Abstract

This study examines the association between various uncertainties and corporate investment and further investigates this association between state-owned enterprises (SOEs) and non-state-owned enterprises (non-SOEs). Moreover, this study analyzes the indirect effects of uncertainty on corporate investment through cash flow. The current research uses an unbalanced panel data of Chinese nonfinancial listed firms for the period 1999–2016. To control endogeneity issues, this study applies a robust two-step system generalized method of moments (GMM) technique to estimate the model. Empirical findings indicate that market-based and firm-specific uncertainties have positive effects, whereas economic policy and CAPM-based uncertainties have negative effects on corporate investment. Furthermore, results indicate that the effects of market-based, CAPM-based, and firm-specific uncertainties (economic policy uncertainty) were less (more) prominent for SOEs. Additional analyses show that cash flow stimulates the effect of firm-specific uncertainty on SOEs’ investment, whereas it weakens the influence of CAPM-based uncertainty (economic policy uncertainty) on investment of non-SOEs (SOEs). Moreover, cash flow attenuates the market uncertainty effect on investment.

Introduction

Researchers have exerted substantial effort in attempting to understand the nature of the uncertainty–investment relationship at the firm and market levels. However, the nature of this relationship is still inconclusive (i.e., uncertainty may positively or negatively affect the investment) from the empirical and theoretical perspectives.

Real options theory (Bernanke, 1983; Dixit & Pindyck, 1994) 1 states that uncertainty adversely affects investment in terms of irreversible capital by obtaining maximum information, which resulted from waiting. 2 Hartman (1972) considers the convex function of the marginal product of capital and argues that firms invest substantially in a high degree of uncertainty. The marginal product of capital is a convex function of stochastic variables under the assumptions of constant returns to scale production technology, perfect competition, risk-neutral firms, and reversibility of adjustment cost function. To support the aforementioned argument, Abel (1983) and Caballero (1991) confirm that uncertainty stimulates investment by extending Hartman’s discrete-time result to a continuous setup. Caballero (1991) proves that under the assumptions of nonconstant returns to scale production technology and imperfect competition, the result of Hartman–Abel can be opposite (i.e., the negative uncertainty–investment nexus). Previous studies have also provided evidence that uncertainty positively influences investment (Baum et al., 2008; Ma, 2015; Shaoping, 2008).

Although researchers have considerably focused on investigating how uncertainty influences investment in developed economies (Bloom et al., 2007; Gulen & Ion, 2015; Kang et al., 2014; Rashid, 2011), only a few studies have explored the phenomena for firms operating in transition economies. Moreover, the literature on uncertainty and investment association for various natures of firms is limited if nonexistent. The current study seeks to expand the literature by exploring the investment and uncertainty association for a transition economy, namely, China.

Prior studies have shown that potential lenders in a highly uncertain environment may be less or unable to determine the credit worthiness of firms, thereby limiting these firm’s capability to raise funds from external sources. In such an environment, lenders demand a high risk premium to provide funds, which leads firms to become liquidity constrained. In the case of internal fund deficiency, state-owned enterprises (SOEs) generally rely on state-owned banks and can access credit easily. By contrast, the non-SOE counterpart substantially relies upon their self-generated funds (Guariglia & Yang, 2016; Khan et al., 2019). Hence, we expect that uncertainty significantly affects investment, either solely or through variations in cash-flow, which may vary across firms of different nature. Previous studies have investigated the influence of cash flow on firms’ investment by introducing cash flow in the basic investment model. However, no previous research has examined whether cash flow has a stimulating or mitigating effect on the uncertainty–investment relationship between Chinese SOEs and non-SOEs. This study also fills in this gap by studying the association among the uncertainty, cash flow, and investment behavior of SOEs and non-SOEs separately.

This study examines the uncertainty–investment relationship for Chinese firms for two reasons. First, as a transition economy, China is moving from a command-based to a market-based economy, and the economy is under a high policy uncertainty (Wang, Chen, & Huang, 2014). Therefore, it will influence firms’ costs, sales, and earnings. China is adopting and practicing free-market principles, thereby creating many investment opportunities for listed firms. However, firms may face variations from different aspects because the capital market is underdeveloped and the market remains in the transition process. Therefore, uncertainty will likely have a significant influence on corporate decisions, particularly those related to investments. In particular, investment is often irreversible and costly in terms of uncertainty. Policy changes can influence the investment behaviors of firms and make the environment uncertain in which firms operate. The prior literature clearly indicates that policy uncertainty has an adverse influence on corporate investment and, therefore, reduces economic growth. Second, the nature of ownership (i.e., SOEs and non-SOEs) is one of the distinctive attributes of Chinese firms. Compared with non-SOEs, SOEs evidently suffer more from various government policies (Fan et al., 2013). In addition, SOEs can access the “policy lending” by state-owned banks, thereby making obtaining loans from state-owned banks comparatively easy for SOEs. For example, SOEs obtain discounted loans from banks to generate funds for investment (some of their interest payments are subsidized by the government) because the government encourages and finance them to develop further (Bo & Zhang, 2002). By contrast, non-SOEs face problems in obtaining loans from banks and rely primarily on their internal funds (Guariglia & Yang, 2016). Kang et al. (2000) argue that firms with close relationships with banks can facilitate and improve investment policies, thereby increasing shareholders’ wealth. Guariglia and Mateut (2016) document that firms with political connections can easily access external financing compared with those that are not politically connected. Therefore, we assume that in a transition economy, fluctuations in various uncertainties influence the investment behavior of firms, which may differ across firms of different nature.

Using Chinese nonfinancial firms during the period 1999–2016, we show significant and positive (negative) impact of market and firm-specific uncertainties (CAPM-based and economic policy uncertainties) on investment. Furthermore, the results show that the impact of market-based, CAPM-based, and firm-specific uncertainties (economic policy uncertainty) on investments are less (more) prevalent for SOEs. Additional analyses show that cash flow strengthens the investment of SOEs when firm-specific uncertainty is high, whereas it weakens the negative impact of CAPM-based uncertainty (economic policy uncertainty) on the investments of non-SOEs (SOEs). Moreover, cash flow has a mitigating impact on the investment of both types of firms under a high market uncertainty. Our findings are robust to several diagnostic tests and alternative proxies for investment, market, and firm-specific uncertainties.

The current study provides three key contributions. First, unlike previous studies (Baum et al., 2008, 2010; Dibiasi et al., 2018; Wang et al., 2014; Xu et al., 2010), we investigate the effects of economic policy uncertainty, along with CAPM, market, and firm-related uncertainties on corporate investment. Therefore, the current research offers important contributions to the literature by studying the effects of four forms of uncertainties on investment. Second, this study examines the differential impact of different forms of uncertainties on the investments of SOEs and non-SOEs. Our findings indicate that the uncertainty–investment relationship varies for firms of different nature. Finally, we contribute to the literature by identifying the factors that can strengthen or weaken the uncertainty–investment association. We explore that cash flow is one of the attributes that can moderate the association between investment and uncertainty.

The remainder of this article is organized as follows. Section “Literature Review and Hypothesis Development” reviews the literature and develops hypotheses. Section “Data, Variables Measurement, and Descriptive Statistics” explains the data set and measures the variables. Section “Econometric Model” presents the econometric model. Section “Empirical Findings” reports the empirical findings. Finally, Section “Conclusion” provides the conclusion.

Literature Review and Hypothesis Development

Researchers have empirically investigated the nature of the uncertainty and investment association, although the theoretical relationship between uncertainty and investment remains inconsistent (Wang et al., 2014). Nickell (1978) finds that the attitude of firms in making investment decisions toward uncertainty may be positive or negative and argues that risk-averse (risk-taker) firms invest less (more) in a highly uncertain environment. Shaoping (2008) argues that uncertainty–investment relationship depends on modeling, specific assumptions, and sample type.

Bernanke (1983) and Dixit and Pindyck (1994) propose real options theory of irreversible investment decisions under uncertainty. Several studies have supported this theory by suggesting a negative uncertainty–investment association for various countries. For example, Leahy and Whitcd (1996), Kang et al. (2014), and Gulen and Ion (2015) for the United States; Bloom et al. (2007) and Rashid (2011) for the United Kingdom; Ma (2015) for Australia; and Rashid and Saeed (2017) for Pakistan. Xu et al. (2010), Wang et al. (2014), An et al. (2016), and Khan et al. (2019) show the negative uncertainty–investment relationship for Chinese firms. Bloom et al. (2007) and (Ma, 2015) argue that a high level of uncertainty weakens firms’ response of irreversible investment to demand uncertainty. Baum et al. (2008) document a negative effect of CAPM-based and firm-specific uncertainties on investment, whereas market-based uncertainty has a stimulating impact. They also show that investment is more affected by firm-specific uncertainty than market-based uncertainty. Moreover, Rashid (2011) reports the significant negative effects of both forms of uncertainty on private firms’ investment. Rashid and Saeed (2017) find that Pakistani firms decrease investments when they face a high market or firm-related uncertainty. Khan et al. (2019) indicate a negative influence of economic policy and CAPM uncertainties on Chinese firms’ investment behavior. Xu et al. (2010) present a negative influence of uncertainty on Chinese firms’ investment and further show that this effect is positively moderated by government control.

Hartman (1972) considers the convex function of the marginal product of capital and explains that firms make substantial investments in response to high uncertainty. Caballero (1991) uses market structure and returns to scale as bases to explain that under the assumptions of constant returns to scale production technology and perfect competition, the convex function of the marginal product of capital leads to a positive association between uncertainty and investment. Ma (2015) reports that Chinese ownership and exchange rate costs are positively associated with the investment behavior of the Australian mining industry and stimulate investment. 3 Shaoping (2008) argues that the higher the risk, the more the investment will result, thereby resulting in higher reinvestment. The aforementioned study finds a significant positive association between firm-specific uncertainty and investment for Chinese firms. Khan et al. (2019) report that Chinese firms increase their capital investment with an increase in firm-specific and market-based uncertainties. We use the preceding discussion to argue that China, as an emerging economy, faces high uncertainty. Moreover, firms show risk-taking behavior and invest substantially under high uncertainty owing to competition among firms. Therefore, we can assume that a high firm-specific uncertainty will stimulate firms’ behavior toward a high investment. Thus, we hypothesize that:

The prior literature has provided evidence that an increase in market uncertainty stimulates investment. Baum et al. (2008) show that market uncertainty induces U.S. firms’ investment. The aforementioned study argues that firms invest more in response to an increase in market uncertainty. Hence, they may have a high opportunity to expand their presence in the market. Shaoping (2008) discusses that market uncertainty enhances investment of Chinese firms. Xu et al. (2010) find positive market uncertainty and investment association. Therefore, we use the preceding discussions to argue that market uncertainty can increase the firm-specific investments of Chinese firms. Hence, we hypothesize as follows:

Although we have argued that market and firm-specific uncertainties increase investment, we assume that investments decrease because of CAPM-based uncertainty. It is because prior studies have reported that CAPM-based uncertainty negatively affects investment. Baum et al. (2008) provide evidence for the negative effect of CAPM-based uncertainty on U.S. firm’s investment. Baum et al. (2010) also report that manufacturing firms in the United States decrease their investment when the CAPM-based uncertainty increases. Dixit and Pindyck (1994) determine that uncertainty can significantly influence firms’ investment decisions, particularly in a situation where the substantial sunk cost is involved in fixed capital investments. Firms have a low likelihood to invest in an uncertain environment under irreversibility, thereby possibly increasing sunk costs. Therefore, uncertainty in the presence of irreversibility will reduce capital formation. Thus, we consider real options theory and the prior literature and argue that CAPM-based uncertainty has a negative influence on the capital investment of Chinese firms. Accordingly, we propose the following hypothesis:

We also assume that Chinese firms reduce investments when there is high policy uncertainty. Prior research has shown that policy uncertainty leads to a decline in firms’ capital investment (Baker et al., 2016; Bhattacharya et al., 2017; Gulen & Ion, 2015; Julio & Yook, 2012). Gulen and Ion (2015) find that uncertainty in policy reduces investments, and this impact is more prominent for financially constrained firms and those operating in less competitive industries. Kang et al. (2014) indicate that policy uncertainty reduces investments. Governments in developing countries significantly influence economic activities, which ultimately affect share performance, financing choices, and firm value (Firth et al., 2013). The Chinese government also intervenes in economic activities and plays a key role. When economic policy uncertainty exists, firms have no adequate information on changes in government policies. In particular, firms have no information on the main direction of industrial development in the future or which industry the government will support. In this situation, when a high policy uncertainty exists, firms bear the risk of irreversible investment in intangible assets and choose the option of waiting to invest (Bhattacharya et al., 2017). Therefore, we consider the preceding discussion and argue that economic policy uncertainty can adversely influence investment. Thus, we hypothesize that:

We expect that uncertainty plays an essential role in firms’ investment decisions operating in transition economies. Uncertainties can influence firms from many aspects and are relative shocks for the firms. However, SOEs in the transition economy have never faced demand uncertainty, and they are not affected by uncertainty in factor markets in a transition economy. Bo and Zhang (2002) find an insignificant influence of demand and supply uncertainties on investment for state enterprises of the Chinese machinery industry, whereas the investment of collective enterprises is positively affected by labor cost uncertainty. The aforementioned research finds no evidence supporting accelerator theory of investment for their sample firms. Khan et al. (2019) determine that the influence of firm-specific uncertainty is strong for non-SOEs.

Managers of SOEs are partially autonomous in making investment decisions because the contract responsibility system links many of these enterprises with the government. When high firm-specific uncertainty exists, SOEs can obtain additional resources on the basis of government ownership (Jebran et al., 2019). By contrast, non-SOEs are highly dependent on their internal resources to compete in the market. The government can provide privileges, such as subsidies, tax incentives, and favorable loan policies, to SOEs, which can mitigate the impact of uncertainty. Therefore, we expect that firm-specific uncertainty is less likely to influence SOEs than other firms. Accordingly, we hypothesize as follows:

SOEs may obtain resources and benefits from the government when a high market uncertainty exists. Wang et al. (2017) report that macroeconomic uncertainty negatively influences R&D investment for Chinese firms. The aforementioned study shows that market-based shocks have a mitigating effect on firms without political connections and has no effect on politically connected firms. Moreover, they argue that when market uncertainty is high, firms with political connections have considerable opportunities and advantages to obtain resources from the government, thereby mitigating the influence of uncertainty. However, non-SOEs are strongly affected by market uncertainty owing to minimal political connections. Therefore, the influence of market uncertainty is strong for non-SOEs. Accordingly, we hypothesize that:

Baum et al. (2008) indicate that the U.S. manufacturing firms’ investment is adversely affected by the CAPM-based uncertainty. However, they report a stimulating effect of CAPM-based uncertainty in interaction with cash flow. Given that CAPM-based uncertainty is the interaction between market and firm-related uncertainties, the previous literature has shown that non-SOEs’ investment is more influenced by firm-specific and market-based uncertainties compared with that of SOEs. Consistent with our prior arguments, we argue that the investment behavior of non-SOEs compared with that of SOEs is more influenced by CAPM-based uncertainty. Thus, we hypothesize as follows:

Government intervention is common in transition economies. The investment behavior of SOEs is “pro-policy” because of their relationship with the government. That is, when the policy aims to stimulate the economy, SOEs increase their investments and vice versa. Wang et al. (2014) show that firms lower their investments as the economic policy uncertainty increases, and this impact is comparatively strong for SOEs. Wang et al. (2017) find that the policy uncertainty impact on R&D investment is negative for Chinese firms. They further report that policy uncertainty only influences R&D of firms with political connections but has no impact on nonpolitically connected firms. Morck et al. (2013) report that compared with non-SOEs, the investment behavior of SOEs in China considerably affected by changes in economic policies. Hence, we hypothesize as follows:

We present the aforementioned hypotheses in a theoretical model, assuming that CAPM-based, market-based, firm-specific, and economic policy uncertainties affect the Chinese firms’ investment behavior, and this relationship may differ for companies of different nature of ownership and is shown in Figure 1.

Theoretical model.

Data, Variables Measurement, and Descriptive Statistics

Data

This study initially considered all A-share Chinese listed firms during the period 1999–2016. We categorized the sample into SOEs and non-SOEs to empirically test uncertainty and investment association. The financial data were obtained from the China Stock Market and Accounting Research Database (CSMAR).

We only considered all nonfinancial firms and excluded financial firms. Furthermore, we excluded the data for missing observations on control variables. We included data for companies with at least three consecutive years for accurate calculation of uncertainty and to appropriately use the endogenous variables as instruments to use a two-step robust system generalized method of moments (GMM) model. After the initial screening, the final sample comprised 17,258 observations (7,738 for SOEs and 9,520 for non-SOEs) for 1,791 firms (561 for SOEs and 1,230 for non-SOEs). All variables are winsorized at the upper and lower one-percentile to control the potential effects of outliers. 4

Variables Measurement

Measuring corporate investment (Inv)

We follow Ding et al. (2016) and An et al. (2016) and define investment as firms’ current year’s net fixed assets, minus the previous year’s net fixed assets, plus the current year’s depreciation, and scaled by the previous year’s total assets.

Measuring firm-specific uncertainty (η)

We follow prior studies (Baum et al., 2008; Shaoping, 2008) and measure the firm-specific uncertainty by estimating the variance of firms’ daily stock return for each year. The use of variance of stock returns as a measure of uncertainty is based on the presumption that stock prices contain information that correspond to firms’ underlying fundamentals. Investors perceive firms’ overall environment by the stock return. Therefore, the volatility of stock returns can be used to measure the uncertainty. 5

Measuring market-based uncertainty (ε)

We follow Wang et al. (2017) and Baum et al. (2009) and use the GARCH model to proxy for market uncertainty. Market uncertainty is measured using the conditional variance attained from the estimation of the GARCH model for the stock market return of Chinese publicly traded firms.

Measuring CAPM-based uncertainty (ν)

To quantify the CAPM-based uncertainty, we follow prior studies (Baum et al., 2010; Leahy & Whitcd, 1996) and estimate the risk of an individual firm by using the covariance between firms’ daily stock returns and the value-weighted index of the Shanghai Stock Exchange (SSE)/The Shenzhen Stock Exchange (SZSE).

Measuring economic policy uncertainty (epu)

Baker et al. (2016) develop an index (i.e., BBD index) to measure the economic policy uncertainty for the United States. Their index for economic policy uncertainty has been used in many studies and found to be a suitable proxy for the real economic policy uncertainty (Bloom et al., 2018; Dibiasi et al., 2018; Leduc & Liu, 2016). Following the same methodology, they constructed epu indices for other countries, which include Canada, Australia, Europe, India, and China. 6 The current study also opts for this index as a proxy for economic policy uncertainty.

Descriptive Statistics

Table 1 reports the descriptive statistics for the full sample, SOEs, and non-SOEs. The mean (median) value of investment for the full sample is 6.63% (3.46%). We observe from the mean value of investment of SOEs (non-SOEs) approximately 7.21% (6.16%). This result suggests that SOEs invest more than non-SOEs possibly because the former is supported by the government. For the uncertainty measures, we find a significant difference among the mean values of market uncertainty, firm-specific uncertainty, and economic policy uncertainty for SOEs and non-SOEs in the sample period. Compared with non-SOEs, SOEs have high average values and high variation for firm-specific and market uncertainty. For other uncertainties, we obtain high mean values and high variabilities for non-SOEs. These figures indicate different levels of uncertainties for both types of firms, even within the same industry.

Descriptive Statistics.

Note. This table presents the descriptive statistics and the estimates for the mean-difference test. Inv = investment; η = firm-specific uncertainty; ε = market-based uncertainty; ν = CAPM-based uncertainty; epu = economic policy uncertainty; Cf = cash flow ratio; Lev = leverage, Tobin’s Q ratio; Sg = sales growth; Size = firm size; SOEs = state-owned enterprises.

Significance level at 1% and 5% are represented by *** and **, respectively.

We further perform t-test to examine the significant differences between SOEs and non-SOEs. The estimates for the t-test are reported in Table 1, which shows that the t-statistics are significant for all variables (except cash flow and sales growth). These findings suggest that the statistics of our main variables (e.g., investment and various uncertainties) significantly vary across SOEs and non-SOEs.

Econometric Model

Baseline Model

We use the following regression equation to examine the association between different forms of uncertainty and investment:

where i denotes firm, t denotes time, and Inv is the investment. We include the first lagged investment in our model because it significantly affects the current investment (Bloom et al., 2007). Moreover, η, ε, ν, and epu represent the firm-specific, market-based, CAPM-based, and economic policy uncertainties, respectively. Cf represents the cash flow ratio, computed as the ratio of net profits and depreciation to total assets (Cleary, 2005; Lima Crisóstomo et al., 2014; Phan, 2018). Lev denotes the leverage of a firm, measured as the ratio of total liabilities to total assets (Bai et al., 2014; Chow et al., 2018). Tobin’s Q is the ratio of the sum of the market value of equity and total liabilities to lagged total assets (Wang et al., 2017). Sg stands for the growth of sales measured as the log of the first difference of total sales during a year (Pukthuanthong et al., 2013; Rashid & Saeed, 2017). Size denotes firms’ size in terms of total assets (Bai et al., 2014; Chow et al., 2018). fi and ft represent the industry and time fixed-effect, respectively. Finally,

Differential Effects of Uncertainty on Investment for SOEs and Non-SOEs

We divide the full sample into SOEs and non-SOEs. Out of 1,791 firms, 561 are SOEs and 1,230 are non-SOEs. Thereafter, we estimate separate models for both groups to examine whether the impact of different types of uncertainties on the investment behavior of SOEs is statistically different from that of non-SOEs. We estimate Equation 1 separately for SOEs and non-SOEs.

Indirect Effects of Uncertainty Through Cash Flow on Investment for SOEs and Non-SOEs

Baum et al. (2010) empirically examine the link among uncertainty, investment behavior, and cash flow of manufacturing firms in the United States. A high level of cash flow can stimulate or mitigate the investment activities of firms. Given that the investment opportunities of a firm depend on its financial condition and level of cash flow generated, the uncertainty will have an indirect effect through cash flow, in addition to its direct impact on firms’ investment. This section empirically investigates the effects of various forms of uncertainties on their own and in interaction with cash flow on the investment of SOEs and non-SOEs. We include the interactions of cash flow with uncertainty measures as follows:

We examine the indirect effects of firm-specific, market-based, CAPM-based, and economic policy uncertainties on the investment of SOEs and non-SOEs by investigating the significance of β4, β6, β8, and β10, respectively. The significance level of these coefficients shows that different forms of uncertainties affect firms’ investment with the change in the level of firms’ cash flow.

Estimation Technique

To estimate the preceding models, we use the dynamic panel data (DPD) approach to control the problem of endogeneity. Given that we jointly determine firms’ investment decision with cash flow and leverage, reverse causality is likely to occur because investment may also affect the leverage and cash flow of firms or the uncertainty, thereby possibly affecting firms’ leverage and cash flow. Therefore, we use a two-step robust system GMM technique to minimize endogeneity issues and consider the panel nature of our data (Arellano & Bover, 1995; Blundell & Bond, 1998; Roodman, 2006). To control for the industry and time effects, the system GMM technique enables us to combine the level equation of variable with the equation in differences of variables as we use the lags of variables and the lags of first difference as instruments. We include time and industry dummies in all estimations and use them as additional instruments.

Empirical Findings

Baseline Model

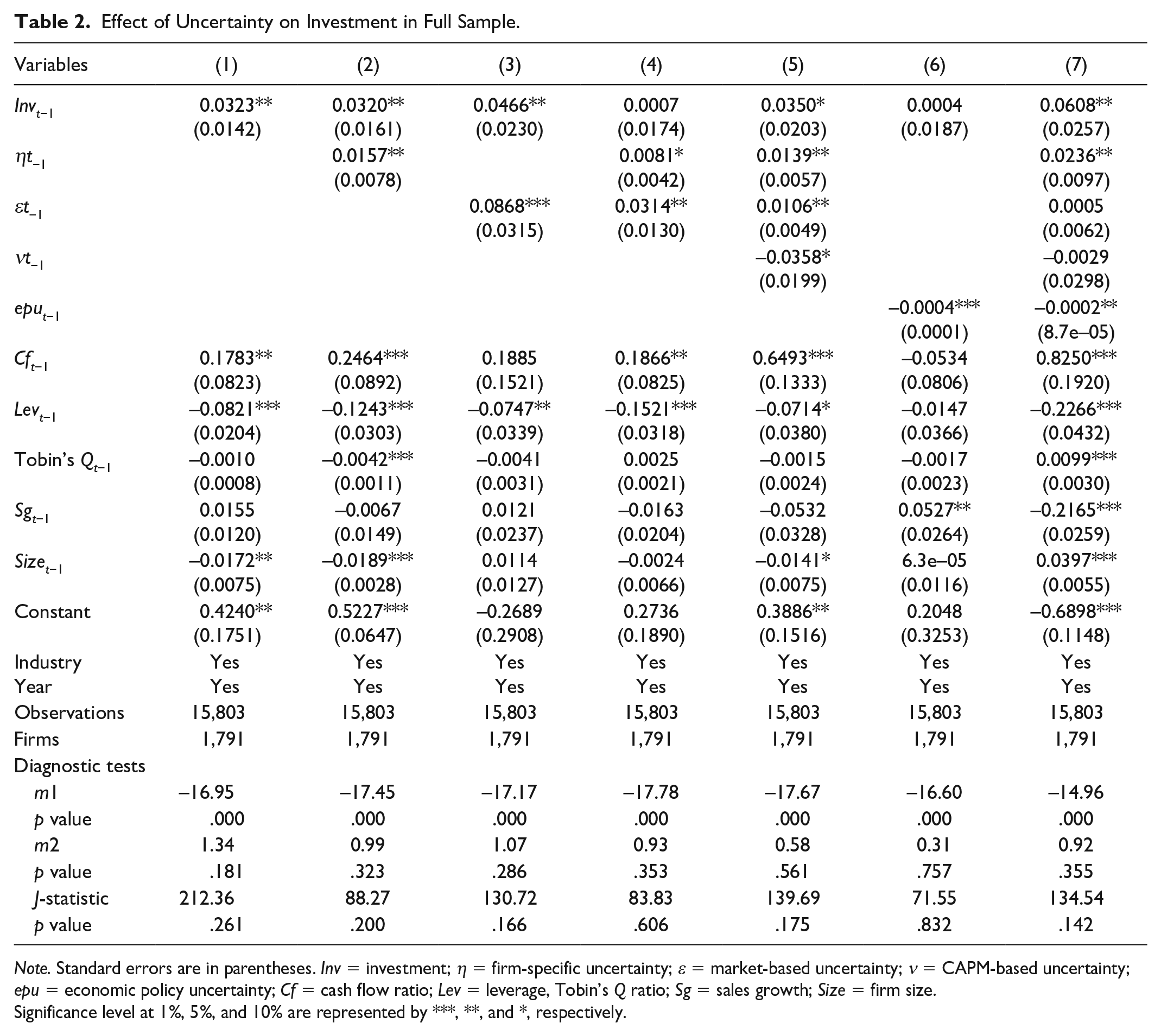

Table 2 presents the regression results for the baseline model (Equation 1). Column (1) reports the standard investment model, which includes the lagged dependent variable (Invit−1) and control variables. The coefficients for the lagged investment and cash flow are significantly positive, which is consistent with Baum et al. (2010), Gulen and Ion (2015), and Julio and Yook (2012). Consistent with the literature (Ma, 2015; Wang et al., 2017), we find an adverse and highly significant effect of leverage and firm size on investment. Moreover, the coefficients for Tobin’s Q and Sg are not statistically different from zero. Therefore, we find no evidence in support to the accelerator theory of investment, which corroborates with Baum et al. (2010) and Bo and Zhang (2002). Furthermore, diagnostic tests are provided at the end of each table. We apply the Arellano and Bond (1991) test under the null hypothesis that there is no serial correlation among the residuals. Moreover, m1 and m2 stand for the first- and second-ordered serial correlations, respectively. We reject (accept) the null hypothesis for m1 (m2). The J-statistic is the Hansen test of overidentifying restrictions, showing the validity of instruments used in the estimations. By considering the brevity, we did not explain these tests in the discussion.

Effect of Uncertainty on Investment in Full Sample.

Note. Standard errors are in parentheses. Inv = investment; η = firm-specific uncertainty; ε = market-based uncertainty; ν = CAPM-based uncertainty; epu = economic policy uncertainty; Cf = cash flow ratio; Lev = leverage, Tobin’s Q ratio; Sg = sales growth; Size = firm size.

Significance level at 1%, 5%, and 10% are represented by ***, **, and *, respectively.

Columns (2) and (3) show that firm-specific and market-based uncertainties significantly positively affect investment (uncertainty coefficients are statistically significant at 5% and 1%, respectively). These results corroborate the assumptions of Hartman (1972) and Caballero (1991) and the prior literature (Shaoping, 2008; Xu et al., 2010), which argued that more the risk, the more the investment and therefore, higher reinvestment. Thus, Hypotheses 1 and 2 are supported.

In Column (4), we include firm-specific and market-based uncertainties in the same equation. Although the coefficients for both forms of uncertainties have decreased, they continue to show the same statistically significant and stimulating impact on investment.

Column (5) shows that the coefficient of firm-specific uncertainty has increased again, whereas the coefficient of market uncertainty has decreased substantially. Both types of uncertainties have the same positive and significant effect. However, we can observe the negative influence of CAPM-based uncertainty on firms’ investment. This result supports real options theory. Hence, Hypothesis 3 is supported.

In Column (6), we find that economic policy uncertainty reduces investment. This result is consistent with Wang et al. (2014) and Kang et al. (2014) and supports theory of irreversible investment and the option value of waiting to invest (Bernanke, 1983; Dixit & Pindyck, 1994). Thus, Hypothesis 4 is confirmed.

In the last column of Table 2, we combine all forms of uncertainties in our investment model and find that the coefficient of firm-specific uncertainty has increased and remains significant at 5%. This result suggests that firms’ investment increases with an increase in firm-specific uncertainty. The signs of market-based and CAPM-based uncertainties remain the same. However, their coefficients are not statistically significant. The coefficient of economic policy uncertainty has decreased in absolute value but remains negative and statistically significant at 5%. This result supports the claim that Chinese manufacturing firms decrease their investment when epu increases.

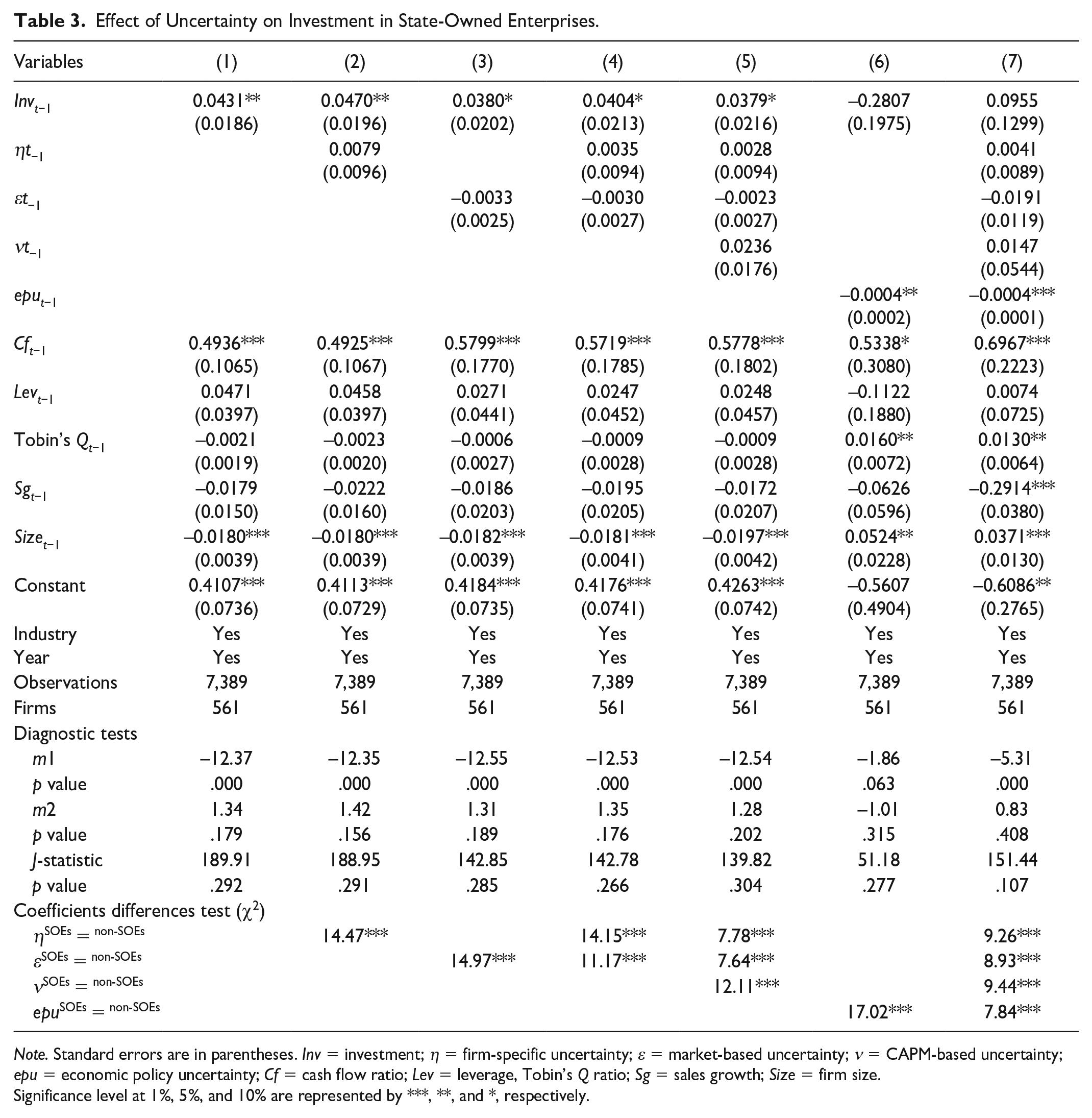

Differential Effects of Uncertainty on Investment for SOEs and Non-SOEs

Tables 3 reports the results of the uncertainties and investment association for SOEs. Column (1) presents similar results to those in Table 2 in terms of signs and significance levels for the lagged investment and control variables. The exception is leverage, which is not different from zero. Columns (2) and (3) show no significant effect of firm-specific and market-based uncertainties on corporate investment, respectively. The coefficients of firm-specific and market-based uncertainties remain statistically insignificant if we combine them in Columns (4) and (5), along with the CAPM-based uncertainty. The results indicate that managers of SOEs have no incentives to react to uncertainty, which may be caused by the contract responsibility system between firms and the government. Column (6) shows that economic policy uncertainty reduces SOEs’ investments. Column (7) shows no significant change in terms of the sign and significance level of uncertainties, thereby indicating that except economic policy uncertainty, no other forms of uncertainty influence SOEs’ investment.

Effect of Uncertainty on Investment in State-Owned Enterprises.

Note. Standard errors are in parentheses. Inv = investment; η = firm-specific uncertainty; ε = market-based uncertainty; ν = CAPM-based uncertainty; epu = economic policy uncertainty; Cf = cash flow ratio; Lev = leverage, Tobin’s Q ratio; Sg = sales growth; Size = firm size.

Significance level at 1%, 5%, and 10% are represented by ***, **, and *, respectively.

Thereafter, we apply the Chow test to investigate the statistical difference in the coefficients of uncertainties across SOEs and non-SOEs. The results reported in Table 3 show significant chi-square values for all uncertainty coefficients. The findings confirm that the coefficients of uncertainties across SOEs and non-SOEs significantly vary.

Table 4 presents the findings for non-SOEs. The results in Column (1) are consistent with the full sample. Furthermore, Columns (2) and (3) show that firm-specific and market-based uncertainties positively affect investment. From these results, we can infer that non-SOEs’ investment behavior appears to be risk-taking by investing substantially in a high degree of uncertainty. These findings support Hypotheses 5a and 5b. The coefficient of firm-specific uncertainty becomes insignificant when we combine both forms of uncertainties in Column (4), and with CAPM-based uncertainty in Column (5). These coefficients indicate that firm-specific uncertainty has no significant impact on non-SOEs’ investment, whereas market-based uncertainty has a stimulative impact, with a negative effect of CAPM-based uncertainty. This result supports Hypothesis 5c. When comparing the results of Column (6) in Table 4 with those of Table 3, we determine that both types of firms are negatively influenced by economic policy uncertainty. However, the coefficient is considerably low in absolute value for non-SOEs, thereby indicating that the investment behavior of non-SOEs is minimally influenced by economic policy uncertainty. Our findings corroborate those of Wang et al. (2014) and Wang et al. (2017) and support the theory of irreversible investment. This result verifies Hypothesis 5d. In Column (7), we find that the coefficient of epu is the same in sign and value, whereas the coefficients of all other forms of uncertainties become statistically insignificant. These findings show that when non-SOEs face epu, their risk-taking behavior changes, thereby resulting in a reduction of their investment in uncertain environments.

Effect of Uncertainty on Investment in Non-State-Owned Enterprises.

Note. Standard errors are in parentheses. Inv = investment; η = firm-specific uncertainty; ε = market-based uncertainty; ν = CAPM-based uncertainty; epu = economic policy uncertainty; Cf = cash flow ratio; Lev = leverage, Tobin’s Q ratio; Sg = sales growth; Size = firm size.

Significance level at 1%, 5%, and 10% are represented by ***, **, and *, respectively.

Indirect Effects of Uncertainty: Does Uncertainty Affect the Firm’s Investment Through Cash Flow?

Table 3 shows that cash flow has a significantly positive coefficient, whereas all forms of uncertainties, except for economic policy uncertainty, have no significant effects on SOEs’ investment. We likewise consider cash flow in isolation only and not in interaction with uncertainties terms. Table 5 presents the estimates for Equation 2 by adding an interaction term of cash flow with each form of uncertainty. Column (1) shows an insignificant coefficient of firm-specific uncertainty in isolation, while it has an exacerbating influence with cash flow interaction. This result indicates that cash flow enhances the association between investment and firm-specific uncertainty.

Indirect Effect of Uncertainty Through Cash Flow on Investment in State-Owned Enterprises.

Note. Standard errors are in parentheses. Inv = investment; η = firm-specific uncertainty; ε = market-based uncertainty; ν = CAPM-based uncertainty; epu = economic policy uncertainty; Cf = cash flow ratio; Lev = leverage, Tobin’s Q ratio; Sg = sales growth; Size = firm size.

Significance level at 1%, 5%, and 10% are represented by ***, **, and *, respectively.

Column (2) presents the findings for market-based uncertainty and its interaction term. The coefficient of market-based uncertainty is insignificant, while the interaction term appears to have a significant negative influence on investment. The results show that cash flow can decrease the effect of market-based uncertainty on investment. This may suggest that managers of SOEs are considerably cautious in highly uncertain market, as pointed out by prior studies, such as Bloom et al. (2007) and Baum et al. (2010).

The signs and significance of the market- and firm-specific uncertainties, along with their interactions, remain unchanged when we combine them in Column (3). However, the coefficients of CAPM-based uncertainty and interaction of the CAPM-based uncertainty in Column (4) are not significantly different from zero. These results are consistent with the findings in Table 3 and suggest that market, CAPM, and firm-specific uncertainties (in isolation) have no meaningful impact on SOEs’ investment. This result may be caused by the contract responsibility system, and managers of SOEs do not show risk-taking behavior in making decisions to invest.

In Column (5), we determine that economic policy uncertainty reduces SOEs’ investment. However, the coefficient of the interaction term is significantly positive, which implies that cash flow mitigates the influence of economic policy uncertainty. These findings are consistent with those of Wang et al. (2014).

Column (6) provides the results for the combined impact of uncertainties and their interaction with cash flow. The signs and significance remains the same for economic policy uncertainty and its interaction term, whereas all other forms of uncertainties and interactions become insignificant.

Table 6 presents the indirect effect of various forms of uncertainties through cash flow on non-SOEs’ investment behavior. Column (1) shows the exacerbating and significant effect of the firm-specific uncertainty and cash flow in isolation, with no meaningful interaction term. Column (2) presents the significant coefficients of market-based uncertainty and its interaction with cash flow. The negative coefficient for the interaction term implies that cash flow weakens the impact of market-based uncertainty. The signs and significance of the market-based uncertainty and its interaction term remain unchanged in Column (3), while the coefficients of firm-specific uncertainty and its interaction term are not statistically significant. In Column (4), we include the CAPM-based uncertainty and its interaction with cash flow. The main effect is significantly negative, whereas the interaction term coefficient was significantly positive, thereby implying that cash flow weakens the effect of the CAPM-based uncertainty. However, the positive effects of market and firm-related uncertainties remain consistent, whereas their interaction terms lack significance. Column (5) shows that non-SOEs’ investment is not influenced by economic policy uncertainty in isolation or through cash flow. Column (6) presents the combined impact of all uncertainties and their interaction terms. Firm-specific uncertainty has a significant positive impact, with no meaningful interaction term. The signs and significance of the CAPM-based uncertainty and its interaction remain unchanged. However, results show that non-SOEs’ investment is not influenced by economic policy uncertainty and market-based uncertainty in isolation or through cash flow.

Indirect Effect of Uncertainty Through Cash Flow on Investment in Non-State-Owned Enterprises.

Note. Standard errors are in parentheses. Inv = investment; η = firm-specific uncertainty; ε = market-based uncertainty; ν = CAPM-based uncertainty; epu = economic policy uncertainty; Cf = cash flow ratio; Lev = leverage, Tobin’s Q ratio; Sg = sales growth; Size = firm size.

Significance level at 1%, 5%, and 10% are represented by ***, **, and *, respectively.

Robustness Tests

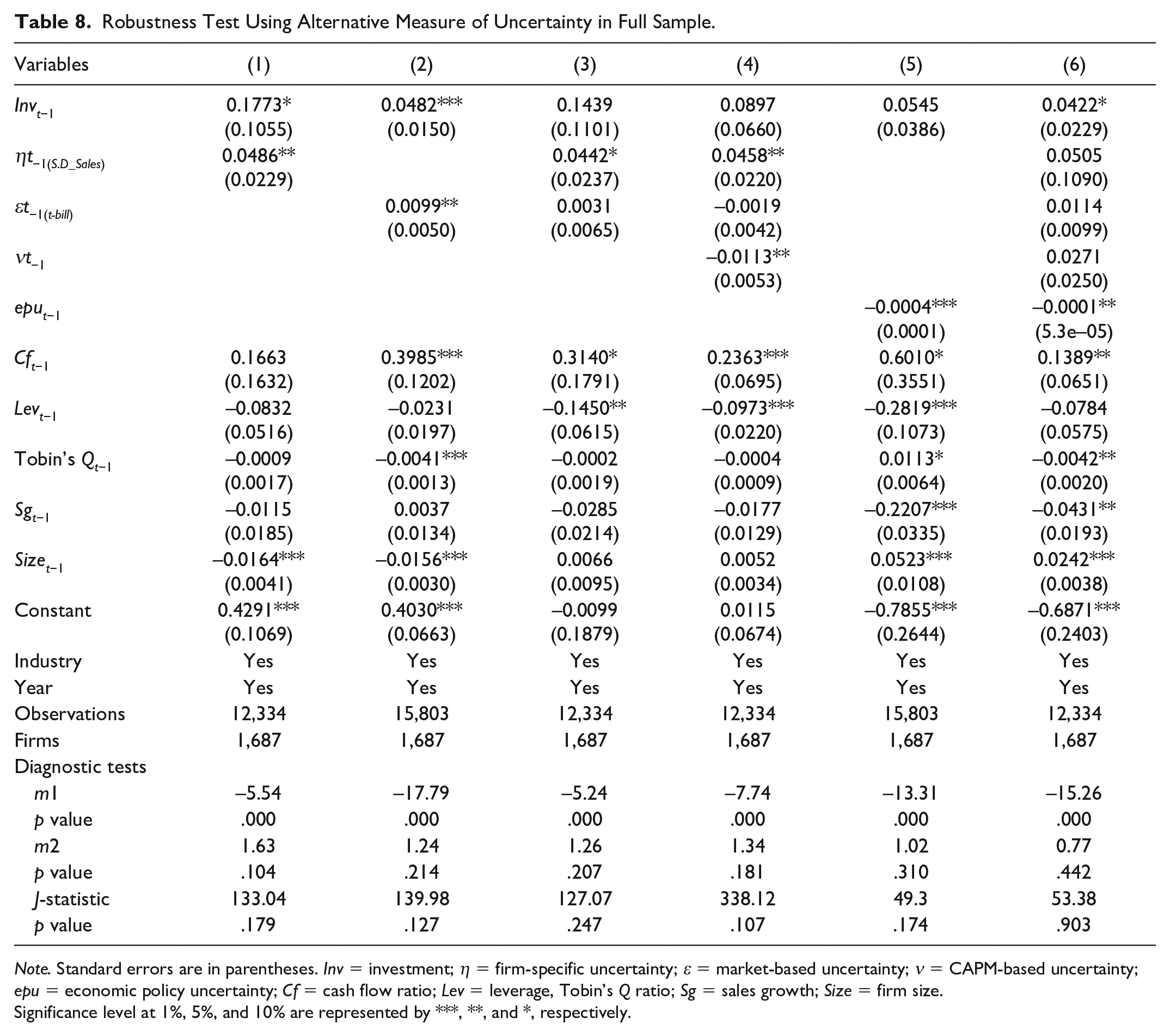

We conducted several robustness checks for the validity of our results. First, we use an additional measure of investment, 7 which is defined as the ratio of expenditures on the purchase of fixed tangible assets during a year to total assets. Table 7 presents the results. We obtain consistent results in terms of sign and significance for coefficients of variables to those reported in Table 2.

Robustness Check Using Alternative Measure of Investment in Full Sample.

Note. Standard errors are in parentheses. Inv = investment; η = firm-specific uncertainty; ε = market-based uncertainty; ν = CAPM-based uncertainty; epu = economic policy uncertainty; Cf = cash flow ratio; Lev = leverage, Tobin’s Q ratio; Sg = sales growth; Size = firm size.

Significance level at 1%, 5%, and 10% are represented by ***, **, and *, respectively.

Second, we use an alternative measure for firm-specific uncertainty (Equation 3), which is defined as the first-order autoregressive model AR(1) for total sales normalized by capital stock for each firm (Baum et al., 2016; Bo & Zhang, 2002; Caglayan & Rashid, 2014):

The uncertainty proxy for each year is measured by calculating the moving standard deviation of the residuals obtained from the estimation of the AR(1) model of the total sales in a five-period rolling window with a minimum of 3 years of residual data. 8 Our findings reported in Table 8 remain consistent with those presented in Table 2.

Robustness Test Using Alternative Measure of Uncertainty in Full Sample.

Note. Standard errors are in parentheses. Inv = investment; η = firm-specific uncertainty; ε = market-based uncertainty; ν = CAPM-based uncertainty; epu = economic policy uncertainty; Cf = cash flow ratio; Lev = leverage, Tobin’s Q ratio; Sg = sales growth; Size = firm size.

Significance level at 1%, 5%, and 10% are represented by ***, **, and *, respectively.

Finally, we follow Caglayan and Rashid (2014) and Rashid (2011) and estimate the GARCH model by using the annual data of the T-bills rate for the period 1997–2016 to measure market uncertainty. Our findings in Table 8 provide consistent results to our prior findings. Overall, the results of these sections suggest that our main results are insensitive to alternative measures of investment and uncertainties.

Conclusion

This study investigates the impact of the four forms of uncertainties on corporate investment, using an unbalanced panel data of 1,791 firms listed on the SSE/SZSE for the period of 1999–2016. This study further tests whether the impact of uncertainty on investment varies across SOEs and non-SOEs. Furthermore, the current research investigated the influence of cash flow on the uncertainty–investment relationship. By controlling for the time and industry-fixed effects and considering the potential endogeneity problem, this study uses a robust two-step system GMM technique to estimate the model.

The empirical findings indicate that market- and firm-specific uncertainties (economic policy and CAPM-based uncertainties) have a positive (negative) effect on corporate investment. The findings further indicate that the investment decisions undertaken by SOEs do not respond to market-based, CAPM-based, and firm-specific uncertainties. By contrast, non-SOEs respond to market-based and firm-specific uncertainties (CAPM-based uncertainty) positively (negatively). The results provide evidence that economic policy uncertainty has a negative impact on firms’ investment. Moreover, the investment behavior of SOEs is more sensitive to economic policy uncertainty than that of non-SOEs. Furthermore, the results show that the influence of cash flow on investment can be exacerbating or mitigating, depending on the underlying uncertainty. In particular, the cash flow exacerbates the impact of firm-specific uncertainty on SOEs’ investment and mitigates the adverse effect of CAPM-based uncertainty (economic policy uncertainty) on investment of non-SOEs (SOEs). Moreover, cash flow attenuates the effects of market uncertainty on investment of SOEs and non-SOEs. Thus, the findings signify that cash flow is an important factor that influences the uncertainty–investment association. Our results remain robust, considering the potential endogeneity problems, and alternative proxies for investment, firm-specific, and market-based uncertainties.

The findings would help firm managers, investors, and policymakers to understand the uncertainty–investment association in a transition economy, such as China. The results of this study facilitate an improved understanding of how different kinds of uncertainties affect the investment behavior of Chinese SOEs and non-SOEs. Given that China is moving from a command-based to a market-based economy, firms face substantial policy uncertainty, which negatively affects their investment behavior. Therefore, firms can be encouraged to invest more by a significant reduction in policy uncertainty. Furthermore, a substantial cash flow can mitigate the negative impact of CAPM-based and economic policy uncertainties.

The findings of this study are beneficial and informative with regard to the understanding of uncertainty–investment relationship, and the role of cash flow in mitigating the negative effect of uncertainty. Investors should consider the results of this study when making future investment decisions because the Chinese market is continuously and rapidly expanding and efficient investment decisions are important in a dynamic market.

Footnotes

Acknowledgements

We are thankful to the editor and anonymous reviewers for many constructive comments and suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is supported by the National Natural Science Foundation of China (Grant Nos 71871040, 71471026, 71731003) and Basic Scientific Research Operating Expenses of Central Universities of China (Grant No. DUT17RW210).