Abstract

This research aims to investigate the relationship between ownership concentration and earnings management (EM) practices in China, focusing on the highly debated role of ESG performance as a moderator. Using data from 36,569 firm-year observations of A-share listed firms in China from 2010 through 2023, we observe a positive link where more concentrated ownership corresponds to higher levels of EM. Crucially, high ESG performance markedly weakens this positive link, suggesting it serves as a substantive governance mechanism rather than an opportunistic tool. Furthermore, our mechanism analysis reveals that this relationship is channeled through the exacerbation of Type II agency costs. The principal findings of our research remain robust following various tests designed to address endogeneity. Overall, this evidence demonstrates that, in the unique institutional setting of China, ESG performance acts as a substantive governance mechanism that effectively mitigates the agency problems associated with highly concentrated ownership.

Introduction

High ownership concentration is a defining characteristic of corporate governance in most emerging markets, China being a prime example. This structure fundamentally alters the nature of the primary agency conflict. It shifts the concern from the typical Type I problem to the more serious Type II agency conflict. The latter is defined by conflicts between majority, or controlling, shareholders and minority shareholders (Tran & Dang, 2021). Moreover, where investor protection is insufficient, concentrated ownership provides controlling shareholders with both the motivation and the means to conduct opportunistic earnings management (EM; Al-Begali & Phua, 2023). Therefore, investigating the factors that both enable and restrict EM is crucial for maintaining the credibility of the market. Given China’s capital market features prevalent concentrated ownership alongside a fast, policy-led movement toward sustainability, grasping this particular dynamic holds paramount importance for all market participants.

Although the association between ownership structure and EM is well-known, the function of Environmental, Social, and Governance (ESG) performance introduces a critical point of uncertainty. We need to determine if ESG operates as a genuine mechanism for better governance or as a tool for opportunistic manipulation. One line of reasoning suggests that strong ESG performance improves both corporate transparency and monitoring. Consequently, this weakens the controlling shareholders’ capacity to engage in EM (Kolsi et al., 2023). In contrast, another perspective posits that managers might strategically deploy ESG to obscure self-interested actions. This would ultimately strengthen the connection between ownership concentration and EM (Y. Lu et al., 2024). Addressing this tension, termed the “sustainable vs. opportunistic” debate, is a primary motivation for our current research.

The precise channels that propagate the relationship between ownership structure and EM have not been extensively researched. Existing work generally examines broader monitoring avenues, such as how efficient internal governance limits managerial opportunism (Saona et al., 2020). A significant void exists in the literature concerning the micro-level processes through which Type II agency conflicts materialize as EM. Our primary research aim is to investigate whether ESG performance serves as a substantive governance mechanism that moderates the association between ownership concentration and EM. To provide a solid theoretical foundation for this inquiry, our study also examines the underlying agency cost channels through which ownership concentration is linked to EM.

Using data from 36,569 observations of A-share listed companies in China between 2010 and 2023, the paper arrives at several key empirical results. First, the data confirms that increased ownership concentration is a positive predictor of EM. Second, strong ESG performance is found to significantly moderate this effect, performing as an effective governance tool. Thirdly, our mechanism tests confirm that this relationship operates through agency cost channels: higher ownership concentration is associated with increased Type II agency costs but lower Type I agency costs. Finally, for firms under strong external scrutiny, such as SOEs or those audited by the Big Four, the significance of ownership concentration tends to diminish. A series of robustness tests confirms that these core findings are reliable.

This study contributes to the academic conversation in three main areas. Firstly, we offer our perspective on the ongoing discussion regarding the role of ESG within corporate governance. Our evidence indicates that, in China, ESG is a substantive tool for governance, not one for opportunistic use. Secondly, our work reveals that the connection between ownership structure and EM operates through the channel of Type II agency costs, thereby providing a clear theoretical underpinning for why a governance mechanism like ESG is needed to attenuate the opportunistic behaviors associated with high ownership concentration. Thirdly, a more detailed analysis shows that external supervision from bodies like regulators, auditors, and the state plays a crucial role in lessening agency problems.

Literature Review and Hypotheses Development

Nexus Between Ownership Concentration and Earnings Management

The primary corporate governance conflict in emerging economies like China is often the Type II agency problem, rather than the Type I problem seen between managers and dispersed owners. This second type deals with disagreements between those who control the company and the minority owners (Tran & Dang, 2021). If investor safeguards are weak, owning a large block of shares gives controlling parties the power and the motive to engage in self-serving behavior. They use EM to maximize private benefits, causing harm to minority investors (Al-Begali & Phua, 2023). Consistent with this, J. Fan et al. (2023) find that higher ownership concentration in listed firms in China significantly reduces accounting information consistency. Dominant shareholders may manipulate accounting policies for private gain, thereby undermining the stability and comparability of financial reporting.

While the expropriation effect primarily explains this positive relationship, the academic literature reveals complex, sometimes contrasting results, often stemming from the alignment hypothesis. For instance, high ownership concentration is sometimes posited to serve as an effective internal governance tool for overseeing managerial opportunism (Saona et al., 2020). Furthermore, an increase in manager shareholding typically aligns their interests with shareholders, potentially reducing the issue of agency conflicts (Dong et al., 2020). Nevertheless, internal monitoring can be restricted in specific scenarios. For this reason, external governance becomes very critical. Some data point to strong external oversight limiting self-interested actions, even when Type II conflicts are clear (Ali et al., 2024).

In addition, some studies find a non-linear connection, such as one forming an inverted U-shape. The expropriation effect might dominate when concentration is moderate, but it could weaken at very high levels due to stronger monitoring or alignment incentives (Yang et al., 2022). Despite these varied findings, the Chinese capital market is marked by poor investor safeguards, considerable information asymmetry, and imperfect corporate governance practices (Dong et al., 2020). In this weak institutional setting, concentrated ownership gives major shareholders strong reasons to focus on boosting their personal gains (Ali et al., 2024).

Thus, rooted in Type II agency theory, this research proposes this hypothesis:

Moderating Role of ESG Performance

While high ownership concentration can result in opportunistic EM, the precise role of ESG performance in this dynamic is a subject of theoretical disagreement. It is not yet established whether ESG acts to weaken or strengthen this link. Thus, we will put forward competing hypotheses to address the moderating effect of ESG.

On one hand, according to stakeholder theory, firms should prioritize maximizing the interests of all investors (Gao & Liu, 2023). Robust ESG performance enhances corporate transparency and the quality of information. This mitigates information asymmetry; for instance, Bilyay-Erdogan et al. (2024) indicate that firms with higher ESG performance have reduced bid-ask spreads and broader analyst coverage. Moreover, this increased transparency, along with stronger monitoring facilitated by stakeholder engagement, restricts the capacity of controlling shareholders to mask their opportunistic conduct (Kolsi et al., 2023). A further point is that adhering to high ESG standards is often indicative of greater managerial ethical awareness. As a result, the temptation to use unethical methods, including EM, tends to decrease (Shang & Chi, 2023). In companies with clear ESG strengths, the connection showing that more concentrated ownership leads to more EM is likely to be softer.

On the other hand, some findings suggest that a strong ESG profile can be a strategic form of deception. If Type II agency conflicts are significant, managers could use ESG investments mainly to build legitimacy and gain stakeholder trust (Kolsi et al., 2023). This positive image allows them to hide opportunistic behaviors, such as EM, and their negative effects. This reduces both public and investor oversight (Z. Lu et al., 2024). Ultimately, for firms with concentrated ownership, a strong ESG score might reinforce the positive association between ownership concentration and EM.

Because the theories conflict, our hypotheses are as follows:

Research Design

Sample Selection

Our research uses a sample of A-share listed companies in China from 2010 to 2023. We gathered data for ownership concentration and all control variables from the China Stock Market and Accounting Research (CSMAR) database. In contrast, we sourced the ESG performance data from the China Research Data Services (CNRDS) database.

To create the final sample, we applied several screening rules. First, mirroring prior studies (Lai & Zhang, 2022), we removed financial and insurance firms. Their business models differ significantly from others. Second, we excluded firms designated with Special Treatment (ST) status. Finally, to lessen the impact of extreme values on our statistical estimations, all continuous variables were winsorized at the 1st and 99th percentiles. After this process, the final sample comprises 36,569 firm-year observations.

Variables Identification

Dependent Variable

This paper centers on earnings management (EM) as its dependent variable. The analytical approach taken is the cross-sectional accruals model, as put forth by Ball and Shivakumar (2008). This approach yields several key benefits. First, it diminishes the selection bias inherent in time-series data and bolsters the accuracy of EM detection. Second, by incorporating the non-linear interplay between accruals and cash flows, this model addresses asymmetric timeliness, thereby refining earlier models (Ball & Shivakumar, 2008). Third, the cross-sectional design provides adequate statistical power, which is especially beneficial for Chinese enterprises with shorter track records (Cui et al., 2021).

Total accruals are represented by Accruals, while CF indicates operational cash flows. To lessen the impact of size, all variables are adjusted using average total assets. The indicator variable

Independent Variable

This research uses ownership concentration (OC) as its independent variable. We measure OC by the percentage of shares held by the top 5 largest shareholders (Cao et al., 2022). This metric shows the level of ownership concentration in a firm.

Moderating Variable

Following Q. Li et al. (2024), this research uses ESG rating data from the China Research Data Services (CNRDS) database to measure the moderating variable, corporate ESG performance. The CNRDS database is selected because it integrates international disclosure standards, including GRI and SASB, while also considering the specific policy context in China, making it highly suitable for this research (H. Wang & Liu, 2025). A higher score on this index signifies better corporate ESG performance. Table 1 offers the measurement methods of variables in the paper.

Variable Definitions: This Table Provides Definitions and Measurement Methods for the Variables in the Study.

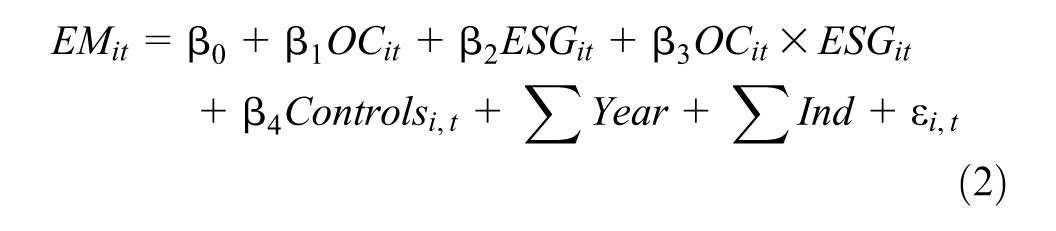

Regression Model

To investigate the link between ownership concentration and EM, this study develops two models to evaluate the direct impact and the moderating role of ESG. The models are delineated as follows:

Equation 1 primarily investigates the effect of ownership concentration on the EM of listed firms in China.

Where

The analysis then focuses on the moderating effect of ESG performance on the association between ownership concentration and EM. ESG performance (

Analysis of Empirical Results

Descriptive Statistics

Table 2 shows the descriptive statistics. The mean of the dependent variable, EM, is 7.216, with a standard deviation of 8.469. This variation shows the diverse EM practices across the sample companies. The finding emphasizes the need to study factors that influence EM. Ownership concentration (OC) averages 53.2%, with a 15.4% standard deviation. This reflects the typical high ownership concentration of Chinese listed companies. ESG performance also shows considerable variability. Its mean is 27.552, and its standard deviation is 10.983. These figures highlight significant differences in ESG ratings among Chinese firms.

Descriptive Statistics: This Table Presents the Descriptive Statistics for all Variables in the Study, Based On a Sample of 36,569 Firm-Year Observations from 2010 to 2023.

Correlation Analysis

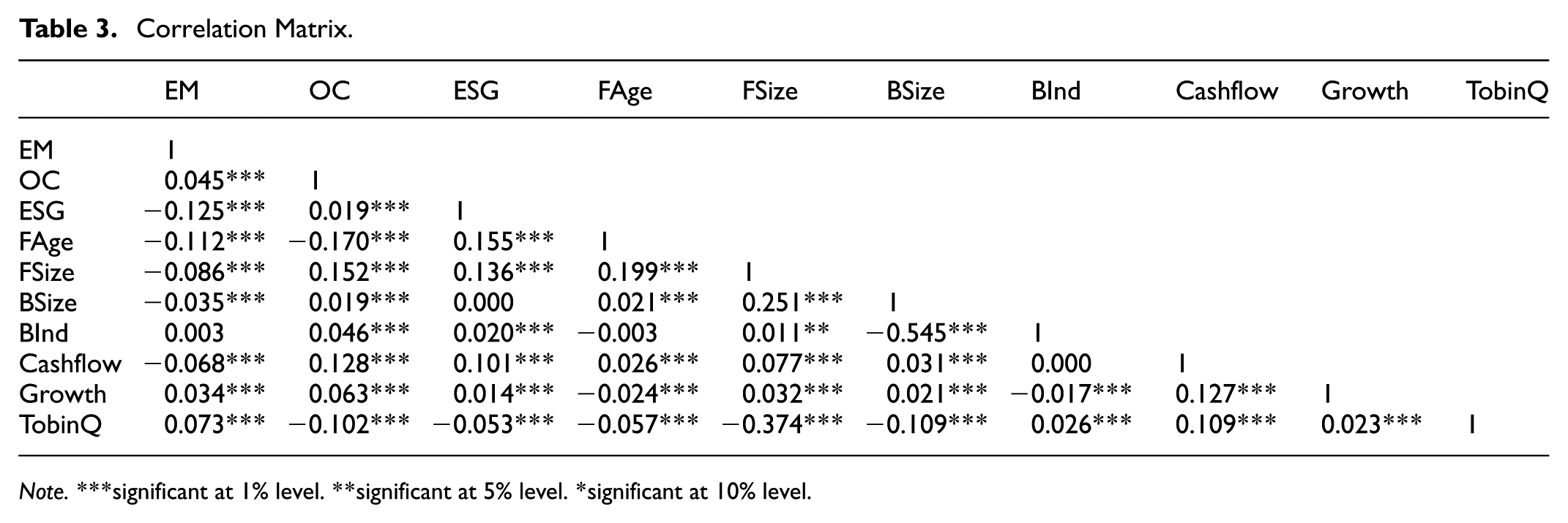

This study checked for potential multicollinearity in the model. We calculated the correlation coefficients between variables. The Pearson correlation coefficients are shown in Table 3. The coefficient between board size (BSize) and board independence (BInd) is −0.545. This statistically significant negative correlation is evident at the 1% level. Thus, board size and board independence are significantly negatively related. However, all other pairwise correlation coefficients have absolute values under .5. This indicates that the empirical model lacks a significant multicollinearity problem. Additionally, the average Variance Inflation Factor (VIF) is 1.21, and the maximum VIF is 1.59. These values also verify the absence of multicollinearity in the model.

Correlation Matrix.

Note.***significant at 1% level. **significant at 5% level. *significant at 10% level.

Regression Analysis

Table 4 shows the panel regression analysis results. Column 4′s findings support

Baseline Model Results.

Note.t statistics in parentheses. *** significant at 1% level. **significant at 5% level. *significant at 10% level.

Concerning the control variables in Column 4, firm size (FSize) and board size (BSize) are negatively related to EM. This supports earlier work suggesting that larger firms and boards better reduce EM. In contrast, Duality and firm growth (Growth) positively correlate with EM. Our findings suggest that firms having a CEO-chairman structure or high growth potential are more likely to manipulate earnings. Lastly, a negative association between cash flow and earnings manipulation means that firms with healthier cash flows require less EM.

The Moderating Role of ESG Performance

This study examines ESG performance as a moderating factor. Column 2 in Table 5 details how ESG affects the link between ownership concentration and EM. The column displays a significant negative interaction effect for OC × ESG at the 10% level, supporting

Moderating Effect Results.

Note. t statistics in parentheses. ***significant at 1% level. **significant at 5% level. *significant at 10% level.

p < .10.**p < .05. ***p < .01.

Robustness Tests

The following methods are employed in this research to verify the robustness of the results:

Propensity Score Matching

Propensity score matching (PSM) is applied to minimize biases by pairing the sample with a group that shares similar characteristics. To prevent specific firm attributes from distorting the results, PSM was implemented to test our hypothesis. We divided the sample at the OC median, as suggested by (Atif & Ali, 2021). Those above the median formed the experimental group, and those below comprised the control group. To ensure the treatment and control groups were equivalent, this study employed the 1:1 nearest neighbor matching method with control variables serving as covariates. Our balancing tests confirm that the feature variables are not significantly different between the two groups of firms once they were matched. Table 6 shows the regression outcomes for the matched sample. The OC coefficient stays positive and is statistically significant. The significance level is 1%. This result verifies our initial finding. Therefore, our primary finding is confirmed: higher ownership concentration is associated with greater EM.

Regression Results After Matching.

Note. t statistics in parentheses. ***significant at 1% level. **significant at 5% level. *significant at 10% level.

Instrumental Variable Method

To manage potential endogeneity, such as reverse causality, we applied two-stage least squares (2SLS). This research uses the 1-year lagged ownership concentration (OC) of the largest shareholder as an instrumental variable (IV). A firm’s ownership structure is typically stable and persistent. Therefore, last year’s concentration is a strong predictor of the current year’s concentration, satisfying the relevance condition. This IV should also meet the exclusion restriction. It seems improbable that the prior year’s ownership structure directly affects current-period EM, other than through its influence on the current ownership structure.

Table 7 displays the outcomes from the instrumental variable (IV) estimation. Column 1 reports the first-stage findings. The IV’s coefficient is .711 and is statistically significant at the 1% level, confirming the relevance of our instrument. The first-stage F-statistic is 4,799.84. This value is well above the conventional threshold of 10, there is less worry regarding instrument weakness. The second-stage outcomes are revealed in column 2. Controlling for endogeneity did not change the results. The ownership concentration coefficient remained positive and statistically significant at the 1% level. This supports the initial conclusion. The positive connection between ownership concentration and EM is confirmed.

IV Estimation.

Note. t statistics in parentheses. ***significant at 1% level. **significant at 5% level. *significant at 10% level.

Heckman’s Two-Stage Regression

While this study used PSM to address observed sample selection bias, unobserved factors might still affect the connection between ownership concentration (OC) and EM. Following (Mingqiang et al., 2024), we applied Heckman’s two-stage estimation method. This choice helped us minimize the issue of extra self-selection bias. The first stage involved a probit regression where if_OC is a dummy variable indicating whether OC exceeded the sample median. We included m_OC, the average ownership concentration of peer firms in the same industry and year, as an exclusion restriction. The rationale is that industry-wide ownership trends can influence a firm’s ownership structure, yet this peer-level average does not directly impact an individual firm’s EM practices.

A significant positive relationship exists between OC and a high concentration of firm ownership, as seen in Table 8, Column 1. Therefore, m_OC is confirmed as a sound exclusion restriction. In the second stage, we added the inverse Mills ratio (IMR), derived from the first-stage probit estimation, to the EM regression. This corrected for possible selection bias. Column 2 indicates that OC remained significantly positive after IMR control. The IMR term was significant at the 1% level. This outcome confirms sample selection bias was an issue. Thus, applying the correction was necessary. The main conclusion’s robustness is confirmed: the positive association between ownership concentration and EM persists after addressing endogeneity concerns related to sample selection.

Heckman’s Two-Stage Correction.

Note. Column 1 presents the first-stage probit model, and Column 2 displays the second-stage regression outcomes. t statistics in parentheses. ***significant at 1% level. **significant at 5% level. *significant at 10% level.

Alternative Variable Definitions

To confirm the reliability of the empirical analysis, this study uses alternative variable measurements. The outcomes of these regression analyses are presented in Table 9. For the dependent variable, we replace the original earnings management proxy (EM) with an alternative measure, EM2, calculated as the absolute value of abnormal cash flows, following Al-Absy (2023). We replaced the initial ownership concentration measure for the independent variable with OC2. OC2 is measured as the total shareholding percentage held by the 10 largest shareholders.

Replace Key Variables.

Note. t statistics in parentheses. ***significant at 1% level. **significant at 5% level. *significant at 10% level.

The findings reported in Table 9 align with our main analysis. In column 3, the coefficient for the alternative ownership concentration measure (OC2) is significantly positive, supporting

Excluding Period-Specific Samples

The COVID-19 pandemic introduced substantial shifts in the production and operational aspects of listed companies. These changes may compromise the accuracy of key indicators, potentially leading to bias within the study sample (Zhang et al., 2023). We handled this concern by excluding data covering the years 2020 and 2021. Following this exclusion, we replicated the main regression analyses. Table 10 presents the results, which align with our main conclusions. Column 1 demonstrates that the ownership concentration (OC) coefficient remains significantly positive at the 1% level. Furthermore, Column 2 confirms the interaction term (OC × ESG) has a statistically significant negative effect at the 10% level. These results demonstrate that the core conclusions of this study are robust after controlling for the potential effects of the pandemic.

Excluding Period-Specific Samples.

Note. t statistics in parentheses. ***significant at 1% level. **significant at 5% level. *significant at 10% level.

Further Analysis

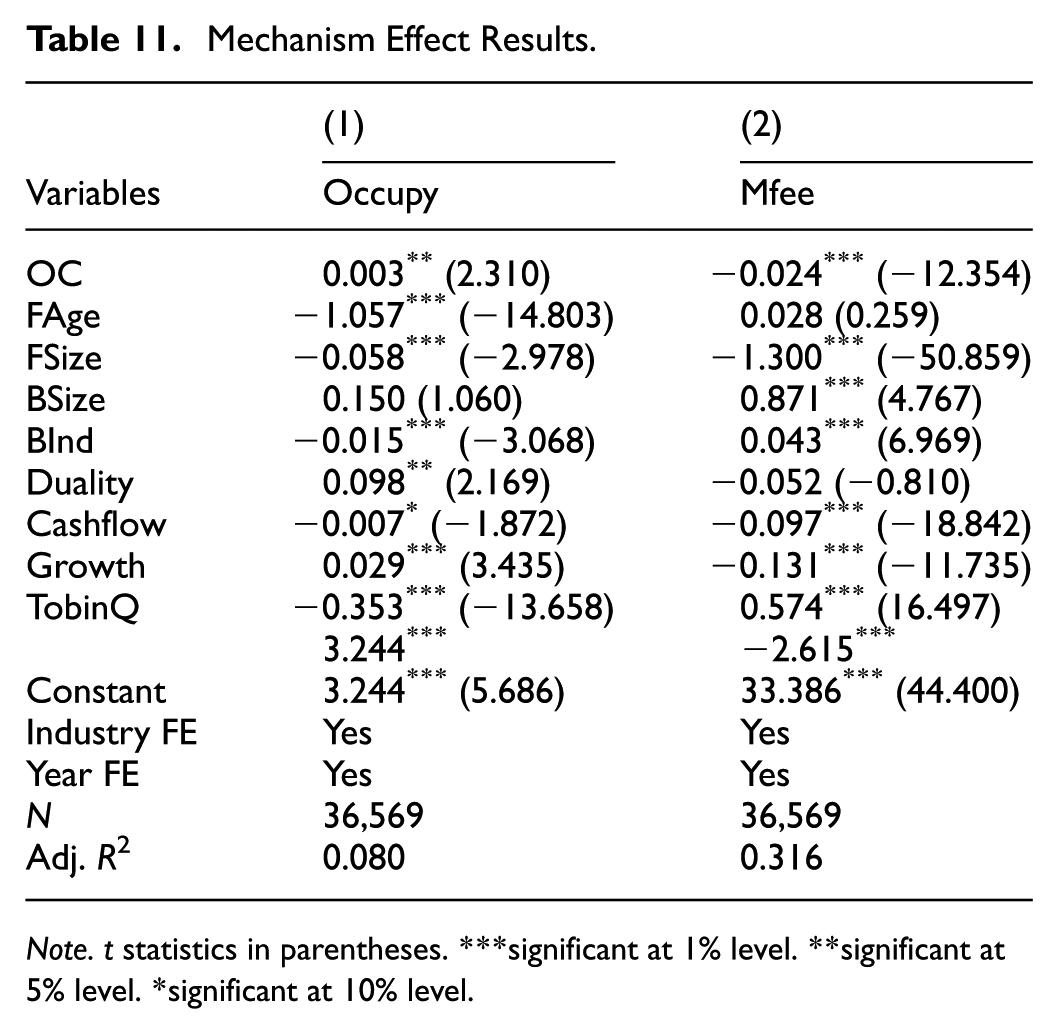

Mechanism Analysis

To provide a theoretical foundation for ESG’s moderating role, it is important to understand why ownership concentration leads to EM. We explore this by examining the channel of agency costs. Agency theory distinguishes between two main conflicts: the Type I conflict involving managers versus shareholders, and the Type II conflict between shareholders who have control and those who have minority stakes.

We use Occupy to capture Type II agency costs. Occupy is simply the proportion of other receivables out of total assets. This metric often serves as a proxy for major shareholders occupying fund assets in China (S. Fan et al., 2023). We measure Type I agency costs using Mfee, the management expense ratio (He & Sheng, 2025).

Table 11 reports our findings. The results in Column 1 show that ownership concentration (OC) has a significant positive effect on Type II agency costs (Occupy). This suggests that higher ownership concentration results in more resource expropriation by dominant shareholders. Prior studies show that higher Type II agency costs lead to more EM, as firms may try to conceal such expropriation (Zhou & Wei, 2025). Therefore, Type II agency costs act as a key channel linking OC to EM.

Mechanism Effect Results.

Note. t statistics in parentheses. ***significant at 1% level. **significant at 5% level. *significant at 10% level.

Furthermore, Column 2 demonstrates that as OC increases, Type I agency costs (Mfee) significantly decrease. This finding supports the alignment hypothesis. Under this hypothesis, concentrated owners possess stronger incentives to supervise managers and manage administrative costs, which ultimately lowers Type I agency problems.

Combining these results clarifies the agency conflict in firms with high ownership concentration. Concentrated ownership may lower Type I agency costs, yet it greatly worsens Type II agency problems. The resulting higher Type II costs offer a direct motivation for engaging in EM. This result supports our study’s main idea and points to the need for a governance tool, like good ESG performance, to lessen this particular problem.

Heterogeneity Analysis

This analysis addresses the question of whether the association between ownership concentration and EM is moderated by distinct regulatory and monitoring environments. Institutional and regulatory oversight can critically influence corporate behavior. We investigate this by focusing on contexts with stronger constraints. For instance, state-owned enterprises (SOEs) often have governance advantages and increased oversight (B. Li et al., 2022). In a similar vein, industries that cause significant pollution are subject to more stringent regulations (R. Wang et al., 2018). Moreover, when Big Four accounting firms audit companies, those firms benefit from better audit quality and closer examination (Lento & Yeung, 2025). We therefore divide the sample based on SOE status, industry pollution levels, and auditor type to test for heterogeneity.

The outcomes are reported in Table 12. Columns 1 and 2 compare SOEs and non-SOEs. For SOEs, the positive link between ownership concentration and EM is notably attenuated. This outcome suggests that the enhanced governmental scrutiny and potential political ramifications faced by SOEs effectively restrict opportunistic conduct by major shareholders.

Heterogeneity Analyzes.

Note. t statistics in parentheses. ***significant at 1% level. **significant at 5% level. *significant at 10% level.

Columns 3 and 4 similarly explore this effect in highly polluting industries. For these firms, the positive link between the concentration of ownership and EM is not as strong. This weaker effect points to environmental regulations and public visibility in these areas acting as a check on behavior. This outside pressure helps prevent concentrated owners from carrying out EM.

Finally, Columns 5 and 6 reveal the most striking difference. The positive association between ownership concentration and EM becomes insignificant for firms audited by the Big Four. Conversely, the impact remains substantial and statistically significant for companies not audited by a Big Four firm. This result underscores the essential function of high-quality external audits. The close examination provided by top-tier auditors seems to effectively limit controlling shareholders’ opportunities to manipulate earnings.

Overall, these results suggest that strong external monitoring can buffer the harmful effects of ownership concentration on earnings quality. This monitoring can come from state ownership, stringent industry regulations, or high-quality external audits.

Conclusion

This paper investigated the critical question of whether ESG performance serves as a sustainable or opportunistic tool in mitigating the earnings management (EM) problems arising from concentrated ownership in China. Our results confirm that higher ownership concentration leads to greater EM. More importantly, we find that strong ESG performance significantly weakens this positive relationship. This is our primary finding and contributes significant evidence to the “sustainable vs. opportunistic” debate. Our results suggest that ESG acts as a genuine governance mechanism in China by increasing the costs of opportunistic behavior for controlling shareholders, thereby effectively constraining their actions.

Our mechanism analysis clarifies the theoretical underpinnings of this relationship. We provide evidence showing that concentrated ownership exacerbates Type II agency costs, which provides a direct incentive for EM. Crucially, our heterogeneity tests reveal that the influence of ownership concentration is not uniform. The effect is much less pronounced in firms benefiting from strong external monitoring. The firms examined here are state-owned firms, companies in highly polluting industries, and those that utilize the auditing services of the Big Four.

This investigation yields several key contributions. First, it offers concrete empirical data detailing the role of ESG in markets with prevalent Type II agency problems. This supports the belief that ESG functions as a mechanism for sustainable governance. Second, we find that Type II agency costs serve as a central link. This work strengthens the theory connecting ownership structure and opportunistic behavior. Consequently, this explains the importance of ESG as an external control. Third, our heterogeneity analysis further extends this by showing that other forms of strong external monitoring can also serve a similar constraining function. Our outcomes have essential practical implications for both policymakers and investors. For policymakers, improving ESG disclosure and performance can be an added governance mechanism for safeguarding minority shareholders. For investors, our findings suggest that high ESG performance can be used as a reliable indicator of lower agency risk, particularly in firms with high ownership concentration where such risks are most pronounced.

This paper has several limitations that open avenues for future research. Our main focus was restricted to ownership concentration. Future work should consider expanding the scope to other ownership characteristics, for example, identifying the largest shareholder. Another point is that our analysis used an aggregated ESG score. Subsequent studies could separate ESG into the environmental, social, and governance categories to determine which component is most influential. Finally, other underlying mechanisms, like managerial entrenchment or political connections, remain open for investigation.

Footnotes

Acknowledgements

We are grateful to all the people involved in the study for their active cooperation.

Author Note

Ethical Considerations

Not applied. This study does not involve any animal or human participants and therefore does not require an ethics statement.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: PhD Start-up Foundation of Guangdong University of Science and Technology GKY-2025BSQDW-129.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.*