Abstract

As the second-largest holder of U.S. Treasuries, China’s investment behavior in U.S. debt has long sparked debate about whether economic factors or strategic considerations primarily drive it. Based on the “weaponized interdependence” theory, the paper uses the time-varying parameter regression (TVP-R) and vector autoregression (VAR) models to capture the influence of China-U.S. relations and economic factors on China’s holdings of U.S. Treasury securities. The results show that the scale of foreign exchange reserves and China-U.S. relations have a significant positive impact on China’s holdings. In contrast, the holdings are not sensitive to Treasury returns or the trade balance. The foreign exchange reserve scale has a far greater impact than the China-U.S. relationship. Dynamic analysis indicates that China-U.S. relations and China’s holding decision show a trend of “decoupling,” and there is no evidence to prove that China weaponized the creditor’s rights. China’s holdings of U.S. Treasuries should be mainly regarded as an economic behavior to preserve the value of foreign exchange reserves. In the future, the strategic competition between China and the U.S. may have only a limited impact on China’s holding behavior.

Plain language summary

This article aims to discuss the primary factors that determine the scale of China’s holdings of U.S. Treasury securities. From the theoretical perspective of “weaponized interdependence,” China’s holding behavior can be regarded as a potential political and strategic tool. The research indicates a clear positive correlation between the size of China’s foreign exchange reserves and the scale of its holdings of U.S. Treasury securities. Among all the factors considered in the study, the foreign exchange reserve is identified as the most significant factor influencing the scale of China’s holdings of U.S. Treasury securities. The correlation between China-U.S. relations and China’s holdings of U.S. Treasury securities is also positive, but the impact is not as pronounced as that of the foreign exchange reserve. In addition, the scale of China’s holdings of U.S. Treasury securities is not particularly sensitive to both absolute and relative returns or the trade balance. This suggests that, apart from investing in U.S. Treasury securities, China lacks relatively secure alternatives for managing its dollar reserves. Examining the temporal trends, the impact of changes in China-U.S. relations on the scale of China’s U.S. Treasury securities holdings has remained very low since 2018. There is a discernible trend of “decoupling” between the bilateral relationship and the scale of holdings and there is no evidence to prove that China weaponized the creditor’s rights. The impact of strategic competition between China and the United States on the scale of China’s holdings of U.S. Treasury securities may be relatively limited in the future. China is likely to remain one of the major creditors to the U.S., holding a substantial amount of U.S. Treasury securities, contributing to a certain degree of strategic stability in the bilateral relationship.

Keywords

Introduction

China and the United States are the world’s largest emerging market and the largest developed country, respectively, and their relations are highly complex in political, economic and other fields. Since the Reform and Opening-up, China has actively integrated into the world economic system and developed an export-oriented economy, leading to the expansion of China’s foreign exchange reserves. After entering the 21st century, China’s holdings of U.S. Treasury securities have increased rapidly. According to the U.S. Department of the Treasury, China’s holdings of U.S. Treasury securities were 1.07 trillion dollars in December 2021, which is the second largest holder after Japan (In this paper, the data of China’s holdings of U.S. Treasury securities do not include Hong Kong, Macao and Taiwan. The data source is the U.S. Department of the Treasury.). The creditor relationship formed by China’s large holdings of U.S. debt constitutes an asymmetric structure between the two countries, which plays a special role and has an influence on bilateral relations. For a long time, policy and academic arenas have different views on reasons for China’s holdings of large-scale U.S. Treasury securities. Some emphasize the economic and technical factors of investment, such as economic interdependence and maintaining the value of foreign exchange reserves (Chow, 2010; Elwell, 2012; J. S. Song & Sun, 2013). There is also a view that China’s holdings of U.S. Treasury securities are factors of strategic stability between the two countries or China’s means of countering the U.S. (Gertz, 2010; Myers, 2018; Thompson, 2007).

As one of the largest foreign holders of U.S. Treasury securities, China has formed an economic dependency on the U.S. fiscal situation in U.S.-China relations. China supports U.S. government spending and monetary policy stability by purchasing U.S. Treasury securities while effectively managing China’s vast foreign exchange reserves. Thus, although China’s holding of U.S. Treasury securities appears to be an economic reciprocal arrangement, it also carries political and strategic significance. From the perspective of “weaponized interdependence,” China’s holding of large amounts of U.S. Treasury securities can be regarded as a potential political and strategic tool. This theory posits that, in the context of globalization and interdependence, nations can achieve strategic objectives by manipulating economic dependencies and even convert such economic reliance into a weapon to influence the other party’s decisions (Farrell & Newman, 2019). Under the theory of weaponized interdependence, if U.S.-China relations deteriorate, China might impact U.S. financial markets or even the global dominance of the U.S. dollar by selling U.S. Treasury securities or adjusting its holdings. However, such actions could backfire, causing market turmoil and decreasing bond values, thereby harming China’s foreign exchange reserves. This creates a risk-benefit trade-off for China when using this tool. Based on the theory of weaponized interdependence, the core issue of this paper is whether the changes in China-U.S. relations can significantly affect China’s U.S. Treasury holding strategy. Specifically, when the relationship between China and the U.S. deteriorates, would China reduce its holdings to exert economic pressure and strengthen the bargaining chip. When the relationship between the two countries improves, would China increase its holdings to support economic stability and strengthen its strategic position in the global economy.

This paper uses empirical methods such as the time-varying parameter regression (TVP-R) model and the vector autoregressive (VAR) model to capture the impact of China-U.S. bilateral relations on the scale of China’s holdings of U.S. Treasury securities, and discusses whether China’s holdings are mainly economic behavior or political and strategic behavior under the influence of bilateral relations. The results show that the scale of foreign exchange reserves and China-U.S. relations significantly impact China’s holdings. In addition, China’s scale of holdings is not sensitive to the returns of U.S. Treasuries, and no significant statistical relationship has been found between China’s trade surplus with the U.S. and China’s holding behavior. Among all the variables considered in the study, the scale of foreign exchange reserves is the biggest factor affecting the size of China’s holdings of U.S. Treasury securities, and its impact is much greater than that of China-U.S. relations. Dynamic analysis indicates that China-U.S. relations and China’s holding decision show a trend of “decoupling.” It can be concluded that China’s holdings of U.S. Treasuries should be mainly regarded as an economic behavior to preserve the value of foreign exchange reserves.

The study contributes to the literature in the following ways. First, to our best knowledge, this paper first investigates the impact of China-U.S. bilateral political relations in the form of time series data on the scale of China’s holdings of U.S. Treasury securities using the approach of quantitative analysis and explores its time-varying effect. By controlling various factors, it can more accurately compare the influence of different political and economic factors on China’s holdings decision. Second, the paper compares the different effects of political factors and various economic factors on China’s holding of U.S. securities. Based on the theory of “weaponized interdependence,” the paper analyzes whether China uses U.S. Treasury securities as a strategic tool toward the U.S. The paper confirms that political and strategic factors are not decisive for China to purchase U.S. Treasury securities. Under the background of intensified competition between China and the U.S. in recent years, China’s holding scale and China-U.S. relations have a certain trend of “decoupling,” and there is no evidence to prove that China weaponized the creditor’s rights. Third, this study indicates that China lacks other safe approach to manage U.S. dollar reserves besides investing in U.S. Treasuries, and the influence of the strategic competition between China and the U.S. on the scale of China’s holdings may be limited in the future. This result will be a reference for further research and policy-making regarding China-U.S. relations and economic cooperation.

The remainder of this paper is structured as follows. Section 2 discusses literatures regarding China’s holdings of U.S. Treasury securities and the research hypotheses of this paper. Section 3 describes the selection and processing of research data. Section 4 presents the construction of OLS and TVP-R regression models and discusses the results. Section 5 provides the construction of a VAR model and analyzes the results. Section 6 provides further discussion and case analysis. Section 7 concludes.

Literature Review and Research Hypotheses

Discussions on China’s Holdings of U.S. Treasury Securities

China’s Foreign Exchange Reserves and Investment in U.S. Treasury Securities

Since the Reform and Opening-up, with the rapid development of China’s economy, the scale of China’s foreign exchange reserves has been expanding. Foreign trade is one of the “troikas” that boosts China’s economy. Through the active promotion of export-oriented economic development, China has maintained a trade surplus for a long time since 1994 and accumulated a large foreign exchange surplus. After joining the World Trade Organization in 2001, China’s export advantage has been further highlighted, gradually becoming the world’s largest processing and manufacturing base and exporter of manufacturing products, and its trade surplus has been further expanded. At the same time, the advantages of sufficient labor supply and a huge domestic market are great attractions to international investment. Chinese governments also launched a variety of preferential policies to actively attract foreign investment, making China an important international investment destination. Since 2017, the scale of foreign investment in China has ranked second in the world. With the development of China’s open economy, China has the largest foreign exchange reserves since 2006. As the dollar is the most important international currency, it accounts for a large proportion of China’s foreign exchange reserves. The huge dollar reserves form the basis for China’s large-scale investment in U.S. Treasury securities.

International finance has strengthened the dollar status as a major reserve currency, and there is no substitute or competitor of the dollar in the world (Brown, 2020; Prasad, 2014). Central banks worldwide hold huge amounts of dollar-denominated assets, further strengthening the dollar’s position (Batson, 2009). The large amount of U.S. debt countries hold is mainly related to monetary value management and the U.S. trade deficit (Hallwood, 2021; Kitchen & Chinn, 2011). Due to the hegemonic role of the dollar, world trade mainly uses the dollar as an international payment currency. Coupled with the deep development of the dollar market, liquidity, homogeneity, and high standardization make the dollar popular with foreign investors, and the homogeneity of U.S. Treasury securities enables foreign investors to carry out free portfolio and flexible asset conversion (Kaltenbrunner & Lysandrou, 2017). As global foreign exchange reserves have risen sharply, a large proportion of it has been invested in U.S. securities, especially in China, Japan, and other emerging markets with high current account surpluses due to a lack of other dollar investment channels (Beltran et al., 2013; Lu et al., 2020).

Since the 1980s, China has purchased and held U.S. Treasury securities and gradually developed into one of the major creditors of the U.S. After entering the 21st century, China’s holdings of U.S. Treasury securities have increased rapidly, surpassing Japan as the largest holder in September 2008, reaching more than $1.3 trillion (June to July 2011). Although China has been overtaken by Japan several times and is now the second largest holder of U.S. Treasuries, its holdings have remained high for a long period. In terms of proportion, China’s holding scale gradually expanded from about 6% in July 2000 to more than 28% in July 2011, and then showed a gradual downward trend but still remained above 12%. Overall, China’s holdings of U.S. Treasury securities fluctuated to some extent, showing a slight downward trend since 2011, and its share of all foreign investors has declined. However, it is still a main creditor of U.S. Treasury securities (see Figure 1). It is worth noting that in recent years, under the intensified strategic competition between China and the U.S., there is also a downward trend in the scale and proportion of China’s holdings of U.S. Treasury securities. Whether there is a clear relationship between the two is an important issue.

China’s holdings of U.S. Treasury securities and the proportion among foreign holders. Data source: U.S. Department of the Treasury.

Economic Factors: The Perspective of “Foreign Exchange Reserve Management”

China’s buying, selling, and holding of U.S. Treasury securities is, first and foremost, an economic phenomenon. At present, many studies have discussed various economic factors affecting China’s holdings of U.S. Treasuries. In essence, China’s investment in U.S. Treasury securities is an investment behavior, which aims to maintain and increase the value of dollar reserves. Therefore, the scale of China’s dollar reserves and the risks and returns of U.S. Treasuries would impact the scale of China’s holdings. First, as the most important international currency, the dollar reserve is the main component of China’s foreign exchange reserves, and the huge dollar “capital pool” is an important reason for China’s investment in U.S. Treasury securities. Many studies believe that China’s active export-oriented economy has accumulated a large amount of dollar foreign exchange reserves which must be properly managed, but China has no better choice than to purchase U.S. securities (Mandelbaum, 2010; Prasad, 2010; J. S. Song & Sun, 2013).

Second, the safety and profitability of U.S. Treasury securities may affect the scale of China’s holdings. Because U.S. Treasuries are guaranteed by the national credit of the U.S., compared with other U.S. assets, they have the advantages of high security, stable returns, large market capacity, and convenient transaction (Rechtschaffen, 2019), making them an effective tool for hedging risks (Gupta et al., 2021). Due to risk aversion, China may be more inclined to allocate U.S. Treasury assets. The U.S. has a stable government and developed financial markets, which makes Treasuries safe-haven assets and can provide investors with low-risk investment returns (Elwell, 2012). The investment strategy of the Chinese government is inherently cautious and conservative, which leads them to prefer U.S. Treasuries of low risk, low yield, and high security (Chow, 2010). From the technical perspective of investment, the opportunity cost of holding certain assets should be considered. China’s investment of dollar reserves in U.S. Treasuries indicates that it has lost the possibility of obtaining returns on other assets. Therefore, the risks and returns of other alternative investments can affect the size of China’s holdings of U.S. Treasury securities. The supply of corporate securities and government bonds in small economies is relatively insufficient, and it is reasonable for the government to invest in government bonds in core economies such as the U.S. to ensure the maintenance and safety of assets (Lysandrou, 2013). Inflation in the U.S. tends to have less downward pressure on the exchange rate than in the U.K. and Eurozone because the dollar reserve currency status reduces the interest rate premium of U.S. public debt (Garrett, 2010). China prefers to hold U.S. Treasuries facing a global slowdown and chronic debt issues in Europe (Morrison & Labonte, 2012).

In addition, some studies believe that China’s holdings of U.S. Treasury securities are mainly an economic behavior with multiple investment strategies at different levels of returns. During the 2008 financial crisis, China increased its purchases of U.S. Treasury securities, but when the U.S. gradually weathered the crisis and the interest rate on short-term debt decreased to near zero, its holdings fell sharply in 2009 (Wang & Freeman, 2013). Some studies also point out that factors such as exchange rates and yields on local currency bonds that may determine the relative returns of U.S. Treasuries also tend to affect the size held by emerging markets such as China (Hagiwara, 2011). Generally speaking, the existing studies concerning China’s holdings of U.S. Treasury securities have considered the size of China’s dollar reserves, the returns and risk.

Political and Strategic Factors: The Perspective of “Interdependence” and “Financial Mutual Assured Destruction”

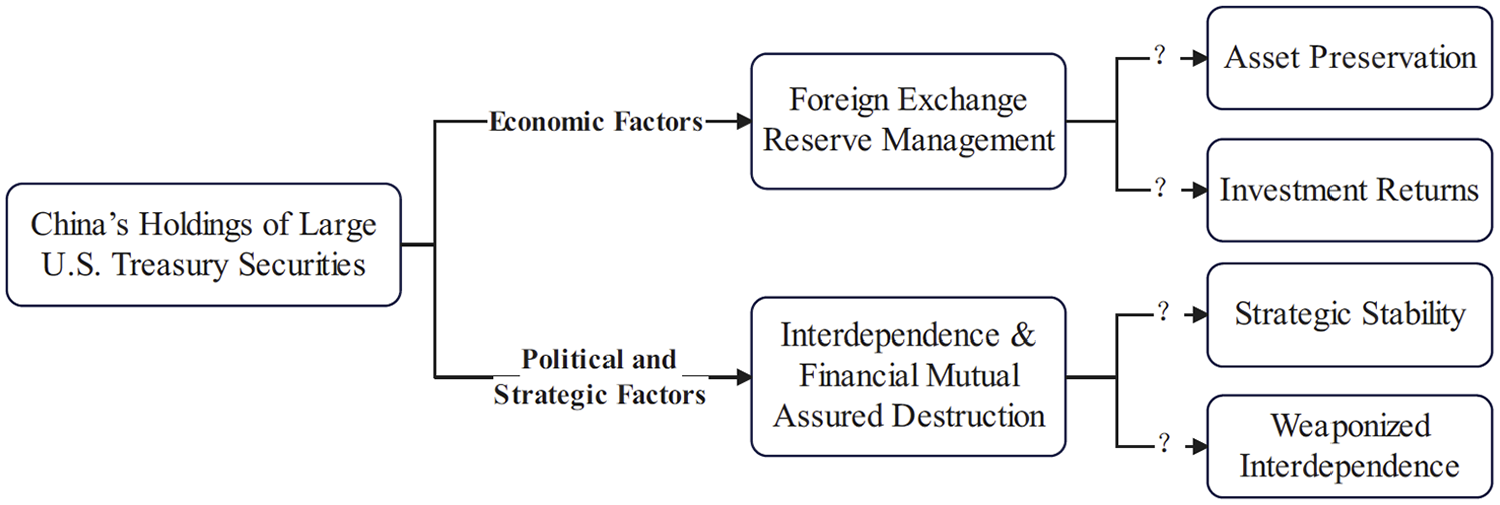

Any economic issue in the China-U.S. relationship has never been purely economic. China’s holdings of large-scale U.S. Treasury securities should not be simply regarded as an economic phenomenon. Considering the special influence and status of China and the U.S. and the importance of China-U.S. relations, its impact has far exceeded the scope of international economy and finance.

Many scholars defended that the political relationship between China and the U. S. has an impact on economic relations. Lust (2024) pointed out that China’s economic and political exchanges with other countries are influenced by the China-U.S. relationship, and intensified competition between China and the U.S. would make other countries take sides. Shi and Qi (2024) suggested that China’s “Belt and Road” economic and foreign policy needs to consider China-U.S. political relations, which will lead to the decision of target countries to accept China’s foreign direct investment. Wang (2023) argued that changes in regulatory frameworks, trade agreements, and geopolitical dynamics would affect the composition of bilateral trade. Some scholars suggested that there is a two-way influence between the China-U.S. political and economic relations (Su et al., 2020). Y. Song et al. (2024) examined the interactive relationship between China-U.S. political relations and bilateral trade at different time points, and showed that the linkage between these two variables varied slightly depending on the specific state of bilateral political relations (friendly, neutral, or hostile). Anaukwu and Anueyiagu (2024) argued that from 2017 to 2022, the economic interdependence between China and the U.S. continued to deepen, while the geopolitical tension has also intensified. China and the U.S. have maintained a delicate balance between cooperation and competition.

Therefore, more researchers are also concerned about the strategic significance of China’s holdings of U.S. Treasury securities in international politics. Some researchers believe that China’s holdings of U.S. Treasuries help to enhance cooperation between the two countries and the stability of China-U.S. relations. China’s large holdings of Treasury securities show the deep economic interdependence between the two countries, and China provides dollar reserves to the U.S. to maintain sustained exports, employment, and economic prosperity in the Chinese manufacturing sector (Roy, 2013). At the same time, China’s holdings of U.S. debt can largely help stabilize the U.S. economy (Morrison, 2009). China’s increase in U.S. Treasuries can express confidence and support for the U.S. and recognize the credit of the U.S. government. After the financial crisis, China increased its holdings of U.S. Treasury securities and even surpassed Japan as the largest creditor of the U.S. for some period, indicating that China is willing to support the U.S.-centered economic system and has a strong incentive to hold the dollar (Stokes, 2014). In addition, China’s large-scale holdings of U.S. Treasury securities actually show its recognition of the hegemony of the dollar, although such recognition may not be entirely voluntary (Hung, 2013, 2015). Some scholars defend that China’s huge holdings of U.S. Treasuries fall into a “U.S. dollar trap.” Initially, due to the large inflow of dollars into China from its trade surplus, China has to buy U.S. securities in order to maintain a low exchange rate. Later, to avoid the depreciation of dollar assets, China has to invest more dollar reserves to buy U.S. Treasury securities, but this is essentially a strong support for the borrowing demand of U.S. economic development (Krugman, 2009).

The dollar hegemony and China’s large-scale creditor’s rights to the U.S. actually constitute a “two-way asymmetric” relationship and structure between the two countries, in which both sides have special influence over each other, thus increasing the strategic stability between the two countries. Lawrence Summers, former Treasury Secretary, put forward the “balance of financial terror” in 2004, arguing that emerging markets represented by China would also face huge losses if they stopped financing the U.S. The U.S. can rely on this “balance of terror” to ensure that countries like China continue to finance it (Summers, 2004). Similar to the concept of “mutually assured destruction” in nuclear strategy, the “financial terror balance” between China and the U.S. also relies on a stable equilibrium of fear. In nuclear strategy, nuclear powers avoid actual conflict by ensuring that any attack would result in mutually assured devastating retaliation. Similarly, in the financial relationship between China and the U.S., China’s substantial holdings of U.S. Treasury securities create an economic interdependence. This dependency means that extreme financial actions by either side (such as rapidly reducing Treasury holdings) could trigger severe economic repercussions for the other side, leading to mutual economic damage. Consequently, both countries maintain a balance of reluctance to provoke conflict in the financial realm, akin to the fear balance in nuclear strategy. On this basis, some researchers argue that neither creditor nor debtor can unilaterally change the status quo without large-scale retaliation, so the “balance of financial terror” will last for a long time (Hudson, 2011). From the perspective of “balance of financial terror” and “financial mutual assured destruction,” China’s large-scale U.S. Treasury securities are actually a strategic chip similar to financial nuclear weapons between China and the U.S. and both sides would be cautious about the debt relationship.

Further, many researchers discuss the possibility that China’s huge holdings of U.S. debt can be used as a strategic strike and countermeasures against the U.S. There is a view that the debt relationship reflects national power and international political relations. China’s holdings of U.S. debt are more politically significant, and China can use the lending relationship as a threat to get the U.S. to make political concessions (Thompson, 2007). Creditor status gives China the potential to generate new power internationally (Chin & Helleiner, 2008), and China’s large holdings of U.S. debt allow China to influence U.S. and world policy (Myers, 2018). In addition, some scholars argue that China views its holdings of U.S. debt as a weapon to resolve the Taiwan dispute (Gertz, 2010). Some literature put forward the concept of “creditor power,” believing that China and other major creditors of the U.S. should jointly reduce their holdings of U.S. Treasury securities at the right time as a means to affect the U.S. and drive other creditors to act together through China to magnify their impact on the U.S. (Kang, 2019). On the other hand, some studies defend that if China focused on selling U.S. Treasuries to strike the U.S. economy, with the sharp depreciation of dollar assets and fluctuations in commodity prices, the world economy would be greatly affected and China itself would suffer huge losses. (Dorn, 2008; Kirshner, 2008). Studies indicate that China is far more sensitive and vulnerable than the U.S. in the economic interdependence between the two countries, so it is unlikely that China would take the initiative to break the “balance of financial terror” (Xiang & Wang, 2014). Seeing huge amounts of U.S. debt as a “weapon” and counterproductive means for China to strike the U.S. is actually more of an unrealistic fantasy, with little chance that China will strike the U.S. by selling U.S. debt in a state of “financial mutual assured destruction” or “mutual assured devastation” (Reilly, 2013). China may gain some policy autonomy by holding huge amounts of U.S. debt, but this is more like a strategic balancing factor than a unilateral means of attack by China, and the strategic deterrent effect of China’s holdings should not be overestimated (Drezner, 2009). In reality, there is no clear evidence or conclusion on whether China has really used U.S. Treasury securities as a “counter weapon.”

It can be seen that the literature generally agrees that China’s holding of U.S. Treasury securities is of political and strategic significance, which is not a purely economic issue. While China’s holdings are affected by various economic factors, they may also be affected by changes in China-U.S. relations and China’s foreign policy toward the U.S. As a political factor, the impact of China-U.S. relations on China’s holdings of U.S. Treasury securities is of great importance in the study of China-U.S. relations and economic diplomacy. However, the relevant empirical studies are still relatively limited, especially in the context of intensified strategic competition between China and the U.S. and the deterioration of bilateral relations. Some researchers have included political factors in their study by setting dummy variables and found that the deterioration of bilateral political relations between China and the U.S. lead to the reduction of China’s holdings of U.S. Treasuries (Wu & Wang, 2010). From the previous literature, the possible explanations for China’s holding of a huge amount of U.S. Treasury securities can be summarized in Figure 2.

Possible explanations for China’s holding of U.S. Treasury securities.

This paper uses time series data on China-U.S. relations to study their impact on the scale of China’s holdings of U.S. Treasury securities. By controlling various economic factors, the paper examines and compares the influence of different political and economic factors on China’s holding decisions.

Research Hypotheses

Under the theory of “weaponized interdependence,” China’s holding a huge amount of U.S. Treasury securities can be regarded as a potential political and strategic tool. Some scholars argued that China and other countries cannot shake off their interdependence with the U.S. in the short term (Nye, 2020). If U.S.-China relations deteriorate, China might impact U.S. financial markets or even the global dominance of the U.S. dollar by selling U.S. Treasury securities or adjusting its holdings. Accordingly, this paper proposes the following hypothesis:

Furthermore, from the perspective of “foreign exchange reserve management,” China’s holding of a huge amount of U.S. Treasuries can be seen as an economic investment behavior. China’s investment aims to realize the preservation and appreciation of U.S. dollar reserves. Therefore, the scale of China’s foreign exchange reserves and the risks and returns of U.S. Treasuries would have an impact on the scale of China’s holdings. Therefore, this paper proposes the following hypotheses:

Data Selection and Processing

Data and Variables

The paper uses monthly data with the time interval from July 2000 to July 2022 due to the data availability. The specific variables and processing are as follows:

China’s Holdings of U.S. Treasury Securities (lnTS)

The original data is from the U.S. Department of the Treasury. The paper takes its natural logarithm as the dependent variable.

Score of China-U.S. Relations (REL)

The data is from the “Foreign Relations Database” of the Institute of International Relations, Tsinghua University, China. The paper takes it as the core independent variable. According to the Institute of International Relations, Tsinghua University (2012a, 2012b), this database uses quantitative measurement methods to score the bilateral relations between China and seven major powers, namely the United States, Japan, Russia (Soviet Union), the United Kingdom, France, India, and Germany. The events include visits, meetings, statements, and diplomatic events (including exceptions and treaty agreements). The main sources of the events are the People’s Daily and the Chinese Ministry of Foreign Affairs website. The score range is [−9, 9], with events with a positive impact on the relationship assigned a positive value and events with a negative impact assigned a negative value. The total score for the current month’s events is calculated based on a formula. It has consistency in statistical methods over a long period of time, and can accurately capture the bilateral political relations between China and other countries (For more details, see the website of the Institute of International Relations, Tsinghua University: http://www.tuiir.tsinghua.edu.cn).

China’s Foreign Exchange Reserves (lnFR)

The original data is from the People’s Bank of China, and the paper takes its natural logarithm. As foreign exchange reserves are the main source of funds for China to purchase U.S. Treasuries, the variable can reflect the changes in the “pool of funds” that China uses to purchase dollar assets.

China-U.S. Trade Balance (lnNT)

The original data is from the General Administration of Customs of China, and the paper takes its natural logarithm. The trade balance between China and the U.S. (totally China’s surplus within the study period) directly reflects the size of China’s dollar reserves from the U.S. in the current account. Some studies believe that the trade surplus with the U.S. is the most important reason for China to have large dollar reserves and purchase large-scale U.S. Treasury securities (Sun, 2014). On the other hand, since the bilateral trade between China and the U.S. is an important area of interaction between the two counties and the China-U.S. trade war has a far-reaching impact on both countries in recent years, the variable can also reflect the economic ties and trend of trade between China and the U.S.

Absolute Rate of Returns of U.S. Treasury Securities (R)

The original data is from the Federal Reserve. As 3-month, 1-year, 3-year, 10-year, and 20-year U.S. Treasuries are the main types purchased by China which cover short, medium, and long-term bonds, the paper refers to the method of Wu and Wang (2010) and takes the arithmetic average of the five bond returns as the absolute level of U.S. Treasury returns. Since the returns are daily data, their monthly average are taken to reduce the loss of information. The variable mainly reflects the economic benefits of China’s investment in U.S. Treasury securities and the effect of maintenance and appreciation of dollar assets.

Relative Returns of U.S. Treasury Securities (CR)

The U.S. corporate bond returns are taken as the benchmark, and the data is from the U.S. Department of the Treasury. The paper takes the arithmetic average of returns of 6-month, 1-year, 3-year, 10-year, and 20-year corporate bonds respectively. It further takes the spread between the absolute returns of U.S. Treasuries and U.S. corporate bonds of each month to obtain the relative returns of U.S. Treasuries. The variable mainly reflects the opportunity cost of China’s investment in U.S. Treasuries and how other investment options affect China’s behavior in holding U.S. Treasuries.

In addition, some scholars have also considered the exchange rate as one of the factors affecting the scale of China’s holdings of U.S. Treasuries (Wu & Wang, 2010). However, China’s dollar reserves are the main source of funds for China’s purchase of U.S. Treasuries. Since China has large dollar reserves and the U.S. Treasuries only account for a portion of them, China will not artificially convert RMB or reserves of other currencies into dollars for U.S. Treasury investment. Therefore, the exchange rate is not taken into account in the paper. Table 1 describes the descriptive statistics of the data sample.

Descriptive Statistics of the Variables.

Stationarity Test of Variables

The variable REL uses the score of the China-U.S. relations in the “Foreign Relations Database.” Since this variable is gained by scoring political events, which is different from general economic variables and not affected by time trends, it does not need to be tested for stationarity. ADF unit root test is used to test the stationarity of other variables, and results are shown in Table 2. It can be seen that all variables can reject the null hypothesis at the 5% significance level, indicating that they are all stationary and can be used for further econometric analysis.

ADF Unit Root Test Results.

Note.** and *** indicate statistical significance at 5% and 1% levels, respectively. The lag order is selected according to SC. C represents the intercept, T represents the linear trend term, and N represents neither the intercept term nor the linear trend term.

Construction of Regression Models and Results

Analysis of the OLS Regression

lnTS is taken as the dependent variable in the OLS regression. In Table 3, column (1) shows the regression results of REL as the only independent variable, and column (2) shows the results of all the variables as independent variables. It is likely that although the coefficient of REL in column (1) is significant, the R2 of the model is only 4.07%, indicating that only the REL is not sufficient to explain the change of lnTS. The R2 in the model (2) reaches 99.37%, implying that the model has good explanatory power. In model (2), the coefficients of variables REL and lnFR are significant at the level of 5%, suggesting that China-U.S. relations and the scale of foreign exchange reserves of China have a significant positive impact on China’s holdings of U.S. Treasury securities, and lnNT and CR have no significant impact. The coefficient of R is even significantly negative, which means that China’s behavior of holding U.S. Treasuries is not consistent with returns of assets and investment profit is not the main factor affecting such behavior. In addition, the trade situation between China and the U.S. has no significant impact on the scale of China’s holdings of U.S. Treasuries.

Estimation Results of OLS Regression.

Note. *** indicates statistical significance at the 1% level. Standard errors are in brackets.

Analysis of the Time-Varying Parameter Regression (TVP-R) Model

Construction of the TVP-R Model

The impact of China-U.S. relations on the scale of China’s holdings of U.S. Treasuries is the core issue of the research. To further explore the dynamic correlation between the two, the paper applies the time-varying parameter regression (TVP-R) model based on Bayesian inference developed by Nakajima (2011). The TVP-R model can capture possible changes in the economy’s underlying structure in a flexible and robust manner, and incorporating stochastic volatility tends to improve the estimation performance (Nakajima, 2011). Due to obvious changes in China-U.S. relations during the sample period, time-varying parameters can better reflect the influence of certain factors at different stages and compare the trend. The coefficient of REL is set to be time-varying, and coefficients of other variables are set to be constant to construct model (1):

where xt=(lnFRt, lnNTt, Rt,CRt), which is a vector of covariates; β is a (4 × 1) vector of constant coefficients; εt is the random error. αt is a time-varying coefficient whose volatility follows a random walk process:

The volatility of the random error also follows the random distribution process:

where ht is stochastic volatility. The paper assumes that lϕl<1, ∑ is a positive-definite matrix, and γ,0.

Compared with the traditional maximum likelihood estimation method based on the Kalman filter, in the Bayesian estimation, the parameters, and variables of the above state space model are treated as random variables. The state variables are inferred according to the joint distribution of the parameters. Therefore, the accuracy of the estimation can be improved. In this paper, the Gibbs sampling approach, which is commonly used in the Markov Chain Monte Carlo (MCMC) sampling method proposed by Nakajima (2011), is used to estimate the TVP-R model. The paper refers to Nakajima (2011) to set the initial value and prior distribution of each parameter: α0 = 0; ∑ is a diagonal matrix with a diagonal element of 0.1; h0 = 0; φ = 0.9; ση = 0.1; γ = 1; μ0∼N(0, ∑0);

Regression Results

Table 4 shows the estimation results of the TVP-R model. According to Geweke (1991), the Geweke values corresponding to all coefficients and parameters are less than the critical value of 1.96 at the 5% significance level, indicating that the parameter simulation results converge to posterior distribution and the MCMC process is basically effective. It can be seen that the constant coefficients are not much different from the OLS regression results.

Estimation Results of TVP-R Model.

Figure 3 shows the estimation results of the time-varying coefficient of the variable REL. It can be seen that from April 2007 to January 2009, the scale of China’s holdings of U.S. Treasury securities was negatively affected by China-U.S. relations, and the negative impact in May 2008 was the largest. Combined with the original values of the two in Figure 4, it is likely that in the above time range, the score of bilateral relations between China and the U.S. has declined slightly while the scale of China’s holdings of U.S. Treasury securities has increased significantly. Between 2016 and 2017, when the Trump administration launched a trade war with China and the strategic rivalry between China and the U.S. began to take shape, China’s holdings of U.S. Treasuries also declined, and the two showed a positive correlation. It is worth noting that the strategic competition between China and the U.S. has intensified since 2018, and the score of China-U.S. relations shows a sharp decrease while the scale of China’s holdings of U.S. Treasury securities demonstrates a gentle decline, with the coefficient fluctuating within a very close range from 0. This implies that under the situation of intensified strategic competition between China and the U.S., the China-U.S. relations and the scale of China’s holdings of U.S. Treasuries are “decoupled,” and the influence of China-U.S. relations on the scale of China’s holdings has become minimal.

Posterior estimates of the coefficient αt.

China’s holdings of U.S. Treasuries and score of China-U.S. relations. Data source: U.S. Department of the Treasury; the “Foreign Relations Database” of the Institute of International Relations, Tsinghua University, China.

Construction of the Vector Autoregression (VAR) Model and Results

Construction of the VAR Model

To further explore the specific impact of various variables on the scale of China’s holdings of U.S. Treasuries and their dynamic changes, this paper constructs a vector autoregression (VAR) model for analysis. The VAR model is used to estimate the dynamic relationship of joint endogenous variables, which is commonly used to predict the trend of multiple time series variables and analyze the dynamic impact of random disturbances on the system. Its strict construction and testing process can improve the accuracy of predictions. According to the Schwarz Information Criterion (SC), this paper constructs a VAR(1) model on all variables, and the estimation results are shown in Table 5. In the second column with lnTS as the dependent variable, the coefficient of lnFR(-1) and REL(-1) are significantly positive at the level of 1%, and 10%, respectively, which still suggests that the scale of foreign exchange reserves and China-U.S. relations positively influence the scale of China’s holdings of U.S. Treasuries to some extent. The coefficient of CR(-1) is significantly negative at the level of 5%, which further indicates that the increase in relative returns cannot lead to China’s increase in its holdings of U.S. Treasuries. Both of the trade situation between China and the U.S. and the absolute returns of U.S. Treasuries have no significant impact on the scale of China’s holdings of U.S. Treasuries.

Estimation Results of VAR(1) Model.

Note. *, **, and *** indicate statistical significance at 10%, 5%, and 1% levels, respectively. Standard errors are in brackets. The lag order is selected according to SC.

Analysis of the Impulse Response Function

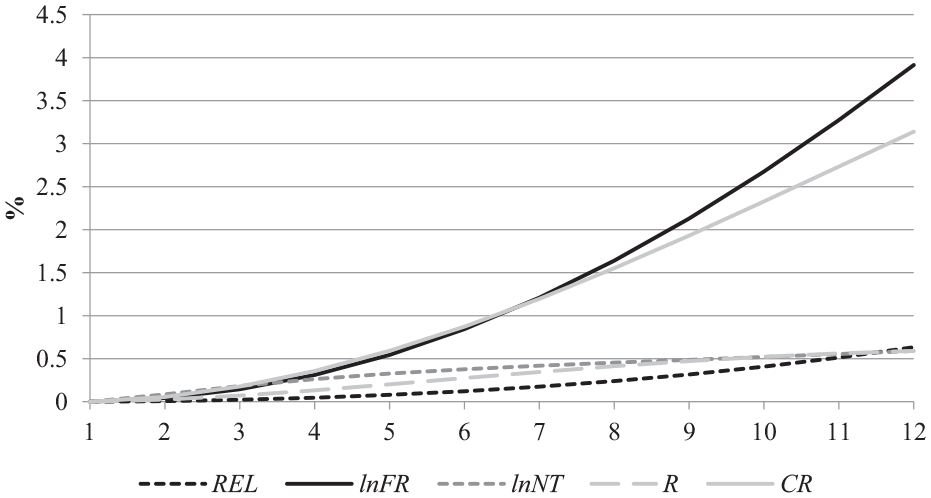

The impulse response function is used to describe the response of an endogenous variable in a VAR model to the impact of another variable, and the evolution of this effect over time. Based on the previous VAR(1) model, the paper investigates the impulse response function (IRF) of lnTS to Cholesky one standard deviation innovations of other variables, respectively, and the results are shown in Figure 5. It can be seen that the innovations of variables REL, lnFR and lnNT have a positive impact on lnTS in the 12 periods, of which lnFR has the greatest impact after the fourth period, about 2 to 3 times of REL, and shows an upward trend. The impact of REL has exceeded that of lnNT since the eighth period following an upward trend. The impact of lnNT shows a downward trend after the sixth period. It suggests that the increase in the scale of foreign exchange reserves is the most important factor affecting China’s holdings of U.S. Treasury securities in the long run, and China-U.S. relations also have a sustained positive impact in the long run. The impact of R and CR on lnTS is negative in all 12 periods, which indicates that the absolute and relative returns of U.S. Treasury securities do not positively influence the scale held by China, and China’s holding behavior is not sensitive to the returns of Treasuries.

IRF of lnTS to Cholesky one standard deviation innovations of other variables.

Variance Decomposition

Variance decomposition is another analysis method of VAR model, which is helpful to understand the proportion of the part caused by other variables in the prediction error of a core variable, which can be used to analyze the relative importance of different variables to changes of a certain variable. The variance decomposition of variable lnTS is further carried out based on the VAR(1) model and the results are shown in Figure 6. It demonstrates that the contribution of lnFR to the impact of lnTS reaches the maximum from the seventh period and continues to increase, reaching 3.91% in the 12th period. The contribution of REL is the smallest in the first 11 periods but shows an upward trend later. Although its contribution to lnTS is only 0.63% in the 12th period, it has exceeded that of lnNT and R. It is likely that the scale of foreign exchange reserves has the greatest impact on China’s holdings of U.S. Treasury securities in the long run, while the impact of China-U.S. relations is rather small but shows an upward trend in the long run.

Variance decomposition of lnTS.

Granger Causality Test

If the information contained in a time series can help predict the future value of another time series, the former is considered to be the Granger cause of the latter. The variable lnTS is tested with other variables using the Granger causality test, and the results are shown in Table 6. At the 5% significance level, lnFR and lnTS are mutual Granger causality, CR is the Granger cause of lnTS, and lnTS is the Granger cause of lnNT. It suggests that the scale of foreign exchange reserves is still more closely related to the scale of U.S. Treasury securities held by China, and the relative yield of U.S. Treasury securities may also have an impact. The scale of China’s holdings of U.S. Treasury securities may affect China-U.S. trade.

Granger Causality Test Between lnTS and Other Variables.

Note. *, **, and *** indicate statistical significance at 10%, 5%, and 1% levels, respectively. The lag order is selected according to SC.

Based on the results of the VAR model, the scale of foreign exchange reserves, as one of the economic factors, is likely to have the greatest impact on the scale of China’s holdings of U.S. Treasury securities and should be regarded as the main factor determining the scale. Although the relationship between China and the U.S., the core independent variable, has a certain impact on the scale of China’s holdings of U.S. Treasury securities, it is much smaller than the impact of foreign exchange reserves. Therefore, it can defend that China’s investment in U.S. Treasury securities is mainly an economic behavior affected by the scale of China’s foreign exchange reserves, and should not be primarily regarded as a political behavior under the influence of China-U.S. relations.

Discussions

Because of the special status of China and the U.S. and the importance of their relations, a profound political and strategic context must exist behind the economic ties between the two countries. Empirical results show that there is a significant positive correlation between the size of China’s foreign exchange reserves and the size of China’s holdings of U.S. Treasury securities. Among all variables considered in the study, it is the strongest factor affecting the scale of China’s holdings. The China-U.S. relations also positively impact the size of China’s holdings of U.S. Treasury securities. The returns of U.S. Treasury securities are negatively correlated with the size of China’s holdings, which suggests that even a reduction in the returns will not lead China to reduce its holdings of U.S. Treasuries, showing that China lacks other safe approaches to invest in dollar reserves. In addition, there is no significant statistical relationship between China’s trade surplus with the U.S. and the size of China’s holdings of U.S. Treasury securities. A comprehensive comparison of various factors suggests that China’s foreign exchange reserve size, an economic factor, has the greatest impact on the size of China’s holdings of U.S. Treasury securities. In contrast, the impact of China-U.S. relations as a political factor is much smaller than that of foreign exchange reserves.

From the early 21st century to the financial crisis, U.S.-China relations remained stable, while China’s holdings of U.S. Treasuries showed an obvious upward trend. This period coincided with rapid growth in China’s economy and foreign exchange reserves, indicating that the scale of China’s U.S. debt holdings was primarily influenced by economic factors rather than an improvement in U.S.-China relations. Figure 3 shows that the time-varying parameters between 2007 and 2008 are also negative. The 2008 financial crisis exposed the vulnerabilities of the U.S. financial system, challenging its global leadership while accelerating China’s rise. The U.S. adopted large-scale monetary easing policies in response to the crisis, indirectly promoting economic growth in emerging markets such as China. Meanwhile, China maintained economic stability through large stimulus plans and expanded its influence in global financial governance. The financial crisis deepened U.S.-China cooperation in global economic governance, and despite differences in trade and exchange rate policies, bilateral relations remained generally positive (Stokes, 2014). Since 2009, the parameters have also become positive, as shown in Figure 3. China’s substantial holdings of U.S. debt demonstrated its support for the U.S.-led global financial system and the status of the U.S. dollar.

After Trump took office in 2017, U.S.-China relations deteriorated significantly, particularly in trade, technology, and geopolitical areas. The Trump administration launched a trade war, imposing tariffs on Chinese goods and accusing China of unfair trade practices. Simultaneously, the U.S. strengthened its technological blockade on China, restricting companies like Huawei. Additionally, the U.S. adopted a tougher stance on issues like the South China Sea and Taiwan, escalating tensions between the two countries. China’s economic strength threatened the economic status and global hegemony of the U.S. and seriously affected the trade relations between the two countries, forming the so-called “Thucydides trap” (Yu, 2022). This series of actions has weakened the trust foundation of China-U.S. relations and intensified competition and confrontation, reflecting Trump’s manipulation of economic interdependence, which can be seen as weaponizing globalization (Nye, 2020). The downward trend in U.S.-China relations continued into the Biden administration, during which China’s holdings of U.S. Treasuries saw a moderate decline. In 2016 to 2017, China made significant reductions in its holdings. However, it quickly recovered, likely a precautionary technical adjustment to Trump’s policies rather than a direct response to the trade war (as this occurred in the early stages of Trump’s term). Figure 3 also indicates that since 2017, the absolute values of the time-varying parameter have gradually decreased.

The COVID-19 pandemic that began in 2019 further exacerbated political and economic confrontation, exacerbating geopolitical tensions between the U. S. and China while limiting policy dialog and amplifying extreme emotions (Ye, 2021). The U.S. accused China of concealing information about the virus and imposed sanctions, which deepened mistrust. Additionally, the pandemic disrupted global supply chains, prompting the U.S. to seek “decoupling” from China to reduce dependency (Zhengyuan, 2024). Both sides also competed fiercely in vaccine diplomacy and global pandemic cooperation, further deepening their differences in global governance, economic, and technological domains. However, the coefficient in Figure 3 does not demonstrate significant fluctuations in 2019, and its absolute value remains around 0, indicating that the deterioration of China-U.S. relations did not lead to a significant decrease in China’s holdings of U.S. Treasuries.

Geopolitical moves, such as establishing the AUKUS (Australia-UK-U.S.) trilateral security partnership, have also heightened tensions in U.S.-China relations (Cu’ờng et al., 2023). The mechanism, established in 2021, was regarded as a geopolitical product of the collision between the emerging world and the declining world, which highlighted the U.S.′s strategic containment of China in the Indo-Pacific region, intensifying security competition between the two nations and increasing tensions in the Asia-Pacific region (Cox et al., 2023). However, despite the clear deterioration in U.S.-China relations, China’s holdings of U.S. debt have only shown a slow decline. This may be more closely related to the slowdown in China’s economic growth and the decrease in foreign exchange reserves, without clear evidence that China used U.S. debt holdings as a tool for diplomacy or geopolitical strategy during this period.

Based on the above analysis, it can be considered that the main purpose of China’s holdings of large-scale U.S. Treasury securities is to maintain and increase the value of dollar assets, which is a necessary step to “store” its own large foreign exchange reserves. The scale of China’s holdings of U.S. Treasury securities is more closely related to economic factors such as the scale of foreign exchange reserves. While deteriorating relations between China and the U.S. may lead China to reduce its holdings to some extent, political and strategic factors should not be considered the main factors affecting China’s investment and holdings of U.S. Treasury securities. At the same time, in the process of intensified strategic competition between the two countries, China has not allowed the large-scale “dumping” of U.S. Treasury securities. The relationship between bilateral relations and the scale held by China shows a trend of “decoupling.” In reality, China’s large-scale holdings of U.S. Treasury securities may play a strategic stabilizing factor between the two countries. However, there is no evidence that China has concentrated on quickly selling U.S. Treasuries as a means and “weapon” to counter the U.S. The decline in China’s holdings should be attributed to the decline in the scale of foreign exchange reserves and the diversification of dollar investment approaches. For example, funding the newly established multilateral financial development institutions such as the Asian Infrastructure Investment Bank, the BRICS New Development Bank, and the Silk Road Fund has also become an important direction for China’s dollar reserve investment. Overall, the results show that China’s increase or decrease in U.S. Treasury securities should mainly be regarded as an economic and investment decision. Although it is also affected by China-U.S. relations and may have certain political and strategic implications, it should not be primarily regarded as an international political and strategic behavior. If China’s investment in U.S. Treasury securities is observed in an “economic-political” spectrum, it is likely more biased toward the economic end.

Conclusions

Analyzing and comparing the effects of economic and political factors on the scale of China’s holdings of U.S. Treasury securities has certain theoretical and methodological innovation values and strong practical policy implications. The paper uses the time-varying parameter regression (TVP-R) and vector autoregression (VAR) models to capture the influence of China-U.S. relations and economic factors on China’s holdings of U.S. Treasury securities. The results show that the scale of foreign exchange reserves and China-U.S. relations significantly positively impact China’s holdings.’ In contrast, the holdings are not sensitive to Treasury returns or the trade balance. The scale of foreign exchange reserves has a far greater impact than the China-U.S. relationship. Dynamic analysis indicates that China-U.S. relations and China’s holding behavior show a trend of “decoupling.” and there is no evidence to prove that China weaponized the creditor’s rights. China’s holdings of U.S. Treasuries should be mainly regarded as an economic decision to preserve the value of foreign exchange reserves.

In view of the trend of “decoupling” between China-U.S. relations and the scale of China’s holdings of U.S. Treasury securities, the impact of strategic competition between China and the U.S. on the scale of China’s holdings may be relatively limited in the future. The change in the scale of China’s holdings of U.S. Treasury securities may mainly depend on the investment requirements of China’s dollar reserves to maintain and increase their value. As a major trading country and an important international investment destination, China will continue to maintain a large scale of foreign exchange reserves in the future and will remain one of the main creditors of the U.S. to hold a considerable scale of U.S. Treasury securities for a certain period of time. This will objectively play a certain strategic stabilizing role in bilateral relations between China and the U.S.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Beijing Municipal Social Science Foundation (22LLZZC058), the Fundamental Research Funds for the Central Universities (2023SKPYGL02), and “the Fundamental Research Funds for the Central Universities” in UIBE (21QD37).

Ethics Statement

It is not applicable.