Abstract

This study examines the impact of audit firm chairperson narcissism on audit market competition and quality in Turkey from 2013 to 2022. Recent research explores the effects of narcissism in company executives and auditors on firm outcomes. This paper focuses on how audit firm chairperson narcissism influences audit firm competition and audit quality. Chairperson personality traits are analyzed in terms of their influence on strategic decisions, using Upper Echelons Theory. Narcissism is measured through signature size, competition by revenue share and market position, and audit quality by discretionary accruals, reporting aggressiveness, and small profit reporting. Ordinary Least Squares, Logistic regression are mainly performed, then System GMM, and Propensity Score Matching are used to address endogeneity. Results show that narcissistic chairpersons negatively impact both competition and audit quality. This research contributes to understanding the role of chairperson narcissism in audit firms, particularly in emerging markets like Turkey.

Keywords

Introduction

The topic of narcissism has captured the attention of both researchers and the general public. Studies and discussions have explored narcissism in various groups, including psychiatric patients, students, celebrities, chief executive officers (CEOs), individual auditors and even American presidents (Miller et al., 2021). While several papers investigate the effect of top managers or individual auditors with narcissistic personality on the company financial quality or audit quality, some of them research the impact of CEOs or top managers on the company performance (Blair et al., 2017; Chatterjee & Hambrick, 2011; Chou et al., 2021; Khaksar et al., 2022; Li et al., 2014; Rosenthal & Pittinsky, 2006; Salehi et al., 2022). Regardless of its perspective, there is evidence that narcissism has an impact on company & audit firm’s outcomes such as performance, audit quality, or financial reporting quality.

Upper echelons theory, as proposed by Hambrick (2007), suggests that a firm’s strategic decisions are at least partially shaped by the personality traits of its top executives. The theory posits that executive perceptions, cognitions (thought processes), and values may play a significant role in shaping the firm’s decision-making process. These underlying factors, in turn, significantly influence an organization’s strategic direction and overall performance, potentially leading to positive or negative outcomes. Audit work is performed by individual auditors on the behalf of audit firm (Hereafter AF or AFs) (Ocak, 2024). According to the Independent Audit Regulation of Turkey (2012) (IART), the chairperson of AFs in Turkey, acting as the legal representative of the AF, is the key leader and principal decision-maker of the AF. They exercise control over the AF and auditors and have a significant influence on strategies regarding audit quality, client acceptance or dismissal, and AF competition (Lent, 1999). Therefore, the personality of the chairperson of AF will affect the AF's output such as its market competition and audit quality.

This study investigates the impact of AF chairperson narcissism on market competition and audit quality. Narcissism is measured by the logarithmic value and scaled size of chairperson signature. AF market competition is assessed using the percentage of total annual revenues, independent audit revenues, and the market share difference between an AF and its closest competitor. Audit quality is measured by discretionary accruals, audit reporting aggressiveness, and small profit presence. Ordinary Least Squares (OLS) and Logistic regression are used for hypothesis testing, and System GMM and Propensity Score Matching are employed to address endogeneity and enhance result validity.

This study contributes to the extant literature in several ways. First, it utilizes upper echelons theory to construct the theoretical framework of a potential association between AF chairperson narcissism, audit quality and AF market competition. This theory suggests that the firm's decision-making process is greatly influenced by the perceptions, cognitive processes, and values of its executives. It can thus be argued that the chairpersons of AFs with narcissistic personality, have a strong impact on decisions such as audit quality policies and AF market competition made by the chairpersons in terms of AFs. This study supports the emphasis of upper echelons theory.

Second, there are much research regarding the importance of individuals’ narcissism such as individual auditors, CEOs on companies’ outcomes such as financial reporting quality (Anderson & Tirrell, 2004; Kontesa et al., 2021; Olsen et al., 2014), performance (Ham et al., 2018; Tett & Burnett, 2003), or audit quality (Chou et al., 2021; Rosenthal & Pittinsky, 2006). However, they do not discuss the importance of AF chairpersons’ narcissism on AF market competition and audit quality. Since AFs’ chairpersons as acting as the legal representative of the AF, is the key leader and principal decision-maker of the AF even though the audit of clients is performed by individual auditors, AFs’ chairpersons have control over the staff (Bass & Steidlmeier, 1999; Blair et al., 2017). Their manipulative nature will cause employees to have manipulative tendencies in the decisions when they perform an audit. Besides, narcissism, which conflicts with the collaborative nature of teams, is likely to hinder team performance (Tett & Burnett, 2003). This issue negatively impacts on organizational outcomes such as the degree of audit market competition. This study is the first study that investigates the effect of AFs’ chairpersons on audit market competition and audit quality.

Lastly, audit research mostly use AFs in developed countries or cross-country datasets. Turkey is an emerging country and follows international regulations regarding AFs. AF organizational structures may differ from organizational structures in Europe or other countries. Besides, AF research of emerging countries is scarce in AF literature. This study tries to contribute to the extant literature using emerging country and providing the importance of the chairpersons of AFs.

Our main findings are consistent with conjecture. Narcissistic chairpersons of AFs negatively affect the AF market competition and audit quality. System GMM and Propensity score matching results indicate that there are no endogeneity issue, and the results of these procedures are in accordance with the main results.

The study is structured as follows: Sections “Institutional Settings and Cultural Background” and “Theoretical Underpinnings” cover Turkey’s institutional setting, cultural background, and theory. Section “Literature Review and Hypothesis Development” reviews the literature and develops hypotheses. Section “Research Design” outlines the research design. Section “Results” presents results, and the final section discusses conclusions, implications, and limitations.

Institutional Settings and Cultural Background

The audit mechanism in Turkey operates on two levels. While all companies are subject to tax audits, companies listed on Borsa Istanbul are also subject to independent audits. Tax audits are conducted by the Ministry of Finance of Turkey and Sworn-in Certified Public Accountants, whereas independent audits are carried out by AFs authorized by the Public Oversight Board of Turkey (POA, hereafter) and the Capital Markets Board of Turkey. Independent AFs emerged in Turkey in the 1960s and 1970s. MUHAS, founded by Touche Ross in 1967, and Arthur Andersen, established in 1975, were among the first (Güvemli & Özbirecikli, 2011; Sanlı & Özbirecikli, 2012). The Turkish audit market is an emerging market, and according to the POA's statistics, while there were 3,452 audit engagements in 2013, this number increased to 15,689 as of 2024.

Audit regulations in Turkey are multi-layered. The POA regulates independent auditors and AFs, while the Capital Markets Board oversees companies in capital markets. The Banking Regulation and Supervision Agency governs bank audits, and the Turkish Commercial Code references these regulations. The Ministry of Finance oversees tax regulations, applying them to Borsa Istanbul-listed companies, which are also subject to the POA and Capital Markets Board for independent audits.

According to the POA, 414 AFs are registered by POA as of 2024. But several AFs have a permission to audit companies quoted in Borsa Istanbul. As of 2022, there are 94 AFs that have public interest entities to audit. AFs in Turkey are required to be established as a capital company such as a joint stock company in compliance with the Independent Audit Regulation of Turkey (IART, 2012), which was issued in 2012 by the POA. As per the Capital Market Board of Turkey's Communiqué No. X-22 (2006), AFs are exclusively permitted to be structured as joint-stock companies, which differs from the practices observed in European nations whereas AFs can exist as Limited Liability Partnerships or Limited Liability Corporations [as mentioned in the Oxera (2007) report]. The publication of annual transparency reports by AFs is required by the Eighth Company Law Directive of the European Union. The stipulations outlined in Article 40 of the European Union Directive bear resemblance to those specified in the Article 36 issued by the Independent Audit By-Law on 26th December 2012 in Turkey.

AFs in Turkey include Big 4 firms (PwC, KPMG, E&Y, Deloitte), second-tier firms like Mazars and Grant Thornton, and local AFs. Arioglu et al. (2024) report that 55% of non-financial Borsa Istanbul-listed firms are audited by Big 4 AFs. Ocak (2021) notes that Big 4 firms operate through network firms, such as Başaran Nas (PwC) and Güney (E&Y). Some international AFs have multiple network firms, like HLB Saygın and Vezin (HLB International) or Engin and Eren (Grant Thornton). Local AFs are often founded by former government auditors.

In Turkey, AFs responsible for auditing the financial statements of public interest entities are typically organized as joint-stock companies. Under Turkish Commercial Law (2011), joint-stock companies differ from limited liability companies in governance. Limited liability companies have a manager, while joint-stock companies have a board of directors and a general assembly. In both, managers and board members are personally liable for public debts (Ocak, 2024). AFs are overseen by a board of directors (Ocak, 2024), and in Turkey, as in other Borsa Istanbul-listed firms, the major shareholder or founder—especially in local AFs—often serves as chairperson with significant power. The chairperson of an AF plays a critical role in ensuring audit quality and enhancing the AF's competitive edge (Lent, 1999). Chairperson of AFs are elected by board members (Oxera, 2007). The procedure of the selection of AF chairperson, the duties of boards and its chairpersons are regulated by the Turkish Commercial Law (2011).

As of 2022, 444 companies are quoted in Borsa Istanbul. Most operate in manufacturing. Despite 414 AFs, only 94 are authorized by Turkey’s Capital Markets Board to audit Borsa Istanbul-listed companies. Companies quoted in Borsa İstanbul should be audited by authorized AFs. POA mandates that AFs (individual auditors) must take a 3-year break after providing services to a company for seven (five) consecutive years.

Turkish culture is collectivist, with power distance and low uncertainty tolerance (Bilgin & Kutlu, 2022; Cohen & Özsoy, 2021). Collectivist regions exhibit higher narcissism than individualistic ones (Li & Benson, 2022). Turkey, a secular democracy with a Muslim majority, blends Islamic and Western influences (Karakas et al., 2015; Arslan, 2001). Islam is tied to national identity, and its work ethic emphasizes intention over outcomes, rejecting unethical actions regardless of benefits (Qasim et al., 2022). Thus, AF chairpersons’ narcissism may have distinct effects within Turkey’s cultural and ethical context.

Theoretical Underpinnings

Upper echelons theory offers a logical and fitting lens because it establishes a link between a leader’s characteristics and motivations, and the ultimate outcomes of the organization (Hambrick & Mason, 1984). The idea that managers aren't interchangeable parts of a company is a core principle of Hambrick and Mason’s (1984) upper echelons theory. This theory proposes that a manager's background, values, and personality influence their decision-making regarding the firm. As a result, different managers facing the same situation might make distinct choices. Various studies investigate how executive personality traits influence corporate decision-making to gain a deeper understanding of leadership styles (Ham et al., 2018). Upper echelons theory, which examines how top-level executives influence firms, emphasizes the importance of considering psychological properties of executives when studying corporate outcomes (Hoskisson et al., 2017). For example, several studies examine the impact of executive overconfidence on various firm behaviors, including investment strategies (Malmendier & Tate 2005), management forecasts of earnings (Hribar & Yang, 2016), and even the likelihood of accounting fraud (Schrand & Zechman 2012).

The board serves as the primary governance and oversight AF. It is tasked with safeguarding the interests and reputation of the AF and its partners, as well as overseeing the strategic management and operations of the AF. Boards are ultimately responsible for more detailed matters such as audit quality, operational performance, and risk management (Fu et al., 2015). According to the IART (2012), AFs that conduct audits on Borsa Istanbul are organized as joint stock companies., the board of directors of these AFs represents the managing body. Board chairperson is top executive of AF. In Turkey, chairpersons are key persons and hold significant power in AFs. They are typically either the founder-owners with substantial ownership stakes or individuals who have worked at the company for many years, especially in cases where the founder is no longer alive. Employees share their chairperson’s view, because the executives in AFs shape AF culture and AF culture determines the values, ethics and attitudes shared by auditors. Thus, the mindsets of AF employees are influenced by the execute of AF (Kritzinger and Barac, 2025). From this perspective, if the chairperson of AF is narcissistic, it will affect audit quality and audit market competition.

Literature Review and Hypothesis Development

Literature Review

Narcissistic individuals often demonstrate a deficit in empathy and exhibit an inflated sense of self-importance. This manifests as an unwillingness to acknowledge or identify with the emotions and needs of others and frequently harbor a belief in their own specialness and uniqueness (Davis et al., 2008; Houlcroft, 2014) and prioritize one's own needs and desires, often at the expense of others (Weidmann et al., 2023). Individuals with narcissistic tendencies are driven by a strong desire for achievement, power, and status (Abdel-Meguid et al., 2021), they have a lack of empathy for others, with narcissists readily exploiting situations and people for personal gain (Cragun et al., 2020). People with high trait narcissism are characterized by an inflated sense of their own importance, a belief they deserve special treatment, and a preoccupation with themselves (Gignac & Zajenkowski, 2021). Narcissistic tendencies are linked to unethical and exploitative behaviors, including cheating, financial crimes, and disruptive actions at work (Grijalva et al., 2015; Johnson et al., 2013). Narcissistic individuals are less likely to exhibit actions that foster a positive social and psychological climate, while simultaneously being more prone to behaviors that intend to harm the organization and its employees (Judge et al., 2006). Recent studies have examined the negative impact of narcissism at the corporate level and auditor levels.

Grijalva et al. (2020) argue that teams with higher average narcissism or many narcissists in key roles experience poorer coordination and lower performance. Since teamwork depends on collaboration, traits like narcissism can significantly impact team dynamics (Li et al., 2014). Ham et al. (2018) find that narcissistic CEOs are linked to several negative outcomes for the company. Companies led by narcissistic CEOs exhibit lower financial productivity, as evidenced by profitability and operating cash flow. Aabo et al. (2021) find a less favorable stock market response to acquisitions announced by companies led by narcissistic CEOs. Al-Shammari et al. (2022) examine the relationship between CEO narcissism and corporate social responsibility performance (CSR). Their findings support an inverted U-shaped relationship, suggesting that CSR efforts increase with CEO narcissism up to a certain point, followed by a decrease. Additionally, the study provides evidence that CEO power moderates the association between CEO narcissism and CSR, aligning with our arguments. Hou et al. (2025) find that CEO narcissism is linked to lower credit ratings.

The negative aspects of narcissism can manifest in a company's performance through volatility, increased financial risk, legal vulnerabilities, a tendency toward overinvestment, and ultimately, lower financial productivity (Garcia-Meca et al., 2021). Abusive supervision, characterized by morally reprehensible behaviors like lying to subordinates, bad-mouthing them, or shifting blame for mistakes (Gauglitz et al., 2023), can have a detrimental impact on both individual employees and the organization as a whole. Blair et al. (2017) link narcissism to unethical behaviors in leadership assessments, finding that highly narcissistic individuals exhibit traits like one-way communication, control, insensitivity, unrealistic judgments, and manipulative communication.

A number of previous studies explore the connection between narcissism and increased risk-taking behavior (Campbell et al., 2004). For instance, Ingersoll et al. (2019) suggest that narcissistic CEOs invest more heavily in risky items, such as research and development. This link often translates into CEOs making riskier decisions in pursuit of recognition (Chatterjee & Hambrick, 2011) or manipulating policies to achieve their desired outcomes (Buyl et al., 2019; Olsen et al., 2014). Existing research also highlights a pattern of questionable behavior among narcissistic CEOs. This behavior can be characterized as unethical, deceptive, illegal, reckless, or purely self-serving. Examples include engaging in fraud (Rijsenbilt & Commandeur, 2013), manipulating financial information (Capalbo et al., 2017), taking advantage of corporate tax loopholes more frequently (Olsen & Stekelberg, 2016), and even resorting to fraudulent financial reporting (Rijsenbilt & Commandeur, 2013). Johnson et al. (2021) explore how personality traits impact risk assessment in audits. The research involves simulated interviews with CFOs displaying varying degrees of narcissism in a quasi-experiment. The results raise concerns that auditors might downplay the risk of fraudulent financial statements when interacting with narcissistic clients.

According to Rijsenbilt and Commandeur (2013), narcissistic senior managers may resort to aggressive and risky tactics to gain admiration. Rijsenbilt (2011) and Campbell et al. (2011) identifies a strong link between reported instances of corporate fraud and CEOs who scored high on a measure that assessed narcissism across multiple dimensions. Theoretical frameworks suggest that narcissistic CEOs favor clear-cut financial reporting to overly enhance the company's image (Amernic & Craig, 2010). Kontesa et al. (2021) find that highly narcissistic CEOs are more likely to engage in earnings management to boost their ego by portraying a stronger financial position. Shen et al. (2024) find that CEO narcissism is linked to speculative accounting behaviors, such as the prompt recognition of positive news and more cautious financial reporting of expected negative news.

The inherent flexibility within accounting allows managers to make strategic accounting choices that can inflate reported earnings, potentially serving to enhance their self-image (Olsen et al., 2014). CEOs with narcissistic tendencies may be inclined to manipulate accounting figures to create an illusion of stronger financial performance, potentially driven by a desire to bolster their self-image (Anderson & Tirrell, 2004). Amernic and Craig (2010) discuss that narcissistic CEOs may engage in accounting policy choices and earnings management decisions motivated by self-preservation and ego protection. A defining characteristic of narcissistic CEOs is their tendency to set unrealistic and unattainable goals, fueled by an inflated sense of self-importance (Garcia-Meca et al., 2021). In pursuit of these goals, they may be inclined to engage in questionable behavior if it promises increased admiration and a bolstered reputation. This propensity for risky actions underscores the significant influence narcissistic CEOs can exert on a firm's overall outcomes.

Salehi et al. (2022) find that narcissism in managers is associated with better performance, while the opposite is true for auditors. On the one hand, narcissists with high self-esteem and a desire for admiration might be more likely to prioritize independence, viewing it as necessary for their reputation as top auditors (Judge et al., 2006). However, their inflated sense of importance could also lead them to compromise independence to maintain relationships with prestigious clients, potentially harming audit quality (Rosenthal & Pittinsky, 2006). Interestingly, narcissists tend to resist social pressure to conform (Chou et al., 2021). If bending the rules to keep clients is somewhat common practice (Krishnan, 1994), a narcissistic auditor might be less likely to follow suit. While this could lead to client losses, narcissists are generally more comfortable taking risks (Maccoby, 2004), so the potential for lost business might not be a major concern. Auditors with stronger dark triad traits (personality characteristics including narcissism, psychopathy, and Machiavellianism) seem to be less likely to lose their professional skepticism when interacting with managers. This might be because they tend to be less emotional, have lower empathy, and are less influenced by social cues (Hobson et al., 2020). On the other hand, Safarzadeh and Mohammadian (2024) state that a higher degree of narcissism in auditors results in increased professional skepticism, which can ultimately improve the quality of the audit process. Also, Kerckhofs et al. (2024) indicate that narcissism is positively linked to the probability of audit partners issuing going-concern opinions for financially distressed clients, as well as to higher audit fees. Overall, the impact of narcissism on independence seems to be a double-edged sword.

Since auditors essentially vouch for the accuracy of financial statements, their own qualities directly impact the credibility of this information. Auditors rely heavily on judgment throughout the audit process, making their inherent characteristics particularly important. A recent study by Samagaio and Felicio (2022) finds a link between an auditor's personality and the quality of their audits. This suggests that certain personality traits might influence how well an auditor performs their job. One such characteristic is narcissism, which can influence how auditors approach their work (Khaksar et al., 2022). An auditor's narcissism may lead them to be inflexible during negotiations, rigidly adhering to their own positions. This unwillingness to compromise could potentially hinder the quality of their audit work (Khaksar et al., 2022). Church et al. (2020) conduct a three-part study in China to explore how auditor narcissism impacts auditor-client negotiations. The researchers propose that narcissistic auditors are more competitive and assertive during negotiations. They argue that this might lead to extended discussions but ultimately result in more conservative financial reporting for the client. Their findings support this theory. According to Kong (2015), individuals high in narcissism are less likely to find common ground during negotiations. They tend to focus on asserting their own views, which could potentially impact the quality of their audit work.

Narcissism has a dark side. Its egocentric traits—inflated self-importance and a need for admiration (Rosenthal & Pittinsky, 2006)—can harm audit quality. Narcissistic partners may aggressively attract prestigious clients to boost their status (Chou et al., 2021), risking independence by tolerating dubious financial reporting. Their self-centeredness can hinder team decision-making, reducing audit quality (Chou et al., 2021). Additionally, they may make biased judgments, leading to inaccurate financial reports (Banimahd et al., 2013).

Auditor narcissism is linked to both audit quality and AF competition. Mohammadi et al. (2021) find that highly narcissistic auditors are less common in competitive markets, measured by auditor and client concentration and competitive pressure. They also report that greater competition improves audit quality. Previous studies examine how narcissistic executives and auditors influence company performance, audit quality, and financial reporting. This study, however, explores the impact of narcissistic AF chairpersons on AF competitiveness and audit quality. Before the hypotheses are presented, their rationale is outlined.

Hypothesis Development

More recently, AF leaders have highlighted AF culture and tone at the top as comprehensive solutions to control auditors' behavior, enhance audit quality, and restore public trust in the profession (Alberti et al., 2022). According to the IART (2012), the chairperson of AFs in Turkey, acting as the legal representative of the AF, is the key leader and principal decision-maker of the AF. They exercise control over the AF and have a significant influence on strategies regarding audit quality, client acceptance or dismissal, and AF competition (Lent, 1999). Chairpersons have power in the AFs, they are generally founder-owner with high shares in the AF ownership structure, or they are people who have worked in the same AF for years, where the founder is not alive. If the chairperson of AF has narcissistic personality, it influences the values and ethics shared by the employees of AFs (Kritzinger & Barac, 2025), thus have an impact on AF market competition and audit quality.

Narcissistic tendencies are associated with unethical and exploitative behaviors, such as cheating, financial crimes, and disruptive actions in the workplace (Grijalva et al., 2015; Johnson et al., 2013). Unethical leaders prioritize their egos over the needs of their followers. They exert excessive control and exploit others for personal gain. These leaders manipulate and deceive, resorting to tactics like falsifying information, sowing distrust, or shifting blame. They favor certain individuals to serve their own interests, rather than empowering their entire team (Blair et al., 2017). They may underestimate the resources needed to succeed (Bass & Steidlmeier, 1999). Lastly, unethical leaders are masters of manipulation. They readily resort to blatant tactics like exaggerating past accomplishments or making false promises about the future (Bass & Steidlmeier, 1999). This manipulative behavior aligns with narcissism. Narcissists are known for their deceitfulness and a tendency to inflate their abilities and performance (Glad, 2002; Paulhus et al., 2002).

This study measures audit quality using discretionary accruals, audit report aggressiveness, and the presence of small profits. Small profits indicate companies use discretionary accruals to attract investors (Burgstahler & Dichev, 1997). Higher audit report aggressiveness suggests lower tolerance for earnings management, making auditors less likely to issue modified opinions (Chen et al., 2017; Gul et al., 2013). Discretionary accrual magnitudes reflect how auditors/AFs limit or allow earnings manipulation and their adherence to accounting standards (Hoitash et al., 2007; Lawrence et al., 2011). High discretionary accruals indicate greater auditor tolerance for earnings management. Although the audit is carried out by individual auditors on the behalf of AF (Ocak, 2024), audit outcomes such audit opinion issued by individual auditor, as the magnitudes of discretionary accruals that tolerated by individual auditor, will be approved by the chairperson of the AF, particularly by narcissistic chairpersons. Across all levels of an organization, employees make judgments about the information they receive from others. This evaluation process involves assessing the credibility of the source. After all, information providers can be motivated by personal gain or organizational pressure to manipulate accounting data (Johnson et al., 2024; Maines & Wahlen, 2006). Narcissistic chairpersons have control over the staff (Bass & Steidlmeier, 1999; Blair et al., 2017). Leaders indicate to employees which norms and values such as which actions are sanctioned, what decision is measured and rewarded; what types of people are selected, recruited, and promoted; and what attitudes and behaviors are communicated and reinforced are encouraged or discouraged, these actions help shape the organization’s culture (O’Reilly et al., 2020). Narcissistic leaders such as AF chairpersons can pressure auditors to rush audits, disregard protocols, or overlook warning flags in financial records (Rehan et al., 2023). Employees who work under narcissistic leaders are more prone to withholding information, neglecting their duties, being frequently absent, and even engaging in sabotage (O’Reilly & Chatman, 2020). Their manipulative nature will cause employees to have manipulative tendencies in the decisions when they perform an audit.

The communication style of chairpersons having narcissistic personality affects the performance of company. Persons having narcissistic personality exhibit one-way communication style (Blair et al., 2017). They often shut down negative feedback on their ideas and show little tolerance for dissenting voices. This controlling behavior likely stems from narcissism (Blair et al., 2017). Narcissists, with their inflated sense of self-importance, may view others' contributions as irrelevant and feel entitled to dictate their will. Furthermore, they struggle with criticism, externalizing blame or dismissing negative feedback entirely (Dimaggio et al., 2002). As discussed by Blair et al. (2017), these behaviors, like ignoring valuable input from colleagues, likely contribute to a decline in employee job satisfaction and wellbeing, increased job stress and intention to quit, and a negative work environment and create ultimately toxic work cultures (Asrar-ul-Haq & Anjum, 2020; O’Reilly et al., 2014). A high concentration of narcissists in key positions such as AF chairperson, experience poorer coordination and ultimately lower performance (Grijalva et al., 2020). Since effective audit work depends on audit partners or audit team members working well together, those in key positions have personality traits such as narcissism can significantly impact team dynamics and performance (Li et al., 2014). Because, narcissism, which conflicts with the collaborative nature of teams, is likely to hinder team performance (Tett & Burnett, 2003). This issue negatively impacts on organizational outcomes such as the degree of audit market competition.

Research Design

Sample Selection

Transparency reports of AFs in Turkey is signed by the chairpersons of the boards of AFs and published accordingly. The signatures utilized to measure narcissism are included in these reports. Besides, these reports include much information about AF governance structure such as board structure, ownership structure, total number of public interest entities, total amount of revenues. Transparency reports of AFs in Turkey have been published since 2013. Besides, the sample ends in 2022 because transparency reports for 2023 had not been published at the time data collection was initiated. The sample covers AFs between 2013 and 2022. Variables employed in the first model are hand-collected and obtained from the transparency reports of AFs. The final sample for first model is presented in the Panel A of Table 1.

Final Sample.

Besides, this paper investigates the association between AF chairperson narcissism and audit quality. To estimate this association, company level sample is employed. Chairperson and AF level characteristics are obtained from the transparency reports of AFs. Individual auditor (i.e., Engagement partner) attributes are obtained from audit reports and their Linkedin profiles. First, engagement partners’ names were obtained from company audit reports, and their education level, gender, and experience were retrieved from their LinkedIn profiles. Company level characteristics such as size, leverage are retrieved from Finnet Database. Corporate governance attributes of companies such as board size, gender diversity at board level are obtained from the activity reports. The final sample for second model is presented in the Panel B of Table 1.

Model

First model is to estimate the effect of chairperson narcissism on AF market competition.

Model of AF Market Competition (Model I)

i donates AFs, t donates years. A negative association between chairperson narcissism and AF market competition is expected.

Model of audit quality (Model II)

Second model is to estimate the effect of chairperson narcissism on audit quality.

j donates companies, k donates individual auditors. A negative association between chairperson narcissism and audit quality in terms of discretionary accruals (AbsDA), small profit (SP), and audit report aggressiveness (AGG) is expected. When small profit (SP) is employed as the dependent variable, the control variable -CROA- is excluded because -SP- is derived from -CROA-.

Dependent Variables

Dependent Variables for Model I

Three dependent variables were employed to measure AF market competition (Francis et al., 2013; FRC, 2022; La Rosa et al., 2019; Numan & Willekens, 2012). First variable is that annual total revenues of an AF is divided by annual total revenues of whole AFs (TRevenue%). Second variable is that annual independent audit revenues of an AF is divided by annual independent audit revenues of whole AFs (IARevenues%). Third, independent audit revenue market share difference between the AF and its closest competitor in the audit market for a year (DiffIARevenues%).

Dependent Variables for Model II

Three dependent variables are used to measure audit quality. First, discretionary accruals are measured using the Kothari et al. (2005) model. Second is the presence of small profits (Goodwin & Wu, 2016). Third is the degree of audit reporting aggressiveness (Chen et al., 2017; Gul et al., 2013).

In this study, Kothari et al.’s (2005) model is employed to calculate discretionary accruals for the clients. Equation (2) presents the Kothari model (2005).

All variables are scaled by lagged total assets (TotalAssetsit-1). The absolute values of discretionary accruals (AbsDA) serve as the primary dependent variable in this study.

Additionally, audit reporting aggressiveness (AGG) is introduced as another dependent variable. AGG is calculated following the methodology outlined by Gul et al. (2013) and Chen et al. (2017):

Here, Modified represents the actual audit opinion. AGG quantifies the difference between the predicted and actual audit opinions. A higher value of AGG indicates lower tolerance for earnings management by individual auditors/AFs and suggests a lower likelihood of issuing a modified audit opinion.

Lastly, small profit (SP) is incorporated as the final independent variable. SP is defined as 1 if a company's reported ROA is between zero and 0.02, and 0 otherwise. This indicator highlights the potential to overlook earnings management practices aimed at achieving small profits, potentially indicating lower audit quality (Goodwin & Wu, 2016).

Variable of Interest

There are several types of measurement of narcissism such as featuring executive's photo in the company's annual report, featuring executives in company press releases, level of using singular personal pronouns by executives, pay disparity (Chatterjee & Hambrick, 2007). This study do not able to employ such measurements because of unavailability of AF chairpersons’ photos, or chairpersons’ speeches in the transparency reports of AFs. Pay disparity’ is not used, because although chairpersons’ shares in the ownership structure of AFs can be obtained, this measurement is heavily influenced by company size, with Tosi et al. (2000) reporting that firm size alone can explain up to 40% of CEO compensation (Cragun et al., 2020). Also, several studies perform survey-based approach to assess leaders’ narcissism. However, the low participation rate of leaders in organizational surveys and personality assessments presents a significant challenge for survey-based studies of leaders’ narcissism. Additionally, the data collected is at risk of bias due to this lack of participation (Van Scotter, 2020). One variable of interest was utilized to test the hypotheses. The variable of interest is the size of signatures of chairpersons of AFs (Church et al., 2020; Takada et al., 2021). Individuals with larger signatures tend to exhibit inflated self-perceptions, a heightened sense of entitlement, and other narcissistic traits (Cragun et al., 2020; Ham et al., 2017). Pronoun use and signature analysis, particularly those that don't require direct individuals’ participation (e.g., pronoun use, signature analysis), is considered crucial for more accurate and unbiased measurement of individuals’ narcissism (Cragun et al., 2020). The chairpersons’ signatures were scaled. First, the logarithmic value of the signature size of the AF chairperson (ChairNarcissismLog) is employed. Second, the signature size of chairperson is divided by the number of letters of chairperson’s name (ChairNarcissismLetters).

Control Variables

Control Variables for AF Market Competition Model (Model I)

AF board size (AFBoardSize), AF board education level (AFBoardEdu), the number of owners (AFOwnerSize), and the number of public interest entities (Pie) are included as control variables in the paper. Large boards have higher variability of performance because larger boards have the communication or coordination problems, and it creates decision making problem (Cheng, 2008). Education level is associated with open mindedness and the capacity of information process, these abilities make companies more competitive (Darmadi, 2013; Hambrick & Mason, 1984). The number of owners and the number of public interest entities are used two of the indicators of AF size. Large AFs have more staff resources, are more experienced and are more independent and conservative (DeAngelo, 1981; Gul et al., 2013).

Second-level control variables relate to chairpersons’ attributes. Studies suggest that gender (ChairGender) and education (ChairEdu) influence decision-making and performance (Peni, 2014). In AFs, chairpersons rarely change, but when they do, narcissism levels may shift, so ChairChange is controlled. In Turkey, auditors hold either a certified public accountant (CPA) or a sworn-in CPA license. While a CPA license is mandatory (IART, 2012), sworn-in CPAs often have government experience (Ocak & Can, 2019). ChairCert reflects experience, which may impact competitiveness. Chairpersons’ ownership share (ChairShare) is also controlled for, as higher shareholding indicates a stronger stake in profits and competitiveness.

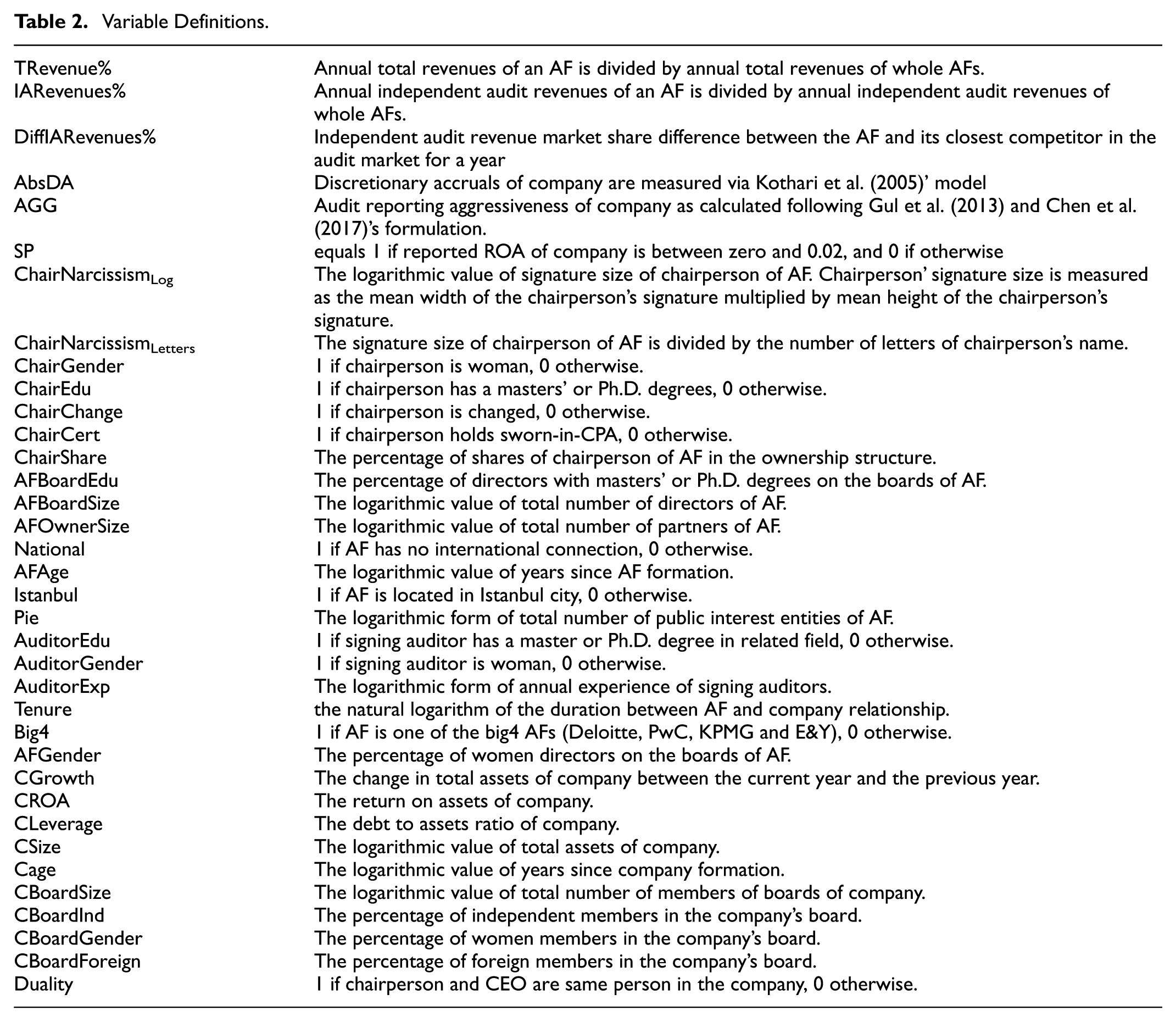

AF location (Istanbul), age, international connection (National), and the number of public interest entities (PIE) are controlled for. AFs in large provinces may have larger client portfolios due to company concentration (Ocak, 2021). Older AFs may attract more clients due to their market presence, increasing revenue (Bröcheler et al., 2004; Woo et al., 2018). The number of public interest entities signals AF competitiveness and revenue size. National AFs face disadvantages as international AFs leverage global connections and stronger reputations (Can, 2018). We also fix years in Model I. Panel A of Table 2 defines the variables used in Model I.

Variable Definitions.

Control Variables for Audit Quality Model (Model II)

First level control variable covers chairperson attributes. Second and third levels indicate AF characteristics, and individual auditor attributes. Fourth level covers company characteriestics, such as financial characteristics and board characteristics. Narcissism and audit quality can be influenced by various factors beyond personality, as discussed by Ham et al. (2018). Thus, this paper controls chairperson attributes.

Individual auditor gender (AuditorGender), individual auditor experience (AuditorExp), and individual auditor education level (AuditorEdu) are also controlled for in the study. The independent audit is performed by the individual auditor on behalf of the AF. Thus, the characteristics of AFs may have an effect on audit outcomes. For instance, big4 AFs (Big4) and older AFs (AFAge) may provide more qualified audit work because of having more quality staffs and resources (El-Deeb et al., 2023, 2024), national AFs (National) may not have sufficient quality personnel and resources compared to big4 AFs (Ng and Tai, 1994; Imam et al., 2001). Besides, according to Chen et al. (2018), new competitors push large AFs to improve quality, while smaller firms, due to limited resources, lower prices in response to increased competition. Thus, AFAge and Big4 were controlled. In Turkey, AFs authorized to audit public companies must be incorporated and have a board of directors (Ocak, 2021). The primary function of AFs' boards is to oversee and monitor the activities of management (Maister, 1993). From the perspective of corporate companies, recent papers found that women on boards and large boards have effective monitoring. Thus, AF board size (AFBoardSize) and the percentage of women directors on the boards of AFs (AFGender) are controlled. The variables Istanbul, AFOwnerSize, and PIE, which were employed in the audit market competition model, are not used because of their high correlation with the Big4 variable in the audit quality model.

Based on Defond and Zhang (2014), this study employs commonly used client-specific control variables such as company growth rate (CGrowth), company performance (CROA), company leverage (CLeverage), company size (CSize) and company age (CAge) in audit quality research. Besides, board independence of companies (CBoardInd) are controlled because of effective mechanism mitigating financial reporting quality (Bravo and Reguera-Alvarado, 2018). Women (CBoardGender) are believed to possess enhanced abilities to monitor and control company management, attributed to their tendency to be more risk-averse (Arioglu, 2020; Dobija et al., 2022). Large boards of directors (CBoardSize) are more likely to include both women and independent board members (Arioglu et al., 2024). Combining the functions of decision-making and control could diminish the effectiveness of the board's monitoring role (Alves, 2023). Thus, Duality is controlled. The percentage of foreign members (CBoardForeign) may reflect the percentage of foreign owners of companies. The monitoring power of foreign investors is higher than the local investors (Lee et al., 2018). Finally, years and sectors were fixed in Model II. Panel A of Table 2 presents the variables of definitions employed in the Model II.

Results

Descriptive Statistics

Descriptive Statistics for Audit Market Competition Model (Model I)

Panel A of Table 3 presents the descriptive statistics regarding the variables employed in Model I. The average values of TRevenue%, IARevenues%, and DiffIARevenues% are 0.013, 0.012, and 0.001. The mean value of ChairNarcissismLog (ChairNarcissismLetters) is 2.881 (1.702). The average percentage of women chairpersons (ChairGender) is 5%. The average percentage of chairpersons with masters’ or Ph.D. degrees (ChairEdu) is 22.9%. The average shares of chairpersons (ChairShare) on the AF ownership structures is 49%. The average percentage of chairpersons with sworn-in CPA (ChairCert) is 67.9%. The average change of chairpersons (ChairChange) is 6.7%. The average board members of AFs (AFBoardSize) is 3 directors. The average number of owners of AFs (AFOwnerSize) is 9 members. The percentage of board members with masters’ or Ph.D. degrees (AFBoardEdu) is 19.4%. The mean value of national AF (National) is 33.5%. The average age of AFs (AFAge) is about 16 years. The average value of AFs located in Istanbul (Istanbul) is 70.3%. The average number of public interest entities of AFs (Pie) is about 19 entities. Variance inflation factors (VIFs) indicate no multicollinearity among the variables.

Descriptive Statistics.

Descriptive Statistics for Audit Quality Model (Model II)

The average values of AbsDA, AGG and SP are 0.053, 0.001 and 0.113. The mean value of ChairNarcissismLog (ChairNarcissismLetters) is 2.847 (1.570). The average percentage of women chairpersons is 12.1%. The average percentage of chairpersons with masters’ or Ph.D. degrees is 14.1%. The average shares of chairpersons on the AF ownership structures is 35.8%. The average percentage of chairpersons with sworn-in CPA is 24.6%. The average change of chairpersons is 8%. The average board members of AFs is 7 directors. Figures regarding other variables employed in the model 2 are shown in the Panel B of Table 3. VIFs indicate no multicollinearity among the variables.

Main Results

Effect of AF Chairperson Narcissism on Audit Market Competition (Model I)

Table 4 presents the results regarding the effect of AF chairperson narcissism on AF market competition. While the coefficients of chairperson narcissism (ChairNarcissismLog and ChairNarcissismLetters) are negatively and significantly associated with TRevenue% and IARevenues%, the coefficient of chairperson narcissism (ChairNarcissismLog and ChairNarcissismLetters) are negatively and insignificantly associated with DiffIARevenues%. The results generally indicate that narcissistic chairpersons affect AF market competition negatively. It is argued that narcissistic chairpersons negatively affect AF market competition because effective work relies on strong teamwork. When individuals in key positions such as AF chairperson exhibit narcissistic traits, it can significantly disrupt team dynamics and performance (Li et al.,2014). Narcissistic chairpersons contribute to a decline in employee satisfaction and create a negative work environment (Blair et al., 2017), ultimately leading to toxic work cultures (O’Reilly et al.,2014). Narcissism, which conflicts with the collaborative nature of teams, is likely to hinder team performance (Tett & Burnett, 2003). Thus, H1 is accepted.

The Main Results of AF Market Competition Model (Model I).

Note. Standard errors in parentheses.

***p < 0.01.**p < 0.05.*p < 0.1.

Effect of AF Chairperson Narcissism on Audit Quality (Model II)

Table 5 presents the results regarding the effect of AF chairperson narcissism on audit quality. The results indicate that narcissistic chairpersons (ChairNarcissismLog and ChairNarcissismLetters) affect audit quality (AbsDA, AGG, SP) negatively. The coefficients of chairperson narcissism are positively and significantly associated with AbsDA, AGG and SP. AFs with narcissistic chairperson manage earnings using discretionary accruals (AbsDA), are more aggressive when they issue an opinion (AGG), and the companies they audit tend to disclose more small profits (SP). Since AFs’ chairpersons as acting as the legal representative of the AF, is the key leader and principal decision-maker of the AF even though the audit of clients is performed by individual auditors, AFs’ chairpersons have control over the staff (Bass & Steidlmeier, 1999; Blair et al., 2017). Their manipulative nature will cause employees to have manipulative tendencies in the decisions when they perform an audit. Thus, H2 is accepted.

The Main Results of Audit Quality Model (Model II).

Note. Standard errors in parentheses.

***p < 0.01.**p < 0.05.*p < 0.1.

System GMM Results

While Table 6 presents the system GMM results regarding the effect of chairperson narcissism on AF market competition, Table 7 indicates the system GMM results regarding the effect of chairperson narcissism on audit quality. This paper addresses the potential for explanatory variables to be influenced by the dependent variable by including lagged dependent variables as explanatory factors. To determine the appropriate number of lags, OLS regressions are conducted, then the first lag of the dependent variables are included (L.TRevenue%, L.IARevenues% and L.DiffIARevenues% for Model I, and L.AbsDA, L.AGG and L.SP for Model II). Importantly, the validity of the system GMM results is confirmed by the absence of second-order correlation and the presence of valid instruments. This is indicated by the statistically insignificant AR(2) and Hansen tests (Díez-Esteban et al., 2019). The system GMM results, presented in Tables 6 and 7 are consistent with the main results. No endogeneity issue is observed when the effect of AF chairperson narcissism on audit market competition and audit quality is investigated using System GMM.

System GMM Results of AF Market Competition Model (Model I).

Note. Standard errors in parentheses.

***p < 0.01.**p < 0.05.*p < 0.1.

System GMM Results of Audit Quality Model (Model II).

Note. Standard errors in parentheses.

***p < 0.01.**p < 0.05.*p < 0.1.

Propensity Score Matching Results

Propensity score matching method (PSM hereafter) was employed to control potential endogeneity. OLS and Logistic regression results were repeated with the PSM sample to enhance the validity of this paper. First, propensity scores were generated using a logit regression to estimate the likelihood of auditing an AF with a narcissistic chairperson. Thus, the median values of ChairNarcissismLog and ChairNarcissismLetters were employed to identify which chairpersons have a narcissistic personality. For instance, Patel and Cooper (2014) identify CEOs as narcissistic person if their narcissism scores in the upper quartile. The median values of ChairNarcissismLog and ChairNarcissismLetters 2.916 and 1.478 for the Model I (Audit market competition). The median values of ChairNarcissismLog and ChairNarcissismLetters 2.961 and 1.335 for the Model II (Audit quality). Without replacement and within a maximum caliper width of 0.03 (Fang et al., 2017; Lawrence et al., 2011), each firm was matched with an AF that has a narcissistic chairperson or with an AF that has no narcissistic chairperson, whichever had the closest propensity score from the logistic regression. The estimation results of propensity score matching are shown in Tables 8 and 9, which suggest that the main results do not change with the application of PSM procedure. No endogeneity issue is observed when the effect of AF chairperson narcissism on audit market competition and audit quality is examined using PSM.

PSM Results of AF Market Competition Model (Model I).

Note. Standard errors in parentheses.

***p < 0.01.**p < 0.05.*p < 0.1.

PSM Results of Audit Quality Model (Model II).

Conclusion, Implications and Limitations

This study examines the impact of AF chairperson narcissism on market competition and audit quality using AFs and listed companies in Turkey. OLS and logistic regressions test the hypotheses, while System GMM and PSM address endogeneity. Findings indicate that narcissistic chairpersons negatively affect both competition and audit quality, with System GMM and PSM results supporting the main findings.

Understanding the chairperson's psychology and personality traits is crucial for assessing audit quality. Traditional proxies for CEO narcissism cannot be directly applied to AF chairpersons due to limited personal data access. Recent studies highlight the negative impact of narcissism on audit quality, corporate performance, and financial reporting (Blair et al., 2017; Chatterjee & Hambrick, 2011; Khaksar et al., 2022; Salehi et al., 2022). This study measures AF chairperson narcissism using their signatures and finds a negative effect on AF competition and audit quality, considering chairperson attributes, individual auditor traits, client characteristics, and corporate governance.

While this study aligns with prior research on the negative effects of auditor and CEO narcissism on audit quality, financial reporting, and corporate performance (Chatterjee & Hambrick, 2011; Khaksar et al., 2022; Salehi et al., 2022), it stands out by focusing on AF chairpersons. Unlike previous studies examining individual auditors, CEOs, or managers, this study explores how AF chairperson narcissism impacts audit quality and market competition.

While some studies highlight the benefits of narcissism, such as improved decision-making in turbulent times (Campbell & Campbell, 2009) and positive effects on financial performance (Olsen et al., 2014), this study finds otherwise. Unlike Chou et al. (2021), who links audit partner narcissism to stronger auditor independence, audit quality and competition are found to be harmed by AF chairperson narcissism in this paper. Narcissistic chairpersons lower employee satisfaction, create toxic work environments (Blair et al., 2017; O’Reilly et al.,2014), and foster manipulative tendencies among auditors.

This study provides valuable insights for AFs, regulators, and policymakers. Independent audits ensure the accuracy and reliability of financial statements, supporting informed decision-making for management, shareholders, employees, creditors, and investors. However, the audit market is highly competitive, with both international and local AFs striving for dominance. In this context, the AF chairperson’s personal style plays a key role in audit quality and competition. Findings show that narcissistic chairpersons negatively impact both. Companies should develop strategies to identify and avoid AFs led by narcissistic chairpersons, as their influence may compromise financial reporting quality. Audit committees and boards, familiar with AFs and their leaders, should take proactive measures to exclude AFs with narcissistic leadership from future engagements.

Second, AFs can mitigate the risks posed by such behaviors by implementing effective monitoring procedures. Since AF chairpersons are elected by their boards (Oxera, 2007), board members can use these findings to make informed decisions when selecting leaders (i.e., chairpersons), thereby safeguarding market competition and maintaining the quality of their services. Although the AF chairpersons are senior partners or founding partners, these AFs serve society. As stated by Salehi and Rouhi (2023), an AF chairperson with a narcissistic personality could engage in psychological assessments to gain deeper insights into their strengths and weaknesses, which may enable them to adapt and refine their behavior. The third implication is about the chairperson's power in the AFs. Chairpersons in AFs are key individuals and hold significant power in AFs in Turkey due to being founder-owners with significant ownership stakes or individuals who have worked at the company for many years. The findings of this paper state that narcissistic chairpersons damage AF market competition and audit quality. As stated by Martínez-Ferrero et al. (2023), regulators need to oversee and limit chairperson power, as chairperson narcissism can lead to undesirable outcomes.

Lastly, Turkish culture is highly collectivist, with strong in-group loyalty, high power distance, and low uncertainty tolerance (Bilgin & Kutlu, 2022; Cohen & Özsoy, 2021). While collectivism may discourage narcissistic traits from harming audit quality (Cohen & Özsoy, 2021), individuals in collectivist regions still exhibit higher narcissism (Li & Benson, 2022). Additionally, Turkey’s predominantly Muslim population is influenced by the Islamic work ethic (Arslan, 2001; Karakas et al., 2015), which may mitigate narcissism’s negative effects. This study does not include cultural variables, but future research could examine their moderating role. Despite potential positive influences, negative outcomes are still produced by narcissistic AF chairpersons. Future studies using face-to-face surveys could further explore these dynamics.

Narcissism is a significant problem for society, especially for individuals in certain positions, as it can negatively affect the outcomes of those positions. Narcissism can seriously impact the well-being of others, whether in a small segment of society or across the entire community. If AFs and their staff are considered a microcosm of society, junior or senior auditors working with a narcissistic chairperson may adopt the behavior patterns they observe and carry them into future generations. Additionally, they may bring these behavioral patterns with them to a new workplace when they leave the AF. Considering its broader societal impact, narcissism can weaken social bonds and communities by prioritizing self-interest over collective well-being. Narcissistic leaders may exhibit authoritarianism, engage in corruption by prioritizing personal gain over societal good, and contribute to the breakdown of community dynamics.

A key limitation of this study is its focus on an emerging country. While audit research often examines AFs in China or Europe, this paper analyzes Turkish AFs, which follow international accounting and auditing standards despite operating in a developing economy. Although the sample size may be a constraint, the findings offer valuable insights for AFs, clients, and policymakers. Future research could expand to developed or cross-country datasets. Comparing AF chairperson narcissism across nations could reveal cultural influences on audit quality and market competition.

Another limitation is the measurement of narcissism. As noted by Rijsenbilt and Commandeur (2013), relying on behavioral indicators provides objective data but lacks the depth of a professional psychological evaluation. This study measures AF chairperson narcissism solely through signature size, excluding other methods like pay disparity or pronoun use. Future research could apply diverse measures to explore the link between chairperson narcissism and AF outcomes. Additionally, due to data limitations, this study does not examine individual auditor narcissism. Future studies could compare chairperson and auditor narcissism to better understand their effects on audit quality and competition.

While chairperson attributes such as gender and education were controlled for and the standardized signature size based on the number of letters in the chairperson's name was tested on audit quality and audit market competition, it is possible that other unaccounted-for influences could introduce random variation in the data. This is another limitation of the paper.

Additionally, this paper does not consider other leadership traits and styles in relation to the effect of the AF chairperson on audit quality and AF competition. It has been empirically established that different types of leadership styles, such as transformational, servant, democratic, and bureaucratic, impact company outcomes. For instance, Hassanzadeh Mohassel et al. (2024) find that both transformational and servant leadership styles play a crucial role in enhancing audit quality through knowledge sharing. Saleh and Auso (2025) state that transformational leadership enhances the competitive advantage of universities. Alblooshi et al. (2021) conducted a systematic literature review and concluded that various leadership styles positively impact company outcomes. According to them, paternalistic leadership builds trust between team members, while charismatic leadership fosters trust and respect due to expertise and reputation. From this perspective, servant or transformational leadership might enhance audit quality and AF competitiveness through knowledge sharing, while charismatic or paternalistic leadership could build trust and respect, thus improving audit quality. Future research could evaluate AF chairpersons in terms of these leadership styles and examine their impact on audit quality and AF competitiveness.

Footnotes

Author Note

Authors equally participated to prepare the paper.

Ethical Considerations

Ethical approval is not applicable as the collected data are publicly available.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data are available from the public sources cited in the text. Data are mostly hand-collected. The sources of data are mentioned in the paper.