Abstract

Personal financial literacy (PFL) is an imperative life skill that all 21st-century students should have. Research shows that the levels of financial literacy in both developing and developed countries are very low across people of all ages. This deplorable state of affairs has negative implications on the well-being of the populace, as evidenced by increased indebtedness, lower saving, poor planning for retirement, and the making of many poor personal financial decisions. Recognizing the potential benefits of financial literacy at both individual and national levels, many countries have started to offer financial education in their schools. This article analyzed the business subjects’ curriculum at secondary school level in Botswana and literature published on the subject of PFL, and found that there exists a gap in this area and a need to offer PFL to all learners in the school system. Despite the need for such a move, Botswana does not have a deliberate program in its curriculum that specifically addresses this problem. This article discusses the benefits of personal financial education, the inadequacy of current business subjects to meet this need, and concludes by recommending a mandatory PFL subject in the Botswana secondary school curriculum.

Keywords

Introduction

Youths at secondary school level are faced with a future that involves lots of financial decisions, especially in their postschool lives. Lack of financial knowledge in adulthood may affect negatively on their spending attitudes, behaviors, and personal financial management. Financial decisions that may be adversely affected include the art of budgeting when living away from parents, saving and investing, how to maximize the use of banking services, and many more. Despite its potential positive impact, levels of financial literacy are unfortunately reported to be lower for high-income countries, and even much worse for middle and lower income countries (Lusardi & Mitchell, 2011; Xu & Zia, 2012). For this reason, policy makers around the world recognize that financial education is an integral component for meaningful development (Xu & Zia, 2012).

Personal financial literacy (PFL) for school going children has become an important intervention against issues pertaining to saving, investing, and spending habits of teenagers and how this will influence their future financial behavior. The failure to both promote and reinforce PFL in schools has the potential to affect consumers’ ability to make sound financial decisions about present and future personal needs (Davis & Durband, 2008). It is important that financial skills are imparted to students during their early days of schooling and before they are exposed to the ever-increasing complex financial products the financial services industry is always dangling via numerous media. Failure to equip students with the requisite personal finance skills is dangerous and counterproductive. According to Beal and Delpachitra (2003) “. . . this lack of financial skill will tend to impact negatively on their future lives through incompetent financial management” (p. 77). The inability of the school curriculum to impart PFL skills to students will likely produce individuals who are more likely to have higher levels of personal and household debt (Lusardi & Tufano, 2009), plan less for retirement (Lusardi & Mitchell, 2007), and less likely to manage wealth effectively (Stango & Znman, 2006). These factors, together with the global recession of 2008 have influenced the call for schools to teach financial education, especially in developed countries (Hite, Slocombe, Railsback, & Miller, 2011).

Although Botswana has ideals of a prosperous and wealthy nation enshrined in its national vision, Vision 2016: Towards Prosperity for All (Republic of Botswana, 1997), it fails to speak to issues of financial literacy more decisively. The national vision voices the need to reduce abject poverty and sees the way to prosperity as coming mainly through investment in entrepreneurial activity and diversification of the economy (Republic of Botswana, 1997). This perhaps explains why financial literacy programs have a stronger leaning toward financial management for entrepreneurship to the neglect of personal financial management (Xu & Zia, 2012). This means the vast populace, who have no entrepreneurial mind-set or intentions are left out in the lurch. The neglect of PFL is such an incredulous oversight especially that financial literacy may have a bearing toward achieving such a glorious envisioned future.

PFL is an invaluable survival skill in the 21st century (Hite et al., 2011). Therefore, teaching of PFL as a lifelong skill must cut across all the domains of human survival just as is the mandatory teaching of HIV awareness in secondary schools. Contrary to common belief, PFL is a not a business subject that is offered to students who are interested in pursuing careers in the world of business and entrepreneurship. Rather, PFL must be treated as a survival skill for every human being who lives in a monetary economy. PFL avails every individual the opportunity to manage and control their own personal finances irrespective of their position, career, and status in society. Depriving students these skills during their secondary school days may result in consumers who fall prey to predatory marketing gimmicks of retailers and financial institutions. In this article, we take the position that PFL should be made a compulsory subject in secondary schools, offered either as a separate subject or at the least, infused into other subjects, taught to all students irrespective of their subject choices. Through the review of literature on the subject, this study has the following objectives: to identify the content that should be included in PFL and discuss factors that make it necessary to teach secondary school students about PFL, to assess the extent to which the existing secondary school business education curriculum imparts financial literacy, and to suggest a possible approach to offering PFL at secondary school level in Botswana.

What Is PFL?

There is no single accepted definition of PFL. Several authors and researchers have diverse meanings of the term (Buckland, 2010; Fox, Bartholomae, & Lee, 2005; Marriott, 2007). Jump$tart (2015) describes PFL as “the ability to use knowledge and skills to manage one’s resources effectively for lifetime security” (p. 2). Financial literacy necessitates effective decision making and understanding of both the consumers’ and investors’ utilization of financial products, their rights and responsibilities, and the making of informed choices (Organization for Economic Co-Operation and Development [OECD], 2005). PFL focuses on the individual self rather than the organization, in matters concerning finance and the managing of financial resources.

The U.S. Financial Literacy and Education Commission (2007, cited in Yates & Ward, 2011) defines financial literacy as, “. . . the ability to use knowledge and skills to manage financial resources effectively for a lifetime of financial wellbeing” (p. 66). Hira (2009) explains it in terms of

. . . being financially knowledgeable about: (a) money, credit, investments, banking, insurance, and taxes; (b) the foundational concepts of financial management (e.g., risk, loss, gain); (c) and being able to use this knowledge to plan and make sound financial decisions. (p. 9)

It can be inferred that the goal of personal finance education is to equip individuals with the skills and ability to use financial knowledge for well-advised decisions in managing their own personal financial resources.

PFL Content in Secondary School Curricula

There is no single agreed secondary school PFL national syllabus or standard. Different countries have included various and diverse content in their curricula, irrespective of whether the course will be infused into existing subjects or will be offered as a stand-alone course. In the United States, the National Standards for Business Educators (2013) and the Jump$tart (2014) coalition include standards for PFL in broad content areas such as personal decision making, earning a living, managing finances and budgeting, saving and investing, using debit and credit cards, and risk management. Students are expected to develop basic personal financial plans for earning, spending, saving, and investing. Students must learn to read and understand credit card policies and statements, the impact of interest rates charged on only paying the minimum balance and extra charges for not paying balances by due dates (National Standards for Business Educators, 2013). In South Africa, PFL is located within the economic and management sciences subject where 40% of the content is financial literacy, 30% is the study of the economy, and 30% is focused on entrepreneurship (Republic of South Africa, 2011).

As already mentioned, the nature of subject content included in PFL for schools differs from country to country depending on whether it is embedded in other related subjects or it is a stand-alone subject. Emphasis is on ensuring that the students’ understanding of financial products and services which they are likely to use is deepened and also aid in the making of informed decisions without being preyed upon by the marketing gimmicks of financial institutions’ sales and marketing personnel whose motivation for commission may influence the advice they offer to their clients. The school curriculum ought to equip students for both the present and future, either as consumers and investors, to understand the financial terrain and how best to maneuver and get the best value for money.

Arguments for Mandatory Personal Financial Course in Secondary Schools

In this section, we discuss why financial literacy is important and why it should be introduced in the Botswana secondary school curriculum. First of all, financial literacy education is made important by the question of need. According to the World Bank study conducted by Xu and Zia (2012), the level of financial literacy is reported to be disappointingly low for both developed and developing countries. The National Foundation for Credit Counseling and the Network Branded Prepaid Card Association (2013) gives the following statistics about adults in the United States: 40% of adults prepare a budget and keep track of their spending, 43% worry about having insufficient savings for an emergency, and 38% are concerned they may not have enough savings for retirement. Close to 61 million (26%) adults do not pay their bills on time. With regard to personal financial knowledge, 40% of adults have rated their knowledge of personal finance at Grade C, D, or F. As unfortunate as these statistics may seem, financial literacy is reported to be far much lower in third world countries, Botswana inclusive (Xu & Zia, 2012).

There are few studies that have examined financial literacy in Botswana. One such study, conducted by Finmark Trust (2004, cited in Republic of Botswana, 2009), found that 48% of the people in Botswana were not making use of available banking facilities. This situation was attributed to lack of financial knowledge, among other plausible explanations. According to Jefferis (2012), the ratio of household debt to disposable income has been on the rise over the years. It increased from 24% in 1999 to 33% in 2012. He also observed that a higher percentage of household debt is skewed toward short-term unsecured loans and not long-term secured loans which is tied to vehicles and property. A scenario of this nature may imply that Batswana use the bulk of their debt to finance consumption. In addition, they will naturally incur higher interest rates which are burdensome to them as consumers but more profitable to commercial banks because unsecured loans tend to have relatively higher interest rates than secured long-term loans (Jefferis, 2012). Financial education, much better at an earlier age, could be one remedy to situations of this nature.

Similarly, the situation is not so pleasing for secondary school and college students for both developed and developing countries like Botswana. According to Yates and Ward (2011), in a 10-year period between the years 1997 and 2008, high school seniors in 47 states in the United States took a Jump$tart quiz that assessed content knowledge on economics and personal finance, scoring an average of 53% (Grade F). Jump$tart (2014) reports on the results of a survey of 962 first-year students from five universities and colleges across the United States who took a 50-item knowledge quiz covering five core areas of financial literacy (earning, spending, saving, borrowing, and protecting). None of the students scored an “A” grade, 11% obtained grade “B,” 22% scored a “C,” and 67% scored in the range of “D” to “F.” In addition, 37% students also indicated that finances gave them stress, 60% spent their means without using a budget, 70% either had a student loan or had intentions of getting one before they graduated, and 30% did not keep track of their spending.

A recent study by Pelaelo and Swami (2014) on personal financial management and financial stability of tertiary education students in Botswana found that although a substantial number students purport to prepare a budget for their finances, they spend the bulk of their income (living allowance) in the first few weeks of the month. Although this may be understandable for students who live off-campus because they incur many expenses such as rent, transportation, utilities, and others, on-campus students seem to lack restraint comparatively. Pelaelo and Swami find that 20% use up all their money in the first week of the month and another 60% in the first 2 weeks. Many of these students would then ask for supplementary funds from family and others which are never paid back. Such situations could be averted if these students came into tertiary education financially literate, a recommendation the duo also make. The consoling finding about college students is that their financial literacy was shown to improve with every year of tertiary education, reaching an average of 64.8% in their final year (Mandell, 2009, cited in Yates & Ward, 2011). More exposure that comes with living away from parents and getting to make financial decisions individually could be an explanation of this phenomenon.

Studies have shown that financial literacy skills gained at a young age last to adulthood. Bernheim, Garret, and Maki (2001) undertook a study that assessed the impact of financial literacy taught at high school level. The study found that students who were exposed to a financial literacy curriculum differed significantly from those who lacked such exposure. The students who took personal finance fared better as adults in terms of financial knowledge, savings, and wealth amassed. A later study by Peng, Bartholomae, Fox, and Cravers (2007) that examined the impact of financial literacy at high school level and college education somewhat corroborated these findings. They found that earlier experience with personal finance correlated with savings rates later on in life. It is therefore plausible to deduce from these studies that financial education has a positive impact on the financial management skills of young people which they carry into adulthood—It results in lasting habits.

Introducing personal finance at an earlier stage in the life of the youth does not only give high school students content knowledge about personal finance, it also gives them opportunities to develop positive financial habits they can carry on in life. In addition, teaching PFL at high school opens to young people more career opportunities in the world of personal financial management. Their job portfolio would entail such functions as retirement planning, advising people on insurance, investments, and other financial products in consultancy firms, insurance companies and banks, and other financial institutions. As employees, they may hold positions of financial planners and advisors, financial analysts, insurance brokers, wealth management professionals among others. The secondary school financial literacy program would lay foundation for tertiary education and career choice.

It has also been found out that financial illiteracy has far-reaching consequences. It is important because the lack thereof can have a devastating impact at personal and macroeconomic levels (Jefferis, 2012). When people lack financial knowledge, they are more inclined to making unwise and costly financial decisions in relation to borrowing, savings, investments, and retirement planning (Chen & Volpe, 1998 cited in Lusardi, 2008; Peng et al., 2007). The recession of 2008, which was the most devastating financial crisis in recent times since the great depression of the 1930s is a case in point. It led to foreclosures, bankruptcies, job losses, escalating credit card problems, and affected the global economy as well. According to Georgiou (2015), the financial crisis of 2008 was caused by a lack of financial knowledge in the general populace and the dishonesty of financial institutions.

Without proper training and discipline, people cannot be expected to make rational financial decisions and neither can financial markets be trusted to create a balance in the economy without a deliberate input of the human mind (Hira, 2009). Georgiou (2015) postulates that issues such as increased indebtedness, unemployment, and loss of homes are symptoms of an underlying problem of the lack of personal financial knowledge. If they are not recognized as such, correct preventive measures are less likely to be implemented, and the vicious cycle will continue.

Another reason why financial education is of paramount importance is the complexity of products and services that have come about as a result of the evolution of technology and financial innovation. Such sophistication makes the uninformed consumers to be more susceptible to fraud and mismanagement (OECD, 2005). Financial education educates students on the concept of risk and predatory lending (such as payday loans and loan sharks). They also learn ways of appraising lenders and are thus reasonably equipped to make wise financial decisions that would help them evade fraudulence and scams.

According to Georgiou (2015), teens in the age bracket of 12 to 19 have an estimated spending power of US$819 billion dollars globally per year. This makes them an obvious prey for targeted marketing from retailers and credit card companies. With limited personal finance knowledge to make informed consumption decisions, these youths can put themselves in a hole they may not easily take themselves out. According to Losey (2009, cited in Georgiou, 2015), there is a rise in college suicide deaths related to credit card debt and student loans.

Also, such knowledge would be helpful in equipping students to consider other options available to them besides loans. These may include application for grants, part-time employment, savings, and others. Even when they make decisions to take student loans, they would be in a good position to evaluate creditors and settle for better deals. Students would know the risks that come with owning credit cards and managing their debts. Although countries such as Botswana are not yet reported to experience such extreme situations in terms of predatory credit card companies, financial literacy will protect youthful graduates from such behaviors by banks as soon as they start working.

Financial knowledge also has wealth distributional implications. According to the OECD (2005), people with the most financial knowledge are often in the well to do class. This means that lack of financial knowledge contributes to the increase in the gap between the rich and the poor. The poor who lack financial knowledge are more likely to spend unwisely, to be defrauded of the hard earned means, and even miss on good investment opportunities (OECD, 2005). Consequently, this worsens prevalent inequalities in society.

It is also worth to note that the benefits of financial literacy accrue to multiple stakeholders. One of the reasons why financial education is a worthy investment from an early age is because its benefits go beyond the individual beneficiary of such a program. OECD (2005) identifies other beneficiaries of financial education among the populace to be financial services industry, policy makers, and the economy as a whole. The financial industry will benefit from increased participation of informed consumers of their various products such as savings, investments, and declines in defaults on loan repayments. There would also be more competitiveness, efficiency, and transparency due to a rise in the number of informed participants in the industry. Policy makers would also have a reduced regulatory and supervisory workload which is often associated with monitoring, interventions, and pushing for reforms of the financial sector. The economy as a whole would be more stable as financial markets run better, thus cutting down expenditures which would occur in the future. For example, as people are taught from a young age to manage their finances well, the expenditure on future welfare programs may be greatly reduced if the students grow up to be financially competent citizens. This is perhaps important for Botswana where household savings are low.

Method

This study analyzed the data on the number of students who have the potential to be exposed to PFL through taking business subjects and mathematics at senior secondary level. It also analyzed syllabi for different subjects at senior secondary school level to determine the extent to which they integrate or infuse financial literacy content. This approach was taken because the syllabi determine what is taught to learners at this level, and is able to provide information on the content taught. This is important because in Botswana’s education system PFL is not offered as a stand-alone subject. Some selected specific topics are taught in different subjects. As is widely believed, business subjects incorporate some elements of financial literacy, albeit at different levels, while mathematics is also inclusive of some topics that revolve around the basic PFL elementary skills. Thus, the study examined the extent to which the syllabi for accounting, business studies, commerce, and mathematics on their inclusion of PFL in the curriculum in terms of aims, objectives, and content.

An Analysis of PFL in the Botswana Secondary School Curriculum

The Botswana General Certificate of Secondary Education (BGCSE) curriculum came about as a result of the localization of the Cambridge Overseas School Certificate starting in 1999. This was in fulfillment of the recommendation of the second National Commission on Education of 1993 and the Revised Policy on Education of 1994, which called for final examinations at senior secondary school level to be graded in Botswana and not Britain as it had been the case since Botswana’s independence in 1996, and a vocationalization of the curriculum at secondary level through the introduction of practical subjects among other things (Weeks, 2002). The BGCSE have two major facets: Group 1 entailing core subjects (English, Setswana, and mathematics), and optional subjects group which are further classified into sciences, humanities and social sciences, creative, technical and vocational, and enrichment subjects (Republic of Botswana, 1998). Business subjects’ localized syllabi, falling under the subgrouping of practical subjects or creative, technical, and vocational group, were thus developed, consisting of three subjects, namely, accounting, business studies, and commerce.

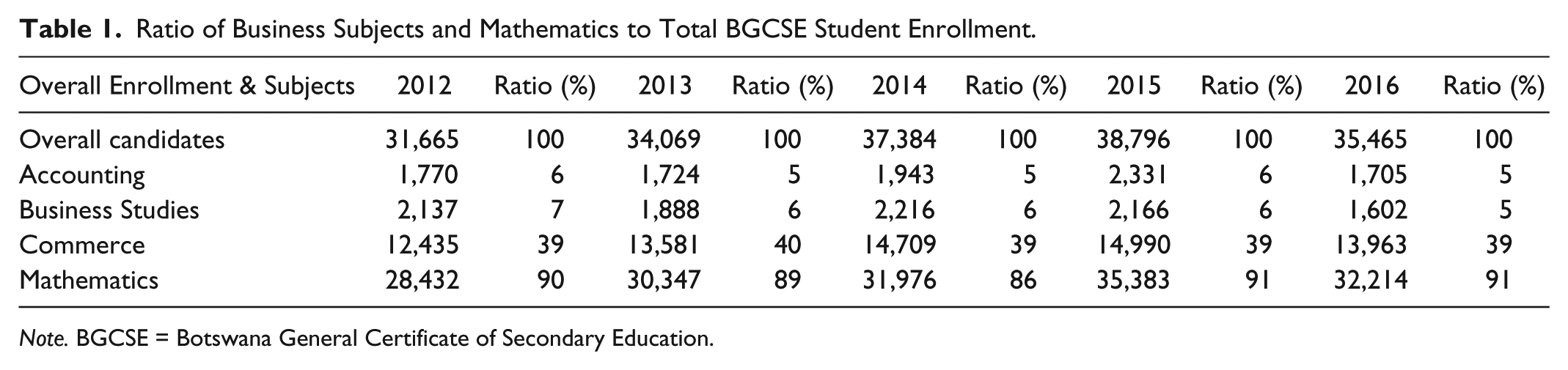

The BGCSE business education curriculum is mandated to equip students of the ages ranging between 16 and 18 years old, on average, with some financial skills for both the world of work and everyday life. This curriculum encompasses the impartation of a variety of cognitive, psychomotor, and affective skills to prepare the students for the future. The Botswana Examinations Council (BEC; 2017) website provided data on the total enrollment at BGCSE and the number of students who sat for final examination for each subject. The data for the past 5 years of business subjects and mathematics, showing the ratio or percentage of students who sat for the exams for these subjects in relation to the total BGCSE graduates for each year, have been summarized in Table 1. Based on these statistics, students who took accounting for the past years have averaged 5%, business studies 6%, commerce 39%, and mathematics 89%, respectively, of total BGCSE student enrollment. Although these figures focus on students who sat for final examinations at senior secondary level for the past 5 years, they also give a glimpse on the number of students who are exposed to PFL at this level. Of course, this exposure to PFL is through integration in business subjects and mathematics, albeit at differing levels depending on the depth and coverage of such.

Ratio of Business Subjects and Mathematics to Total BGCSE Student Enrollment.

Note. BGCSE = Botswana General Certificate of Secondary Education.

Below we analyze the level or extent to which the curriculum endeavors to equip students with PFL skills through the subject matter and content of the business education and mathematics syllabi. Analysis of individual subjects’ rationale, aims and topic objectives and content in comparison with the anticipated personal finance skills aids to ascertain the extent and level of coverage and integration of PFL in the Botswana school curriculum.

Accounting

The rationale of the accounting syllabus is geared toward preparing learners toward success in world of work and business (Republic of Botswana, 2002a). Emphasis is on how the learners can be effective stewards and custodians of business owners’ resources. The recording, classification, and summarization of financial transactions are business-oriented, while the skills to plan, budget, and making of prudent financial decisions is focused on the business rather than the individual. Although the syllabus aims to develop skills to assist learners in solving technical problems, the thrust is on issues pertaining to learners developing into accounting practitioners in different organizations and in different capacities. The content covered in the accounting syllabus aims to equip the learners to be effective and efficient employees and does not address the issues concerning the individual’s ability to self-administer his or her own personal finances. Most of the topics included in the syllabus lack the deliberate inculcation of skills to address the need for personal finance skills in their day-to-day lives outside the world of work.

Business studies

The business studies curriculum endeavors to impart basic concepts of entrepreneurial skills that will enable learners to create jobs for themselves and for others in future (Republic of Botswana, 2002b). The focus of the syllabus is on equipping learners with business knowledge skills to enable learners to be employed or self-employed. Practical skills on how to run a business efficiently and understand the challenges faced by businesses are the major focus. Very few topics, for example, the economic problem, have any relevance to the PFL content. Although some topics such as budgeting and forecasting and cash flow forecast may be relevant to PFL, the main focus in this syllabus is on the business entity rather than the individual.

Commerce

The syllabus rationale includes the need for learners to explain commercial activities and behavior of institutions in the commercial world (Republic of Botswana, 2002c). The content covered in this syllabus equips learners with PFL skills to a greater extent in comparison with the accounting and business studies syllabi. Topics such as production and satisfaction of needs and wants, credit trading, consumer protection and customer relations, simple contract of sale, methods of payment, banking, principles of insurance, types of insurance, and procedures of buying insurance and making claims are relevant to PFL. Other topics relevant to PFL but taught with reference to businesses only include keeping books, business finance, business planning, risks in business, and customs and excise department in Botswana.

Mathematics

Mathematics is a mandatory subject in secondary schools in Botswana. Topics such as applications provide a link between mathematical principles and practical life situations relating to money and personal finances. The topic itself aims to inculcate in students skills to be able to make calculations using money; convert one currency to another; and use given data to solve problems on personal and household finance involving earnings, discount, and profit and loss thus providing a foundation for some PFL content. The topic on fractions which aims to enable students to apply fractions in solving problems and use percentages to calculate and compute simple interest, compound interest, ratios, and proportions covers foundational basics on personal finance numerical analysis. Although mathematics offers some knowledge and skills that may be applied to PFL, it falls short on many other topics that it does not cover such as insurance, managing risk, debt management, broader coverage of financial institutions, and their services to name a few.

Implementing the PFL Course

Having explicated on the limitations of the current business education subjects and mathematics offered in Botswana secondary school on equipping students with financial literacy knowledge and skills, we move forward to suggest how PFL may be implemented. The assessment of business subjects and mathematics discussed above shows that these subjects fall short at offering students all the necessary PFL content. This is even exacerbated by the fact that business subjects, even though lacking, are taken by very few students because they are optional subjects. At the heart of implementation of PFL are two basic issues. The first being effectiveness in increasing student knowledge which translates into financial competence and desired consumer behavior, and the second being educational effectiveness resulting in the increase in the number of students who participate in the program (Tennyson & Nguyen, 2001). Although there are various approaches used in other countries (Pelletier, 2013), we suggest alternatives that may work in Botswana. Among the possible options to implementing PFL to all students at senior secondary education level is to offer it as (a) a stand-alone examinable course, (b) a compulsory personal financial awareness course that is not examinable, and (c) infusion into existing subjects.

Each of these alternatives has pros and cons. The first two alternatives are discussed co-jointly as they are close. Making PFL a requirement for graduation ensures there is a systematic program of implementation, well thought out standards and learning outcomes, and consistency across all schools in the nation. This will make measurement of effectiveness to be more valid and reliable. However, Brown, Collins, Schmeiser, and Urban (2014) submit that challenges may arise when making personal finance mandatory for graduation at high school level. These include limited availability of time and other resources, different level of rigor in courses and unclear timing in implementation of financial education. Requiring personal finance to be taken by every student before graduating means schools must give up some of the already limited time and content to be taught in other subject areas. Schools would also have to commit financial resources to the project to fulfill such a requirement. If they do not get any financial assistance from the government, the project would never be successful. Also, if the subject is offered without requiring examination, students may not feel the need to take it seriously and lose on the intended goals of offering such a program.

Infusion and integration of emerging issues is not new to the Botswana education system. It is in fact enshrined in the Botswana senior secondary school curriculum blueprint which states that “sensitive to emerging issues which will be infused, integrated and/or developed into different subject areas as the need arises” (Republic of Botswana, 1998, p. 4). Infusion has the advantage of using the existing teaching personnel without placing demands on hiring more educators. Also, the timetables do not have to be changed to cater for a new subject. However, Molosiwa (2010) examines the extent to which Botswana teachers infuse emerging issues such as HIV/AIDS and information and communications technology (ICT) into their various teaching subjects, and her findings indicate that educators struggle with integrating emerging issues. They lacked resources and in-service training in the emerging issues. Teachers may not necessarily have the knowledge and competence levels required in infusing emerging issues they are expected to integrate into their specific teaching subjects and this could compromise learning outcomes. She also points out that educators may have problems with infusion because the curriculum is exam-driven. Teachers tend to weigh teaching subject content against the emerging issues and focus their energies on completing the syllabus so that their students are ready for the national examinations.

A study that examined financial literacy of 283 educators across Israel by BenDavid-Hadar (2015) confirms in part these findings, especially in relation to educators’ PFL skills, behaviors and attitudes. The study found that educators have very low financial literacy, and goes further to suggest that their knowledge and skills need to be improved through training if they (educators) are to be effective at imparting PFL skills to learners. These findings, by Molosiwa, 2010 and BenDavid-Hadar (2015), somewhat shed light on what is likely to carry if PFL is infused into existing subjects. Its infusion may be low and this will mean that students will get different levels of rigor and accountability, which naturally casts aspersions on the effectiveness of this approach.

The difference in levels of rigor and accountability means students in some schools may not really get much that is useful from personal finance courses. The differences create a bias in effectiveness of personal financial education (Brown et al., 2014). It can create a false impression that personal financial education in high school is not effective. Rather than being a reason not to make personal finance mandatory, this is a call to have more standardized personal finance classes, where students are taught the same content at the same level of rigor. This way, effectiveness or the lack thereof can be truly established. In schools where there is no accountability, it is hard to make sure teachers do a diligent job and students may not see the need to take the subject more seriously.

Conclusion

PFL is a must-have life skill that cuts across every level of human development and survival. Having gone through the literature on teaching personal finance at high school level, we have arrived at the conclusion that PFL should be a compulsory and examinable subject in secondary schools. First and foremost, taking a PFL course should be mandatory at secondary school due to the question of need. The evidence presented above shows gaps at all levels in society with regard to financial literacy. Without proper training and discipline, people are more inclined to make misinformed decisions about the use of financial resources. We cannot rely on financial institutions that exist to make profit from the nation to provide people with financial literacy. Their main aim is to make profit, and the more gullible and ignorant members of society are the most likely to be exploited. This is evidenced by the recession of 2008 and credit card companies giving the youth who just turned 18 years old credit cards in some countries.

PFL classes have been shown to increase financial knowledge and improve behavior on managing finances. Students at secondary school level are already preparing for college and university where they will have to make financial decisions for themselves. To all these students, knowledge of financial skills such as budgeting, managing debt, earning a living, insurance, and being an informed consumer become handy where students do not have the immediate guidance of their guardians or parents.

Some of the students would naturally not make it to tertiary education but join the workforce immediately after high school. As they join the workforce, they will immediately need financial literacy skills to make wise financial decisions in terms of savings, borrowing, investment, and planning for retirement. These skills are invaluable to both students who go to tertiary education and those who do not as the knowledge they gain will carry through into adulthood. Worries about having sufficient savings for emergencies and retirement which are high among adults are more likely to be reduced.

We acknowledge the limitations of implementing a mandatory PFL subject at high school. Problems such as limited time are a call for policy makers and educators to prioritize something that is more likely to affect the well-being of the nation. The government should also be willing to commit financial resources to this noble course, looking at its benefits in the long term. Although infusion and integration of PFL into existing subjects may be one option, it may create more harm than good. It may lead to differences in rigor and accountability which may undermine the effectiveness of implementation. We conclude by saying that a PFL course should be introduced in secondary schools and that it should be required for secondary school graduation due to its many potential benefits to the youth and the nation at large, now and in the future.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.