Abstract

This study investigates the sentiment effect in the Chinese agricultural futures market by constructing market-level and future-level futures sentiment indices. First, our findings reveal that sentiment in futures and the domestic stock market has a significant and positive impact on future-level sentiment, especially during bull markets, whereas sentiment in the global stock market has minimal influence. Second, an analysis of the relationship between sentiment and futures returns indicates that sentiment, both at the market and future levels, strongly and favorably influences the movement of futures returns. Third, after decomposing the future-level sentiment into contagious sentiment and idiosyncratic sentiment, this paper concludes that contagious sentiment and idiosyncratic sentiment positively affect futures returns in both bull and bear markets. Overall, this research provides clear evidence that sentiment plays a crucial role in determining agricultural futures returns and offers guidance to regulators to identify potential market bubbles and implement “sentiment regulation.”

Plain language summary

We construct market-level and future-level futures sentiment to examine the sentiment effect in the Chinese agricultural futures market. First, this study finds that sentiment in futures and the domestic stock market has a large and favorable impact on future-level sentiment, particularly during bull markets. However, sentiment in the global stock market has little bearing on futures sentiment. Second, an analysis of the correlation between sentiment and futures returns indicates that sentiment, both at the market and future levels, strongly and favorably influences the movement of futures returns. Third, after decomposing the future-level sentiment into contagious sentiment and idiosyncratic sentiment, this paper concludes that contagious sentiment and idiosyncratic sentiment positively affect futures returns in both bull and bear markets. This paper provides clear evidence that sentiment affects agricultural futures returns, and offers guidance to regulators to identify potential market bubbles, and implement “sentiment regulation”.

Introduction

Since the early 2000s, commodity futures prices have exhibited an increasing correlation with commodity prices, coinciding with a surge in index investment in commodity markets. Research has demonstrated a link between the excessive co-movement of commodity prices and the heightened financial impact on these markets (Le Pen & Sévi, 2017). The financialization of the commodity markets is partially responsible for the notable increase in price volatility of the commodities futures (Tang & Xiong, 2012). Established in 1988, China’s futures market has seen fast expansion. The China Futures Association disclosed that in 2023, there was a notable spike in transaction volume, marking a 25.6% increase from last year, to reach an impressive 8.5 billion lots. Simultaneously, China’s futures market saw a 6.28% year-over-year increase in trade turnover, amounting to a massive 568.51 trillion yuan (about 80 trillion U.S. dollars). The increase in turnover reflects the robust activity in the Chinese futures market, symbolizing the market’s growing importance and impact on world financial developments. Chinese Future Exchanges are one of the world’s fastest-growing futures markets, with most of its transactions coming from domestic retail investors. In contrast to mature, developed futures markets dominated by financial institutional investors, the Chinese market is perceived as highly speculative.

This paper focuses on the agricultural futures market in China. Relevant research indicates that agricultural futures are influenced by other asset markets (Andersson et al., 2016; Kang et al., 2017; López Cabrera & Schulz, 2016), financial speculation (Andersson et al., 2016; Sanders et al., 2010), and macroeconomic news (Caporale et al., 2017). Investor sentiment, which represents the inclination to speculate, has an impact on asset prices (Baker & Wurgler, 2006). Strong evidence is provided by empirical research to support the various roles that trading behavior plays in influencing agricultural future price movements. According to Bohl et al. (2018), the volatility of conditional returns is positively impacted by the speculation ratio. Zhou et al. (2019) illustrate how investors buy and sell through agricultural price fluctuations.

Hence, the goal of the paper is to shed some light on the sentiment impact on the agricultural futures market in China. On the one hand, this paper examines the factors affecting future-level sentiment, testing the role of market-level futures sentiment and stock market sentiment. On the other hand, after decomposing the future-level sentiment, this paper examines the impact of market sentiment, contagious sentiment, and idiosyncratic sentiment on futures returns. Additionally, the paper innovatively explores these mechanisms in both bull and bear markets.

Literature Review and Hypothesis Development

Behavioral finance theory suggests that different investors, assets, and markets may exhibit varying attitudes toward investing (Baker et al., 2012; Da et al., 2023; Ding et al., 2017; Y. Li & Ran, 2020). Zhou and Huang (2020) examined the influence of sentiment contagion at the future level on Chinese agricultural futures markets, revealing that agricultural futures prices are driven by contagious future-level sentiment. Furthermore, empirical research strongly supports the role of trading behavior in shaping agricultural futures price movements. This paper investigates the sentiment effect in the agricultural futures market and posits that sentiment has a significant impact on Chinese agricultural futures markets, where speculation is particularly prevalent.

Based on Baker and Wurgler (2006), this paper constructs future-level sentiment for sixteen significant agricultural futures and market-level sentiment in China’s agricultural futures market using principal component analysis (PCA). To the best of our knowledge, distinguishing between bull and bear markets in the Chinese agricultural futures market and examining the effect of market-level futures sentiment on future-level sentiment is a unique experiment. We infer that market sentiment in the agricultural futures market has a significant and favorable impact on the future-level sentiment. We thus hypothesize and test the following:

Next, this paper examines the relationship between sentiment and futures returns. Higher market sentiment will boost investor enthusiasm, which in turn will drive movements in futures returns; therefore, we infer that market sentiment has a positive impact on futures returns. On the other side, future-level sentiment is categorized into two types of sentiment—contagious and idiosyncratic—with reference to Baker et al. (2012) and Zhou and Huang (2020) to examine the impact of contagious sentiment and idiosyncratic sentiment on futures returns. This paper examines the impact of contagious sentiment and idiosyncratic sentiment using agricultural futures. We infer that both contagious sentiment and idiosyncratic sentiment will significantly affect the movement of futures returns, and idiosyncratic sentiment related to the future itself will have a greater impact. By adding more control variables, this paper strengthened the findings by citing Zhou and Huang (2020) and Fang et al. (2023). This section continues to differentiate between bull and bear markets and looks at how sentiment affects futures returns. Hence, the following assumptions are tested:

In addition to the constraints imposed by agricultural policy, market structure, and technological capability, the development of the Chinese agricultural futures market has also been impacted by changes in the equity market. There is ample evidence to support the link between the equity and futures markets (A. D. Ahmed & Huo, 2021; M. Y. Ahmed & Sarkodie, 2021; Cao & Xie, 2023; Wang et al., 2023). Recent trends indicate that the stock market has a dominating role in determining the volatility of the futures market (J. Li et al., 2023). According to Zhang et al. (2024), there is a granger cause for each other between the composite stock price index of listed agricultural companies and the composite price index of grain futures. Despite the fact that the correlation between futures and the stock market has been widely confirmed (Badamvaanchig et al., 2021; B. Chen et al., 2024; Evrim Mandacı et al., 2020; Jiang et al., 2021; Rehman et al., 2023), a few studies have discussed the sentiment connection between the stock market and the agricultural futures market. Considering the distinct roles played by global and local sentiment, as well as the fact that sentiment fluctuates across different stock markets globally (Baker et al., 2012; Y. Li & Ran, 2020). We hypothesize that domestic equity market sentiment has been influenced by global equity market sentiment. As a result, domestic stock sentiment will be more influential than global stock sentiment when analyzing the relationship between stock market sentiment and futures market sentiment. The following hypotheses and tests are thus conducted:

Existing studies examining the relationship between investor sentiment and the agricultural futures market currently have the following shortcomings. On the one hand, the relationship between stock market sentiment and futures markets has not been investigated. Furthermore, previous studies have not paid much attention to varying degrees of sentiment in the futures market. Second, research on investor sentiment does not provide a thorough analysis of the market since it does not distinguish between bull and bear markets. This paper divides the market into bull and bear markets, to understand more about investor sentiment across time (R. Chen et al., 2022). We further explore sentiment by examining the relationship between market-level sentiment and future-level sentiment in both bull and bear markets, as well as the impact of contagious and idiosyncratic sentiment on future returns.

To test the above hypotheses, this paper has done a series of empirical analyses, and the results are as follows. First, this paper reveals that, particularly during bull markets, sentiment in agricultural futures markets and the domestic stock market has a considerable and positive impact on future-level sentiment. However, futures sentiment is not much impacted by sentiment in the global stock market. Second, sentiment at both the market and future levels strongly and favorably influences the movement of futures returns, with contagious sentiment and idiosyncratic sentiment favorably influencing returns, according to an analysis of the relationship between sentiment and futures returns. Furthermore, in bull markets, the effects of contagious sentiment and idiosyncratic sentiment are more pronounced. Third, the market sentiment still has a significant impact on futures returns even in the presence of other macro factors.

This paper offers the following contributions: firstly, it examines the impact of stock market sentiment while analyzing the correlation between market-level sentiment and future-level sentiment. The results indicate that future-level sentiment is not significantly affected by global stock market sentiment; instead, it is profoundly and positively influenced by market-level sentiment and domestic stock market sentiment.

Secondly, this paper reveals that sentiment, at both the market and future levels, exerts a significant and positive influence on future returns. Additionally, it demonstrates that contagious sentiment and idiosyncratic sentiment also have a favorable impact on futures returns.

Thirdly, this paper pioneers the categorization of agricultural futures markets into bull and bear markets. It subsequently investigates how market-level sentiment affects future-level sentiment during various stages, as well as the influence of contagious and idiosyncratic sentiment on futures returns. This study offers a comprehensive analysis of how futures and stock market sentiment impact futures return across different market phases, filling a gap in the existing literature.

The structure of this paper is organized as follows: Section “Data” presents the data utilized in our empirical investigation. Section “Market-level and Future-level Sentiment in Agricultural Futures Markets” examines the relationship between market-level and future-level sentiment. In Section “Sentiment and Agricultural Futures Return,” we provide a comprehensive discussion on the impact of contagious sentiment and idiosyncratic sentiment on agricultural futures returns. Section “Further Research” includes various robustness tests to validate our findings. Finally, Section “Conclusion” concludes the paper.

Data

Summary Statistics of Related Variables

Data collected from the Wind database between January 2003 and October 2023 about China’s agriculture futures market is adopted in this paper. Sixteen futures prices, including Soybean I, Soybean II, Soybean oil, Soybean Meal, Palm oil, Sugar, Corn, Cotton, Egg, Live pigs, Polished round-grained rice, Plywood, Fiberboard, Chinese jujube, Japonica rice, Peanut kernels, are used in this analysis from Chinese agricultural futures markets. The data includes the prices, open interest, and trading volume of agricultural futures in addition to other significant macroeconomic variables. It also includes the consumer price index, the producer price index, the monthly return of the CSI 300 index, the exchange rate, the agricultural price index, M2, and the overnight SHIBOR. This article looks at how the Chinese agricultural futures market has evolved over the past 20 years. Provided below is a comprehensive description of the data. Table 1 displays basic univariate statistics for the important variables in our approach.

Descriptive Statistics.

Note. The mean, standard deviation, minimum, median, maximum, skewness, and kurtosis of the variables are displayed in Table 1.

Definition of Sentiment Indices

For estimating futures and stock markets’ sentiment, this paper builds on Baker and Wurgler’s (2006) strategy. This paper employs several sentiment proxies, each of which combines sentiment and non-sentiment-related idiosyncratic variance. This paper captures the first principal component of sentimental proxies to measure the sentiment at the market and future levels in Chinese agricultural futures markets. This is because the composite sentiment index can better capture investor irrationality and is more comprehensive than the single sentiment indicator. To measure sentiment at the market and future levels for each agricultural future, we obtain the turnover rate (Trading volume/Open interest) of agricultural futures, the psychological line index (PSY), the relative strength index (RSI), and from the Wind database (R. Chen et al., 2021; Zhou & Huang, 2020). In the following, the construction of variables is described.

The main indicator used to measure the sentiment of the futures market is the turnover rate, which is calculated as trading volume divided by open interest (R. Chen et al., 2021; Fang et al., 2023; Zhou & Huang, 2020). On the one hand, trading volume is utilized by Uygur and Taş (2012), Deeney et al. (2015), and R. Chen and Xu (2019) to assess market sentiment. Since trade volume gives a more realistic image of how investors feel about the swings in the value of risky assets, it is a useful indicator for studying investor trading behavior. When market trading volume increases, people are more inclined to buy riskier assets, which implies that investors are feeling more optimistic. Thus, trade volume is one direct measure of market activity. On the other hand, open interest was first presented by Wang (2001) and is a commonly used measure of investor sentiment in futures markets. Numerous research has suggested that it might properly portray investors’ activity in the futures market, such as Bahloul and Bouri (2016), Zhou and Huang (2020), and R. Chen et al. (2021). An increase in open interests in the futures market indicates that investors are growing more interested in this contract and are feeling more optimistic about investing since both long and short sides are opening positions. The turnover rate is the first indicator used to construct the sentiment indicator.

A sentiment proxy called the psychological line index (PSY) is used to measure investor psychological wave movements during financial market ups and downs (Sadaqat & Butt, 2016; Yang & Zhou, 2015, 2016; Zhou & Huang, 2020). In order to determine the prevailing market direction, the PSY is often used as a technical indicator in practice. It can provide accurate guidance for making decisions when determining the direction of the financial market trend in a short amount of time.

Used as a popular market indicator, the relative strength index (RSI) can reflect if the futures market is overbought or oversold. Previous studies, such as Hudson and Green (2015), Yang and Zhou (2015), Sadaqat and Butt (2016), and Ryu et al. (2017) have often used RSI as a sentiment proxy to construct the sentiment index. Since the 14-day RSI is frequently employed in empirical research, we incorporated it into our study.

The market-level and future-level sentiment indices of 16 agricultural futures can be determined using the following formula. In accordance with Baker and Wurgler (2006), we eliminate any possible sentiment-related information by orthogonalizing every proxy to a macro series. Macro factors include the growth rate of M2, inflation, increase in industrial production, and changes in the currency rate (N.-F. Chen et al., 1986; Fama & Schwert, 1977; Y. Li & Ran, 2020; Y. Li & Zhang, 2021). Regarding principal component analysis, as follows:

Where

More pessimistic investors would have short positions on the agricultural future if

Similarly, we get the agricultural futures index’s turnover rate (

Descriptive Statistics of Futures Sentiment.

Note. This table shows the descriptive statistics on the futures sentiment in the Chinese Agricultural Futures markets. The sample period is from January 2003 to October 2023.

Market-level and Future-level Sentiment in Agricultural Futures Markets

This paper selected the top eight most actively traded futures for the study for the empirical analysis that follows. Futures with exceptionally low trading volume or shortlisting periods are not examined. On January 8, 2021, for instance, live hog futures were first listed on the Dalian Commodity Exchange. Another illustration would be the extremely low trading volume of Japanese rice futures. Soybean I, Soybean II, Soybean Meal, Soybean oil, Corn, Cotton, Palm Oil, and Sugar are the eight futures that we examined.

Market-level Sentiment and Future-level Sentiment

Existing research indicates that market sentiment may have an impact on asset-level sentiment (Rao & Zhou, 2019; Zhou & Huang, 2020). This section explores how market sentiment in the agricultural futures market, and stock market sentiment, affects future-level sentiment. Various macroeconomic factors are also incorporated into the framework (Baker & Wurgler, 2006; Baker et al., 2012; Kumar & Lee, 2006). Additionally, the BW index (Baker et al., 2012), a gauge of the global stock market sentiment, is used to look into how the global stock market sentiment influences the agricultural futures market.

For the domestic stock market, the closed-end fund discount, the equity shares in new issues, the number and average first-day returns on initial public offerings (IPOs), the consumer confidence index, and the trading volume are the six underlying measures of sentiment that are used to construct the sentiment index. Data from the CSMAR database is used to orthogonalize the index to macro series.

For the global stock market, the technique for gauging sentiment expands upon Baker and Wurgler’s (2006) approach. The sentiment index (BW index) is based on the first principal component of five standardized sentiment proxies: value-weighted dividend premium, first-day returns on IPOs, IPO volume, closed-end fund discount, and equity share in new issues. These sentiment proxies include a portion of investor sentiment and a portion of idiosyncratic variance unrelated to sentiment. To obtain the stock sentiment, the raw sentiment proxies are orthogonalized to a range of macro series (Industrial production index, nominal durables consumption, nominal nondurables consumption, nominal services consumption, NBER recession indicator, consumer price index). The first principal component of those orthogonalized sentiment proxies is used to assess each sentiment.

We investigate sentiment effects in the agricultural futures market in China. We do a panel data regression to determine the relationship between market-level sentiment and future-level sentiment. Then, we evaluate the influence of sentiment in the stock market and the sentiment cross-effect between the stock and futures markets. Both domestic and global stock market sentiment are included in the regressions.

Where

Table 3 presents futures sentiment regression results. Data underwent a panel unit root test, and a fixed effects model was chosen post Hausmann test. Column (1) shows a significant positive link between future- and market-level sentiment, suggesting market sentiment significantly impacts future-level sentiment, affecting investor behavior and market dynamics. Control variables reveal overnight SHIBOR negatively affects sentiment, with other factors having minimal impact. Column (2) includes stock market investor sentiment, confirming market-level sentiment’s strong positive effect on future-level sentiment. Stock market sentiment’s coefficient,

Results of Panel Data Regression.

Note. This table illustrates how sentiment at the market level affects sentiment at the future level in Chinese agricultural futures markets. The market-level sentiment is represented by

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

To sum up, market-level sentiment significantly influences future-level sentiment in a good way. Furthermore, sentiment in the domestic stock market has a significant impact on future-level sentiment, but sentiment in the global stock markets has no bearing on it. The above conclusions sport Hypotheses 1 and 4.

Market-level and Future-level Sentiment for Each Future

This section examines the eight previously mentioned futures with time series regressions, results in Table 4. The table shows market-level sentiment positively impacts future-level sentiment across all cases, with varying effects of domestic versus global stock market sentiment. Soybean I is influenced by domestic sentiment, Soybean II by global, and Corn is negatively impacted by both. Soybean oil is unaffected by stock market sentiment. Six of eight agricultural futures are influenced by domestic stock market sentiment, with mixed positive and negative regression coefficients. Control variables show diverse impacts on future-level sentiment, confirming influences from futures, stock markets, and macroeconomic shocks, with futures market sentiment impact being consistent. In summary, market-level sentiment’s positive effect on future-level sentiment is clear, but stock market sentiment’s influence varies significantly across futures.

Results of Time-series Data Regressions.

Note. This table reports the effect of market-level sentiment on future-level sentiment for each future of Chinese agricultural futures Markets.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Sentiment and Agricultural Futures Return

Market-level sentiment and future-level sentiment are investigated separately in this section. First, the relationship between sentiment at the market level and futures returns is examined using panel data analysis. After that, we separate future-level sentiment into two categories: contagious sentiment and idiosyncratic sentiment. Next, we investigate the connection between idiosyncratic and contagious sentiment and futures returns for eight different futures.

Empirical Results of Market-level Sentiment on Futures Returns

Before separating the total sentiment indices into contagious and idiosyncratic parts, we first regress the market-level sentiment on agricultural futures returns, adjusting for the one-period lagged agricultural futures returns, trading volume, and open interest. In particular, we run the following regression:

Where

Table 5 shows the impact that market-level sentiment has on futures returns in the Chinese agricultural futures market. We provide the generalized method of moments (GMM) estimate findings due to the endogeneity problems. Therefore, we employ the two-stage least squares method of Raman et al. (2017) and Le Pen and Sévi (2017) to estimate the regressions using GMM regressions. We adopt sentiment change as the instrument.

Regressions for Futures Returns.

Note. This table presents the panel data results of market-level sentiment on Chinese agricultural futures returns.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Results in Columns (1) to (3) indicate a significant positive link between market-level futures sentiment and futures returns, with coefficients at the 1% significance level. Market sentiment overreaction acts as a catalyst, influencing futures returns’ ascent and descent. Futures returns are sentiment-dependent, unaffected by control variables. Adding domestic and global stock market sentiment in Columns (4) to (6) maintains the positive correlation with futures returns, with futures sentiment coefficients remaining significantly positive at the 1% level. Domestic stock sentiment shows a significant negative correlation, while global market sentiment shows a positive correlation with futures returns. In Columns (7) to (9), excluding market-level sentiment, the relationship between stock market sentiment and futures returns is no longer significant, suggesting futures market sentiment is the primary driver of futures returns movement.

The above regression shows that futures market sentiment is the main variable affecting futures returns. In what follows, we decompose future-level sentiment and examine the impact of contagious sentiment and idiosyncratic sentiment on futures returns, while examining the role of stock market sentiment in the process. The above results support Hypothesis 2.

Measurement of Contagious and Idiosyncratic Future-level Sentiment

Contagious future-level sentiment expands upon the findings of Baker et al. (2012), who divided the total sentiment indices into six local and one global component. Here, this paper applies this technique to capture the first main component of eight agricultural future-level sentiment indexes, deconstructing the future-level sentiment (

The co-movement and commonality of eight future-level sentiment indices may be represented by the contagious future-level sentiment (

Where

Where

Sentiment changes in each agricultural future.

Idiosyncratic sentiment changes in each agricultural future.

Empirical Results of Contagious Sentiment on Futures Returns

To address the sentiment effect on agricultural futures returns, we run regressions to examine the influence of contagious future-level sentiment on agricultural futures returns after correcting for the one-period lagged agricultural futures returns and other control variables. We do the following regressions to learn more about the roles of contagious future-level sentiment.

Where

Table 6 shows the impact of contagious future-level sentiment on agri-futures returns. Regressions confirm no endogeneity issues. Column (1) reveals a significant positive coefficient for

Contagious Sentiment and Futures Return.

Note. This table presents the panel data results of contagious sentiment on Chinese agricultural futures returns.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Overall, contagious futures sentiment considerably influences the movement of futures returns, but stock market sentiment has no discernible impact on futures returns, according to the regressions in Table 6. The sentiment of the stock market affects the sentiment of the futures market to some extent, which contributes to the aforementioned results. However, as Table 4 shows, sentiment in the stock market has very little effect on returns. When sentiment is taken into account, the presence of futures market sentiment greatly reduces the influence of stock market sentiment.

Empirical Results of Combined Effects of Contagious Sentiment and Idiosyncratic Sentiment on Futures Returns

To address the sentiment effect on agricultural futures returns, we run regressions to examine the influence of contagious and idiosyncratic future-level sentiment on agricultural futures returns after correcting for the one-period lagged agricultural futures returns and other control variables. We do the following regressions to learn more about the roles of contagious and idiosyncratic future-level sentiment.

Where

Table 7 shows the correlation between contagious and idiosyncratic future-level sentiments and agricultural futures returns. No endogeneity issues found, regressions reveal both sentiments significantly and positively impact returns at the 1% level. Coefficients for contagious (0.004) and idiosyncratic (0.007) sentiments suggest respective returns increases of 21.4% (=0.004*1.0095/0.0189) and 29.3% (=0.007*0.7898/0.0189). Idiosyncratic sentiment has a stronger effect on returns. Both sentiments boost returns, with positive sentiment leading to increases and negative to decreases. Idiosyncratic sentiment more influences returns due to its specific nature. Columns (2) to (3) show domestic and global stock market sentiment have no significant effect on returns, unlike the two futures sentiments. Control variables in Columns (4) to (7) confirm this, with minimal stock market sentiment impact. In Columns (8) to (10), excluding contagious sentiment, idiosyncratic sentiment remains significantly positive at the 1% level, and domestic stock sentiment is positive at the 5% level, indicating stock market sentiment’s role when contagious sentiment is not considered.

Contagious Sentiment and Idiosyncratic Sentiment and Futures Return.

Note. This table presents the panel data results of contagious sentiment on Chinese agricultural futures returns.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

To sum up, the regression findings in Table 7 show that while stock market sentiment has no discernible effect on futures returns, contagious sentiment, and idiosyncratic sentiment have a major influence on the movement of futures returns. The above results are consistent with the findings of Zhou and Huang (2020). Furthermore, the findings suggest that idiosyncratic sentiment has a stronger effect on future returns than contagious sentiment. The above results support Hypothesis 3.

Further Research

The key components of Hypotheses 1 through 4 were examined in the study mentioned above. The results of the empirical analysis support the hypotheses: first, the future-level sentiment of agricultural futures sentiment is significantly influenced by market-level sentiment. Second, there is a significant positive correlation between agricultural market-level sentiment and futures returns. After decomposing future-level sentiment into idiosyncratic and contagious sentiment, the results show that both forms of sentiment positively affect futures returns, with idiosyncratic sentiment producing a more significant effect. Finally, sentiment in the domestic stock market has a greater influence on futures sentiment than sentiment in the global stock market. In the following, the robustness of the tested hypotheses will be examined, and further testing will be conducted on the untested one.

Alternative Measure of Market-level Sentiment

In this study, we investigate the presence of a market-level sentiment influence on agricultural futures returns by employing an alternate measure of market sentiment. Given that the relative strength index (RSI) serves as an indicator of market overbuying or overselling (Hudson & Green, 2015; Ryu et al., 2017; Sadaqat & Butt, 2016; Yang & Zhou, 2015), we utilize the 14-day RSI as an approximate gauge for market sentiment in this analysis. We conduct a regression analysis, regressing agricultural futures returns on market-level sentiment while accounting for one-period lagged agricultural futures returns, trading volume, and open interest. The findings are summarized below.

The results presented in Columns (1) to (3) of Table 8 reveal a significantly positive correlation between market-level futures sentiment and futures returns, with coefficients that are significant at the 1% level. Market sentiment overreaction acts as a catalyst in the futures market, exacerbating both upward and downward movements. In an active trading environment, heightened emotions among market participants lead to increased futures returns, while subdued emotions result in decreased returns. Consequently, sentiment fluctuations have a substantial impact on futures returns. The robustness of these findings remains unaffected by the inclusion of various control variables.

Regressions for Futures Returns.

Note. This table presents the panel data results of market-level sentiment on Chinese agricultural futures returns.

, ** and, * indicate significance at the 1%, 5%, and 10% levels, respectively.

In Columns (4) to (6), we incorporate variables representing domestic and global stock market sentiments into the regressions. Even in this context, market-level futures sentiment maintains a significantly positive correlation with futures returns. Futures returns rise in conjunction with the sentiment of the futures market, with the coefficient of futures sentiment being significant at the 1% level. These results suggest that the primary driver of futures returns movement is the sentiment of the futures market. The regression analysis confirms that futures market sentiment is the key determinant of futures returns. Overall, these findings lend support to Hypothesis 2 and are consistent with the results presented in Table 5.

An Investigation into the Combined Impacts of Idiosyncratic and Infectious Sentiment

This section will assess the combined impact of idiosyncratic and contagious future-level sentiment on each agricultural futures return using time-series regressions. The contagious and idiosyncratic future-level sentiments are therefore incorporated into the regressions. The estimated coefficients are shown in Table 9.

Contagious Sentiment and Idiosyncratic Sentiment and Futures Return for Each Future.

Note. This table reports the regression results of contagious sentiment and idiosyncratic sentiment contagion effects on each agricultural futures return. The agricultural futures return at time

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Table 9 displays the link between contagious and idiosyncratic future-level sentiment and agricultural futures returns. Panel A’s Columns (1–8) indicate both sentiments positively correlate with returns at the 1% significance level, in line with Table 7. Panel B adds domestic and global stock market sentiment, with findings similar to Panel A. Columns (1–8) show these sentiments significantly impact returns, while stock market sentiment’s influence is insignificant, as per Table 7. Stock market sentiment’s effect on returns is reduced when contagious and idiosyncratic sentiments are present. Panel C includes control variables plus stock market sentiment measures, with robust results. Across all regressions, contagious and idiosyncratic sentiment clearly impact futures returns, while domestic and global stock market sentiment’s impact is minimal.

Further research on contagious sentiment and idiosyncratic sentiment reveals that the effects of contagious sentiment and idiosyncratic sentiment on futures returns are robust, with both being significantly positively associated with futures returns. Stock market sentiment, both domestic and global stock market sentiment, did not significantly affect futures returns. The above results support the validity of Hypothesis 3.

Sentiment in Bull and Bear Markets

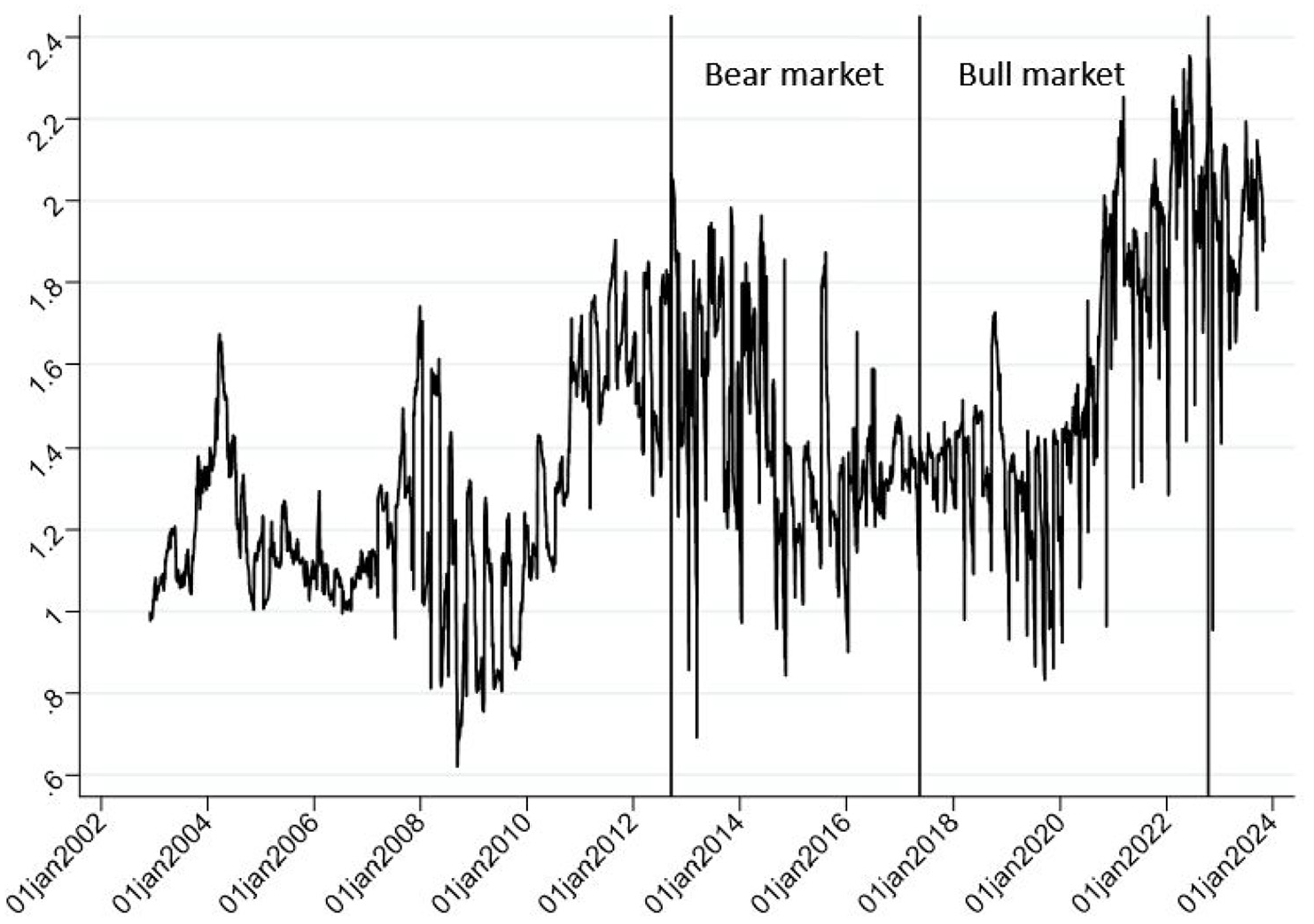

In this part, a market price index is constructed to measure market movements and pinpoint bull and bear markets in the Chinese agriculture futures market. With reference to R. Chen et al. (2022), the weights of the index are established as below.

Where

Where

The above formula is utilized to construct a market price index to differentiate between bull and bear markets in the futures market (Figure 3). In this section, one of the most distinct bear and bull market phases (September 17, 2012–October 14, 2022) was selected and the data for this phase was analyzed.

Market price index trends in the bear and bull markets.

Table 10 presents regression results for sentiment in bull and bear markets. Column (1) shows a significant positive link between future- and market-level sentiment in bear markets. Column (2) includes stock market sentiment, which has minimal impact on futures, while market-level sentiment significantly affects future-level sentiment. The BW index in Column (3) shows no significant correlation with future-level sentiment. In Column (4), domestic and global stock market sentiment

Results of Panel Data Regressions for Bear and Bull Markets.

Note. The impact of market-level sentiment on future-level sentiment for bull and bear markets is shown in this table.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

In bull markets, future-level sentiment is strongly influenced by market-level sentiment, with

To sum up, market-level sentiment has a considerable positive impact on future-level sentiment. Moreover, during bull markets, future-level sentiment is greatly influenced by the sentiment of the stock market. The above results support the validity of Hypotheses 1 and 4.

Table 11 is divided into four parts that examine the futures market for bull and bear markets. Panel A and C are for bear markets and Panel B and D are for bull markets. The results from Panel A show that for all agricultural futures, idiosyncratic sentiment significantly and positively affects futures returns. Contagious sentiment also has a significant and positive impact on futures returns for some futures. While sentiment in the stock market matters, its effects are not always uniformly favorable. The results in Part B differ from those in Part A. It can be seen that for all agricultural futures, contagious sentiment and idiosyncratic sentiment is significantly and positively associated with futures returns. The results suggest that both contagious sentiment and idiosyncratic sentiment have a more significant impact on futures returns under bullish conditions. On the other hand, neither domestic nor global stock market sentiment is significantly correlated with futures returns.

Contagious Sentiment and Idiosyncratic Sentiment and Futures Return for Bear and Bull Markets.

Note. This table reports the regression results of contagious sentiment and idiosyncratic sentiment contagion effect on agricultural futures returns in Chinese agricultural futures Markets. The agricultural futures return at time

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

After adding control variables, the results are displayed in Parts C and D. The results in Part C demonstrate that idiosyncratic sentiment has a strong and positive correlation with futures returns for all agricultural futures. Contagious sentiment has a considerable favorable impact on futures returns for the majority of agricultural futures. Some futures’ returns are impacted by the sentiment of the domestic stock market during bear markets. Conversely, the futures returns are mainly unaffected by global stock market sentiment. The results of Part D are similar to those of Part B. Both contagious and idiosyncratic futures sentiments have a significant positive effect on futures returns under bull market conditions. Futures returns, on the other hand, are largely unaffected by changes in stock market sentiment. The research results indicate that, firstly, similar to the findings of Zhou and Huang (2020), both contagious sentiment and idiosyncratic sentiment have significant impacts on futures returns, with idiosyncratic sentiment playing a more prominent role. Secondly, after extending the research of Zhou and Huang (2020) by categorizing the market into bull and bear markets, we found that contagious sentiment and idiosyncratic sentiment have a more pronounced effect on bull markets. This suggests that under bullish conditions, the futures market is more susceptible to the influence of investor sentiment.

Overall, both contagious and idiosyncratic futures sentiments have a considerable positive impact on future-level sentiment. The above results support the validity of Hypothesis 3.

Macroeconomic Shocks

This section examines the impact of contagious and idiosyncratic future-level sentiment on agricultural futures returns including a variety of macroeconomic factors. The regression model is as follows:

Where

Regressions of Futures Returns With Macroeconomic Factors.

Note. The results of contagious sentiment and idiosyncratic sentiment effects on agricultural futures returns for Chinese agricultural markets are shown in this table.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

In Table 12, extra macroeconomic variables are included to investigate the impact of contagious sentiment and idiosyncratic sentiment on agricultural futures returns.

As can be seen from the regression results, the macroeconomic variables include the consumer and producer price indices, the growth rate of M2, the year-on-year growth rate of industrial value-added, the monthly return of the CSI 300 index, the agricultural price index, the exchange rate, and the overnight SHIBOR. The results indicate that the inclusion of the control variables has not affected the relationship between contagious sentiment and idiosyncratic sentiment and the agricultural futures returns. At the 1% level, both contagious sentiment and idiosyncratic sentiment are significantly greater than zero. Consistent with the results above, neither domestic nor global stock market sentiment has a significant impact on futures returns.

The aforementioned findings confirm the robustness of the regression results above and once again support Hypothesis 3.

Conclusion

We summarize by going over the paper’s primary contributions. Prior research has mostly concentrated on examining investor sentiment indexes in bond and stock markets. In this paper, agricultural futures sentiment indices at the market and future levels are built to investigate the connection between sentiment and futures returns. First, the impact of futures market-level sentiment on future-level sentiment is examined, along with the role of stock market sentiment. Second, future-level sentiment is categorized into contagious sentiment and idiosyncratic sentiment, and the effects of market sentiment, contagious, and idiosyncratic sentiment on futures returns are investigated. Meanwhile, the role of the stock market sentiment is examined. Finally, the paper innovatively separates the futures market into bull and bear markets and examines the relationship between sentiment and futures returns under different market conditions. The article further extends the depth of the study by carefully analyzing the relationship between sentiment and agricultural futures returns.

This paper verifies that market sentiment significantly boosts future sentiment, especially during bull markets. Agriclutrual futures returns are positively affected by market and futures sentiment. Robustness tests show that futures returns are influenced by both contagious and idiosyncratic sentiment, in any market condition. The study on sentiment and futures returns has gaps: it lacks analysis on global sentiment’s impact on domestic returns and doesn’t compare sentiment effects on domestic versus foreign agri-futures. Future research should address these and country-specific differences.

The paper suggests regulators focus on “emotional regulation” in futures monitoring, starting with stakeholders like investors and government. To enhance market efficiency, the regulatory framework must evolve, prioritizing the condemnation of unethical trading and strengthening investor risk education. Rational investor behavior should be encouraged, and institutional behavior restrained. A national futures market risk monitoring system is needed for market efficiency and transparency, mitigating market shocks from futures volatility.

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This project is funded by the research grant 9222008 from the Beijing Municipal Natural Science Foundation and research grant FRSK-2024-004 from the Prosperous Social Science Action Plan Project of Beijing University of Agriculture, for which we express our heartfelt gratitude. We are also deeply thankful to the participants of various seminars for their valuable feedback and suggestions. Any potential errors in this work are solely our responsibility.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability

The data that support the findings of this study are available from the corresponding author upon reasonable request.