., 2019; DiMasi et al., 2016). It plays a critical role in improving human health and addressing various diseases and medical conditions. The importance of fast responding became obvious again after the breaking of the pandemic. The pharmaceutical industry invests heavily in research and development to discover and develop new drugs (Deore et al., 2019; DiMasi et al., 2016). This involves extensive scientific research, clinical trials, and regulatory approval processes. That is why the rapid answer is important not just for the pioneer but also for the second mover.

It is not difficult to find research studies on innovation pioneer’s first-mover advantages. Usually, research in this area includes the hypothesis that it is important for a company to be fast and become a pioneer (Kopel & Löffler, 2008). The idea of imitation speed for the follower’s fast imitation strategy is not very popular. Some of the early studies on this topic explain that a follower can reduce the pioneer advantage of a first mover through reverse engineering (Kerin et al., 1993), and the faster a follower can develop new products, the more distance it can build up from later entrants (Kessler & Chakrabarti, 1996). This idea ensures the diffusion of second-mover advantages and subsequently increases the gap in profitability.

In a company with higher ownership concentration, decision-making power is concentrated in the hands of a few major shareholders or controlling owners. This streamlined decision-making process can enable faster and more decisive actions, including the decision to enter a new market. With fewer stakeholders involved in the decision-making process, the company can quickly assess market opportunities, evaluate risks, and make prompt entry decisions. In companies with higher ownership concentration, major shareholders have a long-term perspective and a clear strategic direction for the company (Kochhar & David, 1996). This strategic focus can facilitate rapid decision-making and execution of market entry plans.

In the pharmaceutical industry, which faces substantial costs related to R&D, clinical trials, and production (DiMasi et al., 2016), this fast decision-making can become crucial. The major factor that raises the importance of R&D investment specifically for second movers lies in the specifics of the industry itself. The pharmaceutical industry is heavily regulated in any country and investing in R&D ensures compliance with existing and changing regulatory standards. Second movers have to conduct their own research to demonstrate the safety, effectiveness, and quality of their products, to meet regulatory requirements imposed by specialized agencies in specific countries (such as the FDA or EMA). The studies on ownership structure showed that firms with higher levels of ownership concentration tend to invest in R&D more. López-Iturriaga and López-Millán’s (2017) study of R&D-intensive industries in 19 developed countries shows that firm R&D investment increases with increasing ownership concentration in countries where legal protection for institutional investors is low. The study also showed that shareholder identity also has an impact on this relationship. While banks and non-financial institutions have a negative impact on R&D as shareholders, institutional investors increase corporate investment in R&D. Kim and Park’s (2016) study of Korean firms also found a positive relationship between ownership concentration and technological innovation activity. The analysis also showed that the coefficient of ownership concentration is much higher for the high R&D spending group than for the low R&D spending group.

Developing new drugs can be a lengthy and costly process. It typically involves several stages, including preclinical research, clinical trials, and regulatory review (Deore et al., 2019). This extensive development cycle, along with high failure rates during clinical trials, contributes to the time and cost associated with bringing a new drug to market. A study of Chinese SMEs (Deng et al., 2013), which focused on examining the differences between single-owner SMEs and multiple-owner SMEs, where principal-agent conflicts and principal-principal conflicts are more likely, found that single-owned firms are more effective at translating research and development into product innovation than firms with multiple owners, who are typically better at leveraging external sources of knowledge. Also, major shareholders often have a significant stake and vested interest in the company’s success. Major shareholders are more likely to be motivated to seize market opportunities promptly, leveraging their influence to drive the entry process forward.

Higher ownership concentration often means that major shareholders possess significant financial resources and influence within the company. They possess deep industry knowledge and networks, that can expedite the allocation of resources required for market entry, such as funding for research and development, production facilities, marketing activities, and distribution channels, which is especially important in the pharmaceutical industry. The concentration of ownership can enable a more efficient mobilization of resources, enabling a quicker market entry.

In view of this, the following hypothesis can be made.

H1. Ownership concentration level in companies pursuing a second mover strategy will positively influence catch-up speed.

The Moderating Role of CEO’s Tenure and Education

The discourse surrounding ownership concentration centers on two main arguments: the potential for enhanced monitoring and control versus the risks of expropriation. On one hand, proponents argue that large shareholders possess both the incentive and the power to effectively monitor and influence managers, thereby mitigating governance issues detrimental to firm performance (Berle & Means, 1932; Shleifer & Vishny, 1986, 1997). Ownership of the company is the source of power that, depending on its concentration and goals, can be used to either side with or against management (Salancik & Pfeffer, 1980). When viewed in this light, ownership serves as the cornerstone of corporate governance and shapes managers’ decision-making about R&D investments and other intangible capital, depending on whether they are looking to the long or short term (Bogliacino et al., 2013; Hill & Snell, 1988). Although major shareholders are primary decision makers in market entry, the chief executive officer (CEO) has the main responsibility, and his personal characteristics can have an impact on the link between ownership concentration and catch-up speed. Specific to this study two major characteristics are chosen: CEO’s tenure and education.

The interest in CEO characteristics and their significance for the company started to gain interest in academic literature due to upper echelon theory. The upper echelon theory shows that there is a correlation between the characteristics of the top manager and some factors of firm performance and strategy choice. Hambrick and Mason’s (1984) seminal article which introduced the concept of upper echelons theory, examines how CEO characteristics, such as age, experience, and education, influence strategic decision-making. It discusses how CEO attributes can shape the strategic direction of the organization. M. A. Carpenter et al. (2004) review and extend the upper echelons theory by examining the antecedents and consequences of TMT composition. It discusses how CEO characteristics interact with the composition of the TMT to influence the strategic decision-making process.

One of the characteristics that received increasing interest from researchers is the CEO’s tenure. According to Herrmann and Datta (2005), tenure is considered a crucial determinant of a manager’s capacity to obtain and analyze information, but as tenure increases there is a noticeable decline in the information gathered and analyzed. The early study on tenure linked longer tenure to better communication, less conflict, and stability (R. Katz, 1982). Also, according to Michel and Hambrick (1992), longer tenure on the top management team may be linked to social cohesiveness and shared cognitive processes. Another study that analyzed the role of CEO’s tenure (Tihanyi et al., 2000) shows that it influences collective decision-making in the company.

Major shareholders, whether they are individuals or institutional investors, use their voting power and board representation to influence CEO appointments. In cases where shareholders have opposing views on the company’s future direction, the selection of a CEO becomes a pivotal decision (Shleifer & Vishny, 1986). Major shareholders advocate for CEO candidates who prioritize initiatives aligned with their strategic objectives, whether it involves cost-cutting measures, market expansion strategies, or innovation initiatives (Nguyen, 2011). The appointment of a CEO who shares their strategic vision enables them to exert influence over the company’s direction and performance. This, in return, creates an environment where the CEO’s decision-making is highly dependent on those of major shareholders.

CEO’s tenure is correlated with accumulated experience and industry knowledge, which provides leaders with insights into market dynamics, customer preferences, and competitive landscapes (Hambrick & Mason, 1984). CEOs with longer tenures may possess a deep understanding of industry trends and market opportunities, enabling them to identify windows of opportunity for fast market entry. This can also be seen through the risky decisions of long-tenured CEOs. Wang and Poutziouris (2010) investigated the relationships between entrepreneurs’ personal characteristics (education level, tenure, and age) and risk-taking in family firms in the UK, and the results provide empirical support for the positive relationship between tenure and risk-taking. Particularly, the authors hypothesize that a family firm CEO with higher tenure in an industry inspires risk-taking, as the CEO has a deeper knowledge of the industry, which enables him to take more risks. The argument presented by Orens and Reheul (2013) suggests that CEOs with experience are more inclined to make risky decisions due to several factors. These CEOs are often more open-minded, which fosters innovation and encourages them to seek out challenges. Moreover, their past experiences equip them with the necessary competence to effectively navigate and manage new risky ideas. Herrmann and Datta (2006) and Chen and Zheng (2014) contribute to this perspective by highlighting that CEOs’ prior experience serves as a reliable indicator of their knowledge, values, and skills. Studies also provide valuable insights into their past activities and strategic choices, which can inform their decision-making process in the present.

As CEOs demonstrate their leadership capabilities and stewardship of the company through longer tenure, major shareholders often develop confidence in their ability to drive value and align with shareholder interests (Dalton et al., 1998). This accumulated trust influences major shareholders’ decision-making, as they may defer to the CEO’s recommendations and strategic initiatives, particularly on matters related to market entry timing. Based on this following hypothesis can be formulated:

H2. CEO’s tenure will positively moderate the relationship between ownership concentration level and catch-up speed.

The pharmaceutical industry is highly dependent on scientific and technical expertise (DiMasi et al., 2016). Professionals in the field must engage in continuous learning to stay updated with the latest developments. Lifelong learning is crucial for maintaining expertise and adapting to evolving industry trends and practices. Many professionals working in this industry, including TMT, researchers, scientists, and drug development specialists, possess advanced degrees such as Ph.D., M.D., or Pharm.D. These educational qualifications provide them with the necessary knowledge and skills to conduct research, develop new products, and enter new markets. Hence, the knowledge and experience of the CEO gathered through working in the industry will facilitate the market entry decision-making process.

According to upper echelon theory (Hambrick & Mason, 1984), the education level of TMT is associated with the capacity for information processing and the ability to find and identify better alternatives for optimal decision-making. Farag and Mallin (2018) based on the study of Chinese IPOs show that CEOs with higher education tend to make risky decisions and they are more resistant to uncertainties. In the study of the airline industry in the US (W. S. Lee & Moon, 2016), education was found to have a positive impact on strategic risk-taking, suggesting that better educated CEOs take more risks because they have more confidence in their intellectual abilities. Comparable results are shown in Herrmann and Datta’s (2005) study on TMT characteristics and international diversification. Above-average educated TMTs should be flexible to change, have a greater tolerance for uncertainty, and have the background and skills necessary to methodically look for new opportunities and weigh their options. Another study by Herrmann and Datta (2002) analyses the influence of CEO’s characteristics and choice of foreign market entry mode. The results marginally supported the hypothesis that a CEO with a higher education level is associated with a preference for fully controlled market entry.

Higher education is perceived as a pathway to success, social status, and personal fulfilment (Jung & Lee, 2016). Graduate degrees, in particular, are highly esteemed, symbolizing advanced knowledge, expertise, and prestige in professional fields. CEOs with advanced degrees in business administration, finance, or relevant industry disciplines are perceived as more qualified to lead the company (Tang et al., 2024), particularly in complex and dynamic industries such as pharmaceuticals. Major shareholders place greater trust in the strategic decisions and recommendations of CEOs with higher education levels, viewing them as leaders with a strong foundation of knowledge and skills. CEOs with higher education levels often possess a broader perspective and strategic vision for the company, which can resonate with major shareholders seeking long-term value creation. Advanced education equips CEOs with analytical tools, critical thinking abilities, and strategic planning skills that are essential for making informed decisions in a rapidly changing business environment.

Based on this following hypothesis can be formulated:

H3. CEO’s education level will positively moderate the relationship between ownership concentration level and catch-up speed.

In the United States different studies show that while privileged individuals are more likely to attend elite universities, the prestige of these institutions also affects graduates’ earnings and status attainment (Dale & Krueger, 2002). In East Asian countries like Korea, there is a widespread belief that graduating from a prestigious university significantly contributes to success in the labor market and facilitates upward social mobility (Jung & Lee, 2016). In Japan, for example, university prestige has a significant positive effect on income and occupational prestige, even after controlling for social background. Graduates of top Japanese universities dominate corporate and governmental elite positions. Institutional networks between schools and employers facilitate job placement in Japan, particularly for graduates of prestigious universities (White & Ishida, 1994). This phenomenon underscores the importance of education at elite institutions for success in the Japanese labor market. Conversely, the Korean higher education system reflects this belief with a clear hierarchical ranking of schools. Admission to the most prestigious universities, known as the SKY universities (Seoul National University, Korea University, and Yonsei University), is seen as a guarantee of access to quality job opportunities. These universities have preferential access to the labor market, especially in large multinational companies, leading to higher wage levels for their graduates compared to those from other institutions (Jung & Lee, 2016).

An early study about the educational characteristics of CEOs (Useem & Karabel, 1986) concluded that individuals with a bachelor’s degree from a prestigious (elite) college, a master’s degree in business administration (MBA) from a prominent program, or a law degree from a leading institution are more likely to rise to top management positions. Finkelstein (1998) also addresses the question of top-ranked colleges. The study suggests that CEOs who graduated from elite universities may experience superior prestige compared to other CEOs. Connection with elite universities may provide graduates with exclusive opportunities to meet other elites from diverse and influential backgrounds.

Jaggia and Thosar’s (2022) empirical study about the relationship between CEOs’ education and risk-taking examined the factor of elite colleges. The results of the study show that CEOs with a degree from an elite university have a higher risk tolerance. Hence, they will be less resilient toward new opportunities and changes in the company.

CEOs from elite schools bring a level of prestige and credibility to the company, which with higher degrees can enhance its reputation in the eyes of investors, customers, and other stakeholders. In the eyes of major shareholders, a CEO with a prestigious educational background can improve the company’s image and attract investment. Considering the specifics of the pharmaceutical industry, graduates of elite schools often have extensive networks within the pharmaceutical industry, including relationships with key leaders in industry, academic researchers, and industry executives. These network connections facilitate collaborations, licensing of new drugs, and partnerships that are critical for regulatory approval, and market entry timing. Major shareholders see CEOs from elite schools as well-positioned to influence these networks to advance the company’s strategic objectives and enhance its competitive advantage.

Based on this following hypothesis can be formulated:

H4. CEO’s academic credentials from an elite university will positively moderate the relationship between CEO’s education level and ownership concentration level-catch-up speed connection.

The Figure 1 below shows the overall model of the study.

Research model.

Research Method

Sampling and Data Collection

For the study, the pharmaceutical industry of South Korea was chosen. This industry’s multidimensional nature, spanning scientific, regulatory, economic, and ethical dimensions, makes it well-suited for a diverse range of business analyses. South Korea has been making significant strides in the development and production of biopharmaceuticals and biosimilars (Chung et al., 2019). Companies have been investing in research and development for innovative biologics and biosimilar products, contributing to the global pharmaceutical market. As of 2021, the pharmaceutical sector in South Korea was valued at over 25.4 trillion South Korean won, making it a noteworthy business (Statista report). A recent study (MarketLine, 2023) assessed that in 2026, the Korean pharmaceuticals market is forecast to have a value of $36.9 billion, an increase of 26.4% since 2021.

Another factor for choosing this sector is the availability of the data. The Ministry of Food and Drug Safety provides statistical databases for all drugs licensed in the country which make it easier to collect the data for market entry timing. The period of study includes the time from 2005 to 2019 and to eliminate the necessity to include more control variables for the period of pandemic years, those years were excluded from this study.

The data sources included two major databases. The data for drug products with the company name, active ingredient, and the date of licenses were collected from the official website of the Ministry of Food and Drug Safety. The data for active ingredients and date of licenses helped to identify first and second mover for specific types of drugs. Overall, for the specified period 2,423 products were identified. The company data (CEO’s personal data included) was collected manually from the official reports that are available on the official website of Repository of Korea’s Corporate Filings. The final sample for the analysis included 279 observations (558 individuals) of first and second market entered drug products for the period of 15 years and 146 companies.

Variables and Their Measures

Independent Variable

The choice of the independent variable differs across studies. Some studies use a dummy variable that simply indicates whether the firm is controlled by a single owner (Deng et al., 2013). On the other hand, concentration measures provide a numerical representation of ownership concentration. A far more popular measure of ownership concentration is the Herfindahl-Hirschman index (HHI). HHI calculates the sum of squared ownership percentages for all shareholders, indicating the level of concentration. Higher HHI scores indicate greater concentration (Kim & Park, 2016; Su et al., 2008).

Another group of measures analyzes ownership structure to identify the largest shareholders and their respective ownership stakes. This involves examining the shareholdings of individual shareholders, institutional investors, insiders, and any significant stockholders, and identifying the percentage of shares held by the largest shareholders or groups of shareholders. Here, the popular method of assessment includes stock concentration, which is the total ratio of stock held by shareholders who own at least 3% of the firm (P. M. Lee & O’Neill, 2003).

For this research purposes, ownership concentration is quantified using the Herfindahl-Hirschman Index (HHI). Higher values of the index indicate a greater level of ownership concentration. The data used to compute the HHI is collected from official year-end company reports, ensuring accuracy and reliability. To maintain temporal precedence and mitigate potential concerns of simultaneity or reverse causality, the ownership concentration measure is calculated for the period preceding the observed market entry time for each firm in the dataset. This approach ensures that the independent variable is measured prior to the dependent variable, to establish the appropriate temporal ordering of variables.

Dependent Variable

The dependent variable is more difficult to assess. The studies on the second mover’s market entry timing are limited. Schoenecker and Cooper (1998) measure the entry timing variable for companies in the minicomputer industry in two parts: entry timing and order. The first method involved calculating the number of months between the sale or installation of the first minicomputer or PC by the firm of interest (in this study first mover) and the month when the firm of analysis (second mover) sold or installed its own first minicomputer or PC. This approach captures the time difference between the initial market entry by other firms and the entry by the firm being analyzed. Measuring entry timing in months provides an advantage by reflecting strategic decisions made by the firm regarding the timing of its entry into the industry. The second operationalization of the dependent variable is the concept of order of entry. This method measures the number of competitors that have already entered the industry when the firm being studied entered the market. By using the order of entry, the analysis considers the relative position of the firm’s entry in relation to its competitors. It provides a practical advantage by reducing the disparity in the mean and variance of the dependent variable across the two industries, ensuring a more comparable and standardized measure of entry timing.

Another, more recent study on followers’ market entry speed (OuYang et al., 2020) introduced two dimensions of entry speed: internal and external. Internal entry speed focuses on a firm’s entry strategies for various products based on its internal factors, such as its product portfolio and strategic intent. It highlights that a firm’s strategic intent is often reflected in the products or services it offers. Internal entry speed considers how the types of products typically provided by the firm influence its timing decisions for market entry. So, for the measure of internal entry timing the number of days passed between the focal new product entry and the prior product entry by the same firm.

On the other hand, external entry speed measures the impact of rivals or other incumbents in the market on entry speed decisions. External entry speed acknowledges trend effects and mimetic behavior, suggesting that followers are more likely to enter the market after observing competitors doing so. This approach to measuring the external entry timing is by considering the number of days a competitor’s product in the same segment has been on the market before the focal firm’s entry. This metric provides a quantitative measure of the competitive landscape and the level of market saturation within a specific product segment. By analyzing the duration between a competitor’s product launch and the focal firm’s entry, researchers and practitioners can gain insights into the strategic considerations driving firms’ timing decisions. A shorter duration indicates a fast-following strategy, where firms aim to capitalize on early market entrants’ investments and learn from their experiences. Conversely, a longer duration suggests a more cautious approach, as firms assess market conditions and gather intelligence before entering.

The dependent variable in this study is competitive market entry speed, operationalized based on OuYang et al.’s (2020) and Schoenecker and Cooper’s (1998) frameworks. It measures the time elapsed (in days) between the entry of a competitor’s product (first mover) and the entry of the focal firm’s product (second mover) in the same segment. For better statistical analysis, the days were converted into months, by considering 30 days as 1 month. This approach captures the speed with which the focal firm enters the market relative to its competitor, reflecting its strategic response to competitor’s actions and market dynamics.

By focusing on competitive market entry speed, the variable provides a quantitative measure of the firm’s relative position in market entry timing. Specifically, the shorter the duration between first mover’s products market entry and second mover’s market entry the faster the catch-up speed.

Moderating and Control Variables

The moderating variables in this study—CEO education level and CEO tenure—capture key aspects of the CEO’s background and experience, which are critical in shaping strategic decisions and firm performance.

The CEO education level is measured as an ordinal variable categorized into four groups based on the highest degree attained: high school (1), bachelor’s degree (2), master’s degree (3), and doctoral degree (4) (Barker & Mueller, 2002; Tang et al., 2024). This categorization standardizes the measurement of academic attainment and reflects the formal educational background of the CEO. Higher values correspond to more advanced education levels, which indicates greater exposure to advanced knowledge, analytical skills, and strategic management concepts. The variable of elite school is a dummy variable that measures whether higher education was obtained in an elite school (Jaggia & Thosar, 2022; Kish-Gephart & Campbell, 2015). Here, an elite school is described as a university ranked in the top 100 universities ranking worldwide.

For more accurate results of the study and firm effect consideration, several control variables were included. The first control variable is family ownership. According to Yoo and Sung’s (2015) study on outside directors and R&D investment, results for Korean firms have shown that family control can have a positive impact on the firm’s R&D investment, facilitating the development and launch of new products. This variable is a dummy variable that takes “1” for companies that are family-owned. Another control variable is firm size, which, according to Hill and Snell’s (1988) study, positively influences R&D spending. Bigger firms also possess more resources that can facilitate market entry. The firm size is measured by the number of employees.

The last control variable included is firm age. Recent studies show that there is a strong connection between firm age and different company outcomes (Coad et al., 2018; Cucculelli, 2018) and older companies due to their insights, experience, and knowledge can facilitate faster market entry.

Results

The means, standard deviations, and Pearson’s correlations among the variables are shown in Table 1. The descriptive statistics reveal substantial variation in ownership concentration (mean = 10.93, S.D. = 11.03) and catch-up speed (mean = 145.48, S.D. = 31.87), reflecting diverse strategic behaviors among the firms analyzed. Correlation analysis highlights a significant positive relationship between ownership concentration and catch-up speed, supporting the main hypothesis that firms with concentrated ownership exhibit faster market entry.

Descriptive Statistics and Pearson Correlation Matrix.

Correlation is significant at the .01 level (2-tailed).

Correlation is significant at the .05 level (2-tailed).

For the regression analysis results are presented in Table 2.

Regression Analysis Results.

Note. Standardized coefficients (standard errors are in parenthesis).

p < 0.1.*p < .05. **p < .01. ***p < .001.

To test the hypotheses OLS regression analysis was conducted in four separate models. The first model examined the relationship between ownership concentration level (OC level) and catch-up speed in Korean pharmaceutical companies, controlling for family ownership, firm size, and firm age. The results revealed a significant positive relationship between ownership concentration level and catch-up speed (β = .243, p < .001), indicating that as ownership concentration increases, market entry speed tends to increase as well, which supports hypothesis 1.

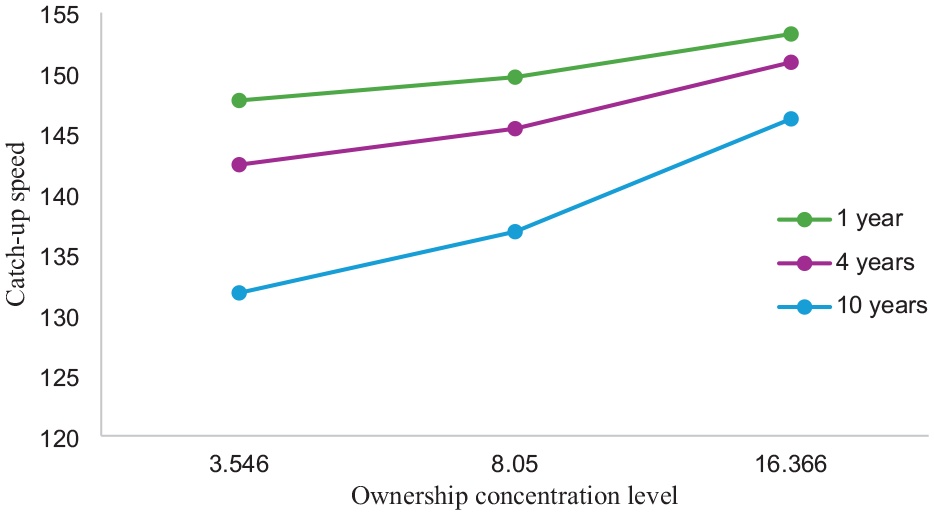

The second model shows results for moderating role of CEO tenure in ownership concentration level - catch-up speed connection. Here, the interaction term between CEO tenure and ownership concentration level was added to the regression model. The results showed a significant interaction relationship (β = .208, p < .05), indicating that in Korean pharmaceutical companies CEO’s tenure positively moderates the relationship between ownership concentration and market entry speed. Simple slope analysis revealed that the positive connection between ownership concentration level and catch-up speed was stronger for long-tenured CEOs compared to short-tenured CEOs (Figure 2).

The moderating effect of the CEO’s tenure.

The third model shows that the level of education of CEOs demonstrated a significant moderating effect on the relationship between the ownership concentration level and catch-up speed (β = .478, p < .05). This indicates that the strength of the relationship between the ownership concentration level and market entry speed varies depending on the level of education. Specifically, the higher the level of education the stronger the main relationship becomes. Figure 3 shows this effect graphically.

The moderating effect of the CEO’s level of education.

The last model describes the three-way interaction involving the ownership concentration level, the CEO’s level of education, and university type. The interaction was found to be not significant (β = −.080). This indicates that the moderating effect shown in the third model is not conditioned by the differences in school types. This result suggests that the level of education but not the type of school where the degree was obtained plays an important role in the main connection.

Discussion and Conclusion

The findings of the analysis shed light on the intricate dynamics underlying the relationships between ownership concentration and catch-up speed in Korean pharmaceutical companies. The significant main effect of ownership concentration on market entry speed indicates that Korean pharmaceutical firms with higher ownership concentration tend to enter markets at a faster pace. This finding aligns with theories suggesting that concentrated ownership structures may lead to faster decision-making and implementation processes within firms, resulting in an increased rate of market entry. Moreover, it highlights the importance of ownership structure in shaping strategic decisions regarding market entry.

This offers valuable insights for managers in the pharmaceutical industry, particularly in resource-constrained environments like South Korea, where strategic decisions about market entry timing are critical for maintaining competitiveness. Ownership concentration has been shown to enable faster market entry, suggesting that firms with concentrated ownership structures benefit from streamlined decision-making processes that allow them to respond more quickly to market opportunities. For managers, this highlights the importance of fostering alignment among key stakeholders to reduce decision-making delays, even in firms with more dispersed ownership structures. By emulating the agility observed in firms with concentrated ownership, managers can better position their companies to capitalize on emerging opportunities.

Furthermore, the moderating effect of CEO’s education and experience on the relationship between ownership concentration and market entry speed adds depth to our understanding of this relationship. The interaction suggests that the influence of ownership concentration on market entry speed varies depending on the education level and tenure. Long-tenured CEOs of the company alongside those with concentrated ownership have more resources available for rapid market entry compared to firms with short-tenured CEOs. This finding underscores the importance of considering contextual factors such as CEO’s experience when examining the impact of ownership concentration on strategic behaviors.

The factor of CEO’s education with two distinct features of the level of education and school type helps us to understand a more complicated connection. Based on the results, even though firms with CEOs who obtained higher levels of education show faster market entry we did not find any significant proof of the importance of the prestige of the alma mater where the degree was obtained. While attending a prestigious university can offer certain advantages, such as access to renowned faculty, huge alumni networks, and a reputation for academic excellence, its significance in various aspects of life and career success can be debated. University prestige is just one factor among many that contribute to a CEO’s success. Factors such as skills, experiences, work ethic, networking abilities, and personality traits also play significant roles in career advancement. In industries such as pharmaceuticals for CEO’s entrepreneurial, practical skills and real-world experience may be of greater significance than academic credentials.

Despite the practical insights provided by the results of this study, several limitations of it should be acknowledged. First, the study may be limited by the characteristics of the sample used. While efforts were made to obtain a representative sample for the study, future research with larger and more diverse in case of industry samples could enhance the robustness of the results.

Second, for this study, the measure of market entry speed may not fully capture the complexities of this construct. Different measures could yield different results, impacting the interpretation and generalizability of findings. Exploring alternative measures and conducting sensitivity analyses could provide further insights into the robustness of the results.

Lastly, the study’s findings may be influenced by contextual factors specific to the period under investigation. For example, changes in market conditions, or specific technological advancements could affect the relationships examined.

Footnotes

Ethical Considerations

Ethical approval was not required for this study as it involved the analysis of publicly available secondary data. The data were anonymized, and no identifying information was used in the analysis.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data for the analysis were derived from the following resources available in the public domain:

1. The Ministry of Food and Drug Safety official website

2. Repository of Korea’s Corporate Filings official website.