Abstract

The increased accessibility and adoption of FinTech in emerging economies prompts researchers to investigate its moderating impact on the prevalent determinants of financial literacy. This research investigates the influence of demographic, socio-economic, psychological, and FinTech innovation factors on mitigating the financial literacy gap. Structured questionnaires were used to obtain primary data from the 1,100 Saudi potential participants. The descriptive and inferential statistics were computed using the Statistical Package for Social Sciences. The study findings revealed that FinTech innovation as a moderating variable has a limited impact on closing the financial literacy gap. Besides, marital status, income, spouse’s educational background, as well as psychographic characteristics like “present financial situation,”“meet monthly payments,”“future is hopeless,” and “don’t expect change” have a bearing on the financial literacy gap. Additionally, women lacked confidence when responding to queries on financial literacy. Finally, the study concludes with implications for the policy-making bodies.

Introduction

According to the 2019 OECD report, “Financial literacy is knowledge and understanding of financial concepts and risks, as well as the skills and attitudes to apply such knowledge in order to make effective decisions across a range of financial contexts, to improve the financial wellbeing, and to enable participation in economic life.” There are wide-ranging theoretical and empirical studies documenting lower financial literacy levels among females compared to their male counterparts in developing or even developed countries (Bucher-Koenen et al., 2017; Klapper & Lusardi, 2020; Lusardi & Mitchell, 2023). Accordingly, about 50% of the 1.7 billion financially excluded persons are from developing nations, with women accounting for 56%. One of the reasons for this situation is a lack of financial literacy (Global Findex Report, 2017). Women with insufficient financial knowledge may be more likely than men to lack self-confidence (Bucher-Koenen et al., 2021; Lusardi & Mitchell, 2023), more affected by the scale of over-indebtedness and less financially prepared during the COVID-19 pandemic (Kurowski, 2021). Women are also more likely to live longer than their husbands, so if their husband dies, they must assume financial responsibility for managing their wealth. Family obligations also disrupt their careers, leading to lower income and retirement advantages. These all-increase women’s vulnerability to financial instability as they age (Lee, 2003; Weir & Willis, 2000).

Four facts motivated this research. First, when it comes to financial inclusion, there is a clear gender gap. In high-income and developing economies, women are much less likely to have access to formal credit (World Bank, 2013). Women lacked savings buffers and were less financially secure than men even before the COVID-19 crisis (Hasler & Lusardi, 2019). They were also less likely to have pensions and to invest in high-yielding, risky assets (Fornero & Lo Prete, 2023; Lusardi & Mitchell, 2008).

Second, a consistent and widespread gender disparity in financial literacy exists in both developed and developing economies (Bucher-Koenen et al., 2017, 2021; Klapper & Lusardi, 2020; Lind et al., 2020; OECD, 2022; Tinghög et al., 2021; Yabokoski et al., 2022). In particular, Lusardi and Mitchell (2023) argued that in addition to being widespread in the general population, financial illiteracy differs substantially between gender groups and may contribute to other forms of economic disparities.

Third, the factors that lead to gender disparity remain poorly understood and are the topic of ongoing studies. According to Preston and Wright (2019), human capital characteristics such as age and education play no role in explaining the financial disparity; however, labor market determinants like union membership, sector, labor market status, occupation, and industry are critical, accounting for approximately 16% of the disparity.

The fourth is the effect of FinTech innovation on financial education that can help companies make bigger profits and bridge the genuine financial gender gap (Arner et al., 2020; Frame et al., 2019; Thakor, 2020). FinTech is one of the areas that is growing at the quickest rate, according to the FinTech Saudi annual report 2022. From 2018, the number of FinTech companies in the kingdom has increased dramatically by 14.7 times. FinTech encompasses a wide range of services that can be used to educate different groups (depending on age, income, lifestyle, etc.) about money matters. Nevertheless, most emerging market studies on the financial literacy gap have concentrated on socio-economic, psychological, and demographic characteristics, which has limited their capacity to capture a wide variety of crucial elements.

This research is one of the few to include the role of FinTech adoption in preventing financial literacy inequalities in Saudi Arabia, an Arabic-speaking country. The study is also the first to focus on basic and advanced financial literacy among Saudi employees, utilizing Lusardi and Mitchell’s questions. It also broadens the pool of knowledge and skills that regulators can incorporate to make policy decisions.

As the points above show, financial literacy is crucial for both men and women. Thus, this study aims to broaden current financial knowledge by focusing on (1) the extent to which Saudi men and women employees are financially literate, (2) whether there is a difference in their financial literacy level based on demographic, psychological, and socio-economic characteristics, and (3) testing the moderating impact of FinTech on financial literacy gap. The research is divided into five sections. Section one introduces the research topic. Section two discusses the literature review. Section three displays the methodology, section four includes the analysis of data, and section five emphasizes the discussions and results.

Review of the Literature

Financial literacy is acquiring financial education that helps a person understand financial concepts, including risk, to make decisions that enhance financial wellbeing (Miller, 2001). Acquiring financial knowledge is of crucial significance. Individuals who lack financial knowledge come across many hurdles concerning handling and managing their money (Ahmad et al., 2018). Although many factors influence the financial literacy level, this study revolves around the factors that comprise the demographic, socio-economic, psychological, and FinTech elements and evaluates their influences on reducing the financial literacy gap.

Gender and Financial Literacy

Determining what leads women to have low financial knowledge levels is critical given changing demographic trends, financial decision shifts, and financial technology (FinTech) development among the different financial institutions. Around the world, there is typically a financial literacy persistent gender gap, with men outperforming women (Klapper & Lusardi, 2020; Koenen et al., 2021; Lind et al., 2020; Lotto, 2020; Lusardi & Mitchell, 2023; Sconti & Fernandez, 2023; Swiecka et al., 2020; Tinghög et al., 2021; Yabokoski et al., 2022). In this regard, theoretical and empirical studies have documented lower financial literacy levels among females than their male counterparts in developing or developed countries (Klapper & Lusardi, 2020; OECD, 2022). Thus, women who lack financial literacy may be more likely than men to experience low retirement confidence. (Fornero & Lo Prete, 2023). When considering demographic characteristics, Łukasz (2021) found that women were surprisingly more affected by the scale of over-indebtedness and their personal finances and were less prepared for the COVID-19 pandemic. According to Li (2018), single women have a more challenging time repaying debt than single men, suggesting that there are gender disparities in borrowing and debt management. More recently, Lusardi and Mitchell (2023) claimed that women have an 8% lower chance than men of answering the interest rate question correctly, 10% less likely to understand inflation, and 17% less likely to understand risk diversification, potentially contributing to various additional kinds of economic and financial decisions inequality like debt management, stock market participation, wealth accumulation and management, and retirement planning. Similarly, Sconti and Fernandez (2023) discovered that certain groups, like women, have low financial education. They asserted a significant gender disparity in risk understanding, with only 44% of women correctly answering the question about risk diversification, compared to 55% of men. These findings are significant since women may be less likely to use financial products or invest in the stock market due to financial illiteracy (Ansar et al., 2023; Bannier et al., 2019).

Demographic Characteristics and Financial Literacy Disparities

A study examining the financial literacy level among non-commerce students revealed that most male students under 26 were more financially literate than their counterparts (Liaqat et al., 2021). In other studies that were conducted to gauge the influence of demographic characteristics on financial literacy, it was discovered that age, gender, and education level impact the financial literacy level (Kiliyanni & Sivaraman, 2016; Potrich et al., 2016; Santini et al., 2019). Fornero and Lo Prete (2023) claimed that women are more likely to live longer than their husbands, so if their husband dies, they will have to take financial responsibility to manage their wealth. Besides, because they have a longer life expectancy, older women are more likely to be poor than older men. Family obligations often disrupt their careers, resulting in lower earnings and retirement benefits. Therefore, enhancing pension financial literacy among women becomes critical to properly planning their retirement. These disadvantages increase women’s vulnerability to financial insecurity in old age (Fornero and Lo Prete, 2023; Lee, 2003; Weir & Willis, 2000). According to Farrar et al. (2019), as people age, the level of financial literacy increases, and, per Agarwal et al. (2009), people aggregate more financial knowledge as they age.

Researchers also revealed that the education level positively and significantly influences the financial literacy level is influenced by the education level and the impact is positive and significant (e.g., Albeerdy & Gharleghi, 2015; Kiliyanni & Sivaraman, 2016). Education is pivotal in financial literacy, echoing psychological theories highlighting cognitive capabilities (Gill & Prowse, 2016; Lusardi et al., 2010). According to the social learning theory, the education level of parents and spouses positively influences financial literacy, and capable parents and spouses can reduce the financial literacy gap (Mahdavi & Horton, 2014; Pinto, 2005). It is also evident from the results of Ergün (2018) and Lusardi and Mitchell (2011) that the higher the education level, the higher the financial literacy level will be. Besides, Zissimopoulos et al. (2008) and Bucher-Koenen et al. (2017) found that unmarried women, especially divorced women, had significantly lower capital than married and unmarried men. However, according to Preston and Wright (2019), human capital characteristics such as age and education do not explain the financial gender gap. Their results showed that labor market determinants such as sector, occupation, industry, union membership, and labor market status are substantial, accounting for roughly 16% of the disparity.

Socio-economic Characteristics and Financial Literacy Disparities

Liaqat et al. (2021) investigated the level of financial literacy among students at private universities, and their findings revealed that students whom family members advised, studied finance as a minor, had a bank account, and had a higher parental income displayed greater financial knowledge. The social circle, comprising the family, friends, and relatives, influences financial literacy. People who have financial advice bestowed upon them by their social circles are more financially literate than those who are not (Ergun, 2018). The family’s primary source of financial information is the parents, who provide financial information that helps a child take care of personal finances (Nidar & Bestari, 2012). The child’s family background has a crucial bearing on the child’s financial literacy. A child from a financially sound family has more opportunities to accomplish a greater financial literacy level (Erner et al., 2016).

However, occupation and employment had a considerable influence on financial literacy. Notably, people who specialized in finance were found to be more financially literate than those who did not have a specialty in the finance stream (Kadoya & Khan, 2020). Lusardi and Mitchell (2011) found that financial literacy levels were higher for those who were employed than those who were not. According to Lusardi and Tufano (2015), income and assets, which are socio-economic factors, positively influence financial literacy. However, Kadoya (2020) found that employment status did not elevate the financial literacy level, but years of work experience did.

Psychological Factors in Financial Literacy

Based on the theory of social identity of Akerlof and Kranton (2000), Cwynar (2021) investigated the origins of gender disparity in financial literacy. According to this theory, all individuals are assigned to one of two abstract social groups: “male” or “female.” These groups include behavioral prescriptions and socially ideal gender roles. Violating these prescriptions can be costly or harmful to individuals who deviate from the social norms because it will bring adverse implications (distress, discomfort, disagreement, worsening happiness). To comply with social norms, women may avoid participating in financial activities, delegate economic responsibilities to their partners, and not invest their time and efforts in acquiring financial knowledge and skills. This rationale indicates that men have greater confidence than women in their financial skills (Barber & Odean, 2001; Bucher-Koenen et al., 2021; Lučić et al., 2020; Lusardi & Mitchell, 2023).

Numerous research investigations have shown that when it comes to tasks that men have traditionally performed and are seen as masculine, gender disparities in confidence are most pronounced (Beyer & Bowden, 1997; Bottazzi & Lusardi, 2021; Deaux & Emswiller, 1974). Driva et al. (2016) indicated that women suffer from inequalities in the resources provided for financial literacy due to different stereotypes and beliefs. Similarly, Tinghög et al. (2021) used data from the Swedish Standardized Scholastic Aptitude Test to investigate if the observed financial education gap can be recognized in non-numerical contexts, whether it is connected to financial matters confidence or whether it is related to stereotype threat, which postulates that ingrained biases regarding gender and finance limit women’s performance in financial tasks. They asserted that the financial gender gap is robust in non-numerical financial contexts and cannot be attributed to differences in confidence. Moreover, their mediation analysis results revealed a strong indirect relationship between gender and financial knowledge via financial anxiety, implying that the stereotype of women in the financial domain may partially explain the observed gender gap.

Bucher-Koenen et al. (2021) revealed that women’s lower confidence levels account for about one-third of the financial literacy disparity. They also claimed that both confidence and financial knowledge explain stock market participation. On average, women are found to make more cautious investments; that is, they are more likely to purchase fixed-income instruments and own fewer stocks than men (Almenberg & Dreber, 2015; Ansar et al., 2023; Sundén & Surette, 1998). Relevantly, given the current crisis due to COVID-19, it was discovered that women are less confident in their ability to withstand a financial shock and are more financially fragile (Hasler & Lusardi, 2019). Similarly, investing in riskier assets, Cupák et al. (2021) highlighted the importance of self-confidence in financial literacy.

The American Psychiatric Association (2013) describes anxiety as a condition marked by feelings of elevated tension and worries. Anxiety obstructs people’s happiness and adversely affects their quality of life, influencing financial literacy (Hofmann et al., 2010). Anxiety is another psychological factor that has an impact on financial literacy. Indeed, Hayhoe et al. (2012). A study revealed that when people have low anxiety levels, they are more inclined to engage themselves in good financial behavior.

Finally, future orientation is another psychological factor that affects the level of financial literacy. People who are futuristic and give more importance to the future than the past or present dedicate more time to acquiring more financial education, which affects their savings behavior (Kadoya, 2020).

FinTech Adoption and Financial Literacy

While FinTech, such as mobile phones and the Internet, have made access to finance easier, faster, and less expensive, increasing financial literacy in the past decade, the impact on gender gaps has varied across countries. FinTech companies leverage different digital services and meet customers halfway with simplified products. Mobile payments, robotic process automation (RPA), artificial intelligence (AI), blockchain, cryptography, biometrics, identity management, and cyber protection in online banking solutions contribute to personally educating customers, building trust, and ensuring continuous usage (Frame et al., 2019; Frost et al. 2019).

In emerging markets, more people can afford Smartphones every year. With moderate digital literacy, these users can access new financial education channels via dedicated apps and web applications. Many FinTech companies are creating interactive online educational platforms and investing in agent-to-user interaction, which has been a critical driver of adoption and success over the last 10 years. Financial literacy programs can effectively provide low-income families with the information and instruments necessary to manage money and make informed financial decisions at a lower cost by utilizing new FinTech (Arner et al., 2020; Thakor, 2020).

In banking and the financial services sector (FSI), the application of AI-based systems holds promise for facilitating safer and quicker transactions, stimulating creative credit scoring, boosting product development and segmentation, and streamlining customer onboarding and verification procedures through Digi-ID solutions (Biallas & O’Neill, 2020). Aicha (2023) discovered that FinTech can improve financial literacy among low-income individuals. She did a study in Kenya and discovered that FinTech products like mobile money can assist in enhancing financial awareness and access to financial services among low-income people. Similarly, Goswami et al. (2023) asserted that FinTech can make financial data more accessible and understandable. The study surveyed 1,000 people in India’s six states and discovered that FinTech organizations, such as microfinance institutions, can leverage technology to give financial information and services to those living in rural areas.

Consequently, the future of FinTech has enormous potential for all people, including Saudis. As a result of the projected benefits, the future of fintech has enormous potential for all people, including Saudis. According to the 2021 Saudi FinTech report, cashless activity is predicted to increase due to development in e-commerce, greater digital payments infrastructure, and government assistance. Moreover, FinTech advances could benefit disadvantaged groups disproportionately (Lee et al., 2021; Ouma et al., 2017).

However, evidence on whether FinTech helps to close the gender gap in the access to and use of financial services is scarce. There is evidence that FinTech Ecosystems (FEs) have gender parity gaps that go beyond the fact that most FinTech start-ups operate at the nexus of three traditionally male-dominated fields: technology, finance, and entrepreneurship (Kelly & Mirpourian, 2021; Ryll et al., 2021). In addition, the FSI has interconnected supply-side and demand-side dynamics that perpetuate gender disparities in an FE. Technology is not neutral, as evidenced by many wealthier economies with greater AI maturity (Han, 2021). AI, in particular, is inherently biased and can amplify pervasive gender and racial discrimination in its deployed ecosystems (Buolamwini & Gebru, 2018; Niethammer, 2020; West et al., 2019).

In line with the preceding literature discussion, the following hypotheses are posited:

H1. There is a significant difference in financial literacy scores among males and females.

H2. Demographic characteristics have a significant impact on financial literacy disparities.

H3. Socio-economic aspects play a substantial role in financial literacy disparities.

H4 .Psychological factors have a significant role in explaining the financial literacy gap.

H5. FinTech adoption decreases the financial literacy difference.

Materials and Methods

The type of research is descriptive and explanatory. The key objective of this research is to explore the basic and advanced financial literacy among the men and women in the Kingdom of Saudi Arabia. The research intends to investigate the impact of demographic, psychological, and socio-economic characteristics, and the impact of FinTech on financial literacy disparities. The research used primary and secondary sources (FinTech Saudi Annual Report, 2022). Primary data were collected by administering structured questionnaires, while secondary sources were utilized to identify the FinTech items available to Saudi citizens.

The questionnaire was divided into three parts. Part A comprised questions on the respondents’ socio-demographic profile, like age, marital status, income level, and place of residence. Part B comprised questions on measuring basic and advanced financial literacy levels. Questions pertain to knowledge on numeracy, compound interest, inflation, time value of money, stocks, stock market functions, bonds, bond maturity, bond prices, mutual funds, risk, returns, and diversification. The questions were drawn from Lusardi and Mitchell (2011, 2017) and Maarten van Rooij et al. (2011). Part C comprised questions on psychological factors. Part D included FinTech questions. Accordingly, these are a set of FinTech questions: (Q1) FinTech apps such as Ziggma, eSignal, Sigfig, and IBM Watson Analytics enhance the financial knowledge of users by providing practical exposure; (Q2) FinTech apps such as PayPal, Google Pay, and Apple Pay eases the financial transactions through digital payments; (Q3) FinTech apps such as Mobile Banking apps and Chime keep users informed about their bank account information; (Q4) Investment related fintech apps such as robo-advisors, MI Finance, etc. encourage savings habits amongst people; (Q5) AI tool “Robo-Advisors” which is part of FinTech leads to greater knowledge on financial literacy and vice-versa; and (Q6) AI Tool “Chatbot,” which is part of FinTech, positively impacts on financial literacy.

Saudi men and women comprised the study’s population; employees from various colleges were examined. The study’s sample size was 1100 random sampling units. Out of 1,100 Saudi employees, 1,029 responded. IBM SPSS (Statistical Package for Social Sciences) was used to compute descriptive statistics such as mean scores and Standard Deviation and inferential statistics such as t-Test, ANOVA, and regression models.

Results

Results of Three-Fold Blinder-Oaxaca Decomposition

Table 1 displays the summary statistics of the distribution of male and female respondents demography-wise. The age range 20 to 30 accounted for 70% of the female sample, whereas the age group 41 to 50 accounts for 73% of the male sample. Many male respondents (57%) have a finance background compared to 43% of females. In this regard, 70% of women respondents had only completed secondary school, while 83% of men had completed post-doctoral studies. As for location, most urban respondents (53%) were females. Among the sources of income, women comprised 53%, the salaried majority, 55% are male, and the women formed a major part 71% of the income group, which is less than $ 5,000 per month, mainly because they depend on rewards and also, they engage in small business. The findings also showed that most single respondents (65%) were women.

Statistics of Demographic Variables with F test of Financial Literacy Scores by Gender (N = 1,029).

The ANOVA test for mean financial literacy showed that the scores significantly differed among the groups within each variable, as the significance of all these variables was less than 0.05. These are marked with “***” against each F value, displayed in the last column of Table 1. These results are consistent with the findings of Barber and Odean (2001), Bucher-Koenen et al. (2021), Lusardi and Mitchell (2023), and Lučić et al. (2020), who documented that men and women have significant differences in their financial skills. The results support our first hypothesis (H1), which presumes that there is a significant difference in financial literacy scores between males and females. Similarly, the findings support the past literature, which revealed that socio-demographic characteristics, such as age, education, and marital status, significantly influence financial literacy (Li, 2018; Łukasz, 2021). They found that single women have a more challenging time repaying debt than single men, suggesting that there are gender disparities in borrowing and debt management. This result aligns with hypotheses two and three (H2 &H3), positing that demographic characteristics and socio-economic aspects significantly impact financial literacy disparities.

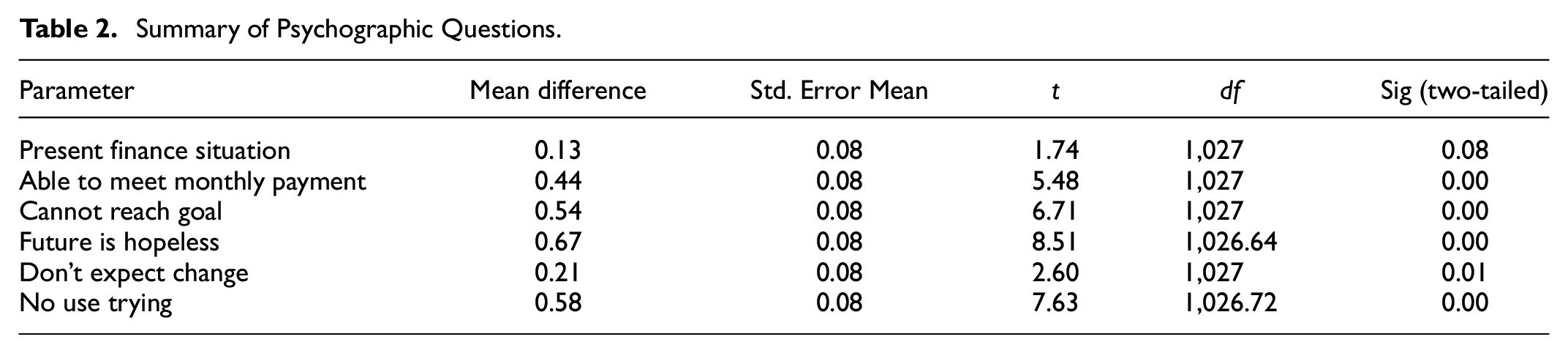

Table 2 presents the summary statistics of responses to the psychographic questions, in which the mean differences in financial literacy (FL) scores can be observed. The scores are substantially higher for males. Only for the first question, “present financial situation,” were the FL scores not statistically different. This finding clearly shows that women agree on “cannot reach goal,”“future is hopeless,”“don’t expect change,” and “no use trying,” whereas men agree less on these factors, which have a negative attitude aspect which probably indicates that they are low on confidence. The result is consistent with the findings of Kadoya and Khan (2020), who revealed a significant influence between psychological factors and financial literacy. The result supported hypothesis four (H4), which predicted that psychological factors significantly explain the financial literacy gap.

Summary of Psychographic Questions.

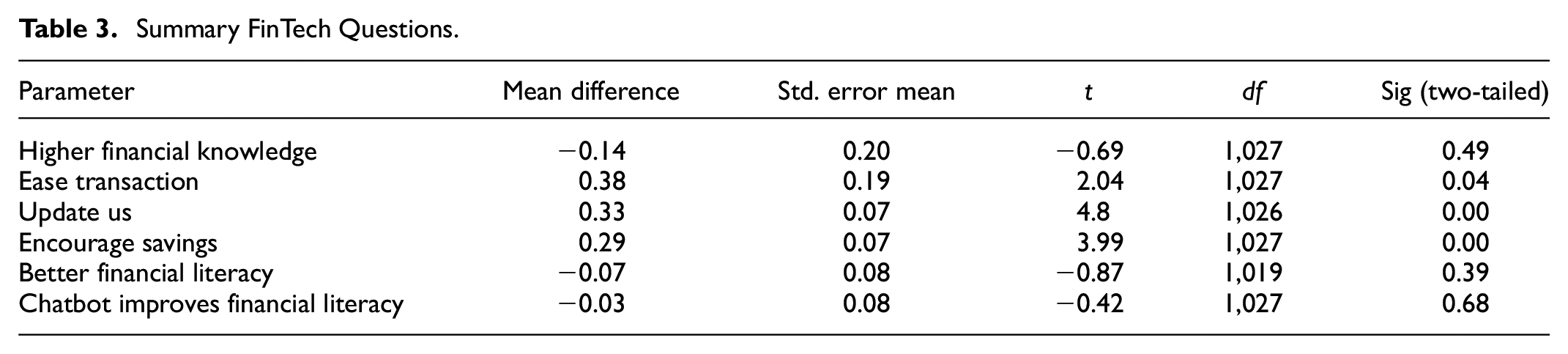

Table 3 displays the responses to the fintech questions where the scores are significantly different for “ease of transaction, fintech updates us, and it encourages savings,” with males having a higher score as the mean difference is positive. This result is due to males’ better adoption of fintech as they would have experienced its benefits. There is no difference in responses to “fintech leads to better knowledge, better financial literacy, and that chatbots improve financial literacy.”

Summary FinTech Questions.

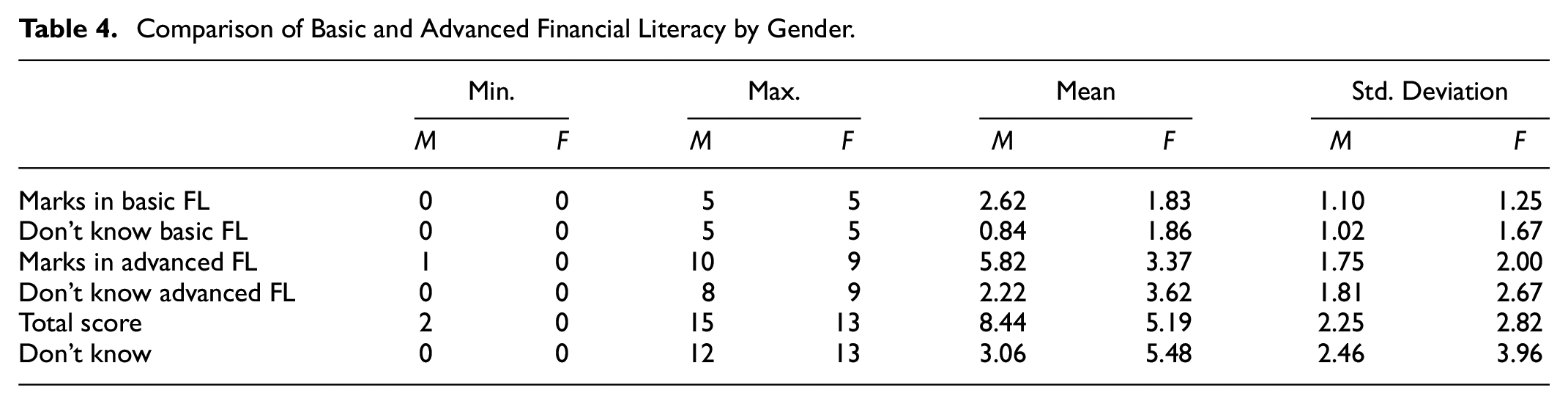

Table 4 compares and summarises the average scores of “don’t know responses” gender-wise and according to basic and advanced financial literacy. The average number of the “know responses” for females was higher at 1.86 compared to 0.86 for males, indicating that males chose the “don’t know options” less than females. In advanced financial literacy, it was 3.62; in males, it was 2.22. The overall average of the “don’t know option” was 5.48 for females and 3.06 for males.

Comparison of Basic and Advanced Financial Literacy by Gender.

Looking into the average correct options chosen, the males were higher at 2.62, 5.82, and overall, 8.44 correct answers compared to 1.83, 3.37, and 5.19 correct answers, respectively, by females in the basic, advanced, and overall scores.

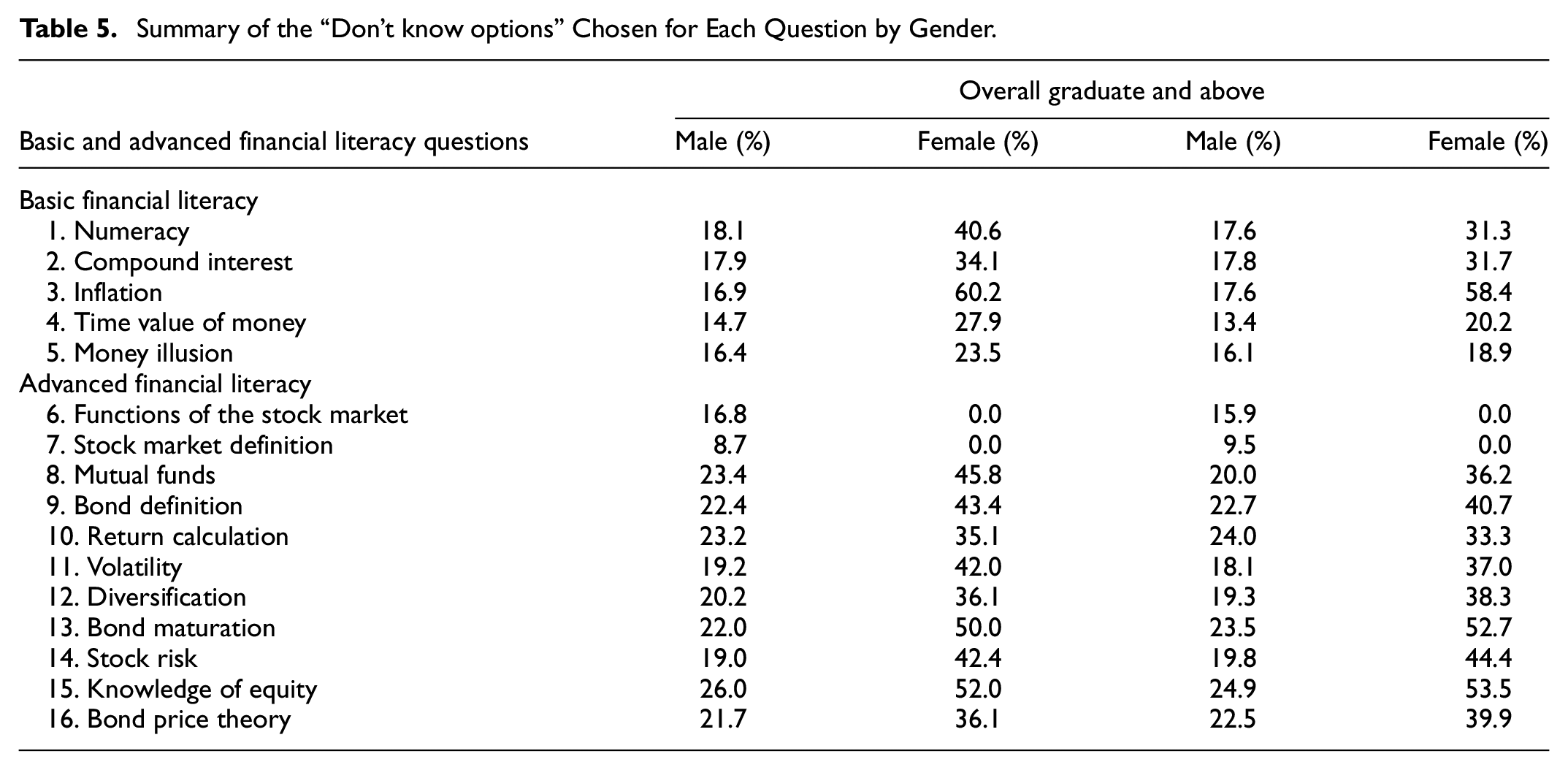

Table 5 summarises the “don’t know responses” to the 16 basic and advanced questions on financial literacy. The overall data shows the percentage of the “Don’t know” answers to each question by the 1,029 respondents of all education backgrounds divided by gender. The last two columns include only data from respondents who hold an education like a degree, master’s, Ph.D., and Post Doc. Both overall and educated women selected the “don’t know option,” indicating a lack of confidence compared to men. Only two questions relating to stock markets (Q6 and Q7) were marginally better for females than males. The maximum difference was related to the inflation question, which was 43.29%. The maximum difference for the same questions between males and females in the higher-educated class was 4.83%. The lowest difference was for the money illusion question, which was 7.1% overall, and the minimum difference was for the same money illusion question, which was 2.79%.

Summary of the “Don’t know options” Chosen for Each Question by Gender.

Table 6 summarizes the various independent sample t-test scores for gender, location, and background, which were statistically significant with t values 20.31, −4.91, and 3.32 with df of 950.38, 179.12, and 1,027, respectively. FL scores significantly differed between males and females, urban and rural respondents, and respondents with financial and non-financial backgrounds. Marital status comparison between single and married had a significant difference in the financial literacy scores with a significance level of 0.00. Married men had higher financial literacy scores, averaging 7.32 correct answers. This result is consistent with the previous literature, which documented that FinTech can aid in improving financial literacy among low-income individuals. Accordingly, the 2021 Saudi FinTech report showed that cashless activity is predicted to increase due to development in e-commerce, greater digital payments infrastructure, and government assistance. Similarly, FinTech advances could benefit disadvantaged groups disproportionately (Aicha, 2023; Lee et al., 2021; Ouma et al., 2017). The results support our hypothesis five (H5), which presumes that fintech adoption decreases the difference in financial literacy.

t-Tests for Demographic, FinTech, and Psychographic Questions (N = 1,029).

The independent samples t-test scores for the FinTech question examined whether the FL scores differed significantly for males and females. For the three FinTech variables, “higher financial knowledge,”“better financial knowledge, and “chatbot can improve financial literary,” the differences between the answers of males and females were statistically insignificant values of all three were 0.49, 0.39, and 0.68, respectively. For the three FinTech variables, “it eases transactions,”“updates us,” and “improves “financial literacy,” the answers of males and females were statistically different with values of all three were 0.00.

The results of the independent sample t-tests, which compared the scores of the males and females concerning answers to the psychographic variables, show that only scores on present financial knowledge were not significantly different, with a value of 0.08.

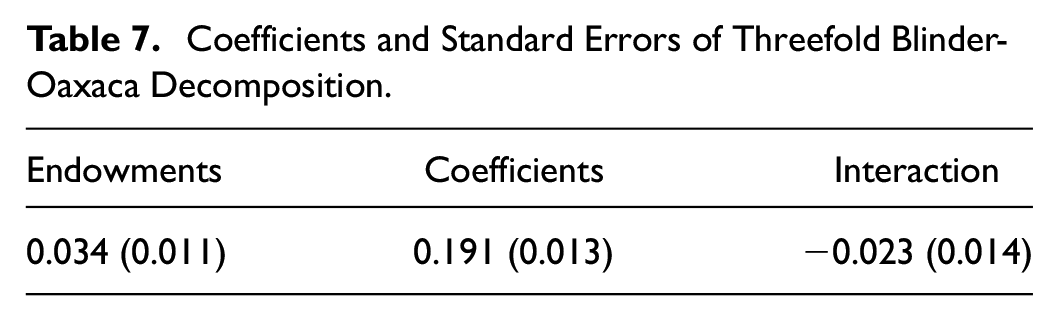

Table 7 displays the coefficients and errors of the threefold blinder-Oaxaca decomposition run on R; the values outside brackets are coefficients, and inside is the standard error. The total difference in the average score between the genders was 0.20, out of which 0.03 is due to endowments like age, income, education, marital status, location, and background. 0.19 is due to the slope or the regression coefficient difference. The value of -0.02 for interaction indicates no significant interaction effect of the independent variables. The dependent variable was the average total score, and the grouping variable was gender. A further study of the endowments through the plots indicates that the scores significantly differ due to the age, especially of the group differences in the category above 50 years. This result implies that women over 50 have very poor financial literacy compared to men.

Coefficients and Standard Errors of Threefold Blinder-Oaxaca Decomposition.

Results of Three-Fold Blinder-Oaxaca Decomposition

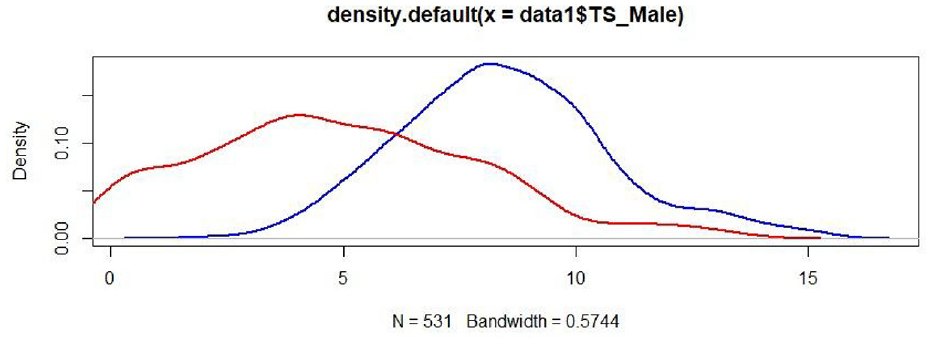

Figure 1 presents the kernel density plot of the total scores for males and females, which shows a substantial difference in financial literacy (FL) scores between the genders.

Density plot of the financial literacy scores of males and females.

Conclusion, Implications, Limitations, and Suggestions for Future Study

Financial literacy is one of the most momentous factors affecting the financial well-being of individuals. Thus, studies on financial literacy are momentously needed. The intensification of FinTech has undoubtedly had consequences on the determinants of financial literacy. Therefore, this study explores FinTech’s moderating impact on the factors contributing to the financial literacy gap. The study concludes that FinTech innovation influences closing the financial literacy gap. Additionally, it was confirmed that women lack confidence when responding to queries on financial literacy. According to the findings, the financial literacy gap is highly influenced by socio-economic variables like marital status and income as well as psychographic characteristics like “current financial condition,”“meet monthly payments,”“future bleak,” and “don’t expect improvement.” The spouse’s educational degree has an impact on the financial literacy gap.

This study stressed the significance of socio-economic status and how it affects financial education among individuals, emphasizing how various people might make financial decisions. Thus, the results of this study will be highly relevant to policymakers when implementing policies because the pervasiveness of digital transactions and virtual banking has changed how individuals manage their finances. Nowadays, people have greater rheostat over their finances using mobile applications and online podiums. This development improved participation in financial dealings and inspired users to become more acquainted with financial ideas and accrue their total financial literacy.

Finally, although FinTech has constructively affected financial literacy, there are probable downsides. For instance, individuals or corporations may depend too deeply on automated financial mechanisms without copiously understanding the fundamental principles. Consequently, a trade-off approach should be used for financial education that involves FinTech instruments with conventional financial literacy resources.

The results of this present study have vital implications for numerous stakeholders such as legislators, academicians, students, and society. Legislators can use its findings to develop and implement programs, strategies, and educational campaigns on financial literacy amongst different population groups. These can include innovations and initiatives targeted at various workplaces, schools, and civic organizations. Similarly, the findings of this study can inform about the financial behavior of different groups across age and gender. This information will assist academicians in developing a suitable financial education syllabus for students across different grades or levels. Academicians can understand which perceptions and skills are most effective for students to learn at which grades or levels. This study can also help students understand the significance of financial planning in the short and long term. This planning includes savings, investment, early retirement plans, and other robust financial decisions. Finally, society can benefit from the findings of this study by identifying various factors that affect individuals’ financial discipline and decision-making. As the study assists in understanding financial awareness and concepts, individuals can make informed and sound financial decisions on savings, investment, budgeting, early retirement, and debt management.

However, despite the various implications of this study, we identify some potential limitations. The study used a sample of 1,029 Saudi male and female employees at various Saudi colleges. Therefore, the study’s results might be used to generalize other Saudi colleges not captured in the sample. Thus, future scholars can utilize more samples covering all Saudi colleges. Similarly, financial literacy was measured using 11 dimensions. Future studies can include other dimensions of financial literacy that are not captured in the current study. This paper is restricted to demographic, FinTech, and psychographic factors. Therefore, prospective scholars can consider dynamics such as government policies, cultural background, and social networks.

Footnotes

Correction (February 2025):

Article updated to include the department name for the first affiliation.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research project was funded by the Deanship of Scientific Research, Princess Nourah bint Abdulrahman University, through the Program of Research Project Funding After Publication, grant No (43- PRFA-P-56 ).

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.