Abstract

The study leverages the trade-off theory to assess the influence of capital structure on business growth following adopting IFRS. Employing a purposive sampling technique, 92 non-financial institutions listed on the Frankfurt Stock Exchange from 1994 to 2021 were selected for analysis. A two-step Generalized Method of Movements (GMM) was utilized to explore the impact of firms’ capital structure on their business growth under IFRS adoption. Results indicated a positive and statistically significant correlation between the debt-to-equity ratio and business growth (assets, sales, and profit). Moreover, the study revealed that the debt-to-capital and long-term debt-to-capital ratios had a negative effect on asset and profit growth but a positive impact on sales growth. Additionally, the debt-to-total-assets ratio demonstrated a negative influence on asset and sales growth but a positive effect on profit growth. Firms adopting IFRS had positive and significant impacts on sales, assets, and profit growth. Furthermore, the findings highlighted the adverse effects of the 2008 financial crisis and the COVID-19 pandemic on business growth. Firms listed on the Frankfurt Stock Exchange can strategically utilize these findings to optimize their capital structure decisions within the framework of IFRS adoption. By comprehending the nuanced relationship between capital structure and business growth, managers can tailor financing strategies to foster sustainable growth while managing financial risks effectively.

Keywords

Introduction

Corporations often prioritize business growth as a pivotal objective, seeking expansion for its benefits. Gatobu and Maende (2019) note that expansion typically leads to increased revenue as organizations achieve economies of scale and spread fixed expenses across a broader production or consumer base. This heightened profitability allows for greater investment in innovation and shareholder rewards. Ansoff et al. (2018) highlight how expanding companies aim to capture a larger share of their target markets, enhancing competitive positioning and influencing industry dynamics while gaining negotiating leverage with suppliers and customers.

Furthermore, Khan et al. (2020) emphasize that expansion improves brand visibility and market presence, attracting more customers and fostering trust and loyalty, which are essential for sustained success. Diversification into new customer segments and geographical markets reduces reliance on specific sectors and mitigates risks associated with regional economic fluctuations. Drury (2013) underscores the importance of economies of scale in lowering average costs per unit, thus boosting profit margins and competitiveness.

Research and development (R&D) investment is pivotal for innovation and competitiveness (Lai et al., 2015). Lynch (2018) highlights how expanding firms wield increased negotiating power, leading to cost reductions and operational efficiencies. Shareholders benefit from business expansion through increased stock prices and dividends, aligning to maximize shareholder value (Queen, 2015). Vernimmen et al. (2022) stress the significance of financing for capital expenditures, enabling the acquisition of new machinery, technology, or facilities to enhance production capacity and efficiency.

Moreover, Gomber et al. (2018) assert that firms emphasizing innovation require substantial financial resources for R&D efforts, crucial for developing and enhancing products to meet evolving market demands. Stallkamp and Schotter (2021) elaborate on the financial requirements for expanding into new markets, encompassing market research, establishing a presence, marketing, and adapting products to local preferences and regulations. Financing plays a pivotal role in fueling business growth and sustaining competitiveness across diverse sectors and markets.

Expansion typically involves broadening the client base and increasing market share. Funding is crucial for marketing and advertising initiatives to establish brand recognition, attract fresh clientele, and effectively endorse items or services (Wheeler, 2017). Corporations invest in staff, training programs, and competitive compensation packages to facilitate development. Financial resources are vital for attracting, retaining, and nurturing a competent and motivated workforce (Mngomezulu et al., 2015). As companies expand, investments are often needed to expand or improve infrastructure, including facilities, warehouses, distribution networks, and IT systems. Sufficient financing is essential for developing the necessary infrastructure to support increased business activities (Bisbey et al., 2020).

The capital structure is crucial in determining the financial framework for business growth (Jensen & Meckling, 2019). A company’s capital structure, comprising debt and equity financing, significantly influences its potential for long-term growth and competitive advantage (Alan & Gaur, 2018). Strategic allocation of capital, balancing debt and equity, impacts a firm’s cost of capital, risk profile, and overall financial health (Akbar & Lanjarsih, 2019). By strategically combining debt and equity financing, companies can capitalize on growth opportunities, allocate resources to research and development, and manage economic risks (Gao & McDonald, 2022). Conversely, an imbalanced or poorly managed capital distribution may constrain innovation, hinder growth, or weaken resilience to economic downturns.

Corporations’ debt and equity allocation decisions significantly affect their ability to expand and achieve strategic objectives (Eniola, 2021). Business growth relies on adapting to evolving conditions, with the capital structure directly impacting financial flexibility. An optimal capital structure fosters financial adaptability, while excessive debt may limit flexibility, and excessive equity dilutes ownership. Maintaining a harmonious balance enhances the company’s ability to seize growth opportunities (Ross et al., 2022).

Debt exposes individuals to financial risk due to interest obligations, while equity, though mitigating financial risk, may dilute ownership. A well-managed capital structure considers risk potential (PeiZhi & Ramzan, 2020). Excessive debt increases financial vulnerability, potentially impeding expansion during economic downturns. Adopting a balanced strategy helps mitigate risk and sustain steady expansion. Investors evaluate a company’s capital structure to gauge risk and growth potential. A favorable capital structure enhances investor confidence (Neves et al., 2020), making companies with robust structures more attractive for investment, securing essential funds for expansion and growth projects.

The allocation of appropriate financial resources for expansion impacts stakeholders. Shareholders may experience direct benefits from business expansion, such as increased stock value and dividends (Malik et al., 2013). An optimal capital structure ensures that financing methods support expansion while minimizing financial risk. Customers benefit from business growth if it improves product quality, expands offerings, and enhances customer service (Payne & Frow, 2016). A well-managed capital structure ensures financial stability to uphold and enhance customer satisfaction. Business expansion may lead to increased tax payments and regulatory compliance requirements. An optimal capital structure enables effective management of financial obligations and compliance with regulatory mandates (Neves et al., 2020).

Growing enterprises often contribute to the economic progress of local communities through job creation and support for local firms. A well-suited financial structure is crucial for ensuring the long-term viability of these contributions (Abrahams, 2018). A company’s expansion may impact rival firms, potentially intensifying market rivalry. The choice of capital structure significantly affects a company’s ability to compete effectively, mainly when it facilitates strategic investments and innovation. Business growth can have environmental and social consequences, and a suitable financial framework allows corporations to allocate resources toward sustainable practices and corporate social responsibility activities, addressing concerns highlighted by advocacy groups (Amran et al., 2014; Obeng, Arhinful, Mensah, 2025; Obeng, Arhinful, Tessema, et al., 2025).

While numerous studies have explored the impact of capital structure on various aspects of the firm, such as financial performance (Abdullah & Tursoy, 2021; Arhinful et al., 2023a, 2023b), dividend policy (Bataineh, 2021; Rehman, 2016), and earnings management (Maswadeh, 2018; Tran & Dang, 2021). The specific impact of capital structure on business growth before and after adopting IFRS remains largely unexplored in the literature, particularly in Germany. Germany, being Europe’s largest domestic market, offers investors a sizable, stable customer base, and a relatively stable economy (Lewis & Wiser, 2007). Increased integration into the global economy has facilitated the acquisition and sharing of resources among businesses in Germany, including knowledge, products, and employees. Technological advancement in the country has further supported business growth, propelling many businesses to become leading industrial players in Germany and Europe.

This study elucidates the relationship between a company’s capital structure and business growth. By analyzing empirical evidence from this study, employing rigorous analytical approaches, and considering various industry contexts, we seek to reveal the impact of capital structure decisions on organizations’ long-term sustainability and success within the framework of IFRS adoption. The study fills a significant gap in the academic literature by investigating the correlation between capital structure and business growth under IFRS adoption.

This study contributes substantially to the existing body of literature in several ways. First, it analyzes the correlation between the debt-to-capital ratio and the growth of sales, profit, and assets. This analysis yields crucial insights into how leverage affects key financial performance metrics. The study introduces a novel perspective by examining the impact of debt on various growth indicators, an area that has not been extensively explored in prior research, which has primarily focused on the influence of debt on profitability.

Second, the study delves into the influence of the long-term debt-to-capital ratio on the growth of assets, profit, and sales. It provides a comprehensive analysis of the impact of the maturity structure of debt on business growth by differentiating between short-term and long-term debt, an area that had not been thoroughly investigated in previous studies.

Furthermore, the study analyzes the impact of the debt-to-total-assets ratio on profit, sales, and asset growth. This research provides a more comprehensive understanding of the broader impact that a company’s total debt has on its growth and performance, addressing a gap in the existing literature, which frequently focuses solely on balance sheet metrics or operational success.

Additionally, this research examines the correlation between sales, profit, asset growth, and the debt-to-equity ratio. The analysis prioritizes the debt and equity financing ratio to provide crucial insights into how it impacts growth patterns, which is vital for making optimal decisions about capital structure.

Finally, the study examines the impact of implementing IFRS on sales, profit, and asset growth. The adoption of IFRS signifies a substantial change in financial reporting standards, and its impact on growth indicators is not yet well understood. This research aims to examine the impact of adopting IFRS on financial performance, substantially contributing to the existing knowledge in this area.

The study’s findings will help professionals and academics understand how capital structure affects firms’ growth paths in today’s dynamic economy. Focusing on Frankfurt Stock Exchange businesses gives the research a unique geographical and market perspective. The findings show how IFRS adoption affects capital structure and growth for German and European financial enterprises. Understanding how IFRS adoption affects capital structure decisions can guide debates about accounting rule changes to support company growth better.

Literature Review and Hypotheses Development

Theoretical Framework

The trade-off theory is particularly significant for this study due to its comprehensive approach to evaluating the benefits and drawbacks of debt financing. This theory posits that firms should balance the advantages of tax deductions from debt with the potential risks of financial difficulties and insolvency, making it a crucial framework for understanding how organizations determine their optimal capital structure during periods of expansion (Madubuike & Ebere, 2023).

The trade-off theory is the most appropriate framework for our research because it focuses on the fundamental aspects of capital structure decisions and their impact on a company’s growth potential. By employing this theory, the study can comprehensively examine the correlation between various debt ratios and growth indicators within the framework of IFRS implementation, providing a robust foundation for the findings.

Hypotheses Development

Debt to Capital Ratio and Business Growth

The impact of the debt-to-capital ratio on business growth hinges on the company’s adeptness in managing the trade-offs between leverage and the benefits of expansion (Ai et al., 2020). This ratio is a crucial metric for assessing a company’s financial leverage and can influence various facets of business expansion, including sales growth, profit growth, and asset growth.

A higher debt-to-capital ratio signals increased financial leverage. Debt can be a means to acquire capital for business expansion and growth. However, substantial debt may lead to heightened interest expenses, affecting profitability and impeding investment in sales-generating activities (C. M. A. Panigrahi, 2019). When employed judiciously, debt can fund strategic initiatives that drive sales, such as product line extensions or market entry, fostering favorable sales growth (Brush et al., 2009). Conversely, high debt servicing costs could limit resources available for sales efforts.

The debt-to-capital ratio’s impact on profit growth is influenced by its effect on interest expenses and financial risk. Elevated debt levels may increase interest payments, potentially reducing net profits. However, leveraging debt for lucrative ventures can amplify returns and bolster profit growth (Pandey, 2017). Financing projects with high returns using debt can enhance a company’s profitability. However, excessive interest expenses or difficulty meeting loan obligations could hamper profit growth.

Debt can fund asset purchases, facilitating asset base expansion. However, the debt-to-capital ratio accurately reflects the financial risk associated with the acquisition strategy. Heightened debt levels can strain finances and impede asset expansion efforts. Effective debt management and investments in high-yield assets can drive asset expansion (Chandra, 2013). Nonetheless, excessive debt may strain finances and hinder asset investment and maintenance.

Yazdanfar and Öhman (2015) discovered that increased debt levels, including trade credit, short-term debt, and long-term debt, harm a company’s profitability. This phenomenon was attributed to increased agency costs and the risks associated with elevated debt levels, leading businesses to increasingly depend on equity financing to alleviate these risks.

Alarussi and Alhaderi (2018) in their study also discovered that high debt levels negatively impact a company’s growth and profitability. The study emphasized that companies with lower debt-to-equity ratios exhibited superior performance, while excessive debt amplified financial distress expenses and diminished the resources allocated for growth endeavors.

H1: Capital structure (Debt to capital ratio) significantly influences business growth.

Long Term Debt to Capital Ratio and Business Growth

The influence of the long-term debt-to-capital ratio on business growth is multifaceted and depends on how effectively a company manages its financial leverage. Sound financial management involves carefully weighing the benefits of utilizing long-term debt for strategic investments against the associated costs and risks (Melicher & Norton, 2013). Companies thoroughly assess their financial position, industry dynamics, and risk tolerance to determine an appropriate long-term debt-to-capital ratio conducive to sustainable and balanced growth.

The long-term debt-to-capital ratio can impact sales growth by affecting the organization’s financial flexibility (Hegde et al., 2023). Higher levels of long-term debt may lead to increased interest expenses, constraining funds available for sales and marketing initiatives. Strategic use of long-term debt by a company for activities that drive sales, such as expanding distribution networks or introducing new products, can support sales growth (Huff & Rogers, 2015). However, if debt management costs impede adaptability and responsiveness, it could hinder the ability to explore and capitalize on growth opportunities.

The long-term debt-to-capital ratio may influence profit growth, as it can affect interest expenses and financial risk. Greater long-term debt amounts might result in higher interest payments, potentially reducing net profits. However, when debt is deployed for profitable ventures, it can increase returns and profit expansion. Effective long-term debt management can enhance profit growth, ensuring that returns from debt-financed investments justify the loan costs (Fulton et al., 2012). Conversely, excessive debt levels can negatively impact profitability by elevating interest expenses.

Long-term debt is instrumental in financing asset expansion, particularly for acquiring durable assets like real estate and machinery. However, a significant long-term debt-to-capital ratio may indicate heightened financial vulnerability and impede asset expansion efforts. Using long-term debt to fund strategic acquisitions or capital expenditures with promising returns can facilitate asset growth (Ahmad et al., 2012). Prudent financial management ensures that the debt incurred aligns with the anticipated returns on the assets acquired.

Alipour et al. (2015) found that companies with a higher percentage of long-term debt in their capital structure showed superior growth indicators. The favorable impact was attributed to the security provided by long-term debt, which enabled companies to pursue substantial capital investments and growth efforts without the immediate burden of short-term repayments. Wahyuni and Gani (2022) found that effective long-term debt management could lead to increased business value and growth. Companies that wisely employ long-term debt can take advantage of tax shields and reduce their cost of capital, resulting in more investments in growth prospects and enhanced financial performance. However, Holmstrom (2015) highlighted the potential risks of relying too heavily on long-term debt, especially in volatile markets. The study found that companies with a balanced mix of short-term and long-term debt achieved better growth and profitability compared to those with a high proportion of long-term debt.

H2: Capital structure (long-term debt-to-capital ratio) significantly influences business growth.

Debt to Total Assets Ratio and Business Growth

The debt-to-total assets ratio holds sway over sales growth by impacting a company’s financial flexibility. Elevated debt levels can escalate interest charges, curbing the allocation of resources toward sales and marketing endeavors (Kurt & Hulland, 2013). Strategic deployment of debt by a company, particularly for investments in sales-generating activities like expanding product lines or entering new markets, can bolster sales growth. However, if heightened debt burdens impede operational agility, it may hinder the ability to seize expansion opportunities.

The debt-to-total assets ratio can influence profit growth by affecting interest expenses and financial risk. Increased debt levels may lead to higher interest payments, potentially eroding net earnings. Nevertheless, if the loan finances profitable initiatives, it can bolster returns and foster profit expansion. Effective debt management can enhance profit growth by ensuring that returns from debt-backed investments justify loan costs (Izzo & Magnanelli, 2012). Conversely, excessive debt burdens can dampen profitability by inflating interest expenses.

Debt is pivotal in financing asset expansion, particularly in acquiring durable assets like equipment. The debt-to-total assets ratio provides insights into how much debt fuels the company’s asset portfolio. Strategic use of debt to finance asset acquisitions or capital expenditures with promising returns can augment the company’s assets (Uysal, 2011). Prudent management entails aligning debt with anticipated returns on acquired assets, ensuring a balanced approach to leveraging debt for asset expansion.

The study by Ando et al. (2017) investigated the factors influencing organizations’ decisions regarding their capital structure. The findings revealed that companies with higher debt ratios to total assets are more likely to encounter elevated financial risk, potentially negatively affecting their growth. However, the study also highlighted that a moderate amount of debt might offer tax benefits and enhance growth through leverage.

Budhathoki and Rai (2020) discovered that companies with higher debt-to-total-assets ratios often experienced slower growth rates compared to companies with lower ratios. This slower growth can be attributed to financial constraints caused by increased levels of debt, which can restrict a company’s capacity to invest in growth opportunities.

H3: Capital structure (debt to total assets ratio) significantly influences business growth.

Debt to Equity Ratio and Business Growth

The debt-to-equity ratio influences sales growth by shaping a company’s financial flexibility. A higher ratio implies greater reliance on debt, potentially escalating interest costs and constraining funds available for sales and marketing efforts. Strategic management of the debt-equity ratio and judicious use of debt for investments in sales-driving activities such as product line expansion or market entry can foster sales growth (Deeb & Ventures, 2013). However, an excessive debt burden may curtail operational decision-making freedom.

The debt-equity ratio can impact profit growth by influencing interest expenses and financial risk. A heightened ratio may increase interest payments, potentially eroding net earnings. Nonetheless, if debt is deployed for profitable ventures, it can bolster returns and facilitate profit expansion. Effective management of the debt-equity ratio can positively affect profit growth, ensuring that returns from debt-backed investments justify loan costs (Sam, 2019). Nevertheless, an excessive debt load can exert pressure on profitability.

Debt is pivotal in financing asset expansion, particularly for acquiring assets with long-term perspectives. The debt-equity ratio provides insights into the extent to which debt fuels the company’s asset base. Strategic use of debt to fund asset acquisitions or capital expenditures yielding favorable returns can facilitate asset expansion (Almazan et al., 2010). Prudent management involves aligning debt with anticipated returns on acquired assets, ensuring a balanced approach to leveraging debt for asset expansion.

Paulo Esperança et al. (2003) examined the factors influencing a company’s capital structure. They found that organizations with higher debt-to-equity ratios generally experienced slower growth rates. This is because high leverage increases financial risk and the burden of debt repayments, which can restrict a company’s capacity to invest in development opportunities.

Ataullah et al. (2007) studied organizations’ capital structure choices and found that companies with lower debt-to-equity ratios tend to achieve superior growth performance. The study indicated that excessive debt can lead to financial hardship, negatively affecting a company’s ability to grow and innovate.

H4: Capital structure (debt-equity ratio) significantly influences business growth.

IFRS and Business Growth

Implementing IFRS enhances the ability to compare financial statements across nations, a boon for organizations engaged in global commerce (Brochet et al., 2013). Improved financial reporting fosters investor and stakeholder confidence, attracting investments and facilitating cross-border transactions. Greater financial transparency and comparability increase a company’s appeal to international investors and access to global capital markets, providing additional funds for expansion plans and contributing to sales growth.

IFRS implementation often involves fair value accounting, necessitating the revaluation of assets and liabilities based on market prices (Majercakova & Skoda, 2015). This practice can impact reported earnings, leading to more accurate and timely recognition of gains or losses. Enhanced visibility into financial performance enables informed decision-making on lucrative investments, benefiting the company. Standardized financial reporting under IFRS enhances investor and analyst understanding and assessment of a company’s financial performance, fostering transparency, trust, and potentially boosting share prices and profitability.

Adopting IFRS encourages organizations to provide comprehensive and transparent financial information, improving the accuracy and clarity of asset-related reporting (Newman et al., 2016). Standardized financial reporting simplifies cross-border mergers and acquisitions, facilitating asset acquisitions across multiple countries and expanding overall asset portfolios.

H5: IFRS adoption significantly influences business growth

Methodology

Data and Sample

The chosen country for this study is Germany, renowned as the powerhouse of Europe’s economy and has a significant global influence. Germany’s robust economic stability and stringent regulatory framework provide an ideal backdrop for examining the enduring impact of capital structure decisions on business expansion. The country boasts a well-established capital market offering diverse funding avenues, including equities and debt (Thompson et al., 2018). Analyzing financing decisions within such a framework is particularly insightful, given Germany’s pivotal role in the European Union and the Eurozone, providing a unique perspective on capital structure within the context of a common currency and economic integration.

This study focuses on non-financial institutions listed on the Frankfurt Stock Exchange, spanning various manufacturing, technology, and services sectors. Concentrating on non-financial entities allows for a specialized examination of capital structure choices and their effects on expansion. Understanding how capital structure decisions affect risk management is crucial for non-financial firms that balance financial risks and returns on investment. Non-financial companies may prioritize innovation and research in Germany’s technologically advanced economy, emphasizing the importance of understanding capital structure choices on innovation and growth.

Data for this study was obtained from the Thomson Reuters Eikon DataStream, initially encompassing 432 non-financial institutions. Employing a purposive sampling strategy, 92 non-financial institutions listed on the Frankfurt Stock Exchange between 1994 and 2021 were selected, yielding 2,576 firm-years of observation. Companies with missing data within the specified timeframe were excluded. These selected companies represent 13 sectors, including construction and materials, food and drug retailers, electronics and electrical equipment, and others.

Dependent, Independent and Control Variables

The measurements and formulas for all variables are succinctly summarized in Table 1

Summary of Variables.

Dependent Variable

Sales Growth

Sales growth measures a company’s revenue or growth over a period. A key performance indicator (KPI) measures the company’s ability to increase market share, client acquisition, and product demand. Sales growth increases the firm’s revenue, allowing it to cover expenses, pursue new prospects, and expand (Eggert et al., 2014). Higher sales growth indicates high demand for the company’s products, boosting investor confidence and stock value.

Reduced sales growth might be financially challenging, especially if the company has high fixed costs (Karadag, 2015). Revenue may not cover expenses, resulting in losses or lower profits. Competitors with greater sales growth rates may take advantage of market possibilities and take market share from companies with lower sales growth. Poor sales growth may generate investor concerns about the company’s prospects, lowering stock prices and shareholder confidence.

Profit Growth

Profit growth measures the increase in a company’s net profit over a specified period compared to a preceding one. This critical financial metric measures a company’s ability to increase earnings over time. Higher dividends, share repurchases, or stock valuation improve shareholder wealth as profitability grows (S. Panigrahi & Zainuddin, 2015). Incredible profit growth gives companies more money for new prospects, acquisitions, RandD, and expansion, providing the groundwork for sustainable growth and competitiveness.

However, if expenses surpass revenue growth, profitability may stay high, and expenses may become impossible to fulfill. Low-profit growth may cause investors and shareholders to lose faith in the company, lowering stock prices and investor trust (Stulz, 2009). Companies with weaker profit growth may need help to fund new projects, RandD, and marketing, hindering their ability to adapt to changing market dynamics.

Asset Growth

Asset growth involves expanding a company’s overall assets over a specified period compared to a previous one. Cash, accounts receivable, inventory, property, plant, equipment, and intangibles are firm assets (E. L. Black & Zyla, 2018). Asset growth helps a corporation grow, allocate resources to new projects, and expand its resource base. High asset growth indicates a company’s expansion, market entry, or resource investment. This growth can increase market share and competitiveness (Bonaglia et al., 2007). Companies with greater asset growth rates may appear financially stable and ready to expand. Asset growth can enhance the company’s borrowing and creditworthiness.

Reduced asset growth may slow businesses’ growth compared to competitors by limiting activities or project launches (Gutiérrez & Philippon, 2016). In dynamic and competitive industries, lower asset growth may signal that a company is not aggressively pursuing new prospects or investing in its future, raising concerns about stagnation. Companies with slower asset growth may lose market share. High-asset growth rivals may outperform in innovation, capacity, and market share (Mazzucato & Parris, 2015).

Independent Variables

Debt to Capital Ratio

The debt-to-capital ratio compares total liabilities to total capital to ascertain the degree of financial leverage (Cole et al., 2015). The ratio measures how much debt a firm has compared to its total capital. It is determined by dividing the interest-bearing debt by the total capital. This ratio includes all debts, whether short-term or long-term. Common stock, preferred stock, and minority interests are all forms of shareholder equity that contribute to a company’s total capitalization.

A company’s debt-to-capital ratio indicates its financial health and investment possibilities. Higher debt increases financial distress risk. Companies with high debt may struggle to pay, especially during economic recessions or lousy business conditions. However, a smaller debt-to-capital ratio means less debt financing. This lowers financial distress risk but restricts financial leverage return amplification.

Long Term Debt to Capital Ratio

One way to measure a company’s financial leverage is by examining its long-term debt-to-capitalization ratio. This ratio shows investors a company’s ability to meet financial obligations over time. As debt becomes the primary source of funding, insolvency risk rises, making large ratios suggest riskier investments (Cummins & Nini, 2002). Financial experts recommend a balanced capital structure with equal debt and equity. A company’s financial leverage shows how much debt it uses to operate. A company with a high leverage ratio must generate more sales and profits than its debt. Long-term debt may benefit a corporation expecting rapid growth and high earnings. Due to lenders’ interest-only repayment and lack of profit share, debt financing is sometimes preferred over equity financing. Long-term debt can be overwhelming for financially unstable organizations and lead to bankruptcy.

Debt to Total Assets Ratio

The debt-to-assets ratio serves as a standard measure of a firm’s level of financial leverage. It quantifies the proportion of a company’s assets financed through debt rather than owned outright by shareholders. This ratio helps a company use its assets for growth (Hertina, 2021). Investors use the debt-to-assets ratio to assess a company’s financial soundness and ability to meet debt obligations and generate profits. A company’s debt-to-asset ratio indicates financial instability. It shows the company’s growth and asset accumulation. A debt-to-assets ratio above one means the corporation uses its assets to pay its debts. If interest rates change, companies with high ratios may default on loans (Emekter et al., 2015). Conversely, a debt-to-assets ratio below one shows that equity finances many of the company’s assets, reducing debt default and bankruptcy risks.

Debt to Equity Ratio

The debt-to-equity ratio is a fundamental measure for assessing how a company utilizes debt and equity to finance its assets (Atidhira & Yustina, 2017). It is calculated by comparing the firm’s total debt with its equity. Companies that use debt to finance their operations have a greater debt-to-equity ratio. Lower debt-to-equity ratios suggest better financial health, and creditors and investors consider companies with lower debt-to-equity ratios less risky (Sultan & Adam, 2015). Interest and debt service payments make debt financing more expensive than equity financing. Businesses with high debt should proceed cautiously. A high debt-to-equity ratio may be dangerous when the company has raised less capital from investors than creditors (Myers, 2001).

Choice of Regression Estimation

The study employed the generalized method of moments (GMM) to examine the impact of capital structure on business growth. This choice was made over pooled ordinary regression models, a random effect model, and a fixed effect model because GMM addresses issues of endogeneity and autocorrelation (Kanyir et al., 2022; Labra Lillo & Torrecillas, 2018) among explanatory variables by incorporating lags (Jean et al., 2016; Ullah et al., 2018). The dynamic GMM method integrates past values of both the dependent and instrumental variables to mitigate potential endogeneity concerns in dynamic panel models. This approach is particularly advantageous in addressing challenges such as unobserved heterogeneity, simultaneity, and potential endogeneity of regressors.

As per Roodman (2009), the validity of instruments is assessed using the Sargan test, where the statistical insignificance of the Sargan test ensures the model’s validity. Additionally, autocorrelation is examined using the Arellano-Bond (AR 2) test, with statistically insignificant results indicating no autocorrelation (Roodman, 2009).

Model Specification

The study employed three models to investigate the relationship between capital structure and business growth, presented below.

Table 1 provides detailed definitions of the variables. The error term was denoted as “ε,”“t” represents years, and “n” represents non-financial institutions.

Empirical Finding and Discussion

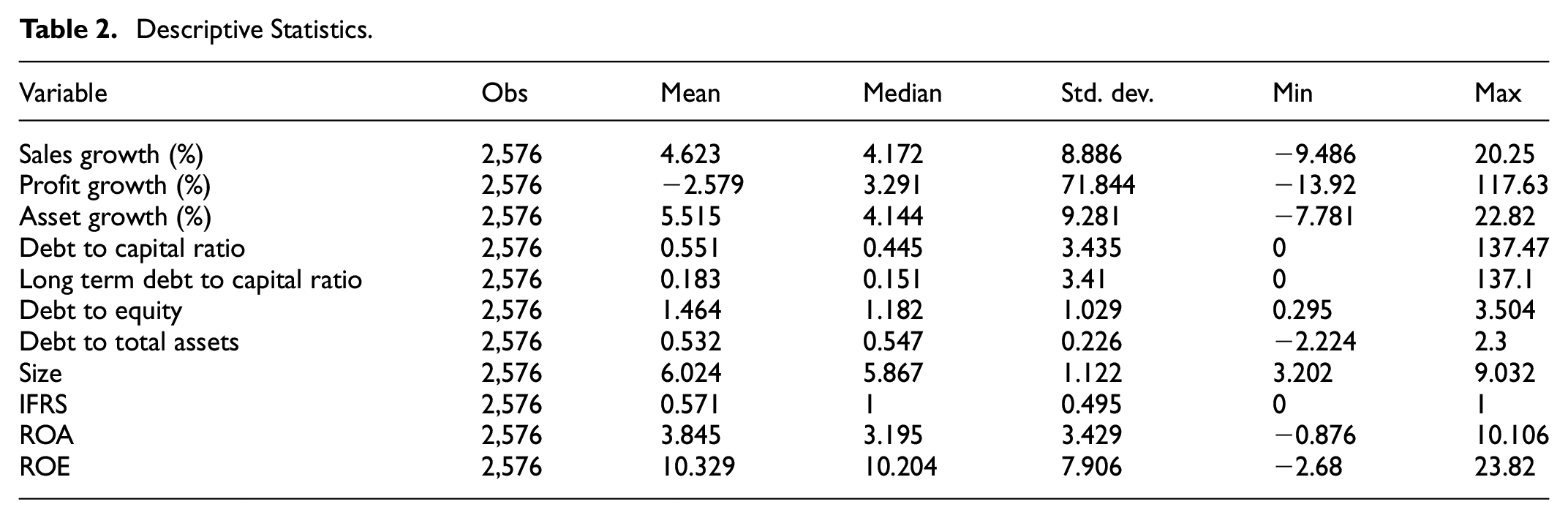

Table 2 presents the descriptive statistics of the variables. The median sales growth of 4.172% indicates the middle value of sales growth rates, suggesting moderate sales growth for the companies. It implies that half of the companies experienced sales growth rates higher than 4.172%, while the other half had growth rates lower than 4.172%. The overall performance, as reflected in the median, suggests a moderate level of sales expansion, serving as a benchmark for comparing individual companies’ sales growth rates.

Descriptive Statistics.

Similarly, the median profit growth of 3.291% indicates the middle value of profit growth rates. This suggests moderate profit growth, with half of the companies experiencing rates higher than 3.291% and the other half experiencing rates lower than this value. The company’s overall profitability indicates a moderate improvement in net profits.

Regarding asset growth, the median of 4.144% implies moderate growth, with half of the companies experiencing rates higher than this value and the other half experiencing rates lower. The overall expansion of assets, reflected in the median, indicates a moderate increase in the companies’ resources and capital base.

The median debt-capital ratio suggests that, on average, companies have moderate financial leverage, with a balance between debt and equity in their capital structure. Similarly, the median long-term debt-to-capital ratio indicates a relatively conservative level of long-term financial leverage, suggesting a cautious approach to leverage.

A median debt-to-equity ratio of 1.182 implies a balanced approach to financing, reducing the risk of financial distress. Companies around this median are less likely to face immediate financial difficulties related to debt obligations. Additionally, a median debt-to-total assets ratio of 0.547 suggests measured use of debt to support operations and investments without overreliance on borrowed funds.

Table 3 displays the outcome of the matrix correlation analysis, which was employed to assess the issue of multicollinearity. Multicollinearity occurs when two explanatory variables exhibit a perfect correlation (Arhinful & Radmehr, 2023a, 2023b). However, in the matrix correlation table, the explanatory variables show coefficients less than 0.70 between them (Mensah & Bein, 2023; Obeng, Arhinful, Mensah, Osei, 2024; Obeng, Arhinful, Mensah, Owusu-Sarfo, 2024; Obeng, Arhinful, Mensah, 2025; Obeng, Arhinful, Tessema, et al., 2025), indicating the absence of perfect correlation. Thus, the matrix correlation results suggest the absence of multicollinearity issues.

Matrix of Correlations.

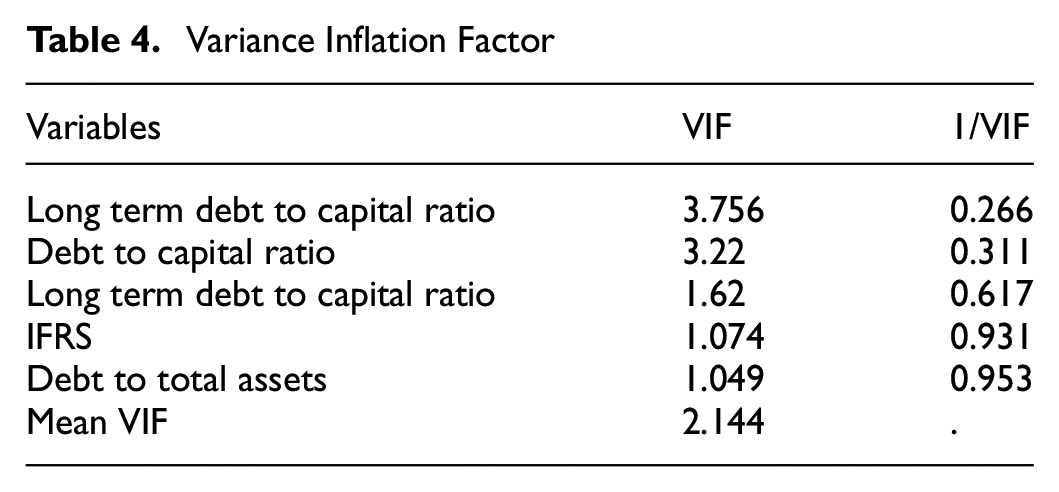

Table 4 presents the results of the variance inflation factor (VIF), which confirmed the absence of multicollinearity, as indicated by the matrix correlation. According to Amin and Cek (2023), Mensah, Arhinful, & Bein, (2024) and Mensah, Arhinful, & Owusu-Sarfo (2024), a VIF below 5 signifies the absence of multicollinearity. The findings reveal that all variables have VIF values below this threshold, with an average VIF of 2.144, further corroborating the absence of multicollinearity and supporting the results from the matrix correlation.

Variance Inflation Factor

Table 5 showcases the result of the panel unit root tests conducted using Levin–Lin–Chu (LLC). The unit root tests were carried out at level, and the first difference and all the variables were stationary, leading to the acceptance of the alternative hypothesis. The alternative results of LLC indicate the stationary nature of the variables.

Panel Unit Root Tests.

p < .01.

Validation of GMM Model

The validity of the GMM model was assessed using Sargan tests and Arellano-Bond tests. In all models, the statistically insignificant results of the Arellano-Bond (AR 2) tests indicate no autocorrelation (Arhinful et al., 2024; Mensah, Arhinful, & Bein, 2024; Mensah, Arhinful, & Owusu-Sarfo, 2024). Similarly, the non-significant Sargan tests suggest that the instruments used in the estimation are not correlated with the error term in the regression equation. This affirms their validity and indicates the absence of endogeneity or other biases in the results (Akinbode et al., 2021; Koroma & Bein, 2024; Arhinful, Mensah, Owusu-Sarfo, 2024c).

A non-significant Sargan test supports the exogeneity of the instruments, indicating that the instrumental variables are not correlated with unobserved factors influencing the dependent variable. This is crucial for ensuring the consistency and efficiency of the GMM estimator. Additionally, in the context of the overidentification test associated with the Sargan test, a non-significant p-value implies the validity of the set of overidentifying restrictions (moment conditions) imposed on the model (Arhinful et al., 2023a, 2023b; Bastardoz et al., 2023). This indicates that the number of instruments used is appropriate for the model.

Table 6 present the results of the GMM regression model, showing the effect of capital structure choices on business growth.

Dynamic Panel-Data Estimation, Two-Step GMM (Difference Method).

p < .01. **p < .05. *p < .1.

Model 1: The Effect of Capital Structure on Business Growth (Asset Growth)

The debt-to-capital ratio exhibited a significant negative impact on asset growth, and these findings support the study’s hypothesis. A high debt-to-capital ratio indicates a company’s heavy reliance on debt compared to its overall capital. While debt can be a valuable source of finance for growth and expansion, excessive dependence on debt can lead to financial difficulties. High debt levels increase interest payments and the likelihood of financial hardship, limiting a company’s capacity to invest in new assets (DeAngelo et al., 2002). This financial burden restricts the firm’s ability to allocate resources toward asset acquisition and expansion due to decreased available cash flow.

The findings presented here support the trade-off theory, demonstrating that the drawbacks of high leverage—such as increased financial risk and reduced financial flexibility—outweigh the advantages of debt financing. Companies with high debt-to-capital ratios may have trouble getting finance and may need to repay debt before investing in new assets (Akeem et al., 2014). The findings show that companies with larger debt-to-capital ratios may prioritize stability over asset expansion (Daniels & Elizabeth, 2010; Li & Zeng, 2019). High debt levels raise interest payments, limiting asset investment and growth funding. Companies may avoid growing debt due to concerns about bankruptcy and agency charges, limiting asset expansion (Ugur et al., 2022).

For practitioners in the field, this discovery emphasizes the importance of maintaining a balanced capital structure to sustain asset growth. Companies must prudently manage their leverage to prevent excessive debt accumulation, which can hinder their ability to invest in assets. Policymakers should prioritize promoting financial practices and policies that encourage responsible debt management, facilitate sustainable growth, and ensure financial stability for businesses.

Similarly, the long debt-to-capital ratio demonstrated a significant negative impact on asset growth, aligning with the study’s hypothesis. As companies increase their reliance on long-term debt, fixed-interest obligations may rise, reducing available financial resources for acquiring new assets (Siegel, 2021). According to the trade-off theory, businesses should evaluate the advantages of taking on debt, such as tax benefits, against the disadvantages, including the possibility of encountering debt-related problems and insolvency. Significant amounts of long-term debt exacerbate these risks and their corresponding expenses, potentially exceeding the advantages and hindering the growth of assets (Gregory et al., 2014). The results are consistent with the trade-off theory.

Due to economic uncertainties or industry obstacles, companies may avoid long-term debt, limiting asset expansion (Al-Hunnayan, 2020). The disadvantages of long-term financing may make it less appealing for new asset investment, reducing asset growth (Wu & Au Yeung, 2012). Keeping the debt-to-capital ratio high hinders asset accumulation, which affects decision-makers and practitioners. This shows financial managers and executives need a strong debt-to-equity ratio for long-term success. An unequal debt-to-capital ratio may hinder a company’s ability to invest in new prospects and assets, reducing innovation and competitiveness. Staying flexible and growing requires debt management.

These findings emphasize the importance of policymakers creating policies that encourage fair capital distribution. Implementing regulations that prioritize transparency and accuracy in disclosing financial information and debt management can mitigate the risks of excessive borrowing. Facilitating a favorable environment for firms to obtain equity financing can provide additional growth opportunities and reduce reliance on debt. By addressing these issues, policymakers can enhance overall financial stability and stimulate growth, resulting in a more robust and dynamic economic environment.

Furthermore, the study identified a significant negative impact of the debt-to-total assets ratio on asset growth, aligning with the study’s hypothesis. Rising debt-to-total assets ratios lead to higher interest expenses, constraining funds available for investment in new assets and hindering asset growth (Bloomfield, 2006). To reduce conflicts and agency costs, companies may limit debt to reduce its negative impact on asset growth (Canarella & Miller, 2022). The trade-off theory posits that firms should weigh the benefits of borrowing, such as tax breaks and cheaper capital expenses, against the risks of large debt, such as bankruptcy and financial issues. A high debt-to-total-assets ratio indicates significant business debt. Capital from debt can increase asset growth, but excessive leverage can counteract this. High debt levels increase financial risk, which may hinder investment in new assets due to distress costs and funding concerns (Habib et al., 2020). Thus, the company’s asset expansion may be limited.

For practitioners, this highlights the importance of maintaining a balanced capital structure. Companies must manage their leverage prudently to avoid the drawbacks of excessive debt, which can impede long-term growth and stability. Policymakers could implement strategies that incentivize companies to maintain optimal debt levels, promoting sustainable asset growth and ensuring overall financial well-being.

The debt-to-equity ratio exhibited a significant positive impact on asset growth, supporting the study’s hypothesis. According to the trade-off theory, a higher debt-to-equity ratio indicates that a company uses a larger proportion of debt compared to equity. Initially, this leverage can boost asset growth by providing additional funds for expansion and investment opportunities. Higher levels of debt financing often lead to a lower overall cost of capital, enabling more aggressive strategies for asset accumulation and growth (Almeida et al., 2011).

For practitioners, this discovery highlights the need to use debt strategically to facilitate the expansion of assets. However, it is crucial to diligently monitor and control leverage to prevent exceeding unsustainable levels of debt that may lead to financial distress. Policymakers should establish frameworks that promote responsible debt management and offer companies access to effective debt financing alternatives, thereby cultivating an environment that facilitates sustainable economic growth.

The adoption of IFRS also had a significant positive impact on asset growth, supporting the study’s hypothesis. Enhanced financial reporting transparency associated with IFRS adoption fosters investor confidence and effective capital allocation, attracting investment for asset expansion (De George et al., 2016; Kimeli, 2017; Neel, 2017; Opare et al., 2021). The rationale behind the findings is grounded in the principles of accounting standards like IFRS. IFRS clarifies, compares, and standardizes financial data to improve decision-making and investor trust. IFRS increases financial statement clarity, making finance more accessible and increasing investor interest (De George et al., 2016). Transparency can boost investor and creditor confidence, helping companies get funding under advantageous terms. IFRS financial reporting improves asset value estimation, enabling strategic decision-making and asset growth investment (Lev, 2018).

These findings suggest that transparent financial reporting rules like IFRS boost asset growth. IFRS helps companies communicate their financial health accurately, improving access to capital markets and growth resources. Implementing IFRS to boost asset growth and financial stability gives practitioners a strategic advantage. To boost economic growth and investment, policymakers should promote IFRS, especially in regions with changing financial reporting requirements.

Model 2: The Effect of Capital Structure on Business Growth (Sales Growth)

The study found that the debt-to-capital ratio had a positive but insignificant effect on sales growth, and the insignificant effect does not support the study’s hypothesis. The trade-off theory posits that a higher debt-to-capital ratio indicates substantial reliance on debt compared to overall capital. Increased leverage can fund expansion, marketing, and operational improvements, directly increasing sales. Debt financing lets organizations invest in revenue-generating projects like entering new markets, releasing new products, or improving sales and distribution (Rao & Bharadwaj, 2008).

Practitioners should note that this discovery emphasizes the advantages of using debt to facilitate sales growth. It highlights the need for a well-balanced capital structure that maximizes debt utilization to support growth. Companies should prudently control their leverage to ensure that the advantages of borrowing money outweigh the associated risks, thereby maximizing their potential for generating sales. Policymakers should create a conducive environment that facilitates access to debt finance while encouraging responsible financial management practices to enable long-term and sustainable sales growth.

Similarly, the long-term debt-to-capital ratio was observed to have a positive but insignificant impact on sales growth, and these insignificant results do not support the study’s hypothesis. Capital structure theory suggests that a high long-term debt-to-capital ratio indicates a significant reliance on long-term debt within a company’s capital base. Long-term debt finances development projects, technology investments, and industrial capacity expansion (Almeida et al., 2011). This capital growth helps companies improve operations, create new goods, and enter new markets, increasing sales. Long-term finance allows expansion project investment without short-term payback responsibilities.

This suggests that well-managed debt, especially long-term debt, can boost sales. Long-term debt can be used to make strategic investments that boost revenue and competitiveness. Companies may actively employ long-term debt to support major initiatives or capital expenses to grow sales (Flammer & Bansal, 2017). This positive link may be vital in capital-intensive sectors where long-term investments drive sales growth (A. Black & Hasson, 2016).

For practitioners, this outcome emphasizes the strategic use of long-term debt to fund expansion and increase sales. However, it is crucial to maintain a balance between the advantages of long-term debt and vigilant oversight of overall financial well-being to prevent excessive leverage. Policymakers should consider establishing conducive circumstances for companies to obtain long-term funding, as this can foster continuous economic growth and development.

Conversely, the debt-to-total assets ratio was found to have a negative and insignificant influence on sales growth, and insignificant results do not support the study’s hypothesis. Firms use the trade-off theory to balance the tax benefits of debt against the potential risks of financial difficulties. A high debt-to-total-assets ratio signifies significant leverage, which can provide tax advantages but also increases the risk of financial troubles. High debt-to-assets ratios increase financial commitments and insolvency risk (Hugonnier & Morellec, 2017). It may be difficult for the company to invest in growth, innovate, and expand due to financial pressure. Debt repayment may distract from revenue-generating operations and impede the company’s market adaptability.

This research highlights for practitioners the critical importance of controlling debt levels to prevent detrimental effects on sales growth. Businesses should aim for a balanced capital structure to effectively leverage debt without taking undue risk. Policymakers should consider endorsing financial procedures and rules that facilitate the optimal management of debt, assisting businesses in attaining long-term expansion while reducing the negative consequences of excessive leverage.

On the other hand, the debt-to-equity ratio showed a significant positive effect on sales growth, consistent with traditional capital structure theory and the study’s hypothesis. As the percentage of debt increases, the weighted average cost of capital (WACC) decreases, facilitating wealth maximization for the firm (Abeywardhana, 2017; Budhathoki & Rai, 2020). Companies may deliberately structure their capital to favor debt over equity, enabling them to utilize borrowed funds to support expansion efforts that drive sales growth (Parvin et al., 2020).

The trade-off theory asserts that a high debt-to-equity ratio signals increased debt dependence. Increased leverage can fund expansion, new endeavors, and scaling. Debt financing can help a company invest in sales-growing operations, including entering new markets, producing new goods, and expanding manufacturing (Gompers, 2022). The positive effect supports the trade-off theory, showing that debt for expansion can offset its costs within limitations. Companies can use leverage to lower financing costs and tax advantages to enhance sales.

Practitioners should consider this finding, as it highlights the potential benefits of using debt to support sales growth. However, it is crucial to maintain a balance between debt use and careful oversight of overall financial health to avoid excessive risk. Policymakers should develop frameworks that promote access to financing while encouraging responsible debt management practices, creating an environment conducive to sustainable sales growth.

Furthermore, adopting IFRS was found to have a significant positive impact on sales growth. IFRS implementation, as an internationally recognized accounting standard, may provide companies with enhanced access to global capital markets, thereby supporting sales expansion on an international scale (Musa, 2019). This positive impact suggests that complying with IFRS can facilitate access to a broader range of investors and financing options, ultimately enhancing a firm’s ability to achieve sales growth (Bakr & Napier, 2022).

Model 3: The Effect of Capital Structure on Business Growth (Profit Growth)

The study found that the debt-to-capital ratio negatively and significantly affects profit growth, which supports our hypothesis. According to the trade-off theory, a high debt-to-capital ratio means a company relies heavily on debt relative to its total capital. While debt can initially boost profitability through tax advantages and lower financing costs, excessive debt increases the risk of financial difficulties. Higher interest costs and debt obligations might lower corporate margins and growth. This negative impact on profit growth confirms the trade-off theory, suggesting excessive debt has costs beyond benefits. High debt-to-capital ratios can strain a company’s finances, resulting in higher interest payments and less reinvestment, limiting profit growth.

For industry practitioners, this finding underscores the importance of managing leverage carefully to avoid the negative impact of high debt levels on profitability. Companies should aim for an optimal capital structure that maximizes the benefits of debt financing while mitigating its potential drawbacks. Policymakers should promote practices and regulations that encourage balanced capital structures and effective risk management. This approach will help businesses sustain profitability and achieve growth.

The study discovered that the long-term debt-to-capital ratio had a negative and insignificant impact on profit growth and did not support the study’s hypothesis. According to the trade-off theory, a high long-term debt-to-capital ratio indicates that a company relies heavily on long-term debt relative to its overall capital. While long-term debt can initially provide funds for expansion and improve profitability through tax shields and lower interest rates, excessive long-term leverage introduces significant financial obligations and increases the risk of financial distress (Kashefi Pour & Lasfer, 2019). These obligations can raise interest costs and strain cash flows, ultimately restricting profit growth.

The trade-off theory posits that high long-term debt can negatively affect profit growth. Rising debt levels can put a company under financial pressure and limit its operational flexibility, hurting profit growth. Strategically using long-term debt to finance capital projects or acquisitions with long-term benefits may not immediately affect profit growth, resulting in little statistical significance. Long-term debt for strategic investments may postpone profit realization, explaining the insignificance. To minimize profit growth impacts, companies can match the maturity of their long-term debt with the expected lifespan of the assets being funded (Zou et al., 2019).

Industry players must recognize that managing long-term debt effectively is essential to avoid negative impacts on profitability. Companies should aim for an optimal balance between debt and equity to maximize financial benefits while minimizing risk. Policymakers should support regulatory frameworks and policies that encourage responsible use of long-term debt, fostering a stable environment conducive to sustained profit growth.

Furthermore, the investigation found a positive and insignificant effect of the debt-to-total assets ratio on profit growth. The insignificant results do not support the study’s hypothesis. The trade-off theory posits that a higher debt-to-total-assets ratio indicates a company relies significantly on debt relative to its assets. Increased leverage can boost profit growth by providing additional capital for revenue-generating projects and opportunities. Debt financing offers advantages such as tax benefits on interest payments and lower capital costs, which can enhance profitability.

This finding highlights the potential benefits of using debt to accelerate profit growth for practitioners. However, it is crucial to manage debt levels carefully to avoid financial distress that can result from excessive leverage. Policymakers should encourage balanced capital structures and create environments that promote effective debt financing practices to support sustainable growth.

The study discovered that the debt-to-equity ratio had a positive and significant impact on profit growth, consistent with findings by Degryse et al. (2012), Manalu et al. (2020), and Delen et al. (2013). This provided support for the study’s hypothesis. According to trade-off theory, firms balance the benefits of debt—such as tax shields and reduced capital costs—against the risks of financial distress associated with high leverage. A high debt-to-equity ratio reflects a company’s debt dependence. Increased debt can raise profits by funding investment and expansion. Lower financing costs and tax-deductible interest payments boost profitability with debt.

Profit growth supports the trade-off theory, suggesting that debt financing can exceed its hazards up to a point. Leveraging debt to invest in operational savings and growth possibilities can boost returns on equity and profit margins if done correctly. High debt-to-equity ratio companies are likely to be financially disciplined and efficient with capital. Positive debt-to-equity ratios may imply efficient loan utilization to boost operational efficiency and profit growth (Akhtar et al., 2016). The significant positive impact shows that well-managed debt improves financial performance. According to the financial discipline theory, a higher debt-to-equity ratio shows financial discipline and capital usage (Mworia, 2016).

This finding highlights the potential benefits of using debt to stimulate profit growth. However, it is crucial to manage leverage carefully to avoid financial distress and excessive risk. Policymakers should promote prudent financial management practices and support frameworks that help firms achieve sustainable profit growth while using debt effectively.

Moreover, the adoption of IFRS by firms had a positive and significant impact on profit growth, aligning with findings by Said (2019), Abdullah and Tursoy (2021), and Hameedi et al. (2021). Implementing IFRS enhances the ability to compare organizations, allowing investors to evaluate performance more accurately. This improved comparability can attract investment and positively impact profit growth (Lin et al., 2019). IFRS adoption allows investors to compare a company’s performance with industry norms more easily, enhancing investor trust (De George et al., 2016). Companies following IFRS reporting requirements may be viewed favorably by the market, leading to higher demand for their securities and improved profitability. The market preference for companies adopting globally recognized reporting standards (Ioannou & Serafeim, 2017) may have a positive and significant effect.

This finding underscores the importance of implementing IFRS to leverage the benefits of enhanced financial transparency and comparability. Improved financial reporting enables more informed strategic decisions and optimizes resource allocation, which can drive profit growth. To foster a more transparent and efficient financial environment conducive to profitability, policymakers should promote the adoption of IFRS, especially in regions where financial reporting standards are still evolving.

Table 7 presents the sensitivity analysis results conducted to assess the robustness of the main findings. The size of the firms, return on assets (ROA), return on equity (ROE), and three macroeconomic variables—GDP growth, inflation, corruption, and unemployment—were added to the initial regression to create an extended model. These macroeconomic variables are crucial factors considered by investors when choosing countries for investment or by business people when expanding their operations (Cumming et al., 2016; Sánchez-Martín et al., 2014). The results obtained from Table 7 confirm the robustness of the main findings presented in Table 6.

Robustness Testing.

p < .01. **p < .05. *p < .1.

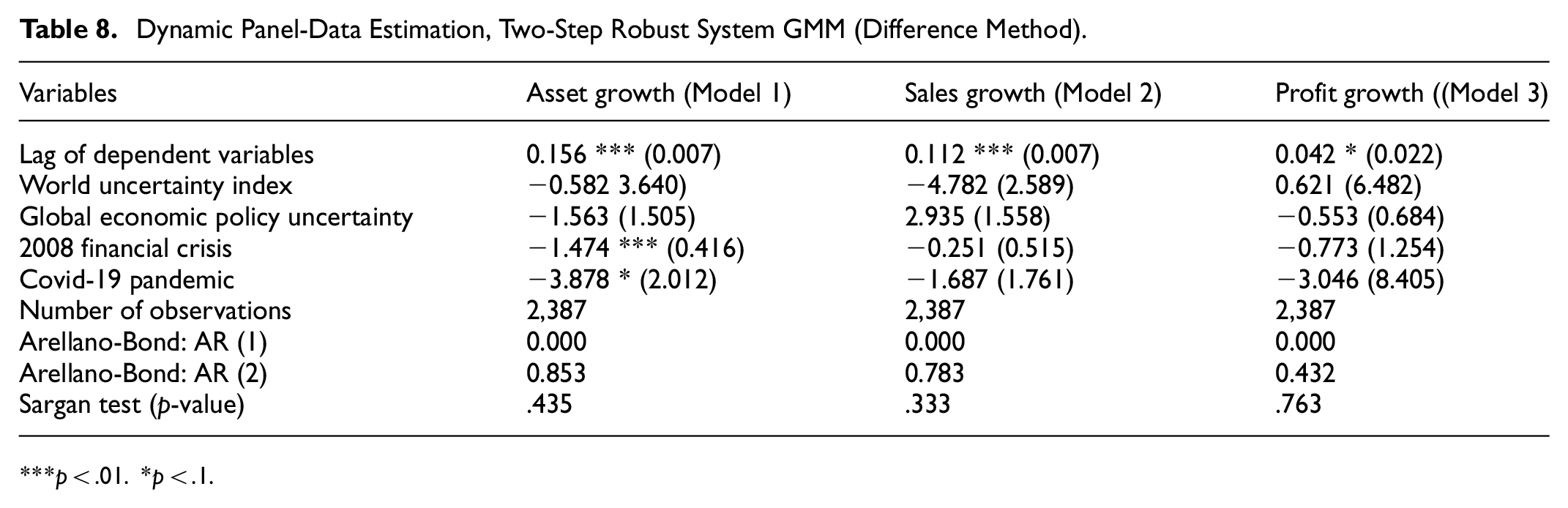

Table 8 presents the effects of WUI, GEPU, the 2008 financial crisis, and the COVID-19 pandemic on asset, sales, and profit growth. The study revealed that the World Uncertainty Index (WUI) had a negative impact on asset and sales growth but a positive impact on profit growth. Akron et al. (2020) demonstrated that the WUI negatively affects investment growth, aligning with this study’s findings. Similarly, Thongkairat and Khiewngamdee (2022) found that the WUI negatively impacts investment prices, consistent with the negative impact on assets and sales growth in this study. These results suggest that global economic uncertainty negatively affects asset and profit growth but positively impacts sales growth. This contradicts the findings of Athari (2021), who reported a positive impact of global economic policy on banks’ profitability in Ukraine. Furthermore, Huang et al. (2021) found a negative effect of global economic policy on non-financial asset allocation, supporting the negative impact observed in this study.

Dynamic Panel-Data Estimation, Two-Step Robust System GMM (Difference Method).

p < .01. *p < .1.

These results highlight the importance of efficiency and adaptability in uncertain environments for practitioners. To maintain profitability during periods of high uncertainty, organizations should implement robust risk management strategies and focus on optimizing their operations. Diversifying revenue streams and maintaining a strong balance sheet can also help organizations navigate these uncertain periods.

Moreover, the study found that the 2008 financial crisis negatively impacted business growth in assets, sales, and profit. These findings align with research by Naudé (2009), Akgün and Memiş Karataş (2021), Klapper and Love (2011), and Zeitun and Saleh (2015), which all demonstrated the negative impact of the 2008 financial crisis on investment growth and economic growth.

These findings highlight the importance of crisis management and financial resilience for practitioners. Firms should develop strategies to mitigate the effects of economic downturns, such as implementing flexible cost structures, diversifying revenue streams, and maintaining strong liquidity. Establishing robust risk management frameworks and contingency plans can help firms navigate financial crises more effectively.

Furthermore, the study revealed that the COVID-19 pandemic negatively impacted the asset, sales, and profit growth of firms in Germany. This is consistent with findings by Van Thi Hong Pham and Nguyen (2022), Qin et al. (2022), Nguyen (2022), and Gajdosikova et al. (2022), all of whom reported a negative impact of COVID-19 on sales growth profitability, investments, and economic growth.

Conclusion

One of the primary objectives behind establishing businesses is to ensure growth and survival. As growth is vital for the survival of any business, competent and skilled managers, well-versed in business planning and growth strategies, are often employed to ensure continuous expansion. A fundamental aspect of business incorporation involves the separation of ownership. When allocating resources, investors consider the growth potential of business operations as a key factor.

Capital structure plays a significant role in facilitating business growth. Capital is essential for various business activities, including procuring raw materials, acquiring assets such as plants and machinery, and covering employee wages and salaries, both permanent and seasonal. Thus, a firm’s capital structure significantly influences its success.

This study aimed to assess the impact of capital structure on the growth of firms listed on the Frankfurt Stock Exchange. Ninety-two non-financial companies listed on the exchange between 1994 and 2021 were examined. The study employed a two-step GMM to analyze this impact, addressing issues of endogeneity and autocorrelation.

The findings revealed that the debt-to-equity ratio had a positive and statistically significant effect on business growth, including assets, sales, and profit. However, debt-to-capital and long-term debt-to-capital ratios negatively impact asset and profit growth while positively influencing sales growth. Similarly, the debt-to-total-assets ratio exhibited a negative impact on asset and sales growth but a positive effect on profit growth.

Furthermore, firm size was observed to have a negative and statistically significant impact on sales, assets, and profit growth. Additionally, firms’ adoption of IFRS was found to positively impact sales, assets, and profit growth, indicating its role in enhancing financial performance and transparency. The study underscores the importance of capital structure in driving business growth, with specific ratios and standards playing crucial roles in shaping the growth trajectory of firms listed on the Frankfurt Stock Exchange.

Managerial Implications

Managers of Frankfurt Stock Exchange-listed companies should carefully evaluate the debt structure because the debt-to-equity ratio affects corporate growth. A precise balance between debt and equity is needed to boost growth while reducing financial risk. Effective debt management should consider short-term and long-term debt obligations. The debt-to-capital and long-term debt-to-capital ratios hinder asset and profit growth, emphasizing the need for capital structure management.

The positive effect of debt-to-capital and long-term debt-to-capital ratios on sales growth implies that targeted financial mechanisms can boost revenue. Managers might examine financing choices that support sales growth and organizational well-being. The debt-to-total-assets ratio hurts asset and sales growth, emphasizing optimizing asset usage. Managers should maximize asset effectiveness to expand while considering debt limits. The debt-to-total-assets ratio boosts profit growth, suggesting that prudent debt use can boost profits. However, managers must weigh the pros and cons of using debt to increase profits versus long-term viability and fiscal discipline.

The negative impact of firm size on sales, assets, and earnings shows that larger companies struggle to grow at the same rate as smaller ones. Managers of larger firms should consider agile expansion tactics to overcome scale constraints. IFRS improves sales, assets, and profit growth, proving that these global accounting rules may help companies improve financial performance. Managers should consider IFRS financial reporting for expansion. The impact of debt ratios on growth indicators emphasizes the need for nuanced risk management. Managers should alter financial strategies based on debt structure risk-return profiles.

Given the volatility of financial markets and corporate settings, constant monitoring and adjustment are necessary. Management must regularly assess its financial frameworks, debt levels, and expansion initiatives. This proactive approach allows for timely reactions to changing market and regulatory situations, ensuring the company’s financial health.

Direction for Future Studies

Future studies in this field should prioritize the following areas:

• Broaden the scope of research to include companies listed on various stock markets across different countries. Analyze how different economic and regulatory environments influence the relationship between capital structure and business growth, particularly following adopting IFRS. This comparative analysis can offer valuable insights into the effectiveness of capital structure strategies in diverse global contexts.

Footnotes

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability

The data that support the findings of this study are available from the corresponding author, upon reasonable request.