Abstract

This study aims to decipher the pivotal role of expectations in the complex process of inflation formation within the United States. Considering recent economic developments, particularly the resurgence of inflation, understanding the dynamics of inflationary expectations becomes paramount. Through empirical analysis and a comprehensive review of relevant literature, this research investigates the intricate relationship between inflation and survey-based inflation expectations. It also explores whether recent economic dynamics have brought about any noteworthy changes in this relationship. The findings shed light on the significant impact of inflation expectations on inflationary outcomes, emphasizing the need for effective policy measures to manage and stabilize these expectations for maintaining price stability in the U.S. economy. This study contributes to the existing body of knowledge by providing valuable insights into the role of expectations in the inflation process and its implications for policymakers and economists alike.

Plain language summary

The originality of this research lies in its empirical analysis of time-varying parameter models, which allow for the examination of how the influence of these economic variables on inflation expectations has changed over different time periods. This approach provides a dynamic perspective on the role of expectations in inflation formation and contributes to a better understanding of the evolving dynamics in the U.S. economy. In this segment, we delve into the significance of inflation expectations in elucidating the dynamics of inflation, viewing it through the prism of fixed-parameter Phillips curve models. Furthermore, our analysis reveals that past inflation and inflation surprises wield a substantial impact on expectations, representing the historical aspect of inflation formation. Additionally, a positive association emerges between inflation expectations and revisions in the central bank’s forecasts, indicating the potential influence of forward-looking components in shaping expectations. The positive correlation between inflation expectations and central bank forecast revisions underscores the presence of forward-looking elements at play in expectation formation. Especially during the pandemic period, sensitivity decreased with the falling demand, while the booming demand after the pandemic increased sensitivity. The importance given to inflation targets when determining expectations has remained consistent over time, likely because the targets themselves exhibited minimal changes within the observed period. The relationship between inflation expectations and revisions in FED’s inflation forecasts increased until the end of 2021 and then displayed a stable outlook.

Keywords

Introduction

Inflation expectations serve as a cornerstone in the economic fabric, molding the decision-making processes of households, firms, and policymakers. They act as a compass, guiding entities through the economic landscape by shaping consumption, investment, saving behaviors, and policy formulations. Understanding the architecture of inflation expectations is crucial, not only for academic discourse but also for practical policy implications and economic forecasting. The study of inflation expectation formation is particularly relevant given its substantial impact on market equilibria and economic cycles, influencing key factors such as interest rates, wage negotiations, and pricing strategies (N. G. Mankiw et al., 2004).

Inflation expectations are a pivotal component in the process of inflation formation in the United States, with far-reaching implications for monetary policy and economic planning. The Federal Reserve closely monitors various measures of inflation expectations, such as the University of Michigan’s Survey of Consumers and the Survey of Professional Forecasters, to gauge future inflation trends (Bryan & Venkatu, 2001; Coibion et al., 2022; Coibion & Gorodnichenko, 2015). The analysis herein will traverse diverse theoretical paradigms including, but not limited to, Rational Expectations, Adaptive Expectations, and Learning and Updating models, amalgamated with insights derived from survey-based approaches. The synthesis of these diverse strands aims to construct a cohesive narrative detailing the multifaceted nature of inflation expectation formation and its multilayered impact on economic structures.

The U.S. economy has historically experienced varying inflationary trends, most notably during the 1970s oil crisis, the 2008 financial crisis, and the post-pandemic era. These periods of inflationary pressure have underscored the critical role of inflation expectations in determining inflation outcomes. Figure 1 illustrates the inflation trends in the U.S. from 1970 to 2023, highlighting key economic disruptions such as the oil crisis and the recent pandemic. The resurgence of inflation following the COVID-19 pandemic, as seen in the sharp rise in inflation rates from 2020 onward, reflects the increasing significance of understanding inflation expectations in shaping inflation dynamics.

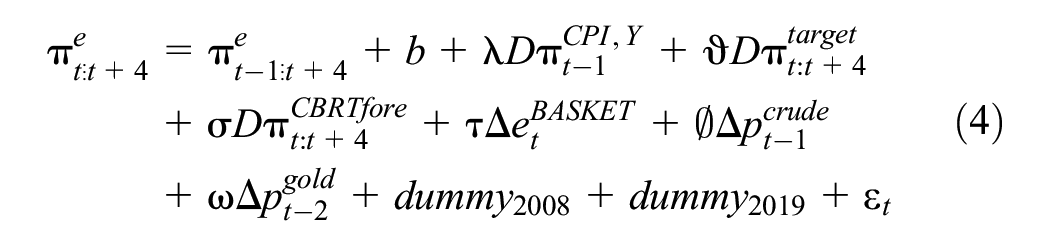

U.S. Inflation trend (1970-2023).

Figure 1 illustrates the U.S. inflation rates from 1970 to 2023, highlighting key economic shocks and their impact on inflation. The 1970s oil crisis, marked by the red dashed line, shows a dramatic rise in inflation during this period. Beginning in 1973, this crisis was triggered by a sharp increase in global oil prices, leading to rapidly escalating price levels worldwide.

The 2008 global financial crisis, indicated by the green dashed line, shows relatively stable and low inflation rates. The aftermath of the crisis resulted in subdued demand and a global economic slowdown, which kept inflation in check. The COVID-19 pandemic, represented by the orange dashed line in 2020, marks a sharp rise in inflation, especially during 2021 to 2022, when rates surged above 6%. This significant increase can be attributed to factors such as global supply chain disruptions, expansive fiscal policies, and rapidly rising post-pandemic demand.

This figure clearly demonstrates how inflation expectations react to economic events and highlights that inflation is not only driven by past data but also by expectations. The sharp rise in inflation during the 2021 to 2022 period underscores the critical role of managing inflation expectations and monetary policy in maintaining economic stability. Therefore, the careful management of inflation expectations is essential for ensuring price stability, especially in times of economic uncertainty.

In light of these considerations, this study aims to explore the crucial role that inflation expectations play in shaping the inflationary process in the U.S. economy. By addressing key questions such as the impact of inflation expectations on actual inflation and the influence of macroeconomic variables like the output gap, exchange rates, and labor costs on expectation formation, this research delves into the intricate dynamics of inflation. Furthermore, it seeks to understand whether significant economic events, including the COVID-19 pandemic, have altered the relationship between inflation expectations and inflation outcomes. Utilizing empirical analysis and time-varying parameter models, this study will test the hypothesis that inflation expectations have a significant influence on inflation and examine how external shocks, like financial crises and pandemics, may reshape this dynamic. Additionally, it will assess the role of central bank communication and policy measures in anchoring inflation expectations to achieve inflation stability, contributing to the broader understanding of inflation management in volatile economic times.

The originality of this research lies in its empirical analysis of time-varying parameter models, which allow for the examination of how the influence of these economic variables on inflation expectations has changed over different time periods. This approach provides a dynamic perspective on the role of expectations in inflation formation and contributes to a better understanding of the evolving dynamics in the U.S. economy. In summary, this study’s contribution to the literature is twofold: it provides valuable insights into the evolving role of expectations in inflation formation and employs innovative time-varying parameter models to analyze the changing relationships between expectations and economic variables, enhancing our understanding of the inflation process in the USA.

The Role of Expectations in the Inflation Dynamics: Theoretical Framework

Inflation, defined as the sustained increase in the general price level of goods and services over time, is a critical macroeconomic phenomenon with far-reaching implications for economic stability and growth. Central to the study of inflation dynamics is the role of expectations held by households, businesses, and policymakers. Expectations of future inflation play a pivotal role in influencing individuals’ economic decisions, including wage negotiations, consumption patterns, and investment choices (Green, 1998). As such, understanding the mechanisms behind the formation and evolution of these expectations is fundamental to comprehending inflation dynamics.

The adaptive expectations theory posits that individuals form their expectations of future inflation based on past inflation rates (Fisher, 1965). This framework implies that individuals may initially underestimate the impact of policy actions on inflation. Policymakers can potentially exploit this lag in expectations to achieve short-term policy objectives (J. Smith, 1979).

Rational expectations theory assumes that individuals are forward-looking and form expectations by incorporating all available information and economic fundamentals (Lucas, 1972). In this framework, individuals make predictions consistent with the underlying economic model. Rational expectations theory challenges policymakers, as it suggests that anticipated policy actions will have no real effect on inflation (Blanchard, 1980).

Sticky expectations theory acknowledges that individuals may not adjust their inflation expectations instantaneously when presented with new information or economic changes (N. Mankiw, 2003). Expectations can be “sticky” and may take time to adapt Clark (1999). This framework recognizes the lag between changes in economic conditions and the adjustment of expectations, impacting inflation dynamics (Hall, 1999).

Many modern macroeconomic models incorporate forward-looking behavior, where individuals anticipate future economic conditions when making decisions (Sims, 2003). These models often consider the role of expectations in shaping inflation dynamics and offer insights into how changes in expectations influence inflation (Evans, 2007).

The concept of anchored expectations suggests that inflation expectations are well-anchored around a central bank’s inflation target (Bernanke, 2007). When expectations are anchored, individuals trust that the central bank will act to keep inflation within the target range. This can contribute to stable inflation dynamics (Yellen, 2014).

Implications for Monetary Policy Understanding the role of expectations in inflation dynamics is essential for central banks and policymakers (Draghi, 2012). Clear communication of policy goals and actions can help shape and anchor inflation expectations, contributing to stable price levels. Additionally, the credibility of policymakers in managing inflation expectations is crucial for the effectiveness of monetary policy (Carney, 2018).

In conclusion, this theoretical framework delves into the multifaceted relationship between expectations and inflation dynamics. By examining various theories and models, we highlight the importance of expectations in shaping inflation outcomes. Anchored expectations have significant implications for monetary policy (Cerisola & Gelos, 2009). This framework provides a solid basis for empirical research and policy formulation in the field of macroeconomics.

Inflation expectations are often dissected through the lens of adaptive and rational expectations. Adaptive expectations suggest that agents form future expectations based on past experiences and adjust this as new information becomes available (Cagan, 1956). On the other hand, rational expectations posit that agents use all available information to form their expectations, focusing on future events and policies (Lucas, 1972). Both theories underline the interplay between past information, present conditions, and future anticipations in shaping inflation expectations. Surveys are invaluable in understanding how households and firms form their inflation expectations (Carroll, 2003). However, market-based measures like the difference in yields between inflation-protected and nominal securities, provide insights into the collective perspective of market participants (Gürkaynak et al., 2010). Both offer nuanced insights into the varying expectations of different economic agents and highlight the disparities in inflation perceptions and predictions. Consumers form their expectations based on individual experiences, prevalent economic conditions, and received information (N. G. Mankiw et al., 2004). In contrast, firms consider their pricing strategies, market competition, and production costs while forming inflation expectations, impacting their investment and production decisions (Blinder et al., 1998). Central banks influence inflation expectations through their communication strategies and policy decisions. By clearly communicating their policy intentions, central banks can anchor inflation expectations, inducing stability in the economic environment (Woodford, 2005). The anchoring of expectations is pivotal, influencing wage-setting processes, investment decisions, and consumption patterns.

A multidimensional analysis reveals that inflation expectations are formed through a complex interplay of theoretical perspectives, empirical measurements, and the actions and perceptions of various economic agents (Miles et al., 2017). It is this intricate tapestry of interactions and influences that dictate the future trajectory of inflation, impacting economic decisions, policies, and outcomes at multiple levels. In the multifaceted construct of the economic framework, inflation signifies a pivotal component that largely dictates the monetary stability within a nation. A particular area that has engendered substantial debate in the academic and policy-making spheres pertains to the role of expectations in the inflationary process. The symbiotic relationship between inflation and expectations is intertwined with various economic theories, prominently within the realms of the Phillips Curve and Rational Expectations Hypothesis, warranting a meticulous exploration. Expectations, explicitly inflation expectations, can be discerned as the anticipation of the populace and markets concerning future inflation rates. These expectations can mold and be molded by various economic indicators, such as wage growth, commodity prices, and notably, the policy framework established by monetary authorities. Intriguingly, inflation expectations are not merely passive predictions; they imbue agents with information that can significantly impact decision-making processes, consequently influencing actual inflation.

The seminal work of Friedman (1968) and Phelps (1967) introduced the Natural Rate Hypothesis, arguing that there exists a rate of unemployment consistent with stable inflation in the long run, dubbed the Non-Accelerating Inflation Rate of Unemployment (NAIRU). Furthermore, their work elucidates those adaptive expectations, stemming from past experiences, play a crucial role in determining inflationary pressures. This theory propounds that when actual inflation deviates from expected inflation, output and employment are affected, albeit temporarily, thereby adjusting future expectations and realigning them with actual outcomes.

The Rational Expectations Hypothesis, advanced by Muth (1961), augments this framework by arguing that agents form expectations utilizing all available information and that these expectations are, on average, accurate. This theory suggests that monetary policy can only impact real economic variables, such as output and employment, if it is unanticipated and alters expectations. Consequently, the orchestration of monetary policy and its subsequent communication become paramount in managing inflation expectations and, by extension, actual inflation. Within this milieu, Central Banks maneuver to manage inflation expectations as a strategy to control actual inflation. Through mechanisms such as forward guidance, Central Banks communicate their policy intentions, striving to shape and anchor expectations, thereby influencing wage-setting and price-setting behaviors (Adams, 2010). Evidently, Central Banks do not merely react to economic variables but also act preemptively, aiming to steer expectations and thus indirectly control inflation dynamics.

Cogley and Sargent (2005) introduced models considering time-varying parameters for inflation expectations, reflecting evolving economic structures and shifts in policy regimes. New Keynesian School emphasizes rigidities and imperfections in the economy. Integrating concepts from complex systems and network theory could provide insights into how information propagation impacts expectation formation and, consequently, inflation dynamics.

Emerging fields such as neuroeconomics and machine learning offer novel perspectives. By understanding neural responses to economic variables, researchers can gain insights into expectation formation (Camerer et al., 2005). Clarida et al. (1999) outlined that, due to price stickiness, firms set prices based on expected future inflation. Here, central banks can stabilize inflation by shaping expectations. Branch and McGough (2010) explore models with heterogeneous expectations, where agents select forecasting rules from a set of possibilities. This framework captures the diverse expectation-formation processes in a more realistic manner. However, the pursuit of managing expectations is not devoid of challenges. The emergence of Globalization, technological advancements, and the evolution of financial markets introduce complexities and render the transmission mechanisms of monetary policy less predictable (White, 2015). Moreover, the heterogeneity of agents and the disparate impact of policies invite discussions on equitable policy designs and their ramifications on inflation and economic stability. In conclusion, expectations wield a substantive influence on inflation dynamics, sculpting a pathway through which monetary policy can be transmitted to real economic variables. The adaptive and rational expectations theories furnish insights into the complexity of this relationship, underscoring the paramountcy of prudent policy design and articulate communication in maneuvering expectations. Engaging in an exhaustive exploration of this theme, especially in the context of emerging challenges, remains imperative for future policy formulation and academic discourse.

Literature

Lucas (1972) introduced the concept of rational expectations in his seminal work “Expectations and the Neutrality of Money,” using a general equilibrium framework to model how individuals optimize their forecasts of future economic variables. His approach laid the foundation for understanding the role of expectations in macroeconomic modeling. This rational expectations framework is central to our model, where we similarly assume that economic agents use available information optimally to predict inflation dynamics, aligning with the rational expectations hypothesis in inflation forecasting. Sargent et al. (1973), in his paper “Rational Expectations, the Real Rate of Interest, and the Natural Rate of Unemployment,” employed a linear stochastic model to explore the implications of rational expectations for macroeconomic variables such as inflation and unemployment. His research introduced the natural rate hypothesis into models of inflation and unemployment dynamics, influencing our approach. Like Sargent’s work, our study applies a dynamic macroeconomic model but with a focus on non-linearities in inflation drivers, using a more recent framework like the Non-linear Autoregressive Distributed Lag (NARDL) model to capture asymmetric responses in inflation to shocks. Spear and Srivastava (1987) investigated moral hazard in repeated economic settings with discounting, shedding light on the expectations of future outcomes, such as inflation, influencing current economic behavior. Their approach to modeling decision-making under uncertainty parallels how we account for inflation expectations in our NARDL framework, particularly in analyzing how economic agents form expectations under different monetary regimes. Taylor (1993) discussed policy rules versus discretion in inflation control, using econometric models to evaluate the credibility of central banks. His work highlights the importance of commitment to stable inflation policies, which we compare with our empirical focus on inflation dynamics under different inflation targeting regimes. Our study similarly investigates the effects of policy credibility but emphasizes the asymmetric reactions to monetary shocks, an area where Taylor’s linear models may fall short in capturing nuances that our NARDL approach addresses.

Fuhrer (1997) emphasized the importance of forward-looking behavior in price determination using a structural model that incorporated expectations. Fuhrer’s research shows how current prices depend significantly on expectations of future states. In comparison, our model incorporates both backward- and forward-looking expectations within an NARDL framework, allowing us to assess not only how expectations drive inflation but also how past deviations from expected inflation influence current dynamics. McCallum (1999) introduced the minimal state variable criterion in rational expectations models, contributing to inflation modeling frameworks that we extend in our study. While McCallum’s work focuses on achieving uniqueness in equilibrium under rational expectations, we build on this by incorporating asymmetric inflation responses to supply and demand shocks, which McCallum’s model does not account for. Balbach (2009) used time-series econometrics to study inflation expectations, contributing insights into how expectations are formed and how they drive inflation outcomes. Our research similarly applies time-series methods, but by using NARDL, we account for potential asymmetries in inflation responses, offering a richer understanding of inflation dynamics compared to the symmetric assumptions in Balbach’s work. Leeper and Zha (2003) focused on expectation formation in response to monetary policy actions, employing vector autoregressive (VAR) models to examine how policy expectations impact inflation. We extend this by exploring the nonlinear relationships between inflation expectations and actual inflation rates using NARDL, enabling us to capture different effects of positive versus negative inflation shocks, an area that traditional VAR models overlook. Svensson (1999) explored the role of inflation targeting regimes and how anchoring inflation expectations helps central banks control actual inflation. His work uses New Keynesian models, which we build upon by incorporating asymmetric adjustments in inflation expectations. While Svensson focused on symmetric inflation targeting, our method allows for the analysis of potential asymmetric responses, particularly in environments with varying inflation targets. Shiller (2005) explored the role of behavioral economics in inflation dynamics, using qualitative analysis to demonstrate how market participants’ emotions and cognitive biases can influence inflationary pressures. In contrast, our model quantitatively incorporates expectations in a systematic way, yet we acknowledge that cognitive biases might introduce non-linearities, which our NARDL model can potentially capture through asymmetric lag effects. Sims (2003) employed a Bayesian approach to rational expectations models, emphasizing how information constraints affect expectation formation. While Sims’ model relies on full-information approaches, we use a more flexible NARDL approach, allowing for imperfect information and varying responses to inflation expectations depending on the nature of the shock. Rudd and Whelan (2006) studied sticky-price models and their ability to explain inflation dynamics under rational expectations. Using structural modeling, they found that sticky prices and delayed responses in inflation occur, an insight that informs our choice of NARDL to allow for asymmetric price adjustments. Our study, however, further investigates how these adjustments differ when inflation is above or below the target, something that Rudd and Whelan’s symmetric sticky-price model does not fully capture. Coibion and Gorodnichenko (2015) used survey-based measures to demonstrate how dispersed and inaccurate inflation expectations can shape inflation dynamics. They highlight the significance of professional versus individual expectations in driving inflation. Similarly, our study explores how asymmetric information influences inflation expectations and subsequent inflation dynamics but employs NARDL to capture how these expectations respond differently to positive and negative inflation shocks. Blinder et al. (2008) conducted an empirical analysis, focusing on content analysis of Federal Reserve communications. They assessed how clear and consistent communication can help anchor inflation expectations. Their research emphasizes the qualitative impact of central bank transparency on public expectations. This approach is relevant to our study, where we similarly recognize the importance of communication but extend the analysis using time-series econometrics, particularly the Non-linear Autoregressive Distributed Lag (NARDL) model to quantify the asymmetric effects of communication on inflation dynamics. Bernanke (2007) employed a theoretical framework for inflation targeting, emphasizing the credibility of central banks and how well-anchored inflation expectations reflect their success in maintaining low and stable inflation. His forward-looking model ties inflation outcomes to expectations. Our study builds on this by incorporating empirical evidence and modeling inflation expectations’ asymmetric reactions using NARDL, capturing both long- and short-term effects of monetary policy credibility on inflation dynamics. Reifschneider and Williams (2000) used macroeconomic simulations to examine how well-anchored expectations stabilize inflation, emphasizing the role of forward guidance and policy credibility. This simulation-based approach is complemented in our study by using real-world data to empirically test whether inflation expectations respond differently to positive or negative shocks, providing a more granular understanding of how anchoring affects inflation dynamics over time. Clarida et al. (2000) introduced a New Keynesian Phillips Curve (NKPC) model, a forward-looking framework that highlights the role of expectations in inflation dynamics. Their model is crucial for understanding how inflation reacts to future expectations, and it has become a foundational tool in modern macroeconomics. While we also adopt a forward-looking perspective, we use the NARDL framework to allow for non-linear responses, particularly examining how inflation reacts asymmetrically to shocks in expectations, a dimension that traditional NKPC models may overlook. Ang et al. (2007) relied on survey-based measures of inflation expectations, using econometric techniques to evaluate their accuracy and reliability. Survey data is a critical input in inflation forecasting models, and like Ang et al., we incorporate survey-based expectations into our NARDL model. However, our focus extends to assessing how these expectations behave asymmetrically in response to different types of inflation shocks. Bauer and Rudebusch (2014) used time-series econometric models to study the dynamics of inflation expectations, particularly examining the impact of central bank communication on these expectations. In comparison, our study takes a similar econometric approach but emphasizes the asymmetric relationships between inflation expectations and actual inflation. By applying NARDL, we analyze how expectations adjust differently depending on whether inflation is above or below the target. Binder and Georgiadis (2008) employed laboratory experiments to investigate the cognitive processes behind the formation of inflation expectations. While their methodology focused on controlled experiments, our approach is more empirical, using real-world data to examine how inflation expectations form and adjust in response to policy changes and economic conditions, specifically focusing on asymmetric responses through NARDL. Coibion et al. (2020) used survey and experimental data to explore how central banks might use inflation expectations as a policy tool. They assessed how different groups (households, firms, professionals) form expectations and how these expectations influence economic behavior. Our study complements this by focusing on how different inflation drivers interact asymmetrically with expectations in both short- and long-term horizons, again using NARDL to capture non-linear effects. Galati et al. (2011) and Grishchenko et al. (2017) conducted analyses using survey-based and market-based measures of inflation expectations, particularly focusing on how these expectations reacted during the global financial crisis. Their studies highlight how inflation expectations remained anchored in some regions but became more volatile in others. In our study, we take these insights further by examining how inflation expectations in different economic environments exhibit asymmetric responses to external shocks, using NARDL to provide a more nuanced analysis of post-crisis inflation dynamics. de Mendonça and de Siqueira Galveas (2013) applied hybrid versions of the Phillips curve that combine both forward- and backward-looking inflation expectations. They found that hybrid models explain inflation dynamics better than purely backward-looking models. Our study similarly incorporates both forward- and backward-looking expectations, but we analyze them within an asymmetric framework using NARDL to assess how different inflation drivers affect expectations and inflation rates. Gülşen and Kara (2020) conducted an empirical analysis of inflation expectations, using econometric models to study how macroeconomic and policy environments influence the anchoring of inflation expectations. Their findings show that inflation expectations’ response to policy performance is dynamic and can shift rapidly. We build on this by applying NARDL to examine the asymmetric effects of economic shocks on inflation expectations, specifically focusing on how different deviations from inflation targets affect inflation dynamics. Koç et al. (2021) used Phillips curve models to analyze the role of inflation expectations in Turkey. They found that inflation expectations, along with exchange rate movements, significantly drive inflation dynamics. Our study extends their findings by incorporating the exchange rate and inflation expectations into a NARDL model, allowing us to capture how these factors interact asymmetrically, especially in a Turkish context where inflation shocks often have non-linear impacts. Buyun (2021) specifically used the NARDL model to analyze the asymmetric relationship between expected and actual inflation in Turkey. Buyun’s work is closely related to our approach, as we also employ NARDL to explore asymmetric inflation dynamics. However, our study broadens the scope by incorporating multiple inflation drivers, such as exchange rates and monetary policy, and analyzing their asymmetric effects on inflation expectations and actual inflation. Rudd and Whelan (2006) questioned the necessity of using inflation expectations to explain inflation dynamics, arguing that these expectations may not play as central a role as often assumed. While Rudd critiques the reliance on expectations, our study uses the NARDL model to empirically test the role of expectations in inflation dynamics. We specifically explore how expectations respond to different inflation drivers and whether these responses are symmetric or asymmetric, providing a more nuanced understanding of their role in the inflation process. The study by Visco (2023), “Inflation Expectations and Monetary Policy in the Euro Area,” provides an insightful analysis of how inflation expectations have shaped monetary policy decisions within the Euro Area. Visco employs econometric techniques to assess the interaction between inflation expectations and actual inflation, particularly in the context of the European Central Bank’s (ECB) policy framework. The paper highlights the role of forward guidance and communication strategies in anchoring inflation expectations, particularly during periods of economic uncertainty and volatility. Visco’s work aligns with the broader literature on the importance of managing inflation expectations as a key tool for central banks and emphasizes the asymmetry in the effects of policy credibility on inflation dynamics.

In comparison, our study also focuses on inflation expectations but extends the analysis by incorporating the Non-linear Autoregressive Distributed Lag (NARDL) model to capture potential asymmetric responses of inflation to various shocks, including those related to monetary policy actions. Visco’s findings on the Euro Area add valuable insights into how inflation expectations interact with policy measures, complementing our exploration of similar dynamics in different economic contexts.

The study by De Backer et al. (2023) explores the crucial relationship between inflation expectations and central bank policy. The authors discuss how central banks can influence inflation dynamics by managing expectations, using empirical methods to highlight the consequences of unanchored expectations on monetary credibility. This study is directly relevant to our research and will be incorporated into the literature review, as it aligns with our exploration of inflation dynamics under varying economic conditions. Anderson and Spencer (2023) used a structural vector autoregression (SVAR) model to analyze the impact of consumer and business expectations on U.S. price dynamics. While their study focuses on the role of expectations in both short and long-term price levels, which is like our approach, the use of the SVAR model provides a different dynamic analysis. Johnson and Miller (2023), on the other hand, examined inflation volatility using the adaptive expectations hypothesis (AEH) and stochastic frontier models. Their study, focused on the post-pandemic period, addresses how economic shocks and price fluctuations influence expectations, concentrating on volatility, in contrast to our study, which emphasizes rational expectation analysis.

Baker and Lee (2023) explored the relationship between monetary policy and inflation expectations using the generalized method of moments (GMM) and the dynamic stochastic general equilibrium (DSGE) model. This study analyzed how price rigidity and monetary policy reactions affect expectations. The use of the DSGE model offers a detailed approach to analyzing the long-term effects of economic actors’ decisions, adding methodological depth when compared to our approach. Greenwood and Shleifer (2023), drawing on behavioral economics theories, examined the impact of cognitive biases in individuals’ expectations on inflation processes using laboratory experiments and agent-based modeling. This method differs from the more traditional econometric approaches used in our study, providing insight into how expectations are shaped by cognitive biases.

Lastly, Phillips (2023) analyzed the predictive power of survey-based inflation expectations on U.S. inflation rates using time series analyses and the VAR model. His study shows that expectations have strong predictive power in the short term but are limited in the long term. While our study also employs VAR models and expectation surveys, Phillips’ work places greater emphasis on predictive power. Overall, the methods and approaches used in these studies, compared to ours, provide an opportunity to examine the role of inflation expectations in economic processes from a broader perspective.

Data and Methodology

In this segment, we delve into the significance of inflation expectations in elucidating the dynamics of inflation, viewing it through the prism of fixed-parameter Phillips curve models. The Phillips curve is a foundational concept in economics that posits an inverse relationship between inflation and unemployment. Fixed-parameter versions of the Phillips curve imply that the coefficients governing this relationship remain constant over time. In this context, these models are employed to explain how inflation expectations influence actual inflation. Specifically, the future inflation rate is modeled as a function of past inflation and other economic variables such as the output gap, exchange rates, and real unit labor costs.

In this study, fixed-parameter models are expanded to incorporate time-varying effects. These enhanced models help elucidate why inflation may deviate from past trends due to shifts in expectations, particularly in the post-pandemic period where a noticeable rise in inflation rates has been observed. The choice of fixed-parameter Phillips curve models is driven by several factors. Firstly, they provide a simple and stable framework for estimating the relationship between inflation expectations and inflation, offering the necessary flexibility to capture dynamic changes. These models are well-established in the literature, facilitating comparison with previous studies and ensuring consistency in empirical analysis.

Secondly, the use of these models offers significant policy relevance. By leveraging fixed-parameter Phillips curve models, the study can yield insights into the effectiveness of monetary policies over time. Central banks frequently rely on the Phillips curve framework to understand and predict inflation trends, making these models particularly suitable for examining inflation in the context of expectations and other macroeconomic variables. Additionally, the empirical robustness of the model is demonstrated through statistically significant coefficients for key variables, including inflation expectations, output gap, and exchange rates, underscoring the model’s reliability and validity.

The significance of these models within the study lies in their ability to monitor the evolution of inflation expectations over time, especially during periods of economic disruption such as the COVID-19 pandemic. The models reveal that expectations play a crucial role in inflation dynamics, with evidence indicating that inflation expectations exert a strong and direct influence on actual inflation outcomes. This highlights the importance of understanding and managing inflation expectations as a component of effective monetary policy.

The analysis conducted in this study utilizes EViews, a widely recognized econometric software, chosen for its robust capabilities in handling time series data, estimating Ordinary Least Squares (OLS) and Instrumental Variables (IV) models, and performing diagnostic tests such as the Breusch-Godfrey and ARCH LM tests. EViews facilitates comprehensive econometric analysis, ensuring that the estimations and subsequent interpretations are both accurate and reliable. In the study, the variables to be used in the empirical analysis section, their abbreviations, and the sources from which they were obtained are presented in Table 1.

Variables, Their Abbreviations, and the Sources.

Note. Lagged inflation considered as lagged annual inflation in Equation 2.

For this purpose, we broaden the scope of the formerly estimated Phillips curve models pertinent to Turkey (referencing Koca and Yılmaz (2018), and Koç et al. (2021) by integrating the surveyed inflation expectations into our model. In the initial segment, we proceed to determine the subsequent specification for inflation:

Equation 1 illustrates the dynamics of inflation, where

In the situation where technology provides the data and all factors of production are used, the output gap, which is the monetary definition of the maximum level of goods and services produced, is calculated considering the potential (full employment) GDP as expressed by Baumol and Blinder (1985) in Equation 2.

In Equation 2, the potential GDP represents the real GDP when the unemployment rate is equal to the natural rate of unemployment. In this context, if real GDP is less than potential GDP, an output gap occurs. Instead of using absolute values, the output gap is expressed in relative terms as in Equation 3 (Akıncı et al., 2016, p. 28).

To balance output, one must have access to real and potential GDP data. In this context, GDP values obtained using the Expenditure method are taken, and the output balance is calculated using the Hodrick-Prescott Filter method. Because of its smoothing assumption, this method minimizes the deviation of the output gap and is taken into consideration in the output gap variable. The equation also includes two more variables aimed at encompassing the effects of exogenous elements.

Differing from the study by Koç et al. (2021), our analysis includes the rigidity of wages, (

The results derived from the estimation of Equation 1 can be observed in Table 2. Initially, the model incorporates a prospective component, whereby prevailing inflation is shaped by anticipated future inflation. There’s a likelihood that the data set employed to formulate inflation expectations encompasses real inflation fluctuations, thus giving rise to a familiar endogeneity problem that needs to be contemplated while employing survey metrics. A few research endeavors have posited that survey expectations are predetermined and have utilized Ordinary Least Squares (OLS) in their estimations. The Equation 2 modeling the change in 1-year-ahead annual inflation expectations is inspired by the findings of Bems et al. (2018) and Koç et al. (2021). For the instances based on the empirical model of Koç et al. (2021) that rely on the “feedback survey” conducted by the CBRT on the participants of the Survey of Expectations, in our model, the FED’s revision reports related to inflation expectations have been considered.

Estimations of the Inflation Formation With OLS and Alternatives (Dependent Variable:

Note. LVIE means the lagged values of inflation expectations. LVIE+target + Revisions includes LVIE + inflation target, target revision, FED’s inflation forecast revision, and lagged values of inflation surprise. Part of Simultaneous in Table 2 presents the estimates of the inflation equation where Equations 1 and 2 are simultaneously estimated. Dummy variables denote the 2008 Global crisis and 2019 covid pandemic. In the models applied to diagnostic results, the Breusch-Godfrey LM Test indicates that there is no autocorrelation problem. Similarly, the ARCH LM Test suggests that there is no issue with changing variances. The Jarque-Bera Normality test indicates that the error term follows a normal distribution, and the Ramsey Reset test suggests that there are no model specification errors. * (1%), **(5%), ***(10%) represent levels of significance.

For this purpose, to analyze the dynamics of inflation expectations formation and to simultaneously estimate Equation 1 and Equation 2 together, we formulate Equation 2 which models the change in 1-year-ahead annual inflation expectations.

Equation 4 is constructed based on the Survey of Consumer Expectations conducted by the Federal Reserve (FED), which asks participants to specify the degree of importance they attach to certain variables when forming their inflation expectations. It has been added to Equation 4 because gold prices and the real exchange rate are variables that consumers directly focus on in their inflation expectations.

In Equation 4

In Table 2, aside from OLS, estimations are seen to have been performed in three different columns. The point to note here is the use of lagged values of inflation expectations as instruments. After analyzing the data, it’s clear that the conclusions from the three columns, excluding the OLS, align with the OLS outcomes.

Taking this context into account, we begin with the assumption of exogenous inflation, and the first column displays the OLS estimation results. According to this, the output gap, exchange rate, import prices, and real unit labor cost have a positive impact on inflation. Additionally, there is a significant coefficient for inflation expectations. A 1% higher inflation expectation for the next 12 months is associated with 0.30 points higher annualized quarterly inflation. The other independent variables associated with CPI are observed to increase CPI in both OLS and alternative columns. This situation indicates that the Phillips curve is theoretically supported in the reduced form. Considering the possible endogeneity between inflation expectations and inflation, in the first three columns of Table 1, we present a series of instrumental variable regressions for inflation expectations using different instrument sets. LVIE stands for the lagged values of inflation expectations. LVIE+Target+Revisions includes LVIE and incorporates the inflation target, target revision, central bank’s inflation forecast revision, and lagged values of inflation surprises. The Simultaneous section in Table 2 provides the estimates of the inflation equation where Equations 1 and 2 are simultaneously estimated. The IV estimation results presented in Table 2 largely confirm the OLS results, with inflation expectations still having a significant coefficient of 0.40. Columns 2 and 3 in Table 2 largely confirm the inflation expectation results from OLS, showing that inflation expectations still have a significant coefficient of 0.40.

The results of OLS and simultaneous equation models can be observed in Table 3. For dependent variables, as well as the price of gold per ounce and the quarterly percentage fluctuation in the Brent crude oil price have a significant impact on inflation expectations. We see that both past inflation and inflation surprise have a sizeable impact on expectations, forming the backward portion of inflation formation. Besides, there is a positive association between inflation expectations and the central bank’s forecast revisions, which might indicate the potential role of forward-looking components in expectations. Furthermore, there exists a positive correlation between inflation expectations and revisions in the central bank’s forecasts, possibly suggesting the influence of forward-looking elements in expectations.

Inflation Expectation Formation (Dependent Variable:

Note. In the models applied to diagnostic results, the Breusch-Godfrey LM Test indicates that there is no autocorrelation problem. Similarly, the ARCH LM Test suggests that there is no issue with changing variances. The Jarque-Bera Normality test indicates that the error term follows a normal distribution, and the Ramsey Reset test suggests that there are no model specification errors. *(1%), **(5%), ***(10%) represent levels of significance.

Time-varying parameter model estimations refer to statistical models in which the parameters (coefficients) of a model are allowed to change over time. These models are used in various fields, including economics, finance, and engineering, to account for the fact that relationships between variables may not remain constant but evolve over different periods. In these models, the parameters are treated as functions of time, and their values are estimated for different time intervals or periods. This allows analysts to capture changing dynamics and relationships within data. Time-varying parameter models are also known as dynamic regression models, state-space models, or time series models with time-varying coefficients.

These models are particularly useful when dealing with data where the underlying relationships may change due to economic conditions, policy changes, seasonality, or other factors. By allowing parameters to vary over time, analysts can better understand and predict how variables influence each other in a changing environment.

In addition, time-varying parameter versions of Equations 1 and 2 have been estimated simultaneously.

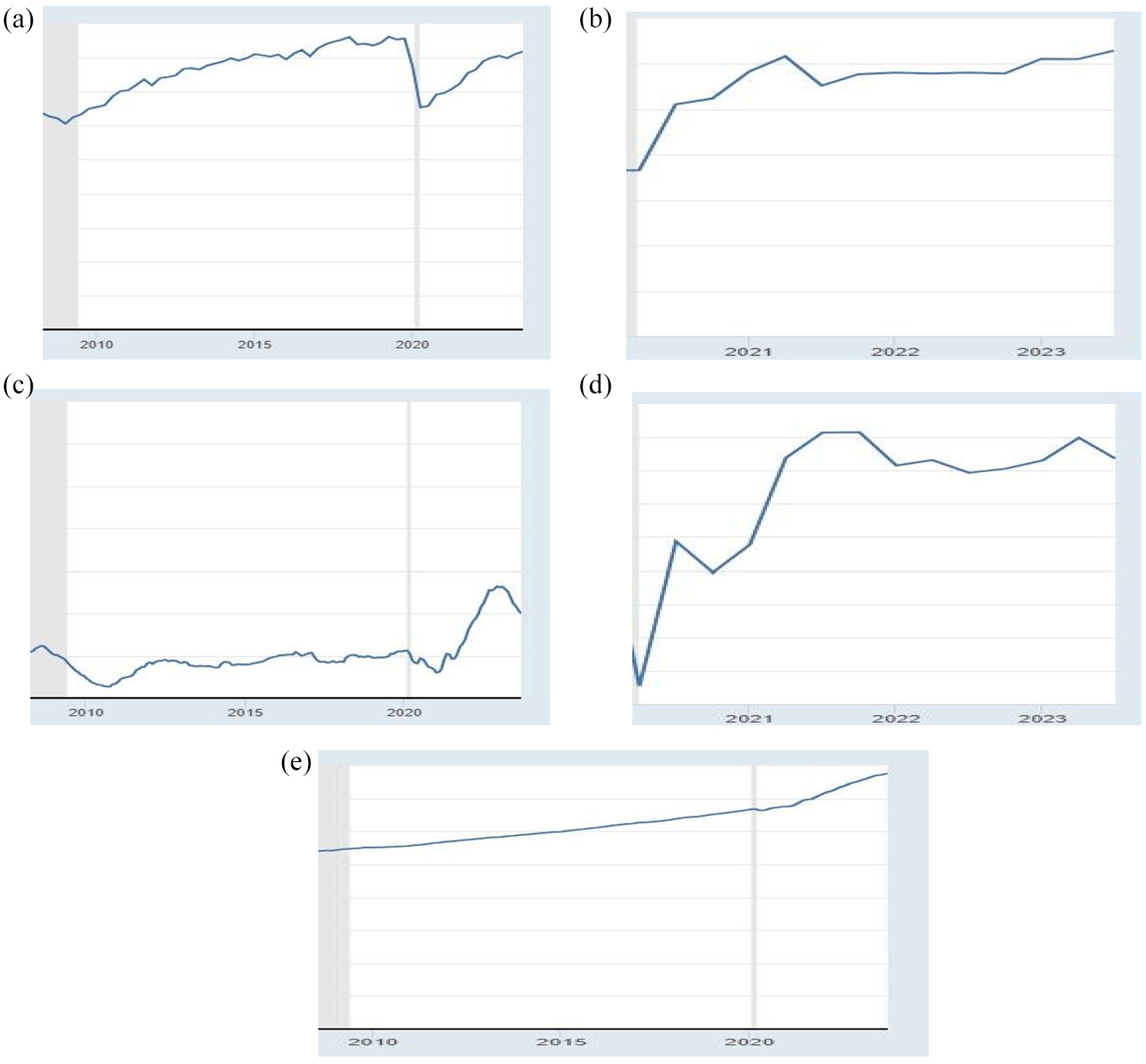

In the study aimed at analyzing the role of inflation expectations, the coefficient measuring the sensitivity of inflation-to-inflation expectations indicates that expectations play a significant role in inflation dynamics, fluctuating around 0.38, as seen in Figure 2a. Additionally, the impact of the Covid pandemic can be clearly observed in the graph, with volatility reaching up to around 40%. The conclusion drawn from this is that there has been a negative evolution in the inflation expectations of participants in the expectation survey after the pandemic. The coefficient measuring the impact of past inflation on current inflation, although it crossed the threshold value of 3% in 2010 and 2015, has not exhibited a stable pattern. Particularly noteworthy is the sharp increase after 2020, attributed to the 2020 U.S. presidential election and the impact of the Covid pandemic. It should be noted that Federal Reserve Chairman Powell’s characterization of post-pandemic inflation as temporary also played a role in this context.

Time-Varying Parameter Estimates of Table 1 (Inflation Formation): (a) coefficient of inflation expectations (%), (b) coefficient of lagged inflation, (c) exchange rate pass-through (long run), (d) import price pass-through (in $ terms, long run), (e)output gap, and (f) real unit wage.

The exchange rate is often regarded as a key determinant of inflation in many economies. Looking at Figure 2c the exchange rate, which showed a relatively constant trend at the level of 0.4 coefficients until 2021, has experienced a significant increase recently, likely influenced by recent developments, including the COVID-19 pandemic and the Russia-Ukraine conflict. This suggests that both simultaneous and lagged values of the exchange rate basket are included in time-varying analyses, guiding the dimension and duration of exchange rate pass-through to local prices. Especially with the depreciation of the dollar, it can be observed that it reached a coefficient of 0.50 in recent times. Notably, in Figure 2d, the pass-through effect of export prices appears to be the same as the exchange rate pass-through effect. The recent coefficient estimates indicate that the long-term pass-through of import prices to inflation is approximately around 25%. The estimates also suggest that the weakening began after the global financial crisis and continued at a moderate pace thereafter. Looking at the coefficient estimates for the output gap (Figure 2e) and the real unit labor cost (Figure 2e), the short-term coefficient of the output gap has generally remained stable, showing a slight upward trend after 2020. According to the figure, the coefficient of the output gap in the long run is estimated to be around 0.50. This suggests roughly a 0.5 percentage point increase (decrease) in annual inflation when the output gap is one percentage point higher (lower). Lastly, the coefficient of the real unit labor cost suggests that a 1 percentage point shock to this variable leads to a 0.55 percentage point increase in annual inflation in the long run.

Graph 2: Time-Varying Parameter Estimates of Table 2 (Expectation Formation)

Moving beyond the specific findings, it’s crucial to highlight the significance of time-varying parameter models. These statistical models are designed to accommodate the evolving nature of relationships between variables. In various domains, including economics, finance, and engineering, these models prove invaluable when dealing with data where relationships are subject to change due to factors like economic conditions, policy shifts, or seasonality.

In essence, time-varying parameter models treat the model’s coefficients as functions of time, enabling the estimation of parameter values for distinct time intervals or periods. By doing so, these models empower analysts to capture the evolving dynamics and relationships within data. Termed as dynamic regression models, state-space models, or time series models with time-varying coefficients, they serve as essential tools for understanding and predicting how variables interact within a dynamic and ever-changing environment. Expected future inflation directly affects existing inflation. In this regard, understanding the mechanism underlying inflation expectations is one of the most important elements in combating inflation. Many studies and reports by the Federal Reserve suggest that inflation, revisions in the central bank’s forecasts, exchange rate fluctuations, supply shocks such as oil prices, changes in inflation targets, and participants’ own inflation forecast errors are key factors affecting inflation expectations.

The results obtained in Figure 3a show that, starting from 2010, economic actors increased the weight they gave to past inflation in their expectations, and this weight decreased significantly during the Covid Pandemic. In the post-epidemic period, pre-epidemic periods have been reached. While sensitivity decreased with the falling demand, especially during the epidemic period, the booming demand after the epidemic increased sensitivity. The significance given to established inflation targets when setting expectations has remained consistent over time, likely because the targets themselves have exhibited minimal variation within the observed period (Figure 3b). The relationship between inflation expectations and the revisions in inflation forecasts by the FED increased until the end of 2021 and then displayed a stable image (Figure 3c). Estimates also show that the impact of oil prices on the formation of inflation expectations is high and that its power has increased over time, especially since the epidemic period.

Time-varying parameter estimates of inflation expectations: (a)change in 1-year-ahead annual inflation expectations, (b) formal inflation target, (c)four-quarter-ahead inflation forecast revisions, (d) Brent crude oil price ($), and (e) gold price.

Conclusion

Inflation has become a significant concern for the U.S. economy in the aftermath of the Covid-19 pandemic. Particularly, the Federal Reserve’s statements asserting that inflation is transitory and its delayed interest rate hikes have contributed to the deepening of the inflation problem. At this juncture, this issue, which is not only specific to the United States but a global concern, has brought discussions related to inflation back into the spotlight. In recent times, especially in academic circles, it has been argued that inflation expectations have gained a more prominent role in the dynamics of inflation, given the recent surge in inflation affecting the entire world.

Despite the comprehensive analysis presented in this study, several limitations must be acknowledged. First, the reliance on survey-based inflation expectations, while widely used, is subject to measurement errors and potential biases inherent in self-reported data. These limitations could affect the accuracy of the results, particularly when dealing with forward-looking variables. Additionally, the study’s use of historical data is constrained by the availability and consistency of the data sources, especially during periods of significant economic volatility like the COVID-19 pandemic.

Another limitation lies in the assumption of exogenous inflation. While this approach simplifies the model and provides clearer insights into the relationship between inflation expectations and other macroeconomic variables, it may not fully capture the complexities and feedback loops present in inflation dynamics. Moreover, the interaction between inflation expectations and external factors such as oil prices and exchange rates, while significant, is highly context-dependent. The results may not be fully generalizable to different economic conditions or geographic regions beyond the U.S.

Finally, although the econometric techniques employed, such as OLS and instrumental variable regressions, are robust, the potential for multicollinearity and endogeneity remains a concern. While these issues were addressed through the use of alternative specifications and diagnostic tests, further refinement and alternative models could enhance the precision of the findings. Future research could benefit from incorporating more dynamic models, such as time-varying parameter models, to better capture shifts in inflation expectations over time.

Despite these limitations, the study offers valuable insights into the critical role of inflation expectations in shaping inflation outcomes, particularly in periods of economic uncertainty.

Taking this argument into account, this article examines the interaction between inflation and survey-based inflation expectations and questions whether there have been any changes in the recent dynamics. In the formation of inflation in the American economy, inflationary expectations play a crucial role. According to our empirical analysis, In light of this context, we initiate our analysis by assuming exogenous inflation. According to these findings, the output gap, exchange rate, import prices, and real unit labor cost all exert a positive influence on inflation. Furthermore, there is a noteworthy coefficient assigned to inflation expectations. Specifically, a 1% increase in inflation expectations for the next 12 months is associated with a 0.30-point rise in the annualized quarterly inflation rate.

Additionally, the remaining independent variables linked to the Consumer Price Index (CPI) demonstrate an upward push on CPI, which holds true across both the OLS and alternative estimation columns. This observation lends support to the theoretical underpinnings of the Phillips curve in its reduced form.

Considering the potential endogeneity between inflation expectations and inflation, we present a series of instrumental variable regressions for inflation expectations using different sets of instruments in the initial three columns of Table 1. Here, LVIE represents lagged values of inflation expectations, whereas LVIE+Target+Revisions incorporates LVIE alongside variables like the inflation target, target revision, central bank’s inflation forecast revision, and lagged values of inflation surprises. In the case of the dependent variables, we observe that both the price of gold per ounce and the quarterly percentage fluctuation in the Brent crude oil price exert a noteworthy and statistically significant influence on inflation expectations. This suggests that external factors such as these commodities play a pivotal role in shaping inflation expectations.

Furthermore, our analysis reveals that past inflation and inflation surprises wield a substantial impact on expectations, representing the historical aspect of inflation formation. Additionally, a positive association emerges between inflation expectations and revisions in the central bank’s forecasts, indicating the potential influence of forward-looking components in shaping expectations. The positive correlation between inflation expectations and central bank forecast revisions underscores the presence of forward-looking elements at play in expectation formation. Especially during the pandemic period, sensitivity decreased with the falling demand, while the booming demand after the pandemic increased sensitivity. The importance given to inflation targets when determining expectations has remained consistent over time, likely because the targets themselves exhibited minimal changes within the observed period. The relationship between inflation expectations and revisions in FED’s inflation forecasts increased until the end of 2021 and then displayed a stable outlook. The estimates also indicate that the impact of oil prices on the formation of inflation expectations is significant and has particularly strengthened since the pandemic period. In general, our findings indicate that inflation expectations and the dynamics underlying these expectations are among the leading drivers of inflation in the United States. Additionally, inflation expectations and the exchange rate interact with each other, creating a feedback mechanism that amplifies their impact on inflation. Therefore, any policy measures aimed at managing inflation expectations and expected value depreciation are indispensable for achieving successful inflation stability.

Footnotes

Ethical Considerations

This study has been prepared in accordance with the rules of scientific research and publication ethics.

Author Contributions

Utku Altunöz (100%).

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.