Abstract

Using a sample of 5,039 hand-collected panel data from Bursa Malaysia spanning 2009 to 2015, this study examines the impact of brain-gain directors (i.e., foreign directors and returnee directors) on firm performance. A two-step robust system GMM is implemented to control for data endogeneity. In line with the resource-based theory, the findings show that brain-gain directors are positively associated with firm performance. Specifically, for each additional foreign director or returnee director on the board, firm performance is expected to increase by an average of 7.41% and 3.23%, respectively. This indicates that a director’s foreign exposure and connectivity are valuable firm resources, with foreign-born directors contributing more significantly to firm performance due to their greater international experience and resources compared to returnee directors. However, further analysis reveals that this positive relationship diminishes when the board consists solely of males, suggesting that gender diversity on the board is essential for brain-gain directors to effectively contribute. A diverse range of directors across borders (e.g., nationality and international working/tertiary education background) and genders represents a spectrum of assets that could potentially provide competitive advantages to firms. The results align with the resource-based theory and support the implementation of brain gain and corporate governance policies that encourage greater female representation on boards.

Keywords

Introduction

Given that human capital is a vital resource for nations to compete on the global stage and foster development, the departure of the best and brightest, commonly referred to as brain drain, has long been a concern globally. Coined in the mid-20th century by the British Royal Society, brain drain originally described the migration of scientists and technologists from the United Kingdom to North America (Cervantes & Guellec, 2002; Gibson & McKenzie, 2011). While the sending country (i.e., the United Kingdom) experiences brain drain, the receiving country (i.e., North America) receives the talents and encounters brain gain. In today’s increasingly interconnected world, human capital movement across borders is so convenient that brain drain, talent outflow, and human capital flight are inevitable. Consequently, policymakers and researchers have noticed a notable shift in attention towards “reverse brain drain,” another form of brain gain to maintain the talent pool in the country. Instead of drawing in talent from other countries, this shift entails skilled individuals who have studied or worked abroad in developed countries returning and contributing to their home countries (Ho et al., 2015; Saxenian, 2005).

The trend of attracting local talents who stay abroad to back and work in their home countries instead of foreign nationality talents aligns with the findings of Y. Dai et al. (2021), who observed a shift in firms’ hiring criteria for chief financial officers. Rather than prioritising demographic traits (e.g., nationality, age and gender) and functional background, firms seem to value a new attribute in hiring, which is the foreign experience gained from developed economies (Y. Dai et al., 2021). Prior literature in management also viewed directors’ countries of origin and foreign experiences as distinct characteristics which affect firm performance. For instance, Ruigrok et al. (2007), Masulis et al. (2012), and Estélyi and Nisar (2016) measure the effects of foreign nationality directors, while Wen et al. (2020) and Belaounia et al. (2024) investigate the impact of directors with foreign experience. However, these studies often treat foreign nationality and foreign experience as separate factors, not considering their combined effect.

Similarly, researchers who define and address the issue of “brain gain” in the firm focussing either on foreign experience (Y. Dai et al., 2021; Giannetti et al., 2015; L. Liu et al., 2022) or foreign-born individuals (Chen & Yoon, 2023; Hussain et al., 2024; Wang et al., 2023), but not both at the same time despite local-born talents with foreign experience and foreign-born talents are brain gain to the firms. Notably, there is a gap in the “brain gain of corporate board” literature regarding the effects of foreign talents (foreign directors) and local talents with foreign experience (returnee directors). This distinction is essential as foreign directors and returnee directors, despite both being considered sources of brain gain, are fitted with different levels of “foreignness” and thus affect firm performance differently. Foreign directors and returnee directors have various levels of exposure to foreign cultures and environments: the former are born and raised overseas, while the latter have spent limited but significant time abroad. Using resource-based theory, this study posits that the international experience of these directors constitutes valuable resources for firms. Foreign directors bring a deep understanding of global markets and diverse cultural perspectives. In contrast, returnee directors offer local and international insights, potentially facilitating better strategic decisions and cross-border collaborations compared to local talents without foreign experience.

This study contributes to the current literature by introducing the concept of “brain gain” of corporate boards, which comprises both foreign-born directors and returnee directors with foreign working or tertiary education experience. This study aims to bridge the gap in the literature by providing a comprehensive analysis of the individual and combined effects of these brain-gain directors on their firm performance. By distinguishing between foreign and returnee directors as two distinct categories of brain-gain directors, this study clarifies whether varying levels of international experience affect firm performance. In this globalising world, talent is not only being poached across borders but also across genders. In further analysis, this study examines whether the presence of female directors significantly influences the relationship between brain-gain directors and firm performance. Given the increasing emphasis on gender diversity in corporate governance, we hypothesise that female directors may enhance the positive impact of brain-gain directors by contributing additional perspectives and fostering a more inclusive decision-making environment. Tobin’s Q, the market-based measure which incorporates market expectations of a firm’s future performance (Belaounia et al., 2024), is selected as the measurement of firm performance. Foreign directors and returnee directors are valuable human capital resources and possess intangible resources, such as their knowledge, reputation, international connectivity and cultural exposure, that contribute to the firm. As stated by Usman et al. (2020), brains concentrated at the highest levels of an organisation have a significant multiplier effect, influencing outcomes throughout the company. Hence, a board of directors with diverse national backgrounds and foreign experience can generate positive results for the firm.

We study this question in the Malaysian setting because it offers several advantages. As a small and open economy, Malaysia has always adopted an open policy to attract foreign investments to contribute to its economic development. Since the pre-colonial era, from the days of Melaka city, the land of Malaya has always been the destination of foreigners from both the East and the West for commercial activities to create wealth. Economically, Malaysia is a good role model for emerging markets where the private sector remains the main driver of economic growth, especially after the 1997 Asian Financial Crisis. The development of these corporations needs to be supported and led by talented company boards and management. Foreign directors have grown considerably in Malaysia, with many independent directors from Singapore and the United States (Shukeri et al., 2012). Malaysia’s current efforts in promoting foreign talent can be traced back to 1995 when the Ministry of Science, Technology, and Innovation (MOSTI) launched its first brain gain programme (Davenport & Prusak, 1998). Then, Talent Corp Malaysia Berhad (TalentCorp), an agency in the Prime Minister’s Department, was also mandated to assess and fulfil Malaysia’s talent needs. TalentCorp has implemented numerous brain gain programmes that offered net fiscal benefits estimated at RM27,000 per returned applicant (World Bank, 2011). However, statistics on the specific contributions of brain-gain directors remain limited, primarily due to data privacy and scarcity and the challenges associated with tracking returnee individuals. While there is an abundance of anecdotes, there is a dearth of research focussing on brain gain issues within the context of corporate finance. Most recent studies on brain gain in Malaysia have involved interviewing and surveying foreign and returnee directors, as well as analysing the push and pull factors associated with brain drain and brain gain. Through the utilisation of hand-collected data from company annual reports, we are able to trace the backgrounds of directors, identify brain-gain directors, and estimate the magnitude and significance of brain gain within corporate boards and its impact on firm performance. The panel data collected enables us to analyse brain gain issues within corporate boards across different years and firms.

Our results show that regardless of foreign or returnee directors, their experience, knowledge, and expertise are valuable, rare, inimitable, and non-substitutable resources that make up board potential (Barney, 1991; Barroso et al., 2011). Using the sample of 803 firms from 10 industries in Bursa Malaysia from the year 2009 to 2015 (total of 5,039 observations), the two-step robust system GMM estimation result showed that for every additional number of brain-gain directors on board, we could expect firm performance to increase by an average of 4.55%, holding others constant. For every number of foreign directors and returnee directors increased on the board, firm performance is expected to increase by an average of 7.41% and 3.23%, respectively. Corporate boards are expected to comprise members of diverse nationalities and international working/educational backgrounds. As countries continuously target high-skilled talent and value international experience by paying higher wages, it raises a similar concern in a corporate setting, where shareholders are concerned about whether hiring foreign directors is worth the money. Besides that, we also find that the presence of at least one female director on the board has a significant moderating impact on the relationship between brain-gain director and firm performance. Further analysis of directors’ gender showed that the positive relationship between the brain gain of the corporate board and firm performance disappeared in the all-male board but was more pronounced in the gender diversity board. The findings align with resource-based theory, which proposes that human capital is one of the firm’s resources. A diverse array of human resources spanning borders and genders constitutes a variety of resources that can potentially confer competitive advantages to firms. It also supports the implementation of the brain gain policy as well as the Malaysian Code on Corporate Governance 2017, which encourages firms to have more females on the board.

By investigating the relationships, firms can better leverage the diverse experiences and nationalities of their board members to enhance their competitive advantage in the global market. This research not only contributes to the academic discourse on brain gain and board gender but also offers practical implications for corporate governance and international business strategies. The brain drain issue does not only affect developing countries such as Malaysia, China, and India but also developed countries like the United States, the United Kingdom, and Singapore. However, talent outflow in the United Kingdom and Singapore was alleviated by a large number of foreigners (Batalova, 2007; World Bank, 2011). In South Korea, returnee workers come back with knowledge and unique experiences acquired abroad, creating a favourable environment for South Korea to develop its economy (Song, 1997). Developing countries such as Malaysia need to identify the right talents to lead the corporations. Overall, the findings underscore the importance of strategic hiring and board composition to leverage diverse talents (i.e., nationality, foreign experience, gender), enhancing firm performance and competitive advantage.

The rest of this paper is divided into the following sections. Section 2 presents the literature review and hypotheses development. Section 3 discusses the data and methodology, while Section 4 shows the results and discussion. Section 5 is our concluding remarks.

Literature Review and Hypotheses Development

Resource-Based Theory

Over the past five decades, resource-based theory (RBT) has become a pivotal framework in strategic management, elucidating how firms’ internal resources and capabilities influence their competitive strategies and market performance. The theory’s roots can be traced back to 1959, when Edith Penrose published “The Theory of the Growth of the Firm” (Curado, 2006). Penrose viewed the firm as an administrative organisation with a collection of physical and human resources. These productive resources provide the firm with different services or functions, where the same resources can be allocated in different ways depending on the decision by the firm.

The core idea of resource-based theory is that organisations should look inside the firms for the resources to create the sources of competitive advantage (Nemati et al., 2010; Wernerfelt, 1984). In a strategic management context, a firm is said to have identified its internal strategic factors, including its strengths and weaknesses, so that it can determine whether it can take advantage of opportunities while avoiding threats. One of these internal scanning processes concerns recognising and developing its resources (Wheelen & Hunger, 2012). Resources are assets and the basic building blocks of the organisation (Wheelen & Hunger, 2012). RBT posits that competitive advantage arises from internal resources that are valuable, rare, inimitable, and non-substitutable (VRIN criteria; Barney, 1991). Resources, as defined by various scholars, include both tangible and intangible assets. Barney (1991) categorised them into physical, human, and organisational resources. More recently, resources have been grouped into tangible, intangible, and human categories (Barney, 1995; Wheelen & Hunger, 2012) as shown in Figure 1.

Types of resources.

Other than the word “resources,” two important terms in resource-based theory are “capabilities” and “competency.” Capabilities refer to a firm’s ability to exploit its resources, and competency refers to the cross-functional integration and coordination of different capabilities (Wheelen & Hunger, 2012). According to Barney (1991), firm resources include all assets, management skills, capabilities, organisational processes and routine, firm attributes, information, knowledge and so on, as they are all controlled by a firm and enable the firm to implement strategies that improve its efficiency and effectiveness (Barney, 1991; Barney et al., 2001). Thus, firm capabilities and competency, the managing process of the interaction among resources to turn input into output (Wheelen & Hunger, 2012), are all considered as the firm’s resources. Effective boards allocate resources efficiently and provide critical oversight to ensure that these resources are used effectively and sustainably. This argument is supported by recent researchers, as reflected in Figure 1. For example, reputations, skills, know-how, and capacity for communication and collaboration.

The Role of Brain-Gain Directors

Using resource-based theory, the roles of the board could basically be separated into two: a human capital resource for strategy setting and providing critical resources to the firm by connecting the firm to other resources. Researchers such as Araci (2015), Barroso et al. (2011), O. Dai and Liu (2009), and X. Liu et al. (2014) have explored these aspects in depth, highlighting the impact of board members’ unique backgrounds and experiences on firm performance.

Human Capital Resource for Strategy Setting

From a strategic perspective, brain-gain directors are seen as valuable human capital resources. Their skills, knowledge, and expertise can offer firms a competitive edge. As businesses and corporations become more global, firms are increasingly looking for board members with international experience. These directors bring with them unique insights and practices learned abroad, which can be instrumental in enhancing firm performance. For example, Araci (2015) notes that multinational firms benefit from directors who provide global knowledge in production, marketing, and management. Such directors are often considered valuable, rare, inimitable, and non-substitutable resources (Barroso et al., 2011).

Providing Critical Resources to the Firm by Connecting the Firm to Other Resources

Beyond strategy setting, directors play a crucial role in connecting firms to critical external resources through their networks and social capital. Brain-gain directors, with their extensive international ties and social capital, can act as boundary spanners, facilitating cross-border acquisitions, foreign capital raising, and international sales (Giannetti et al., 2015; Masulis et al., 2012). These directors leverage their connections to reduce transaction costs and stimulate trade and foreign direct investment (World Bank, 2011).

Another theory that may support the relationship between brain-gain directors and firm performance is Upper Echelons Theory (UET). According to UET (Hambrick & Mason, 1984), the characteristics of the highest-ranking individuals within an organisation, such as the chief executive officer (CEO), top management team (TMT), and board of directors (BOD), can influence the corporation’s involvement in risk-taking activities. Their experiences, values, and personalities significantly shape their interpretations of situations (Hambrick, 2007), ultimately leading to varying firm performance. Drawing upon UET, foreign directors who were born and raised in their home countries, returnee directors who have spent a significant but limited time working and studying abroad, and local directors without foreign experience may each have different exposures to international experiences, foreign cultures, and values. These exposures shape their perspectives and influence their business decision-making and performance. Although UET suggests that directors’ international experiences play a role, it does not clearly indicate the direction of the hypotheses development (i.e., whether the relationship is positive or negative). Therefore, resource-based theory is utilised in the following hypotheses development.

Hypothesis Development: Brain-Gain Directors and Firm Performance

Returnee directors are often knowledgeable and fitted with specific human capital related to a range of skills and knowledge with varying degrees of transferability. They may have acquired such knowledge academically from their general tertiary education and scientific-technical training overseas or practical business skills from their unique working abroad experience (O. Dai & Liu, 2009). These individuals often have greater exposure to knowledge, skills, and expertise, which forms tacit knowledge that is very much needed in the homeland. This tacit knowledge is unique in that it is difficult to express in words and illustration and thus challenging to transfer to other individuals or replicated by competitors (Amit & Schoemaker, 1993; Polanyi, 2015). Prominent examples, like Qian Xuesen, illustrate the significant impact that returnee directors can have. Qian Xuesen, the famous Chinese rocket scientist who pursued his master’s and doctoral studies as well as a scientific career in the United States for 20 years, is one of the early pioneers of rocketry and ballistic missile technology in the United States. He returned to China and became the director of the Fifth Academy of the Ministry of National Defence, significantly advancing China’s missile technology by 20 years.

Expanding beyond valuable scientific expertise, returnee directors, through their pursuit of tertiary education or work experience abroad, also gain insights into foreign cultures and how foreign organisation work. Their presence on the board may facilitate the adoption of superior management practices that enhance firm operating efficiency and productivity (Bloom & Van Reenen, 2007). Inkson et al. (1998) suggested that returnee directors with years of experience overseas return to the country with new knowledge that may benefit the nation’s development. From the interaction of the returnee directors with other directors, valuable and rare skills are shared (Cervantes & Guellec, 2002). Returnees allow better technology diffusion, encourage exchanging ideas, and boost entrepreneurship and innovation, which improve institutions in the home country (World Bank, 2011). Consistent with resource-based theory, returnee directors would probably provide better and greater resources to the firm to achieve higher performance as compared to local directors without international resources. Moreover, foreign-experienced directors, influenced by developed countries’ external environment, are more reputation-conscious and motivated to fulfil their supervisory functions impartially and objectively, according to reputation theory (Su et al., 2023). They instil these values in management, thereby enhancing the firm’s reputational capital.

Besides that, returnee directors have broader networking and social ties; this formed social capital, which is often lacking by non-brain-gain directors. According to Pruthi (2014), as individuals lived and worked abroad, they accumulate social capital based on personal ties of family or friends, industry ties such as former colleagues, suppliers, customers, and investors and intermediary ties such as individuals they knew through exhibitions, conferences or seminars. These ties enable them to act as boundary spanners, gather local information, identify business opportunities, and serve as resource providers (Au & Fukuda, 2002; Pruthi, 2014). Directors with foreign experience also ease the process of international capital-raising activities in foreign private placement and can increase firms’ foreign sales (Giannetti et al., 2015). Foreign directors who are native to foreign countries naturally have access to broader international resources, owing to their upbringing and deep immersion in foreign environments. This stands in contrast to returnee directors, who, although they have spent a significant amount of time abroad, may not have the same level of ingrained understanding and exposure. As highlighted by Zhang et al. (2018), the authors concluded that only long-term foreign professional or academic experiences of returnee directors have a meaningful impact, whereas short-term visits do not significantly contribute. Consequently, foreign-born directors who have resided abroad for extended periods may be better equipped to bring valuable international resources to the firm. Foreign independent directors are shown to make better cross-border acquisitions (Masulis et al., 2012), and foreign national directors actively provide input to board operations and increase firm performance (Estélyi & Nisar, 2016). Masulis et al. (2012) found that foreign independent directors’ influence is more substantial in home regions, where the firm can benefit from their expertise and social ties. The World Bank (2011) asserts that diasporas foster scientific and business networks, lower transaction costs, facilitate knowledge exchange, and stimulate trade and investment, though some scholars argue otherwise.

However, Masulis et al. (2012) also found that foreign directors’ presence in the US negatively impacts firm performance, especially if their home region’s importance diminishes, and their unfamiliarity with the local working environment can hinder growth. Araci (2015) reports that 16% to 40% of expatriate managers end their foreign assignments early due to cultural, language, and miscommunication issues, leading to poor performance. Similarly, Ho et al. (2015) suggest that returnees with extensive overseas experience may experience reverse cultural shock and consider re-expatriation post-service.

This study suggests that hiring brain-gain directors, as per the resource-based theory, could provide significant benefits to the firm Thus, this study hypothesises that:

H1: Brain-gain directors have a positive impact on firm performance.

H2: Foreign directors have a positive impact on firm performance.

H3: Returnee directors have a positive impact on firm performance.

Hypothesis Development: The Moderating Effect of Board Gender Diversity on the Relationship Between Brain-Gain Directors and Firm Performance

Previous literature highlights the significance of female board members, as they challenge homogeneous norms and represent different voices, highlighting the need for diversity in board composition (Maznevski, 1994; Zelechowski & Bilimoria, 2004). Recent research also indicates that the presence of female directors positively influences innovative investment and development activities (Vafaei et al., 2021). According to Yu (2023), a firm with at least one female director on its board has significantly less investment inefficiency than firms without one. Female directors that a firm appoints for the first time since being listed also lead to larger boards, more female employees, and larger foreign ownership ratios (Nguyen & Thai, 2022), signalling female directors may change board practice and culture. Unlike male directors, female directors focus on details and address issues missed by male directors, preparing well before meetings and taking their roles seriously (Huse & Grethe Solberg, 2006). According to Peng et al. (2022), firms with board gender diversity prioritising vulnerable stakeholders, focussing on diverse stakeholder groups, and increasing corporate social disclosures. Similarly, the inclusion of female managers in senior management teams positively impacts cross-border M&A performance due to the unique advantages of women and maintaining good connections with the enterprise’s external environment (Wu et al., 2023). A diverse board, despite its potential to moderate risk reduction, generally leads to conservative corporate decisions that do not lead to profitability or performance reduction (Mohsni et al., 2021).

In contrast, Adams and Ferreira (2009) discovered a negative correlation between board gender diversity and firm performance attributed to over-monitoring by women directors. Carter et al. (2010), Farrell and Hersch (2005), and Rose (2007) found no significant relationship between gender and firm performance. Moreover, women’s representation in corporate boards faces challenges such as perceived lack of business dynamics, work-life balance, aggressive attributes, employers bias, career progression opportunities, and inequitable pay (Amin et al., 2022).

Female directors are more vocal and active, especially when three or more females are on the board (Konrad et al., 2008). Carter et al. (2003) revealed that in Fortune 1000 firms, firms with at least two females performed better than all-male boards in terms of Tobin’s Q and ROA. The study by Sarkar and Selarka (2021) reveals that having a woman director on the board in India leads to higher firm performance, with the effect being primarily driven by independent women directors. While the absolute number of female directors matters, their proportion is also positively related to firm performance (Y. Liu et al., 2014). According to Harakeh et al. (2023), firms with gender diverse boards experience a softer decline in stock returns during a financial crisis, with board gender diversity moderating the association between firm opacity and crisis-related decline. Moreover, the Malaysian Code on Corporate Governance (MCCG) in 2017 requires large firms with a market capitalisation of RM2 billion or more to have at least 30% women representatives on the board.

The board’s inclusion of female directors reflects diversity and values, potentially enhancing firm performance through resource-based theory, thereby promoting brain-gain directors (Selby, 2000). Hence, this study hypothesises that:

H4: The board gender diversity positively moderates the relationship between brain-gain directors and firm performance.

H5: The board gender diversity positively moderates the relationship between foreign directors and firm performance.

H6: The board gender diversity positively moderates the relationship between returnee directors and firm performance.

Data and Methodology

The Data

There is a lack of brain gain research in corporate finance due to the unavailability of data, owing primarily to privacy reasons and capacity. Most countries do not keep detailed records of citizens who return after prolonged absences, which has posed a challenge in data collection (Foo, 2011). Data extracted from the annual report helped us overcome the limitations posed by the lack of brain gain data. Although this process is time-consuming and requires significant effort, researching brain gain on corporate boards using company annual reports as the primary source is feasible. After data cleaning, our panel dataset comprised 40,040 director-year level data from 803 non-financial firms from 10 industries in Bursa Malaysia’s Main Market from 2009 to 2015, which generated a total of 5,039 firm-year observations for analysis. The panel data is a two-dimensional dataset that combines time series and cross-sectional data, capturing information of the same firms over time. Thus, it enhances the data quality and discloses more information embedded in the data by increasing the degrees of freedom and reducing the collinearity among variables.

As aforementioned, the brain gain data, such as directors’ nationality and foreign working and tertiary education experience, are hand-collected via the company’s annual report. Other data collected from annual reports include the gender of the directors and board-level control variables such as board size and busy board (other directorships/multiple directorships in other publicly listed firms) data. In the case of missing data, we refer to data sources such as personal profiles available online on the company’s official website, Bursa Malaysia website (i.e.,“announcement of appointment” and “change in the boardroom”), Bloomberg.com (i.e., Bloomberg Executive Profile & Biography), LinkedIn.com, director’s autobiography, and newspaper (directors interview). Based on the mentioned sources, this study identifies whether they are a foreigner or Malaysian fitted with foreign working or tertiary education experience. Foreign directors could be identified based on their nationality. Returnee directors are natives who studied and/or worked abroad and returned to their home country (O. Dai & Liu, 2009). Following Giannetti et al. (2015), we do not consider a Malaysian who worked in a foreign branch of a Malaysian company (e.g., Genting Hong Kong Limited) or an office of an international company in Malaysia (e.g., Nestlé Malaysia) as having overseas working experience.

It is crucial to acknowledge that a director who has completed an online and external course or globally recognised qualifications, such as the Association of Chartered Certified Accountants (ACCA) in Malaysia, is not considered to have foreign education experience. However, a director who has completed their articleship (practical training) overseas is considered to have foreign working experience. Finally, we do not relate a director who holds an honorary doctoral degree (honoris causa) from a foreign institution to having foreign education experience, as the degree is bestowed as an honour rather than the accomplishment of education in a foreign country. Following Lee and Roberts (2015), who used the absolute number to define outside foreign directors, our foreign director (BG1) is the number of directors on the board who are foreigners; returnee director (BG2) is the number of Malaysian directors on the board who have either foreign tertiary education and/or foreign working experience.

Firm financial data, such as Tobin’s Q (dependent variable) and total assets, total liabilities, and sales, which are used to generate firm-level control variables, are downloadable from Datastream. Five firm and board-related control variables are used: firm size, firm leverage, firm growth, board size, and busy board. We report the measurements for all variables in Table 1. Tobin’s Q, a market-based measure that includes market expectations of a firm’s future performance (Belaounia et al., 2024), represents the market’s valuation of a firm’s assets relative to their replacement cost. This ratio provides a clear perspective on how the market views the firm’s potential for future earnings and growth. Unlike accounting-based measurements such as return on assets (ROA) or return on equity (ROE), as the market-based measure, Tobin’s Q enables comparison across firms and industries, unaffected by variations in accounting methods or capital structures.

Descriptions of Variables.

Dynamic Panel Data Estimations – GMM Estimations

GMM is designed for large N and small T data, linear functional relationships, dynamic dependent variables, endogenous independent variables, fixed individual effects, autocorrelation, and heteroscedasticity (Roodman, 2009). Law et al. (2018) found that two-step GMM is more efficient than one-step GMM due to consistent weighting of moment conditions and covariance matrix estimation. While Difference GMM and System GMM use different estimation methods for time-invariant variables, the Difference in Sargan-Hansen Test determines the appropriate analysis method. The study’s analysis uses a two-step robust System GMM estimation, as the results indicated its preference (Roodman, 2009; Windmeijer, 2005).

The baseline model using two-step GMM in this study could be represented as follows:

where FP is the Firm Performance (Tobin’s Q); FPi,−1 is the one lagged of firm performance; brain-gain director is proxied by BGtotal, while the control variables are Fsize, Flev, Fgrowth, Bsize, and Bbusy, which represent firm size, firm leverage, firm growth, board size, and busy board, respectively; α is a constant term or intercept; β is the coefficient of the variable; ε is the error term; i denotes firms, and t denotes year. The brain-gain directors are further categorised into foreign directors (BG1) and returnee directors (BG2) in the following models:

From the above models, we examine the moderating effects of board gender diversity (Female) on firm performance as below:

Results and Discussion

Descriptive Statistics

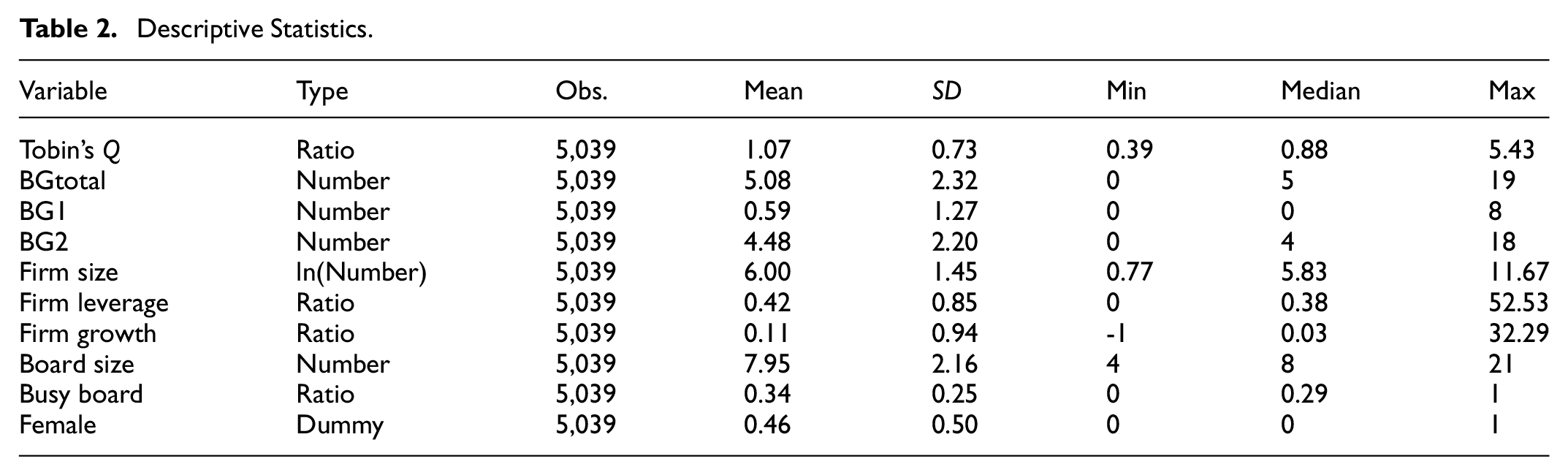

The descriptive statistics in Table 2 show that the brain-gain of a corporate board is prevalent in Malaysia. There is a total of 5,039 observations. BGtotal ranged from 0 to 19 with a mean value of 5, indicating, on average, that there are five brain-gain directors on the board in our study. Malaysian Airline System Berhad (MAS), with a board size of 20, had one foreign director and 18 returnee directors in 2011. Hence, the number of returnee directors (BG2) has a maximum value of 18. The maximum value for a foreign director (BG1) is 8, which is Chin Teck Plantations Berhad. All the foreign directors are from Singapore.

Descriptive Statistics.

For moderating variables, the descriptive statistics show that out of 5,039 observations, the female director variable shows that only 46% of the observations in this study have at least one female director on the board. This ratio implies that most of the boards in Malaysia are homogeneous boards (all-male boards). This situation needs to be improved to promote gender equality and gender diversity on the board.

Understanding the Brain-Gain Directors

Figure 2 shows the distribution and frequency of brain-gain directors. The left histogram shows a bell-shaped curve, indicating the number of brain-gain directors in Malaysia is normally distributed, lying within a range with some outliers, such as 16 and 19 brain-gain directors on the board. There are only 36 observations that show zero brain-gain directors, implying 5,003 observations (5,039 − 36 = 5,003) have at least one highly skilled and talented board director responsible for monitoring and controlling the firms. The centre histogram shows that 73.11% of observations, or 3,684, have zero foreign directors, suggesting that most brain-gain directors are returnee directors. The right histogram shows the number of returnee directors on the corporate board, which is also normally distributed. The mode is 4, indicating that most of this study’s observations have four returnee directors on board.

Distribution of brain-gain directors, foreign directors and returnee directors on board.

Correlation Analysis and Variance Inflation Factor (VIF) Analysis

Table 3 shows the correlation analysis. All the correlation values are between −.5 and .5, except BGtotal versus Board Size (.6693), BG2 versus Board Size (.6195) and BG2 versus BGtotal (.8437). As BGtotal (brain-gain director) is the summation of the number of foreign directors (BG1) and returnee directors (BG2), the correlation value between BGtotal and BG2 is high. However, this relationship will not affect the results as neither is included in the regression models simultaneously. For BGtotal versus Board Size (0.6693) and BG2 versus Board Size (0.6195), VIF is carried out. All the values of VIF analysis are more than 1 and less than 2.5, indicating that all the variables in this study are not multicollinear. As stated by Hair et al. (2013), a VIF greater than 0.2 and less than 5 indicates the model does not have multicollinearity issues. The study’s VIF analysis results are not publicly available but can be accessed upon request from the authors.

Correlation Analysis.

The Analysis of Baseline Model Using Dynamic Two-Step Robust System GMM

The endogeneity problem is a critical issue in panel data, which may affect the robustness of the estimations. The rationale is that firms with better performance may be more afforded to hire foreign or talented returnee directors; thus, there might be a simultaneous relationship (Wooldridge, 1995). In this study, where brain-gain directors contribute to firm performance, better firm performance may affect the firm’s chances of having more brain-gain directors on the board. A dynamic GMM estimator is applied to avoid the effects of endogeneity in the regression.

There are two types of GMM, namely Difference GMM and System GMM, which can be applied in one-step and two-step variants. Law et al. (2018) mentioned that as parameters in one-step GMM depend on the initial weight matrix, while in two-step GMM, moment conditions are weighted by a consistent estimate of their covariance matrix, two-step GMM is asymptotically more efficient than one-step GMM. Hence, this study applied a bias-corrected robust estimator two-step GMM (Windmeijer, 2005) instead of one-step GMM, using two robust syntax in Stata. The difference between Difference GMM and System GMM is the estimation of the effect of time-invariant variables. Both Difference GMM and System GMM undergo differentiation, but the latter uses the level version of the dynamic panel model in addition to the differenced version. Hence, the effect of time-invariant variables in System GMM could be estimated. To decide whether Difference GMM or System GMM should be applied in the analysis, Difference in Sargan – Hansen Test is carried out. As the p-value of the Difference in Sargan-Hansen Test is more than 5%, this suggests that System GMM is preferred. (The procedure and results for Difference in Sargan-Hansen Test can be accessed upon request from the authors). Hence, the following analysis in this study is conducted using a System GMM estimator instead of Difference GMM.

Research Findings

We report the estimates in Table 4. What stands out is the significance of all the brain-gain variables (BGtotal, BG1, and BG2). Model 1 shows that brain-gain directors positively affect firm performance. For every additional number of brain-gain directors on board, we can expect Tobin’s Q to increase by an average of 0.0455 or 4.55%. As the coefficients of BG1 and BG2 remain positive in Models 2 and 3, this suggests that the positive relationship applies regardless of the type of brain-gain directors. The positive result remains even though we controlled the effects of one another, as in Model 4, and it also shows that, compared to returnee directors, foreign directors are more positively related to firm performance. Holding others constant, it is found that for every additional number of foreign directors on the board, we can expect Tobin’s Q to increase by an average of 7.41%. On the other hand, every additional number of returnee directors on the board is expected to increase Tobin’s Q by an average of 3.23%. To control for year and industry effects, year and industry dummies are included in the two-step robust System GMM model throughout the analysis.

The Impact of Brain-Gain Directors on Firm Performance Using Two-Step Robust System GMM Estimation.

Note. Variable L. Tobin’s Q in the table represents the lagged of Tobin’s Q. Figures in ( ) are the robust standard error; Figures in [ ] are the p-value; ***, **, and * denote the significance at the 1%, 5%, and 10%, respectively. Year and industry dummies have been included in the model.

Prior literature such as Estélyi and Nisar (2016) define the foreign director variable as a dummy variable if the firm has a foreign nationality director, while Giannetti et al. (2015) using the A-share Market as the sample and controlling the proportion of foreign directors, define brain-gain in corporate board in China as the proportion of directors with foreign experience. Our study follows Lee and Roberts (2015), who believe every director is a unique voice rather than a voting bloc, hence using the number of brain-gain directors in the analysis. Despite the differences in definition, our findings are consistent with Estélyi and Nisar (2016) and Giannetti et al. (2015), in which brain-gain director is positively related to firm performance. Similarly, Ashraf and Qian (2021) reveal that board internationalisation decreases real earnings management, as foreign directors enhance board effectiveness in monitoring management and reduce agency costs.

Based on resource-based theory, this positive relationship can be attributed to two key aspects of their roles. Firstly, brain-gain directors play a crucial role in strategy setting and serve as significant human capital resources for firms. When foreigners or returnees join the corporate boards of publicly listed firms in Malaysia, their international background, tertiary education abroad, foreign industry-specific experience, and previous roles as CEOs or board members in foreign firms make them valuable assets (Barroso et al., 2011). Their unique knowledge, experience, expertise, and skills, accumulated over their tenure, are heterogeneous (distinct across individuals) and immobile (stable for at least a short period). These attributes make brain-gain directors valuable, rare, and difficult to imitate, creating a temporary competitive advantage for the firms. If firms are structured to capitalise on the contributions of these directors, they can achieve sustained competitive advantage and improved performance. Notably, foreign directors with extensive international experience have a more positive impact on Tobin’s Q compared to returnee directors. Secondly, brain-gain directors act as resource providers, connecting firms with various external resources. Their international experience affords them extensive networks and social ties, facilitating the firm’s internationalisation and cross-border acquisitions. They also aid in transferring superior management and governance practices, as well as technological know-how (O. Dai & Liu, 2009; Giannetti et al., 2015; Masulis et al., 2012). This enables firms to access necessary resources, even if the directors themselves do not possess them directly.

Moderating Effect of Board Gender Diversity

The results in Model 1 and 2 in Table 5 are supported by Carter et al. (2010), Farrell and Hersch (2005) and Rose (2007) who also found insignificant direct relationship between female directors and firm performance. Despite the absence of significant direct relationship between female directors and firm performance in Models 1 and 2, Model 3 shows that the moderating term of BGtotal×Female significantly impacts firm performance. The result is robust even after the brain-gain directors (BGtotal) have been categorised into foreign directors (BG1) and returnee directors (BG2), as shown in Models 4 and 5, with a coefficient of 0.0783 which are significant at 10% level. These results are consistent with Carter et al. (2003); thus, Hypotheses 4 to 6 are supported. As female directors are more detailed-oriented, get ready before meetings, and tend to have more questions, they brighten up the boardroom atmosphere (Huse & Grethe Solberg, 2006; Konrad et al., 2008). Their presence may facilitate boardroom discussion since female directors pick up the details and contribute to the firms. As female directors tend to hold different perspectives and values, the female director may be a unique resource; hence, including female directors on the board concomitantly includes diverse resources in the firm (Konrad et al., 2008; Selby, 2000).

Moderating Effect of Board Gender Diversity on the Relationship Between Brain-Gain Directors and Firm Performance Using Two-Step Robust System GMM Estimation.

Note. Variable L. Tobin’s Q in the table represents the lagged of Tobin’s Q. Figures in ( ) are the robust standard error; Figures in [ ] are the p-value; ***, **, and * denote the significance at the 1%, 5%, and 10%, respectively. Year and industry dummies have been included in the model.

Further Issues – All-Male Board Versus Gender Diversity Board

Based on the results that board gender diversity does prevail in moderating the effect of brain-gain directors, this study further examines the effect using subsampling, namely, all-male board and gender diversity board. These subsamples allow us to compare the gender issue on the differences between the two types of brain-gain directors. As shown in Table 6, the brain-gain directors positively impact firm performance only on the gender diversity board.

The Impact of Brain-Gain Director on Firm Performance Using Two-Step Robust System GMM Estimation (Board Type Subsample).

Note. Variable L. Tobin’s Q in the table represents the lagged of Tobin’s Q. Figures in ( ) are the robust standard error; Figures in [ ] are the p-value; ***, **, and * denote the significance at the 1%, 5%, and 10%, respectively. Year and industry dummies have been included in the model.

To check the robustness of the results, we repeat the analysis by separating brain-gain directors into foreign directors and returnee directors. With this, we examine whether the types of brain-gain directors affect firm performance. The results presented in Models 3 and 4 are consistent with the findings in Models 1 and 2, as the positive impacts of foreign directors and returnee directors on firm performance disappears in the all-male board. On top of that, foreign directors (BG1) have more positive effects on firm performance than returnee directors (BG2). Hence, we summarised that for every additional number of brain-gain directors, Tobin’s Q will increase by an average of 0.0596 or 5.96% in board with at least one female director. For every additional number of foreign director and returnee director on the gender diversity board, we can expect Tobin’s Q to increase by 8.33% and 4.23% respectively.

This research concluded that the positive impact of brain-gain directors on firm performance disappears in all-male board, but is more pronounced in gender diversity board when at least one female director is present on the board. There are two reasons. Firstly, female directors play a role in strategy setting and are essential company resources. An all-male board often exhibits groupthink, while female directors offer diverse perspectives from minority groups, enabling the board to make decisions that prioritise the firm’s best interests (Konrad et al., 2008; Selby, 2000). In this case, the gender diversity boards have relatively abundant resources in values and ideas compared to the all-male board. Secondly, female directors are detail-oriented, preparing for meetings, asking questions, and addressing issues missed by male directors, facilitating discussion and creating an environment for resource sharing (Huse & Grethe Solberg, 2006; Konrad et al., 2008). In line with resourced-based theory, diverse directors, encompassing individuals from various nationalities, foreign work or tertiary educational backgrounds, and genders, present a range of assets that might potentially confer competitive advantages to firms.

Conclusions

To the best of our knowledge, most of the related brain-gain studies of the board investigate either foreign directors or returnee directors, rarely treating both as the main interest of research, and if there is, one of them is treated as the control variable. For instance, Giannetti et al. (2015) studied the directors’ foreign experience and Masulis et al. (2012) focussed only on foreign directors. This may be due to the fact that there is no standard definition of brain gain, and researchers are free to term either foreigner or returnee as brain gain sample. While some think that brain gain should include only foreign directors, some argue that returnee is another form of brain gain. Literature on brain gain has shown that brain gain policy does not only focus on foreign talents, attracting local talents who stay abroad to return and work in their home countries (reverse brain drain) is another trend. This argument is supported by Y. Dai et al. (2021), who observed a shift in firms’ hiring criteria and increasing appreciation of the firms to directors’ foreign experience gained from developed economies. The literature gap encourages us to explore the relationship between different brain gain groups and firm performance to see how foreign directors and returnee directors impact Tobin’s Q. As the focus of human capital flow literature has shifted from brain drain to the brain gain topic, our study is timely and relevant.

The findings indicate that brain-gain directors on the board, regardless of foreign or returnee directors, are positively related to firm performance. Further analysis shows that foreign directors substantially impact firm performance more than returnee directors. Zhang et al. (2018) demonstrated that only prolonged foreign professional or academic experiences among returnee directors carry significant influence, while short-term visits do not make a notable contribution. Our research expands upon existing literature by revealing that returnee directors, despite spending considerable time abroad, might not possess the same depth of understanding and exposure as foreign-born directors. The latter, being native to foreign countries, naturally have access to broader international resources due to their upbringing and extensive immersion in foreign environments. Consequently, foreign-born directors who have resided abroad for extended periods may be better positioned to leverage valuable international resources for the firm. Drawing upon resource-based theory, two possible explanations for these findings are the roles played by brain-gain directors as human resources (encompassing knowledge, experience, skills, stored within the individual) and as resource providers (in terms of international connectivity and social capital), linking the firm to valuable external resources. Thus, for shareholders, the recruitment of both foreign and returnee directors is deemed worthwhile, given the evident financial impact brought about by brain-gain directors.

Last but not least, our research also showed that the positive impact of both brain-gain directors on firm performance diminished in all-male boards, but is more pronounced in gender diversity boards. This implies that although our earlier finding showed that the employment of a brain-gain director is beneficial to the firm, firms need to ensure the board composition in terms of gender and that the boardroom atmosphere is suitable for the brain-gain director to function well. Female directors bring diverse insights and values to firms, thereby enhancing the decision-making process. In comparison to all-male boards, gender-diverse boards are also more dynamic due to the proactive nature and characteristics of female directors. They tend to prepare before meetings, ask more questions during discussions, and exhibit a greater attention to detail. As described by Huse and Grethe Solberg (2006), the presence of female directors enlivens the boardroom atmosphere. Therefore, it is recommended that the presence of female directors on boards facilitates discussions, interactions, and knowledge-sharing among directors, resulting in benefits for firms and improvements in performance. This finding also proposed that while hiring a talented director is critical for the firm, the board itself need to revise its board composition periodically to ensure the whole boardroom is optimally functioning. Enhancing diversity within an organisation boosts firm performance by fostering varied representation, ideas, skills, knowledge, and expertise. This, in turn, maximises benefits and improves decision-making (Ali et al., 2022), while also generating valuable, rare, inimitable, and non-replaceable resources for the firms.

This research investigates the impact of having brain-gain directors on corporate boards on firm performance, emphasising the importance of brain gain in Malaysia’s corporate sector. Theoretically, our findings align with the resource-based theory and the work of Y. Dai et al. (2021), demonstrating that firms should value directors’ foreign experience acquired from developed economies, as these experiences are valuable resources. Additionally, our study extends the findings of Zhang et al. (2018), who argue that short-term foreign experience does not benefit firms, whereas long-term foreign professional or academic experiences among returnee directors have a significant positive impact. We discovered that foreign directors, who are born and raised overseas and possess greater international resources, are more positively associated with firm performance compared to returnee directors who have spent only part of their lives abroad. This underscores the importance of the level of directors’ international exposure or “foreignness” in contributing valuable resources to the firm. Besides that, the findings support UET, indicating that the experience, values and knowledge gained by the board of directors play a role in influencing their decision-making and performance.

The findings also suggest that the government should foster a business environment that attracts high-skilled foreign and returnee directors through appropriate brain-gain policy measures, as brain-gain directors significantly contribute to market-based firm performance. On the other hand, our findings also support the appointment of female board members as stated in the MCCG 2017, which requires all large companies to have 30% female directors on the board. Our results endorse this gender diversity policy, revealing that all-male boards might hinder the positive impact of brain-gain directors on firm performance. Our collected data also showed that only 46% in Malaysian publicly listed firms have at least one female director on the board, indicating a need for improvement in this area by recruiting more qualified female directors. Boards should consider a diverse gender composition to incorporate varied perspectives and insights into the decision-making process, ensuring decisions that best serve the firm’s interests.

One notable limitation of our research is the absence of a standardised definition for brain gain; each study interprets the brain gain of the corporate board differently. While our findings indicate that, holding other factors constant, each additional brain-gain director on the board is associated with an average increase of 4.55% in Tobin’s Q, this positive outcome may not be directly comparable with other studies that define brain gain differently, such as those focussing solely on foreign talents. Therefore, our results are applicable only to individuals, organisations, or countries that adopt a definition of brain gain encompassing both foreign and returnee talents. The lack of a standardised definition for brain gain hampers research on this issue, as existing literature often focuses exclusively on either foreigners or returnees, but not both. Nonetheless, we aim to offer a comprehensive definition of brain gain for corporate boards and encourage future researchers to examine the brain gain topic from the perspectives of both foreign and local talents. By doing so, academic research findings can better align with government policies that emphasise not only the importance of attracting foreign talents but also of retaining local talents who have gained working or education experience abroad to return and contribute to their home countries (reverse brain drain).

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Ministry of Higher Education Malaysia (MOHE) under the Fundamental Research Grant Scheme (Project Code: FRGS/1/2020/SS01/USM/02/6). This research was conducted while the corresponding author, Char-Lee Lok was on sabbatical leave.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data generated during this study are not publicly available, but are available from the author(s) on reasonable request.