Abstract

This study aims to explore the role of financial literacy in determining financial well-being during COVID-19. Additionally, we plan to examine how risk tolerance mediates between financial literacy and overall well-being. The data of 367 active individual investors on the Pakistan Stock Exchange was taken utilizing convenience sampling and the survey methodology. The relationship between financial literacy, risk tolerance, and financial well-being was investigated using structural equation modeling. The data were analyzed through Smart PLS. The finding of the study highlights that both advance and basic financial literacy have a positive and significant association with investor well-being. Furthermore, financial literacy has a favorable indirect impact on financial well-being highlighted in this study through risk tolerance. The effect of financial literacy on financial well-being was remarkably consistent across levels of demographic variables such as education, gender and age suggesting that improving financial literacy levels in the population may be an effective strategy to increase financial capability across the board during the COVID-19 crisis. The outcome of the study has several policy implications for investors and policymakers during uncertain times such as COVID-19, as providing literacy positively contributes to their risk tolerance which then translates into higher financial well-being. The paper’s novelty is that the authors have explored the mechanism by which basic and advanced levels of financial literacy influence investors’ risk tolerance and financial well-being during the COVID-19 pandemic in an emerging economy. It adds to the literature in behavioral finance, explicitly probing the impact of financial literacy on financial well-being; this field is in its initial stage, even in developed countries, while little work has been done in emerging countries.

Keywords

Introduction

Divergences in the proclivity of financial planning continue to be attributed to disparities in the subjective financial well-being of households. Household financial planning is a comprehensive evaluation of a family’s current and prospective financial situation. Effective household financial planning results in positive outcomes such as sustaining short- and long-term financial well-being. Financial well-being is defined as the perceived ability of individuals to oblige their liabilities and effectively achieve their future financial goals without anxiety and discomfort (Lusardi & Mitchell, 2007). Therefore, effective financial well-being remains integral for households and essential to sustain the well-being of the whole society (Arpana & Swapna, 2020). The recent financial crises highlighted the perils that households often make inefficient allocations of their resources and remain unable to understand the complexity of financial products. As a result, scholars, businesses, organizations, and governments are increasingly focused on improving individuals’ ability to make successful decisions about the mobilization of their savings and efficient allocation of their resources to sustain their financial well-being (Lusardi & Mitchell, 2007). Households’ current and future financial condition largely reflect their financial behavior based on their subjective knowledge. Financial knowledge, that is, financial literacy, which includes basic financial concepts such as interest, inflation, and the time value of money (Lusardi & Mitchell, 2011), is often directly associated with higher levels of financial well-being.

Financial literacy, which encompasses an understanding of fundamental financial concepts such as interest, inflation, time value of money, and investment basics, largely determines the level of households’ effective financial planning which, in turn, affects their financial well-being. Policymakers are concerned that a sizable proportion of households lacks fundamental financial knowledge and money management skills, which remain necessary to safeguard and increase their financial well-being (Falahati & Paim, 2011). Financial literacy has evolved into a necessary ability for households to meet their financial challenges effectively. Because of the instability in the global economy, households face financial decisions that have become more complex due to the increased complexity of financial products and challenges. Past studies extend the notion that planning leads to wealth maximization and financial well-being. However, planning without relevant knowledge and skill remains flimsy and nonproductive (Muhammad et al., 2022; Tan & Singaravelloo, 2020).

Financial literacy refers to the capacity of individuals to comprehend and proficiently apply a range of financial skills, encompassing the management of personal finances, the creation and adherence to budgets, and the art of investing. The importance of this study stems from various factors

The study aims to explore the impact of financial literacy on individuals’ ability to achieve their financial well-being. Financial literacy is the knowledge and understanding of financial concepts and skills necessary to make informed and rational decisions about personal finances. Financial literacy is seen as a protective factor against financial fraud, a crime involving deceiving individuals for monetary gain (Gignac et al., 2023). Furthermore, the study acknowledges the role of financial literacy in preparing individuals for emergencies, such as job loss or unexpected expenses, by equipping them with the necessary skills to save and manage their money effectively (Anshika & Singla, 2022). Accordingly, financial literacy improves individuals’ confidence and overall well-being, as it empowers them to make informed financial decisions and navigate the complexities of personal finance with greater ease.

The significance of financial literacy cannot be overstated, as it is a topic that requires ongoing learning and understanding. The acquisition and application of diverse financial skills and concepts is a continuous and enduring process throughout one’s life. Improving one’s financial literacy is a crucial aspect of personal finance management. Various methods can be employed to enhance financial literacy, such as engaging in extensive reading of books, actively listening to informative podcasts, subscribing to reliable financial content sources, or seeking guidance from qualified financial professionals (Hwang & Park, 2023). These approaches provide individuals with valuable insights and knowledge necessary for making informed financial decisions and achieving long-term financial well-being. In addition to traditional learning methods, individuals can leverage online resources to enhance their financial literacy.

The significance of financial literacy extends beyond the individual level, encompassing the broader societal and economic dimensions. The level of financial literacy among individuals has been found to have a significant impact on a country’s economic growth, stability, and innovation. When individuals possess a strong understanding of financial concepts and can effectively manage their finances, they are more likely to make informed decisions that positively contribute to the overall economic well-being of their nation. This increased financial literacy empowers individuals to engage in investing, entrepreneurship, and responsible borrowing, stimulating economic growth and innovation. Additionally, financially literate individuals are better equipped to navigate economic uncertainties and make sound financial choices, thereby promoting economic stability at both the individual and national levels (Basha et al., 2023; Umar et al., 2021; Yousaf & Ali, 2021). Therefore, enhancing financial literacy among the population emerges as a crucial factor in fostering economic development, stability, and innovation within a country. The study aims to investigate the potential correlation between certain factors and individuals’ reduced reliance on social welfare programs, as well as their decreased likelihood of becoming a financial burden on public finances.

Financial literacy is widely recognized as a crucial skill that individuals should actively seek to attain and enhance. The importance of financial planning cannot be overstated, as it plays a crucial role in helping individuals achieve their personal and professional goals. By carefully managing their finances, individuals can safeguard themselves from potential financial risks and uncertainties that may arise (Naveed et al., 2023). Moreover, effective financial planning can significantly enhance one’s overall quality of life, providing security and stability.

Households with a high level of financial awareness remain able to make sound asset allocation decisions. Additionally, financial literacy fosters a positive financial attitude, which results in financial well-being. Financial literacy is critical for making informed financial decisions and is necessary for financial well-being. Moreover, a higher level of financial literacy is linked with more rational behavior. Households with a lower level of financial knowledge exhibit poor financial planning and have low financial well-being (Ahah et al., 2021). Financial literacy remains essential to analyze and understand financial alternatives and plan for the future to respond to profitable investment opportunities effectively. However, despite the significance of financial literacy, past research has shown that the level of financial literacy around the world, particularly in developing and underdeveloped countries remains minimal (Muhammad et al., 2022). Besides efficiently allocating resources, households’ financial literacy remains critical in determining their willingness to accept the risks connected with financial investing. According to Almenberg and Dreber (2015), If households do not understand the fundamentals of an investment opportunity, they remain hesitant to participate. Similarly, Investors with financial understanding and knowledge have higher risk tolerance levels (Lusardi & Mitchell, 2014).

Despite the proliferation of research on the relationship between “financial literacy” and financial well-being, there is no universally accepted definition of financial literacy, and current measures of financial literacy have not been empirically validated as causal predictors of subsequent financial well-being or financial behavior. Additionally, no such evidence examines the role of basic and advanced financial literacy in predicting households’ current and future financial well-being (Andreou & Philip, 2018).

The influence of financial literacy on one’s financial well-being is a topic of considerable importance. By equipping individuals with the necessary knowledge and skills, financial literacy enables them to make informed and astute financial choices. This ability to make sound decisions has far-reaching implications for their financial health and stability. The present study examines the impact of financial literacy on various aspects of personal finance, including budgeting, debt management, saving and investing, and retirement planning. It is widely acknowledged that individuals with a higher level of financial literacy possess the necessary knowledge and skills to make informed decisions in these areas (Setiyani & Solichatun, 2019). By effectively budgeting their income, individuals can allocate resources wisely and optimize their financial situation. Furthermore, a strong understanding of debt management allows individuals to navigate the complexities of borrowing, ensuring that they can effectively manage their debts and avoid financial pitfalls. Additionally, individuals with a higher level of financial literacy are more likely to engage in strategic saving and investing practices, leading to long-term wealth accumulation and financial growth (Lusardi & Mitchell, 2007). Lastly, individuals with a solid understanding of retirement planning are better equipped to make informed decisions about their future financial security, ensuring a comfortable and satisfying retirement.

However, according to statistics such as the Consumer Financial Protection Bureau (CFPB), 2023 released a report on the financial well-being of Hispanics in 2018, which showed that Hispanic adults had an average financial well-being score of 48, compared to 54 for the US adult population. Accordingly, another survey conducted online in the United Kingdom between 18th and 20th March 2020, at the onset of the COVID-19 outbreak approached 1,000 respondents, with a mean age of 36 years, 55.3% of them female, and 54.3% with at least a university degree. Based on the survey results, In the UK, 4 in 7 people are financially illiterate. It is estimated that about 78% of Americans live paycheck to paycheck. The report shows that people are very pessimistic about the economic outlook for the future due to the COVID-19 pandemic. However, they are less pessimistic about their private economic situation compared to the national and global economy. Therefore, considering the rapidly growing significance of financial literacy in navigating households’ financial behavior, this study aims to achieve two main objectives. Firstly, it seeks to investigate the role of financial literacy in determining financial well-being during the COVID-19 pandemic. Secondly, the study explores the mediating role of risk tolerance in the relationship between financial literacy and financial well-being. The objective is to examine how risk tolerance acts as a mechanism through which financial literacy influences an individual’s overall financial well-being during times of uncertainty, such as the COVID-19 crisis. More specifically, we aim to respond to multiple research questions such as how financial literacy relates to individual investors’ financial well-being during the COVID-19 pandemic. We also examine to what extent risk tolerance mediates the relationship between financial literacy and overall financial well-being in the context of emerging economies facing uncertainty like the COVID-19 crisis.

Financial literacy is attributed to sound consumer financial planning and enables them to make wise allocations of their resources. Likewise, investors with sound financial literacy may have an edge in effectively understanding the perceived meaning of corporate signals. Also, with requisite financial literacy investors may be able to manage their financial well-being effectively (Allgood & Walstad, 2016). Financial literacy may function as a crucial determinant of financial well-being which in turn affects investors’ behavior (Brüggen et al., 2017). In March 2020, the economic catastrophe induced by the COVID-19 epidemic caused the global financial markets to lose around $20 trillion. Accordingly, the effect of COVID-19 hit the economy of Pakistan severely, and the KSE-100 Index of the Pakistani Stock Exchange fell by over 25% in March 2021, while the currency fell by over 6%. As a result of the lockdown imposed on the country, disruptions in trade, a probable decline in remittances, and fluctuations in other sectors of the economy such as tourism and hospitality are estimated to cost Pakistan’s economy up to 4% of its GDP. The economic downturn has had a profound influence on people’s financial status. People are less risk-tolerant, more financially vulnerable, and ill-equipped to deal with financial shocks. Thus, individuals may become financially vulnerable and unable to pay substantial future expenses (Lusardi et al., 2011)

While there have been many studies in the literature on the determinants of well-being, only limited empirical investigations have been dedicated to the subjective well-being of households. Likewise, past studies also used objective measures of well-being instead of subjective well-being. The most recent study proclaimed that subjective well-being is more effective in measuring one’s responses about the quality of life and satisfaction. Well-being as a self-centric construct should contain the household response rather than objective responses (Mahendru, 2021). Likewise, the level of education also remains divergent in different geographies of the world. Recent studies have overlooked investor and their perceived financial well-being (Mahendru, 2021). Individual investors have a low level of risk tolerance as compared to institutional investors due to limited resources. Therefore, individual investors do not participate in stock trading. There is evidence that posits that households’ low stock market participation is due to their low level of risk tolerance and low level of financial knowledge since financial markets are subject to uncertainty rather than risk alone; therefore, household due to limited knowledge remain to abstain from risky investment opportunities (S. Ali et al., 2022; Manjunath & Bankar, 2021; Yousaf & Ali, 2020). Literature on stock market investment remains limited to shedding light on individual investor trading behavior and its nexus with their financial well-being. Considering the aforementioned factors, it is impossible to generalize the findings of a study undertaken in developed countries in the context of developing economies like Pakistan. Therefore, this study aims to understand how financial literacy remains pragmatic in predicting individual investors’ financial well-being (Manjunath & Bankar, 2021).

Financial literacy is the capacity to comprehend fundamental financial principles and make prudent financial decisions. Financial literacy is a vital skill for making rational financial decisions that benefit consumers. Past studies on financial literacy have investigated how it contributes to the wise allocation of resources to maximize returns and minimize risk (S. Ali et al., 2022, 2023, 2024). Among these outcomes are enhanced retirement planning and savings (Lusardi & Mitchell, 2014), risk-taking behavior (van Rooij et al., 2011), and greater lifetime savings (Lusardi & Mitchell, 2014). However, the outbreak of COVID-19 has changed the whole world and increased the level of uncertainty. The household’s financial behavior and risk tolerance have been reshaped due to the COVID-19 outbreak. The current stream of research offers limited evidence regarding the role of financial literacy during a crisis in influencing investors’ trading behavior and risk-taking behavior. Particularly, the evidence in developing economies such as Pakistan remains limited. Therefore, the objective of this study is to determine the role of financial literacy in determining the investor’s financial well-being by considering the mediating role of financial well-being.

The rest of the paper is organized as a literature review, Data, and methodology followed by a discussion and conclusion.

Literature Review

Financial Literacy and Financial Well-Being

Household financial planning remains integral to determining well-being which enables them to meet their financial obligations effectively. Effective household financial planning also remains prognostic to sustain the economic well-being of the whole society. The research on household financial planning is much extensive and an important factor in determining the individual standard of life. Individuals’ financial planning should be the ultimate criterion for their sustained financial well-being. Several pieces of research have been carried out to investigate the link between households’ financial planning and financial well-being (Hwang & Park, 2023). The prior study by Li et al. (2023) examines whether the households’ personal characteristics, for example, educational level, financial pressures, risk, financial activity, financial literacy, and financial ability influence financial well-being. They used data that are collected from 220 white-collar clerical workers and concluded that financial literacy has an impact on financial well-being. Furthermore, J. Kumar et al. (2023) showed that financially literate individuals are less stressed, more driven in their financial activities, and have stronger family relationships. Financial literacy is the ability of individuals to understand and effectively use various financial skills, including managing personal finances, creating and following budgets, and investing in sustaining their financial well-being (Tan & Singaravelloo, 2020). Accordingly, the term financial well-being is defined as the perceived ability of individuals to oblige their liabilities and effectively achieve their future financial goals without anxiety and discomfort (Lusardi & Messy, 2023; Lusardi & Mitchell, 2007. The significance of this study arises from multiple factors. Besides this, they are physically and mentally healthier which shows that financial well-being is an important factor in their lives. In contrast, if individuals are financially stressed then they are more affected mentally and physically.

P. Kumar et al. (2023) posits that individuals who remain financially literate are likely to effectively allocate their resources. In contrast deficiency in financial literacy results in inefficient allocation of resources. Likewise, the study of Li et al. (2023) examines the link between financial literacy and financial well-being and concludes that financial well-being can be increased through financial literacy. Similarly, Lone and Bhat (2024) empirically investigate financial well-being and financial literacy and develop a questionnaire for collecting data. According to the findings of the study, a higher level of financial literacy leads to improved financial well-being, which has a beneficial influence on a household’s overall psychological well-being. However, there are studies that also indicate that there is no such positive link between financial literacy and financial well-being (Cheah et al., 2015). The rationale for such findings is supported due to the fact that every person has a fundamental need, and the inability to satisfy that need generates stress, which leads to a reduction in financial well-being, affecting both literate and illiterate people (Prakash et al., 2022). It means financial literacy increases the level of financial well-being however, the impact of fundamental requirements on financial well-being cannot be mitigated. P. Kumar et al. (2023) assert that formal education is the main source of financial knowledge and it may improve the attitudes and behavior that lead to financial well-being. Further, Li et al. (2023) examine the impact of financial literacy on financial well-being in the United States and conclude that financially literate individual makes a better-informed decision which will increase the level of financial well-being and help in community development. Several studies (Li et al., 2023; Lone & Bhat, 2024; Lusardi & Messy, 2023; Mahendru et al., 2022) argue that increased financial literacy leads to increased financial contentment which, in turn, increases the level of households’ financial well-being.

Furthermore, Chu et al. (2017) find that an individual whose financial literacy level is higher makes better decisions and, in its reward, the level of financial well-being also increases. Andreou and Philip (2018) explore financial aptitude, financial literacy, and behavior and confirm the positive association between financial literacy and financial knowledge, which ultimately helps them make good financial decisions that will benefit them in the long run. Similarly, Philippas and Avdoulas (2020) and Younas & Rafay (2021) also report similar results in Greece and Pakistan respectively.

Limbu and Sato (2019) empirically explore the association between credit card literacy and financial well-being by collecting data from 427 students and conclude that Credit card literacy significantly affects financial well-being. Those students who do not have any knowledge about credit cards will benefit from the seminar, lecture, and workshop that are organized for improving student knowledge about credit card usage which ultimately increase their financial well-being (She et al., 2023). Findings suggest that usage of multiple credit cards can negatively affect, so stakeholders have to launch a campaign for educating students that usage of fewer credit cards in the long run improves financial well-being. Further, Riitsalu and Murakas (2019) examine how financial literacy, for example, subjective finance knowledge and objective finance knowledge influenced financial well-being. The study found a stronger relationship between subjective finance knowledge with financial well-being as compared to objective. That’s why focusing only on the improvement of knowledge and skills is not enough; it also means developing confidence and motivation for the improvement of financial well-being (Singh & Malik, 2022). Similarly, Setiyani and Solichatun (2019) examine the impact of financial literacy on financial well-being; financial literacy appears to have a beneficial impact on financial well-being, according to the research.

Mahendru (2021) argues that for a longer period, the government faces challenges to financial well-being and they carried out a study that explores this challenge through an integrative approach and suggests a new understanding of financial well-being. Financial literacy and financial competence increase financial well-being, and individuals’ financial well-being can be improved by understanding the relationship between financial literacy and financial capability. Tahir et al. (2021) also explore the association between financial literacy and financial well-being in the presence of financial capability in Australia. The empirical results show that financial capability stronger association between financial literacy and financial well-being. For improving financial well-being, this study highlights the importance of financial literacy and suggests that there are many other factors, for example, risk-taking attitude that may be influenced the financial well-being and decision of an individual. Furthermore, Moghavvemi and Muniandy (2021) investigate how financial literacy improved Malaysia’s well-being and helped to alleviate the financial crisis during COVID-19. Accordingly, there is rising activism that households with sound financial literacy have a higher propensity to make sound investment decisions (Attiq et al., 2021; Mahendru et al., 2022; H. J. Shah et al., 2016). Although past studies have explored the various determinant of investor financial well-being in the context of developed economies, literature in the context of developing or emerging economies is scant. Besides theory validation and contextual divergence, the study offers novel insight to understand how the underlying mechanism of financial literacy remains integral for sustaining improved financial well-being of the retail investor. Based on the above substantive review, we hypothesize the following hypotheses:

H1: Financial well-being is positively affected by basic financial literacy.

H2: Advanced financial literacy has a positive relationship with financial well-being.

Financial Literacy, Financial Well-Being and Risk Tolerance

A huge amount of empirical research focused on risk tolerance while making financial decisions. Prakash et al. (2022) define risk as a function of profit and loss and it is the basic concept of the financial decision-making process. Risk is further divided into three levels risk-taker (lover), risk-averse, and risk lover. The perceptions of people about risk are different from person to person because they are influenced by information that is readily available to them (Lusardi & Messy, 2023). Wood and Zaichkowsky (2004) argue that the risk attitude of every individual is different, such as risk-tolerant investors always preferring to purchase stocks. Li et al. (2023) show that financial literacy directly influences the risk-taking behavior of investors. Similarly, Aren and Zengin (2016) suggest that financial literacy has a substantial influence on financial decision-making behavior. Similarly, Lone and Bhat (2024) examines the attitudes of financially educated students regarding financial risk-taking and gambling. In the context of risk-taking and gambling behavior, students in finance show a positive attitude.

In addition, Bayar et al. (2020) Investigate the effects of financial literacy on risk tolerance. They find that financial literacy is a major driver of the financial risk tolerance of university employees. Using the 38,000 MiFID surveys, Bajo et al. (2015) investigate the influence of financial literacy on a financial risk-averse choice. The findings of the study show that individuals with less financial literacy are more risk-averse. Similarly, Nguyen et al. (2016) investigate the link between customer risk tolerance and financial decision-making and conclude a positive association between risk tolerance and financial decision-making in the Australian context. Zakaria et al. (2017) find that financial literacy has a substantial association with risk tolerance. On the contrary, Hendrawaty et al. (2020) risk tolerance level is not affected by the level of financial literacy, Bannier and Neubert (2016) and Manjunath and Bankar (2021) investigate the impact of demographic variables on high-risk financial decisions and non-risky financial decisions by using a sample size of 100 respondents and conclude that there is an insignificant association among demographic factors and risky financial decisions and non-risky financial decisions. Moreover, Ahmad et al. (2020) investigate the Indonesian retail investor’s risk tolerance level with respect to sociodemographic variables and collect data from 407 individuals. The empirical findings suggest that financial risk tolerance is affected by most socio-demographic characteristics, and ethics does not affect financial risk tolerance. Further, Rahman (2020), Payne et al. (2019) conclude that only lower-risk-tolerance user’s financial satisfaction levels decrease because of credit card mismanagement.

Financial literacy also affects the propensity to take risks while making an economic decision. The idea of risk is one of the most important concepts in the investment decision-making process. Investors are divided into three groups based on their risk tolerance: risk-averse, risk-neutral, and risk-lovers. Each economic decision is surrounded by uncertainties, for example, unlike a result of getting 100% guaranteed, all sorts of economic decisions contain an element of risk (Kourtidis et al., 2011). Tauni et al. (2017) argue that financial risk tolerance is decisive due to the fact that consumers who are unfamiliar with the subject may exhibit behavior that is too conservative to make optimal choices and perceive that taking a financial risk is the exact opposite of financial well-being (Naveed, Ali et al., 2020). Based on the aforementioned literature, we have developed the following hypothesis.

H3: Risk tolerance mediates the relationship between basic financial literacy and financial well-being.

H4: Risk tolerance mediates the relationship between advanced financial literacy and financial well-being.

Past different definitions, measurements, and indicators of financial literacy, financial well-being, and risk tolerance may limit the comparability and generalizability of the results across different contexts and populations (Hwang & Park, 2023; Li et al., 2023; Lusardi & Messy, 2023; She et al., 2023). The studies rely mostly on self-reported surveys or questionnaires, which may introduce biases such as social desirability, recall error, or response inconsistency. Moreover, some of the surveys or questionnaires may not have been validated or tested for reliability and validity. The studies use mostly cross-sectional or correlational designs, which may not capture the causal or dynamic relationships between financial literacy, financial well-being, and risk tolerance. Moreover, some of the studies may not control for potential confounding or moderating variables, such as income, education, age, gender, culture, or personality. The studies have different sample sizes, sampling methods, and sampling frames, which may affect the representativeness and diversity of the respondents. Moreover, some of the studies may have low response rates or high attrition rates, which may reduce the statistical power and increase the sampling error.

Some studies find a positive and significant relationship between financial literacy and financial well-being (e.g., Li et al., 2023; Lone & Bhat, 2024; Lusardi & Messy, 2023; Mahendru et al., 2022), while others find no such relationship (e.g., Cheah et al., 2015; Prakash et al., 2022). Some studies find that financial literacy influences the risk-taking behavior or attitude of investors (e.g., Aren & Zengin, 2016; Bajo et al., 2015; Bayar et al., 2020; Li et al., 2023), while others find no such influence (e.g., Bannier & Neubert, 2016; Hendrawaty et al., 2020). Some studies find that risk tolerance mediates the relationship between financial literacy and financial well-being (e.g., Tahir et al., 2021), while others do not test or report this mediation effect (e.g., Limbu & Sato, 2019; Riitsalu & Murakas, 2019). The different operationalizations and measurements of financial literacy, financial well-being, and risk tolerance may capture different aspects or dimensions of these concepts, which may lead to different results depending on the indicators or scales used. The different contexts and populations of the studies may reflect different levels of financial literacy, financial well-being, and risk tolerance among the respondents, which may be influenced by various factors such as economic conditions, cultural norms, institutional regulations, or individual characteristics. The different methodologies and analytical techniques of the studies may account for different sources of variation or error in the data, which may affect the estimation and inference of the relationships between financial literacy, financial well-being, and risk tolerance.

Theoretical Background

The study used transformative service research (TSR) as an overarching theory to explain the causal relationship of the proposed model (Anderson et al., 2013). Aligning with the theoretical perspective of TSR, the study findings validate it in the context of Pakistan and affirm that different interventions such as financial literacy and risk tolerance remain integral to triggering households’ financial well-being. Transformative Service Research (TSR) is research that focuses on creating “uplifting changes” aimed at improving the lives of individuals (both consumers and employees), families, communities, society, and the ecosystem more broadly. TSR addresses this shortcoming by focusing on empirical and conceptual studies that have the potential to enhance the well-being of individuals (e.g., consumers, employees), communities, and ecosystems (Blocker et al., 2022). Transformative Service Research (TSR) is an emerging area of research that aims to understand the role of services in enhancing consumer well-being. TSR focuses on creating uplifting changes and improvements in the well-being of individuals (consumers and employees), communities, and ecosystems. TSR is based on the premise that service is the fundamental basis of exchange and that service can have a transformative impact on the lives of people and the planet. TSR is an interdisciplinary and multidimensional field that draws on various theories and methods to understand and enhance well-being through service. Accordingly, our underlying notion is to examine how the transformative role of financial literacy triggers household’s financial well-being (see, Figure 1).

Conceptual framework.

Data and Methodology

Data Collection

The population of this study includes individual investors involved in stock trading at the Pakistan Stock Exchange (PSX). For data collection, questionnaires have been adopted and distributed among investors in various stock exchanges, that is, Islamabad, Lahore, and Karachi. Prior to participation, all participants were informed of the voluntary nature of their involvement, and no incentives were provided. The study employed a non-probability sampling technique, specifically Convenience sampling, which is consistent with previous TAM-related research (M. Ali et al., 2018; Etikan et al., 2016; Raza & Khan, 2022). This approach was chosen for its alignment with the established methodology in this field. The questionnaire was developed in English, and its reliability was assessed through a pilot study involving the distribution of 30 questionnaires. This step aimed to assess the questionnaire’s utility and validity within the survey context. Additionally, both market professionals and academic experts validated the content and construct validity of the questionnaire items. We have distributed 700 questionnaires, out of which 367 returned with a response rate of 53.17%.

Instrumentation

To measure financial literacy, we have adapted the items from Lusardi (2008) and Lusardi and Mitchell (2005) to design questions that were useful to reflect individuals’ understanding of such concepts that formed the basis of their daily financial transactions and decisions. It contains a total of 13 questions, specifically 5 questions to gauge basic financial literacy and 8 for advanced financial literacy. To measure risk tolerance, we follow Pasewark and Riley (2010) so that the scale has 14 items. Perceived financial well-being is measured by using Prawitz et al.’s (2006) construct containing 8 items.

The recent economic crisis has had a significant impact on the financial situation of many people. People are less willing to take risks, are more financially susceptible, and are poorly equipped to deal with sudden changes in their financial situation. As a result, individuals run the risk of becoming financially precarious and unable to meet large future obligations.

Methodology

To empirically test the relationship between literacy, risk tolerance, and financial well-being, we employ structural equation modeling (SEM) using PLS. We follow Mulaik and Millsap (2000) for testing the relationship between the variables of interest; they suggest using a three-step model, which includes (i) reliability of the construct, (ii) confirmatory factor analysis using a measurement model, and (iii) the structural model. To establish the reliability of the constructs, we use Cronbach’s alpha. Furthermore, we use several model fit indices to validate the results of the measure and structural model, which includes the Goodness-of-Fit Index (GFI), Adjusted Goodness-of-Fit Index (AGFI), Relative chi-square (CMIN/DF), Comparative Fit Index (CFI), and Root Mean Square Error of Approximation (RMSEA). The cross-sectional data have been collected during the first wave of COVID-19 which makes our contribution novel to consider the variation in investor financial behavior to determine the effect of the health crisis.

Based on a substantive literature review, in this paper, we conceptualize the proposed model to examine the role of financial literacy in triggering individual investor’s perceived financial well-being in the following figure:

Empirical Analysis and Discussion

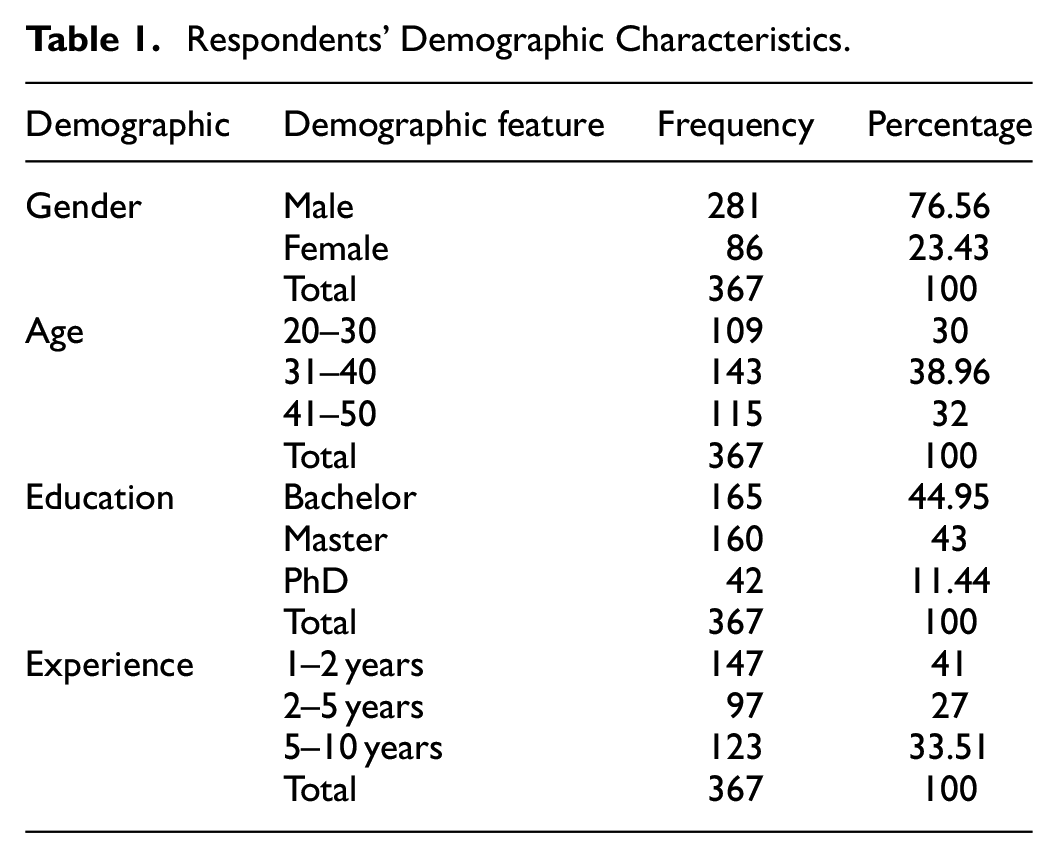

Table 1 presents a detailed overview of the demographic profile of the individuals involved in the study. The provided data provides valuable information regarding the demographic composition of the respondents, including their gender distribution, age groups, educational backgrounds, and levels of experience. In terms of gender, the demographic breakdown of participants reveals that a significant majority, accounting for 76.56% of the total sample, identified as male. On the other hand, females constituted 23.43% of the participants. The demographic breakdown indicates that the majority of respondents, comprising 38.96% of the total, were between the ages of 31 and 40. This was closely followed by individuals aged 41 to 50, accounting for 32% of the sample, while those in the age range of 20 to 30 made up 30% of the respondents. Regarding educational attainment, the demographic data reveals that a significant proportion of individuals possess a Bachelor’s degree (44.95%), followed closely by those holding a Master’s degree (43%). A smaller percentage of the population has achieved a PhD (11.44%). The demographic breakdown of experience levels reveals that among the respondents, 41% reported having 1 to 2 years of experience, 27% reported having 2 to 5 years of experience, and 33.51% reported having 5 to 10 years of experience. In general, this table provides a comprehensive overview of the various demographic characteristics of the individuals involved in the study. It offers insights into their gender, age, educational background, and professional experience.

Respondents’ Demographic Characteristics.

Measurement Model

Table 2 reports the factor loadings, composite reliability (CR), average variance extracted (AVE), and Cronbach Alpha. J. F. Hair et al. (2011) suggest keeping the items if the factor loading is greater than 0.60 and removing them otherwise. Similarly, the composite reliability and Cronbach alpha of the construct are greater than the threshold value of .70 to ensure the internal validity of the construct. All the values reported in Table 2 are well above the threshold level thus confirming the internal validity of all the constructs. To establish the convergent validity of the construct, we use AVE, also reported in Table 2. According to Fornell and Larcker (1981), the value of AVE must be higher than 0.50 to ensure the convergent validity of the construct. The value of AVE for all the variables ranges from 0.50 to 0.609; hence, convergent validity is established.

Factor Loading of Standardized Estimates.

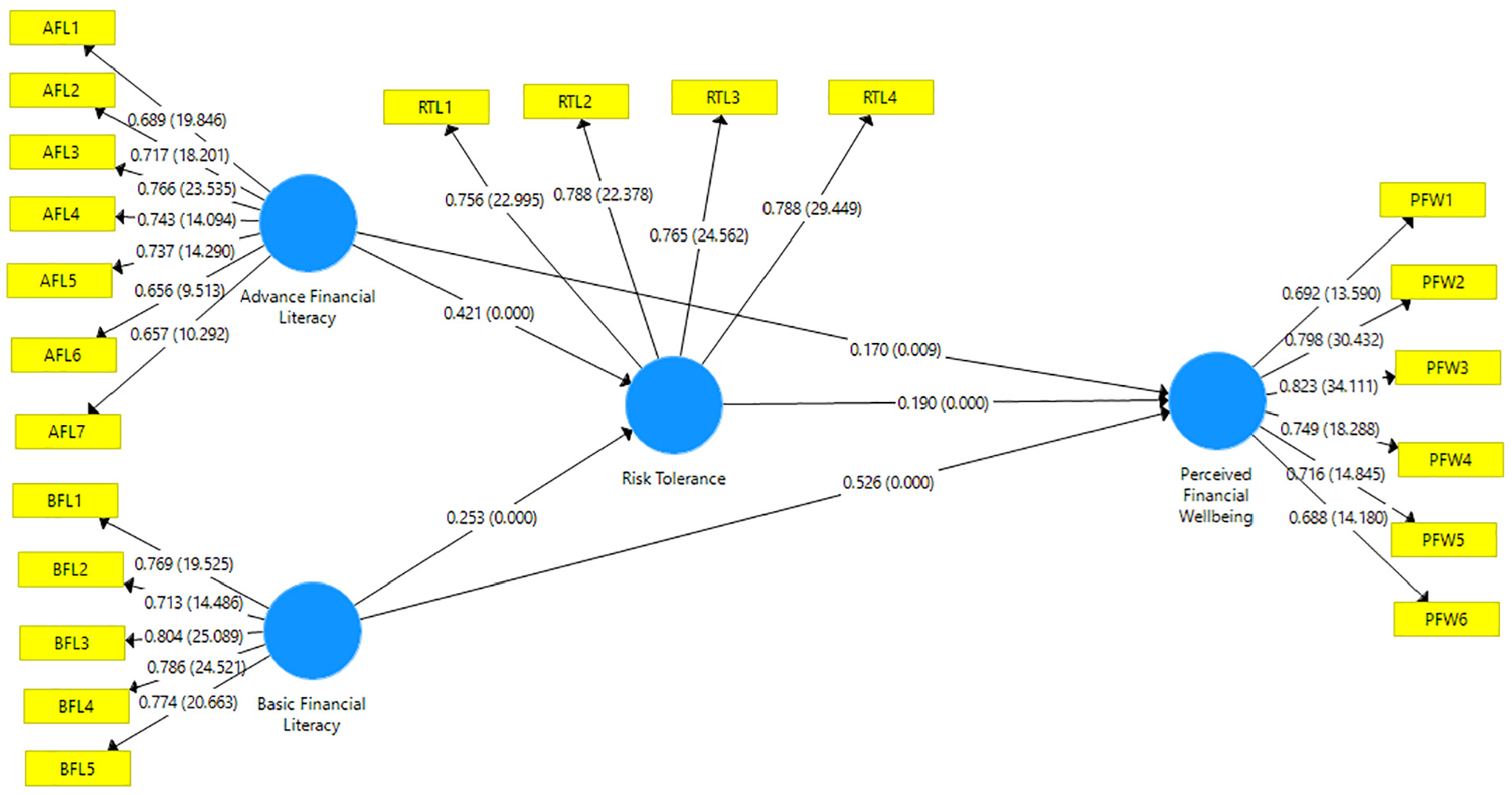

For establishing the discriminant validity of the construct, the heterotrait-monotrait ratio (HTMT) technique was employed and reported in Table 3. All the values were below the maximum acceptable range of 0.85, and discriminant validity was established for each construct (Henseler et al., 2016). Figure 2 shows the measurement model, which displays the factor loading of each item against it.

Discriminant Validity.

Mesurement model.

After establishing the convergent and discriminant validity of the construct and checking the measurement model results, we proceed to the structural model.

Structural Model

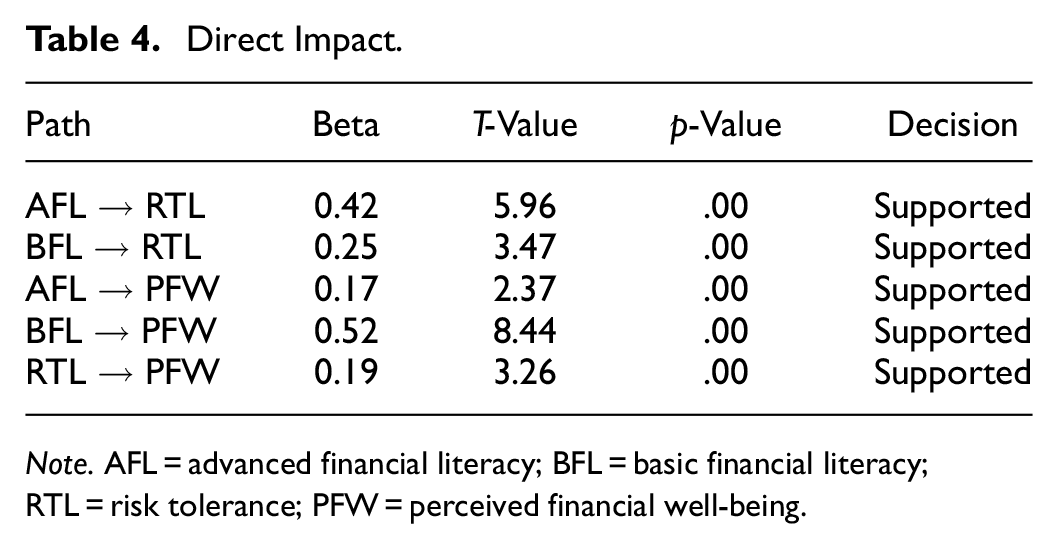

To empirically test the hypotheses, the conceptual model is transformed into a structural model, where we use a variety of criteria, including R2 value (coefficient of determination; J. F. Hair et al., 2012) and value (model path coefficient; Chin, 1998). To evaluate the hypotheses, this current study employed a 5,000 bootstrap sample bias-corrected bootstrapping approach, in which the t-value was assessed for its significance level. Figure 3 shows the estimate of the structural model.

Structural model.

Before going to the mediation analysis, we must see whether advanced financial literacy has a substantial impact on risk tolerance. Only then we can move toward the main model. Table 4 reports the direct impact of one variable on other variables. The findings of the study suggest that advanced financial literacy has a positive impact on risk tolerance. The results revealed that β = .42, p < .00, demonstrating that advanced financial literacy significantly impacts risk tolerance. Similarly, we also tested whether risk and basic financial literacy have any association, and the study’s findings confirm that basic financial literacy has a positive impact on risk tolerance. The results revealed that β = .25 with p < .000, demonstrating that basic financial literacy significantly impacts risk tolerance. The outcomes of the study, such as those of Lone and Bhat (2024) and Bayar et al. (2020), also claim that financial literacy has a favorable impact on an investor’s risk tolerance. The study’s findings are also further supported by Zakaria et al. (2017) who concluded that financial literacy improves the investors’ risk tolerance level.

Direct Impact.

Note. AFL = advanced financial literacy; BFL = basic financial literacy; RTL = risk tolerance; PFW = perceived financial well-being.

Mediation Analysis

To evaluate the mediation, the current study follows J. Hair et al.'s (2017) proposal to use the Preacher and Hayes (2004, 2008)] bootstrapping approach. Therefore, in line with the aforementioned studies, we estimate the specific indirect effect by using bias-corrected bootstrapping with 5,000 resampling. The indirect impact must be statistically different from zero and t-statics greater than 1.654 (J. F. Hair et al., 2011, 2014; J. Hair et al., 2017). The indirect impact of 5% and the 95% confidence interval should not overlap zero.

Table 5 shows that the indirect effect of advanced financial literacy on financial well-being through risk tolerance is 0.08, which is statistically significant at 1%. Furthermore, the value of the lower confidence interval is 0.04 and the upper confidence interval is 0.12, which does not have zero between them, thus confirming the mediating role of risk tolerance in the relationship between advanced financial literacy and financial well-being.

Significance of Indirect Paths.

Note. AFL = advanced financial literacy; BFL = basic financial literacy; RTL = risk tolerance; PFW = perceived financial well-being.

The indirect impact of basic financial literacy on financial well-being through risk tolerance level is positive (β = .04) and significant (p < .00). The results confirm that risk tolerance mediates the relationship between financial literacy and investor financial well-being.

Discussion

The result of the study exhibits that financial literacy remains significant in determining the investor’s financial well-being during COVID-19. The mediating effect of risk tolerance also remains significant which adheres to the notion that investor during an uncertain environment remains rational to make wise allocation of their resources which in turn sustain their financial well-being. The result also asserts the robustness of financial literacy during the COVID-19 crisis to sustain the investors’ financial well-being and rationalize their risk-taking behavior. Financial literacy remains essential to analyze and understand financial alternatives and plan for the future to respond to profitable investment opportunities effectively. However, despite the significance of financial literacy, past research has shown that the level of financial literacy around the world, particularly in developing and underdeveloped countries, remains minimal. Furthermore, past studies have overlooked the phenomena of financial well-being and its causal relationship with financial literacy. Therefore, the main concern of this study was to determine how financial literacy could potentially impact the household’s financial well-being in the context of a developing economy such as Pakistan. The current study examined the relationship among financial literacy, risk tolerance, and financial well-being we used structural equation modeling and analyzed it through Smart PLS. The data of 320 active individual investors was used for the analysis. The cross-sectional data were collected during the first wave of COVID-19, which makes our contribution novel. We need to consider the variation in investor financial behavior to determine the effect of the health crisis. The findings of the study highlight that both advanced and basic financial literacy has a positive and significant association with investor well-being (Naveed, Sindhu, & Ali, 2020). Furthermore, financial literacy has a favorable indirect impact on financial well-being, as highlighted in this study through risk tolerance. The results confirm that risk tolerance positively mediates the linkage between financial literacy and financial well-being. The study used transformative service research (TSR) as an overarching theory to explain the causal relationship of the proposed model. Aligning with the theoretical perspective of TSR, the study findings validate it in the context of Pakistan and affirm that different interventions, such as financial literacy and risk tolerance remain integral to triggering households’ financial well-being. The findings of our study also remain aligned with recent studies which also confirm the significance of financial literacy in nurturing households’ well-being (Bayar et al., 2020; Chong et al., 2021). The study, besides validating TSR in the context of Pakistan, also has strong policy implications for regulators and banks to take initiatives to educate their customers, which will, in turn, trigger their financial well-being. The improved financial literacy will not only improve the household’s financial well-being but also result in improved economic-financial well-being, which remains essential for the whole society (Naveed et al., 2021).

Conclusion

The findings of the study suggest that having a solid understanding of finances will continue to be an important factor in determining an investor’s financial well-being throughout COVID-19. The moderating influence of risk tolerance continues to be considerable, as does its adherence to the premise that investors may maintain their rationality in the face of an uncertain environment to make resource allocation decisions that, in turn, maintain their financial welfare. The findings also provide evidence that there was a high level of financial literacy during the COVID-19 crisis, which helped investors maintain their financial well-being and explain the level of risk they were willing to take.

This research aims to examine whether basic financial literacy or advanced financial literacy is more critical for risk tolerance and the perceived financial well-being of investors traded in PSX. In other words, this study tested whether either basic financial literacy or advanced financial literacy first influences risk tolerance or directly influences perceived financial well-being. This study highlights the importance of basic financial literacy, advanced financial literacy, and risk tolerance toward perceived financial well-being during the COVID-19 outbreak. The hypothesized relationships were tested through Structural equation modeling in Smart PLS. The empirical evidence has been collected through a structured questionnaire from 320 investors trading in PSX. The findings revealed that basic financial literacy and advanced financial literacy significantly influence individual investor’s risk tolerance and perceived financial well-being. Furthermore, risk tolerance has a significant influence on perceived financial well-being. Additionally, the results indicate that risk tolerance partially mediates the nexus between advanced financial literacy and perceived financial well-being, and risk tolerance significantly partially mediates the relationship between basic financial literacy and perceived financial well-being. This research recommends that investors give sufficient attention to basic and advanced financial literacy and risk tolerance to enhance perceived financial well-being.

Practical and Policy Implications

The policy and practical implications for investors and policymakers navigating the challenges of the COVID-19 crisis are carried by the outcomes of this research. Enhancing perceived financial well-being is dependent on both basic and advanced financial literacy, as well as risk tolerance, as highlighted by the study. If investors acknowledge these factors, then they can make more informed decisions, which will safeguard their financial interests during uncertain times. Accordingly, policymakers and regulators can utilize the study’s findings to design policies that promote financial literacy and risk awareness. By integrating financial education initiatives into broader economic relief measures during crises, governments can enhance citizens’ ability to manage financial challenges effectively.

Limitations and Future Directions

While the study provides valuable insights, it is important to recognize certain limitations. The study’s findings may not be applicable to all investors as it is based on a specific sample from PSX. Furthermore, it is important to acknowledge that the cross-sectional design employed in this study imposes limitations in determining causal relationships between financial literacy, risk tolerance, and financial well-being. Moreover, it is essential to note that the study is limited by its reliance on self-reported data from participants. This introduces the possibility of response bias and potential inaccuracies in capturing the intricate relationship between financial literacy, risk tolerance, and perceived financial well-being.

To build on this study’s foundation, future research avenues should explore the broader determinants of financial well-being beyond financial literacy and risk tolerance. Probing the interaction between individual personality traits and the relationship between financial literacy and financial well-being during COVID-19 offers a promising avenue for deeper understanding. Such investigations could yield insights into developing more tailored strategies for enhancing investor financial resilience during crises. Future research can also identify the other determinants of financial well-being. Furthermore, how individual personality traits affect the relationship between financial literacy and investors’ financial well-being during COVID-19 is another important area that needs attention.

Footnotes

Acknowledgements

We would like to thank Dr. Imran for his inputs.

Authors’ Contributions

All authors contributed equally. All authors read and approved the final manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data is available if demanded.