Abstract

This study investigates the relationship between capital structure and firm performance, concentrating on the moderating influence of monetary policy by means of bank credit. By using a sample of 49 real estate firms listed on the Ho Chi Minh City Stock Exchange between 2007 and 2021 and applied some econometric models such as ordinary least squares, fixed-effects, random effects estimation, and two-step system GMM, this research pioneers the concept of a minimum debt threshold or lower-bound debt threshold, addressing theoretical and empirical gaps in the evaluation of the effects of maintaining debt levels below this threshold, in contrast to traditional studies that primarily emphasize the optimal debt level or maximum debt threshold. Moreover, the study highlights the semi-moderating impact of bank credit on the threshold, emphasizing the important interaction between monetary policy and capital structure decisions. Specifically, this study finds that debt financing below the minimum threshold has a negative impact on performance, encouraging firms to seek alternative capital solutions or increase leverage above the minimum threshold, which is defined for each industry in accordance with the context of individual economies. The research offers significant insights for companies in capital budgeting and adjusting to variations in credit policies, particularly within Vietnamese real estate sector, which is highly dependent on debt financing and sensitive to monetary changes.

Introduction

In developing economies, financial leverage is essential for stimulating growth, particularly in capital-intensive industries like real estate. The Vietnamese real estate sector exemplifies a pronounced reliance on borrowed capital and a substantial vulnerability to fluctuations in monetary policy. Although prior studies have predominantly examined the risks associated with exceeding debt leverage beyond the maximum threshold, the adverse effects of conserving debt levels below the minimum threshold remain insufficiently explored. Inadequate leverage level hinders businesses from exploiting potential advantages of debt, such as tax reduction, creditor governance oversight, and capital cost optimization. These advantages have already been acknowledged in conventional capital structure theories. This deficiency impedes the advancement of capital structure theory and constrains its practical implementation in corporate financial decision-making.

Removing perfect market assumptions from the classical proposition on the irrelevance of capital structure (Modigliani & Miller, 1958), one can hardly argue that the firm’s financing choices have no influence on its performance. According to Margaritis and Psillaki (2007), the correlation between capital structure and firm performance depends on the level of leverage and the relationship is positive only when the increased benefit from debt leverage exceeds the marginal cost of debt financing (Hutchinson, 1995), which suggests a nonlinear relationship. The positive relationship between Capital structure and firm performance is indicated mostly in the “trade-off theory” of Myers (2001) and “agency cost theory” of Jensen and Meckling (1976). While trade-off theory shows that the use of higher debt gives firms a larger tax shield, as well as reduces cost of borrowings and renegotiations (Chemmanur & Fulghieri, 1994; Rajan & Winton, 1995), hence higher debt ratio optimizes tax expenses and cost of capital. In other words, it is implied that underuse of debt financing will not suffice to optimize profit goals.

Agency cost theory suggests that the use of debt, accompanied by closer supervision of lenders can have a positive effect on firm performance. Specifically, Diamond (1991) and Myers (1977) proposed a more effective monitoring feature provided by bank loans on firm management, hence eliminating the problems of adverse selection and moral hazard in accordance with the level of leverage. In detail, Jensen (1986) demonstrated that managers of the firm, with high levels of debt, are motivated to invest in intense profitable projects in order to generate cash flows for interest and capital payment, hence reducing shareholder-manager conflicts. Thus, previous studies have neglected to acknowledge that a minimal debt level does not necessarily ensure a more efficient monitoring system, thereby failing to eradicate the issues of adverse selection and moral hazard. Notably, recent studies indicate that maintaining an appropriate debt threshold is essential for optimizing firm performance. Excessive and insufficient debt financing can both have detrimental effects. Excessive financial flexibility is beneficial primarily during crises; however, it frequently results in inefficient expenditure (Nguyen, 2024b).

In contrast to conventional research, our study contributes to the literature by emphasizing the minimum debt level. Moreover, contemporary research has shifted its focus to the examination of financial flexibility. By contrasting actual debt levels with projected debt levels, the financial flexibility approach offers superior management insights. However, this method encounters practical difficulties, particularly in accurately assessing debt levels, leading to complexities in identifying unused borrowing capacity. On that basis, this study proposes a more practical approach by integrating the concept of a minimum debt threshold, thereby improving the traditional theoretical framework for optimizing debt leverage. This method is particularly appropriate when examining specific industries and economic contexts. Thus, the investigation concentrates on Vietnam’s real estate sector, emphasizing the necessity of either reducing or increasing debt levels in the event that the actual debt falls below the minimum threshold. The study fills an important gap in understanding the effective use of debt. Specifically, it addresses a significant gap in the literature on the effective use of debt, particularly in developing economies, where businesses often face high borrowing costs and the complexities of volatile monetary policies (Tran & Nguyen, 2025).

In addition to being a pioneering study in determining the minimum debt threshold, the study also examines the impact of bank credit, a critical element of monetary policy that directly affects the cost and accessibility of debt, on the lower bound threshold at which businesses should confidently increase their debt levels. On that basis, this study poses the research questions including “How does identifying a minimum debt threshold influence the nonlinear relationship between capital structure and corporate performance in the real estate sector of an emerging economy like Vietnam?” and “What is the role of bank credit in such relationships?.”

The paper is structured as follows: Section 1, introduction, highlights the research context, key concepts, and the novelty of the research. Section 2 shows the literature review provides a theoretical foundation for conceptualizing research hypotheses. The research method is presented in Section 3. Section 4 shows the results and discussion Finally, Section 5, the conclusion, summarizes the research results as well as the implications.

Literature Review and Hypothesis Development

Controversy Relationship Between Capital Structure and Firm Performance

Over the past half-century, there has been a great deal of theoretical and practical research on the relationship between capital structure and firm performance. At the forefront of modern capital structure theory, the M&M theorem I concludes in the absence of taxes and inflation, capital structure has no effect on firm performance as in perfect capital markets the bankruptcy costs do not exist since assets always can be sold at economic value without transaction costs (Modigliani & Miller, 1958). Later, Modigliani and Miller (1963) acknowledged the effect of leverage on firm performance under the effects of taxes and transaction costs (referred to as M&M theorem II). The concept of leverage can be classified into operational leverage and financial leverage. While operational leverage refers to fixed operating expenses, financial leverage describes the cost of fixed debt (Westgaard et al., 2008). This paper examines a firm’s total leverage as the sum of both financial and operating leverage.

From the above two theorems, many theories on this issue have been proposed, supplemented, and perfected. Trade-off theory shows that a higher debt ratio optimizes tax and profit margins, although financial distress and bankruptcy costs increase (Myers, 2001). Jensen and Meckling (1976)and Meckling and Jensen (1976) with the agency cost theory suggest that the use of debt, accompanied by closer supervision of lenders can have a positive effect on performance. On the same page, the efficient risk hypothesis assumes that better-performing firms use more leverage because a firm’s management has a higher incentive to meet its debt obligations in order to avoid bankruptcy and financial distress, hence predicting a positive relationship between performance and leverage (Yeh, 2010). Contradictory to the expected positive relationship of the above theories, the Pecking order theory states that there is a prerogative about actual capital financing, due to information asymmetry, internal capital is often used in advance, followed by loans and finally equity, as the more capital structure based on loans financing, the less expected financial performance as a result of debt financing expenses (Myers & Majluf, 1984).

The inconsistency is also expressed through empirical studies. While the study of El-Sayed Ebaid (2009) shows that there is no correlation between capital structure and firm performance, researches by Antoniou et al. (2008), Margaritis and Psillaki (2007), Nazir et al. (2021), and Brav (2009) show a negative relationship. Others argue the positive effect of debt leverage (Al-Haddad et al., 2024; Hutchinson, 1995). Berger and Bonaccorsi di Patti (2006) argues that high leverage helps to limit agency costs by motivating managers to work for the benefit of shareholders and that debt dependence is a common trend of many profitable businesses. Firms with high debt financing exercise more effective monitoring system, and hence the problems of adverse selection and moral hazard can be eliminated, and renegotiation costs are lightened (Diamond, 1991). Utilizing more debt either decreases the required equity investment or amplifies financial capability (Albuquerque, 2024; Cannaday & Yang, 1996).

Most theories and empirical studies search for an optimal capital structure, which is the maximum leverage point, above which marginal benefits are no longer sufficient to offset the costs of debt financing, hence suggesting a convey relationship between capital structure and firm performance (Ayaz et al., 2021; Khan et al., 2021; Margaritis & Psillaki, 2007; Ronoowah & Seetanah, 2024; Tsuruta, 2017). The firm’s leverage decision involves a tradeoff between the expected advantage of debt and expected leverage-related costs hence leverage need to reach a minimum threshold before marginal benefits begin to offset debt financing costs (Bradley et al., 1984). Distinctively, Ibhagui and Olokoyo (2018) state that the adverse effect of debts on performance diminishes as the business grows. Specifically, Zeitun and Goaied (2022) confirm the existence of a U-shaped relationship between firm performance and current debt.

Overall, although the topic of the relationship between firm performance and capital structure has been extensively researched, it is still controversial and mostly to just only reconfirm the theories regarding debt burden and debt – overhang theory proposed by Myers (1977). Those studies do not adequately control for regulatory effects or, if any, do not clarify the mechanism effect of the moderator. While most aimed at determining the optimal leverage, this study, however, focus on the lower bound of leverage at which under that point, capital structure would injure firm performance and would benefit firm performance from that point forward.

Bank Credit Moderates the Relationship Between Capital Structure and Firm Performance

Levy and Hennessy (2007) argues that there is a systemic variation in funding options adapting to macroeconomic conditions, typically monetary policy. Frank and Goyal (2003) argue that intrinsic factors determine about 30% of differences in Capital structure, while the majority of the remainder comes from external determinants. Specifically, market timing theory suggests when the cost of debt is low, firms prefer debt and prefer external equity otherwise (Baker & Wurgler, 2002). In other words, lower financial constraints and more affordable interest rates due to higher money supply will encourage firms to borrow and vice versa (Huang & Ritter, 2005). Expansionary monetary policy increases the supply of loanable funds available through the banking lending channel, causing interest rates to fall, which leads to an increase in aggregate expenditures on investment and consumption demand, and hence benefits firm financial performance (Millikan, 1938). Research on the real estate sector has reported a relationship with the macroeconomy and monetary policy (Chen et al., 2012). With higher real output and income, as the optimistic economy under monetary expansionary, market demand side is more inclined to purchase real estate and hence the demand for both financial and supply funds for this purpose increases (Guirguis & Trieste, 2020). Besides, according to Friedman’s Modern Quantity Theory of Money, in the context of monetary expansionary, there is a decrease in the need to hold cash, which will increase consumer demand, resulting in higher business performance (Mishkin, 2007).

Ippolito et al. (2018) find evidence that firms with more bank debt are more sensitive to monetary policy shocks as a result of interest rate risk. The changes in monetary policy, specifically bank credit, substantially influence risk-taking behavior and hence firms’ capital structure strategy (N. Berger & F. Udell, 1998). Levy and Hennessy (2007) substantiate the argument by finding evidence of tactical managerial activism, in which financial managers actively substitute equity for debt during economic expansionary, and in contrast during economic contractionary. The strategic adjustment of the distribution between debt and equity in various macroeconomic conditions functions as a form of signaling. During economic contractions, managers intentionally raise their proportion of overall equity holdings, thereby conveying a confidence signal to market participants.

Specifically for the real estate sector, Shen and Yin (2016) argues that macroeconomic conditions or particularly credit supply, besides the demand-side factors in traditional theories, also influence firm’s capital structure and thereby indicates a microeconomic channel of monetary policy on a firm’s capital structure and profitability. Inspired by previous studies on financial management in the real estate sector, but distinct in the context of considering the impact of monetary policy, this study investigates the aspect of financial resources management of real estate companies, where debt financing is considered indispensable. Real estate investors often try to minimize equity investment and maximize borrowed capital as returns of real estate investment were due largely to tax benefits, level of gearing and capital gains. Without debt financing, the benefits might be greatly reduced (Ferreira & Sirmans, 1987). Therefore, it can be seen that the larger the credit supply, the higher the demand for housing products thanks to the impetus from the financial source on the purchasing capacity of real estate investors, which might contribute to the bidding up of property prices thus contributing to higher real estate firm performance (Gau & Wang, 1990).

Regarding the presented theory, monetary policy has an impact on the efficiency of debt use. By considering the change in the relationship between capital structure and firm performance in response to the quantity of money supply. Very few studies demonstrate the mechanism of the influence of capital structure on firm performance regarding the moderating effect of monetary policy, especially regarding real estate sectors. This study contributes to the literature exploring the moderating effect of bank credit on the relationship between capital structure and firm performance, which is expected to be able to explain the nonlinear relationship between capital structure and firm performance as well as being one of the reasonable explanations of the controversial results of previous studies. This study expects that an expansionary monetary policy will lower the cost of debt as well as increase investment and speculative motive of businesses to take advantage of higher consumption demand. Therefore, the lower bound threshold is expected to decrease as a result of larger marginal positive effect of debt and therefore occurs at lower leverage ratio during higher bank credit. Based on these discussions, we propose the hypothesis as follows:

Method

Data

The financial data is taken from the Fiinpro Platform, while macroeconomic data are collected from the International Monetary Fund (IMF). Our sample is real estate firms listed on the Ho Chi Minh City Stock Exchange (HOSE). To guarantee the reliability of the data, the companies taken into consideration for the sample in our study had to have financial statements spanning a minimum of 6 years (Ayalew, 2021; Zeitun & Goaied, 2022). Dropping observations from an unbalanced data set to make it balanced may result in significant efficiency loss (Baltagi & Chang, 1994; Biørn, 2004; Mátyás & Lovrics, 1991). As a result, our unbalanced data consisted of 617 observations for 49 firms over the 2007 to 2021 study period. This article winsorizes the firm-level data at 5% and 95% to reduce the potential impact of extreme outliers. Each variable’s details are displayed in Table 1.

Definitions of the Variables.

Source. Authors’ own collection.

Empirical Model

This study employs numerous explanatory variables in estimating the value of the dependent variables using multiple panel data regression. In order to deal with spatial heterogeneity, authors employ a one-way error component model. We expand the baseline model presented by Quoc Trung (2021) to include curvilinear effects and curvilinear-by-linear interactions to examine the moderating impact of bank credit on the curvilinear relationship between capital structure and firm performance. The new model illustrating how the threshold of the relationship between Capital structure and mean performance reacts to variations in bank credit (Kutner et al., 2005), can be described as follows:

Where

To ensure the robustness and stability of the model, firm performance is measured using three metrics: return on assets (ROA), return on equity (ROE), and return on invested capital (ROIC). ROA and ROE are frequently employed in empirical research on capital structure as the key indicator assessing a company’s operational efficiency (Ayaz et al., 2021; Nguyen, 2023). Meanwhile, ROIC is often prioritized in the assessment of efficient financial capital management (Kumar et al., 2022).

The existence of non-linearity between capital structure and firm performance can be inferred if the null hypothesis of

Data Analysis

Three widely used methods—Pooled OLS, FEM, and REM—are employed in panel data analysis, each with distinct strengths (Nguyen, 2024a; Nguyen & Dang, 2023; Pham et al., 2022). Pooled OLS assumes no differences between entities, treating all data as homogeneous, making it suitable when unobserved factors do not affect independent variables. FEM controls for time-invariant factors that may correlate with independent variables, reducing bias but not estimating fixed variables. In contrast, REM assumes unobserved factors are random and uncorrelated with independent variables, enabling the analysis of both fixed and time-varying variables. However, REM is unsuitable if this assumption is violated. The random effects estimator uses the generalized least squares method to solve the composite error serial correlation problem in the scenario where the unobserved effect

Results

Descriptive Statistics and Correlation Matrix

Table 2 show the summary of the descriptive statistics for all variables. ROA of the real estate company averaged 4.8% during the research period; the highest ROA was 15.1% and the lowest was roughly 0%. For this time period, ROE varied from 0.00% to 36.70% with an average of 11.1%. However, the ROIC values were, respectively, −3.8%, 6.4%, and 24.2% at the minimum, mean, and maximum levels. In terms of sample variation, the standard errors of ROA, ROE, AND ROIC are 4.02%, 10.2%, and 7.4%, respectively. The advantage of using leverage during the observed period is demonstrated by the mean ROE being higher than ROIC and ROA. The potential return rises with an increase in risk, which is consistent with risk-return tradeoff theory. The Capital structure varies significantly and ranges from zero to the highest value, which was 41.7% for TDTA, 31.4% for LDTA, and 24.0% for SDTA, while bank credit has considerable fluctuation in the spectrum of 75.7% to 123.8% with a coefficient of variation of approximately 0.152. The other control variables also change in the observed time span.

Descriptive Statistics.

Source. Author’s calculation.

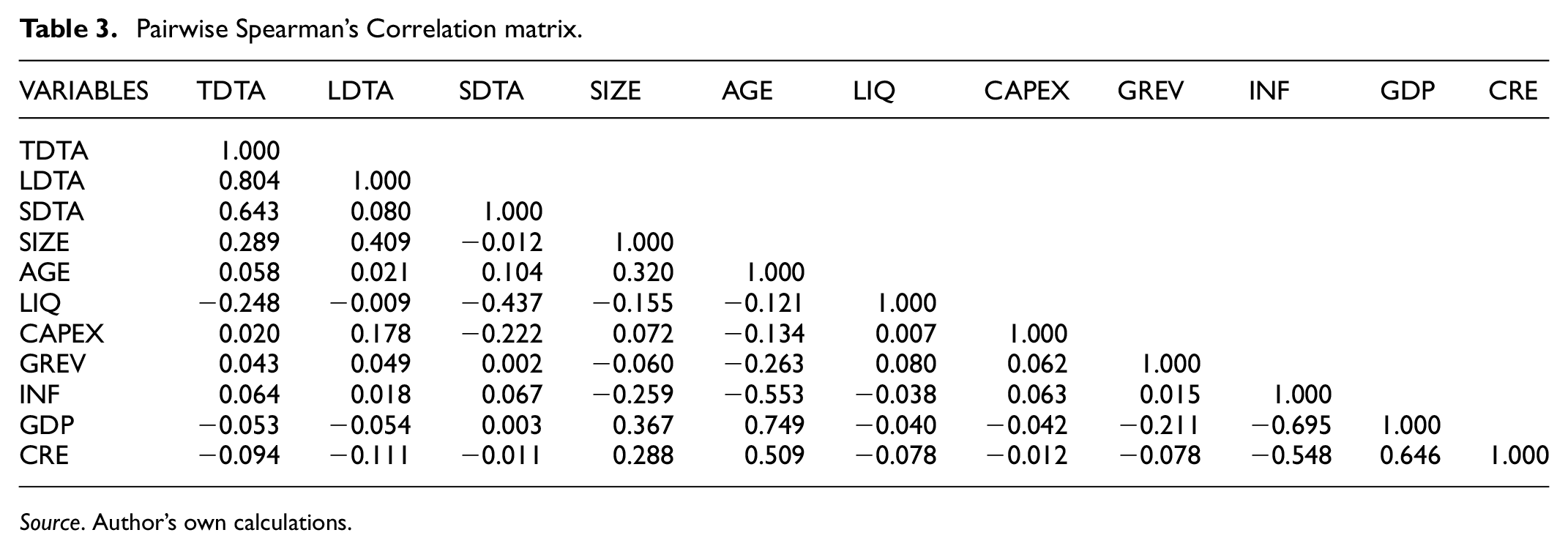

Multicollinearity will arise when models with interaction terms are used, so this problem should be addressed by demeaning the independent (Cohen et al., 2002; Nguyen, 2025). The correlation coefficient and using it for regression, three metrics for capital structure and bank credit will be centered. Spearman’s correlation coefficients range from −1 to +1, indicating the direction and strength of linear relationships. Hence Table 3 shows that the correlation coefficients of all independent variables are all less than 0.8. The correlation coefficients of all independent variables displayed in Table 3, all less than 0.8, suggest it is likely that multicollinearity won’t be a problem.

Pairwise Spearman’s Correlation matrix.

Source. Author’s own calculations.

Regression Results

The results indicate that the residuals of all our models have autocorrelation and heteroskedasticity as evidenced by the statistical significance of key coefficients (e.g., CS and CS2) with low standard errors in all models (e.g., CS: −0.102*** with SE 0.015 in OLS for ROA, −0.072*** with SE 0.019 in FEM, and −0.080*** with SE 0.017 in REM). Therefore, all models employ robust standard errors to enhance the valid and reliable results. Total debt to total assets (TDTA) was used as an independent proxy for the degree of leverage using a variety of estimation techniques, including pooled OLS regression, the FE estimator, and the RE estimator (As displayed in Table 4).

TDTA as a Metric for Capital Structure—Pooled OLS, FEM and REM.

Source. Authors’ own calculations.

Note. Standard error in parentheses.

Significant at the 10% level; **significant at the 5% level; ***significant at the 1% level.

The F-test and Wald test results for all models (e.g., 13.669 for OLS, 9.150 for FEM, and 118.261 for REM in ROA) show that all independent variables are jointly significant at the 1% level, indicating that the chosen independent variables provide an appropriate explanation for variations in the dependent variables, as measured by ROA, ROE, and ROIC.

With regard to the core of our analysis, the pooled OLS outputs show that TDTA has a significant correlation with all profitability variables. The first hypothesis that TDTA has a nonlinear effect on firm performance, specifically curvilinear, is clearly supported by the evidence. The positive sign of the quadratic term indicates an upward curvilinear connection between TDTA and profit, with coefficients of 0.366* for ROA (1% significance) and 1.352* for ROE (1% significance). Given that the range of leverage is non-negative and combined with the linear term’s negative sign, researchers draw the conclusion that this nexus has a threshold.

The estimated coefficient is positive and significant at the 10% level when considered in the context of the interaction between linear TDTA and BC (0.157* for ROA in the pooled OLS model). However, there is a negative coefficient (−0.013) but it is not significant for the interaction between the square of TDTA and bank credit. That reinforces our statement that the amount of bank credit available to the economy determines how firm performance responds to its leverage ratio. Thus, the second hypothesis about the moderating role of level bank credit on the capital structure–performance nexus is accepted. More specifically, a significant covariation between company profit and bank credit at the 1% level demonstrates that bank credit functions as a quasi-moderator.

Moreover, the FE estimator and RE estimator results supported a U-shaped relationship between capital structure and firm performance as well as the first-order impact of bank credit on firm performance. For instance, the coefficient of CS2 under FE for ROE is 0.620 (5% significance), while for RE it is 0.711* (1% significance). However, the sign of first-order interaction between leverage level and amount of credit banks still remains, but it is insignificant. In other words, firm performance will respond to changes in leverage ratio separately from level of bank credit if there is heterogeneity across firms, which will eliminate the moderating role of bank credit. The main findings are stable when the proxy for capital structure is changed.

Using robust standard errors, autocorrelation across time and groupwise heteroscedasticity eliminates the effectiveness of estimators, which reduces the significance of first-order interaction. The FGLS method fixes the issue and produces reliable and valid outcomes, as shown in Table 5. For example, the coefficient for CS remains negative and significant across all metrics of capital structure, such as −0.082* for TDTA with ROA, −0.108* with ROE, and −0.187* with ROIC. Similarly, the quadratic term CS2 shows a positive and significant U-shaped relationship. The interaction term CRE*CS is significant for ROE across TDTA (0.660*) and LDTA (0.698), reinforcing the moderating role of bank credit.

Results From FGLS Estimator.

Source. Authors’ own calculations.

Note. Standard error in parentheses;

Significant at the 10% level; **significant at the 5% level; ***significant at the 1% level.

All models pass the Wald test at the 1% level, indicating that all explanatory variables are jointly significant and that the models adequately account for the data. Researchers’ declarations that capital structure and firm performance have an upward curvilinear nexus and also that bank credit has a quasi-moderating effect on the cutoff point in this connection are supported by the findings of nonlinear static models, demonstrated by the positive and significant quadratic term (CS2) coefficients, such as 0.254* for ROA and 0.888* for ROE with TDTA. Furthermore, bank credit shows a quasi-moderating effect, as indicated by the interaction term CRE*CS, which is significant in some instances.

Nevertheless, in some instances where the metrics for firm performance and capital structure have changed, the conclusion is unsound. Heteroskedasticity, autocorrelation and unobserved effects can both be reduced by using the FGLS method, but the endogenous problem, which results in biased and inconsistent estimators, may still be present. The research uses a two-step robust system GMM dynamic panel data estimation in order to deal with the endogenous problem of a 1-year lag in firm performance. The outcomes of the system GMM are reported in Table 6.

Results From Two-Step System GMM.

Source. Authors’ own calculations.

Note. Standard error in parentheses.

Significant at the 10% level; **significant at the 5% level; ***significant at the 1% level.

The p-values of the Arellano-Bond test for serial correlation (the AR(2) p-values for TDTA and ROA, ROE, and ROIC are .714, .624, and .826, respectively) and the Hansen test of overidentification restriction (.995, .964, and .362, respectively), all under the 10% threshold, confirm that the model does not exhibit overidentification or autocorrelation issues. The rule of thumb proposed by Roodman (2009) is satisfied because the number of instruments in all models (ranging from 16 to 19) is less than the number of firms (equals 49). Therefore, the two-step SGMM estimator produces reliable and unbiased results, and the instrument variables can effectively handle the endogeneity. It continues to strongly support the conclusions about the relationship among bank credit, capital structure, and firm performance even after changing the proxy for capital structure and firm performance.

The study conducted a number of sensitivity analyses to examine the validity of the regression outputs displayed above. The results held even after the capital structure and firm performance proxies were changed, along with the estimation techniques, which included feasible generalized least squares, fixed effects estimator, random effects estimator, and pooled OLS. The study winsorizes firm-level variables at 5% and 95% before starting the regression analysis’s initial steps. The patterns are the same as before when winsorize for the intervals of 10% and 90%. Overall, the research findings support hypotheses H1 and H2.

Discussions

Figure 1 shows that low levels of capital structure are negatively related to firm performance. On the contrary, a high level of Capital structure, above the lower bound threshold specifically, the debt advantages take its role and hence benefit firms with higher performance. Notably, this study also successfully determines the moderating impact of monetary policy on the relationship between capital structure and firm performance, corresponding to high (one standard deviation above the mean) and low (one standard deviation below the mean) bank credit, the lower bound will be shifted to be lower and higher, respectively.

The moderating effect of bank credit on the convex relationship between capital structure and firm performance: (a–c) relationship between TDTA and ROA.

The results are accompanied by the research of Ibhagui and Olokoyo (2018) and Zeitun and Goaied (2022), which clarify the convex relationship between Capital structure and firm performance. This shows that the use of debt has a positive effect on firm performance only when leverage is large enough as suggested by Campello (2006). In other words, a high level of debt not only deducts the cost of borrowing and financial distress but also imposes pressure and incentives on managers to enhance performance. Therefore, low levels of debt negatively affect performance (Diamond, 1991; Scott, 1977). The defined threshold marks the level of debt financing, above which the debt benefits surpass the cost associated with debt. Specifically, Solomon (1963) suggests that the M&M proposition amended to take the tax deductibility of interest into account would postulate that companies ought to be financed 99.9% with pure debt. An agency problem can be managed with an appropriate Capital structure that leverages the role of a loan by a debt policy allowing control from lenders and thereby minimizing agency costs (Hart & Moore, 1994). Jensen (1986) proposes that firms with capital structure with high levels of debt will pressure managers to be motivated to invest in intense profitable projects to generate cash flows for interest and capital payment, hence reducing conflicts between shareholders and managers. Therefore, low levels of debt negatively affect performance due to less pressure and/or incentive for managers to enhance performance (Zeitun & Goaied, 2022). Furthermore, bank loans, which can eliminate the problems of adverse selection and moral hazard with more effective monitoring features (Diamond, 1991; Myers, 1977), reduce costs of borrowing and renegotiation (Chemmanur & Fulghieri, 1994; Rajan & Winton, 1995), and mitigates problems of free cash flow since debt must be repaid to avoid bankruptcy (Jensen, 1986; Jensen & Meckling, 1976).

The economic states modeled in this paper are monetary policy context, with an indicator of bank credit, moderate the relationship between capital structure and firm performance. In the context of monetary expansion, high bank credit with abundant and easily accessible capital and favorable lending rates will further reduce the risk of bankruptcy and the burden of borrowing costs (Warner, 1977). During monetary expansionary, through the bank credit channel, the minimum level of leverage, at which the marginal benefit of using debt can fully offset the marginal cost of debt, will be reduced. Conversely, monetary contractionary reduces investment opportunities, and this in turn reduces corporate performance and increases the risk of insolvency (Judge & Korzhenitskaya, 2012). In addition, limited borrowing capability threatens firms with greater refinancing risk (Diamond, 1991). This implies that the firm will incur a higher cost of debt, which causes the defined threshold to be upward. Therefore, there is a theoretical basis for the research results of this paper to confirm that monetary policy has a moderating effect on the convex relationship between capital structure and firm performance.

Conclusions

Theoretical Contribution

This study meaningfully extends the capital structure strategy literature by providing support for the argument of the convex relationship between capital structure and firm performance being moderated by monetary policy, which upon our latest review, has not been under consideration in any paper, especially in real estate sector. The results strengthen the M&M theory, the agency theory and the risk-shifting hypothesis by determining the minimum threshold from which the impact of capital structure on firm performance is consistent with the views of these theories. Specifically, with sufficient leverage in the view of Campello (2006), debt financing contributes to minimizing agency costs and limiting free cash flow problems, as well as utilizing the benefit of a debt tax shield.

The study challenges earlier approaches to just examining the linear relationship, which are based on a simplified and less sophisticated perspective. Instead of looking for the optimal capital structure, which is the ideal maximum leverage ratio, this study successfully identifies the minimum cut-off point in which a positive impact of capital structure on firm performance, is moderated by bank credit.

Contribution for Practical Implication

Consistent with the initial expectations, there is strong evidence to propose that capital structure has a curvilinear relationship with firm performance. The study reaffirms the control value of macroeconomic factors (including GDP growth and inflation rate), and firm characteristics (including size, liquidity, growth, capital expenditure, and age) on firm performance.

The research results are expected to support businesses in general and the real estate industry planning capital strategies compatible with the monetary condition to allow more effective financial management. Based on the research result, businesses can consider the minimum level of leverage when making capital structure decisions, especially in considering the effect of monetary policy.

At the same time, the Government could consider these findings helpful in monitoring capital market as well as related laws and regulations in the real estate industry and especially monetary policy. The government should consider the ability to amend capital structure strategy by adapting to the changes in monetary policy of the businesses in order to avoid negatively affecting the economic performance.

Limitations and Suggestions for Further Research

Although this study individually considers the real estate industry due to its representative capability of the capital market, the relationship between capital structure and firm performance can be influenced by many factors, hence generalizing the results beyond Vietnam deserves revalidation. Similar to other frontier capital markets, Vietnam is classified as an emerging economy where firms highly depend on debt financing due to limited financial resources (Patnaik et al., 2011). Moreover, the characteristics of the real estate industry use high leverage, long-term capital and vulnerability to exchange rates, hence is highly cyclical. To further confirm the universal validity of this research to other industries will require further research on other industries and in other emerging countries in the region.

Second, although using listed firms helps satisfy the requirements for data accuracy, and ensuring representativeness of the market share, these businesses have the common characteristics of industry leaders, easy access to loans, and high standard corporate governance due to listing standards. Therefore, to further strengthen the practical implication, further research could further consider unlisted real estate firms.

Third, the level of longitudinal variation in our dataset may not be as significantly high, which may prevent us from controlling firm-specific unobservable factors. However, it is reasonable to consider that this study has taken into account all of the listed real estate firms, with the maximum available longitude data. While these numbers may appear unproblematic and maintain the robustness of the model, the possibility that the level of longitudinal variation may not be ideal needs to be acknowledged.

Conclusion

Traditionally, researchers have operated under the implicit assumption that the connections between capital structure and performance follow a linear pattern. While this assumption has been both conceptually and empirically questioned, the outcomes thus far have been inconclusive. More recent findings predominantly lean toward identifying an upward curvilinear relationship when determining the optimal capital structure. The study successfully confirmed the proposed hypotheses and found the moderating effect of monetary policy, specifically bank credit on the curvilinear relationships between capital structure and firm performance, such that higher bank credit is associated with a lower cut-off point. By focusing on Vietnamese real estate firms, the result suggests that high levels of capital structure may be more helpful in maximizing firm performance in high bank credit rather than in low bank credit. Overall, current findings have important theoretical and practical implications for real estate companies. Theoretically, the findings help clarify the nature of the relationships between capital structure and firm performance and show the moderated mechanism of monetary policy (i.e., bank credit). Practically, the findings can help those real estate firm managers enhance the utility of capital structure and support policymakers in monitoring monetary policy.

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is partially funded by Ho Chi Minh City Open University.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.