Abstract

In this research endeavor, we delve into exploring how CSR acts as a moderating force and capital structure assumes a mediating role in shaping the interplay between managerial ability and firm performance. Utilizing data from 219 non-financial firms listed on the Pakistan Stock Exchange from 2008 to 2021, we employ fixed-effect regression with robust standard errors to mitigate concerns of heteroscedasticity and autocorrelation. Our findings unveil a compelling narrative: managerial ability and capital structure positively influence firm performance, with capital structure acting as a partial mediator in the relationship. Additionally, a positive correlation is observed between CSR and firm performance, while the interaction between managerial ability and CSR shows a positive, though weakly significant, correlation with firm performance This research significantly contributes to the literature by emphasizing the influence of managers on capital structure and the importance of reporting CSR activities in decision-making processes. It enhances our comprehension of these interactions, providing valuable insights into their critical roles within modern business environments.

Plain Language Summary

This research explores how corporate social responsibility (CSR) and financial decisions impact firm performance in Pakistan. Analyzing data from 219 non-financial firms listed on the Pakistan Stock Exchange from 2008 to 2021, we used fixed-effect regression to address statistical concerns. Our findings show that skilled managers and effective capital structures contribute positively to firm performance. Capital structure also acts as a mediator in this relationship, partially explaining how managerial abilities affect performance. Additionally, we found a positive link between CSR activities and firm performance, especially when combined with strong managerial skills. This study underscores the significant influence managers have on a firm’s financial structure and highlights the importance of CSR reporting in strategic decision-making. It provides valuable insights into these dynamics, enhancing our understanding of their critical roles in modern business environments.

Keywords

Introduction

In the contemporary, dynamic, and competitive landscape of the business world, the prevailing consensus among researchers emphasizes the integral connection between the success and expansion of businesses and the proficiency of their management. In this fast-paced environment, the ability to make well-informed decisions in a timely manner is deemed essential. The impact of managerial capabilities on firm performance has been extensively explored in both management and organizational literature (Bertrand & Schoar, 2003; Naushad et al., 2020). A multitude of research studies consistently affirm a positive correlation between managerial ability and firm performance, underscoring the notion that managers with higher levels of proficiency contribute significantly to superior organizational outcomes (Dong & Doukas, 2021; Huang & Xiong, 2023). However, in today’s rapidly evolving business landscape, simply analyzing the direct impact of managerial skill on firm performance might not provide a comprehensive understanding of a manager’s capacity to maintain a competitive edge. Therefore, it is imperative for research to investigate how managerial ability impacts firm performance by considering the mediating role of capital structure and the moderating influence of CSR.

Initially, this study endeavors to unravel the intricate role of capital structure as a mediator, navigating the relationship between managerial ability and corporate performance within the unique context of Pakistan. In the dynamic and evolving economic landscape of Pakistan, understanding the interplay between managerial ability, capital structure, and firm performance has become increasingly critical for sustainable corporate growth and competitiveness. Managerial ability, which reflects the efficiency and strategic acumen of top executives, plays a pivotal role in shaping financial decisions, particularly those related to capital structure—the mix of debt and equity used to finance operations. Optimal capital structure decisions can significantly influence a firm’s cost of capital, risk profile, and ultimately, its financial performance (Modigliani & Miller, 1958; Myers, 1984). However, in emerging markets where access to capital is constrained and financial markets are still developing, the influence of capable management on financial structuring and operational performance becomes even more significant. Firms led by high-ability managers are more likely to make informed financing decisions, effectively balance leverage, and ultimately drive superior firm performance.

Managers in Pakistani firms face unique challenges when managing capital structure in an unstable economic environment, especially compared to their counterparts in developed nations. Due to factors such as political instability, inflation, currency depreciation, and limited access to long-term financing, Pakistani managers tend to adopt more conservative and flexible capital structure strategies. Unlike in developed countries where firms can easily access deep and stable financial markets, Pakistani firms often rely more heavily on internal financing or short-term debt from local banks. Moreover, Pakistan’s corporate sector is characterized by weak legal frameworks, limited shareholder protection, and a high concentration of family-controlled firms. These governance deficiencies create an environment where managerial decision-making may not align with shareholder interests, leading to suboptimal financial decisions. For instance, S. Khan et al. (2025) note that in Pakistan, the dominance of family ownership often leads to decisions that prioritize control over profitability, which can distort capital structure choices. Similarly, Shah et al. (2023) emphasize that weak regulatory oversight in Pakistan impedes managerial accountability, ultimately affecting how managers make critical decisions regarding capital structure and investment, which can directly influence firm performance. The lack of robust corporate governance in Pakistan presents a unique opportunity to examine how these deficiencies impact managerial ability in making financial decisions.

In contrast, developed economies typically exhibit stronger regulatory frameworks, enhanced investor protection, and more transparent corporate governance practices. This is reflected in studies like La Porta et al. (2000) who found that such environments promote better managerial accountability and more efficient capital structure decisions, leading to improved firm performance. Additionally, Ararat et al. (2014) also highlighted that the stronger legal protections and clearer financial regulations in developed markets help mitigate the risks of poor financial decision-making. Moreover, in emerging markets where information asymmetry and corporate governance issues may be more pronounced, investors often rely on signals from managers as proxies for the firm’s underlying fundamentals and future prospects. Managers who effectively communicate their strategic vision, financial acumen, and commitment to maximizing shareholder value through capital structure decisions are likely to garner investor confidence and support. Asymmetric Information Theory asserts that firm managers, being insiders, possess superior knowledge about their company compared to outside investors (Ross, 1977). This informational advantage prompts well-informed managers to strategically disseminate positive information to the market or less informed investors, aiming to enhance the perceived value of their firm. This behavior aligns with the Signaling Theory, which suggests that managers are motivated to utilize diverse methods to convey distinctions between their firm and weaker competitors.

In addition, our study endeavors to assess the moderating impact of CSR on the relationship between managerial ability and company performance. In recent years, the strategic role of CSR in enhancing firm reputation, customer loyalty, and financial performance has attracted significant attention in both academic and business circles. CSR refers to a firm’s initiatives to assess and take responsibility for its effects on the environment and social well-being. While CSR is often driven by external pressures such as regulatory frameworks, stakeholder expectations, and global sustainability trends, emerging research emphasizes the crucial influence of managerial ability in determining the extent and effectiveness of a firm’s CSR engagement (Waldman et al., 2006). In developed countries, CSR is typically institutionalized within corporate strategy, guided by strong legal frameworks, standardized reporting practices (such as GRI or ESG disclosures), and active stakeholder oversight. Firms in these economies often pursue CSR not only as a moral or legal obligation but also as a means to gain competitive advantage, build long-term stakeholder trust, and meet investor expectations, especially from ESG-conscious funds (Carroll & Shabana, 2010).

Meanwhile, CSR is gradually gaining momentum in Pakistan as firms recognize its importance for long-term sustainability, stakeholder trust, and competitive advantage. With increased awareness among consumers, pressure from international partners, and evolving government policies, many Pakistani companies—especially in sectors like banking, textiles, and manufacturing—are incorporating CSR into their business strategies. Initiatives often focus on education, health care, environmental protection, and community development. However, despite this positive trend, firms in Pakistan face several challenges in effectively implementing CSR. One major hurdle is the lack of a well-defined regulatory framework and enforcement mechanisms, which leads to inconsistent standards and practices across industries. Additionally, limited financial resources, especially for small and medium-sized enterprises (SMEs), restrict their ability to invest in meaningful CSR programs. There is also a general lack of awareness and expertise among corporate leaders regarding the strategic benefits of CSR. Cultural barriers, low stakeholder engagement, and weak corporate governance further hinder effective implementation (F. M. Khan et al., 2012). In such a challenging environment, managers in Pakistani firms play a pivotal role in successfully implementing CSR by acting as change agents and strategic leaders. Their commitment and vision are crucial in integrating CSR into the core business strategy rather than treating it as a peripheral activity.

This paper introduces a novel conceptual model that integrates the role of managerial ability as a mediating or moderating factor between CSR, capital structure, and firm performance. Our paper offers a distinct contribution by integrating stewardship, signaling, and stakeholder theories into a unified framework. This multi-theoretical approach provides a deeper understanding of how MA influences both CSR and capital structure, which in turn affect FP—an angle less explored in the context of emerging markets. Furthermore, we highlight the relevance of these theories under weak institutional environments, where signaling and stewardship play a more critical role. Furthermore, research endeavors often exhibit a tendency to concentrate solely on specific. sectors within the developing market, predominantly concentrate on sectors such as power, pharmaceuticals, food, and industrial domains (Ahmad et al., 2012; Chowdhury & Paul Chowdhury, 2010; Pouraghajan et al., 2012; Salim & Yadav, 2012), thereby failing to adequately represent the broader spectrum of transitioning economies. To address this limitation, we have comprehensively examined 219 non-financial sectors in Pakistan. Additionally, many studies are characterized by relatively short time spans (Basit & Hassan, 2017; Muhammad et al., 2014; Naseem et al., 2019), which may compromise the precision and clarity of results. In light of this, we have opted for an extended time series analysis to ensure the attainment of more accurate and well-defined findings.

The subsequent sections of this work are delineated into the following categories. The second and third segment delves into the literature review and the formulation of hypotheses. Following that, the fourth section encompasses discussions on sample selection, data collection, variable construction, and empirical methods. Section 5 and 5 provides commentary, offering insights into the empirical findings and facilitating discussion. The conclusive segment, the final section, entails discussions on conclusions drawn and the policy implications derived from the study.

Theoretical Review

Stakeholder Theory, proposed by Freeman (2010) posits that a firm’s success is contingent upon its ability to meet the needs and expectations of various stakeholders, including employees, customers, investors, and the broader society. In emerging economies such as Pakistan, where regulatory enforcement is weak and social institutions are underdeveloped, firms often engage in CSR as a strategic response to build legitimacy, mitigate risk, and secure stakeholder support. High-ability managers are better equipped to understand the complex expectations of diverse stakeholder groups and strategically align CSR initiatives to meet these demands while also creating long-term value. Thus, managerial ability becomes a central mechanism through which CSR is effectively integrated into the firm’s strategy. Empirical studies, such as those by Cheng et al. (2014) and Mishra and Modi (2016) provide evidence that CSR initiatives, when effectively managed, improve stakeholder engagement, lower the cost of capital, and ultimately lead to better financial performance. These findings align with Stakeholder Theory, which posits that a strong focus on stakeholder interests, supported by managerial ability, is crucial for long-term success (Davis et al., 2018).

Davis et al. (1997) emphasize managerial ability through the lens of stewardship theory, viewing managers as aligned with firm and stakeholder interests rather than self-serving agents. This perspective is particularly relevant in Pakistan, where many firms are family-owned and governance may lack independence. High-ability managers with integrity often treat CSR as a strategic investment and favor conservative, sustainable capital structures. Additionally, A. Khan et al. (2013) find that firms with strong stewardship practices, characterized by managers who focus on long-term objectives, tend to adopt more conservative capital structures, relying more on equity financing than debt. This more prudent approach to capital structure helps firms avoid financial distress and enhances overall firm performance.

On the other hand, signaling theory proposes that companies use their capital structure decisions as signals to communicate confidential information to external stakeholders, such as creditors and investors, about their risk profile and future prospects (Myers & Majluf, 1984). In this regard, a company’s choices about its capital structure, such as issuing debt or equity, are seen as indicators of the company’s confidence in its capacity to provide future cash flows and successfully manage financial risk. Moreover, Spence (2007) suggest that high-ability managers can use CSR disclosures and conservative capital structure choices to signal competence and stability to investors and the public. Engaging in CSR, for example, sends a signal of ethical commitment and long-term orientation, while maintaining an optimal capital structure signals financial prudence and risk-awareness.

Empirical Review and Hypothesis Development

Managerial Ability and Firm Performance

Managerial ability is a critical determinant of a firm’s success and plays a pivotal role in reducing agency conflicts. It includes a variety of skills, expertise, and qualities that enable managers to lead effectively and make decisions that benefit the organization (Ashiq et al., 2022; Naushad et al., 2020). According to stewardship theory, managers are most effective when they prioritize increasing their own utility in ways that align with shareholder interests. As such, managers with higher levels of ability are likely to act with greater diligence, make more informed decisions, and ensure their actions are consistent with the goals of the firm’s shareholders (Chrisman, 2019). Consistent with the theory, several studies, such as Bamber et al. (2010) and Bertrand and Schoar (2003) have investigated the significance of managers’ characteristics in affecting corporate success and demonstrate that several leader- and firm-specific elements influence firm behaviors.

In Pakistan, few studies examined the relationship between MA and FP. Inam Bhutta et al. (2021) analyzed the relationship between management talent and FP using a sample of 246 firms listed on the Pakistan Stock Exchange from 2009 to 2017. The study findings suggest that managers who demonstrate competence have a notable and positive influence on the FP. Similarly, W. Ahmed et al. (2022) analyzes a sample comprising 100 businesses listed on the KSE 100 Index in Pakistan, spanning 2014 to 2020. The study’s findings indicate a positive association between managers’ risk-taking capabilities and companies’ overall performance. However, there is another perspective, as mentioned in the second school of thought. This viewpoint suggests that more capable managers might engage in ill-advised actions such as investment manipulation or earnings management. Despite their capabilities, these actions typically have negative consequences and diminish the firm’s overall value (Francis et al., 2008; Malmendier & Nagel, 2011).

Managerial Ability and Capital Structure

As H. K. Baker and Martin (2011) highlighted, a firm’s capital structure embodies the blend of debt and equity deployed to underpin its operations, assets, and future growth prospects. This amalgamation is a pivotal determinant in gaging the firm’s overall cost of capital while exerting a profound influence on its risk exposure. By strategically managing this composition, companies navigate a delicate balance between leveraging borrowed funds to fuel growth and maintaining an optimal level of equity to fortify resilience against financial uncertainties. Furthermore, Bhagat et al. (2011) suggests that managers opting for lower levels of long-term debt may inadvertently sacrifice internal equity ownership and management effectiveness, thus subjecting the company to enduring dangers that could impact its worth. Moreover, Matemilola et al. (2018) highlight that, in order to protect the company’s earnings from taxes, competent executives frequently engage in the use of additional debt, which subsequently increases the company’s dependence on debt capital. Additionally, Bhagat et al. (2011) reveals that a firm’s financial decisions are significantly influenced by the transparency of management and the inherent conflicts of interest between managers and shareholders, which ultimately shape the company’s capital structure and market valuation. These factors play a crucial role in understanding a company’s leverage.

Enhanced educational attainment among CEOs correlates positively with their ability to make astute financing and investment choices. Conversely, optimistic and self-assured managers within various industry echelons tend to lean toward elevated debt levels, thereby potentially enhancing firm value (Hackbarth, 2008; Naseem et al., 2019). In the context of pecking order theory, managerial expertise impacts the firm’s ability to generate internal cash. Moreover, managers who are skilled at efficiently managing resources and generating profits are more likely to generate higher levels of internal funds through retained earnings. Conversely, managers with poor ability may struggle to generate internal funds, leading them to rely more heavily on external financing options, disrupting the pecking order.

Capital Structure and Firm Performance

Research investigating the relationship between capital structure and firm performance has yielded varied and nuanced findings over the years. A well-orchestrated capital structure can yield positive ramifications on financial performance, enhancing metrics such as profitability and return on investment (Dabi et al., 2023). Signaling theory suggests that companies may strategically use their capital structure decisions to communicate their quality or financial strength to investors. Myers and Majluf (1984) argued that the selection between debt and equity financing serves as a signal regarding the firm’s underlying value to investors. They emphasized how adverse selection problems in capital markets might arise from shareholders and managers having uneven access to information. Furthermore, Rahman et al. (2019) focused on assessing how the capital structure influences the profitability of publicly traded manufacturing firms operating in Bangladesh. To accomplish this, the researchers conducted an analysis using data collected from 10 specific manufacturing companies listed on the Dhaka Stock Exchange, comprising a total of 50 data points. The results revealed a statistically significant positive relationship between the levels of debt and equity ratios and Return on Equity (ROE). Similarly, Lemmon and Zender (2010) argued that when a firm issues debt, it signals confidence in its future cash flows to meet interest payments. This can lead to positive effects on firm value and performance.

However, excessive debt may lead to financial distress, affecting performance negatively (Dalci et al., 2019; Forte & Tavares, 2019; Le & Phan, 2017; Ullah et al., 2020). Similarly, Ahmed Sheikh and Wang (2013) research revealed an inverse correlation between capital structure and firm performance, suggesting that agency problems could drive companies to incorporate excessive levels of debt into their capital structure. This overreliance on debt may augment the influence of lenders, subsequently constraining managerial autonomy in effectively overseeing operations. As a result, this phenomenon detrimentally affects the overall performance of the firm. In a parallel study, Ullah et al. (2020) scrutinized the influence of capital structure on the financial performance of 90 textile companies listed on the Pakistan Stock Exchange (PSX) over the period spanning from 2008 to 2017. Findings revealed a complex dynamic between capital structure and performance, suggesting that higher levels of debt could negatively impact profitability due to increased financial risk and interest obligations. Furthermore, Nguyen and Malik (2022) findings show a negative correlation between the performance of Vietnamese-listed non-financial enterprises and their capital structure.

Capital structure mediates the relationship between managerial ability and firm performance by influencing how effectively managers utilize available financial resources to drive growth. Skilled managers can optimize the capital structure to balance debt and equity, enhancing firm profitability and stability (Jensen & Meckling, 1976). Studies have shown that managerial characteristics, such as CEO duality, tenure, and personal traits, influence capital structure decisions, which in turn affect firm performance. Fernando et al. (2020) investigated how management competence mediated the relationship between gender diversity and company success. Effective management, characterized by high levels of managerial aptitude, is essential for leveraging the benefits of gender diversity within a company. On a similar note, Naseem et al. (2019) delved into the impact of CEO traits on company performance, highlighting the potential mediating role of capital structure in this dynamic. Although their sample period was quite short (7 years), they included CEO duality, tenure, age, gender, and educational background as important explanatory factors in their analysis.

Furthermore, Research by Shakri et al. (2025) shows that the link between corporate governance (CG) compliance and financial performance (FP) weakens when capital structure (CS) is considered, suggesting partial mediation. In developing economies, firms may underestimate the costs of financial distress and bankruptcy, leading to excessive debt and reduced profitability. Over-leveraging can also trigger management behaviors like over-conservatism, short-termism, and under-investment, which harm long-term financial performance.

CSR and Firm Performance

The relationship between CSR and financial performance in Pakistan has gained attention in recent years, but the findings are mixed. Studies have shown that CSR activities can contribute to improved financial performance by enhancing brand equity, customer loyalty, and operational efficiencies. Hameed (2024) examined the textile industry in Pakistan and found that CSR initiatives, such as community development and environmental sustainability, lead to positive financial outcomes, such as higher profitability and better market performance. Similarly, Javeed and Lefen (2019) provides insight into the empirical connection between CSR and FP in Pakistan. It was found that CSR and FP are positively correlated, as social initiatives boost businesses’ trust in their internal and external surroundings. Furthermore, empirical evidence from a study by Adnan Akhtar et al. (2024) indicated that CSR engagement improved the financial performance of Pakistani firms, especially in manufacturing and services. Ethical practices and environmental sustainability enhanced corporate image and attracted socially responsible investors, increasing capital inflows and financial outcomes.

While CSR in Pakistan has been primarily focused on social welfare and environmental initiatives, the nature of CSR practices varies widely across industries. In the manufacturing and industrial sectors, CSR often takes the form of environmental sustainability initiatives, such as waste management and energy conservation. Zahid et al. (2024) argue that these CSR practices help firms reduce operational costs, especially in energy-intensive industries. Conversely, in the service sectors, such as banking and telecommunications, CSR is more oriented toward community engagement and financial inclusion. For example, banks in Pakistan often adopt CSR initiatives focused on providing access to financial services for underprivileged communities, thereby enhancing their reputation and customer base (Hafeez et al., 2014).

Comparatively, in developed countries, such as the United States or the European Union, CSR is more deeply embedded in corporate strategies, with a greater regulatory framework and investor demand for transparency. In these regions, managers leverage CSR as a tool not only for enhancing public image but also for compliance with environmental, social, and governance (ESG) standards, which can lead to improved financial performance through cost savings, risk management, and increased investor confidence. For example, companies in the U.S. and Europe have increasingly adopted green technologies and ethical sourcing practices, which have proven to reduce operational costs and enhance profitability (Porter & Kramer, 2006). Similarly, Bacinello et al. (2020) developed maturity models to examine the influence of CSR Management (CSRM) on Strategic Innovation Management (SIM) and the impact of those traits on FP. The study was founded on resource-based theory and employed structural equation modeling for a sample of 154 Brazilian businesses. The study’s findings indicated that CSRM positively influences SIM, and both CSRM and SIM positively influence FP. Moreover, the results (Cormier and Magnan, 2014) suggest a positive relationship between CSR practices and financial performance. Based on their research, it has been observed that companies that actively participate in socially responsible initiatives generally exhibit solid financial performance.

In Pakistan, Corporate Social Responsibility (CSR) provides managers with a unique opportunity to enhance their abilities in driving financial performance while addressing social and environmental concerns. By integrating CSR into business strategies, managers can improve a company’s reputation, which plays a crucial role in enhancing customer loyalty, attracting new customers, and expanding market share. In the Pakistani context, CSR is particularly important as consumers are becoming more socially conscious, and they are increasingly likely to support businesses that contribute positively to society (Hafeez et al., 2014).Similarly, When and Respond (2004) highlight that consumers are more likely to support companies with ethical practices, boosting revenue and market share. CSR also promotes operational efficiency by encouraging waste reduction, resource optimization, and sustainable practices, leading to lower costs and long-term profitability.

The researchers discovered that the managerial competence of CEOs encourages sustainable practices. A study by M. K. Khan et al. (2022) conducted on Chinese listed firms spanning the period from 2010 to 2019 indicates a positive correlation between the managerial competence of CEOs and the implementation of sustainable practices within these firms. Similarly, Jiang et al. (2021) indicates that CSR moderates the association between female executives and firm performance in China. Gender-diverse boards focusing on CSR can enhance the firm’s reputation and stakeholder relations. Improved stakeholder relationships can lead to increased customer loyalty, access to capital, and a more supportive business environment, all of which can contribute to better financial performance. Furthermore, Orlitzky et al. (2003) emphasize that companies with strong CSR practices are more likely to gain investor confidence, reduce capital costs, and increase access to funding, ultimately boosting financial performance. In conclusion, CSR enables managers to exploit their abilities to foster long-term profitability by improving brand reputation, operational efficiency, employee engagement, and attracting investment.

Methodology

Sample Selection

This study utilizes a randomly selected sample of 219 non-financial firms listed on the Pakistan Stock Exchange (PSX), chosen based on the availability and completeness of relevant financial data. Covering a 14-year period from 2008 to 2021, the sample reflects the diversity of Pakistan’s economic landscape, spanning various non-financial sectors. A total of 130 financial institutions were excluded from the initial pool of 552 listed companies, owing to their specialized operational structures and the separate regulatory and legal frameworks under which they operate. Furthermore 203 firms were removed from the sample due to insufficient data availability or delisting during the sampling period. The analysis is based on secondary data obtained from multiple credible sources, including companies’ annual reports, the Pakistan Stock Exchange, the Pakistan Bureau of Statistics, the Business Recorder, and the State Bank of Pakistan. In accordance with the regulatory requirements set by the Securities and Exchange Commission of Pakistan (SECP), all registered firms are mandated to disclose accurate and timely information regarding share issuance, annual and semi-annual reports, as well as reports on significant corporate events (Adnan Akhtar et al., 2024; W. Ahmed et al., 2022; Javeed & Lefen, 2019, Table 1).

Sample Selection.

Managerial Ability (Independent)

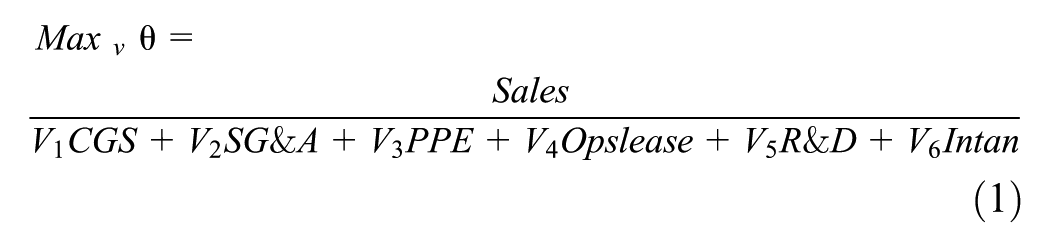

To quantify managerial ability (MA) in line with the methodology proposed by Demerjian et al. (2012), a two-step approach is employed. In the first phase, the Data Envelopment Analysis (DEA) technique is used to measure a company’s industry-specific input-output efficiency. The DEA model compares a firm’s input and output to determine its efficiency, where the efficiency score ranges from 0 to 1. A score of 1 represents firms on the efficient frontier, while a score of 0 indicates the least efficient firms.

The output variable in Equation 1 is the firm’s sales (Sales), and the input variables are: CGS refers to cost of goods sold (reflects direct material and labor costs; critical to operational efficiency),

However, the MA component and firm-specific variables can influence how the DEA method determines a company’s efficiency score. In the second phase, Demerjian et al. (2012) regress the firm-level efficiency score derived from DEA on various firm-specific parameters to estimate managerial ability (MA). The regression equation is as follows:

Where;

The residual from this regression,

Thus, the managerial ability score (MA) for firm i at time t can be calculated as:

Capital Structure (Mediator)

The debt to equity ratio serves as a gage of a company’s capital structure, revealing the extent to which it relies on debt to finance its operations. This metric illuminates the dynamic between debt and equity value within the company (Wijaya et al., 2023).

Firm Performance (Dependent)

Market-Based Performance (Tobin’s Q)

Tobin’s Q is widely used in empirical research to study investment decisions, firm growth, corporate governance, and financial performance. A high Q ratio generally signals good future prospects, while a low Q ratio could indicate inefficiencies or undervaluation. Tobin’s Q ratio is determined by dividing the combined market capitalization and total debt by the company’s total assets. This ratio serves as a financial metric that reflects the market’s evaluation of a company’s overall performance.

Where,

MVS = Market value of stock is equity

ST = Short term debt,

LT = long term debt,

FA = Fixed asset,

CA = Current asset,

Inv = Inventory

If the value of Tobin Q > 1 confirms that the market value exceeds the firm value assets and vice versa (Kalantonis et al., 2021; Weir et al., 2002). The existing literature argues that a higher value of Q shows better performance in the market (Butt et al., 2023; Tan & Peng, 2003).

Corporate Social Responsibility (Moderating Variables)

Many studies have developed CSR measuring indices, most of which cover comparable elements, such as minority rights, shareholder rights, individual freedoms, and human rights. Using the Carroll (2021) framework, researchers in Pakistan developed a questionnaire to quantify CSR (Asrar-ul-Haq et al., 2017). A study in China established a CSR index based on 63 factors, including stakeholder rights, labor, and humanity, and conducted an impartial operation (Han & Stoel, 2017). This study develops a CSR Index to assess the extent of CSR engagement among companies in Pakistan. The index is based on four widely acknowledged CSR dimensions: community involvement, employee welfare, customer/product responsibility, and environmental sustainability. These dimensions reflect the key areas where corporations are expected to demonstrate social accountability and are consistent with both academic literature and the local regulatory context (e.g., SECP CSR guidelines in Pakistan).

The CSR index is calculated using a binary scoring system, where each CSR indicator is assigned a value of 1 if disclosed or implemented by the company, and 0 if not. The total CSR index score for a company in a given year is obtained by summing the scores of all indicators and dividing by the total number of indicators. This produces a normalized CSR score between 0 and 1, where higher values reflect greater CSR engagement. This measurement technique is consistent with previous CSR studies in emerging economies (B. Ahmed et al., 2022; Reverte, 2009) and is particularly suitable for Pakistan, where CSR reporting is still largely voluntary and varies widely across sectors. The data for index construction were collected manually from annual reports, sustainability reports, and corporate websites of companies listed on the Pakistan Stock Exchange (PSX) over a selected time frame (Xia et al., 2018).

Control Variables

Consistent with prior research, such as studies conducted by Abdullah et al. (2022), McWilliams and Siegel (2011), and Muhammad et al. (2014), which investigate the impact of control variables on firm performance, we incorporated board size, firm age, firm tax, and firm size into our analysis. To control for firm size, it is customary to utilize a size proxy, such as the natural logarithm of the book value of total assets (Latif et al., 2017; Tabassam & Khan, 2021). Board size is defined as the total number of directors serving on the board (Vaidya, 2019; Sharma et al., 2023) and neutral log value of (In-tax) payment (F. Ahmed et al., 2024). Moreover, ownership concentration refers to the percentage of a company’s shares that are held by its top five shareholders, calculated by dividing the total shares. Institutional ownership, on the other hand, represents the proportion of a company’s equity that is held by institutional investors (Latif et al., 2017; Table 2).

Description of Variables.

Mediation Analysis

Through the use of a mediating variable (capital structure), we investigate the relationship between an independent variable (managerial ability) and the dependent variable (firm performance) in a mediation study (Chou et al., 2013). Preacher and Hayes (2008), provide a bootstrapping method for assessing the significance of the indirect effect, which is particularly useful for handling non-normal distributions of the mediation effect. This method helps determine whether the mediator significantly explains the relationship between dependent and independent and quantifies both direct and indirect effects, making it a robust tool for testing mediation hypotheses (Figure 1).

The effect of managerial ability (MA) on firm performance (FP) can be divided into two components: the direct effect, represented by ‘c', and the indirect effect, which operates through the mediating variable of capital structure. The indirect effect is calculated as ‘ab', which is the product of the ‘a’ and ‘b’ pathways

Causal association among managerial ability, capital structure, and firm performance.

The following equations represent the econometric model used to analyze the direct and indirect effects of managerial ability (MA) on firm performance (FP).

Where;

DR represents the debt-to-equity ratio, MA refers to managerial ability, FZ indicates firm size, BS stands for board size, and lnTax denotes the firm’s tax burden, LSH is ownership concentration, INS is institutional ownership, Tobin’s Q (TQ) is used as a measure of market-based firm performance. The subscript ‘i’ refers to individual firms, while ‘t’ represents the time period.

Moderation Analysis

To reflect the direct impact of managerial ability and CSR on firm performance, we have constructed the following econometric model:

Where;

MA is managerial ability, CSRI is Corporate Social responsibility Index.

Moderated Regression analysis conducts a moderating variable test using the following equation.

The positive sign of the interaction term (MA × CSRI) concludes that CSR enhances the effect of MA on the FP relationship and will behave as a complement. The significant negative sign concluded that MA and FP relation is weaker and will behave as a substitute (Figure 2).

Managerial ability and firm performance with CSR as a moderator.

Results and Discussion

Descriptive Analysis

In Table 3, crucial statistical metrics are meticulously presented for comprehensive data scrutiny. The mean values offer insights into the central tendency of each variable, showcasing their typical magnitude. Meanwhile, the standard deviation quantifies the extent of dispersion around these means, shedding light on the variability within the dataset. The minimum and maximum values denote the range within which the data fluctuate. Descriptive values indicate that all variables remain within normal ranges, affirming the reliability of the data. Consequently, the data associated with the endogenous construct holds potential for future research endeavors.

Descriptive Statistics.

Correlation analysis serves as a statistical tool employed to unveil the magnitude and orientation of a linear connection between two variables. In Table 4, the Pearson correlation coefficients are provided, offering insights into the associations among the variables. This analysis reveals that both the correlation coefficients and the examination of covariance fail to detect any signs of multicollinearity within the dataset.

Correlation Matrix.

Significant at 1%. **Significant at 5%. *Significant at 10%.

Regression Analysis

This section explores the different channels through which managerial ability (MA) affects firm performance (Tobin’s Q), with capital structure acting as a mediating variable. Study utilizes both fixed and random effects models to analyze panel data, with the Hausman test applied to identify the more suitable approach (Semykina & Wooldridge, 2010). As shown in Table 5, the test produces a p-value of .0000, signifying strong statistical significance. This outcome favors the selection of the fixed-effects model over its random-effects counterpart. Further, Model 6 reveals a significant and positive direct relationship between managerial ability and market-based performance (Tobin’s Q), with a coefficient of .156 at the 1% significance level. This finding supports Hypothesis H1 and aligns with earlier studies that have reported a positive association between managerial ability and Tobin’s Q (W. Ahmed et al., 2022; Andreou et al., 2013). In essence, improvements in managerial competence contribute to enhanced firm performance. In Model 7, managerial ability also demonstrates a positive effect on debt ratio (DR), with β1 = .221 and a p-value less than .01. Furthermore, Model 8 indicates that DR has a significant positive influence on Tobin’s Q, with a p-value of .004, significant at the 10% level (Ahmed Sheikh & Wang, 2013; Lemmon & Zender, 2010; Rahman et al., 2019). Stewardship theory is supported by our results, which show that managers acting in the firm’s long-term interests make more optimal capital structure decisions, which enhance firm performance.

Results of Fixed Effects with DR Acting as a Mediator (Models 6–9).

Note. Hetro -Auto consistent Standard Errors, as suggested by Newey and West (1987) suggested.

Significant at 1%. ** Significant at 5%. * Significant at 10%.

Model-9 depicts the total effect (TE), concluding that direct (0.156, p < .01) and indirect effects are significant at (.098, p < .001), respectively. The significant direct and indirect effects confirmed the existence of partial mediation (Zhao et al., 2010) and supported hypotheses H1, H2, H3, and H4. Results are based on signaling theory (communicating managerial confidence and future prospects), which suggest that competent managerial decisions—such as strategic use of debt—serve as positive signals to the market about the firm’s strength and future prospects. Furthermore, empirical evidence indicates that firms led by capable managers adopt value-enhancing capital structures, consistent with stewardship theory, which posits that managers act as responsible stewards of corporate resources to maximize shareholder value. (Hossain, 2021). Control variables such as firm size and age have been observed to exert a negative influence on firm performance. This finding aligns with Anowar (2016) research, which suggests that as firms grow larger, they often increase their debt levels, leading to higher interest expenses and consequently an elevated cost of capital. On the other hand, board size and tax were found to have a positive impact. Larger boards can enhance governance effectiveness, while debt can provide tax shields that boost net income. Additionally, institutional ownership and concentrated ownership appear to have a positive effect on Tobin’s Q, suggests that having informed and engaged owners (institutional investors) or concentrated ownership might lead to better corporate governance and higher firm value.

Table 6 presents the estimated fixed effects regression coefficients for the interaction between MA and corporate financial valuation, incorporating CSRI as a moderator. The Hausman test was conducted to determine whether the fixed effects or random effects model would be more appropriate for the analysis. The test yielded a p-value of .0000, which is highly statistically significant. As a result, the fixed effects model is preferred for this analysis. Further on, Model-10 and 11 is analyzed for the testing of hypothesis (H5 & H6). The fixed effect regression with robust standard error option and cluster option has been used in the study to correct any issue of unobserved heterogeneity and serial correlation. The robust standard error and cluster technique correct any cross-section and serial correlation problems in the data (Wooldridge, 2013).

Fixed Effect Results for TQ (10 & 11).

Note. Hetro-Auto consistent Standard Errors as suggested by Newey and West (1987).

Significant at 1%. **Significant at 5%. *Significant at 10%.

The direct effect of MA on TQ is consistent, and the results indicate a statistically significant positive relationship in all of the models as (β1 = .199, p < .01, β2 = .187, p < .05. The positive and significant coefficients show that MA optimizes the company’s efficiency (TQ). Moreover, Table 6 also depicts the estimates of moderating variable CSRI. The interaction term coefficient (MA × CSRI) is positive but weakly significant (0.070, p < .05). These findings illustrated that the possibility of CSRI moderates the relationship between MA and TQ, but the effect is not strong. In emerging markets like Pakistan, CSR is often driven more by regulatory compliance and reputational concerns than by a genuine strategic integration into business practices. As a result, CSR activities may not effectively enhance or strengthen the link between managerial ability and firm performance. The company’s size is statistically significant and negative, while board size, tax, and age is positive. Ownership concentration and institutional ownership have a positive effect on firm performance. This is likely because they have stronger incentives to oversee management and ensure the firm operates efficiently.

Discussion

Managerial Ability, Capital Structure, and Firm Performance

The study’s conclusions showed how MA affected TQ. The direct effect of MA on TQ is positive and significant. These results align with the previous studies of Bamber et al. (2010), Bertrand and Schoar (2003), and Tabassam and Khan (2021), which explored the relationship between MA and FP. These studies demonstrate that several leader- and firm-specific elements influence firm behaviors. M. A. Baker and Kim (2020) recently found that firms led by managers with higher emotional intelligence and cognitive skills tend to outperform their competitors. However, these results contrast with those of Francis et al. (2008) who argue that highly capable managers may sometimes engage in questionable practices, such as investment manipulation or earnings management. Despite their competence, such actions often lead to negative outcomes and undermine the firm’s overall value. Furthermore, these findings are corroborated by previous research by W. Ahmed et al. (2022), Inam Bhutta et al. (2021), which observed a positive relationship. In this context, Stewardship theory supports the notion that managerial ability can have a favorable effect on firm performance (Chrisman, 2019). Managers can make decisions that align with the organization’s long-term goals, navigate challenges, and maximize stakeholder value, rather than pursuing self-interested behavior that may harm the firm’s overall performance.

Empirical findings underscore the positive and significant impact of managerial ability on a firm’s capital structure, in line with Matemilola et al. (2018) observations. Stewardship orientation suggests that managers with a high sense of responsibility are more likely to adopt prudent capital structure decisions that minimize financial risk while promoting sustainable growth and performance. Moreover, the nexus between capital structure and firm performance manifests a positive effect, echoing Ross (1977) seminal work on signaling through debt issuance. In Pakistan’s high-information-asymmetry market, capital structure decisions act as key signals. Taking on long-term or favorable debt can signal confidence in future cash flows, boosting investor trust and firm valuation. This is especially impactful where financial transparency varies, and stakeholders rely on observable actions. However, the signal is effective only when balanced; excessive debt in a volatile economy may indicate financial distress, undermining credibility and performance. Strategic debt use thus plays a crucial role in shaping market perceptions.

Notably, capital structure acts as a partial mediator in the relationship between managerial capability and firm performance. This indicates that capital structure acts as an intermediary, facilitating the positive impact of managerial competence on firm performance. Results are consistence with the study of Ting et al. (2021). Likewise, Frank and Goyal (2003) found that firms with better managerial ability tend to make capital structure decisions that effectively communicate the firm’s financial health and future prospects to the market, which, in turn, positively impacts firm performance. Therefore, capital structure, as mediated by managerial ability, serves not only to optimize firm operations but also to communicate the firm’s value proposition to external stakeholders, influencing its market performance.

Managerial Ability and Firm Performance: Moderated by CSR

The study’s findings show that managerial ability, CSR adoption and business performance are positively correlated. The results align with a previous study Cormier and Magnan (2014) which concluded that well-implemented CSR measures enhance corporate performance and foster sustainability. By integrating CSR into their strategies and operations, companies can enhance their reputation, manage risks, drive innovation, engage employees, and create long-term value, leading to improved performance outcomes. Additionally, the results are consistent with the findings of Javeed and Lefen (2019) who supported the importance of CSR for firm performance in the Pakistani market. It was found that CSR and FP are positively correlated, as firms engage in CSR activities as a signal to the market, investors, and other stakeholders that they are committed to ethical practices and long-term sustainability. By doing so, they differentiate themselves from competitors, build trust, and enhance their reputation, which can lead to greater customer loyalty, higher sales, and improved financial performance. Results are aligns with stakeholder theory, which emphasizes that businesses achieve long-term success by addressing the needs and interests of all stakeholders—not just shareholders. Stakeholder theory supports the idea that by meeting the expectations of a broad range of stakeholders through CSR, firms not only fulfill ethical and social obligations but also create value that enhances overall firm performance. Furthermore, Adnan Akhtar et al. (2024) highlighted that CSR engagement had a positive impact on the financial performance of Pakistani firms, especially those within the manufacturing and services sectors.

In Pakistan’s complex socio-economic environment, where public trust, social inclusion, and regulatory alignment are essential for business sustainability, CSR serves as a strategic instrument for navigating these challenges. A strong example is Engro Corporation, which—under capable leadership—has effectively integrated a clear strategic vision with impactful CSR efforts through the Engro Foundation. This has led to strengthened public trust and lowered resistance to its operations in sensitive sectors. Likewise, Bank Alfalah has demonstrated how skilled leadership can align CSR initiatives—such as promoting financial literacy and women’s empowerment—with core business goals, leading to meaningful social outcomes and heightened customer loyalty. These examples highlight how CSR enhances the positive impact of managerial competence by building goodwill, minimizing operational friction, and unlocking new market opportunities—outcomes that are particularly crucial in the Pakistani business landscape.

Furthermore, the interaction terms between MA and FP moderated by CSR are only weakly significant, it suggests that while CSR may influence the relationship, its impact is not strong. This could be linked to inconsistencies in CSR reporting, lack of standardized disclosure frameworks, and limited stakeholder pressure may reduce the visibility and impact of CSR efforts. Many firms may also engage in CSR superficially, without aligning these activities with core business strategies or leveraging them to improve long-term performance. Furthermore, socio-political instability, weak enforcement mechanisms, and resource constraints can hinder firms from making substantial CSR investments, thereby weakening its role as a moderating factor. Overall, while managerial ability may independently influence performance, the moderating effect of CSR in Pakistan may be diluted due to these institutional and operational challenges. However, in developed economies, CSR is often embedded in corporate strategy, supported by strong regulations, transparent reporting, and active stakeholder engagement. These factors enhance CSR role in strengthening the impact of managerial ability on firm performance. In line with this, Jiang et al. (2021) found that in China, CSR significantly moderates the link between female executives and firm performance, with gender-diverse boards and strong CSR focus improving reputation and stakeholder trust. This effect is attributed to China’s solid legal and corporate governance framework, which facilitates effective CSR integration.

Conclusion

Findings

Validated framework showing accepted hypothesis and relationships

This study pertains to research conducted in Pakistan, a developing country, focusing on 219 non-financial enterprises listed on the Pakistan Stock Exchange (PSX) over 14 years (2008–2021). The estimate was obtained through panel regression, a fixed effect model, and the Hausman test. Research underscores the multifaceted interplay between managerial ability, capital structure and CSR in shaping firm performance. Evidence aligns with the hypotheses posited by stewardship theory regarding how managerial competence influences firm performance. Additionally, a significant and positive correlation was found in the Capital structure-performance relation. Moreover, our findings reveal that capital structure significantly mediates the relationship between managerial ability and firm performance. Furthermore, findings indicate that CSR improves a firm value. When implemented effectively, CSR initiatives can have several potential benefits that positively impact financial performance. Furthermore, CSR positively moderates the relationship between managerial ability (MA) and firm performance (FP), although this effect is relatively weak (Table 7, Figure 3).

Hypothesis Summary.

Validated framework showing accepted hypothesis and relationships.

Implications

The link between managerial competence and firm performance, with capital structure acting as a mediator and CSR as a moderator, carries significant implications for both theory and practice. The results emphasize the need to consider the broader impact of managerial decisions on organizational outcomes. From a theoretical perspective, Stewardship theory suggests that managers, motivated by concerns for their reputation and career growth, are inclined to act in the best interests of shareholders, thus minimizing agency costs within the organization (Donaldson & Davis, 1990). This reinforces the idea that effective leadership can shape key strategic and structural decisions, which directly influence the firm’s success. Additionally, signaling theory provides a useful framework for understanding the positive relationship between capital structure and firm performance, particularly in the context of Pakistan. By strategically managing their capital structure, firms can effectively signal their financial health and prospects to external stakeholders, thereby enhancing access to capital and fostering improved performance.

Given the significant influence of managerial ability (MA) on financial decisions, continuous professional development in areas like financial management and strategic decision-making is vital. Strengthening these skills enables managers to navigate Pakistan’s complex business landscape and make more informed, sustainable capital structure decisions. A transparent regulatory framework that balances managerial discretion with accountability can further enhance decision-making quality. Policymakers should promote corporate governance reforms and support managerial training initiatives to build leadership capacity. Investors, in turn, are encouraged to prioritize firms with strong, capable management teams, as such leadership is key to optimizing capital structure, managing risk, and driving long-term value—particularly in Pakistan’s dynamic and evolving market.

In Pakistan, the corporate sector is often characterized by family-owned businesses, where decision-making power is concentrated in the hands of a few individuals. This centralization can lead to a misalignment between managers and the broader interests of stakeholders, including those related to CSR. Additionally, the relatively weak regulatory environment and limited transparency can diminish the effectiveness of CSR initiatives, hindering firms from fully realizing their long-term potential. Given these challenges, firms should adopt a strategic and cost-conscious approach to CSR spending. Family-owned firms in Pakistan should integrate CSR into their long-term vision, ensuring that CSR activities are not viewed as a short-term expenditure but rather as a tool for building lasting relationships with customers, employees, and other stakeholders. Furthermore, firms should adopt a strategic and phased approach to CSR spending. First, cost-effective CSR initiatives that provide social value without significant financial outlay should be prioritized. For example, firms can focus on employee welfare, local community development, and environmental sustainability projects that require minimal investment but can enhance firm reputation and stakeholder relationships.

Additionally, firms should leverage their managerial ability to ensure CSR initiatives are aligned with their core business strategy, ensuring that CSR activities not only fulfill ethical responsibilities but also strengthen the firm’s competitive position. For instance, firms in Pakistan could implement CSR initiatives that focus on improving supply chain sustainability or corporate governance practices, which directly enhance operational efficiencies and help attract long-term investment. Moreover, continuous management training is essential to adapt to evolving business landscapes, involving participation in industry events, workshops, executive education programs, and fostering ongoing learning within the organization. This commitment to skill development enables leaders to better support their teams, foster innovation, and ultimately improve company performance, ensuring sustained growth.

Limitations

This study has limitations in terms of generalizability. Due to time constraints, the analysis focused on a sample of 219 publicly listed firms. The banking sector was purposely excluded from the scope of this research because its capital structure and accounting practices are notably different from other industries. Therefore, the conclusions drawn may not be applicable to sectors outside the study’s scope. Additionally, the research is confined to a single emerging market economy. Future research could broaden the comparison by including both developed and emerging economies. Additionally, future studies might explore other areas, such as the financial sustainability of firms or the risks of stock price instability, as alternatives to focusing solely on firm performance. Furthermore, additional effects of CSR marketing and customer purchasing behavior must be examined, Indeed, while CSR marketing has attracted significant attention and recognition recently as a strategy for businesses to showcase their social and environmental initiatives, it is important to acknowledge that research in this area is ongoing and there is still much to explore.

Footnotes

Acknowledgements

The authors have no acknowledgments.

Ethical Considerations

Not applicable.

Informed Consent

Informed consent was obtained form all individuals participants included in the study.

Authors Contribution

Conceptualization, Anam Ashiq; Methodology, Anam Ashiq; Software, Aftab Hussain Tabasam, Safdar Hussain Tahir; Validation, Anam Ashiq; Formal Analysis, Aftab Hussain Tabasam, Safdar Hussain Tahir; Investigation, Anam Ashiq; Resources, Anam Ashiq; Data curation, Anam Ashiq; Writing-orignal draft preparation, Anam Ashiq; Writing-review and editing, Anam Ashiq; Visualization, Anam Ashiq; Supervision, Zhang Guoxing; Project administration, Zhang Guoxing; Funding acquisition, Anam Ashiq.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.