Abstract

Internet infrastructure has gradually become a driving force for foreign investment in the digital age, but it also brings about risks for the digital divide. This study innovatively investigates how Internet infrastructure has influenced foreign investment inequality across 30 provinces in China. It also explores pathways to reduce the foreign investment inequality within the digital divide. The digital divide is also introduced innovatively with matrix form across the econometric model. Results provide that Internet infrastructure reduces the inequality of foreign investment inflows at the national level. Further, Internet infrastructure makes foreign investment the convergence effect in Chinese eastern provinces but broadens the foreign investment gap in mid-western provinces. As for provinces with well-developed foreign trade regimes, Internet infrastructure reduces foreign investment inequality. Thus, given the reality of the digital divide, improving access to transportation and finance can significantly reduce inequality in foreign investment.

Plain language summary

This study examines the relationship between internet infrastructure and foreign investment inequality across 30 provinces in China. It further explores strategies to narrow foreign investment inequality within the digital divide. The results indicate that internet infrastructure can reduce foreign investment inequality across the entire economy, after a series of endogeneity and robustness tests. Our grouped regression model, which categorizes provinces based on geographical factors and trade policies, indicating heterogeneity in the impact of internet infrastructure on foreign investment inequality. In addition, policies targeting financial and transportation infrastructure are recommended as effective measures to mitigate foreign investment inequality within the inevitable digital divide.

Introduction

Amid the tide of economic globalization, China and other emerging market nations ardently vie for foreign direct investment (FDI) inflow. Not only can FDI serve as a direct contributor to Chinese economic expansion by unleashing considerable potential, but it also plays a constructive role in alleviating employment pressures, optimizing the industrial structure, and diversifying trade channels (Borensztein et al., 1998; Dhrifi et al., 2020; Javorcik, 2004; Sun et al., 2019). While experiencing rapid growth, foreign capital exhibits uneven distribution and polarization due to regional endowment differences such as open policies, economic levels, and infrastructure. The imbalance of foreign capital inflows leads to the imbalance of advanced production factor allocation, further exacerbating the uneven distribution of innovative technology, investment, and labor factors among regions. This “Matthew effect” hinders economic exchanges between underdeveloped and developed regions.

Meanwhile, the Chinese continually improving network facilities and its substantial digital marketplace are increasingly alluring prospects for foreign investors. In June 2024, the number of Internet users in China reached 1.097 billion, with an Internet penetration rate of 75.64%. Stable Internet infrastructure is conducive to reducing investment risks for external investors caused by discrepancies between reality and expectations (Götz & Jankowska, 2022). Factors such as artificial intelligence and 5G communication, representing production elements, are gradually weakening the location selection of traditional factors such as land and labor for foreign investment. With the deepening impact of Internet infrastructure on international capital flows, an increasing amount of foreign investment is inclined to flow into regions with developed digital infrastructure (Paul et al., 2023). In the context of opening up to the outside world, the disadvantage of digital facilities in attracting foreign investment in central and western regions is gradually becoming apparent.

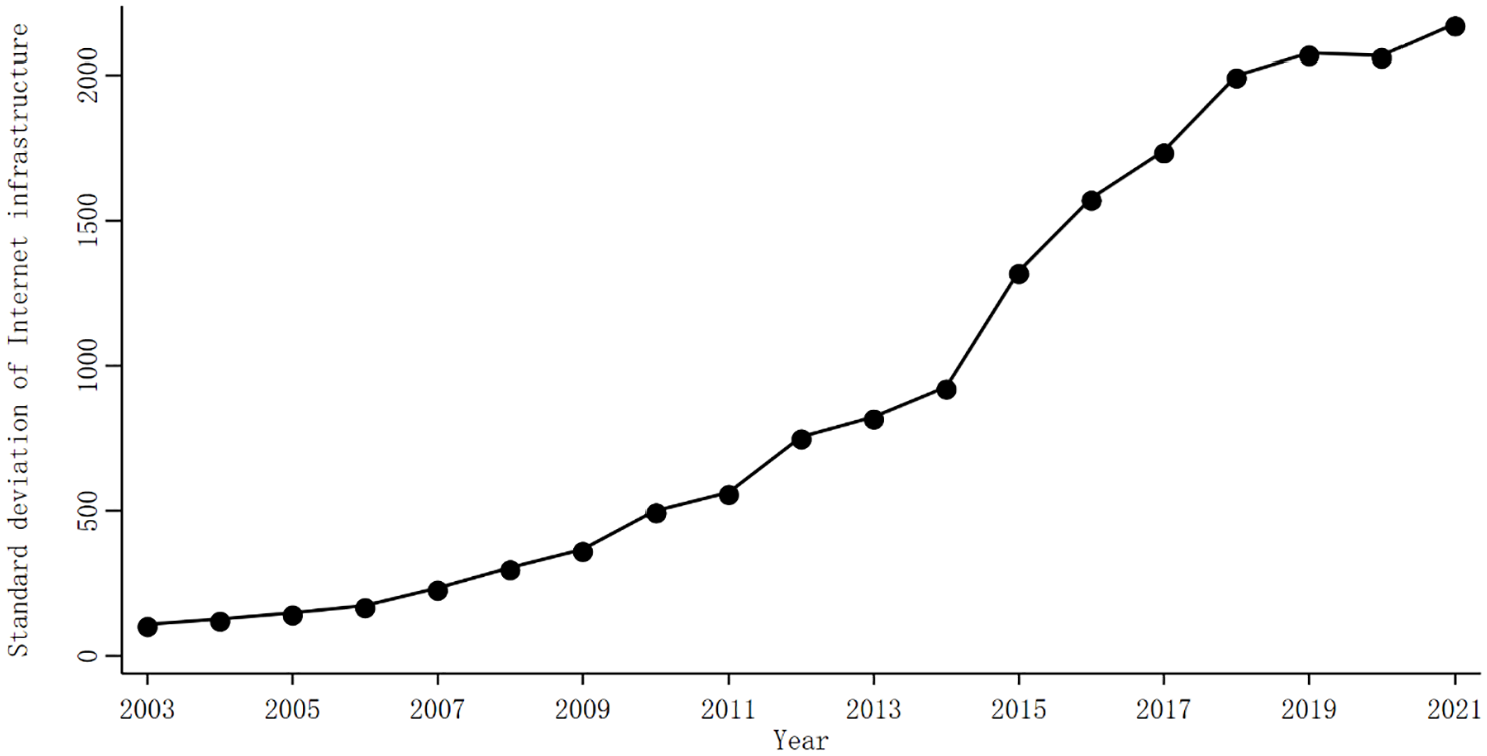

The development of Internet infrastructure has not only propelled China’s economic growth but also has brought about the digital divide issue. The digital divide fundamentally represents an imbalance in the allocation and utilization of Internet infrastructure and technology (Lythreatis et al., 2022). Because of unbalanced technological development, disparity of economic resources, cultural differences, inadequate policies, and geographical barriers, every region finds it difficult to maintain a synchronized Internet development, meaning that a digital divide is inevitable from the beginning. As shown in Figure 1, there has been an upward trend in the standard deviation of China’s Internet level in the past 20 years. This reflects the widening gap in Internet construction among China’s provinces. There is a digital divide in China’s Internet development, which is still widening.

The standard deviation of China’s annual internet infrastructure.

The unbalanced FDI results in economic growth differences, affecting national economic coordination and sustainable development, exacerbating the gap between the rich and the poor. Understanding how Internet infrastructure affects FDI inequality is crucial to preventing economic inequality, because it enables local markets to efficiently allocate foreign capital, thereby avoiding unbalanced economic growth. At the same time, it is a more realistic economic question of reducing the FDI inequality in the existing digital divide. Researchers have extensively analyzed the impact of Internet infrastructure on the location selection of foreign investment. However, few studies have focused on the direct effect of Internet infrastructure on FDI inequality. Therefore, the main objective is to clarify the FDI distribution in the digital context by constructing an FDI inequality variable. Spatial econometric models give ways to reduce FDI inequality in the digital divide. This article mainly contains contributions across three aspects.

Firstly, different from previous studies on the FDI motives, the research perspective was turned to the FDI inequality, influencing paths of Internet infrastructure on FDI inequality, which were clearly illustrated based on existing research. Secondly, the FDI inequality ratio was calculated for China’s 30 provinces and identified the effect of Internet infrastructure on the FDI inequality through regression. Instrumental variables were adopted to test the robustness of the causality. Thirdly, the digital divide was quantified through a matrix of Internet infrastructure, which was incorporated into a spatial econometric model. This provides a new approach to reducing FDI inequality and new evidence for eliminating regional gaps. Overall, our research provides empirical support for government departments to manage the inflow of foreign investment and leverage the synergies between foreign investment and digital infrastructure.

Subsequent chapters are as follows. Research hypotheses were proposed by reviewing the relevant literature in Chapter 2. Chapter 3 contains the empirical model, data sources, and variable construction. The regression results for robustness and heterogeneity are discussed in Chapter 4. The digital divide is quantified and introduced into spatial econometric models to reduce FDI inequality in Chapter 5. Our findings and policy recommendations are in Chapter 6.

Literature Review and Hypotheses

The determinants of FDI have always been one of the main topics in economics. Even before the spread of the Internet, theories already pointed out that geographical location, international trade, industrial organization, and other factors are the main determinants of FDI flows internationally. These determinants specifically include market size and growth potential (C. Wu et al., 2017), labor costs and skills (Ma & Ruzic, 2020), infrastructure conditions (Li et al., 2022), legal and institutional environment (Zhu et al., 2016), political stability (Alguacil et al., 2011), and environmental policies and sustainable development (Paramati et al., 2016). Compared with the western region, China’s eastern provinces have attracted much foreign investment via policy advantages, developed infrastructure, large market scale, highly qualified workforce, and excellent industrial agglomeration effects (Gaur et al., 2018). In contrast, underdeveloped regions have difficulty obtaining foreign investment, which leads to regional inequality in foreign investment. This inequality was often characterized by some regions attracting much foreign investment. Nevertheless, underdeveloped regions lack foreign investment.

International FDI flows have shown the digitalization trends, de-intermediation, customization, and the traditional determinants were weakened by the Internet economy. The digital economy allows enterprises to enter the global market at lower costs through technologies such as the Internet, e-commerce, and cloud computing, which no longer depend on a specific local physical market (Moeuf et al., 2018). With the broad application of artificial intelligence (AI) and robots, many industries’ low-cost labor has decreased significantly (Skare et al., 2023). Firms have become less dependent on the physical infrastructure of their target markets through digital platforms and remote delivery models (Lythreatis et al., 2022). Digital products made multinational investment profits no longer dependent on natural resources and the physical environment, which reduces the environmental policy’s influence on location selection for business investment (Ren et al., 2021). Traditional industrial boundaries are blurred, and industrial structure no longer significantly attracts FDI (Gawer, 2021). Asset focus shifts from fixed, tangible forms to intangible, mobile. It represents a structural shift in the profitability of digitized, multinational assets. As a result, the path of cross-border investment has been profoundly transformed, such as a lower proportion of overseas assets, lower employment, more diverse location determinants, a higher proportion of investment in the service industry, an increase in non-equity investment, and a more flexible global layout for multinational companies (Arvin et al., 2021). The digital economy has created a global Internet of innovation. Companies can participate in global innovation activities through telecommuting and online innovation platforms without physically investing in a destination.

In underdeveloped regions, Internet infrastructure promotes the diffusion of technology and innovation. Digital technology supports these regions in upgrading their industrial structure, improving production efficiency and competitiveness. Foreign investment no longer concentrates primarily on developed regions. It is willing to invest in these regions with growth potential (Guo et al., 2023). Online investment platforms, cross-border payment technologies, and digital currencies are constantly emerging, enabling investors easier access to global markets, especially small and medium-sized investors, who could participate in interregional capital allocation (Peng & Tao, 2022). Digitalization also supports e-government and regulation, further improving the local business environment. By simplifying administrative approval processes, and improving regulatory efficiency, Internet infrastructure reduces investors’ compliance costs and enhances investment willingness (Han et al., 2021). Telecommunication has created an inclusive entrepreneurial environment and lowered the technological and financial barriers for entrepreneurs. As a result, the capital factor has been reallocated among the population. In public services, digital infrastructure construction is accelerating in education, healthcare, finance, and other industries (Benzidia et al., 2021), providing favorable conditions for FDI inflows.

In summary, factors such as geographical location, international trade, and industrial structure have promoted FDI to converge toward developed regions, which has resulted in unequal FDI distribution. The digital economy has not only improved the production efficiency and market competitiveness of less developed regions but also digital technology, data (such as data assets, data security, and data property rights), and related strategic assets (such as talent, innovation, and research capabilities) have increasingly become key factors in international investment. At the same time, these factors are weakening the traditional motivators for FDI inflows in many contexts. Less developed regions have become new destinations for FDI in the digital era; thus, FDI inequality has been reduced. Therefore, the Hypothesis 1 was proposed.

Some studies have discussed the impact of the Internet infrastructure’s heterogeneity on the motives for foreign investment inflow in the empirical evidence (Chen & Kamal, 2016; Choi, 2010; Clarke, 2008), but they have not yet directly studied the relationship between the Internet facilities and the inequality of the inflow of foreign investment. Provinces with advantageous geographical locations typically have well-developed port, railway, and highway networks, which enable them to rapidly join the global market. These regions serve as major centers for global investment flows due to their geographical advantages (Zhang et al., 2023). Information technology has improved the speed at which foreign enterprises capture market demand, and reduced their business period and management costs (Miao, 2022). Forman et al. (2012) discovered that the proliferation of the Internet, despite its advantages, exacerbated income inequalities. Chinese inland regions are challenged by their limited geographical advantages compared to the coastal areas. These inland areas encounter hindrances, inefficient production factors, and information flow.

For provinces that have established free trade zones (FTZs), Internet infrastructure becomes a channel between policy and the market and helps foreign-funded enterprises obtain more timely policy updates. The investment risk caused by information asymmetry is reduced (Jiang et al., 2021). The joint effect of policy and infrastructure has accelerated the inflow of foreign investment, and FDI has been more widely dispersed to multiple free trade zones. Paul and Jadhav (2019) examined the determinants of FDI in emerging market countries using World Bank data. Internet infrastructure significantly promotes FDI inflows across countries, while trade tariffs dampen FDI growth, and political institutions make FDI growth heterogeneous across countries. High-speed Internet has become a new route for disseminating information such as tariff policies, exchange rate changes, and logistics developments (Yao & Whalley, 2016); foreign-funded enterprises can make investment decisions more effectively and improve the profitability of FDI.

Therefore, Internet infrastructure depends on geographical location, and foreign investment is looking for a favorable trading environment. In this context, Internet infrastructure can play a better optimization role in those provinces that meet geographical conditions and trade systems, which can reduce FDI inequality. So, Hypothesis 2 was proposed.

Methodology and Data

Empirical Model

This article establishes the basic regression model of Internet infrastructure on regional foreign investment inequality as shown in model (1):

Data Description

We have chosen Chinese provincial regions as our sample for analyzing the impact of Internet infrastructure on regional FDI inequality. Our study spans 19 years, from 2003 to 2021. Hong Kong, Macau and Taiwan are special administrative regions of China. They maintain autonomous economic activities and cannot directly participate in the economic market of mainland China. Statistical data for Tibet is largely missing. Samples from the above four regions were excluded to ensure data availability and the conclusions’ robustness. This covers 570 balance panel observations from 30 provinces. Our primary data sources include the China Statistical Yearbook, statistical yearbooks of individual provinces and autonomous regions, and the EPS data platform. The specific data processing methods are outlined below.

Foreign investment inequality (FDIgap). We calculated the FDI inequality ratio for each sample by using Equation 2. FDI inequality reflects inefficiencies in the distribution of external investment across regions, rather than the absolute average of FDI across regions. If FDI continuously flows into a certain region over time and brings about a “Siphoning effect” on other regions, this phenomenon would also affect the balanced distribution of foreign investment. The ratio reflects how much the observed value deviates from the sample mean. If the FDI inequality ratio consistently decreases over time, it indicates a “Convergence effect” in FDI for that province. Conversely, if it gradually increases over time, it suggests a “Matthew effect” in FDI. Calculating the ratio eliminates the dimensional units of this variable, obviating the need for further standardization.

Internet infrastructure (INTER). Existing research on Internet infrastructure measurement primarily relies on virtual variables derived from the “Broadband China” policy at the urban level (Fang et al., 2022; Tang et al., 2021; H. Wu et al., 2021). However, using virtual variables as independent variables may encounter issues such as multicollinearity and regression underfitting. The primary task of Internet infrastructure construction involves building broadband ports and laying fiber optics. Broadband ports are more indicative of the scale of Internet infrastructure usage. Therefore, the number of broadband access ports was selected as a proxy variable for the Internet infrastructure, and the length of long-distance optical cable routes was selected as a substitute variable for the robustness testing of Internet infrastructure. Both variables are standardized to address dimensional differences.

A total of six control variables were introduced into our regression model. Financial development level (Fin), developed financial markets can provide foreign capital with multiple financing channels, including bank loans, equity financing, bond markets, etc., to reduce investment risks. Marketization (Market), there is usually a more complete competition mechanism in a better market, and foreign-funded enterprises can operate in a fairer market environment. Economic volume (Lngdp), a higher economic means greater consumer markets, purchasing power, and economic stability, thereby allowing foreign enterprises to gain greater profits. Amount of labor (Labor): Foreign-funded enterprises tend to choose regions with an abundant workforce, which can reduce labor costs, make recruitment easier, and ensure the continuity of production. Innovation level (Ino), regions with higher innovation capabilities can increase technology spillovers and cooperation opportunities for foreign-funded enterprises. Industrial structure (Indus), optimizing the industrial structure enables foreign investment in sophisticated manufacturing and modern service industries. Table 1 demonstrates the measurement of control variables

Measurement of Control Variables.

As depicted in Table 2, the dependent variable FDIgap exhibits a standard deviation of 1.105, with a minimum value of 0.058 and a maximum value of 6.232. These statistics highlight a considerable disparity in foreign investment inflow across different provinces, underscored by the substantial standard deviation. The core independent variable INTER demonstrates a mean value of 0.147 and a standard deviation of 1.177. Notably, it exhibits a small mean and a significant standard deviation, thereby reflecting a digital divide among Chinese provinces to some extent.

Results of Descriptive Statistics.

Empirical Results

Benchmark Regression Results

Table 3 presents the outcomes of the baseline linear regression in model (1), examining the impact of Internet infrastructure on regional disparities in foreign investment. The regression results in column (1) indicate that Internet infrastructure mitigates regional foreign investment inequality. To enhance the robustness of our findings, columns (2) through (7) present regression outcomes for Internet infrastructure, progressively incorporating control variables, including financial development, marketization, economic volume, labor factors, innovation standards, and industrial structure. Gradual inclusion of control variables did not significantly alter the regression coefficients associated with network facilities, and all coefficients remained statistically significant at the 1% level. This consistency underscores the robustness of our baseline regression results and affirms the relevance of the selected control variables in the model. The Hausman test for random and fixed effects yielded a p-value of less than .001, supporting the choice of a double fixed effects model with robust standard errors for all subsequent empirical analyses. Hypothesis 1 is consistent with the above results.

Benchmark Regression Results of Internet Infrastructure on Foreign Investment Inequality.

Note. Robust standard errors are reported in parentheses in the table. ***, **, and * indicates that the regression results pass the significance test at the 1%, 5%, and 10% levels, respectively. The same representation is used in the subsequent tables.

This empirical result can be interpreted from two perspectives. On the one hand, foreign enterprises often face high operational costs and stringent regulatory restrictions in developed investment destinations. Additionally, the high market maturity in developed regions leaves little room for incremental growth, leading to intense market competition between foreign and local enterprises (Paul & Jadhav, 2019). This discourages the inflow of foreign capital into developed regions. On the other hand, Internet infrastructure not only enhances total factor productivity in less developed regions but also provides new channels for technology spillovers. Moreover, digital infrastructure reconfigures locational advantages through virtual spaces, thereby diminishing the importance of transportation costs and agglomeration effects in traditional economic geography theories. Developing regions, with their lower market entry barriers, are more likely to achieve first-mover advantages, further strengthening the motivation for foreign capital inflows into less developed regions. It is evident that in the Internet era, compared to developed regions, FDI tends to favor developing regions, leading to a convergence in investment between developed and less developed regions and alleviating the inequality in FDI distribution.

Instrumental Variable Regression Results

The endogeneity bias remains in the baseline regression results. From a practical perspective, it is observed that foreign investment does not influence government-led infrastructure development, such as the Internet, within a specific region. While there is no apparent issue of reverse causality based on logical analysis, the potential correlation between the core independent variables and the error perturbation term cannot be definitively eliminated. Consistency with the regression outcomes presented above may be influenced by endogeneity in two distinct manners. Firstly, the relationship between Internet infrastructure and foreign investment may be influenced by unobservable factors, such as provincial policy incentives, which could simultaneously drive Internet facility improvements and foreign investment attraction. These omitted policy variables can result in biased estimation results. Secondly, utilizing the number of network access ports as the core independent variables is intrinsically prone to statistical errors and omitted estimation information.

Consequently, the instrumental variable method is adopted to overcome the endogeneity problem from a geographical and historical perspective. Regarding Internet infrastructure, the geographic slope index was selected as the instrumental variable, which represents the standard deviation of the elevation across each province, as an instrumental variable. The geographical slope determines the construction cost and layout of infrastructure. Thus this indicator satisfies the instrument variable correlation assumption. In addition, the gradient index is a geographical variable, and the measurement process is irrelevant to the economy. Thus, it satisfies the exogenous assumption of the instrument variable. The paper also incorporates the number of post offices per million people in 1984 as an additional instrumental variable to address endogeneity problems. Network development and progress are based on and referenced to the historical postal and telecommunications services, satisfying the correlation requirements of the instrumental variable. The construction of post offices 20 years ago is not directly related to current foreign investment, satisfying the exogenous assumption of the instrumental variable.

It’s important to note that both the slope index and the number of post offices represent cross-sectional data and are not directly applicable as instrumental variables for panel data. In line with the approach used by Nunn and Qian (2014), a lag of one period of the total telecommunications business in each province is multiplied by the slope index and the number of post offices to create the panel data. Table 4 reports the results of the two-stage regression.

Two-stage Least Squares Estimation Results.

Note. Robust standard errors are reported in parentheses in the table; Kleibergen-Paap rk LM statistic’s p-values are reported in {}; Values in [] are critical values at the 5% level of the Stock—Yogo weak identification test. ***, **, and * indicate that the regression results pass the test of significance at the 1%, 5%, and 10% levels, respectively.

In the first stage, the regression coefficient of IV.1 for INTER is −0.002, which is statistically significant at the 1% level, indicating a significant correlation between IV.1 and INTER. Similarly, the regression coefficients of IV.1 and IV.2 for INTER are −0.003 and −1.201, respectively, both statistically significant at the 1% level, suggesting that the combination of IV.1 and IV.2 is significantly correlated with INTER.

About the “Underidentification test,” the “Kleibergen-Paap rk LM” statistic is calculated to determine whether the selected instrument variables pass the “Underidentification test,” to determine whether the instrument variables are correlated with the endogenous variables. According to the test results, the KP.LM value of IV.1 is 8.885, and the KP.LM value of IV.1 and IV.2 is 17.609, both of which are significant at the 1% level. This shows that the hypothesis of “insufficient identification of instrumental variables” should be rejected, and the selected instrumental variables can identify our endogenous variable INTER.

About the “Weak identification test,” the “Kleibergen-Paap rk Wald F” statistic is calculated to determine whether the selected instrument variable passes the weak instrument variable test. If the instrumental variable only contains rare information related to the endogenous variable, the 2SLS estimation result obtained through this instrumental variable is inaccurate. Such instrumental variables are also called “weak instrumental variables.” Therefore, the KP.Wald statistic should be compared with the threshold values (Stock et al., 2002). According to the test results, KP.Wald for IV.1 is 9.818 (greater than the threshold value of 8.96), and KP.Wald for IV.1 and IV.2 is 29.273 (greater than the threshold value 11.59). This suggests that we must reject the null hypothesis of “weak identification,” indicating that the selected instrumental variables are relevant to the endogenous variable and provide sufficient information.

In the second stage, the 2SLS results using IV.1 show that the regression coefficient of INTER on FDIgap is −2.917, which is statistically significant at the 10% level. The 2SLS results using the IV.1 and IV.2 pair indicate that the regression coefficient of INTER on FDIgap is −1.847, which is statistically significant at the 5% level. Both sets of 2SLS results suggest that Internet infrastructure significantly reduces FDI inequality, confirming the robustness of baseline results.

Finally, combining IV.1 and IV.2 requires testing for over-identification. This test is necessary only if the number of instrumental variables exceeds the number of endogenous variables. The p-value of the result is .4167, indicating that the difference between the 2SLS results (

Robustness Analyses

Replacement of Core Independent Variable

Internet Fiber Length (INTER_sub), as another indicator of telecommunication capacity, reflects the degree of sophistication of network facilities in terms of interconnection channels. Thus, the original independent variable was replaced by the new variable (INTER_sub) and standardized. Its result is presented in Table 5 (2). Findings demonstrate the ability of Internet infrastructure to bridge regional FDI inequality and pass the significance test, which illustrates the continued robustness of the paper’s conclusions.

Robustness Test Results.

Note.*** and ** indicate that the regression results pass the test of significance at the 1% and 5% levels, respectively.

Replacement of the Dependent Variable

Regional total exports-imports volume measures foreign trade at the level of actual goods. In contrast, most foreign investment enters Chinese soil as imports of actual goods, such as foreign direct investment in China to produce equipment. Therefore, Regional total exports-imports volume was substituted into formula (2), and a new substitution variable (FDIgap_sub) was calculated for FDI inequality. After replacing the dependent variable, regression results are shown in Table 5 (3). Internet infrastructure narrows the regional foreign investment inequality, that is, it has a “Convergence effect” on foreign investment, and passes the significance test, confirming to some extent the robustness of the baseline regression in Table 5 (1).

Change the Sample Interval

Considering the impact of COVID-19 in late 2019 on world economic growth and the control of foreign investment by each country’s epidemic prevention and policies. After 2019, 90 sample data were removed, accounting for 15% of the total sample. The regression results of the remaining sample data are shown in column (4) of Table 5, and the results show that the Internet infrastructure still has the effect of eliminating the regional disparity of FDI before the impact of COVID-19.

Simultaneity Test

There may be a simultaneity problem in the causality between Internet infrastructure and FDI inequality. Some provinces’ network infrastructure may not have a synchronous impact on FDI inequality, and they have a time lag. To eliminate the simultaneity, the lag of the independent variable was introduced into the regression equation. The regression results are shown in Table 5, column (5). The coefficient of INTER.L1 is −1.383, which is significant at the 1% confidence level. Compared with column (1) of Table 5, the coefficient remains negative, and it robustly supports that Internet infrastructure can reduce FDI inequality. The results of simultaneity test show that the current Internet infrastructure will still reduce future FDI inequality.

Heterogeneity Analysis Based on Provincial Characteristics

Analysis of Geographic Heterogeneity

In contrast to the mid-western provinces of China, the eastern regions benefit from coastal geography and favorable open-door policies that make them more attractive to foreign investment. Chinese economically advanced provinces are predominantly located in the eastern region, enabling them to lead digitization by leveraging their economic prowess. This concentration of economic development and digitization has led to a spatial distribution known as the “East High, West Low” ladder pattern (Luo et al., 2021), which in turn has given rise to what can be described as the “Internet infrastructure divide.” Foreign investors seek to invest and generate returns within a more optimized Internet environment. Consequently, Internet infrastructure disparities further influence the FDI levels and contribute to regional FDI discrepancies. The sample provinces are divided into three groups: eastern, central, and western regions. Group regression analysis is employed to assess the impact of Internet facilities on regional FDI disparities, as presented in columns (1)–(3) of Table 6. The findings reveal that Internet infrastructure has significantly reduced foreign investment inequality in eastern provinces while widening the investment gap in the mid-western provinces. This suggests that Internet infrastructure has driven a trend of convergence in FDI among eastern regions while simultaneously engendering an FDI “Matthew effect” within the mid-western provinces. Compared with the central and western provinces, the eastern region has more mature industrial clusters and more educated labor. These attributes align with the resource, market, and efficiency-seeking motives of FDI. Consequently, the eastern region has emerged as China’s dominant destination for foreign investment. The proliferation of broadband facilities has further expedited intra-regional FDI convergence. Contrary to our expectations, the regression coefficients for broadband facilities are significantly larger among central provinces compared to their western counterparts. Due to the spillover effect of network facilities from the east, the central region is prioritized over the western region. However, a delay in FDI and the tendency of foreign investors to depend on their initial investment region have amplified regional disparities in FDI within the central region.

Subgroup Regression Results.

Note. As of 2021, China has set up FTZs in Shanghai, Tianjin, Guangdong, Fujian, Liaoning, Zhejiang, Henan, Hubei, Chongqing, Sichuan, Shaanxi, Hainan, Shandong, Jiangsu, Guangxi, Hebei, Yunnan, Heilongjiang, Beijing, Hunan and Anhui, totaling 21 provinces. ***, ** and * indicate that the regression results pass the test of significance at the 1%, 5%, and 10% levels, respectively.

Analysis of Policy Heterogeneity

Establishing Chinese free trade zones (FTZ) signifies an escalated phase in Chinese governmental decentralization reforms concerning foreign trade. This evolution primarily revolves around reducing barriers to entry through the adoption of national treatment and negative list systems. This comprehensive approach reflects Chinese commitment to economic system reforms. Currently, China has approved the establishment of FTZs in 21 provinces, encompassing a majority of regions spanning from border areas to the interior. This expansion underscores the idea that FTZ creation is a coordinated effort, considering various provinces’ unique geographical advantages and distinctive development models. Hence, considering the external regulatory framework, the sample is classified into free trade zones with and without established free trade zones to assess the influence of Internet infrastructure on the regional disparity in FDI. The outcomes are presented in Table 6 (4) and (5), revealing that the FDI adjustments attributed to Internet facilities are predominantly observed in regions with less developed open-door policies. This analysis reaffirms the findings in columns 1 to 3 of Table 6. Due to their higher degree of openness to international markets and relatively superior institutional frameworks compared to the mid-western provinces and inland regions, Eastern provinces exhibit a more favorable environment for investment activities. In provinces with less developed foreign trade regulations, despite ongoing enhancements in Internet infrastructure, the lack of institutional safeguards facilitates the outflow of limited external funds through digital channels.

In summary, the p-values in Table 6 for both geographic heterogeneity and policy heterogeneity are less than .05 (0.0081 < 0.05; 0.0263 < 0.04). This indicates that there are significant differences in the coefficients of the heterogeneity regressions, demonstrating that heterogeneity exists in the impact of Internet infrastructure on FDI inequality. Hypothesis 2 was consistent with the above results. On a subregional level, network facilities have fallen short of their potential in facilitating information flow, dismantling institutional obstacles among regions, and ameliorating the investment gap. Instead, they have inadvertently compounded regional disparities as an additional barrier alongside pre-existing systemic and economic challenges. This phenomenon has led to a polarization effect, predominantly benefiting more economically advanced provinces and impeding the progress of less developed regions, ultimately hindering the harmonized development of the nation.

Addressing the “Matthew Effect” of FDI in the Digital Divide

The Situation of China’s Digital Divide

The available literature highlights the favorable impact of Internet infrastructure on FDI inflows, yet it tends to overlook the digital divide concept. Previous research has predominantly focused on how this digital divide might exacerbate disparities in regional development. This research highlights the importance of actively addressing the digital divide when formulating policies in various nations. There is a clear digital divide between Chinese coastal and inland cities, with cities in Jiangsu, Zhejiang, Shanghai, and Guangdong regions having significantly higher levels of digital infrastructure than those in Chinese northwestern and mid-north regions. At the same time, residents’ income, years of education per capita, and the number of laborers contribute to the digital divide. Hence, Song et al. (2020) classified the digital divide as a socio-economic issue. Luan et al. (2023) constructed a digital divide index for Chinese households, which found that the digital divide exacerbates energy poverty among low-income populations, while western regions of China have a higher incidence of poverty, making it difficult for digital facilities to be equitable and economically efficient. Some scholars (Paunov & Rollo, 2016; Sadorsky, 2012) utilized digital infrastructure as a moderating variable to investigate the influence of economic development indicators on foreign investment inflows. Nevertheless, it’s worth noting that the digital divide likely plays a significant role in the unequal foreign investment inflows. Further policy recommendations are required to address and narrow regional development disparities in the context of the digital divide.

The fundamental source of the digital divide lies in the unequal accessibility to digital infrastructure. The digital divide is quantified as the difference between the annual mean values of each province’s Internet infrastructure level, as depicted in Figure 2. A pronounced digital divide is readily apparent, particularly in the differentiation between Chinese eastern provinces and the remaining regions. Furthermore, there exists a substantial disparity in the level of Internet infrastructure development, with a notable contrast between most provinces in China and the provinces of Guangdong, Zhejiang, and Jiangsu. Within the central regions, the disparity in infrastructure is particularly notable when compared to Henan. Sichuan Province, situated in the southwestern region of central China, has focused its development resources, leading to a more pronounced gap in Internet infrastructure compared to other provinces in the region. This observation, to some extent, illustrates the capacity of resource-rich areas to prioritize the expansion of Internet facilities and attain a position of digital leadership. It’s worth noting that there are also intraregional disparities beyond the broader digital divide observed between eastern and mid-western provinces. Within the eastern region, disparities in Internet infrastructure are noticeable in Tianjin and Fujian compared to other eastern provinces. Similarly, Henan exhibits discernible gaps in the central region compared to its neighboring provinces. Meanwhile, Sichuan, located in the western region, also demonstrates pronounced disparities with its neighboring provinces in the same region.

Illustration of the digital divide.

Digital Spatial Econometric Regression

The digital divide has emerged as a significant impediment to coordinated interregional development (Wang et al., 2021). The development of Internet infrastructure, as revealed in the baseline regression results, may inadvertently worsen the existing disparities in foreign investment inflows. Thus, it is argued that efforts to reduce the gap in foreign investment inflows through Internet infrastructure development may, paradoxically, intensify the digital divide. Consequently, to alleviate the “Matthew effect” of FDI, exploring other investment channels outside the digital field is necessary. Specifically, transportation and finance will be examined.

Assuming that there is a digital divide formed by the gap in Internet infrastructure among regions, we refer to the practice of previous research (Ning et al., 2016; You & Lv, 2018) in constructing the economic distance matrix to construct a matrix of differences in Internet infrastructure.

Where

Where

According to Elhorst et al. (2013), we decomposed the spatial spillover effect into direct and indirect effects. In practical economic situations, the direct effect is the change of local dependent variables attributed to independent variables, and other regional spillover effects are not considered. Indirect effects are the impact of local independent variables on neighboring dependent variables. Economic variations of a certain region may influence neighboring regions’ economic operations through spatial correlations. The total effect is the sum of the direct and indirect effects. It shows that all impact on the dependent variable comes from the independent variables in each region (both its own and other regions). The difference between direct and indirect effects is that (1) direct effects only exist between local independent and dependent variables, while indirect effects exist between neighboring independent variables and local dependent variables due to spatial correlation. (2) Direct effects only include changes caused by local independent variables, while indirect effects only include changes caused by neighboring independent variables.

Transportation to Mitigate Foreign Investment Inequality

In the regression results presented in Table 7, regarding the impact of the Trans on FDIgap, the direct effect in the context of the digital divide is notably positive. This suggests that local transportation facilities can exacerbate the existing imbalance in foreign capital inflow. However, within the realm of the Internet, regional foreign investment inequality is subject to significantly negative indirect effects from neighboring regions. Notably, these indirect effects are much more pronounced than the direct ones, signifying that transportation infrastructure has a distinct narrowing effect on the regional gap in foreign investment. It is found that the presence of a well-developed local transportation channel can lead to an expansion effect on regional foreign investment inequality. However, the dynamics of foreign investment within the Internet space also exhibit strong spillover effects. This spillover occurs through the interconnected network of similar regional transportation channels, resulting in a more significant narrowing effect than the expansion effect. Therefore, in a broader perspective, enhancing the transportation channel can effectively mitigate the “Matthew effect” associated with FDI within the digital divide, ultimately reducing regional disparities. Transportation infrastructure plays a dual role by exacerbating disparities in foreign investment inflows and catalyzing external investments to enhance trade growth. Enhanced transportation infrastructure within the context of the digital divide has facilitated economic interactions among provinces. Notably, in China, where regional development disparities are most pronounced between the western interior and the eastern coastal provinces, improvements in transportation networks have heightened the likelihood of trade between the interior regions and foreign investors, consequently reducing the investment gap with the more developed eastern provinces.

Results of the SDM in Internet Space Based on the Digital Divide.

Note.*** and ** indicate that the regression results pass the test of significance at the 1% and 5% levels, respectively.

Finance to Mitigate Foreign Investment Inequality

Advanced financial markets have demonstrated a positive impact on attracting external investments across high, middle, and low-income regions (Nguyen & Lee, 2021). In addition, the financial construction in digitization has both positive and negative effects. On the one hand, digital finance leverages information channels to enhance inclusivity. On the other hand, financial markets supported by digital technology foster economic growth bubbles, contributing to heightened macroeconomic market uncertainty. As shown in Table 7, the regression results of Finance on FDIgap. In contrast to the transportation channel, the financial channel exhibits both a significant direct and indirect effect in reducing the disparities in foreign investment inflow. In other words, expanding financial networks at both the provincial and network levels has narrowed the regional FDI inequality. Consequently, the heightened financial development under the digital divide fosters a “convergence effect” on FDI. It becomes evident that financial channels, such as capital account liberalization, market-based exchange rates, and currency internationalization, influence cross-border capital flows. These financial mechanisms augment the volume and the likelihood of investments in less economically developed regions. Furthermore, the development of financial systems within host countries has a positive impact on technology through FDI, reducing regional technology disparities (Alfaro et al., 2004; Hermes & Lensink, 2003). Enhancing the financial system can effectively mitigate regional enterprise financing costs (Alfaro et al., 2004), extending vital financial backing to lagging regions and enterprises that attract foreign capital. This, in turn, stimulates the inflow of FDI across regions.

Conclusion and Policy Implications

This study examines the relationship between Internet infrastructure and foreign investment inequality across 30 provinces in China. It further explores strategies to narrow foreign investment inequality within the digital divide. The following three findings are the main conclusions of this article. Increasing Internet infrastructure can significantly reduce FDI inequality, which validates Hypothesis 1. The Internet infrastructure has a “convergence effect” on FDI in eastern China and a “Matthew effect” on FDI in western China. The effect of Internet infrastructure reducing FDI inequality exists in provinces with FTZs. The two heterogeneous results confirm hypothesis 2. In the digital divide, finance, and transportation are effective solutions to reduce the FDI inequality.

Based on the above conclusions, three policy recommendations are proposed:

Firstly, priority is given to developing the Internet infrastructure in underdeveloped areas. In the central and western regions where foreign investment inflows are lower, the government should improve Internet access and service levels to narrow the digital divide and promote a more balanced inflow of foreign investment. Intelligent manufacturing, e-commerce, and other foreign capital-intensive industries should be encouraged to deeply incorporate online infrastructure, thereby improving regional productivity and attracting foreign investment, to achieve a balanced distribution of foreign investment in all regions.

Secondly, interregional cooperation should be emphasized, and digital networks should transmit the advantages of FTZs. Eastern and Western enterprises use the Internet to achieve industrial chain collaboration, and less developed regions can absorb the technology and management experience of developed regions, narrowing the economic gap. Provinces establishing FTZs can further upgrade their digital infrastructure to help foreign capital enhance market competitiveness. Regulators can reduce the cost and time of foreign investment through digital platforms and online approvals to maintain the FTZ’s attractiveness to foreign investment.

Lastly, governments should utilize transportation and financial mechanisms to eliminate the negative impact of the digital divide. The importance of traditional infrastructure, such as financial channels and transportation networks, in safeguarding foreign investment should be emphasized. Governments should guide the digital upgrading of transportation and financial infrastructure. Especially in less developed areas, transportation, and finance are valuable tools to help these areas overcome the digital divide, thereby avoiding the exacerbation of regional inequality caused by the “digital divide.”

Footnotes

Acknowledgements

N/A.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by Major Projects of the National Social Science Foundation of China [grant number 21ZDA006].

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability

All data are collected from publicly available sources. The data that support the findings of this study are available from the corresponding author, [Liu WJ], upon reasonable request.