Abstract

Based on a quasi-natural experiment on the acceptance of China’s Golden Auditing Project II, this study investigates the impact of state audit digitization on the green technology innovation of SOEs and its mechanism using the difference-in-difference model. First, state audit digitization significantly improves the level of green technology innovation in SOEs, and this role is time-differentiated from green invention patents and green utility models. Second, the results of the heterogeneity test show that the facilitating effect of state audit digitization is reflected mainly in heavily polluting SOEs and central SOEs. Third, the influence mechanism test results found that state audit digitization promotes the green technology innovation of SOEs through R&D investment and subsidy channels, and the mediation effect of the environmental regulation channel is not significant. This study broadens the research related to the economic consequences of state audit digitization and the influencing factors of enterprises’ green technology innovation and reveals the significance of audit digital transformation.

Keywords

Introduction

Enterprises are important entities that promote economic development. While they create material wealth, they also negatively impact the ecological environment (Blampied, 2021). As the largest developing country, China’s environmental pollution is particularly prominent, facing serious environmental problems such as high emissions, energy consumption, and pollution (X. A. Li, 2021). Green technology innovation is the core means to solve the environmental pollution problem; it is difficult to realize the optimal allocation of environmental resources automatically, and the state must promote the green technology innovation of enterprises through appropriate environmental governance mechanisms (L. Zhao & Zhang, 2020).

With its preventive, revealing, and defensive functions in environmental governance, state auditing is an important method of monitoring corporate green technology innovations. We used Chinese data to study the impact of state auditing on corporate green technology innovation from a digital perspective for the following reasons: First, while enjoying the fruits of rapid economic growth, emerging market countries generally face increasingly severe environmental problems such as high emissions, high energy consumption, and high pollution. China is a typical representative of emerging market countries and has the commonalities of emerging market countries; its experience in environmental governance can provide a certain degree of reference for other emerging market countries. Second, digital technology is developing rapidly and is widely used in many fields, such as environmental and social governance. Digital technology has completely changed the traditional auditing thinking mode and supervision method system, bringing subversive changes in the field of auditing, and is an important tool for promoting the function of state auditing (Qin, 2014; Vogl et al., 2020).

As far as existing studies are concerned, the literature mainly focuses on the impacts of fiscal decentralization, credit allocation, and media attention on enterprises’ green technology innovation (X. Cai et al., 2020; B. Chen & Li, 2020; Shang et al., 2022; J. Zhang et al., 2022). There is a lack of research on the relationship between state auditing, an important environmental monitoring mechanism, and enterprises’ green technology innovation. Meanwhile, research on audit digitization is still lacking and mainly focuses on audit models, professional impacts, and realization paths (Cui & Yang, 2024; Fotoh & Lorentzon, 2023; Qin, 2014; Tiberius & Hirth, 2019). The acceptance of China’s Golden Auditing Project II (hereafter referred to as CGAP II) provides a good opportunity to study the economic consequences of state audit digitization. Therefore, we investigate the relationship between state audit digitization and green technology innovation of state-owned enterprises (SOEs) using the difference-in-difference model with data from Chinese A-share listed companies. Can the state audit digitization significantly affect the green technology innovation of SOEs? Does the relationship differ among SOEs with different traits? What is the impact mechanism of the above relationship? This will complement existing research. This study makes several contributions.

First, it extends the literature on audit digitization. Prior literature suggests that audit digitization has had a significant impact on the auditing profession and that the use of new technologies not only changes the audit process but also improves audit quality and narrows the audit expectation gap (Cui & Yang, 2024; Fotoh & Lorentzon, 2023; Tiberius & Hirth, 2019). Our study expands the scope of audit digitization research by exploring the impact of audit digitization on corporate green technology innovation. Second, this study extends the literature on corporate green innovation. Promoting corporate green innovation is a global phenomenon, and previous studies have investigated the roles of environmental enforcement, green finance, and media attention in corporate green innovation from the perspectives of administration and public finance (Z. Chen et al., 2022; Shang et al., 2022; Y. M. Zhang et al., 2021). Our study suggests that state auditing, an external supervisory force, can promote corporate green innovation. It is the first to investigate the impact of state audit digitization on green technological innovation in SOEs and its mechanisms. Third, our study has policy implications for corporate green innovation. This study reveals how state audit digitization affects the green technology innovation of SOEs, which can provide valuable guidance for emerging market countries to promote the green development of enterprises.

The remainder of this paper is organized as follows. Section 2 presents a literature review; Section 3 provides the theoretical analysis and hypothesis development; Section 4 explains the sample selection and data treatment; Section 5 presents the analysis of the model and regression results; Section 6 is the discussion, and Section 7 presents the conclusion and implications.

Literature Review

The literature on state audit digitization focuses on the use of audit digitization and its impact of state audit digitization on audit quality, corporate governance of SOEs, and anti-corruption. “The final purpose of the audit technique is to quantify those aspects of the management system that directly impact reliability and effectiveness” (Guldenmund et al., 2006). State audit digitization has “changed the technology and methodology of auditing” (Zhou, 2013). It can effectively improve the “timeliness and effectiveness of auditing” (Y. Zhang & Yang, 2021) in important economic sectors, but the heterogeneity of audit object data and audit technology innovations pose challenges to state audit digitization, which need to be addressed using information standardization (Ni et al., 2020). It has also been argued that although blockchain technology has led to the innovation of modern audit technology methods, independence remains the most critical factor for audit quality. In contrast, the lack of computing power resources, difficulties in physical and evidential collaboration, and audit skills are major challenges that must be addressed in audit digitization (Nguyen et al., 2016; C. Xu & Chen, 2020). Regarding the economic consequences of state audit digitization, digital technology has changed the sociotechnical relationship between workers and their tools (Bierstaker et al., 2001) and how work is organized (Vogl et al., 2020). In addition to improving audit quality, it adds value to corporate governance (Merhout & Havelka, 2008; Zheng et al., 2020). M. N. Guo et al. (2022) found that state audit digitization can facilitate SOEs to increase innovation input and output and thus improve innovation efficiency. Y. M. Jiang et al. (2021) argue that applying blockchain technology to state audits could promote information transparency, reveal hidden corruption, and improve the efficiency and effectiveness of big data in fighting corruption. Meanwhile, some scholars have investigated the impact of state audit digitization on the quality of economic development and found that it promotes green total factor productivity growth in regions and cities (Han et al., 2020).

Research on corporate green technology innovation has focused on measuring green technology innovation and its influencing factors. Many scholars adopt a scale or use indicators of green patents for measurement, for example, L. Li et al. (2020) used a scale to measure the level of green technology innovation of enterprises in terms of product recycling, green product innovation, and green publicity. However, more scholars use indicators of the number of green patents applied for or granted. J. Zhang et al. (2022) adopted the indicator of the proportion of green patents applied by listed enterprises to all their patent applications in that year, J. Xu and Cui (2020) and Tang and Yang (2022) who use the indicator of the number of green invention patent and green utility model applications, and X. Li et al. (2022) used an indicator of the number of green building patents. Meanwhile, some scholars have adopted the indicator of the cumulative years of green technology innovation (Zhong & Yang, 2021). Regarding the factors influencing green technology innovation, the existing literature has a more diverse focus, mainly on environmental regulation (X. Li et al., 2021; Shang et al., 2022), green finance (Z. Chen et al., 2022; X. Z. Li et al., 2022), media attention (L. Zhao & Zhang, 2020), fiscal decentralization (X. Cai et al., 2020; B. Chen & Li, 2020), government subsidies (X. A. Li, 2021; Yang et al., 2021), and R&D investment (Orlando et al., 2022; H. Zhao & Huang, 2020).

The above literature review reveals that green technology innovation is the key to achieving harmonious development of the economy, society, resources, and environment, and is also a hot topic in recent literature. Scholars have researched the factors influencing green technology innovation in enterprises from different perspectives. State audits facilitate the achievement of a state’s economic and political management objectives through supervision (Song et al., 2012). The use and promotion of digitization have changed the traditional system of audit supervision methods, improved the effectiveness of audit supervision, and helped strengthen the supervision of green technology innovation in SOEs; however, this has not been studied in the literature. This study empirically examines the impact of state audit digitization on green innovation in SOEs and its impact mechanism based on a quasi-natural experiment of CGAP II acceptance, which can enrich the research on state audit digitization and corporate green innovation and have certain implications for promoting corporate green innovation.

Theoretical Analysis and Hypothesis Development

According to fiduciary duty theory, ecology is a public good (Hakim & Yunus, 2017). The public is the ultimate principal of environmental protection and management, whereas governments and enterprises are trustees of environmental responsibility. Since environmental pollution has typical externality characteristics, in the case of information asymmetry between the principal and trustee, the trustee may cause damage to the interests of the principal because of trustee’s own claims, which in turn creates agency costs and causes serious social injustice (Nguyen et al., 2016). State auditing can compensate for the incompleteness of the environmental contract network, reduce the degree of information asymmetry between the public and fiduciary parties, and reduce agency costs by objectively and impartially monitoring and evaluating the fulfillment of environmental responsibilities.

Green development is an inherent requirement of China’s high-quality economic development strategy. The property rights characteristics of SOEs determine that they should play an important role in China’s green technology innovation system. However, in the current context, SOEs lack a high degree of self-awareness and long-term constraints on green technology innovation. “Green technology innovation is characterized by strong externality, high investment, and high risk” (J. Zhang et al., 2022), which not only brings positive environmental externalities but also may bring positive externalities of technological spillovers, and therefore needs to bear huge innovation risks, but is difficult to obtain high returns (Zhong & Yang, 2021). SOEs operators have the task of maintaining and increasing the value of state-owned assets, and the lack of incentives makes it difficult for them to form a positive attitude toward green technology innovation; they deliberately hide and provide false information to avoid their responsibilities. Regarding the supervisory constraints on SOEs, which are limited by time and space, traditional auditing methods can only obtain information through on-site audits, and “auditors are easily caught up in the mechanical, repetitive work of reviewing, checking, and verifying data” (Chang, 2021). At the same time, the heterogeneity of the audited units’ information systems and the possibility of concealment and falsification lead to low availability of audit information, making it difficult for auditors to systematically understand the status of the audited units and target audit suspicions; thus, the effectiveness of audit supervision is low.

After the completion of CGAP II, the networked audit system was fully implemented in the National Audit Data Center of the China Audit Office and local audit authorities and has been popularized and applied in networked follow-up audits of key industries and enterprises. The National Audit Data Center and Clearinghouse interconnect and share information among audit systems at all levels, realizing the transition from after-the-fact audits to full-process audits, sample audits to comprehensive audits, and single on-site audits to combined on-site and off-site audits (Zheng et al., 2020; Zhou, 2013). Increased audit breadth and depth can more comprehensively and effectively monitor SOEs’ fulfillment of environmental fiduciary responsibilities, such as environmental protection and green innovation, discourage management’s environmentally opportunistic and myopic behavior, and encourage SOEs’ long-term behavior and green technology innovation. Therefore, hypothesis 1 is proposed:

H1: State Audit Digitization can Promote Green Technology Innovation in SOEs

“The damage caused to the natural environment by governments and social organizations based on GDP pursuit motives threatens the public interest of the community” (C. Cai & Bi, 2014). Strengthening the supervision to fiduciary environmental responsibility of governments and enterprises becomes an important element of public fiduciary responsibility. By strengthening direct and indirect supervision, state audit digitization can promote green technology innovation in SOEs.

In terms of direct supervision, state audit digitization has improved the capacity of audit supervision, effectively identifying environmental protection formalism that may exist in the form of falsehoods, inconsistencies, and perfunctory responses and forming a long-term deterrent mechanism for the fulfillment of SOEs’ fiduciary environmental responsibilities, which in turn promotes their efforts to increase investment in environmental protection and R&D. Supervising SOEs to actively fulfill their social responsibilities is the duty and mission of the audit institutions (C. Cai et al., 2023), and it includes supervising the implementation of environmental protection policies, the management and use of environmental protection funds, the efficiency and effectiveness of environmental protection project implementation, and the use of power and fulfillment of responsibilities by SOE operators. The use of digital tools such as networked auditing and big data auditing can improve the professionalism of auditors, the objectivity of their judgments, and the dynamic supervision of the whole process of SOEs; reveal deficiencies and problems in the environmental management of SOEs; keep abreast of and follow up on the handling of environmental violations by environmental protection, judicial, and other government departments against SOEs; and curb the short-sighted and opportunistic behavior of operators, thus improving the timeliness and deterrent effect of state auditing. The stronger the deterrent effect of state audit supervision, the more likely that SOEs will increase their investment in environmental protection and R&D (C. Cai et al., 2021). Simultaneously, with the increased effectiveness of state audit supervision, SOEs may also take the initiative to increase their R&D investment to maintain good political and business relations and obtain support in loan financing, environmental subsidies, tax and electricity tariff concessions, and land use.

In indirect supervision, state audit digitization can supervise the government fulfilling its fiduciary environmental responsibilities, push the government to strengthen environmental regulations, and introduce environmental incentive policies, thus promoting green technology innovation in SOEs. China has adopted a decentralized model of environmental governance, with local governments assuming most of the implementation functions (C. Xu, 2011). In the implementation process, energy conservation and emission reduction are not consistent with local governments’ socioeconomic and political interests (Kostka & Hobbs, 2012), so the implementation behavior of local governments tends to deviate from the requirements of the central government, leading to environmental policy implementation bias. State audit digitization has further increased the breadth and depth of auditor oversight and the pressure on local governments to be environmentally accountable. According to career prospect theory, local government officials, as “political people,” see future promotion opportunities and potential political prestige as their current reward for their work (Holmstrom, 1999). They will, therefore take substantive governance measures to improve the progress and quality of local environmental governance. State audit digitization can also accelerate local governments’ introduction of environmental incentive-based policies. In addition to environmental regulatory measures, such as environmental protection legislation and enforcement, R&D subsidies to enterprises are also a common environmental governance tool used by local governments (X. A. Li, 2021). The provision of R&D subsidies can alleviate resource constraints and reduce the costs and risks of green technology innovation (Montmartin & Herrera, 2015), thus promoting green technology innovation in SOEs.

Based on the above analysis, the following assumptions are made:

H2a: State Audit Digitization Promotes Green Technology Innovation in SOEs through the Channel of R&D Investment by Enterprises

H2b: State Audit Digitization Promotes Green Technology Innovation in SOEs through the Channel of Government Environmental Regulation

H2c: State Audit Digitization Promotes Green Technology Innovation in SOEs through the Channel of Government R&D Subsidies

Sample Selection and Data Processing

Sample Selection and Data Sources

Our sample consists of A-share companies listed on the Shanghai and Shenzhen stock exchanges from 2008 to 2016. The reason for setting the starting and ending period as 2008 to 2016 is that CGAP II started in 2008 and was accepted and fully utilized by the National Audit Office and provincial audit offices in 2012. The construction of CGAP III by the National Audit Office began in 2016 (still under construction). The sample exclusion procedure was as follows: (a) because it was impossible to determine the time of completion and acceptance of CGAP II in the seven provinces of Tibet, Hainan, Heilongjiang, Inner Mongolia, Ningxia, Xinjiang, and Shaanxi, this part of the sample was excluded; (b) listed firms in the financial industry, ST, and *ST were excluded; and (c) sample firms with missing data on the study variables were excluded. Finally, 17,008 firm-year observations were obtained. The CGAP II acceptance time data come from the websites of the National Audit Office, provincial audit offices, and provincial development and reform commissions. The indicators of green technology innovation include the number of green invention patents and green utility models granted to listed companies and their subsidiaries annually. Data on green technology innovation and firm characteristics were obtained from the China Stock Market and Accounting Research Database (CSMAR). To reduce the influence of extreme values on the test results, this paper shrinks the continuous variables by 1%.

Variable Selection

The variables in the empirical model were selected as follows:

Explained Variables

The methods of measuring the level of green technology innovation of enterprises mainly include the use of statistics related to green patents (Tang & Yang, 2022), product processes, product recycling data (L. Li et al., 2020), and cumulative years of green technology innovation (Zhong & Yang, 2021). The statistics related to green patents reflect the innovation and application of enterprises’ technologies in resource conservation, energy efficiency improvement, pollution prevention, and control and can be a more intuitive measure of the overall level and scale of enterprises’ green technology innovation activities compared to other indicators. This study refers to the approaches of Tang and Yang (2022) and B. Wang and Qi (2016), using statistics related to green patents for measurement, that is, the number of granted green invention patents to measure the innovation level of green invention patents, and the number of green utility models to measure the innovation level of green utility models, which are denoted by Grninvt and Grnuty, respectively. Two types of patents—invention patents and utility models—are adopted because Chinese patents consist of three types—invention patents, utility models, and designs—with decreasing levels of technology innovation. Using these two types of patents can differentiate between the difficulty and innovativeness of firms’ patents (J. Zhang et al., 2022). The number of green invention patents and green utility models granted is used instead of the number of applications because the number of green patents granted after a review is considered the most direct reflection of a firm’s green technology innovation activities and more accurately reflects the level of green technology innovation. However, it has also been argued that green patents may be affected by political interference during the review process (Z. Wang et al., 2021). Therefore, this study used the number of green patent applications to measure firms’ green technology innovation in the robustness testing process to ensure the conclusions’ reliability and validity.

Explanatory Variable

The Difference-in-Difference (DID) model estimates the impact of an event by comparing changes in the treatment and control groups before and after the event (Y. Guo et al., 2020; Rajgopal & Tantri, 2022). Based on the basic idea of the DID model, this study considers the acceptance of CGAP II as a “quasi-natural experiment” based on the approaches of Y. Guo et al. (2020) and Rajgopal and Tantri (2022). First, the grouping dummy variable Gold is constructed; when the listed company is an SOE, Gold is assigned a value of 1; otherwise, it is assigned a value of 0. Second, the staging dummy variable Time is constructed. In the year when the provincial auditing authority where the enterprise is registered completes the acceptance of CGAP II and the following years, Time is assigned a value of 1; otherwise, it is assigned a value of 0. The event effect of state audit digitization is measured by the cross-multiplier term of the grouping and staging variables Gold*Time.

Control Variables

Considering that factors such as firm size and profitability may potentially affect firms’ green technology innovation, this paper draws on J. Zhang et al. (2022), Tang and Yang (2022), and X. Cai et al. (2020) to set the following control variables: human capital (Humcap), firm size (Size), growth capacity (Growth), profitability (ROA), investment opportunity (TobinQ), gearing ratio (Lev), firm age (Age), capital intensity (Capinten), and equity concentration (Top10). The specific definitions of all variables are presented in Table 1.

Definition of Variables.

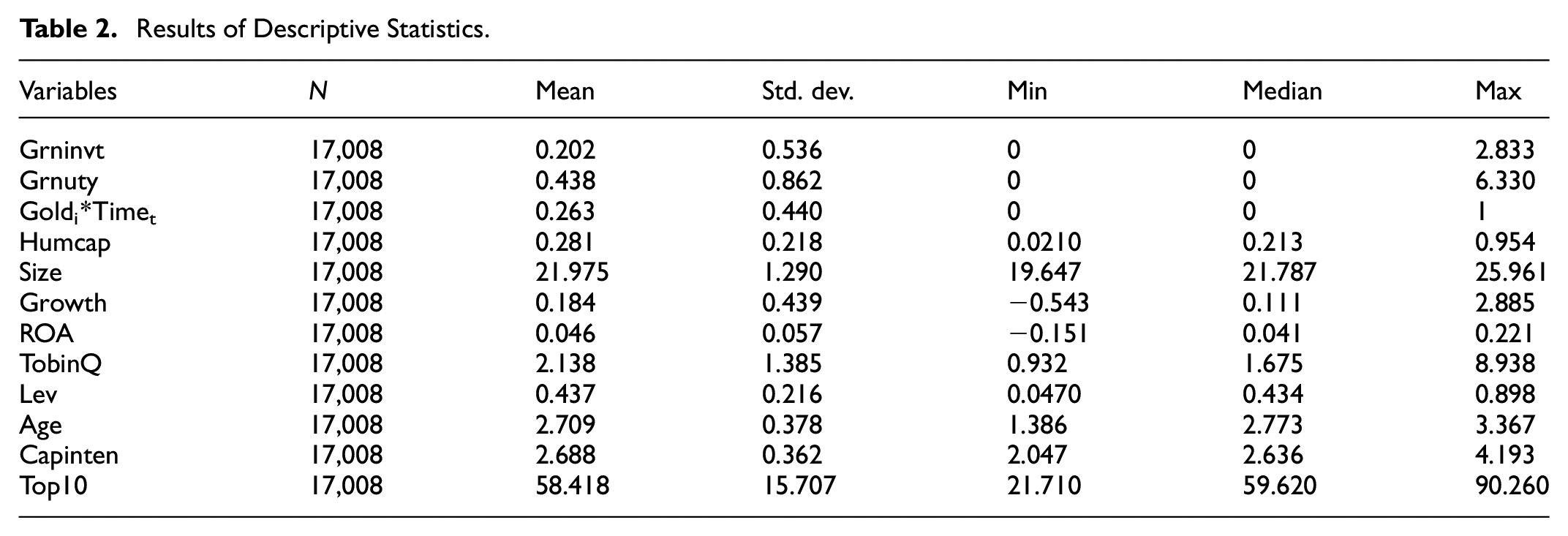

Table 2 shows the descriptive statistics for all variables. As can be seen from the statistical results, the mean for green invention patents (Grninvt) is 0.202, and the mean for green utility models (Grnuty) is 0.438, with a median of 0 for both. The mean is greater than the median, indicating that most of the sample firms do not have green invention patents or green utility models, and the overall green technology innovation capability of Chinese firms remains low, in line with the findings of Tang and Yang (2022). The mean value of state audit digitization (Gold*Time) is 0.263, indicating that 26.3% of the sample is affected by the CGAP II.

Results of Descriptive Statistics.

Table 3 presents the results of the t-tests for the means of the explained variables. The statistical results show that after the acceptance of CGAP II, the mean value of green invention patents increased by 0.152, and the mean value of green utility models increased by 0.247 among the sample companies; both were significant at the 1% level.

T-test for the Mean of the Explained Variable.

Note.***, **, * indicate that the test is statistically significant at the 1%, 5%, and 10% levels, respectively.

Model and Regression Analysis

Regression Model

The Difference-in-Difference (DID) model estimates the impact of an event by comparing the changes in the treatment and control groups before and after the event, which can better control for unobserved confounding variables. To test the impact of state audit digitization on green technology innovation in SOEs, this study draws on the results of Rajgopal and Tantri (2022) and Y. Guo et al. (2020) to construct the following DID model:

where Grntechi,t is green technology innovation, including green invention patents (Grninvt) and green utility models (Grnuty); Goldi*Timet is state audit digitization, the main explanatory variable of the model; Xi,t is the control variable, γi is the individual fixed effect, μt is the time fixed effect and εi,t denotes the random error term.

Baseline Regression

Fixed effects were added to the baseline regression to avoid endogeneity problems caused by individual and time factors. Table 4 shows the regression results of state audit digitization on green technology innovation, where columns (1) and (2) are regressions of green invention patents, columns (3) and (4) are regressions of green utility models, and columns (1) and (3) do not include control variables. The coefficient of Gold*Time is 0.041 (p < 5%) in Column (1) and 0.057 (p < 1%) in Column (2), suggesting that state audit digitization significantly increases the number of green invention patents in SOEs. The coefficient of Gold*Time is 0.056 (p < 5%) in Column (3) and 0.049 (p < 5%) in Column (4), indicating that state audit digitization also significantly increases the number of green utility models in SOEs. Thus, Hypothesis 1 is verified.

Baseline Regression Results.

Note. The t-statistics are shown in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Robustness Tests

To ensure the reliability of the study’s findings, four separate robustness tests were used in this paper: the parallel trend test, the placebo test, the propensity score matching method, and changing the measure of the explained variable.

Parallel Trend Test

The premise of using the DID model is that the treatment and control groups share a common trend prior to an event. Following Amore et al. (2013), this study sets up a series of dummy variables measuring the time to CGAP II acceptance, namely, Before1, Current, After1, After2, After3, and After4, and conducts parallel trend tests. The regression coefficients for Before1 and Current in Table 5 are insignificant, indicating no significant difference in the impact of state audit digitization on the treatment and control groups before and during CGAP II acceptance, thus satisfying the parallel trend hypothesis of the DID model. In Column (1), After3 and After4 are significant at the 10% and 5% levels, respectively, and in Column (2), After1 and After2 are significant at the 10% level. These results indicate that the promotional effect of state audit digitization on SOEs’ green utility models started to emerge in the first and second years after CGAP II acceptance. However, the promotional effect of state audit digitization on SOEs’ green invention patents did not emerge until the third and fourth years after CGAP II acceptance. This may be because green invention patents are more innovative and require longer development and patent examinations than green utility models. These results suggest that state audit digitization has a sustainable effect on green technology innovation in SOEs.

Dynamic Effects of State Audit Digitization.

Note. The t-statistics are shown in parentheses.

***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Placebo Test

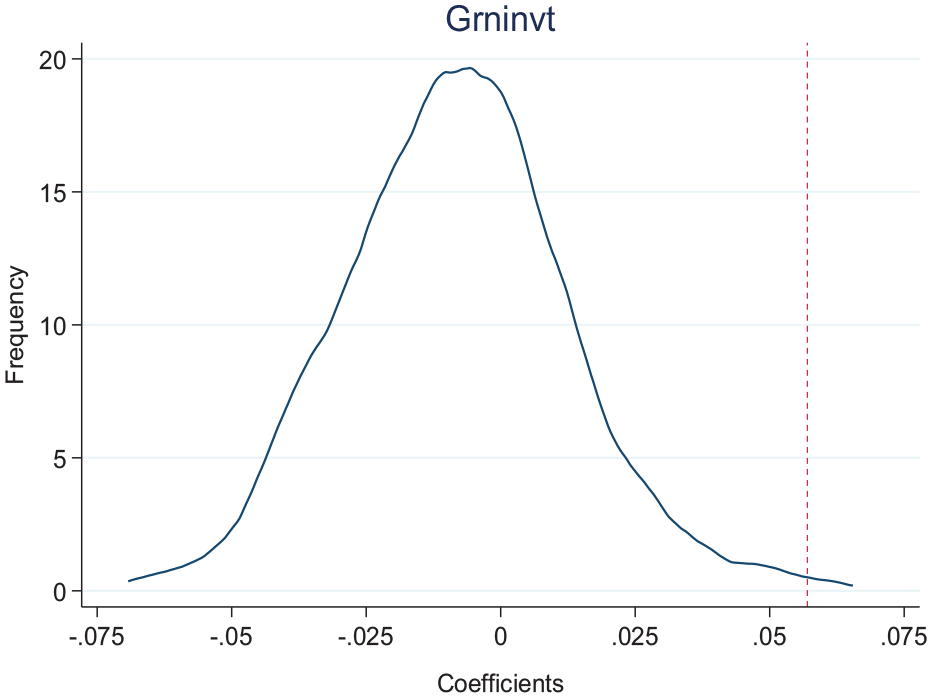

To demonstrate that green technology innovation in SOEs is caused by state audit digitization and not by other factors, this study draws on Cao and Zhang (2020) to randomly disrupt the treatment and control groups to determine the impact of state audit digitization on green technology innovation in SOEs. This was done by randomly selecting 810 firms as the treatment group based on the number of SOEs in the sample firms and the remaining firms as the control group and substituting them into the model for testing, after which the process was randomly repeated 500 times. After randomization, the impact of state audit digitization on green technology innovation in SOEs became insignificant. Figures 1 and 2 show the distribution of coefficients after the regression of Gold*Time against the green invention patent and green utility models, respectively, after 500 random repetitions. It can be seen that most of the regression coefficients for Gold*Time are smaller than the estimated true values of 0.057 and 0.049, indicating that the measurement error does not affect the conclusions of this paper.

Coefficient distribution of Gold*Time regressions with green invention patents.

Coefficient distribution of Gold*Time regressions with green utility models.

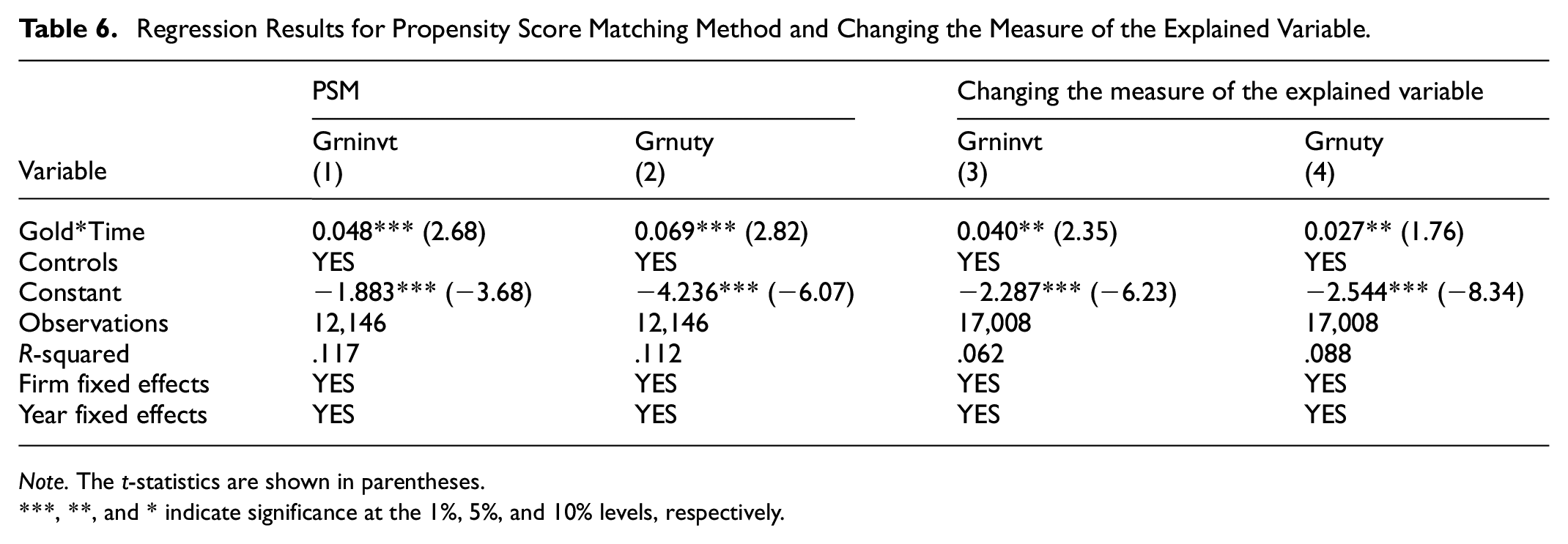

Propensity Score Matching Method

To mitigate the possible endogeneity problem caused by selectivity bias, this paper, following Y. Guo et al. (2020), uses the propensity score matching (PSM) method to select the sample closest to the audited SOEs as the new control group. This was done by selecting the model’s human capital, firm size, growth capacity, profitability, investment opportunities, gearing, firm age, capital intensity, and equity concentration as covariates, using the logit model to calculate propensity scores and a 1:1 nearest neighbor no-put-back matching of the sample data. The regression was then re-run according to Model (1) using paired sample data. The regression coefficients for Gold*Time in Columns (1) and (2) of Table 6 are both significantly positive at the 1% level, indicating that this study’s findings remain unchanged.

Regression Results for Propensity Score Matching Method and Changing the Measure of the Explained Variable.

Note. The t-statistics are shown in parentheses.

***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Changing the Measure of the Explained Variable

Z. Wang et al. (2021) argue that the number of green patents granted is unstable because of the possible influence of political factors and that the number of green patent applications is a more reliable and timelier indicator of a company’s green technology innovation capability. To ensure the robustness of the results, this study uses the number of green patent applications by listed firms as a proxy variable for green patent innovation. In Columns (3) and (4) of Table 6, the regression coefficients for Gold*Time are significantly positive at the 5% level, indicating that the findings of this study have not changed.

Heterogeneity Test

This study examines the heterogeneity of the relationship between state audit digitization and corporate green technology innovation regarding the industry and management authority of state assets.

Industry Differences

State audit digitization has improved the efficiency and effectiveness of audits, enhanced the state’s ability to regulate corporate environmental pollution, “increased the cost of corporate violations through the exercise of punitive power” (L. Li & Sun, 2019), and made firms aware of the state’s ability to conduct audits over a long period and with high intensity. Administrative penalties, operational uncertainty, and behavior in response to state audit digitization vary depending on the level of pollution emitted by companies. To explore the heterogeneous impact of state audit digitization on industries, this study classifies listed companies belonging to heavily polluting industries as heavily polluting enterprises and other listed companies as non-heavily polluting enterprises according to the Industry Classification Management List for Environmental Verification of Listed Companies issued by the Ministry of Ecology and Environment of China. Then, it uses model (1) for regression. In the regression results in Table 7, the regression coefficients for Gold*Time are 0.067 (p < 5%) in column (1) and 0.042 (p < 10%) in column (2), and the regression coefficient for Gold*Time is significantly positive in column (3) but not significant in column (4). These results show that state audit digitization’s green technology innovation effect differs among industries with different pollution levels. In heavily polluting industries, state audit digitization has a catalytic effect on green invention patents and green utility models; in non-heavily polluting industries, state audit digitization only has a catalytic effect on green invention patents. This conclusion is consistent with the findings of Y. M. Zhang et al. (2021), that is, heavily polluting enterprises are the key objects of environmental protection supervision, and in order to avoid damage to their reputation and interests under increased regulatory pressure, they will try to satisfy the environmental demands of stakeholders through technology innovation, regardless of the content of green technology innovations; on the other hand, non-heavily polluting enterprises are not the key objects of environmental protection supervision, which pays more attention to patents for green inventions that are highly innovative and effective in improving the environment.

Regression Results for the Heterogeneity Test.

Note. The t-statistics are shown in parentheses.

***, **, and * Indicate significance at the 1%, 5%, and 10% levels, respectively.

Differences in the Management Authority of State Assets

According to the management authorities for state-owned assets, China’s SOEs can be divided into central and local. “Compared with local SOEs, central SOEs are large and powerful and are the main form of state control over major industries and key areas of the national economy” (Yang et al., 2013). Regarding the audit supervision of state-owned assets, the National Audit Office supervises central SOEs, while local audit authorities supervise local SOEs (M. N. Guo et al., 2022). In terms of audit supervision quality, “the special office of the National Audit Office, which is vertically led, has higher audit quality than the local audit authorities, which are under dual leadership” (F. Wang et al., 2012). To investigate the difference in the impact of state audit digitization on green technology innovation between central and local SOEs, we use Model (1) to conduct a regression test on two different types of SOEs. Columns (5) and (7) of Table 7 show the regression results after excluding local SOEs, whereas columns (6) and (8) show the regression results after excluding central SOEs. The regression coefficients of Gold*Time in Columns (5) and (7) are 0.193 and 0.205, respectively, and both are significant at the 1% level, whereas the regression coefficients of Gold*Time in Columns (6) and (8) are not significant. These results show that the facilitating effect of state audit digitization on green technology innovation is mainly reflected in central SOEs, which is consistent with F. Wang et al. (2012) and M. N. Guo et al. (2022), who suggest that the quality of supervision by the National Audit Office for central SOEs is superior to that of supervision by local audit authorities for local SOEs.

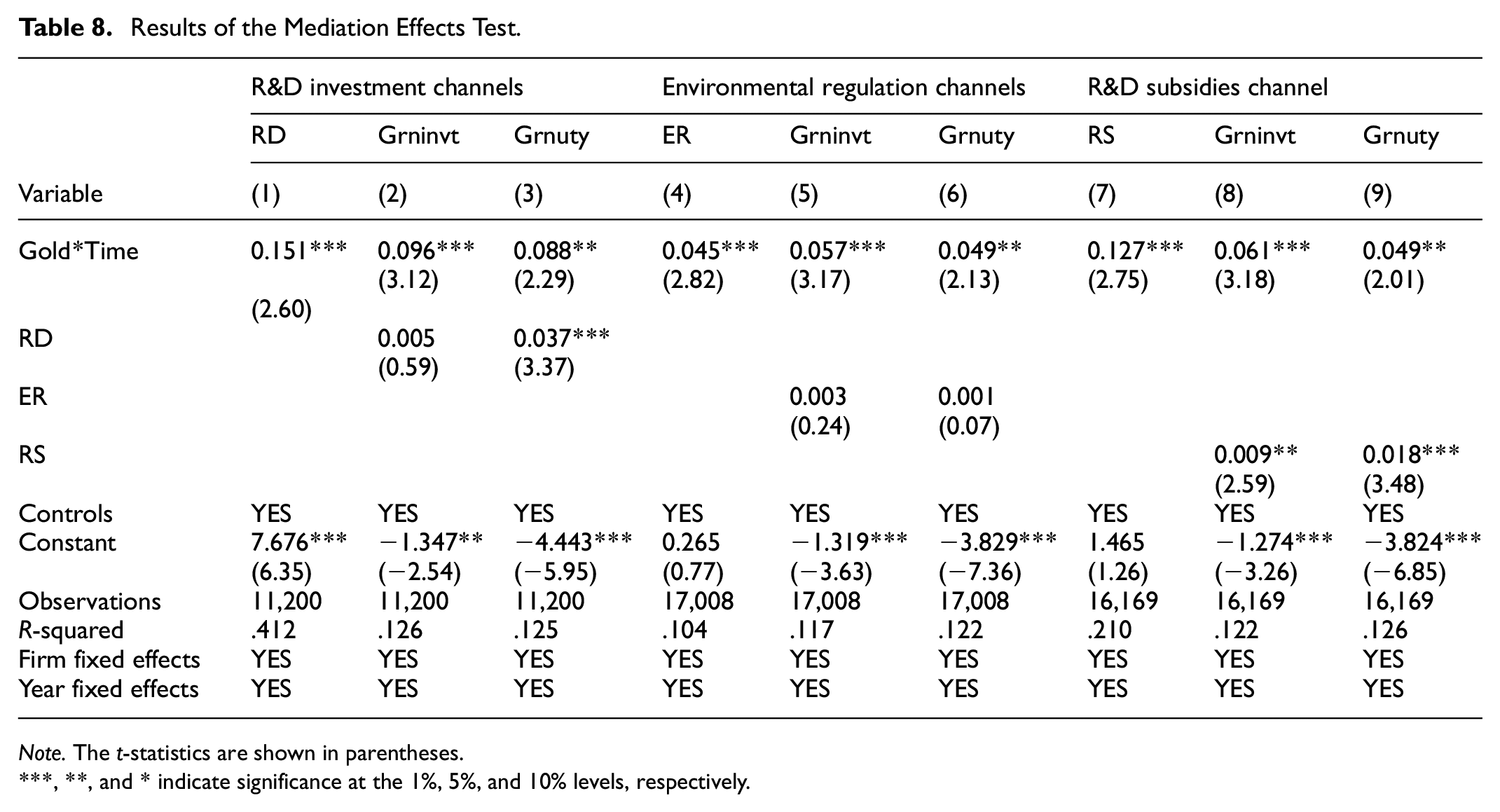

Testing of Impact Mechanisms

Based on examining the role of state audit digitization on green technology innovation in SOEs and its heterogeneity, this paper explores the impact mechanisms of state audit digitization from three channels: corporate R&D investment, government environmental regulation, and government R&D subsidies. Drawing on the mediation effect test of Y. Guo et al. (2020), this study constructed Models (2) and (3) based on Model (1):

where MEDi,t is the mediation variable, the transmission channel through which state audit digitization affects green technology innovation in SOEs. R&D investment (RD) is expressed as the natural logarithm of corporate R&D investment. Government environmental regulations (ER) were obtained using X. A. Li (2021) by performing the following steps: First, the emissions of major pollutants (wastewater, sulfur dioxide, and soot) from each province were normalized using the following formula:

where DPij and

The adjustment coefficient for each pollutant emission indicator was calculated using the following formula:

Where Wij is the adjustment coefficient for pollutant j in province i in each year, Eij/∑Eij is the ratio of emissions of pollutant j in province i to the emissions of the same pollutant in China in that year, and Yi/∑Yi is the ratio of GDP of province i to the total GDP of China in that year.

Finally, the level of environmental regulation for each province was calculated using the following formula:

Government R&D subsidies (RS) are the natural logarithm of R&D innovation subsidies received by firms from the government. The remaining variables were defined as described in the previous section.

Since a1 in the model (1) is significant at least at the 5% level, the coefficients b1 and σ2 are tested first. If b1 and σ2 are significant and σ1 is also significant, then there is a partial mediation effect. If b1 and σ2 are significant and σ1 is not, then there is a full mediation effect. A Sobel test is required if at least one of b1 and σ2 is not significant. If the Sobel test result is significant, there is a mediating effect; otherwise, there is no mediating effect.

R&D Investment Channel

The supervision of state audits can facilitate SOEs to increase their investment in environmental R&D, and studies have shown a correlation between R&D investment and corporate green technology innovation (Irfan et al., 2022; Orlando et al., 2022). Based on this, we use R&D investment as a mediation variable to examine whether state audit digitization enhances green technology innovation in SOEs through corporate R&D investment. Columns (1)–(3) of Table 8 report the test results for the R&D investment channels. The regression coefficient of Gold*Time in Column (1) is 0.151, which is significant at the 1% level, indicating that state audit digitization significantly increases the effort to R&D investment by SOEs. The regression coefficient of Gold*Time in column (2) is 0.096, which is significant at the 1% level, while the regression coefficient of RD is 0.005, which is not significant. After conducting the Sobel test, the Z-value of the test results was 0.746 (p > .1), indicating that the mediation effect was insignificant. The regression coefficient for Gold*Time in Column (3) is 0.088, significant at the 5% level, and the regression coefficient for RD is 0.037, significant at the 1% level. The Sobel test showed a Z-value of 2.983 (p < .01), indicating a significant mediation effect. The above results show that R&D investment only has a mediating effect on green utility models. R&D investment is a mediating variable for state audit digitization that promotes higher levels of green utility models in SOEs.

Results of the Mediation Effects Test.

Note. The t-statistics are shown in parentheses.

***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Environmental Regulation Channel

Local governments are the main participants and supervisors in environmental governance and provide standards and regulatory benchmarks for environmental protection. It has been found that state audit supervision can “effectively enhance the implementation and quality of local governments’ environmental governance” (Huang & Xie, 2022). It has also been argued that external environmental constraints motivate firms to engage in green technology innovation and that state environmental regulation can facilitate firms’ green technology innovation (X. Li et al., 2021; Shang et al., 2022). Based on this, we examine the impact of state audit digitization on green technology innovation in SOEs through an environmental regulation channel. Columns (4)–(6) of Table 8 report the results of the environmental regulation channel tests. In Column (4), the regression coefficient of Gold*Time is 0.045, which is significant at the 1% level, indicating that state audit digitization increased the level of environmental regulation by local governments. In Column (5), the regression coefficient of Gold*Time is 0.057, which is significant at the 1% level; the coefficient of environmental regulation (ER), although positive (0.003), is not significant. The Sobel test showed that the Z-value of the model was 0.293 (p > .1), and the mediation effect was insignificant. In Column (6), the regression coefficient of Gold*Time is 0.049, which is significant at the 5% level, and the coefficient of ER is 0.001, which is not significant. Using the Sobel test, the Z-value of the model was 0.082 (p > .1), and the mediation effect was insignificant. Together, these results suggest that state audit digitization fails to improve the level of green technology innovation in SOEs through government environmental regulations.

R&D Subsidies Channel

Government R&D subsidies can compensate firms for environmental compliance costs and reduce their R&D risks. Cheng and Hu (2020) find that when faced with environmental accountability, local governments reduce the disbursement of soft-binding government subsidies but do not reduce their subsidy support for firms’ environmental innovation. X. A. Li (2021) and Yang et al. (2021) find that government R&D subsidies significantly promote green technology innovation in firms. Based on this, we use R&D subsidies as a mediation variable to study the impact of state audit digitization on green technology innovation in SOEs. Columns (7)–(9) of Table 8 report the test results for the R&D subsidy channels. The regression coefficient of Gold*Time in Column (7) is 0.127, which is significant at the 1% level, indicating that state audit digitization increased the level of R&D subsidies to enterprises by local governments. The regression coefficient of Gold*Time in Column (8) is 0.061, significant at the 1% level, and the regression coefficient of R&D subsidies (RS) is 0.009, significant at the 5% level. The Sobel test showed a Z-value of 2.137 (p < .05). In Column (9), the regression coefficient of Gold*Time is 0.049, which is significant at the 5% level, and the regression coefficient of RS is 0.018, which is significant at the 1% level. The Sobel test showed a Z-value of 2.675 (p < .01). The combined results suggest that the mediating effect of R&D subsidies is significant. R&D subsidies are mediation variables in state audit digitization to promote green technology innovation in SOEs.

Discussion

Digital technology has changed traditional production processes and economic operation modes, reshaped market economic patterns, and affected the direction, scope, and extent of future economic and social development. Adapting to the digital transformation of the economy and society, making full use of digital technology and resources, and realizing the digital transformation of auditing are inevitable ways of improving the governance capacity of state auditing. This study explores the effect and influence mechanism of state audit digitization on the green technology innovation of SOEs.

First, state audit digitization significantly improves green technology innovation in SOEs. Previous studies have found that firms’ green technology innovation is influenced by green finance, fiscal decentralization, and R&D investment (X. Cai et al., 2020; Z. Chen et al., 2022; Orlando et al., 2022). Using the acceptance of CGAP II, a quasi-natural event, we test the impact of state audit digitization on the green technology innovation of SOEs and find that the improvement in audit supervision efficacy brought about by state audit digitization can also improve the level of green technology innovation of enterprises. This promotion function has a time difference between the green utility model and green invention patents, with a lagged effect on green invention patents.

Second, the role of state audit digitization in facilitating green technology innovation varies among SOEs with different pollution levels and management authorities. State audit digitization can encourage heavily polluting SOEs to improve their green invention patents and green utility models. However, it only contributes to green invention patents for non-heavily polluting SOEs. This finding further supports the findings of S. L. Jiang and Wu (2024) that heavily polluting firms are subject to greater environmental pressures than non-heavily polluting firms and that stringent regulations prompt them to invest more resources in green technology innovation. Our study also found that state audit digitization only facilitates green technology innovation in central SOEs; it is not significant for local SOEs. This finding is consistent with F. Wang et al. (2012) and M. N. Guo et al. (2022), who suggest that the quality of supervision conducted by the National Audit Office for central SOEs is better than that conducted by local audit offices for local SOEs.

Third, the results show that state audit digitization encourages SOEs to improve their green utility models through the R&D investment channel and promotes SOEs to improve their green invention patents and green utility models through the government R&D subsidy channel. However, the mediation effect of the government environmental regulation channel is not significant. This shows that resource investment is a key factor in enterprises’ green technology innovation and that state audit digitization forces enterprises and governments to increase environmental protection investment by strengthening audit supervision, thus enhancing enterprises’ green technology innovation level.

Conclusion and Implications

Conclusion

Based on the acceptance of CGAP II, this study empirically examines the impact of state audit digitization on SOEs’ green technology innovation and its mechanisms using the DID model. The study finds that (1) state audit digitization significantly improves the level of green technology innovation of SOEs; (2) the facilitating effect of state audit digitization is mainly reflected in heavily polluting SOEs and central SOEs; and (3) state audit digitization promotes green technology innovation of SOEs through the R&D investment and subsidy channels, and the mediation effect of the environmental regulation channel is not significant.

Theoretical Contributions

The results of this study provide new evidence on firms’ green technology innovations and the economic consequences of state auditing. First, it examines whether state audit digitization affects SOEs’ green technology innovation and provides a new perspective for studying influencing factors related to green technology innovation in enterprises. The literature suggests that environmental regulations, green finance, media attention, and fiscal decentralization influence corporate green technology innovation. Our study shows that state audit digitization also influences corporate green technology innovation. Second, we extend the literature on audit digitization because this study is the first to use CGAP II acceptance to examine the impact of state audit digitization on green technology innovation in SOEs and its mechanisms. Third, this study contributes to the literature on environmental governance in emerging markets. Our research suggests that state auditing is also an important environmental governance tool and that emerging market countries can improve the quality and effectiveness of audit regulation through state audit digitization, which in turn promotes green technology innovation in enterprises.

Practical Implications

This study had several practical implications. First, the study shows that audit digitization can enhance audit supervision capacity and promote the effective implementation of fiduciary environmental responsibility. Thus, emerging market countries should further improve state audit digitization and increase the training of auditors on digitization technology. Information technology has dramatically changed the concepts and methods of modern auditing. Auditing techniques and methods are changing and developing in the direction of data, intelligence, timeliness, and predictability, and digital operations have become the norm in auditing. It is important to note that the digitization of auditing will not occur overnight. On the one hand, it is necessary to improve auditing regulations and the construction of a big data platform per the development strategy for state audit digitization and increase research and development of audit analysis models and software; on the other hand, it is also necessary to focus on training auditors in digital technology. Second, the study results show that state audit digitization only has a facilitating effect on the green technology innovation of central SOEs, but not on local SOEs; therefore, attention should be paid to the audit supervision carried out by local audit authorities on local SOEs. Local audit authorities should actively use the results of state audit digitization to strengthen audit supervision, promptly discover local SOEs’ deficiencies in green technology innovation, and urge them to rectify these deficiencies. Higher-level audit authorities should strengthen their supervision and guidance for local audit authorities and standardize their working procedures and methods. Simultaneously, local audit authorities can cooperate with external supervisory authorities, such as the Supervisory Commission, to improve audit supervision synergy. Third, the study found that state audit digitization promotes the green technology innovation of SOEs through enterprise R&D investment and government R&D subsidies; thus, audit authorities should focus on the R&D investment of SOEs and local governments in green technology innovation. Audit authorities should, on the one hand, audit the sources of funds, fund arrangements, utilization of funds, and project management of R&D inputs by SOEs and, on the other hand, pay attention to the compliance, appropriateness, and performance of environmental protection subsidies provided by local governments to enterprises.

Limitations and Future Research

This study has the following limitations. First, the construction period of the CGAP is divided into three phases: the construction of an on-site audit system and audit management system in Phase I, the construction of a networked audit and big data audit in Phase II, and the construction of an economic security and performance evaluation system in Phase III; however, this study only focuses on the impact of the acceptance of CGAP II. Second, it does not compare the differences between state audit digitization and accounting firms’ audit digitization regarding the impact of corporate green technology innovation. Digital technology, which can both improve audit efficiency and effectively reduce audit risk, is widely used in accounting firms. However, this study does not include accounting firms in the scope of investigation. Therefore, future research directions include (1) studying the changes in green technology innovation, operational efficiency, and development quality of SOEs during the period from the inception of the CGAP to its completion and (2) studying the current status of the use of digital technology tools in accounting firms and their impact on auditors’ professional judgment and audit risk.

Footnotes

Acknowledgements

This article is supported by Guangdong Office of Philosophy and Social Science. Jing Wang is the corresponding author of this paper. Authors appreciate the valuable comments from editors and anonymous reviewers.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research received funding from the Guangdong Office of Philosophy and Social Science (Grant No. GD20YDXZGL07).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

All the data used in this analysis will be made available upon request.