Abstract

We use an analytical research model to analyze the effect of the auditor’s personal income tax on audit effort. We show that the auditor’s level of care crucially depends on the tax rate and amount of loss recognition. Taxes may cause paradoxical effects on the auditor’s effort, audit quality, and marginal audit fee if profits and losses are taxed differently or in case of risk-averse decision-makers. Therefore, compared with the pretax setting, taxes have distortional effects. Thus, common auditing standards (e.g., International Standards on Auditing framework) will imply diverse audit quality and marginal audit fees depending on the respective national tax law. Our results are relevant for standard setters, auditors, and financial statements’ addressees.

Introduction

In this study, we investigate the influence of auditors’ personal income taxation on audit quality using an analytical model. Audit quality and auditors’ effort decision are directly linked. We contribute to the analytical audit literature by proving that auditors’ personal income taxation is a relevant factor in auditors’ effort decision.

The study is motivated by standard setters’ concerns about audit quality and the related initiatives to improve audit quality. For example, standard setters’ concerns about audit quality are expressed in the European Union (EU) Market report where the EU Commission (2021) identifies deficiencies regarding audit quality. In a globalized world, the International Auditing and Assurance Standards Board (IAASB) provides a common framework for auditing—International Standards on Auditing (ISA)—to achieve a common and comparable level of audit quality. For instance, these standards were implemented EU-wide in 2016 and additional measures of the EU-Regulation 537/2014 and EU Directive 2014/56/EU became effective in the EU member states.

Although common audit standards exist, national standard setters crucially determine the institutional audit environment by establishing liability systems, for example. This part of the institutional audit environment constitutes the auditors’ potential “downside.” The audit-related risk is that an auditor may fail to exert due diligence and thereby falsely issue an unqualified auditor’s opinion although the financial statements are not in line with the respective accounting principles. The risk for the auditor arises (apart from reputational damages) from the liability regime that defines the consequences for auditors in the event of an audit failure.

A key concept in ISA is professional judgment (ISA 200.16). An auditor must base their opinion on sufficient and appropriate audit evidence. According to the auditing standards, an auditor must spend sufficient time to obtain appropriate audit evidence before issuing an audit opinion (IAASB, 2018; ISA 300.20). Thereby, according to IAASB’s Framework on audit quality, the “time dedicated to the audit” is one key element contributing to audit quality. Empirical evidence suggests that audit effort is positively associated with audit quality (Caramanis & Lennox, 2008; Che et al., 2018; Xiao et al., 2020).

Any professional judgment on “sufficiency” and “appropriateness” is an economic trade-off. For example, audit evidence generated by sampling is, by nature, less reliable than auditing the complete population of documents, but sampling is cost-efficient. Hence, the design of audit procedures (e.g., sample sizes) is the result of an economic trade-off.

Auditors are subject to individual or corporate tax. Particularly, auditors can be considered as tax experts who are aware of tax effects and thus consider tax effects in decision-making (e.g., Kubick et al., 2020; McGuire et al., 2012). Hence, their decision affects the tax base and thereby the distribution of audit-related outcomes (cash flows an auditor receives depending on the situation if an audit failure occurs). Consequently, an economically optimal effort decision requires considering after-tax effects. In general, tax regimes are national, and the audit quality framework is international. Therefore, we explain why even uniform audit regulations may lead to diverse levels of audit quality.

The national tax framework defines the tax base and tax rates. Therefore, tax rates do not reflect tax effects sufficiently. In the context of an economic decision on audit effort, two tax features are important. First, the tax-deductibility of direct audit costs in a profit scenario generates tax savings resulting in decreasing audit cost with increasing tax rates.

Second, in the event of audit failures, liability obligations will likely exceed auditors’ normal annual profit. Hence, the tax regulation of losses and loss carryforwards is relevant. If liability obligations do not generate immediate tax savings, then audit cost and potential audit damage—the two main aspects in the auditor’s economic trade-off in professional judgment—are affected asymmetrically by taxes.

The purpose of this study (research question) is to show how, and under which circumstances, the taxation of auditors affects their audit effort decision. Thus, we analyze the combined incentive effects of audit-specific regulations and tax law on audit effort. This is novel in audit literature.

Asymmetric taxation of profits and losses leads to tax effects for risk-neutral auditors. Because risk-averse individuals may assess taxes systematically differently, compared with risk-neutral individuals (i.e., Domar & Musgrave, 1944; Ewert & Niemann, 2012; Sarkar, 2008), we also expect different effects of taxes on audit effort decisions. Therefore, we cover this effect and give up the simplifying assumption of auditors’ risk neutrality. This is also supported by Amir et al. (2014), who show that, within audit firms, an individual audit partner’s risk preferences will play a crucial role in client-specific audit quality determination.

Our study contributes to analytical audit literature dealing with incentives on audit effort. In this context, several analytical papers address different aspects of the institutional parameters and the effect on audit effort (and the related audit quality). Most of these papers focus on aspects of the liability regime (Bigus, 2015; Deng et al., 2012; Narayanan, 1994; Rothenberg, 2019; Simunic & Stein, 1996). Thereby, different liability regimes result in various incentives on audit effort (London Economics & Ewert, 2006), and a general result is that lower liability is associated with lower incentives on audit effort (DeFond & Zhang 2014). We contribute to extant literature by proving that liability is affected by taxation and thus the assessment of a liability regime requires a combined assessment with the (national) tax system. Hence, our study is also related to those papers discussing EU policy about auditor liability (London Economics & Ewert, 2006; Philipsen, 2014; Samsonova-Taddei & Humphrey, 2015).

Other analytical studies discuss the precision of auditing standards in the context to the incentives from liability regime and show that the effects of liability may depend on the type of standards (Schwartz, 1998; Simunic et al., 2015; Willekens et al., 1996; Willekens & Simunic, 2007; Ye & Simunic, 2013). In this regard, by considering the tax system, we enlarge the perspective of factors affecting the effectiveness of liability regimes. Thereby, we also contribute to the discussion (Simunic et al., 2017) on how the audit environment and characteristics of the legal system influence the effectiveness of auditing standards. In line with this, our results can help to specify the models for empirical investigation in the context of audit quality (He et al., 2017).

Furthermore, we contribute to audit-related literature because the effects of auditors’ income tax and optimal audit effort have not been explicitly covered in the literature (DeFond & Zhang, 2014; Haapamäki & Sihvonen, 2019). The results also contribute to tax management literature, which, in general, focuses on the tax effects of decisions. To our knowledge, no analysis of the tax effects on auditor’s effort exists in tax management literature (Hanlon & Heitzman, 2010). However, tax management literature shows that taxes have an effect of risk-taking, and Ewert and Niemann (2012) analyze those tax effects on risk-taking in a general context of limited liability. Thus, we contribute to the tax management literature by focusing on tax effects in the context of auditor’s liability. Moreover, despite this, there is awareness that taxation of auditor’s profits is an important feature of the institutional audit environment regarding the legal form of an audit firm (Oxera, 2007); this issue has not directly been addressed in previous audit literature investigating incentives on audit quality.

Our analysis of tax effects on auditing is novel; it indicates that taxes may substantially affect auditor’s performance. The analysis reveals two counteracting effects of taxes: Taxes reduce audit risk, if audit-related outcomes are taxable. Decreasing risk is associated with decreasing effort. Simultaneously, taxes reduce the marginal costs of audit effort. That is, a less costly audit effort, all other things being equal, will increase audit effort. The overall effect depends on the assessment of the individual auditor.

We show that audit-related loss recognition is fundamental to the effect of auditors’ income taxes on the optimal audit effort. In general, higher tax rates are associated with lower audit quality. However, it is remarkable that the relationship between a proportional tax rate and optimal audit effort is non-monotonic for risk-averse auditors. An important finding is that, in the context of taxes, an increasing marginal audit fee is conditionally related to increasing audit quality.

Our results indicate that even a common supranational audit framework will imply substantially different audit quality, driven by the respective national tax law. Therefore, if standard setters want to achieve comparable audit quality in globalized markets (Kleinman et al., 2014), the national institutional environment for auditing has to consider the respective national tax effects. Otherwise, distortional tax effects may cause a substantial deviation of intended incentives provided by the audit-specific institutional environment.

For empirical audit research, our results help to understand that less obvious features of tax systems, particularly the system of tax loss recognition, will influence audit quality. Hence, for comparing audit quality, the audit-related framework (e.g., liability regime) and respective tax system must be considered. Thus, studies researching the relationship between liability and audit quality, such as the study by He et al. (2017), should control for tax effects. In general, in countries with high tax rates and a high probability for tax savings from loss recognition, auditors’ pretax risk must be higher (e.g., higher litigation risk because of a higher liability limitation) to induce equal audit quality, compared with low tax countries with strict loss offset restrictions. Predictions for specific countries, however, require a simultaneous assessment of tax effects on auditor’s marginal costs and liability.

The remaining sections of this article are organized as follows. In section “Model,” we first outline our assumptions for modeling the tax and audit environment. Using this framework, we determine auditors’ optimal audit effort—first assuming risk neutrality, and then relaxing the simplifying assumption for risk-averse auditors. In section “Analysis of Tax Effects,” based on auditors’ optimization, we discuss relevant features of the tax regime influencing the optimal audit effort. In addition, we show the relationship between taxes and the auditor’s marginal audit fee. We explain why we particularly focus on audit effort instead of marginal fee although taxes influence both. Then, we introduce a numerical example to illustrate our results before discussing the implications of our findings. Section “Summary and Conclusion” concludes the article.

Model

Model Framework

Audit-specific considerations

Auditing is important for frictionless markets because the public’s reliance on financial statements is encouraged (Newman et al., 2005). An auditor acts on behalf of all addressees of the financial statement, although they are engaged by the client. In general, auditors’ effort and audit quality are unobservable for financial statements’ addressees. Therefore, auditing is a credence good (Causholli & Knechel, 2012). If auditors maximize utility, they might use the unobservability of their audit effort and audit quality to the addressees’/clients’ disadvantage. Against this background, the audit-related institutional environment provides incentives to incentivize an auditor to choose a proper audit-effort level. The institutional environment establishes potential legal consequences in case of an audit failure.

In the audit literature, auditors’ obligation to compensate the audited client/other addressees for damages caused by an audit failure is considered to be a main driver of audit effort and, therefore, audit quality (Deng et al., 2012; Dye, 1993; Laux & Newman, 2010; Schwartz, 1997; Simunic & Stein, 1996; Willekens et al., 1996; Willekens & Simunic, 2007). Therefore, the institutional environment establishes audit-related risk. Compared with ISA, we use a broader definition of audit risk. We define audit risk as the risk to be sued and found liable to compensate parties for damage suffered.

In general, two types of liability regimes can be distinguished (Schwartz, 1997). In a strict liability regime, an auditor unconditionally has to compensate addressees in case of an audit failure. In a negligence regime, an auditor’s obligation to cover audit-related damage is associated with auditors’ due diligence. Although different liability regimes have different effects on the audit effort, there is a general relationship between auditors’ liability and the audit effort. As we focus on the tax implications, we simplify by focusing on the general risk induced by liability without distinguishing among different liability regimes. Below, we explain why the overall audit-related risk in the context of our analysis is more important than the origin of audit-related risk.

Particularly, for listed companies, there exists a market expectation concerning the auditor’s reputation (Gao & Zhang, 2019), although this effect has weakened after the collapse of the Arthur Andersen network (Chang et al., 2010). Higher reputation is, thus, associated with the auditor’s ability to audit clients that are more attractive. An auditor’s error may cause a loss of reputation, independently of any liability (DeFond & Zhang, 2014). Hence, independent of legal consequences of an auditor’s error, a potential loss of reputation may be a relevant incentive to exert due diligence.

Subsequently, we address all negative consequences of an auditor’s error as damage. Without auditing, this damage occurs with a client-specific probability. The auditor will use costly audit technology to reduce the probability of an audit’s error. If the damage is affected by the tax system, and audit-related costs are subject to taxation as well, then taxes may influence auditors’ optimal audit effort. Therefore, we discuss the general tax environment underlying our analysis in section “Tax Considerations.”

Tax considerations

Tax consequences of audit-related costs, or damage, depend on the structure of the audit entity. In general, the organization of an audit entity may vary from a single entrepreneur to corporations. In case of a single entrepreneur, the profit/loss of the audit entity is assigned to the individual auditor and directly taxed using a convex tax schedule. If the audit entity is organized as a corporation, usually two levels of taxation apply. On the first level, corporate taxes are levied. Corporate tax rates are usually proportional. On a second level, taxes based on profit distribution are levied. According to the variety of taxable structures, we focus on corporations because this is a typical organizational form of larger audit firms in the EU. Despite the lack of an overview of the distribution of the legal forms of audit firms within the EU, empirical evidence for Germany (one of the largest economies within the EU) indicates that approximately 85% of audit firms (Big4 and non-Big4 audit firms) are corporations (with limited liability, e.g., WPK [German Chamber of Public Auditors], 2021), which is similarly true for Austria. Nevertheless, the framework presented in this article is also applicable for private partnerships and individual auditors because they are also subject to taxation. Significant differences between the taxation of individuals and corporations typically consist in the taxation of losses and the ability to transfer them in future periods (loss carryforwards). Because of the business judgment rule, which is usually implemented in European legislations (e.g., Austria and Germany), individual decision-makers (auditors) have to act in the interest of the company. Consequently, the appropriate basis for decision-making must also allow for the tax effects on the company.

We analyze the combined incentive effects of audit-specific regulations and tax law. In the context of our analysis, it is important that taxation of regular operating profits/losses may substantially differ from the damage event. For periods without a damage event, it is reasonable to assume that the audit entity is profitable. Thus, tax-deductible audit-related costs will reduce the audit corporation’s tax burden. Therefore, an auditor will only consider net costs.

In case of damage, the tax situation may alter substantially if the assumption of a profitable audit entity is no longer justified. This is likely if damage consists solely of compensations to parties affected by the auditor’s error. In that case, the potential effects of losses carried forward (LCF) must be considered. Tax regulation regarding LCF is diverse in different jurisdictions. Hence, whether damage-related losses will lead to future tax savings is not solely a matter of the future economic performance of the audit entity. If LCF is subject to time constraints, or to a specific company, then LCF caused by auditor’s damage may be lost without future tax savings. Thus, in addition to the economic risk of sufficient future profits, additional legal risk may exist. If the damage is solely a loss of reputation, then it equals a reduction in future taxable profits. Then, limiting LCF regulations will not affect future error-related tax savings.

According to the specific tax environment of an audit entity, there are numerous potential tax consequences of an error. We use the following set of simplifying assumptions to derive general results concerning the relationship between optimal audit effort and auditors’ income tax. The main assumptions are highlighted in section “Specific Assumptions.”

Specific assumptions

The auditors’ core task is to detect and report accounting errors. If the financial statement is adopted according to the auditor’s findings prior to publication, then the financial statement is free of substantial errors. Hence, the auditor will issue an unqualified audit opinion. Otherwise, readers of the financial statement will be informed of an error by a qualified audit opinion. If the auditor fails to detect and report accounting errors, then audit-related damage may occur. However, because of natural limitations, the auditor’s optimal audit effort is determined by an economic trade-off between costly effort and a reduction in error probability. We model the auditor’s optimal audit effort decision by explicitly assuming the following:

The preaudit probability for a damage-causing error is r. This probability represents the contingent probability of all events that are a prerequisite for auditor’s damage (e.g., error probability, that is, probability to be sued and found liable).

Damage D is binary. Direct monetary damage may vary from a deductible arranged in third-party liability insurance contracts to unlimited liability when the auditor offends—for example, rules of independence or in case of an intended error. In addition to direct monetary damage, an undetected error may cause a loss of reputation. This will decrease the auditor’s future income.

Auditors may use costly audit technology to detect and report accounting errors. The postaudit damage probability

We assume vague auditing standards. Hence, the probability that the effort level chosen by the auditor is considered insufficient by a court is always greater than 0 (Gao & Zhang, 2019; Schwartz, 1998).

Any unit of audit effort causes marginal costs of c. Therefore, the costs related to a specific client are

The audit fee F is fixed in terms of not being conditional on the audit outcome (e.g., Hillegeist, 1999).

For a profitable audit firm, we assume a proportional corporate tax rate t.

In case of a damage, the damage is tax-deductible in subsequent periods. We cover loss offset restrictions, or LCF restrictions, by introducing the factor l. This factor represents the relative participation of the tax authorities in case of a loss. For

Auditor’s Optimal Audit Effort

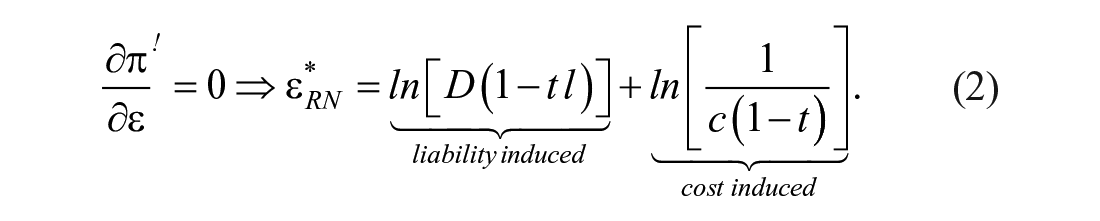

Risk-neutral auditors, in general, base their audit effort decision on the expected profit. Allowing for taxes and the limited loss participation of the tax authorities, auditor’s expected profit (π) is

The auditor maximizes their expected profit if they choose the following audit effort

In general, optimal audit effort is determined by the potential damage D and marginal costs

The second part of Equation 2 is—assuming reasonable parameters again—negative. Therefore, with increasing D, the auditor will increase audit effort, whereas with increasing marginal costs c, the auditor will decrease audit effort.

Tax effects on optimal audit effort only exist if taxes affect potential liability and costs differentially. For

Optimal audit effort determines the direct audit costs and the postaudit error probability and, thus, expected damage. Optimally, marginal productivity must equal marginal costs. Therefore, the expected damage in optimum for a risk-neutral auditor is

Thus, the higher the tax rate, the lower the acceptable expected damage from the risk-neutral auditor’s perspective. The optimized expected damage is not a function of potential damage (D). This results from optimization because marginal productivity is solely determined by the technology function and independent of the potential damage.

An auditor will not participate in the audit market if optimized expected profit is negative. There exists an audit fee F setting the optimized auditor’s profit to 0. We refer to this specific audit fee as the marginal audit fee

Assuming risk neutrality is a common simplifying assumption in the audit literature, in general, decision-makers are not risk neutral. Otherwise, no risk premia in markets will occur. Since Domar and Musgrave (1944), it is known that taxes may be assessed differently, depending on the decision-maker’s risk aversion. We consider this to be important, particularly in the context of auditing because the auditor has to decide on spending unconditional costs to decrease the error (damage) probability. Thus, audit effort can be considered as the insurance premium for reducing the risk of being sued and found liable. The trade-off between unconditional costs and a conditional negative outcome is fundamentally different for risk-neutral and risk-averse decision-makers. Hence, tax effects on audit quality must be expected, even if the expected profit is unaffected by taxes, when the simplifying assumption of risk neutrality is dropped (Bonroy et al., 2013; Farmer, 1993).

There are numerous options to model risk aversion, or loss aversion, in the context of auditing (Burton et al., 2011). It is common to all these options that, in the real world, risk aversion, or loss aversion, is hard to measure (Amir et al., 2014). We do not claim to derive empirically valid predictions of tax effects but aim to discuss tax effects on a general basis. Therefore, we model risk-averse auditors by introducing an exponential utility function, where a represents the individual auditor’s risk aversion:

Auditors’ expected utility as a function of audit effort is

Because of the first-order condition, expected utility is maximized when the auditor chooses the following optimal audit effort:

The audit fee is unconditional. Maximizing expected utility, therefore, equals minimizing (direct and expected litigation) cost-driven disutility. Thus, optimal audit effort is independent of audit fee. The audit fee at least has to compensate the auditor for audit-related disutility. Otherwise, the auditor will not participate in the audit market. We discuss tax effects on this market entry condition in section “Analysis of Tax Effects.”

Again, the optimal audit effort is determined by two parts: The –1 in the logarithm in Equation 6 represents the “no-audit option.” Thus, from an economic perspective, the argument of the logarithm represents the change of utility. Compared with Equation 2, the auditors’ risk aversion matters because potential damage is scaled by the utility function, but marginal costs remain unscaled, as they are unconditional. This is of fundamental difference to the simplifying assumption of auditor’s risk neutrality. A risk-neutral auditor does not deal with audit-related risk at all, but does so with the effects on expected profit. Therefore, the auditor’s individual risk aversion matters in the case of assessing tax effects on optimal audit effort. We discuss these potential tax effects in section “Analysis of Tax Effects.”

Analysis of Tax Effects

Tax Effects on Auditor’s Optimal Audit Effort

Risk-neutral auditors’ tax effects according to Equation 2 are straightforward. In the case of

Dropping the simplifying assumption of risk neutrality results in less obvious tax effects on optimal audit effort. Following an intuition that effects will differ quantitatively, but not systematically, is misleading in the case of risk-averse auditors. Auditors have to balance linear effects on marginal costs to nonlinear effects on potential liability by using an exponential technology function. In the context of taxes and optimal audit effort, taxes may cause a fundamentally different auditor’s assessment of preaudit risk. Jullien et al. (2007) argue that intuition is a poor guide for these types of decisions. In the following, we explore this relationship based, first, on boundary solutions and, second, on the functional relationship between tax rates and optimal audit effort.

We determine a first boundary solution by considering that optimal audit effort must be at least finite. Assuming reasonable parameters, the first part in Equation 6 is positive and finite. Hence, limitations for finite optimal audit effort may arise from the second part. This part is only finite if

holds. We refer to the tax rate as

The derivative of risk-averse auditors’ optimal audit effort with respect to the tax rate is

The first part of the derivative is infinite for

In the center of

The first part in Equation 8 is a concave function of the proportional tax rate because a minimum exists. The second part of the derivative in Equation 8 is negative and monotonically decreasing with increasing tax rates. Thus, up to two extrema of optimal audit effort in the interval

A prerequisite for at least one extremum is

The tax effects on optimal audit effort require

The neutral loss participation

Whenever the tax authority’s participation in auditor’s damage-related losses is not equal to

(All proofs are in the appendix.)

Proportional taxes lower the potential damage with the same rate as marginal audit costs. In case of risk-averse auditors, it must be considered that risk-averse auditors, for determining optimal audit effort, scale the potential net damage according to their utility, and then compare resulting disutility with disutility caused by unconditional audit effort. Accordingly, the auditor’s assessment is that the tax effects on potential damage are subject to utility function, but that the effects on marginal costs are not. Thus, the tax effects on unconditional marginal costs and conditional potential damage can be assessed differently. Considering this, increasing taxes always reduce marginal audit costs. Accordingly, for

For higher levels of tax authority’s loss participation

Thus, for l* ≤ l ≤ 1, increasing tax rates starting from

For tax rates close to 1, net costs converge to 0; however, because of the technology function, a small audit risk remains. Hence, with (theoretical) tax rates close to 1, it is optimal from the auditor’s perspective to increase audit effort. Then, the auditor, with increasing tax rates, will expand audit effort instead of reducing audit effort over lower regions of t. This implies a local minimum.

Overall, according to Proposition 2, with increasing tax rates, risk-averse auditors adopt their strategy to face changing tax rates twice. For low tax rates, they expand their optimal audit effort up to a maximum, and then they decrease audit effort up to the tax rate, for which the effects on marginal audit costs on potential damage are exactly outweighed. These tax effects originate from the different assessment of net preaudit risk and net audit costs. Risk-neutral auditors do not consider risk at all. Thus, in case of the simplifying assumption of auditor’s risk neutrality, these relevant effects remain hidden.

In the case of full loss participation (l = 1), for low tax rates, the situation does not substantially differ from the explanation for Proposition 2. Again, the auditor changes their strategy to face increasing tax rates in the way that they first increase the optimal audit effort, and then decrease optimal audit effort because the tax effects on potential damage outweighs the tax effects on marginal costs. For

The analysis proves that distortional effects of taxes on auditor’s optimal audit effort will occur. Audit technology directly links audit effort to audit quality in terms of the postaudit error probability. Therefore, tax distortions will affect audit quality and thus, simultaneously, auditor’s marginal fee. From an addressee’s perspective, an assessment of tax distortions on auditing requires the analysis of auditor’s behavior and the implicit marginal audit fee, although auditor’s marginal audit fee is solely relevant in highly specific market conditions.

Taxes and Auditor’s Marginal Fee

An auditor will only participate in the audit market if the audit engagement is associated with nonnegative utility. An unconditional audit fee does not influence optimal audit effort, but determines auditor’s utility based on net payoffs. We refer to the particular audit fee exactly offsetting negative audit-related utility as our marginal audit fee

To determine marginal audit fee, we set Equation 11 to 0 and solve for the audit fee F. This leads to the marginal audit fee, where

From an economic perspective, the certainty equivalent is grossed up because the auditor’s risk premium is not tax-deductible, whereas audit costs and audit fee are subject to taxation. The derivative of the marginal audit fee with respect to the tax rate is

The tax effects on marginal fee systematically differ from the tax effects on audit effort. Hence, the minimum price for quality—the marginal audit fee—is effected differently from audit quality. The first part of the derivative for

For the theoretical case of

An important feature of the tax effect on marginal audit fee is that the marginal audit fee for

In general, the auditor’s marginal fee is solely an indicator of audit quality if the market is dominated by audit clients in competitive markets. Otherwise, the market fee is determined by the deviating market mechanism. The results of empirical audit research indicate that audit markets are far away from being fully competitive (Chang et al., 2019). Therefore, we consider the analysis of tax effects on audit effort and directly linked audit quality to be more important than the analysis of tax effects on marginal audit fees. However, our analysis indicates that the combination of tax effects on audit quality and marginal audit fee may result in paradoxical results.

Illustration of Results

We introduce a numerical example to illustrate the stated relationships between the taxes and optimal audit effort. In general, we assume the following set of parameters:

Our model is based on an exponential audit technology. We scale the technology function by marginal costs than introducing an efficiency factor. If marginal costs are €50,000, then the optimal audit effort does not equal audit hours. Based on the parameters, a reduction of preaudit risk by 95% leads to overall audit costs of €149,787.

The certainty equivalent of the preaudit expected damage is €–767,704.67, and if taxes are neglected, it is €−892,704.22. Thus, taxes do substantially reduce preaudit risk. The preaudit expected damage is €−175,000 versus €−200,000 without taxes. The auditor with the assumed utility function, therefore, considers a substantial risk premium.

The optimal audit effort according to Equation 6 is 11.26. Based on the assumed technology function, the postaudit damage probability is 2.565 × 10−6. This substantial reduction of the error probability is explained by the auditor’s risk aversion. The postaudit certainty equivalent is €−477,521.12. It consists of direct audit costs in the amount of €422,409.21 and the risk premium of €55,111.90. Optimally, the expected damage because of the low error probability is €2.56.

The optimized net certainty equivalent according to Equation 11 is €636,694.82. If the auditor receives this audit fee, the tax-deductible direct audit costs are €563,212.28. The tax base is €73,482.54. Thus, the net profit after considering the proportional tax rate of 25% is €55,111.90 and, therefore, equals the expected net damage and the auditor’s risk premium.

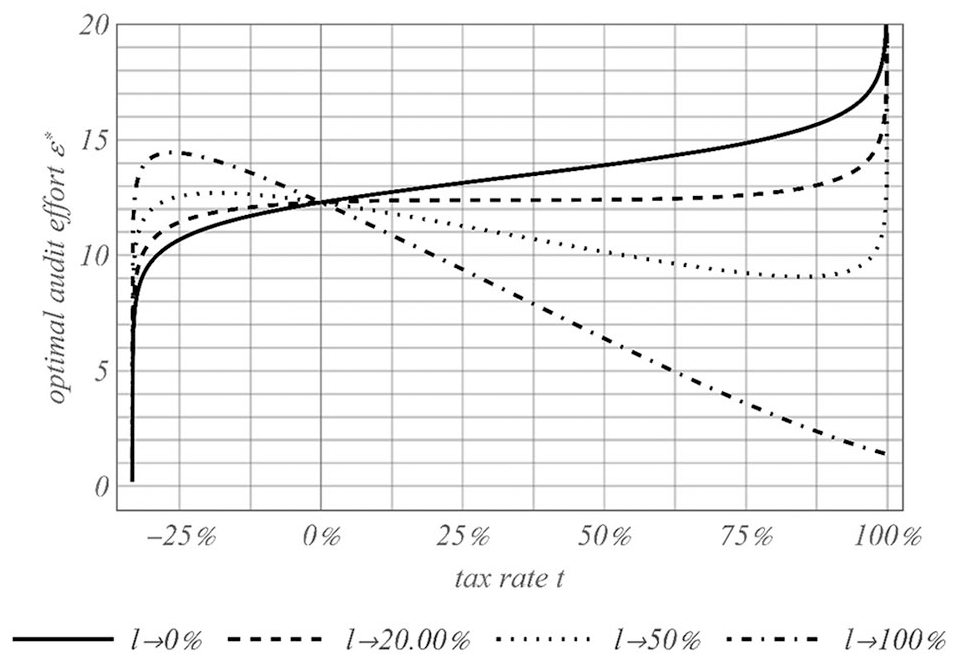

We elaborate on the importance of loss participation in the analytical model. In Figure 1, we show optimal audit effort as a function of the proportional tax rate for

Optimal audit effort and tax rate.

For the set of parameters,

In the case of

Symmetric taxation of profits and losses

In case of

For higher tax authority’s loss participation

The numerical example illustrates the importance of the effect of the tax authority’s loss participation on

The results of the numerical example also underline the importance of the auditor’s risk aversion. This is not limited to the analysis of taxes because for

The numerical example illustrates that the tax effects on audit effort significantly depend on fiscal’s loss participation in case of auditors’ liability payments. In general, less constrained loss-offset and loss carryforwards regulations are related to lower audit risk. The extent of fiscal’s loss participation (by tax-deductibility of losses) depends on the tax regulations and on the profit situation of the audit firm. The following scenarios, regarding the fiscal’s loss participation (l in the model context) and the audit firms’ economic situation, are to distinguish

If low damages that are covered by the profits of the audit firm lead to a full loss participation of the fiscal because the tax-deductibility immediately lowers audit firm’s tax, the audit entity’s future profits—and, thereby, firm value—are impaired, resulting in a lower tax burden. This is also true if damage occurs in terms of a reputational loss. In these cases, l is (close) to 1, representing a fiscal’s full loss participation.

If damage exceeds the profit of the current period but the audit firm is a going concern, then damage payments cannot be fully offset against the tax base from current operations. In such cases, tax regulations for loss carryforwards become relevant. Whether losses can be offset in future periods depends on the ability (of the audit firm) to generate profits in future and restrictions concerning the use of loss carryforwards. In these scenarios, fiscal’s loss participation can be considered in the interval of 0 to 1.

In general, damages related to audit failures may put the audit firm’s going concern at risk. In case of bankruptcy, loss carryforwards usually expire as they cannot be transferred to other profitable entities.

Hence, tax consequences in case of an audit failure may cause diverse after-tax payoffs even in a given pretax liability regime. Therefore, auditors’ risk, as the basis for his professional judgment, depends on the audit firm’s income tax. This implies that empirical studies about audit effort and audit quality should control for aspects of asymmetric taxation (i.e., loss carryforwards) as part of the legal audit environment. Moreover, the considerations suggest that, in the context of loss carryforwards, the economic performance of an audit firm is relevant. In general, more profitable audit firms will face lower audit risk due to potential fiscal’s loss participation compared with less profitable companies, which face the pretax expected damage.

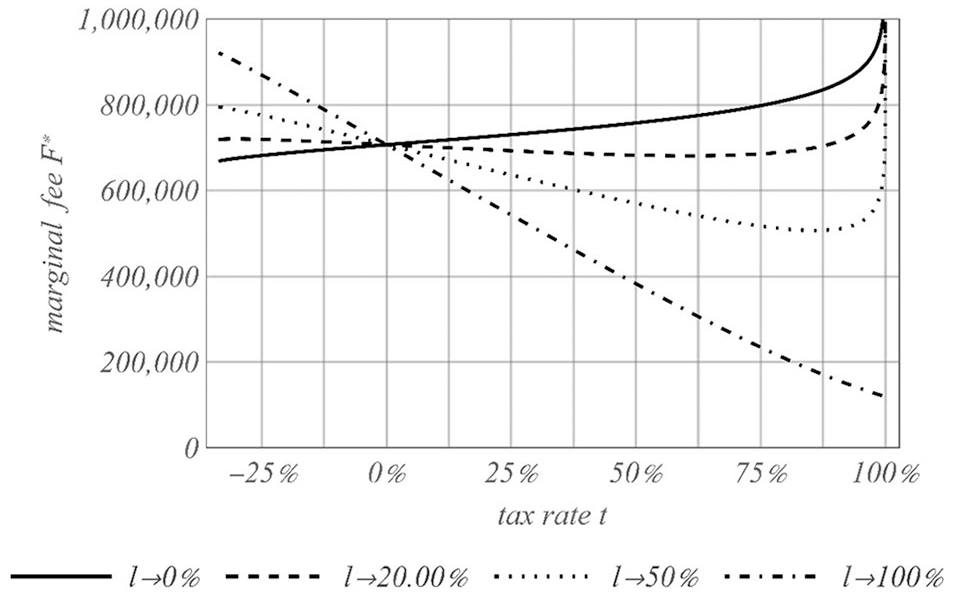

Audit effort is linked to expected liability. Theoretical analysis of marginal audit fee has proven that tax effects on the auditor’s marginal fee differ from the effects on optimal audit effort. In Figure 2, we show graphs for auditor’s marginal fee for different levels of fiscal’s loss participation:

Marginal audit fee and tax rate.

In case of fully asymmetric taxation

Comparing tax effects on audit effort—a proxy for quality—and on marginal audit fees, we can sum up that audit fees are less sensitive, compared with audit effort, if tax rates change. From an addressee’s perspective, this is unfavorable, because lower quality becomes more expensive if taxes are considered.

Summary and Conclusion

In this study, we analyzed the effects of a financial auditor’s income tax on his optimal audit effort based on an analytical model. We focused on audit effort as a proxy for audit quality. Our key aspect was that we focused on after-tax instead of pretax outcomes as a basis for an auditor’s professional judgment The main results of the analysis were that optimal audit effort is mainly driven by the auditor’s risk aversion, the tax rate, and the level of fiscal’s loss participation in case of an audit failure. Considering the auditor’s income tax in the context of his professional judgment, in regard to the optimal audit effort level, is novel.

The study of the relationship between the auditor’s income tax and his audit effort decision is a special form of economic analysis of tax law and audit regulations because there are interactions between the auditing standards, with the purpose of ensuring high audit quality and tax law. In case of a—usually implemented—convex tax system, the auditor’s income tax may have a significant effect on audit effort decision. On one hand, after-tax direct audit costs are unconditionally lower than in a pretax perspective. Therefore, the use of audit technology is less costly in an after-tax perspective, resulting—all things being equal—in higher optimal audit effort implying higher audit quality. On the other hand, the after-tax assessment of audit-related risk depends on the fiscal’s loss participation. In convex tax systems, the audit-risk-related losses may not induce corresponding tax savings. Thus, the audit-related after-tax risk profile is asymmetrically influenced by the auditor’s income taxes. The overall assessment of tax effects depends on the auditor’s risk aversion.

The results are relevant for auditors who must make a reasoned decision about the appropriate audit effort level, considering all relevant factors of the decision environment. The expected response of auditors to the institutional audit environment is, in general, relevant for standard setters because the standards aim to incentivize auditors behaving in a certain desirable way and thereby delivering sufficient audit quality. Consequently, interactions between audit-specific standards and tax law must be considered in the standard-setting process to ensure that standards do have the desired effects. At least the definition of auditor`s liability and the definition of elements of the tax system (i.e., tax rate, tax exemptions) are in the sphere of national policy makers who should be aware of the interaction between auditing standards, liability regime, and taxation of auditors.

Despite the standard setters’ objective to provide uniform audit quality in globalized markets, our analysis suggests that international auditing standards must be seen in a national tax context. Taxes may influence audit effort substantially. Hence, even an internationally uniform set of standards will not provide uniform audit quality.

The results of our analytical study should be useful for empirical audit research because we show that auditor’s income tax may be an important driver of audit effort and therefore audit quality. Hence, not controlling for relevant aspects of the respective national tax system may limit the explanatory power of empirical studies—in particular, of studies with an international focus comparing audit quality in different countries with differences in tax law.

Due to the nature of analytical research, our study has limitations because the findings are developed within a specific set of (simplifying) assumptions. Having the shortcomings of analytical models in mind, our model provides a useful framework to analyze the potential effects auditor’s income tax have on audit quality.

The results of the model are helpful to generate predictions for empirical research and implications for standard setters if the underlying assumptions and their limitations are considered. Hence, the provided analytical model in this study may serve as a starting point for further research to consider tax effects in the auditor’s decision environment, which is relevant to the determination of audit effort.

The empirical analysis of tax effects is often limited by the availability of relevant data because, in most jurisdictions, tax files are private information and not publicly available or can only be observed on an aggregated level. In the context of decision-making in auditing, it is also relevant to consider that major audit failures are—fortunately—infrequent events. Hence, conclusions of singular events are an unlikely representative for the whole population. To overcome limitations of measurability of private tax information and limited observability of motives in auditor’s professional judgment, we suggest applying an experimental approach to further investigate the relationship. The experimental approach enables the research to control for tax effects (and related parameters such as the risk aversion) on audit effort decision. Thus, from our perspective, further research is required to analyze tax effects. The results of our analytical study can serve as a starting point.

Footnotes

Appendix

From Equation 8, the derivative of risk-averse auditor’s optimal audit effort

Acknowledgements

The authors would like to thank the discussion participants at various conferences, where we presented earlier versions of the article, for valuable suggestions and improvements.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research and/or authorship of this article.