Abstract

This study examines the impact of green finance innovation reform on pollution emissions within high-polluting firms in China. Drawing on the Environmental Kuznets Curve (EKC) hypothesis, endogenous growth theory and resource-based view, our theoretical framework posits that green finance innovation reduces pollution by fostering increased R&D investments, encouraging the adoption of cleaner production technologies, and promoting a reduction in output scale. We employ data from China’s A-share listed high-polluting firms over the period 2011 to 2023, leveraging the establishment of green finance innovation pilot zones in 2017, 2019, and 2022 as a quasi-natural experiment. A double machine learning model is used to estimate the causal effects. The results support our hypotheses. Further, heterogeneity analysis suggests that the pollution reduction effect is most pronounced in large-scale firms, firms located in regions with advanced financial development, and areas characterized by high institutional quality. These findings highlight the critical role of green finance innovation in mitigating pollution, offering actionable insights for policymakers to expand such reforms across regions and industries.

Plain language summary

Our theoretical model posits that green finance innovation reform reduces pollution emissions through three channels: increasing R&D investments, adopting cleaner production equipment, and reducing output scale. We analyze data from China’s A-share listed high-polluting firms from 2011 to 2023, utilizing the establishment of China’s green finance innovation pilot zones in 2017, 2019, and 2022 as a quasi-natural experiment to validate our findings. The baseline and mechanism results, derived from a double machine learning model, align with our theoretical predictions. Additionally, heterogeneity checks indicate that the pollution reduction effect of green finance innovation reform is most significant for large-scale high-polluting enterprises, firms in regions with stronger financial development, and those in areas with high institutional quality.

Keywords

Introduction

With growing global concerns over climate change and environmental degradation (Joshua et al., 2024), green finance has become a vital tool for advancing sustainable development (Falcone et al., 2018). By integrating environmental goals into financial systems, green finance encourages investments that drive sustainability (Scholtens, 2017). For instance, the European Union’ carbon emissions trading scheme, launched in 2005, was the first global initiative of this kind. Similarly, the European Commission’s Sustainable Finance Strategy (SFS) and Sustainable Growth Financing Action Plan (SGFAP) emphasized redirecting capital toward sustainable economies. High-polluting sectors such as energy, manufacturing, and mining, which contributed around 70% of China’s carbon emissions in 2021, are critical targets for environmental reforms. To address this challenge, China introduced the Green Finance Reform and Innovation Pilot Zones (GFRIPZ) in 2017. Initial statistics indicate that firms within these pilot zones increased R&D investments in green technologies by 12% and adopted cleaner production equipment at a 10% higher rate than firms outside these zones, highlighting the potential impact of green finance reforms.

Despite this process, the micro-level impacts of green finance innovation on pollution emissions within high-polluting firms remain underexplored, particularly in the context of emerging economies. This study aims to explore the micro-level impacts of green finance innovation reform on pollution emissions within high-polluting firms in China. Specifically, we address the following questions: How does green finance innovation reform influence pollution emissions in high-polluting firms? What are the internal mechanisms driving these changes in emissions? How do the effects of green finance reform vary across firms of different sizes, financial environments, and institutional contexts?

This study is grounded in several theoretical perspectives (Awan et al., 2023; Khan et al., 2024). The Environmental Kuznets Curve (EKC) hypothesis suggests that green finance can accelerate firms’ transitions to cleaner technologies, particularly in high-polluting industries. Stakeholder Theory argues that firms are accountable to a wide range of stakeholders, and green finance can align corporate behavior with environmental concerns. Additionally, the Resource-Based View (RBV) posits that green finance provides firms with the necessary resources to invest in innovative, sustainable practices. Lastly, Innovation Diffusion Theory suggests that green finance can drive the adoption of green technologies in high-polluting sectors. Empirical studies support the view that green finance mechanisms, such as green bonds, green credit policies, and green investment funds, can significantly reduce firms’ pollution emissions (e.g., Akomea-Frimpong et al., 2021; Bhutta et al., 2022; W. Li & Jia, 2017). For instance, Flammer (2021) found that issuing green bonds led to substantial reductions in carbon emissions, while Bai and Zhong (2024) showed that green credit policies reduced pollution levels by offering favorable loan terms to environmentally responsible firms. Zhou and Du (2021) further emphasized the effectiveness of green investment funds in promoting cleaner production practices.

However, most studies focus on developed economies, leaving a research gap concerning emerging economies like China, where high-polluting firms play a significant role in environmental degradation. While previous research provides important insights, the specific pathways through which green finance innovation impacts firm-level pollution emissions, particularly in high-polluting industries, remain underexplored. Furthermore, traditional empirical methods face challenges such as high-dimensionality and nonlinearity, which complicate the study of green finance’s impact on pollution. This study addresses these gaps by focusing on the effects of green finance innovation reform in China, utilizing a more sophisticated econometric approach to ensure the robustness of the findings.

This study makes three main contributions. First, it provides firm-level empirical evidence on the impact of green finance innovation reform within high-polluting sectors in China, filling a critical gap in the existing literature. Second, it develops a theoretical framework that explains the mechanisms through which green finance reforms reduce pollution emissions, focusing on increased R&D investments, adoption of cleaner technologies, and reduction in output scale. Third, by employing a double machine learning method, this study enhances the credibility and robustness of its findings, providing a more reliable estimation of causal effects and setting a precedent for future research in this field.

The remainder of the paper is structured as follows: Section 2 explores the institutional background of green finance in China and provides a theoretical analysis of the mechanisms driving pollution reduction. Section 3 outlines the research design. Section 4 presents the baseline results and robustness checks, while Section 5 delves into the mechanisms through which green finance innovation reform influences pollution emissions and discusses the heterogeneous effects. The final section concludes the paper.

Institutional Background and Theoretical Analysis

Institutional Background

In 2017, China’s State Council of designated areas in Zhejiang, Guangdong, Jiangxi, Guizhou, and Xinjiang as pilot zones for green finance innovation reform. This group, known as the “five provinces (districts) and eight cities,” expanded in August 2022 to include Lanzhou New District in Gansu Province and Chongqing. In support of these reforms, seven ministries, including the People’s Bank of China, the National Development and Reform Commission, and the Ministry of Finance, jointly released the “Overall Plan for Green Financial Reform and Innovation Pilot Zones.”

These pilot zones aim to establish various green financing mechanisms, such as green credit, green bonds, green insurance, and green funds. From 2017 to 2022, the issuance of green bonds in these pilot zones increased by an average of 45% annually, while green credit growth averaged 37% annually. Concurrently, sulfur dioxide and nitrogen oxide emissions from high-polluting industries in these zones dropped by approximately 15%.

To facilitate these reforms, financial institutions and environmental protection departments have established platforms to share pollution information. Companies are rated on their pollution emissions by financial institutions based on their pollution emissions. As a result, financial institutions not only link green industries to finance but also restrict financial resources for companies that heavily pollute and consume large amounts of energy. Since the reform began, lending to high-pollution industries has decreased by 20%, with resources redirected to environmentally friendly businesses. Green banks have also implemented a “one-vote veto system for environmental protection,” reducing credit to polluting and energy-intensive enterprises by 25%.

The Financial Division assists qualified environmentally friendly companies in issuing more green bonds while reducing corporate bond issuances for high-pollution and high-energy-consuming sectors. Consequently, green bond issuance by environmentally friendly companies in the pilot zones has surged by 60% since 2017. Additionally, compulsory environmental pollution liability insurance for high-pollution businesses has increased insurance coverage for environmental risks by 30%. Each pilot zone has established a green fund to promote investment in energy conservation and environmental protection sectors, attracting over 200 billion RMB in private and public investments.

Furthermore, pilot zone governments have developed assessment methods for new constructions. To incentivize financial institutions to support green financial and limit loans to high-pollution industries, the People’s Bank of China has integrated green credit performance into macro-prudential assessments and other evaluation systems. Since the introduction of these assessments, financial institutions with strong green credit performance have seen a 12% average increase in their macro-prudential scores, highlighting the growing importance of sustainability in financial practices.

Theoretical Analysis

Drawing on multiple theories, including the Porter Hypothesis (Porter & Van der Linde, 1995), Endogenous Growth Theory (Romer, 1990), Stakeholder Theory, the Environmental Kuznets Curve (EKC) hypothesis, and the Resource-Based View (RBV), this study explores the mechanisms through which green finance reforms influence firms’ environmental performance. Integrating these concepts with the framework developed by Forslid et al. (2018) and Bøler et al. (2015), we construct a comprehensive model that explains firm’s pollution behaviors in response to green finance reforms.

Green finance aims to mitigate the environmental externalities of industrial activities by incentivizing firms to invest in green technologies and R&D. The Porter Hypothesis suggests that stricter environmental regulations can stimulate innovation, yielding to both environmental and economic benefits for firms. Endogenous Growth Theory emphasizes the role of financial resources in fostering technological advancement, particularly through R&D investment, which contributes to sustainable production processes. The Environmental Kuznets Curve (EKC) hypothesis suggests that as economies grow and environmental awareness increases, pollution levels initially rise but eventually decline as firms adopt cleaner technologies and environmental regulations become more stringent—factors which green finance reforms accelerate.

Moreover, Stakeholder Theory posits that firms are accountable not only to shareholders but also to a broader range of stakeholders, including environmental groups, regulators, and society at large. Green finance reforms align these diverse interests by encouraging firms to reduce their pollution emissions and enhance environmental responsibility. Lastly, the Resource-Based View (RBV) argues that green finance provides firms with the necessary resources—such as capital for cleaner production technologies and R&D investment—that enable them to develop sustainable competitive advantages. By leveraging these resources, firms can improve their environmental performance and reduce pollution emissions, while positioning themselves as leaders in sustainability.

Consumer

The utility function of a representative consumer is given as follows:

Where i represents differenced products; σ > 1 indicates the elasticity substitution between products;

Where

Producer

This paper assumes that the firm’s production follows Cobb-Douglas form.

Where

Following Bøler et al. (2015), firms increases productivity through R&D investments. Due to the knowledge spillover effect of R&D, the productivity function takes the following form.

Where

Given that the government imposes an emission tax t on each unit of pollution emissions, firms allocate a proportion

Where

where 0 < γ < 1,

The final product production function then becomes:

where

Green financial innovation reforms have increased the opportunity cost of high-polluting firms using financial resources. In other words, the opportunity cost of high-polluting enterprises increasing R&D investments and cleaner production equipment increased. Assume that

According to the cost minimization conditions, the firm cost function is:

where

Meanwhile, according to Shephard’s lemma, the firm’s capital demand

The firm’s R&D equipment investment

The firm’s price adopts the markup pricing method. Combined with the consumer demand function, the firm’s profit function is as following:

where

Based on the profit maximization condition, the firm’s investment in cleaner production equipment

where η = 1 - γρ (σ− 1), and 0 < η < 1.

The Influence of Green Finance Innovation Reform

By applying the chain rule, the impact of green finance innovation reform on high-polluting firms’ pollution emissions can be decomposed into the following three mechanisms:

Based on Equation 14, we can develop the following hypotheses.

Green finance initiatives, including green bonds, loans, and subsidies for environmentally friendly projects, significantly reduce the cost of capital for firms investing in green technologies. This reduction in financial barriers incentivizes firms to enhance R&D efforts, particularly in cleaner and more sustainable technologies (Böhringer et al., 2015). According to Endogenous Growth Theory (Romer, 1990), financial support for innovation, especially through targeted green finance mechanisms, can accelerate the pace of technological development, promoting sustainable practices. Firms benefiting from green finance are more likely to prioritize environmental sustainability in their R&D activities, resulting in innovations that lead to lower emissions and a smaller carbon footprint (Flammer, 2021; Ghisetti & Rennings, 2014). This relationship also aligns with the Porter Hypothesis (Porter & Van der Linde, 1995), which suggests that stringent environmental regulations, complemented by green financial support, can drive innovation and enhance both environmental and economic performance. Additionally, RBV suggests that green finance provides firms with essential resources, enabling them to develop competitive advantages through sustainable practices, such as innovative green technologies (Appiah et al., 2024). Furthermore, the establishment of GFRIPZ in China acts as a catalyst by reallocating resources from high-pollution industries to greener sectors (Liu & Wang, 2023). The “environmental protection one-vote veto system” (Shi et al., 2022; Wu et al., 2024) reinforces this trend by preventing companies with poor environmental performance from accessing financial aid, thereby pressuring high-polluting firms to improve their environmental performance through R&D investments (Yan et al., 2022).

Drawing on these insights, we propose the following hypothesis:

One of the key mechanisms through which green finance innovation impacts pollution is by enabling firms to adopt cleaner, more energy-efficient production technologies. Within GFRIPZ, financial incentives and regulations often require firms to invest in advanced pollution control equipment or energy-efficient machinery. These technologies directly contribute to reducing emissions, and the financial accessibility provided by green finance mechanisms accelerates this transition. The RBV suggests that firms capable of acquiring new resources, such as cleaner production technologies through green finance, will outperform competitors in reducing emissions and gaining sustainable competitive advantages. Moreover, the EKC hypothesis suggests that as economies grow and firms’environmental awareness increases, firms are likely to adopt cleaner technologies, especially when supported by green finance. For example, companies operating in these pilot zones report significantly higher investments in cleaner production equipment, correlating with measurable reductions in pollution emissions (Liu & Wang, 2023). By lowering capital costs and providing structured financial support, green finance mechanisms create an enabling environment for firms to invest in environmentally sustainable technologies, fostering long-term environmental benefits. Based on these insights, we propose the following hypothesis:

Green finance can also impact pollution indirectly by influencing production decisions in high-polluting industries. By increasing the cost of financing for environmentally risky activities, green finance disincentivizes firms from maintaining or expanding their most polluting operations. As firms face higher financing costs due to stringent green finance criteria, they often reduce their production scale, particularly if they encounter barriers in adopting cleaner technologies due to cost or technical limitations. This contraction in production can be explained by the EKC hypothesis, which suggests that at earlier stages of development, firms are more likely to pollute, but as they mature and gain access to more sustainable finance, they reduce their production of environmentally harmful goods. Empirical evidence shows that when firms reduce their output, pollution levels tend to decline proportionally, as emissions are typically by-products of industrial production (Tang & Zhang, 2020). Moreover, green finance innovation reforms specifically target high-polluting activities by limiting financial resources for firms that do not meet environmental standards, compelling them to scale down their operations. This contraction in production results in fewer emissions, particularly in sectors where pollution is strongly correlated with production volume. Based on the above analysis, we propose the following hypothesis:

Research Design

Data

Data from China’s A-share listed high-polluting firms spanning 2011 to 2023 were used. According to the details outlined in the “Industry Classification Management Directory for Environmental Inspection of Listed Enterprises” No. 373 issued by the Ministry of Environmental Protection in 2008, and the “Guidelines for Environmental Information Disclosure of Listed Companies” (Draft for Comments) which stipulates 16 heavily polluting industries, we have merged the required disclosure industries with the China Securities Regulatory Commission’s 2012 Industry Classification Standard, resulting in the following high-polluting industries: (1) Mining Industry: Coal mining and washing industry; oil and natural gas extraction industry; non-ferrous metal ore mining and dressing industry. (2) Manufacturing Industry: Alcohol, beverage, and refined tea manufacturing industry; textile industry; paper and paper products industry; petroleum processing, coking, and nuclear fuel processing industry; chemical raw materials and chemical products manufacturing industry; pharmaceutical manufacturing industry; chemical fiber manufacturing industry; rubber and plastic products industry; non-metallic mineral products industry; ferrous metal smelting and rolling processing industry; non-ferrous metal smelting and rolling processing industry. (3) Electricity, Heat, Gas, and Water Production and Supply Industry: Electricity and heat production and supply industry (limited to thermal and coal-fired power plants).

The primary financial data for these firms is sourced from the China Stock Market & Accounting Research (CSMAR) database. Pollution emissions data is primarily obtained from annual reports, corporate social responsibility reports, and official company websites. Relevant data from annual reports is sourced from the official websites of the Shenzhen and Shanghai Stock Exchanges. This study excludes firms that have undergone special treatment, such as ST and PT firms. Additionally, firms with significant missing data, fewer than eight employees, or negative environmental investments in construction projects were excluded. To perform 1% winsorization on a continuous variable in both the upper and lower tails. Ultimately, we obtained 8,755 firm-year observations for the period from 2011 to 2023.

Method

Based on Chernozhukov et al. (2018), this study adopts a double machine learning (DML) model to evaluate the impact of green finance innovation reform on the pollution emissions of high-polluting enterprises for the following reasons:

First, the DID model typically relies on the correct specification of the functional form. If the functional form is misspecified, such as assuming linearity when it is nonlinear, the estimates can become biased and inconsistent. In contrast, DML models mitigate this risk by utilizing flexible machine learning techniques that do not require strong assumptions about the functional form between covariates, treatment, and outcome. This flexibility allows DML to produce more robust estimates, even when the exact nature of the relationship is unclear.

Second, the DID model struggles with high-dimensional covariates, especially when these covariates interact in complex ways. DID requires the explicit specification of such interactions. DML, however, effectively handles high-dimensional covariates by employing machine learning algorithms like random forests and gradient boosting, which can automatically select the most relevant variables and reduce the bias associated with omitted variables (Belloni et al., 2014). The DML model of this study is as follows.

The partial linear models are specified as follows

Where the subscripts i and t represent firm and year, respectively. pollution represents the total pollution emissions of firms, while green is the treatment variable representing “green finance innovation.” It equals 1 if the region j where firm i is located is a polit zone for green finance innovation reform in year t, and 0 otherwise. The coefficient

Given the small sample size, this study constructs an auxiliary regression to ensure that the estimator of

Where

Additionally, to account for the heterogeneous effects of green finance innovation on pollution emissions, and following Chernozhukov et al. (2018), a more general model is developed:

Variables

Pollution Emissions

Pollution emissions (

Green Finance Innovation Reform

To measure green finance innovation (Green) reform, we use the implementation of the pilot zones for the “green finance innovation reform” strategy as the treatment variable. The variable Green is defined as the interaction term between T and D. Here, T equals 1 if the year is the same as or latter than the year in which the area where firm i is located was designed as an experimental green finance zone; otherwise, T equals 0. Similarly, D equals 1 if the firm is located in an experimental green finance zone, and 0 otherwise.

The first batch of Green Finance Reform and Innovation Pilot Zones, established in 2017, includes Quzhou City and Huzhou City in Zhejiang Province; Huadu District in Guangzhou City, Guangdong Province; Gui’an New District in Guizhou Province; Ganjiang New District in Jiangxi Province; Hami City and Changji Hui Autonomous Prefecture in the Xinjiang Uygur Autonomous Region; and Karamay City. The second batch, introduced in 2019, is Lanzhou New District in Gansu Province. The third batch, established in 2022, is Chongqing City. This study excludes municipalities, as well as Hong Kong, Macao, and Taiwan, retaining prefecture-level regional samples.

Control Variables

When selecting control variables, this paper first identifies the following control variables that may affect corporate pollution emissions, based on existing economic theories and relevant literature. These includes: profitability (Profit), calculated as the ratio of operating profit to operating income; asset-liability ratio (LEV), estimated as the ratio of the total liabilities to total assets; capital intensity (Capital), measured as the ratio of the fixed assets to total assets; total Return on assets (ROA), calculated as the ratio of the operating profit to the total assets at the beginning of the year; effective corporate income tax rate (CIT), estimated as the ratio of actual corporate income tax paid to operating income; firm size (Size), estimated as the logarithm of the total assets at the beginning of the period; firm age (Age), calculated as the natural logarithm of the difference between the statistical year and the year of establishment plus 1. The descriptive statistics for these main variables are presented in Table 1.

Descriptive Analysis of Main Variables.

Empirical Results

Baseline Results

In the DML model, one of its main advantages is the use of LASSO to automatically select control variables. Building upon the selection of control variables based on theory and literature, this study further employs the LASSO algorithm to automatically select control variables, thereby ensuring the accuracy of causal effect estimation. The results are represented in Table 2. Columns (1) and (2) utilize the random forest algorithm within a partial linear model framework, employing a sample split ratio of 1:4. Columns (3) and (4) use an interactive model for estimation. The results indicate that green finance innovation reform has a statistically significant negative impact on the pollution emissions of high-polluting firms. The significant reduction in pollution emissions suggests that green finance innovation reform strongly encourages high-polluting firms to adopt more environmentally friendly practices.

Baseline Results.

Note. *** indicate significance at the 1% significance level; the values in parentheses are robust standard errors. The control variables determined by LASSO incudes ROA, Capital, Age, and CIT.

These results align with findings from other studies, such as Flammer (2021), who also reported a significant reduction in pollution emissions following the adoption of green finance mechanisms. The alignment of our findings with existing literature strengthens the validity of our analysis and highlights the importance of financial policy in driving environmental performance improvements.

For the control variables, we observe the following results: First, the coefficient of ROA is significantly positive at the 1% level. This suggests that when a firm’s ROA increases, reflecting higher profitability, it tends to expand production to meet demand and boost profits. However, in high-pollution industries like manufacturing, chemicals, and steel, production expansion often leads to increased resource consumption and emissions (Robaina & Madaleno, 2020). Second, the coefficient of capital is negative, indicating that greater capital reduces a firm’s pollution emissions. As capital grows, firms have more resources to invest in green technologies and pollution control measures, improving efficiency and lowering emissions. Investments in modern clean technologies, energy-efficient equipment, and pollution treatment systems, which require significant capital, are more accessible to well-capitalized firms (Jiang et al., 2023). Third, we find a positive relationship between firm age and pollution emissions. Older firms may develop path dependence, relying on outdated production processes and being slower to adopt environmentally friendly technologies (Solikhah et al., 2021). This inertia can lead to higher emissions. Lastly, an increase in the effective corporate income tax rate raises the firm’s tax burden, reducing net profits and dampening incentives to invest or expand, particularly in high-pollution sectors. Consequently, if firms reduce investment in high-pollution production lines, overall production decreases, leading to lower emissions.

Excluding the Impact of Other Environmental Policies

In 2013, China introduced the Air Pollution Prevention and Control Action Plan. To assess the impact of this policy, we re-analyzed the data after excluding companies located in the 57 high-target cities identified by the plan. Column (1) of Table 3 demonstrates that the baseline results remain robust.

Excluding the Impact of Other Environmental Policies.

Note. *** indicate significance at the 1% significance level; the values in parentheses are robust standard errors.

In 2013 and 2014, carbon emissions trading pilot projects were initiated in Beijing, Tianjin, Shanghai, Chongqing, Hubei, Guangdong, and Shenzhen. We re-ran the regressions to account for the potential effects of these pilots. Column (2) of Table 3 shows that the results are consistent with the baseline findings.

Furthermore, in 2014, the Ministry of Environmental Protection implemented interim measures aimed at reducing pollution emissions through command-style environmental regulation. To minimize potential interference from these measures, we excluded firms located in the affected cities. Column (3) of Table 3 confirms the robustness of the baseline results.

In 2018, the Environmental Protection Tax Law of the People’s Republic of China was enacted, replacing environmental protection with taxes, which may have influenced the pollution control behavior of high-polluting firms. We excluded data from 12 provinces, including Hebei, where environmental protection tax standards were increased. The results in column (4) of Table 3 further validate the baseline findings.

Robustness Results

Alternative Measurement of Dependent Variable

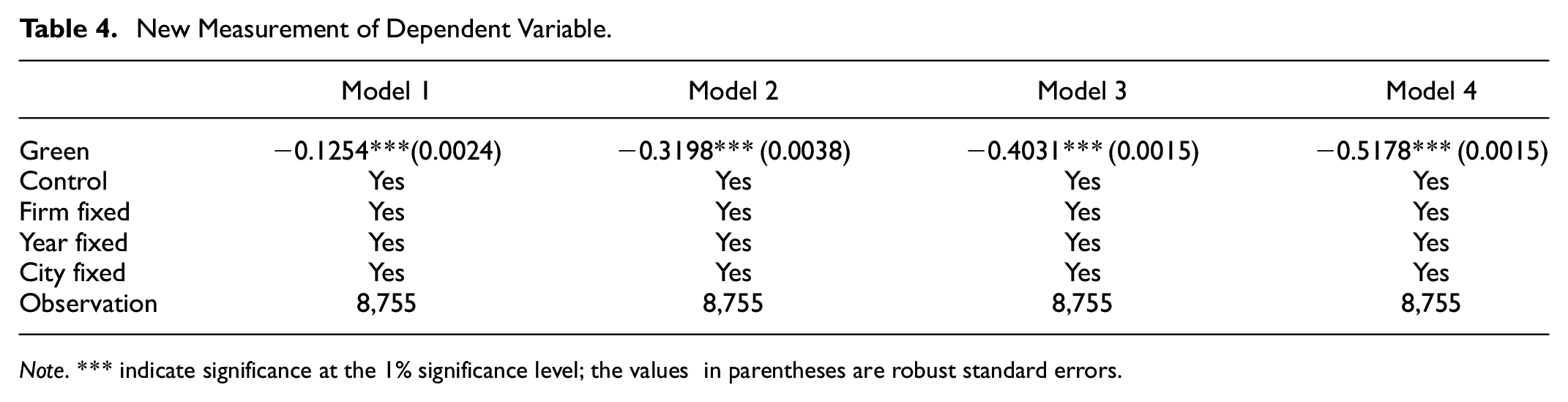

Drawing on existing literature, we reconstructed pollution emissions indicators for high-polluting firms using four specific measurements: the ratio of air pollution emissions to operating income, the ratio of nitrogen oxide emissions to operating income, the ratio of comprehensive water pollution to operating income, and the ratio of ammonia nitrogen emissions to operating income. Columns (1) to (4) of Table 4 demonstrate that the results align with the baseline findings.

New Measurement of Dependent Variable.

Note. *** indicate significance at the 1% significance level; the values in parentheses are robust standard errors.

Alternative Method

First, we lagged the dependent variable by one period to account for the time required for the “green finance innovation reform” strategy to achieve policy efficiency. The coefficient for green finance innovation in Column (1) of Table 5 confirms the robustness of the baseline results.

New Method.

Note. *** indicate significance at the 1% significance level; the values in parentheses are robust standard errors.

Second, given the similarities in location characteristics, policy background, culture, and lifestyle across prefecture-level cities, we included region-time interaction fixed effects to control for these macro-system effects. Column (2) of Table 5 indicates that the benchmark conclusion remains valid.

Third, while DML models offer advantages such as flexibility in handling non-linear relationships between variables, they also provide the added benefit of incorporating machine learning techniques, like LASSO and random forest, to automatically select relevant control variables. This approach enhances the precision of causal inference and reduces the risk of omitted variable bias. To further validate the robustness of our findings, we employed traditional multiple linear regression models, specifically the staggered difference-in-differences (staggered DID) approach. As shown in Column (3), the results are robust. However, as Goodman-Bacon (2021) highlighted, traditional staggered DID models may introduce bias. To address this potential issue, we also applied the improved method proposed by Callaway and Sant’Anna (2021) for additional robustness checks. Ultimately, both the partial linear models and the multiple linear regression models produced similar empirical results. These findings consistently demonstrate that green finance innovation reform significantly reduces pollution emissions in high-polluting firms, reinforcing the robustness and validity of our conclusions.

Resetting the Dual Machine Learning Model

To mitigate potential biases in the model specification of the double machine learning method, we conducted robustness checks by adjusting the machine learning model. First, we altered the sample split ratio from 1:4 in the baseline regression to 1:2 and 1:7 to access the impact of these changes on the results. Second, we replaced the random forest algorithm with Lasso regression and neural networks methods. The results, presented in Table 6, consistently show that green finance innovation has a negative impact on the pollution emissions of high-polluting firms.

Resetting the Dual Machine Learning Model.

Note. *** indicate significance at the 1% significance level; the values in parentheses are robust standard errors.

Endogeneity Issues

While the DML method effectively alleviates endogeneity concerns, this study further addresses the potential issue of reverse causality-induced endogeneity by following Yang et al. (2023), utilizing the number of listed banks in a city offering green financial services as an instrumental variable (Fin). This variable satisfies two critical conditions: (1) relevance, as the number of such banks reflects the city’s green finance level and is positively associated with the likelihood of becoming a green finance innovation pilot zone; and (2) exogeneity, as this number is determined by banking demand, with no evidence linking it directly to the city’s green financial development level. Building on the framework of Chernozhukov et al. (2018), a partially linear instrumental variable model under double machine learning is employed to test for endogeneity. The model is as follows:

The results are in Table 7. After employing the instrumental variable, the results remain significantly negative at the 1% level, confirming the robustness of the baseline results.

Endogeneity Issues.

Note. *** indicate significance at the 1% significance level; the values in parentheses are robust standard errors.

Sample Selection Bias

To address potential sample selection bias, given that pollution emissions from high-polluting enterprises may be influenced by non-random factors such as regional environmental regulations, this study employs the Heckman two-stage method to re-estimate the impact of green finance innovation on pollution emissions from high-polluting enterprises. The results are in Table 8. High-polluting enterprises with the top 30% green credit levels are classified as the treatment group, while the remaining 70% constitute the control group. To mitigate severe multicollinearity between the inverse Mills ratio derived from the first-stage regression and the explanatory variables in the second-stage model, the first-stage regression includes the regional environmental governance intensity variable (gov). The variable gov influences the strategic choice of whether high-polluting enterprises adopt emission reduction measures but is not directly linked to green finance innovation. Gov is measured by the ratio of regional environmental governance investment to GDP. As shown in column (2), the inverse Mills ratio is significantly positively correlated with green finance innovation. Moreover, the coefficient of Green is significantly positive, indicating that green finance continues to significantly drive emission reductions among high-polluting enterprises, even after accounting for selection bias, thus confirming the robustness of the baseline findings.

New Method.

Note. *** indicate significance at the 1% significance level; the values in parentheses are robust standard errors.

Mechanism Tests and Heterogeneity Checks

Raising Financing Cost and Reducing Financing Scale

Green finance innovation reform aims to reallocate financial resources toward environmentally sustainable projects by imposing stricter criteria and higher costs for firms involved in high-polluting activities. The underlying theory suggests that by increasing the cost of capital and tightening access to financial markets for high-polluting enterprises, these reforms incentivize firms to either reduce their scale of operations or invest in cleaner technologies to qualify for better financing terms (Glomsrød & Wei, 2018). This dual mechanism, raising the cost of financing and incentivizing sustainable practices, can significantly reduce in the financing scale of high-polluting firms, as they are either priced out of the market or forced to downsize to meet new regulatory standards (Campiglio, 2016). Moreover, the increased financing costs reflect the higher risk premiums and interest rates charged by financial institutions, accounting for the elevated financial risk of environmental non-compliance.

Next, we examine the impact of green finance innovation reform on the financing scale and costs of high-polluting enterprises in the pilot zones. First, we use a firm’s current liabilities to estimate its financing scale. Columns (1) and (2) of Table 9 present the results, showing that the coefficients for green finance innovation are significantly negative. This indicates that the financing scale of high-polluting enterprises drops significantly following the implementation of the pilot zones. Second, to verify the impact of green finance innovation on financing costs, we use the ratio of interest expenses to liabilities. Columns (3) and (4) of Table 9 confirm that green finance innovation reform increases financing costs.

Mechanism Tests.

Note. *** indicate significance at the 1% significance level; the values in parentheses are robust standard errors.

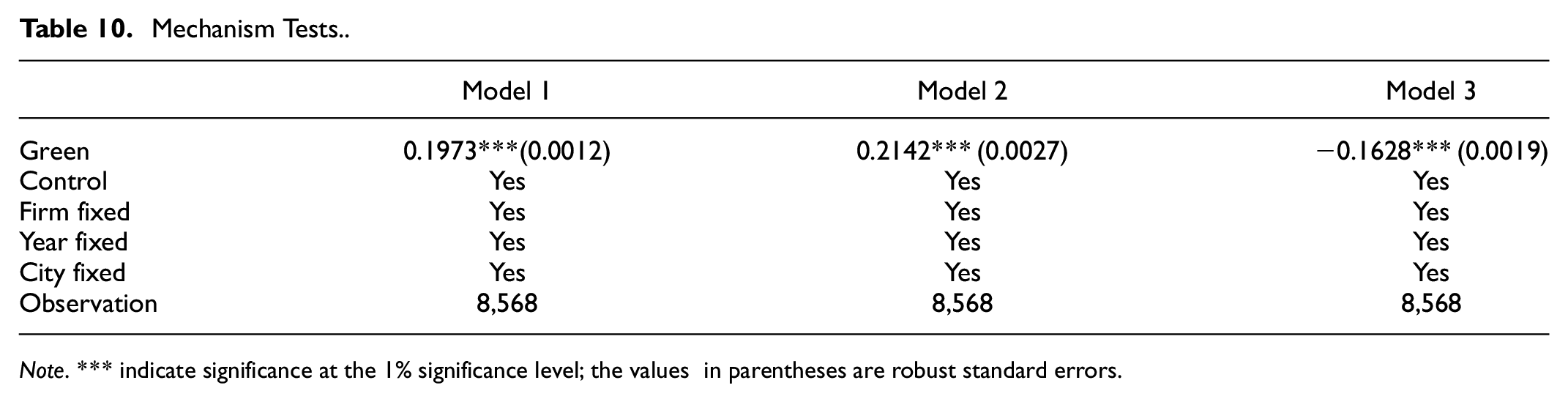

Increasing R&D Investments

Based on H1, green finance innovation reform is designed to influence firms’ behavior by altering the financial incentives associated with environmentally harmful practices. Theoretically, such reforms should lead high-polluting enterprises to reallocate resources toward more sustainable activities. One of the key mechanisms through which green finance operates is by providing financial incentives, such as lower interest rates or preferential loan terms, for firms that engage in environmentally friendly practices, while simultaneously imposing higher costs for non-compliance (Heinkel et al., 2001). This dual approach creates a financial environment where high-polluting firms are economically motivated to shift away from traditional, pollutive processes toward more sustainable practices, including increased investment in research and development (R&D) of cleaner technologies.

R&D investment plays a crucial role in enhancing long-term sustainability by enabling firms to develop and adopt new technologies that reduce emissions and improve resource efficiency. Green finance reforms, by shifting the financial landscape, make it more attractive for firms to invest in cleaner technologies as a way to not only comply with environmental regulations but also to secure a competitive advantage. Firms that prioritize R&D in cleaner technologies are better positioned to reduce operational costs through improved efficiency, as well as to mitigate the risks associated with regulatory penalties and reputational damage linked to environmental non-compliance.

In this study, R&D investment is measured by the natural logarithm of R&D investment value. The results in column (1) of Table 10 show that the coefficient for green finance innovation is significantly positive, indicating that the reform has effectively incentivized high-polluting enterprises to increase their R&D investments.

Mechanism Tests.

Note. *** indicate significance at the 1% significance level; the values in parentheses are robust standard errors.

Improving Cleaner Production Equipment Investments

Based on H2, green finance innovation reform should theoretically encourage increased investment in cleaner production equipment, as firms face greater financial incentives to reduce emissions and improve environmental performance. The underlying mechanism can be explained through the lens of cost-benefit analysis and regulatory compliance. As green finance reforms impose higher costs for non-compliance and offer preferential financing terms for environmentally sustainable practices, firms are incentivized to adopt cleaner technologies and production methods to remain competitive and reduce their financial risk (Porter & Van der Linde, 1995).

From an economic perspective, firms respond to the increased cost of capital by seeking more efficient production methods to mitigate these costs. Cleaner production equipment, which includes technologies that reduce waste, lower emissions, and improve resource efficiency, becomes a valuable investment. By improving environmental performance, firms not only reduce their exposure to penalties and higher interest rates but also enhance their reputation and access to better financing opportunities (Ren et al., 2020). Additionally, as consumers and regulators increasingly demand sustainable practices, firms that invest in cleaner production equipment may gain a competitive advantage in the market, further justifying the investment.

The ratio of the current year’s cleaner production equipment consumption to operating income is used to estimate investment in cleaner production equipment. The results in column (2) of Table 10 indicate that green finance innovation reform has effectively encouraged high-polluting enterprises to improve their investments in cleaner production equipment.

Reducing Production Scale

Based on H3, by increasing the financial burden of maintaining high levels of pollution, green finance innovation reform can theoretically incentivize firms to scale down their overall production output. This outcome aligns with the pollution haven hypothesis, which suggests that when environmental regulations tighten, firms facing higher costs associated with pollution may either invest in cleaner technologies or reduce their production scale to minimize costs (Copeland & Taylor, 2004).

Green finance reforms can impose additional financial pressures on high-polluting firms by increasing the cost of capital for non-compliant activities and rewarding environmentally sustainable practices with more favorable financing options (Heinkel et al., 2001). For firms that are unable or unwilling to invest in cleaner technologies, the higher costs associated with pollution—such as increased risk premiums, higher interest rates, and reduced access to financial markets—may lead them to downsize their operations. This downsizing effect is particularly evident in industries where pollution control technologies are either prohibitively expensive or difficult to implement without fundamentally altering production processes.

Theoretically, green finance reforms serve as a market-based approach to controlling pollution by internalizing the external costs of environmental harm. As firms are forced to account for the environmental costs of their activities, they may respond by cutting production, especially in sectors where environmental compliance raises production costs significantly (Ambec & Lanoie, 2008). This can lead to a contraction in output, particularly in firms where the cost of pollution abatement exceeds the potential gains from maintaining high levels of production.

In this study, output scale is estimated by the logarithm of operating income. The results in column (3) of Table 10 show that green finance innovation reform reduces the output scale of high-polluting firms.

Heterogeneity Checks

Firm Scale

Large-scale enterprises, due to their extensive production capacities and higher levels of resource consumption, face greater financial, and regulatory pressures under green finance innovation reforms. These pressures include higher costs of non-compliance, more substantial financial incentives to adopt cleaner technologies (Porter & Van der Linde, 1995), and heightened scrutiny from regulators and the public (Johnstone et al., 2010). Consequently, these factors are expected to drive larger firms to make more significant reductions in pollution emissions than their smaller counterparts. Hence, we can propose that larger firms are often more responsive to green finance innovation reforms aimed at improving environmental performance (Hart & Ahuja, 1996).

This study measures firm size using the number of employees. If a firm with more than 500 employees are classified as large-scaler, and those below 500 as small- and medium-scale. The results are reported in Columns (1) and (2) of Table 11. The findings support that green finance innovation reform has a more significant inhibitory effect on the pollution emissions of large-scale high-polluting enterprises.

Heterogeneity Checks.

Note. *** and ** indicate signifiance at the 1% and 5% significance level, respectively the values in parentheses are robust standard errors.

Regional Financial Development

Financial development plays a critical role in the implementation and effectiveness of green finance initiatives. In regions with well-developed financial systems, there is typically better access to financial services, a more robust regulatory environment, and greater availability of capital for environmentally sustainable investments (Claessens & Feijen, 2007). These factors contribute to a more efficient and effective response to green finance innovations, such as the adoption of green bonds, loans, and incentives for sustainable practices (Chen & Zhao, 2021). In contrast, regions with lower levels of financial development may face challenges such as limited access to credit, weaker financial infrastructure, and less sophisticated financial markets (Thompson, 2023). These challenges can hinder the ability of firms and investors in these regions to fully engage with and benefit from green finance innovations. As a result, the impact of green finance reforms may be muted, leading to less significant changes in environmental performance compared to regions with more advanced financial systems.

In this paper, we construct a regional financial development indicator using the proportion of deposits and loans provided by urban financial institutions in each province relative to regional GDP. Based on the median of this indicator, we divide the sample into two subgroups: high and low levels of regional financial development. Columns (3) and (4) of Table 11 present the results for these subgroups, respectively. The coefficients for green finance innovation are significantly negative and larger for the high development level group. This indicates that green finance innovation has a more pronounced inhibitory effect on the pollution emissions of high-polluting enterprises in areas with higher levels of financial development.

Regional Institutional Quality

Institutional quality—characterized by effective governance, strong regulatory frameworks, and transparent enforcement mechanisms—enhances the impact of green finance innovation. In regions with high institutional quality, green finance initiatives are more likely to be effectively implemented and monitored, leading to a more substantial reduction in pollution emissions (Kaufmann et al., 1999). The presence of strong institutions ensures that financial incentives and penalties associated with green finance are properly enforced, making it more difficult for firms to evade environmental responsibilities (Acemoglu et al., 2019). As a result, green finance reforms in these regions are expected to have a more pronounced effect, reflected in a significant negative coefficient, which represents the reduction in pollution emissions.

In this study, based on Xu and Mao (2018), we employ the following formula to estimate the regional institutional quality:

Conclusion and Policy Implication

Conclusion

This study provides valuable insights into the impact of green finance innovation reform on pollution emissions in high-polluting firms in China. By developing a robust theoretical model and analyzing data from China’s A-share companies in high-polluting industries between 2011 and 2023, we employed a double machine learning approach to evaluate the effectiveness of these reforms. Our findings demonstrate that green finance innovation reform significantly reduces pollution emissions in high-polluting firms through three primary mechanisms: (1) increased R&D investments in green technologies, (2) the adoption of cleaner production equipment, and (3) a reduction in output scale.

In addition to these primary findings, our heterogeneity analysis provides further insights. We observed that the pollution reduction effects of green finance innovation are more pronounced in (1) large-scale enterprises, (2) firms located in regions with advanced financial development, and (3) those operating in areas with strong institutional quality. This indicates that the effectiveness of green finance reforms varies based on firm size, regional financial conditions, and institutional strength.

Overall, this study contributes to the existing literature by providing firm-level empirical evidence on how green finance innovation reforms can mitigate environmental damage caused by high-polluting firms. These findings underscore the importance of promoting green finance policies, particularly in regions with strong financial and institutional infrastructure, to achieve broader environmental sustainability goals.

Policy Implications

Based on the findings of this paper, several policy implications can be proposed to further enhance the effectiveness of green finance innovation in reducing pollution emissions in high-polluting firms:

First, enhancing financial support and accessibility. Governments should amplify financial incentives, such as tax credits or subsidies, to motivate high-polluting firms to increase investments in R&D for green technologies. Accelerating the development and adoption of cleaner production methods is crucial for reducing emissions. Additionally, the availability of green finance instruments, such as green bonds and loans, should be expanded, particularly in regions with lower levels of financial development. Financial institutions should be encouraged to design and promote these products to ensure that even smaller firms can access the capital necessary for environmental upgrades.

Second, strengthening institutional and regulatory frameworks. It is essential to reinforce institutional frameworks and enhance regulatory oversight to ensure the effective implementation and monitoring of green finance initiatives. Clear standards for environmental reporting should be established, along with improved transparency in the allocation of green finance. Firms must be held accountable for meeting their environmental commitments. Furthermore, implementing a robust monitoring and evaluation framework is crucial for continuously assessing the effectiveness of green finance policies. This framework should include tracking key performance indicators, gathering stakeholder feedback, and making data-driven adjustments to policies as needed.

Third, expanding and tailoring green finance initiatives. To maximize the benefits of green finance, the geographical coverage of GFRIPZ should be expanded to include more regions, particularly those with high levels of industrial pollution but lower financial development. For regions not currently designated as pilot zones, tailored strategies should be developed to introduce elements of green finance innovation. This could involve setting up smaller-scale pilot projects, providing technical assistance, and facilitating partnerships between non-pilot and pilot areas to share best practices.

Fourth, fostering collaboration and scale-appropriate solutions. Tailored green finance policies should be developed to address the specific needs of firms of different sizes. For large-scale enterprises, policies could focus on facilitating significant investments in clean technologies, while for smaller firms, incentives should target cost-effective, incremental improvements in production processes. Collaboration between the public and private sectors should be encouraged to pool resources and expertise in financing green initiatives. Public-private partnerships can be particularly effective in mobilizing large-scale investments in green infrastructure and technology development, thereby amplifying the impact of green finance. Moreover, cross-regional collaborations between pilot and non-pilot areas should be promoted to facilitate knowledge transfer, capacity building, and joint projects in green finance. Establishing networks of firms, financial institutions, and regulators across different regions will help share best practices and co-develop green finance initiatives.

Limitations and Further Research Avenues

While this study provides significant insights into the impact of green finance innovation reform on pollution emissions in high-polluting firms, several avenues for future research remain open.

First, although this study focuses on China’s A-share listed high-polluting firms from 2011 to 2023, future research could broaden the scope to include a wider range of firms, particularly SMEs and non-publicly listed firms. SMEs, often with fewer resources and distinct organizational structures, may exhibit different responses to green finance innovation reforms. Understanding how these firms react to such policies would provide a more comprehensive perspective on the overall economic and environmental impact of green finance across a broader spectrum of firms.

Second, while our analysis is concentrated on firms within high-polluting industries in China, future studies could explore the effects of green finance innovation reforms in other sectors or across different countries, particularly in emerging economies. Cross-country comparisons would be particularly valuable in determining whether the mechanisms identified in this study—such as increased R&D investments, the adoption of cleaner production technologies, and output reductions—are universally applicable or vary depending on regional economic, financial, and institutional contexts.

Third, future research could delve deeper into the cultural and organizational factors that influence a firm’s responsiveness to green finance initiatives. Corporate culture, leadership commitment to sustainability, and employee engagement in environmental practices are intangible but crucial factors that may significantly shape the success of green finance policies. Investigating these internal dynamics could provide valuable insights into how green finance innovation is adopted and maintained within firms and across industries.

Fourth, exploring the role of regional and sectoral characteristics is another important area for future research. Investigating how financial development, institutional quality, and industrial competitiveness interact with green finance innovation reforms could reveal the nuanced effects these reforms have on different firms. A more detailed examination of these interactions could help policymakers tailor green finance initiatives to maximize their effectiveness in specific contexts.

Finally, while this study employed a double machine learning approach to address model complexity and endogeneity, future research could benefit from exploring alternative econometric and computational methods. The application of artificial intelligence, network-based models, or other advanced methodologies may provide more refined insights into the dynamic and long-term effects of green finance reforms on firm behavior and environmental outcomes.

Footnotes

Acknowledgements

We would like to express our deepest gratitude to all those who have supported and guided use throughout the completion of this work. We extend our sincere thanks to reviewers and editors for their invaluable insights and expertise, which have significantly shaped the direction and quality of this research.

Author Contributions

“Xiaohui Xu contributed to the study conception and design. Material preparation, data collection and analysis were performed by Xiaohui Xu, Qing Yu, and Yi Liu. The first draft of the manuscript was written by Xiaohui Xu and Chunheng Fu, and Xiaohui Xu and Chunheng Fu commented on previous versions of the manuscript. Xiaohui Xu Xu, Qing Yu, and Yi Liu read and approved the final manuscript.”

Ethics Approval and Consent to Participate

Not applicable

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by Ministry of Education Humanities and Social Sciences Project No. 23YJC790165. Research Project Results of the Zhejiang Federation of Social Sciences (2025N097).

Consent for Publication

Not applicable.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability

The datasets used and/or analyzed during the current study are available from the corresponding author on reasonable request.