Abstract

The rapid increase in household leverage in China has led to potential financial risks and threatened socio-economic stability. In mitigating household debt risks, the effectiveness of monetary policy regulation varies significantly with differences in household financial literacy. Based on micro-level household financial data from China, this paper delves into the impact of monetary policy on household leverage and its underlying mechanisms and analyzes the role of financial literacy in the transmission of monetary policy. The findings reveal that expansionary monetary policy helps reduce household leverage, while contractionary monetary policy leads to an increase. Monetary policy affects household leverage through the “income effect,”“wealth effect” and “substitution effect.” Notably, low financial literacy amplifies the impact of contractionary monetary policy on leverage, whereas high financial literacy mitigates this effect. This paper suggests strengthening financial regulation and risk warning systems, optimizing the design of monetary policy transmission, promoting multi-tiered financial product supply, and deepening the promotion of financial literacy education to achieve an effective balance between “stable growth” and “risk prevention.”

Introduction

Since the subprime mortgage crisis, China’s non-financial enterprises, local governments, and households have all experienced significant “leveraging” processes. However, in recent years, the leverage ratios of non-financial enterprises and local governments have shown signs of slowing down, while household leverage continues to rise. This has made China the fastest-growing country in terms of household leverage among major global economies since 2016. According to the People’s Bank of China’s “China Financial Stability Report (2023),” by the end of 2022, the household leverage ratio in China reached 71.8%, exceeding the 65% debt warning line defined by the International Monetary Fund. Moderate growth in household debt can promote consumption and investment, playing a positive role in driving economic growth. However, excessively high leverage can increase the vulnerability of the financial system, triggering systemic financial risks and severely threatening economic stability. Therefore, it is particularly important to reasonably regulate and supervise household debt levels. This is crucial for achieving “stable growth” and “risk prevention” and ensuring sustained and healthy economic development.

To mitigate household debt risks and achieve stable economic growth, the Chinese government has actively introduced regulatory policies. The report of the 20th National Congress of the Communist Party of China emphasized the importance of “maintaining the bottom line of preventing systemic risks.” In line with this, the People’s Bank of China released the “Macro-Prudential Policy Guidelines (Trial)” in 2022, which clarified the framework for “prudential regulation and behavioral regulation.” This framework provides robust policy support for creating a coordinated system aimed at preventing and resolving systemic financial risks. Based on liquidity preference theory and debt deflation theory, monetary policy affects household debt levels by altering market liquidity supply and asset values. Thus, monetary policy plays a crucial role in regulating household debt. Existing research has explored the relationship between monetary policy and household leverage, with findings showing that expansionary monetary policy can either increase household leverage (Jordà et al., 2015; Korinek & Simsek, 2016) or decrease it (Alpanda & Zubairy, 2017), and there is even the possibility of short-term increases followed by long-term decreases (Bauer & Granziera, 2017). Moreover, once the economic system enters a state of low or even zero interest rates, monetary policy may lose its influence on household leverage (Eggertsson & Krugman, 2012). Most existing studies analyze the impact of monetary policy on household leverage from a macro perspective and have not reached a consensus, highlighting the complexity of the relationship between monetary policy and household leverage. In light of this, the primary research question of this paper is to explore the impact of monetary policy on household leverage from a micro-household perspective and to understand the mechanisms through which monetary policy affects household leverage.

From an economic perspective, the relationship between monetary policy and household leverage originates from household participation in financial markets. Household financial decisions influence financial market equilibrium, thereby constraining the transmission of monetary policy. Conversely, monetary policy can affect household financial asset allocation by altering financial system liquidity, thus adjusting household borrowing incentives (Cloyne et al., 2020). This indicates that changes in the correlation between the two may stem from household financial decisions driven by financial literacy. It emphasizes the need for a dual-peak regulatory system that combines macroprudential and microbehavioral regulation, particularly amid ongoing leveraging. It also highlights the importance of financial literacy in monetary policy transmission (Lusardi et al., 2017). This paper examines not only the impact of monetary policy on household leverage but also the role of financial literacy in this process.

To address these questions, this paper uses mixed cross-sectional data from 2010 to 2017, based on the China Urban Household Consumption Financial Survey by the China Financial Research Center of Tsinghua University and the China Household Finance Survey (CHFS) by the Survey and Research Center for China Household Finance of Southwestern University of Finance and Economics. The results show that contractionary monetary policy exacerbates the rise in household leverage. Further mechanism analysis reveals that monetary policy affects household leverage through the “income effect,”“wealth effect,” and “substitution effect.” Additionally, this paper explores the role of financial literacy in the impact of monetary policy on household leverage, finding that low financial literacy amplifies the effect of contractionary monetary policy on leverage, while high financial literacy mitigates it. This demonstrates that exploring the relationship between monetary policy, financial literacy, and household leverage is not only theoretically significant but also helps achieve a long-term balance between risk prevention and stable growth in the era of high-quality development.

The innovations of this paper are primarily reflected in three aspects. First, using micro-level household debt data, it reveals the direct impact of monetary policy on household leverage and its mechanisms, thereby expanding research on this topic. This provides theoretical support for more precise monetary policy formulation. Existing studies largely rely on macro data and lack detailed micro-level data to explore specific household behaviors and their responses to policies. In particular, there is scarce research on the channels through which monetary policy affects household leverage. This paper analyzes how changes in monetary policy influence household leverage through the “income effect,”“wealth effect,” and “substitution effect,” providing more specific empirical evidence of the nuanced impact of monetary policy on household debt behavior.

Second, from the perspective of household financial literacy, this paper systematically explores for the first time the moderating role of financial literacy in the impact of monetary policy on household leverage. By innovatively incorporating financial literacy into the monetary policy transmission framework, it offers new perspectives and empirical evidence for monetary policy transmission theory. Traditional theories focus on interest rates, credit, and asset price channels. With the growing importance of financial literacy in individual financial decisions, current research mainly examines its direct impact on savings and investment, neglecting its potential role in the transmission of monetary policy. This paper empirically reveals that households with higher financial literacy can more effectively respond to monetary policy adjustments and optimize their debt structures. The analysis enriches the theoretical framework of the interaction between financial literacy and monetary policy, providing empirical support for enhancing financial literacy as a means to mitigate policy shocks.

Finally, by integrating behavioral economics and financial literacy theory, this paper provides a theoretical foundation for constructing a dual-peak regulatory system that combines macroprudential regulation with micro behavioral regulation. Previous studies lack systematic analysis of the role of financial literacy in behavioral regulation and fail to fully reveal its potential role in macroeconomic management. Traditional behavioral regulation focuses on standardizing the behavior of financial market participants, overlooking the significant impact of financial literacy on individual financial decisions and overall market stability. Using micro-level household data and econometric models, this paper examines the heterogeneous responses of households with different levels of financial literacy to changes in monetary policy. By incorporating financial literacy into the macroprudential and behavioral regulation framework, this paper offers theoretical support and empirical evidence for constructing a more comprehensive and effective dual-peak regulatory system.

The article is structured as follows: The second part is the literature review, the third part describes the data and econometric analysis model used, the fourth part verifies the impact of monetary policy on household leverage and analyzes the mechanism, the fifth part analyzes the impact of monetary policy on household leverage under the constraint of financial literacy, and the last part presents the conclusion and policy recommendations.

Literature Review

Factors Influencing Household Leverage

Household leverage, as a crucial indicator of household debt levels, is influenced by various factors, including the macroeconomic environment, financial market conditions, household income, and asset status. The macroeconomic environment, encompassing economic growth, inflation rates, and unemployment rates, significantly affects household borrowing behavior. Household leverage tends to rise during economic booms and fall during recessions (Aladangady, 2017; Mian & Sufi, 2018). Financial market conditions, including interest rates, credit supply, and financial innovations, directly impact borrowing costs and accessibility, with households more likely to increase debt in low-interest environments (Fuster et al., 2021; Justiniano et al., 2019). Household income levels and asset status also directly influence leverage, with higher-income and asset-wealthy households more likely to obtain credit and increase leverage (Di Maggio et al., 2020; Garriga et al., 2017). Additionally, financial literacy has garnered attention for its impact on household leverage, as financially literate households can manage debt more effectively, thereby reducing leverage (Lusardi & Mitchell, 2017). Future research should further explore the interactions among these factors and their policy implications to provide comprehensive theoretical support for household debt management and macroeconomic policy formulation.

Monetary Policy Transmission

Early research focused on traditional monetary policy transmission channels, such as the bank lending channel (Bernanke & Gertler, 1995) and the balance sheet channel (Kiyotaki & Moore, 1997). However, these studies often overlooked the heterogeneity of market participants. With the implementation of unconventional monetary policies like quantitative easing and forward guidance, research has shifted to examining monetary policy transmission from a liquidity perspective (Bianchi & Bigio, 2022; Di Tella, 2017). Macroeconomic policies, including monetary policy, influence liquidity premiums by adjusting the supply of liquid assets, thereby altering micro-level leverage behaviors and impacting the real economy, potentially accumulating risks (Gertler & Kiyotaki, 2015; Guerrieri & Lorenzoni, 2017).

Mechanisms of Monetary Policy Impact on Household Leverage

Existing literature indicates that monetary policy influences household borrowing behavior and leverage through multiple channels, including the “substitution effect,”“income effect,” and “wealth effect.” The contractionary monetary policy raises interest rates, increasing the cost of credit and reducing household borrowing (Cúrdia & Woodford, 2016; Korinek & Simsek, 2016). Additionally, contractionary policy suppresses aggregate demand, reducing household income and influencing borrowing behavior (Jeanne & Korinek, 2019; Kaplan et al., 2018). The wealth effect, based on Kiyotaki and Moore’s (1997) collateral mechanism, suggests that monetary policy affects asset prices, thereby impacting household net worth and borrowing capacity.

Financial Literacy in Monetary Policy Transmission

Financial literacy encompasses numerical computation ability (Banks & Oldfield, 2007; Lusardi & Mitchell, 2014), cognitive ability (Gerardi et al., 2010; Stango & Zinman, 2009), and financial knowledge (Lusardi et al., 2017), reflecting households’ comprehensive capability in financial planning, asset allocation, pension management, and debt decisions (Lusardi & Mitchell, 2014). While existing literature does not directly address the role of financial literacy in monetary policy transmission, similar concepts have been explored. Research by Sims (2003) highlights the significant impact of limited information processing capacity on monetary policy transmission, characterized by “rational inattention,” which can affect inflation expectations and consumption volatility, potentially leading to hump-shaped macroeconomic responses. Studies by Farhi and Werning (2019) and Gabaix (2020) further emphasize the importance of bounded rationality in explaining the effects of forward guidance and other monetary policies, noting that considering “cognitive discounting” can better explain financial crises and monetary policy impacts. Ignoring micro-level behavioral biases makes it difficult to explain the frequent occurrence of excessive credit expansion under tightened financial regulation. These studies underscore the importance of micro-level behavioral characteristics in monetary policy regulation, which can alter the effectiveness of classic monetary policy transmission mechanisms and potentially create new transmission pathways. Financial literacy, reflecting bounded rationality behaviors in behavioral macroeconomics, plays a crucial role in monetary policy transmission. Households’ financial literacy levels directly affect their response to and understanding of monetary policy. Financially literate households can more accurately predict the impact of monetary policy changes on their financial status, enabling them to make more rational financial decisions and ensure effective transmission and achievement of policy objectives.

Data Description and Model Specification

Data Source

The data for this study are sourced from two key surveys: the China Household Finance Survey (CHFS) by the Southwestern University of Finance and Economics and the Chinese Urban Household Consumption Finance Survey by the China Center for Financial Research (CCFR) at Tsinghua University. The Tsinghua University data assess household financial literacy based on individuals’ understanding of financial products across 24 provinces from 2010 to 2012. These provinces include Anhui, Gansu, Inner Mongolia, Beijing, Guangdong, Guangxi, Hainan, Jilin, Shandong, Yunnan, Henan, Jiangxi, Sichuan, Fujian, Shanghai, Liaoning, Shanxi, Xinjiang, Hubei, Shaanxi, Jiangsu, Heilongjiang, Chongqing, and Hunan.

Simultaneously, the Southwestern University of Finance and Economics data measure household financial literacy from three dimensions: interest rates, inflation, and risk perception, covering 29 provinces in 2013, 2015, and 2017 (Gan et al., 2013). These two datasets were combined to construct the pooled cross-sectional data used in this study, spanning the period from 2010 to 2017.

It is important to emphasize that, despite certain differences in the measurement of financial literacy in the aforementioned household micro-databases, interest rates and inflation directly affect the pricing of financial products, while risk perception determines households’ acceptance of specific financial products and influences their choice of financial product types. From the perspective of household micro-behaviors, the three aspects of interest rates, inflation, and risk perception—highlighted in the data from the Southwestern University of Finance and Economics—constitute important dimensions of households’ understanding of financial products. In other words, there is a close correlation between the financial literacy measured by the two sets of data. For data processing, we first conducted a 1% trimming on the data and removed samples with missing or abnormal values in key variables. Next, we standardized the quantified measures of financial literacy obtained from the two databases to ensure that the values were between 0 and 1. Through these procedures, not only could the financial literacy information implicit in the two databases be fully exploited, but also the financial literacy could be compared between the two databases. In addition, our analysis also involved regional variables represented by economic and openness levels, as well as national-level macro data represented by monetary policy and real estate prices. These data were obtained from the Wind database, CSMAR database, and the “China Statistical Yearbook,” respectively.

Model Specification and Variable Selection

The Intuitive Statistical Relationship Between Monetary Policy, Financial Literacy, and Household Leverage Ratio

Figure 1 illustrates the relationship between monetary policy, financial literacy, and household leverage. Figure 1a shows that under an expansionary monetary policy, an increase in the money supply leads to a decrease in household leverage. Conversely, Figure 1b indicates that under a contractionary monetary policy, rising interest rates lead to an increase in household leverage. Figure 1c reveals an inverted U-shaped relationship between financial literacy and household leverage. Research by Lusardi and Mitchell (2014) and Campbell (2006) highlights the dual impact of financial literacy on household financial decisions. Therefore, financial literacy may have a nonlinear effect on the relationship between monetary policy and household leverage. Enhancing financial literacy is crucial for households to better understand and respond to changes in monetary policy and to stabilize their leverage levels (Lusardi & Mitchell, 2017).

The relationship between monetary policy, financial literacy and household leverage ratio: (a) the relationship between money supply growth and household leverage, (b) the statistical relationship between the national bond repurchase rate and the leverage ratio of the household sector, and (c) household financial literacy and leverage ratio.

Model Construction

A Baseline Model to Characterize the Relationship Between Monetary Policy and Household Leverage

In general, monetary policy affects both the likelihood of households being in debt and the size of their debt. Therefore, the impact of monetary policy on household leverage is divided into two dimensions, namely the “intensive margin” (reflecting the impact of monetary policy on the leverage of individual households) and the “extensive margin” (showing the impact of monetary policy on the likelihood of household debt). The combination of these two dimensions reflects the overall impact of monetary policy on household leverage.

The rationale for studying both the extensive and intensive margins is as follows: Monetary policy adjustments directly affect borrowing costs and disposable income, thereby altering debt levels (intensive margin). Additionally, these adjustments influence the likelihood of households incurring debt by modifying credit availability and financial market risk preferences (Jappelli & Pagano, 1989; Kiyotaki & Moore, 1997; extensive margin). The combination of the two models can reveal the overall impact of monetary policy on household leverage ratio from both the depth and breadth of debt, thus assisting policymakers in gaining a more comprehensive understanding of policy implications and formulating more targeted policy interventions. Additionally, it can enhance the robustness of empirical results.

Given that many households in micro-level survey data have zero debt, a Tobit model is employed to estimate the following econometric model. The Tobit model is particularly suitable for this analysis because it accounts for the censored nature of the dependent variable, which is household leverage in this case (Tobin, 1958). This approach allows us to examine the impact of monetary policy shocks on the “intensive margin” of household leverage:

In Equation 1,

Since the “extended margin” reflects the possibility of household debt, we adopt the Probit model to analyze the impact of monetary policy on the household leverage ratio via the “extended margin.” The specific model is as follows:

where wdebt represents whether the household has debt. When the household has debt, wdebt = 1, otherwise, it equals 0.

Model Specification for the Impact Mechanism of Monetary Policy on Household Leverage

To verify the “income effect,”“wealth effect,” and “substitution effect” mechanisms in the impact of monetary policy on the leverage ratio, we construct the following mediation effect model for verification:

To test whether the explanatory variable

Variable Selection

Main Explained Variable: Household Leverage Ratio

We use the ratio of total debt to total assets to represent household leverage (K. Dynan & Edelberg, 2013). This ratio clearly reflects a household’s debt repayment capacity relative to its asset base and also indicates its debt risk, which is crucial for understanding financial risk and instability. In the real world, financial institutions determine loan amounts by assessing a household’s repayment capacity, and typically, the loan amount does not exceed the value of the household’s assets. Therefore, our study excludes samples where debt exceeds assets.

Core Variables

Monetary Policy

From an economic logic perspective, changes in household leverage are related to both the scale of credit and the assets or income they possess, both of which are influenced by monetary policy. Simultaneously, changes in leverage can impact the broader economy, thereby affecting monetary policy decisions. This could lead to a bidirectional causal relationship between monetary policy and household leverage. Therefore, before examining the impact of monetary policy on household leverage, it is essential to exclude endogenous variations from monetary policy measures and extract exogenous variations as monetary policy shocks (Chen et al., 2018; Cloyne et al., 2020). Regarding the identification of monetary policy shocks, Chen et al. (2018) introduced the Markov regime-switching model, considering the “stable growth” characteristic of China’s macroeconomic policies. Furthermore, in the context of China’s monetary policy practices, which include targets for economic growth, inflation, and money supply growth, we adopt the approach of Chen et al. (2018) to estimate both quantitative and price-based monetary policy shocks.

Financial Literacy

Financial literacy is a micro feature variable that reflects households’ comprehensive financial decision-making ability (Lusardi et al., 2017; Lusardi & Mitchell, 2014). Previous research has generally assessed respondents’ financial literacy by posing a series of financial knowledge questions. By assessing respondents’ answers to financial knowledge questions using factor analysis or scoring methods, a quantitative measure of financial literacy is obtained. However, because the financial knowledge survey questionnaire is highly subjective, it may reflect not only respondents’ mastery and understanding of financial knowledge but also their subjective emotions and cognition. If the latter factors are more prominent, it may lead to biased empirical analysis. Therefore, this paper used the factor analysis method to extract the most critical information about respondents’ answers to financial knowledge questions in the survey questionnaire and remove impurities, achieving a relatively objective characterization of financial literacy. The simple scoring method based on the survey questionnaire lacks the previously mentioned advantages. In the data released by Tsinghua University, the understanding of financial products by individuals is primarily used to measure household financial literacy. In the data of Southwest University of Finance and Economics, micro individuals’ understanding of interest rates, inflation, and risk awareness characterizes household financial literacy, and the measured financial literacy is normalized for comparability.

Mediating Variables

According to previous studies, monetary policy affects household leverage through the “income effect,”“wealth effect,” and “substitution effect” (Cúrdia & Woodford, 2016; Jeanne & Korinek, 2019; Kaplan et al., 2018; Korinek & Simsek, 2016). To measure the income effect, this paper employs the growth rate of disposable income at the provincial level as the mediator variable. To measure the wealth effect, the growth rate of housing prices in each province is used as the mediator variable. To measure the substitution effect, this paper adopts the ideas of Auclert (2019) and Slacalek et al. (2020) and uses household savings plus matured assets minus matured liabilities as the mediator variable. Due to data limitations, this paper uses the sum of household savings and net assets to represent the substitution effect, which can still reflect the impact of annual monetary policy changes on household behavior.

Control Variables

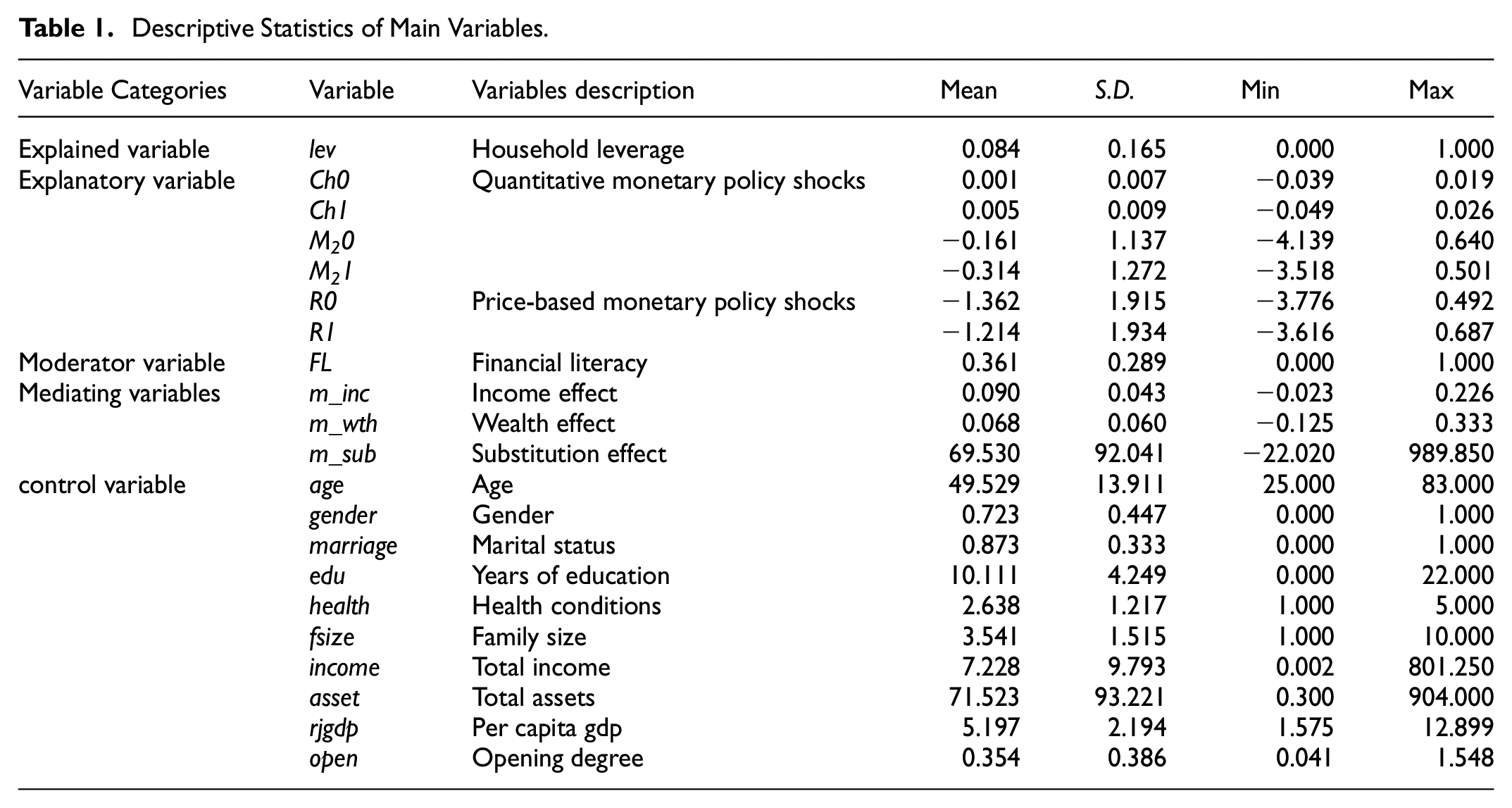

The selection of control variables considers both micro and macro levels. At the micro level, we include demographic factors such as gender, age, marital status, and education, which significantly influence financial decision-making and risk preferences (Croson & Gneezy, 2009). We also incorporate household characteristics like size, health status, total assets, and income, reflecting financial capacity and needs—key determinants of borrowing behavior (K. E. Dynan & Kohn, 2007). At the macro level, per capita GDP and economic openness represent the city’s economic environment. Per capita GDP indicates economic development and credit access (Rajan & Zingales, 1998), while economic openness reflects market integration and potential exposure to external shocks, influencing leverage decisions (Lane & Milesi-Ferretti, 2007). This comprehensive framework analyzes household debt leverage, highlighting the interplay between individual decisions and broader economic factors. Table 1 shows the measurement and descriptive statistics of the main variables.

Descriptive Statistics of Main Variables.

The Influence and Mechanism of Monetary Policy on Household Leverage

The Impact of Monetary Policy Shocks on the Household Leverage Ratio

As an external environmental factor, monetary policy changes significantly affect household leverage. The impact of monetary policy on household leverage can be categorized into two dimensions: the “intensive margin” and the “extensive margin.” The former dimension reflects the effect of monetary policy on the leverage of individual households, while the latter shows its effect on the likelihood of household indebtedness. The sum of these two effects represents the overall impact of monetary policy on household leverage.

The results presented in Table 2 demonstrate the estimated impacts of monetary policy shocks on the “intensive margin” of household leverage using the Tobit model. Specifically, Columns (1) to (4) show the estimated impacts of quantitative monetary policy shocks on leverage, while Columns (5) and (6) present the impacts of price-based monetary policy shocks. Each column incorporates controls for householder characteristics, household features, as well as regional characteristics, while also accounting for temporal and regional fixed effects. Column (1) reveals a significantly negative coefficient for quantitative monetary policy shocks (coefficient = −2.1968, standard error = 0.5444), indicating that a loose monetary policy significantly reduces household leverage. At the same time, the size of the coefficient also means that for every unit increase in the quantitative monetary policy shock, the potential household leverage ratio decreases by 2.1968 units. The remaining results for quantitative monetary policy shocks are similar to Column (1). Column (5) demonstrates a significantly positive coefficient for price-based monetary policy shocks (coefficient = .1913, standard error = 0.0474), suggesting that a tightening monetary policy significantly increases household leverage, possibly due to the increased debt costs in a high-interest environment, making it more difficult for households to repay debts, thus leading to an accumulation of debt and an increase in leverage. Overall, regardless of whether quantitative or price-based monetary policy tools are employed, a loose monetary policy (increased money supply growth or interest rate cuts) significantly reduces household leverage, while a tightening monetary policy significantly increases it (Alpanda & Zubairy, 2017; Di Maggio et al., 2017).

The “Intensive Margin” of the Impact of Monetary Policy on Leverage.

Note. Robust standard errors are in parentheses, *, **, *** indicate significance at the 10%, 5%, and 1% levels, respectively.

These findings provide important policy insights for monetary policymakers. In the current global economic environment, where uncertainty and economic fluctuations are frequent, accommodative monetary policy can reduce borrowing costs, alleviate household debt pressures, and thereby reduce household leverage (Gertler & Karadi, 2015). This is especially important during economic recovery periods, as it can stimulate consumption and investment, driving economic growth (Jordà et al., 2015). Conversely, restrictive monetary policy may exacerbate household debt burdens, leading to declines in consumption and investment, thus inhibiting economic activity. Therefore, a cautious balance is necessary during policy implementation (Ramey, 2016). Understanding the impact of monetary policy on household leverage at the intensive margin not only helps evaluate the effectiveness of monetary policy measures but also aids in formulating more effective and comprehensive economic policies to promote long-term economic stability and sustainable growth.

Table 3 presents the impact of monetary policy shocks on the “extensive margin” of household leverage, estimated using the Probit model. Similar to the findings in Table 2, the results demonstrate that quantity-based monetary policy shocks have a significantly negative impact on the leverage rate on the “extensive margin,” while price-based monetary policy shocks have a significantly positive impact. Overall, both quantity-based and price-based monetary policy tools indicate that loose monetary policy reduces the likelihood of household debt, while tight monetary policy increases it. These results suggest that monetary policy can influence the probability of household indebtedness.

The “Extended Margin” of the Impact of Monetary Policy on Leverage.

Note. Robust standard errors are in parentheses, *, **, *** indicate significance at the 10%, 5%, and 1% levels, respectively. Table 3 reports the marginal coefficients estimated by the probit model.

Analysis of the Mechanism of Monetary Policy on Household Leverage

As an important external environmental factor for households, changes in monetary policy can influence the household leverage rate. In the framework of heterogeneous individual models, the impact of monetary policy on the household leverage rate typically arises from the “income effect,”“wealth effect,” and “substitution effect” (Cúrdia & Woodford, 2016; Jeanne & Korinek, 2019; Kaplan et al., 2018; Korinek & Simsek, 2016). The income effect is expected to reduce the household leverage rate when monetary policy is loose, as the growth rate of household disposable income increases, it becomes less likely for households to resort to debt as a means of increasing liquidity. Similarly, the wealth effect reduces the leverage when monetary policy is loose, as the growth rate of housing prices increases and the overall level of household housing wealth increases. For substitution effects, when monetary policy is loose, the substitution effect represented by the sum of savings and net assets increases, which means that the debt scale relatively decreases, resulting in a decrease in household leverage.

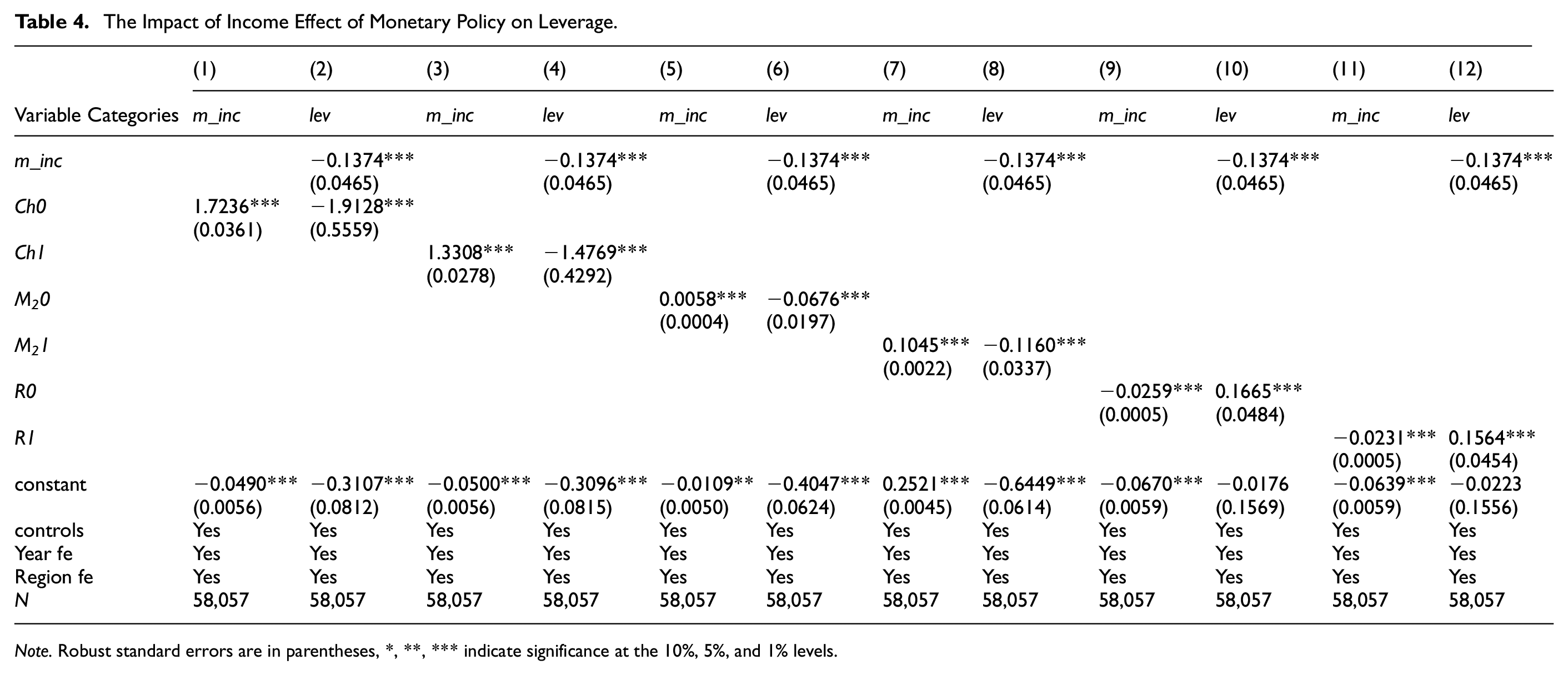

Table 4 presents the impact of the “income effect” of monetary policy on leverage. In column (1) of Table 4, the coefficient of the quantity-type monetary policy shock (Ch0) is significantly positive (coefficient = 1.7236, standard error = 0.0361), indicating that loose monetary policy shock significantly increases the disposable income of residents’ households. The magnitude of the coefficient also suggests that for every 1 -unit increase in quantitative monetary policy shock, the potential income effect increases by 1.7236 units. In column (2), the coefficient of the “income effect” is significantly negative (coefficient = −.1374, standard error = 0.0465), indicating that increasing the “income effect” decreases the household leverage, thus verifying the previous hypothesis. This finding aligns with the results of Andersen et al. (2023), indicating that accommodative monetary policy can increase household disposable income. Columns (3) to (8) obtain consistent results using other measured quantity-type monetary policy tools. In column (9), the coefficient of price-type monetary policy shock (R0) is significantly negative (coefficient = −.0259, standard error = 0.0005), indicating that contractionary monetary policy significantly reduces the disposable income of households. In column (10), the coefficient of the “income effect” is significantly negative (coefficient = −.1374, standard error = 0.0465), indicating that increasing the “income effect” decreases the household leverage, again verifying the previous hypothesis. Columns (11) to (12) obtain consistent results for other price-type monetary policy shocks. Results show that quantity-type monetary policy (Ch0, Ch1, M20, and M21) has a significant positive effect on the income effect, while price-type monetary policy (R0 and R1) has a significant negative effect on the income effect. This indicates that loose monetary policy enhances the “income effect” of monetary policy, regardless of whether it is price-type or quantity-type monetary policy. Overall, the income effect has a negative impact on the leverage rate, which is consistent with expectations that loose monetary policy reduces the household leverage rate by enhancing the income effect.

The Impact of Income Effect of Monetary Policy on Leverage.

Note. Robust standard errors are in parentheses, *, **, *** indicate significance at the 10%, 5%, and 1% levels.

These results have significant practical implications. Particularly during economic downturns, expansionary monetary policy can increase household disposable income, alleviate debt pressure, and promote consumption and economic recovery. At the same time, it helps maintain household financial health, reducing the financial risks associated with high debt levels, and thereby promoting overall economic stability. Finally, these findings reveal that policymakers can flexibly use monetary policy tools to balance controlling inflation and reducing household debt risks, thereby addressing economic fluctuations and maintaining financial stability.

Table 5 presents the impact of the “wealth effect” of monetary policy on leverage. In column (1), a significantly positive coefficient of the quantitative monetary policy shock (Ch0) indicates that the loose monetary policy shock significantly stimulates household wealth appreciation (coefficient = 2.0876, standard error = 0.0605). In column (2), a significantly negative coefficient of the “wealth effect” confirms the previous hypothesis that the appreciation of household wealth through the “wealth effect” reduces household leverage (coefficient = −.0914, standard error = 0.0377). This is similar to the findings of Albert et al. (2020), who argue that expansionary monetary policy leads to an increase in overall wealth effects and exacerbates wealth inequality among households with different investment portfolios. Columns (3) to (8) exhibit consistent results using other measured quantitative monetary policy tools. In column (9), a significantly negative coefficient of the price monetary policy shock (R0) suggests that the contractionary monetary policy significantly decreases household wealth appreciation (coefficient = −.0533, standard error = 0.0009). In column (10), a significantly negative coefficient of the “wealth effect” confirms the previous hypothesis that increasing the “wealth effect” reduces household leverage (coefficient = −.0914, standard error = 0.0377). Other price monetary policy shocks in columns (11) to (12) lead to consistent results. Overall, it can be observed that quantitative monetary policy (Ch0, Ch1, M20, and M21) has a significant positive impact on the “wealth effect,” whereas price monetary policy (R0 and R1) has a significant negative impact on the “wealth effect,” explaining how loose monetary policy enhances the “wealth effect” of monetary policy. Furthermore, whether it is price or quantity monetary policy, the “wealth effect” negatively affects the leverage, consistent with the expectation that loose monetary policy reduces household leverage by enhancing the “wealth effect.”

The Impact of Wealth Effect of Monetary Policy on Leverage.

Note. Robust standard errors are in parentheses, *, **, *** indicate significance at the 10%, 5%, and 1% levels.

These findings delineate the impact of monetary policy shocks on household leverage through the wealth effect, providing insights into how such policies influence debt behavior via property values. Expansionary measures drive up asset prices, thereby increasing household wealth and improving consumption and investment prospects. Conversely, contractionary measures diminish wealth accumulation, emphasizing the necessity for a thorough assessment of their implications for household wealth and leverage.

Table 6 presents the impact of the “substitution effect” of monetary policy on leverage. In column (1), the coefficient of the quantity-based monetary policy shock (Ch0) is significantly positive (coefficient = 107.2031, standard error = 14.5210), indicating that a loose monetary policy shock significantly increases the household’s substitution effect. In column (2), the coefficient of the “substitution effect” is significantly negative (coefficient = −.0095, standard error = 0.0002), indicating that household leverage is reduced through the “substitution effect,” confirming the previous hypothesis. Consistent results are obtained in columns (3) to (8) using other measured quantity-based monetary policy tools. This is similar to the findings of Auclert (2019), where monetary policy affects household consumption behavior through the redistribution of income and wealth, with the substitution effect being a key mechanism. In column (9), the coefficient of the price-based monetary policy shock (R0) is significantly negative (coefficient = −2.4034, standard error = 0.2016), indicating that contractionary monetary policy significantly reduces the household’s substitution effect. In column (10), the coefficient of the “substitution effect” is significantly negative, indicating that the household’s leverage is reduced by increasing the “substitution effect,” confirming the previous hypothesis. Consistent results are obtained for other price-based monetary policy shocks in columns (11) to (12). Overall, it can be observed that quantity-based monetary policy (Ch0, Ch1, M20, and M21) has a significant positive impact on the substitution effect, while price-based monetary policy (R0 and R1) has a significant negative impact on the substitution effect. This finding explains how loose monetary policy enhances the “substitution effect” of monetary policy. Furthermore, regardless of whether it is a price-based or quantity-based monetary policy, the substitution effect has a negative impact on the leverage, which is consistent with the expected results in the previous text. In other words, loose monetary policy reduces household leverage by enhancing the substitution effect.

The Impact of Substitution Effect of Monetary Policy on Leverage.

Note. Robust standard errors are in parentheses, *, **, *** indicate significance at the 10%, 5%, and 1% levels.

These results have significant practical implications, underscoring the importance of intertemporal substitution in monetary policy regulation. Financial institutions should consider the impact of monetary policy on household intertemporal consumption when providing loans to more accurately assess household loan risks. Additionally, financial markets should adjust their products and services in response to changes in monetary policy to meet household consumption needs in different economic environments.

The Role of Financial Literacy in the Impact of Monetary Policy on Household Leverage

Monetary policy shocks significantly impact household leverage, and financial literacy, as a crucial behavioral trait at the micro level, may influence the transmission of monetary policy. Accordingly, this paper will analyze the effect of monetary policy on household leverage, incorporating financial literacy as a moderating variable to precisely delineate how differences in financial literacy affect monetary policy transmission.

Consistent with the prior analysis, the following discussion will unveil the role of financial literacy in the transmission of monetary policy from two dimensions: “intensive margin” and “extensive margin.” Firstly, dummy variables FZq are introduced to represent changes in financial literacy, where q denotes the percentile position of financial literacy. FZ1 equals 1 when financial literacy is in the 0% to 30% percentile, and 0 otherwise; FZ2 equals 1 when financial literacy is in the 30% to 40% percentile, and 0 otherwise; FZ3 equals 1 when financial literacy is in the 60% to 70% percentile, and 0 otherwise; FZ4 equals 1 when financial literacy is in the 70% to 100% percentile and 0 otherwise. Meanwhile, the sample with financial literacy in the 40% to 60% percentile is used as the control group to better distinguish high and low levels of financial literacy. Secondly, monetary policy (

Where (5) corresponds to intensive margin and (6) corresponds to extensive margin.

Table 7 provides insights into the “intensive margin” of the impact of monetary policy on household leverage. When the monetary policy tool is quantity-based, a significantly negative coefficient

The Impact of Financial Literacy on the “Intensive Margin” of Household Leverage.

Note. Robust standard errors are in parentheses, *, **, *** indicate significance at the 10%, 5%, and 1% levels.

Cross-multiplication coefficient of Table 7: (a) quantitative monetary policy estimation and (b) price-based monetary policy estimation.

Table 8 shows that similar to the “intensive margin” of monetary policy’s impact on household leverage, changes in financial literacy affect the “extensive margin” of this impact. Specifically, low financial literacy amplifies the positive impact of contractionary monetary policy on debt probability, while high financial literacy weakens this impact, regardless of the monetary policy tool used for verification. Figure 3 illustrates the main results from Table 8.

Cross-multiplication coefficient of Table 8: (a) quantitative monetary policy estimation and (b) price-based monetary policy estimation.

The Impact of Financial Literacy on the “extended Margin” of Household Leverage.

Note. Robust standard errors are in parentheses, *, **, *** indicate significance at the 10%, 5%, and 1% levels.

The findings suggest that variations in household financial literacy can alter the transmission of monetary policy, resulting in changes to its impact on household leverage. Low financial literacy not only enhances the impact of monetary policy on household leverage from an “intensive margin” perspective but also from an “extensive margin” perspective. Conversely, high financial literacy weakens the impact of monetary policy on household leverage. As such, low financial literacy serves as an “amplifier” of the impact of monetary policy on household leverage, whereas high financial literacy weakens its impact. Previous research has primarily focused on the impact of financial literacy on individual financial decision-making. Lusardi and Mitchell (2014) found that individuals with high financial literacy are better at planning savings and investments and avoiding excessive debt. The findings highlight the crucial role of financial literacy in the transmission of monetary policy, establishing it as a key bridge connecting macroeconomic policy and micro-level household financial behavior.

The potential reasons for the aforementioned findings are as follows: households with low financial literacy typically lack the necessary financial knowledge and skills to effectively cope with the increased borrowing costs due to rising interest rates. Consequently, they may continue borrowing to maintain their consumption levels, leading to higher leverage. Additionally, these households are more driven by short-term consumption needs and lack long-term financial planning capabilities, making them more susceptible to financial distress under tight monetary policy. In contrast, households with high financial literacy exhibit stronger financial planning abilities, allowing them to flexibly adjust their consumption and investment behaviors in response to monetary policy changes, thereby mitigating the impact of tight monetary policy on leverage. When interest rates rise, they tend to reduce non-essential consumption, increase savings, or invest in high-yield financial products to offset the increased borrowing costs. These behaviors not only help maintain household financial stability but also alleviate the impact of economic fluctuations on household finances to some extent.

Main Conclusions and Policy Recommendations

The rapid rise in household leverage in China has led to potential financial stress, increased credit risk, and threatened socio-economic stability. As a key macroeconomic tool, monetary policy is continuously evolving to enhance its ability to prevent and mitigate systemic risks, thereby regulating household debt levels. However, the effectiveness of this regulation varies significantly with household financial literacy. Based on micro-level household financial data in China, this paper explores the impact of monetary policy on household leverage and its underlying mechanisms, with a focus on the critical role of financial literacy in the transmission of monetary policy. The findings show that expansionary monetary policy helps reduce household leverage, while contractionary monetary policy leads to an increase. Monetary policy affects household leverage through “income effect,”“wealth effect,” and “substitution effect.” Notably, low financial literacy amplifies the impact of contractionary monetary policy on leverage, whereas high financial literacy mitigates this effect.

Based on these findings, this paper proposes the following policy recommendations to effectively manage household leverage in China, optimize the transmission mechanism of monetary policy, and enhance household financial literacy to better prevent and mitigate systemic risks, thereby maintaining macroeconomic stability.

First, strengthen financial regulation and risk warning systems. The government should establish a multi-level risk management system for household debt, covering debt monitoring, risk warning, and emergency response. Special attention should be given to dynamically monitoring high-leverage households and implementing differentiated risk control measures based on varying levels of financial literacy to prevent systemic risks arising from monetary policy adjustments. For households with lower financial literacy, more explicit credit conditions and support should be provided to alleviate their financial stress.

Second, optimize the design of monetary policy transmission. During the formulation and implementation of monetary policy, the heterogeneous responses of households with different levels of financial literacy should be fully considered to optimize the transmission pathways of monetary policy, balancing risk control and household financial stability. Implement differentiated transmission strategies, such as providing more specific and intuitive financial education and consulting services for households with lower financial literacy, to enhance their sensitivity and adaptability to monetary policy changes, thereby reducing policy distortions. For households with higher financial literacy, more conventional monetary policy adjustments can be applied to promote autonomous financial structure adjustments in response to policy changes.

Third, promote multi-level financial product supply. Financial institutions should develop and promote financial products tailored to different levels of financial literacy. For households with lower financial literacy, design simple and easy-to-understand savings and investment products with low usage thresholds. For households with higher financial literacy, offer diversified and high-yield investment options to help optimize asset allocation. The innovation and dissemination of financial products, enhance households’ ability to cope with monetary policy changes and reduce overall debt risk.

Finally, deepen the promotion of financial education. The government should collaborate with financial institutions and community organizations to strengthen the dissemination and deepening of financial literacy education. Develop long-term educational plans and use a combination of online and offline methods to teach households basic financial knowledge, risk management skills, and financial planning methods. Tailor educational programs to different age groups, income levels, and regions to ensure comprehensive and effective financial literacy education.

This study has several limitations. Despite our efforts to obtain the latest household data, the sample period remains limited, hindering our ability to estimate the impact of short-term adaptive adjustments by households on future outcomes. Future research should utilize updated data for longer-term studies. Additionally, financial literacy, being a multidimensional concept, presents challenges in measurement. The tools and indicators used in this study may not fully capture the breadth of individuals’ financial knowledge and behavior across different contexts. Future research could benefit from developing more comprehensive indicators to refine the analysis further. Additionally, there are other avenues of exploration, such as examining the manifestations and impacts of financial behavior across diverse cultural and economic systems. Furthermore, researching how fintech influences household financial literacy and behavior, particularly its potential in offering personalized financial education and enhancing accessibility to financial services, offers a more profound and comprehensive perspective on understanding family financial behaviors.

Footnotes

Ethical Considerations

All procedures performed in this study were in accordance with the ethical standards of the university.

Informed Consent

Informed consent was obtained from all participants.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability

All data used in this study have been made publicly available either within the article or in the supplementary materials. The micro-level household data in the original dataset are sourced from https://www.weiyangx.com/jtxfjrsj. The city-level data are obtained from ![]() . All these data are publicly accessible.

. All these data are publicly accessible.