Abstract

This paper aims to theoretically and empirically test whether the Weather Index Insurance for Mutton Sheep (WIMS) which protects the herders from increased feeding costs resulting from drought and snow disasters promotes the income of herders in China’s Inner Mongolia or not. We have applied the OLS, PSM, and quantile regression models using field survey data from 261 herders in Xilin Gol, Inner Mongolia Autonomous Region for our objective. The findings demonstrate that the WIMS significantly increases the overall and high-income herders’ income, but has no significant effect on herders’ income at other income levels.. According to the results, we recommend that as the subsidized agricultural insurance product, the government should expand the pilot region of WIMS to furtherly test its income effect and consider reducing or exempting insurance premiums for low-income herders to reduce their financial pressure.

Since the World Trade Organization (WTO) confirmed that agricultural insurance has relatively fewer trade-distorting effects, many developing countries have successfully adopted it as one of the essential means to stabilize farmers’ income and encouraged them to participate through premium subsidies (Fadhliani et al., 2019; Glauber, 2016; Yu & Sumner, 2018). In 2007, China initiated a pilot project for agricultural insurance; and the government has regarded agricultural insurance as an essential and effective tool for rural stability and agricultural development. In 2019, the number of farmers covered by agricultural insurance reached 180 million in China. From 2008 to 2019, more than 240 billion yuan was paid to 360 million farmers as compensation. The agricultural insurance covers about 270 varieties of crops, which encompass the bulk agricultural products related to livelihoods and food security in China (Guo et al., 2021). As an effective risk management tool, agricultural insurance can alleviate farmers’ natural disasters and market risks, which could transform farmers’ production behavior and structure, thereby maintaining and increasing their income. Additionally, agricultural insurance is also of great significance to the development of the rural economy in China (Guo et al., 2021; Yin, 2015). Therefore, the “added value” of agricultural insurance, namely the income effect, has became one of the research hotspots in this field.

Due to the lack of professional risk management tools for a long time, the weather variety-induced natural disasters such as drought and snow pose a severe threat to herders’ livelihoods in Inner Mongolia, China. In 2019, the weather insurance for mutton sheep (WIMS) was implemented as a pilot project in 11 county regions of Xilin Gol League, Inner Mongolia, China and was formally included in the “Insurance Award and Subsidy for Local Advantageous and Special Agricultural Products” and “government-subsidized agricultural insurance product” projects by the Ministry of Finance of China and the Inner Mongolia government. That means a portion of the premium for the WIMS is subsidized by the government, and the insured herdsmen only need to pay a smaller proportion of the premium. The WIMS is a brand-new insurance product that directly hedges the increased production cost risk of herders induced by natural disasters (drought and snow). Its essential characteristics are quite different from other traditional agricultural insurance. Therefore, its impact on the income of herders is also different.

There are so many studies that analyze the impact of agricultural insurance on farmers’ income based on the macro panel or micro survey data. According to some studies, agricultural insurance can affect the net agricultural income of farmers to a certain extent (Agbenyo et al., 2022; Deng, 2005; Giné et al., 2007; Ji, 2006; Y. R. Li & Wang, 2022; Liang et al., 2008; Nie & Holly, 2011; Yang & Zhou, 2010; Z. X. Zhang et al., 2018). But some scholars concluded that the agricultural insurance can’t play a role in increasing farmer’s income due to the imperfect agricultural insurance system, chaotic compensation, and “low insurance and wide coverage” (X. A. Chen, 2013; Gao, 2008; Zhao et al., 2016; Zhu & Tao, 2015). The existed researches on agricultural insurance’s income effect has three apparent characteristics. First, most of the studies have similar research objectives, such as studying yields and income-based agricultural insurance products which only cover part of the materialized cost; Second, most of the studies have similar research contents such as the effect of agricultural insurance on the overall farmer income; Third, the conclusions are inconsistent, specifically that agricultural insurance has (significantly or insignificantly) positive or negative effects on farmers’ income.

In this paper, we construct the impact path of WIMS on herders’ income by studying the relevant theory and insurance clause. According to our field research data of Xilin Gol League, the herder’s income effect of WIMS is empirically tested to identify whether this new agricultural insurance product can increase herders’ income and whether its policy effect covers the primary beneficiary of herders. To our knowledge, this article is an rare empirical analysis which focus on the income effect of grassland animal husbandry weather index insurance by using micro herders filed survey data. Our results could fill the research gap for the study of grassland animal husbandry insurance and propose some suggestions for improving this insurance product.

Theory and Verbal Analysis

Theoretical Analysis

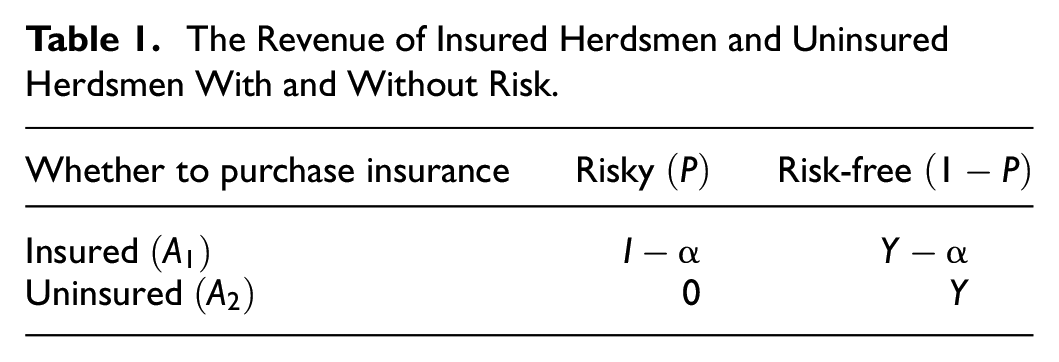

Based on previous studies (Agbenyo et al., 2022; Bhuiyan et al., 2022; Chai, 2014), this paper conducts the theoretical analysis. The theoretical analysis needs to satisfy the following assumptions. First, herders face only two possible natural states in the production and management of grassland animal husbandry, which are the risk state and the risk-free state. Among them, the probability of risk occurrence is

The herders must make two decisions, purchasing an insurance product (insured) and not (uninsured). The herdsmen who purchase the insurance are required to pay the premium

The Revenue of Insured Herdsmen and Uninsured Herdsmen With and Without Risk.

According to the above table, the expected revenue and expected revenue variance of insured herdsman and uninsured herdsman can be calculated respectively:

Formulas (1) and (2) are the expected revenue for insured and uninsured herders, respectively. In formula (1),

From formulas (3) and (4), it can be found that

According to the above theoretical analysis, it can be found that the WIMS with government premium subsidy can effectively disperse the production and management risks of herders. Although the herdsman needs to pay a part of the premium to participate in the insurance, the insurance policy can provide some compensation for the insured herder when the risk occurs. Furthermore, the government premium subsidy further amplifies this compensation effect. On the one hand, government subsidies potentially boost herders’ income; On the other hand, this can incentivize herders to participate in insurance policies, thereby reducing the volatility of herders’ income.

Verbal Analysis of Income Effect for WIMS

Before analyzing the mechanism of the herders’ income effect of WIMS, it is necessary to understand its characteristics. Although the WIMS covers a whole year, it has two separate sub-insurance intervals based on periods of drought and snow. According to our survey results, about 66% of interviewed herdsmen considered the natural risk situation in the region to be “relatively high” or “very high.” Among them, nearly 95% of herders believe that drought is the primary natural disaster faced by the region. Therefore, the mechanism analysis in this paper takes drought risk as our case for the introduction.

It should be clear that the WIMS hedges the risk of increased forage costs caused by the change in herders’ production behavior (from grassland grazing to sheds feeding or semi sheds feeding) induced by natural disasters(drought and snow). The WIMS utilizes the water deficit degree

where,

The core problem in the WIMS is the rationality of insurance amount, which means whether the feeding cost of 2 yuan per day could indemnify the loss induced by the disaster. Our survey questionnaire involves questions such as the actual number of days of mutton sheep in sheds in a year, the amount of forage consumed per day in the sheds, and the price of forage. According to our survey results, the basis dam’s average daily consumption of forage in sheds is 1.7 kilograms, and the price of forage will be 0.96 yuan per kilogram in 2020. The daily forage cost per adult mutton sheep in sheds is 1.632 yuan per day. Therefore, the insurance clause’s feeding cost of 2 yuan per day covers the actual cost of forage.

Based on the above theoretical and mechanism analysis, the research hypothesis is put forward:

H: the WIMS has a positive effect on herders’ income.

Data Source, Variable Description, and Model Setting

Data Sources and Variable Descriptive Statistics

In China, the grassland area covers approximately 400 million hectares, and Inner Mongolian grassland ranks 2nd (X. Li & Hou, 2019). Due to the large grassland area and the small population, the herders locate in extremely scattering, which poses a great challenge for us obtaining the sample. The data is collected from a field survey conducted by the research team in six counties of Xilin Gol League. The research sites are Xilinhot, Dong Ujimqin, Xi Ujimqin, Abaga, Sonid Right Banner and Boarder Yellow Banner. The final number of valid questionnaires is 261, including 127 insured herders and 134 uninsured herdsmen.

This paper mainly examines the herders’ income effect of WIMS. The “personal disposable income” and “per capita net income” are two indicators related to income level of farmers (Zong et al., 2014). According to the information from the field survey, the main source of income for herders in Xilin Gol League is the sale of livestock. Out of 261 surveyed households, only three households have wage or property income. Thereby the explained variable in this study is the household per capita income from animal husbandry. The core explanatory variable is whether the herders purchase the WIMS, which is a binary dummy variable, purchase denoting 1 and otherwise 0. At the same time, herders’ income is also affected by other factors. Due to the lack of research on the impact of agricultural insurance on the income of herdsmen, the selection of control variables in this paper refers to relevant research on the impact of income of herders (L. Hou et al., 2021; Shao et al., 2020; Tang et al., 2022; J. Zhang et al., 2019). Therefore, the following control variables are added to the empirical analysis: age, education level, grazing time, household labor force, distance from the nearest township, breeding scale, shed area, housing area and vehicle number. The specific variable definition and descriptive statistics are shown in the following table.

Table 2 presents the descriptive statistics and definitions of variables. The average value of the surveyed herders’ net animal husbandry income per person is 75,600 yuan, with a minimum value of 1,400 yuan and a maximum value of 558,800 yuan. Nearly 50% of interviewed herders in this survey chose to purchase the WIMS. The mean age of interviewed herders is 48 years old, and the average education year is 8.89 years. The average labor force is about two people. The average breeding scale is 5,100 sheep. The average shed and housing occupancies are 340 and 151 square meters, respectively.

The Definition of Variable and Descriptive Statistics.

Table 3 shows that the t-test results of the characteristics of insured herdsmen and uninsured herdsmen are the difference between each variable. According to the single-sample t-test results, there are significant differences between insured herdsmen and uninsured herdsmen in household per capita income from animal husbandry, education level, breeding scale, shed area and housing area. The differences in other variables are not significant.

The Comparison of Characteristics Between Insured and Uninsured Herdsman.

, **, and *** represents the significance levels of 10%, 5%, and 1%, respectively.

Model Setting

According to the divergence of previous scholars’ research results on the income effect of agricultural insurance, the impact of agricultural insurance on farmers’ income is highly complex. Only analyzing the income effect of farmers under the conditional mean but ignoring the income situation at the top and tail of the income distribution will lead to the heterogeneity of results (J. Hou et al., 2018). In our empirical part, the ordinary least square (OLS) is firstly used to test the overall effect of the WIMS on herdsmen’s income. Subsequently, the quantile regression method is introduced to identify the income effect of WIMS on the herders at different income scales based on the conditional distribution of herders’ income. Koenker and Bassett proposed the quantile regression in 1978. They advocated using a weighted average of the absolute values of the residuals as the objective function for minimization, which was less susceptible to extreme values. The classical “mean regression” of OLS is extremely susceptible to extreme values because the objective function of minimization in OLS is the sum of squares of residuals. With relatively robust results, quantile regression can provide comprehensive information about conditional distribution (Q. Chen, 2010).

However, traditional regression methods, such as OLS, may exhibit “self-selection” behavior in the test of the effect of WIMS on herders’ income. (For instance, the larger the scale of herders, the greater the propensity to buy weather index insurance. Moreover, insurance companies prefer large-scale farmers). In this case, the selection bias problem could arise. The solution to the sample self-selection problem is the instrumental variable method or the Heckman two-stage model, which has relatively strong assumptions and constraints. In contrast, the assumptions of property score matching (PSM) are easier to satisfy. (In more detail, the two basic assumptions PSM must satisfy are the conditional independence assumption and the expected support assumption.)

In summary, this paper applies the PSM model to further test WIMS’ overall effect on herders the initially OLS identified. The impact of WIMS on herdsmen with different scale incomes is examined through quantile regression. The specific model settings are as follows:

Ordinary Least Square (OLS)

To examine the effect of the WIMS on the overall income of herdsmen, the following multiple linear regression model is established:

where, Y is the explained variable, which is the household per capita income from animal husbandry. X is the core explanatory variable, representing whether the herdsmen purchase WIMS. As a binary dummy variable, it is assigned a value of 1 when it is purchased and a value of 0 when it is not purchased.

Propensity Score Matching (PSM)

The specific steps of using the PSM method are as follows. Firstly, Logit selection model is built to calculate the probability

where,

Secondly, for each herdsman

where,

Finally, the matching methods used in the PSM are nearest neighbor matching, radius matching and kernel matching.

Quantile Regression Model

The quantile regression model not only broadens the assumption of the independent distribution of random error terms in sample mean regression but also describes the conditional distribution in detail to explore further the difference in the effect of mutton sheep weather index insurance on herders income of different income scales.

Analysis of Empirical Results

OLS Regression Model Results

The estimation results of the OLS regression model are shown in Table 4. In the regression results, the core explanatory variable, the purchase of WIMS by herders, has a significant positive effect on herders’ income at the 10% significance level. Therefore, it can be concluded that purchasing insurance can significantly increase the household per capita income from animal husbandry.

The OLS Regression Results.

Note. The values in parentheses are t values.

*, **, and *** represent the significance levels of 10%, 5%, and 1%, respectively.

Age, labor force, breeding scale, housing area, and vehicle number significantly affect herders’ income among the control variables. The portion of results are consistent with the previous studies (Agbenyo et al., 2022; L. Hou et al., 2021; Y. R. Li & Wang, 2022; Shao et al., 2020; Tang et al., 2022; J. Zhang et al., 2019). In more detail, the older, having a large household labor force, the breeding scale, housing area, and more vehicles, farmers have higher net animal husbandry income. It is quite acceptable as older herders may have rich grazing experience and are more familiar with feeding techniques, risk management and market regulation. The more household labor show the more labor force is put into production of animal husbandry, which is conducive to increased income. Driven by market interests and the rising price of sheep and beef in recent years, herders’ current farming scale and enthusiasm are higher than in previous years. Under the premise of controlling price factors, the increase in feeding scale and output will inevitably increase herders’ income. In order to avoid multicollinearity among explanatory variables, we conducted VIF test on the explanatory variables. The results show that the mean value of VIF is 1.54, which is less than 2, and all the VIF value is not greater than 10, indicating that there is no multicollinearity among the explanatory variables.

But this result is not reliable due to the selection bias. Therefore, we employ the PSM for further testing.

PSM Estimation Results

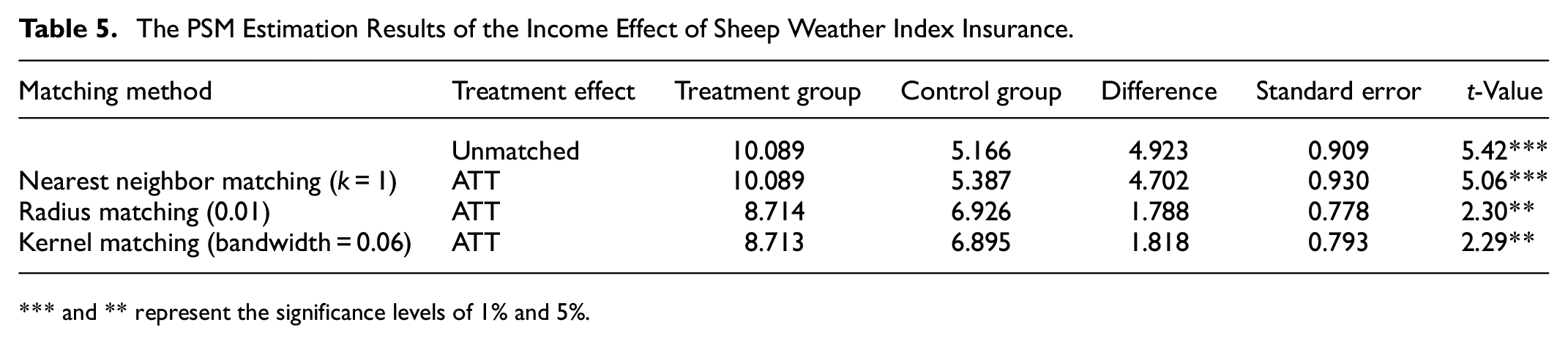

Table 5 shows the results of the income effect of WIMS obtained after propensity score matching on the data. It can be found that the treatment group ATT obtained by nearest neighbor matching, radius matching and kernel matching are all significant at the 5% and 1% levels. Among them, nearest neighbor matching selects k = 1, namely, one-to-one matching. The radius value of radius matching is 0.01. Kernel matching uses the default kernel function of Stata software and a bandwidth of 0.06. The results obtained by the three matching methods are similar, reflecting the robustness of the matching results to a certain extent (Xu et al., 2020). In addition, the matching results are consistent with the OLS estimates, further illustrating that the WIMS significantly impacts herders’ income.

The PSM Estimation Results of the Income Effect of Sheep Weather Index Insurance.

and ** represent the significance levels of 1% and 5%.

To further test the robustness of the PSM estimation results, the estimation is re-conducted by Mahalanobis match. The specific results are shown in Table 6.

The Mahalanobis Match Estimation Results of the Income Effect of Sheep Weather Index Insurance.

represent the significance levels of 1%.

The result of the above table indicates that the matching results are similar to another three matching methods which shows the stability of the results.

Quantile Regression Model Results

Based on the existing quantile regression model application research (C. S. Li & Zhang, 2015; Wen et al., 2015), 0.1, 0.25, 0.5, 0.75, and 0.9 quantiles are selected to distinguish different herder’s income levels (very low-income group, low-income group, middle-income group, high-income group, and very high-income group). The specific regression results are shown in Table 7.

The Quantile Regression Results.

Note. The values in parentheses are t values.

, **, and *** represent the significance levels of 10%, 5%, and 1%, respectively.

According to the results, the insurance adoption is significant at 0.75 quantile among the 0.1, 0.25, 0.5, 0.75, 0.9 quantile. It shows that the WIMS significantly affects high-income herders’ income. None of the other quantiles passes the significance test. At 0.1 quantile, the effect of WIMS on very low-income herders’ income is insignificant and it should be noted that the sign of the coefficient is negative, which may result from the fact that the premium of the WIMS imposes a certain burden on very low-income herders and affects their income.

Conclusions and Policy Recommendations

This study tries to identify the herders’ income effect of the WIMS. The hypothesis is put forward through theoretical and mechanism analysis: the WIMS positively impacts herders’ income. Based on field data at Xilin Gol League, OLS and PSM are used to test our hypotheses. The results show that the WIMS significantly positively impacts herders’ income. The impact of the WIMS on herdsmen’s income at different income levels is explored through the quantile regression model. According to the model regression results, the WIMS only has a positive effect on the income of high-income herders but no significant effect on herders’ income at other income levels. It should be noted that farmers need to pay part of the premium for purchasing the WIMS. Therefore, the WIMS may have a negative impact on the income of very low-income herders. Since the grassland in Xilin Gol League has all grassland types, and the sample collection area in this paper also covers almost Xilin Gol League. If the WIMS is extended to Inner Mongolia and even other pastoral areas in China, while ensuring the scientific and reasonable insurance clause, the research conclusion of this article also has a certain degree of credibility in other grassland area. But limited sample size may have a certain impact on the empirical results of this article. In the future, with the continuous development of WIMS, we could use the advanced causal analysis methods to further analyze its income effect for herders.

Based on the results, we put forward some suggestions for promoting the operation and improving the systems of the WIMS. Firstly, the WIMS policy should be piloted in other pastoral areas to further test its income effect on herders. Secondly, the WIMS has now obtained the “local characteristic agricultural insurance incentive and subsidy policy” issued by the Ministry of Finance. On the one hand, the WIMS is implemented in counties with relatively poor financial conditions which their income source is mainly from grassland animal husbandry. Therefore, an appropriate reduction in the county government’s premium subsidy proportion can ease the financial pressure on them. On the other hand, reducing or exempting insurance premiums for very low-income herders can avoid the living burden caused by insurance premiums to such herders. Through the above methods, the policy effect of the WIMS can be truly implemented.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by National Natural Science Foundation of China [71863028 & 72173069 & 72163026], and Fujian Provincial Natural Science Foundation Youth Project [2023J05217], and Directly Affiliated University Basic Scientific Research Operating Expenses Project [BR221316, BR221042], Key Research Base for Humanities and Social Sciences in Universities “Agricultural and Pastoral Risk Management Research Base”.

Data Availability Statement

Data will be provided on the request.