Abstract

The sustainability of private enterprises is foundational to the high-quality development of the national economy. This paper investigates the role of state ownership in enhancing the sustainable development of private enterprises, utilizing data of A-share private enterprises in China from 2009 to 2022. The findings indicate that state ownership significantly enhances sustainable development of private enterprises, with government agencies yielding a more pronounced effect compared to state-owned enterprise. Mechanism analyses show that state ownership enhances sustainable development by increasing research and development (R&D) investments and efficiency, as well as by enhancing environmental information quality. Furthermore, results show that the influence is more pronounced in private firms with greater financing constraints, severe principal-agent problems, and higher competitive pressures. This study contributes to the understanding of the guiding role of state ownership in the sustainable development of private firms, particularly in the context of weak external institutions.

Plain language summary

It is found that state ownership participation in private enterprises mainly have resource effect and governance effect which can affect firms’ financial performance. We supplement the literature by emphasizing the guiding role of the multi-tasked state ownership which would integrate social value into business value by means of equity blending. We use data of listed private enterprises in China to demonstrate the positive impact of state ownership on the long-term sustainable development of private enterprises.

Keywords

Introduction

Sustainability is the cornerstone and main content of the high-quality development of national economy. With the advancement of market-oriented reforms and mixed-ownership economy development, privately-owned enterprises play a crucial role in enhancing the development of the Chinese economy. However, they still face challenges such as disadvantages in social status and reputation, as well as the adverse effects of systematic discrimination (He et al., 2022). Given severe resource constraints and intense market pressures (Bai et al., 2021), their insufficient capacity for long-term development has raised concerns. During the COVID-19 pandemic (Khan, Parvaiz, Bashir et al., 2022), many private enterprises have closed down, highlighting their vulnerability. Therefore, there is an urgent need to find pathways for improving their sustainable development (Ren et al., 2022).

Since 2013, the Chinese government has proposed the policy of mixed ownership reform (MOR) to stimulate the vitality of state-owned enterprises (SOEs) to adapt to the needs of market-oriented economic system. In parallel with introducing private equity into SOEs, state-owned equity participation in privately-owned enterprises (POEs) as non-controlling shareholders is another pathway to develop mixed-ownership economy, which is known as “reverse mixed ownership reform” (X. Li et al., 2023). This reform aims to optimize the allocation of state capital and enhance the development quality of private enterprises.

An increasing number of studies have focused on the consequences of reverse mixed-ownership reform, yet the findings remain inconclusive. Most studies argue that state ownership has a beneficial influence on private firms’ performance (He et al., 2022; Mohr et al., 2016; Song et al., 2015, 2016), while others prove that it may have adverse effects (P. Wang et al., 2023). Different theories are adopted to elucidate the divergent effects of state ownership, including the resource dependence theory, and principal-agent theory. On the one hand, more resources from state ownership can alleviate resource constraint and contribute positively to business performance. However, this resource support may diminish the private firms’ need to pursue organizational legitimacy through engaging in social responsibility activities (G. Xiao & Shen, 2022). On the other hand, state shareholders could enhance the corporate governance structure of private enterprises. Yet, it may lead to conflicts among shareholders and managerial inertia of executives, and thereby increasing the risk of “zombification” and “dissolution” of the mixed-ownership private firms (P. Wang et al., 2023; Z. Xiao et al., 2022). Zheng et al. (2024) finds that state ownership participation exacerbates labor cost stickiness and harm corporate productivity in the short term but can benefit corporate innovation in the long term.

Considering these inconclusive findings, does state ownership enhance or diminish the sustainable development of private firms? This intricate relationship needs a comprehensive analysis from a new theoretical perspective. Grounded in the multi-task theory, we first explore whether state ownership in private firms can provide an internal driving force for more sustainable development. We further examine the heterogeneous effects of government shareholding and SOE shareholding, providing additional support for the main hypothesis under multi-task theory. We next conduct a series of robustness and endogeneity tests, including alternative variables, samples, and models. Then, we explore the mechanisms through which the enhancement operates, and find that R&D investment, innovation efficiency and environmental information disclosure quality are the main mediators. Our final analyses examine the heterogeneous effects in private firms with different characteristics regarding financing constraints, principal-agent problems, and competitive pressures.

This study examines the role of state ownership in supporting the long-term sustainable growth of private firms by using publicly listed private firms in the China A-share market from 2009 to 2022. China provides a good setting for testing our idea for several reasons. First, it is a representative nation where many private firms are vulnerable in development and facing considerable business disadvantages and pressures. Second, the phenomenon of state ownership in privately-controlled firms is widespread. Third, inadequate external institutions are a typical characteristic of emerging markets. Given these considerations, it is crucial to understand the impact of state-owned capital on the sustainable development of private enterprises in the context of weak external institutions.

This study contributes to the research on mixed-ownership reform, the sustainability of private firms, and ownership structures. First, this study enriches studies on the impact of reverse mixed-ownership reform. Existing literature focuses primarily on the impact of state-owned capital shareholdings on firms’ survival and financial performance. This study extends researches by examining how state ownership affects firms’ sustainable development. Second, the research highlights the guiding role of state ownership beyond the resource provision and monitoring roles. While prior literature emphasizes the resource provision and monitoring roles of state ownership in private enterprises, this paper finds that the multi-tasked state shareholders can help the private firm to focus more on social and environment activities and to pursue long-term value, providing a new theoretical perspective. Third, it supplements research on the pathway to enhance the sustainable development of private enterprises through the mixed ownership structure.

Literature Review and Hypotheses

Literature Review

Role of State Ownership

Government not only constitutes an important component of the external institutional framework influencing all firms in China but also consolidates itself as a key characteristic of socialist market economy system through SOEs (Gabriele, 2010). Since 2013, the Chinese government has proposed the policy of mixed ownership reform (MOR) to stimulate the vitality of SOEs to adapt to the needs of market-oriented economic system. Participation of state-owned equity in privately-owned firms is another form of mixed ownership reform, which is known as “reverse mixed ownership reform” (X. Li et al., 2023). With the continuous promotion of mixed ownership reform, the influence of the policy has attracted increasing academic researches.

Previous research has extensively explored the effects of MOR of SOEs (Guan et al., 2021; Gupta, 2005; Zhao & Mao, 2023), which is realized by introducing non-controlling private shareholders. MOR of SOEs aims to separate the roles of government and SOEs, and introduce market-oriented mechanisms. MOR reshapes and enhances corporate governance (Guan et al., 2021; J. Wang & Tan, 2020) through widening the internal salary gap and reducing the policy burden (Zhao & Mao, 2023). Besides, mixed-ownership SOEs benefit from both government support and the private firms’ market vitality (G. S. Liu et al., 2015). Overall, this reform improves SOEs’ managerial efficiency and innovation capability (X. Zhang et al., 2020), subsequently resulting in better performance (Gupta, 2005) as well as enhanced ESG performance (K. Liu et al., 2023).

Conversely, studies of state ownership participation in private enterprises are relatively scarce, even though it is an important pathway of MOR. Private enterprises in China experience social and economic discrimination (He et al., 2022), and must adapt to an unfavorable institutional environment. They adopt two main strategies to address these challenges. First, private firms leverage personal political connections of board members or the CEO, which can alleviate financing friction and under-investment in family firms (Xu et al., 2013) and improve long-term performance (W. Zhang et al., 2022). Second, privates firms may introduce partial state ownership (Song et al., 2015). Evidence shows that private enterprises with partial state ownership benefit from reputation guarantees (He et al., 2022; H. Yu et al., 2017) and enjoy enhanced protection of their private properties (Sun & Liu, 2021). State ownership in private firms plays an important role in resource provision. It is positively associated with debt financing including bank loan access (Song et al., 2015), debt structure, loan maturity, and securities issuance (Boubakri & Saffar, 2019). Furthermore, it contributes to reduced debt cost (Borisova et al., 2015; Shailer & Wang, 2015) and tax burden (Q. Li et al., 2022). Partial state shareholding raises the innovative capacity (Lo et al., 2022), strategic risk-taking (X. Li et al., 2023), financial performance (Song et al., 2016), ESG performance (Wei et al., 2023), and mitigate the violation behaviors (Y. Yu & Qi, 2022) by addressing the principal-agent problems and providing resources (Zhu et al., 2024).

However, some studies argue that state ownership participation may negatively affect private enterprises. Dong et al. (2016) argues that state ownership is not the decisive factor in bank loans access for Chinese enterprises. Wehrheim et al. (2020) find that mixed ownership with government shareholding after privatization is associated with reduced innovation in response to discontinuous technological change. Dong and Liu (2021) find that state ownership participation increases labor costs and fixed asset investment, which subsequently undermines the technological progress, total factor productivity, and profitability of private enterprises. P. Wang et al. (2023) reveal that state equity has two-sided effect and lower the survival rate of IJV due to unfavorable governmental intervention. Zheng et al. (2024) finds that state ownership participation exacerbates labor cost stickiness and harm corporate productivity but can benefit corporate innovation. Moreover, state ownership increases the possibility of “zombification” of private firms due to the cost-plus effect, resource misallocation, and reduced managerial effort (Z. Xiao et al., 2022).

Firm Sustainability and Influencing Factors

The United Nations explicitly proposed Sustainable development in 1987, emphasizing that the human development must meet the needs of the present generation without compromising the ability of future generations to meet their own needs (Strategic Imperatives, 1987). At the firm level, Reinhardt (2005) indicates that a company must maintain financial sustainability while accounting for its social costs, and consider both economic and environmental performance. The concept of sustainability has evolved over time and is regarded as a triple bottom line encompassing economic, social, and environmental responsibility (M. Yu & Zhao, 2015). However, the sustainable development cannot be directly observed. Researchers have used the membership in the Dow Jones Sustainability Index as a comprehensive measure (M. Yu & Zhao, 2015). With the widespread adoption of the ESG report, which is an acronym for environmental (E, environmental responsibility), social (S, social responsibility), and governance (G, corporate governance), the ESG rating emerged as a valuable indicator of firm sustainability. To promote sustainable development, the literature has explored various factors that affect firms’ ESG performance.

The existing literature mainly studies the driving factors of corporate ESG investment or performance at the institutional, industrial, and firm levels. Both formal and informal institutional factors are important (Ioannou & Serafeim, 2012). The national economic development stage, social and characteristics and culture can explain why enterprises in certain countries tend to exhibit overall higher levels of social responsibility (Cai et al., 2016). However, relying solely on market mechanisms is insufficient. In this context, regulatory policies are needed, for example, environmental tax reform (Bosquet, 2000; F. Li et al., 2024; G. Liu et al., 2022) and environmental regulation (Q. Chen & Li, 2024; Hong et al., 2024). In developed economies, intensified industry competition tends to enhance corporate social responsibility (Fernández-Kranz & Santaló, 2010; Flammer, 2015). However, the opposite effect may occur in emerging markets (Martins, 2022), because a firm’s CSR has no impact on firm value in the context of low product competition or low product fluidity (Sheikh, 2018). Research shows that firms exhibit different social responsibility strategies under different levels of competitive pressures (Dupire & M’Zali, 2018; Leong & Yang, 2020). Digital transformation can promote traceability and transparency of information (Khan, Parvaiz, Dedahanov et al., 2022) that reduce asymmetry between firms and stakeholders, which in turn positively affects corporate ESG performance (Mu et al., 2023).

At the firm level, socially responsible investments are motivated by a range of corporate factors. Larger firms and firms with better financial performance tend to exhibit superior social responsibility (Borghesi et al., 2014). However, DasGupta (2022) finds that companies with poor financial performance engage more in ESG activities in order to maintain their future legitimacy. Family firms might invest less in environmental protection, and exhibit lower level of social responsibility (El Ghoul et al., 2016), unless their shareholders’ interests coincide with societal interests (Abeysekera & Fernando, 2020). State-owned enterprises tend to exhibit higher ESG performance (Weber, 2014) and pay more attention to environmental protection (Hsu et al., 2023; Q. Wang et al., 2022). Controlling shareholder pledging is often associated with a decline in ESG disclosure quality (Huang et al., 2022). Studies show that institutional investors are important determinants in firms’ ESG performance, although the empirical findings remain mixed (Borghesi et al., 2014; T. Chen et al., 2020; Dyck et al., 2019), which may be attributed to the heterogeneity of institutional investors (Y. Wang et al., 2023). CEO attributes also play a crucial role. Firms led by female, younger, or altruistic managers are more inclined to undertake social responsible activities (Aabo & Giorici, 2023; Borghesi et al., 2014). Furthermore, managers’ personal reputation (Rehbein, 2014) or political strategies to maintain favorable political relations also influence corporate social responsibility (Borghesi et al., 2014).

In conclusion, existing research has focused on how state ownership affects the behavior and financial performance of private firms. However, no consensus has been reached, which can be attributed to two main factors. First, the multi-task characteristics of state-owned equity have been overlooked. Second, the subjective initiative and catering behavior of private shareholders has not been adequately addressed. Therefore, research should examine the role of state ownership from a new theoretical perspective. In addition to the resource dependence theory and principal-agent theory, this paper adopts multi-task theory to explain the important role of state ownership in promoting long-term sustainable development of the private sector.

Research Hypotheses

The sustainable development of enterprises is crucial for achieving high-quality development. However, private enterprises in China face multiple challenges and exhibit low sustainable development, which can be attributed to three reasons. The first one is the negative externality caused by profit-seeking. Based on principal-agency theory, private enterprises may maximize the profit of their managers and controlling shareholders at the expense of environmental, social, and other stakeholder interests (El Ghoul et al., 2016). The second one is the short-term decision-making when facing resource constraints and competitive pressure (Leong & Yang, 2020). In the transition to market-oriented economic system, private enterprises are in a disadvantageous position in resource acquisition and market competition. These disadvantages lead private firms to make short-term and suboptimal decisions (Guo et al., 2023), for example, due to insufficient innovation and low cash holdings. The final reason is the imperfect institutional environment. Under weak institutional regulations, private enterprises not only lack awareness of social responsibility, environmental protection and information disclosure (Weber, 2014), but also are reluctant to invest in ESG activities due to difficulties in accurately assessing the return on such investment.

Drawing upon existing literature, this paper argues that state ownership participation may significantly influence private enterprises’ sustainable development ability. However, there are opposite effects based on different theoretical perspectives: one is the “spillover effect” emphasizing the guiding role of state owners, while the other is the “substitution effect” which suggests state ownership may diminish the need for responsible investment to get corporate legitimacy.

State ownership can generate an internal driving force to sustainable development of private enterprises based on multi-tasked theory, which is the “spillover effect.” Shareholders’ nature and composition are important factors affecting firms’ strategic orientation (T. Chen et al., 2020; El Ghoul et al., 2016; P. Wang et al., 2023). State shareholders are very different from private shareholders. The state shareholders are multitask takers under the political logic emphasizing multiple objectives, such as economy sustainability, social welfare, and employment (Lennox & Wu, 2022; Ye & Zhang, 2022). However, private capital focuses on profit maximization under the market logic (Z. Liu et al., 2020; Q. Wang et al., 2022). This fundamental difference is particularly salient in China’s socialist market economy, where the state capital serves as a crucial instrument for implementing government strategies and promoting social welfare. Evidence shows that SOEs controlled by the state are more responsive to social and environmental issues (Hsu et al., 2023; Weber, 2014). State ownership participation in private firms may be an effective way to integrate the governments’ multiple objectives.

When state-owned capital enters private enterprises, it creates a coexistence of political and market logic. The dual-logic system may raise conflicts if the influence of state ownership grows larger than that of the private ownership (Dong & Liu, 2021; P. Wang et al., 2023). However, this effect may be alleviated if the state owners remain as minority shareholders. The resource support and property protection effect grants them influence on corporate decision-making. Private controlling shareholders and managers will make concessions and tend to align their strategies with government expectations instead of merely personal interests. Consequently, the state shareholders’ multi-tasks are embedded into the corporate operation guidelines of private enterprises.

Another manifestation of the guiding role is that state ownership encourages a focus on long-term value rather than short-term profits. Firstly, state owners are active supervisors and enhance corporate governance quality, which foster more balanced strategic decisions (Chen et al., 2024). Existing studies show that the state shareholder can provide reputation guarantees to the participating private firms (He et al., 2022; H. Yu et al., 2017). In fact, the transmission of reputation mechanisms is bidirectional and dynamic. If the participating private firm engages in misconduct for short-term interests, the bad reputation will extend to the state shareholders. Therefore, state shareholders have a strong motive to supervise private firms’ short-term behaviors, such as business and information disclosure violations (Y. Yu & Qi, 2022). Secondly, state ownership enhances long-term confidence by mitigating the external pressures. Dyck et al. (2019) reveal that institutional connections reduce market uncertainties, allowing private firms to focus on sustainable development initiatives. Besides, state ownership participation enables private firms to access broader financing channels and more favorable credit terms, which can increase the confidence and risk-taking behaviors (X. Li et al., 2023).

Taken together, state ownership embeds multi-tasks into the mixed-ownership private enterprises and guides them to care more about social welfare, environmental protection and long-term development.

Hypothesis 1: State ownership participation will improve the sustainable development of private enterprises.

However, from the perspective of resource dependence theory, state ownership may negatively affect private enterprises’ willingness to invest in social responsible issues, resulting in the “substitution effect.” Organizations actively make efforts to mitigate the disadvantages of external institution environment rather than passive recipients. Private firms may adopt certain approaches to gain organizational legitimacy and deal with the unfavorable environment, including constructing political connections (Xu et al., 2013; W. Zhang et al., 2022) and undertaking more social responsibility (Abeysekera & Fernando, 2020). DasGupta (2022) finds that private enterprises generally face certain resource constraints and “ownership discrimination” and may show higher ESG performance in order to gain organizational legitimacy or attract investors.

State ownership is a good way to construct a political connection with the government (Song et al., 2015, 2016). Its resource provision role is highlighted in the literature, including bank loans and bonds (He et al., 2022; Song et al., 2015), government subsidies and tax burden (Q. Li et al., 2022; Ye & Zhang, 2022), and even human capital (Zhou & Yun, 2022), which is good for the survival and financial performance of the private enterprises. However, this resource-supporting effect also reduce the willingness to meet the demand of stakeholders. G. Xiao and Shen (2022) found that political connections reduce the resource allocation for environmental protection, and thus impede firms’ environmental performance. This finding suggests that private enterprises’ environmental investments are primarily driven by instrumental motivations. If these objectives can be achieved in alternative pathways, they will reduce social and environmental investments which are perceived as discretionary costs rather than strategic necessities. For private enterprises, political connections through introduction of state ownership enhance their organizational legitimacy and facilitate resources acquisition, which may substitute for the initial motive of social responsibility and environmental protection. Therefore, we hypothesize that due to the resource substitution effect, private enterprises with state ownership participation will reduce their commitment to social and environment responsible initiatives, leading to a lower level of sustainable development.

Hypothesis 2: State ownership participation will reduce the sustainable development of private enterprises.

Data and Methodology

Data

Sample in this paper consists of non-financial companies originally listed as private firms in China’s A-share stock market from 2009 to 2022 to exclude the influence of the 4 trillion RMB stimulus plan in 2008. Besides, firms with missing data are excluded. Finally, we obtained 19,796 firm-year observations. Additionally, all continuous variables were winsrized at the 1st and 99th percentiles. We obtain corporate sustainable development data from the Hua Zheng ESG rating in Wind Database and other data from China Stock Market & Accounting Research (CSMAR) database.

Definition of Variables

Dependent Variables

The dependent variable is the sustainable development of private enterprises (SusDev), measured by Hua Zheng ESG rating (Mu et al., 2023). Hua Zheng ESG rating system adopts a top-down three-tier framework based on ESG principles with three primary indicators, 14 secondary indicators, 26 tertiary indicators. The rating system collects over 130 basic indicators from both corporate public disclosures and additional information extracted from government websites, regulatory announcements and news media by using machine learning and text mining techniques. It emphasizes features of China’s market context including information disclosure quality, regulatory compliance, and poverty alleviation activities. Besides, the system applies adjusted weights and indicators in different industries to enhance rating accuracy. Therefore, the Hua Zheng ESG rating serves as a reliable and relevant measure of corporate sustainable development. The Hua Zheng ESG ratings have nine levels, ranging from “C” to “AAA,” which are assigned a score from 1 to 9, respectively, and a higher score indicates better sustainable performance.

Independent Variables

The independent variable is the state ownership in private firms, which is measured by two indicators. The first one is a dummy variable (SO1) that equals 1 if there is at least one state shareholder among the private firms’ top 10 shareholders, and 0 otherwise. The second one is the proportion of state shares (SO2), measured by the total shareholding ratio of the state shareholders among the top 10 shareholders. These two measures are complementary to address the presence and influence of state ownership in private firms.

In addition, in order to examine the different influences of different types of state shareholders, the state ownership are classified into government ownership (SOG1 and SOG2) and SOE ownership (SOC1 and SOC2), representing shares held by the government agencies and SOEs, respectively.

Control Variables

The following variables are selected as control variables: company asset size (Size), leverage ratio (Lev), profitability (ROA), growth rate (Growth), firm age (Age), ownership concentration (Top1), board of directors size (Lnbd), independent directors’ ratio (Indep), CEO duality (Dual), and the political connection (PC).

Definitions of major variables are presented in Table 1.

Definitions of Major Variables.

Research Models

To test the hypotheses, we employ the following OLS regression Model (1):

where SusDev is the annual ESG rating score. SO represents state ownership participation, including SO1 and SO2. Controls include a set of firm-level control variables. Year and Ind represent year and industry fixed effects. OLS regression has several methodological limitations despite its wide application in academic researches, such as concerns about multicollinearity, self-selection bias and reverse causality. Therefore, this paper conducts a series of robust checks and endogeneity tests.

Empirical Results Analysis

Baseline Regression Results

Descriptive Statistics

Table 2 shows that the mean of SusDev is 4.136 and the median of SusDev is 4, indicating that most of the sample firms’ ESG rating is below BB. The mean of SO1 is 0.386, suggesting that only 38.6% of the samples have at least one state equity shareholder among the top 10 shareholders. The mean of SO2 is 0.015 with the maximum value of 0.263, meaning that the average ratio of state shareholders is only 1.5% and the largest ratio is 26.3%.

Descriptive Statistics of Major Variables.

For different types of state ownership, the mean of SOG1 is 0.137 and SOG2 is 0.003. The mean values of SOC1 and SOC2 are 0.298 and 0.014, respectively, which are higher than SOG1 and SOG2, suggesting that SOEs are more likely to hold shares in private enterprises than government agencies.

Baseline Regression Results Analysis

Table 3 presents the baseline OLS regression results of Model (1). We used robust standard errors to obtain more reliable standard errors and more accurate regression estimates. The regression model shows reasonable explanatory power, with an R-squared value of approximately 0.17 and F-statistics greater than 250. The variance inflation factor (VIF) values of all control variables are below 2, indicating no significant multicollinearity issues.

Baseline Regression Results.

Note. t-Values are in parentheses.

Significance level p < .1. **Significance level p < .05. ***Significance level p < .01.

The coefficient of SO1 is 0.081 and statistically significant at 1%, which means that private enterprises with state ownership exhibit higher ESG rating than those without. The coefficient of SO2 is 0.495, and statistically significant at 1%, suggesting that higher state ownership ratios are associated with higher ESG rating. The results mean that partial state ownership positively affects private enterprises’ sustainable development, supporting hypothesis 1, rather than hypothesis 2.

Existing research shows that state ownership reduces the debt cost and improves the financial performance (He et al., 2022; Song et al., 2016). However, some research finds that it will increase policy burden such as labor costs and fixed asset investment, which reduce short-term performance (Dong & Liu, 2021; Z. Xiao et al., 2022). This study finds that state ownership enhances private enterprises’ sustainable development. State shareholders serve as a guide in balancing economic interests, social benefits and environmental protection efforts. Although this strategic shift may increase the cost and reduce short-term financial performance, it creates greater firm value through sustainable development in the long run. For instance, state ownership may increase private firms’ labor costs under the government’s policy of raising labor income, which reduces short-term financial performance. However, this strategy enables private firms to attract more high-skilled talent and enhance creative potential, supporting their long-term development. The finding is consistent with the findings of Zheng et al. (2024).

In China, state equity is collectively owned by all citizens and serves to maximize public interests. The attributes of state equity fundamentally drive SOEs’ multiple tasks. Q. Wang et al. (2022) argue that although SOEs are criticized for their inefficiency, they play a crucial role in promoting social welfare. When state shareholders participate in private firms, they integrate social welfare considerations into business decisions, promoting a balance between commercial profits and social value. This study shows that reverse MOR is a crucial way to guide private firms in fulfilling social and environmental responsibilities, thus enhancing the sustainability of national economic development, providing a reconciliation for mitigating short-term performance.

State equity is held by central governments, local governments or (and) SOEs in China. To examine whether the impact varies across different types of state shareholders, this paper replaces SO1 with SOG1 (SOC1), and replaces SO2 with SOG2 (SOC2). Results in columns (3) to (6) of Table 3 show that the coefficients of SOG1 and SOG2 are 0.1677 and 4.845, respectively. The coefficients of SOC1 and SOC2 are 0.034 and 0.308, which are much lower than those of SOG1 and SOG2. The results indicate that government yields a more pronounced effect than SOEs.

The differential effect between government shareholding and SOEs shareholding can be explained by their motivations for equity participation. Direct government shareholding is primarily driven by economic regulation under political logic (Z. Liu et al., 2020), whereas SOE shareholders must balance social responsibility and economic profit under both political logic and market logic. Therefore, private enterprises with government shareholders are required to give greater consideration to social and environmental responsibilities than those with SOE shareholders.

Robustness Test

Robustness tests are conducted as follows:

(1) Alternative explanatory variable and dependent variable

To address concern of potential reverse causality, we use 1-year lagged explanatory variables (L.SO1 and L.SO2) as alternative measures of state ownership participation. The results in Table 4, columns (1) to (2) show that coefficients of L.SO1 and L.SO2 remain significantly positive.

Robustness Test: Alternative Explanatory Variables and Dependent Variables.

Note. t-Values are in parentheses. *Significance level p < .1. **Significance level p < .05. ***Significance level p < .01.

Hua Zheng ESG ratings are released quarterly, and they may exhibit seasonal volatility. This study uses the mean of the quarterly ESG rating scores (SusDev_avr) as an alternative dependent variable, instead of the year-end rating scores. As shown in columns (3) and (4) of Table 4, coefficients of SO1 and SO2 in columns (1) and (2) of Table 4 are still significantly positive.

(2) Sub-sample analysis

First, we restrict the sample period from 2009 to 2019 to exclude the impact of COVID-19 which may affect both state owners’ behavior and private firms’ ESG investment. Coefficients of SO1 and SO2 in columns (1) and (2) of Table 5 remain significantly positive.

Robustness Test: Results of Sub-samples.

Note. t-Values are in parentheses. *Significance level p < .1. **Significance level p < .05. ***Significance level p < .01.

Furthermore, to address potential self-selection bias in state ownership participation, this paper examines a sub-sample of private enterprises that have experienced state ownership participation for at least 1 year during the sample period. This approach helps to mitigate the concern that firms with higher ESG rating are more likely to attract state equity. The coefficients of SO1 and SO2 in columns (3) and (4) of Table 5 are still significantly positive.

(3) Two-stage instrumental variable approach

To address potential endogeneity concerns, this paper employs a two-stage instrumental variable (IV) method. Specifically, the industry average state ownership ratio (excluding the target firm) is used as the instrumental variable (SO_IV). The rationale is that a higher average ratio indicates that the industry is more attractive to state equity, and may increase the likelihood of state equity participation, but should not directly affect the target private firm’s sustainable development. The endogenous tests for SO1 and SO2 yield p-values of 0.0334 and 0.0304, which means the IV method can alleviate potential endogeneity problem.

The results of the two-stage IV regression are shown in Table 6. In the first-stage regression, the coefficients of SO_IV are −0.684 and −0.087, both significant at 1%. In the second-stage regression, the coefficients of the instrumented SO1 and SO2 are 1.305 and 10.260, respectively, corroborating the baseline regression.

Results of Two-stage IV Approach.

Note. t-Values are in parentheses. *Significance level p < .1. **Significance level p < .05. ***Significance level p < .01.

(4) PSM-DID approach

To provide evidence of causal relationship regarding the impact of state ownership on private firms’ sustainable development, this section employs a time-varying difference-in-difference (time-varying DID) approach (He et al., 2022), considering that private firms introduced state ownership at different points in time. The time-varying DID model is shown in Model (2):

where SOE is a dummy variable indicating whether private firm i introduces state shareholders for the first time in year t, which equals 1 for the participation year and the following 3 years and 0 for the 3 years prior to the participation year, thus creating the double difference between the treated group and control group, as well as between “pre-treatment” and “post-treatment” periods.

To minimize potential selection bias between treated and control groups, we conduct propensity score matching (PSM) before time-varying DID analysis. We use the binary logistic model to estimate the propensity score, adopting the following covariates: size (Size), leverage ratio (Lev), profitability (ROA), ownership concentration (Top1), independent directors (Indep), annual stock return rate (ASR) and stock risk (Risk, measured by stock negative skewness). Then, we proceed to match respondents on the propensity scores using one-to-one nearest neighbor matching without replacement to identify the matched firm in the same industry-year from control group for the treated firm. After that, we use standardized mean differences (SMDs) to evaluate matching quality, and results reveal that the SMDs of the covariates between the treated group and control group are not significant, with p-values above 0.1.

The parallel trend assumption, which requires that treated and control groups must exhibit similar trends prior to the intervention, is the basic condition for DID analysis. Since the time of state ownership participation varies across private firms, we use an event study method by examining interactions of treatment indicators and year dummy variables, as shown in Model (3):

where

Results of Model (2) and Model(3) are shown in Table 7. In Column (1), coefficient of SOE is significantly positive, indicating that state equity participation enhances private firms’ sustainable development. Column (2) shows that coefficients for SOE−3, SOE−2, and SOE−1 are consistently insignificant, proving that there were no significant differences between treated and control groups prior to the state ownership participation. Coefficient of SOE0 is significantly positive, while that of SOE+1, SOE+2, and SOE+3 are insignificant, suggesting that state ownership participation generates immediate positive effects on private firms’ decision in the entry year without lagged effects.

Results of PSM-DID Model.

Note. t-Values are in parentheses. *Significance level p < .1. **Significance level p < .05. ***Significance level p < .01.

Mechanism Channels Analysis

The baseline regression results indicate that state ownership enhances sustainable development of private enterprises because the state shareholders play a guiding role due to their multi-tasked nature. However, the mechanisms through which this “spillover effect” operates need further investigation. This paper examines three potential channels: R&D investment level, innovation efficiency, and environmental information disclosure quality, all of which represent long-term sustainable development orientation.

Mediating Effect of R&D Investment

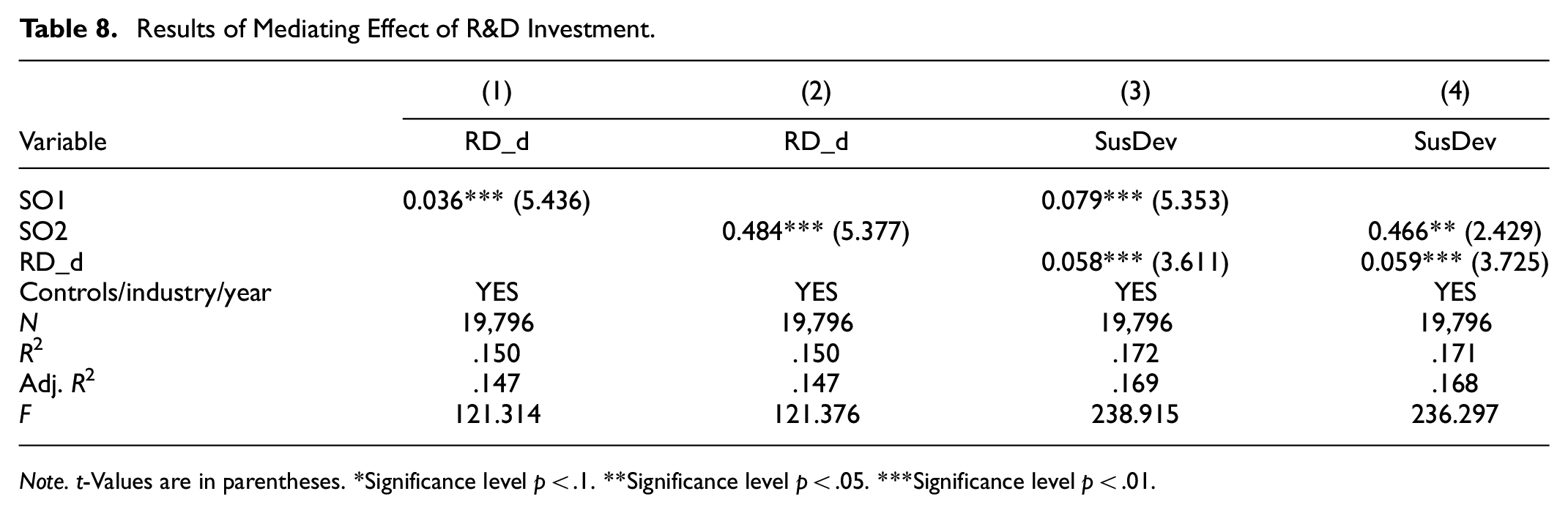

Innovation activities are crucial for firms’ sustainable development, and R&D investment serves as a vital input. However, R&D activities often require a large amount of capital and are risky, as their potential to generate intangible assets and create competitiveness is highly uncertain. As a result, private firms often underinvest in R&D. State ownership can provide tangible and intangible resources to private enterprises. These resources enhance sustainable development only if they are allocated to activities that create long-term corporate value rather than serving the controlling shareholders’ short-term interests. This raises the question: do private enterprises allocate more resources to R&D activities when state ownership is present?

In this paper, we use a dummy variable (RD_d) to measure R&D investment, which equals 1 if the firm’s R&D investment exceeds the industry average level, and 0 otherwise. The coefficients of SO1 and SO2 in columns (1) to (2) of Table 8 are 0.036 and 0.484, respectively, demonstrating that state ownership can evidently increase the probability of more R&D investment than industry average level. In columns (3) to (4), when RD_d is added as a mediator, coefficients of SO1 and SO2 are still significantly positive, and coefficients of RD_d are 0.058 and 0.059, statistically significant at 1%. The results indicate that R&D investment above the industry average is positively associated with higher ESG ratings, suggesting that state ownership can improve the sustainable development ability of the participating private firms by allocating more resources in R&D than their industry peers.

Results of Mediating Effect of R&D Investment.

Note. t-Values are in parentheses. *Significance level p < .1. **Significance level p < .05. ***Significance level p < .01.

Mediating Effect of Innovation Efficiency

While high R&D investment signals a commitment to long-term corporate value, the R&D activities inherently carry substantial risks. Without enhanced research capabilities, such investments may lead to undesired losses, potentially undermining sustainable development. Therefore, we examine whether state ownership participation improves private firms’ innovation efficiency by specifying the following Model (4):

Where Patent is measured by the natural logarithm of total number of patent applications plus 1, and Green is measured by the natural logarithm of total green patent applications plus 1. R&D is measured by the natural logarithm of R&D investment plus 1. Interaction term R&D*SO is included to test the innovation promotion effect of state ownership participation.

The regression results in Table 9 show that the coefficients of R&D are all significantly positive at 1%, indicating that R&D investment is positively associated with total and green patent applications. The coefficients of R&D×SO1 and R&D×SO2 are 0.010 and 0.086 in columns (1) to (2), indication that private firms with state ownership exhibit higher innovation efficiency at a given level of R&D investment. The coefficients of R&D×SO1 and R&D×SO2 are 0.010, and 0.057 in columns (3) to (4), respectively. The results show that, for a given level of R&D investment, private firms with state ownership have a stronger orientation toward green innovation. This finding suggests that state ownership not only enhances innovation efficiency, but also promotes green innovation activities. The result extents the research by Zheng et al. (2024) to the domain of green innovation.

Results of Mediating Effect of Innovation Efficiency.

Note. t-Values are in parentheses. *Significance level p < .1. **Significance level p < .05. ***Significance level p < .01.

Mediating Effect of Environmental Information Disclosure

Information disclosure reduces information asymmetry between firms and stakeholders. With government’s initiatives to promote sustainable information disclosure, more and more private enterprises disclose CSR or ESG reports. However, they show lower quality than SOEs because of lower external regulatory pressure (Weber, 2014).

State ownership participation may act as an internal driver for better environmental information disclosure. First, private enterprises with state ownership do better in sustainable development and show greater willingness to disclose relevant information. Second, the attributes of state ownership will raise awareness to disclose social and environmental information. Third, state ownership participation in private firms attracts increasing public attention and government supervision, pushing firms to improve their information disclosure quality.

Environmental information, extracted from firms’ annual reports, CSR or ESG reports, includes waste gas, waste water, dust (soot), solid waste, noise, light pollution, radiation, and cleaner production. Each pollutant is scored according to its disclosure quality: 0 for no relevant information, 1 for qualitative description, and 2 for quantitative information. Environmental information disclosure (EID) is measured by the natural logarithm of the sum value plus 1.

Table 10 presents the regression results. In columns (1) and (2), the coefficients of SO1 and SO2 are 0.033 and 0.624, indicating that private firms with state ownership exhibit significantly higher level of environmental information disclosure. In columns (3) and (4), when EID is added, the coefficients of SO1 and SO2 are still positive, while those of EID are 0.195 and 0.196, respectively. These results suggest that higher environmental information disclosure is associated with better sustainable development performance. Overall, environmental information disclosure quality acts as a mediator between state ownership participation and private firms’ sustainable capability.

Results of Mediating Effect of Environmental Information Disclosure.

Note. t-Values are in parentheses. *Significance level p < .1. **Significance level p < .05. ***Significance level p < .01.

Heterogeneity Analysis

The Heterogeneous Impact of Financing Constraints

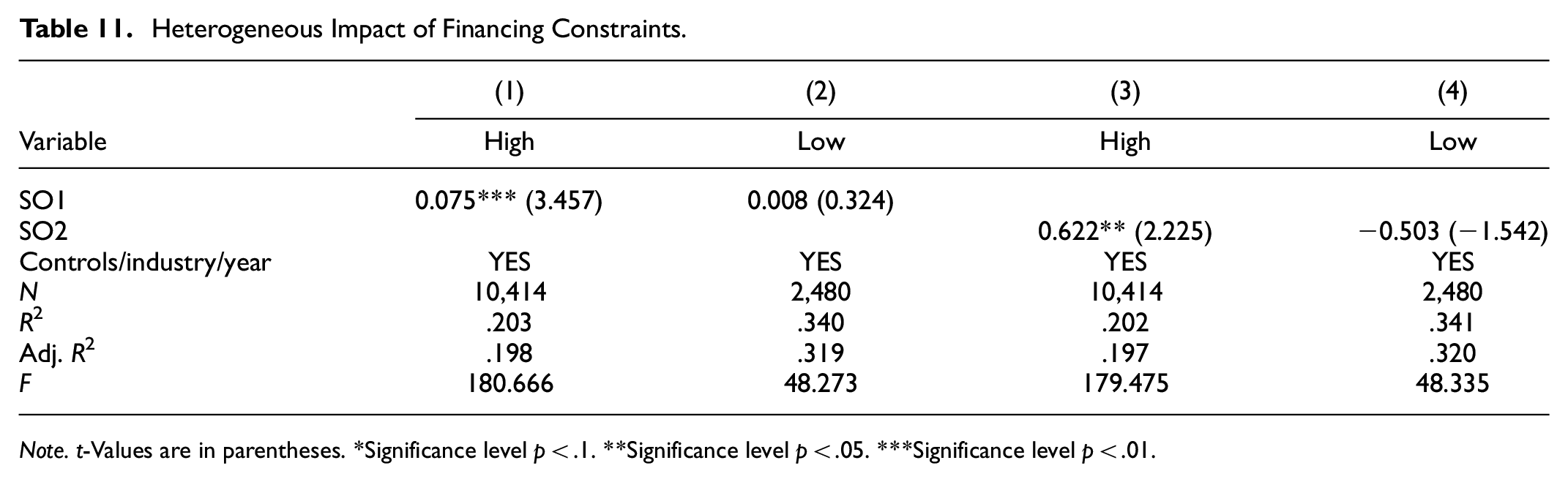

Private enterprises face financing constraints in emerging markets due to underdeveloped financial intermediaries (Guo et al., 2023). However, the financing constraints level varies among private firms. For enterprises with greater financing constraints, state ownership is particularly valuable, and consequently exerts greater influence.

To examine this potential heterogeneous impact, this paper classifies all samples into two groups based on their financing constraint levels measured by Kaplan-Zingales (KZ) index (C. Li et al., 2023): firms with a KZ index above the industry average level are placed in the high financing constraint group, while others are in the low financing constraint group.

Results in Table 11 show that the coefficients of SO1 and SO2 are significantly positive only in the high financing constraint group, indicating that the impact of state ownership on sustainable development is more pronounced for private firms with high financing constraints. The findings suggest that the resource support effect of state shareholders grants them influence over corporate strategy, thereby exerting a stronger impact on private firms with greater financing constraints.

Heterogeneous Impact of Financing Constraints.

Note. t-Values are in parentheses. *Significance level p < .1. **Significance level p < .05. ***Significance level p < .01.

The Heterogeneous Impact of Principal-Agent Problem

Compared to SOEs, the principal-agent problem between controlling and minority shareholders is more prominent in private enterprises, where controlling shareholders divert corporate resources for personal benefit at the expense of minority shareholders, resulting in a loss of investor confidence in long-term firm value. State shareholders serve as active supervisors and effectively monitor controlling shareholders’ self-serving behavior, with greater influence in firms with severe principal-agent problems.

Tunneling behaviors represent a typical principal-agent problem that occurs in firms with separate cash-flow rights and control rights. Based on this characteristic, samples are divided into two groups: firms with separate cash-flow rights and control rights are placed into high principal-agent problem group and firms without such separation are in the low principal-agent problem group. The coefficients of SO1 and SO2 in Table 12 are significantly positive only in samples with separated cash flow rights and control rights. The results indicate that state ownership generates stronger effects in private firms with severe principal-agent problems, and prompts private controlling shareholders to prioritize sustainable development over short-term self-serving behavior.

Heterogeneous Effects of Principal-Agent Problem.

Note. t-Values are in parentheses. *Significance level p < .1. **Significance level p < .05. ***Significance level p < .01.

The Heterogeneous Impact of Industry Competitive Pressure

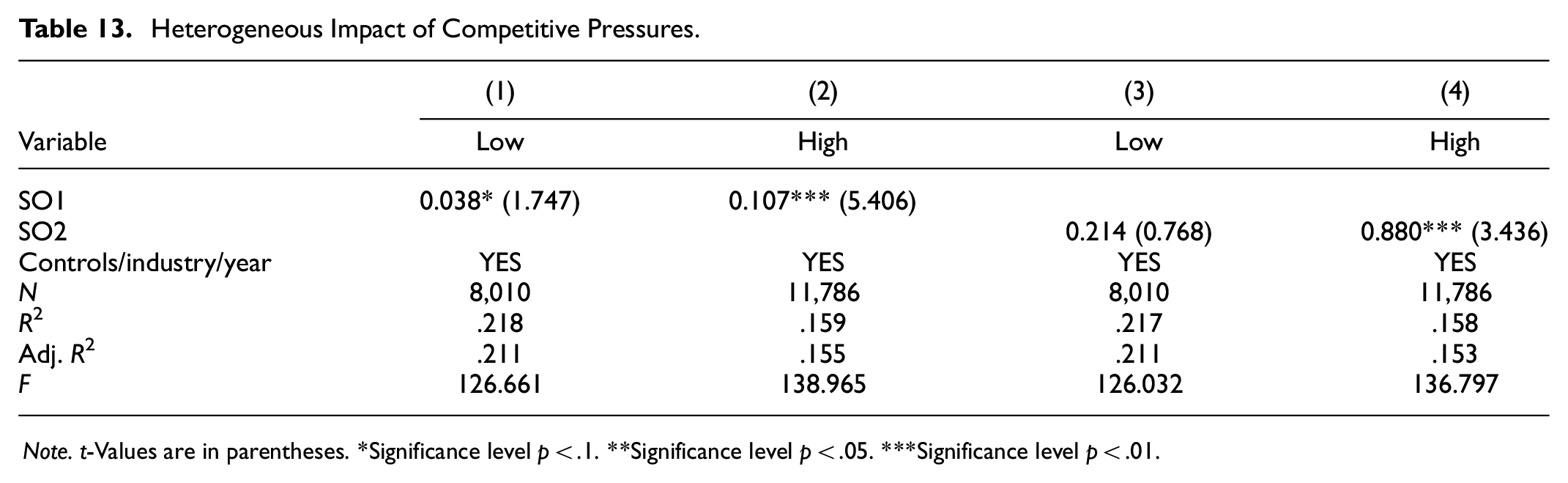

Industry competitive pressure promotes the short-term decision making, and decreases long-term investment in emerging market countries (Martins, 2022), because less efficient markets make it difficult to properly evaluate social and environmentally responsible investments. In addition, severe industry competition heightens perceived uncertainties, leading firms to focus on short-term profit. State ownership can increase the confidence in long-term development through resource provision and reducing perceived uncertainties. So, state ownership exerts stronger effects on sustainable development in industries with higher competitive pressure.

This paper uses the Herfindahl-Hirschman Index (HHI) based on revenue to measure industry competitive pressure. A lower HHI indicates higher competitive pressure due to more non-dominant competitors. Samples are divided into two groups: firms in industries with HHI below the annual average HHI are placed in the high pressure group and others in the low-pressure group. Table 13 shows the coefficient of SO1 is 0.038 in the low pressure group and 0.107 in the high-pressure group. The coefficient of SO2 is 0.214 (statistically insignificant) in the low pressure group but increases to 0.880 (p < .01) in the high pressure group, indicating that state ownership participation is more effective in promoting sustainable development in industries with high competitive pressure. The results suggest that state ownership can help address private firms’ short-sighted behavior under high market competition in emerging markets where legal institutions are insufficient to ensure fair competition.

Heterogeneous Impact of Competitive Pressures.

Note. t-Values are in parentheses. *Significance level p < .1. **Significance level p < .05. ***Significance level p < .01.

Conclusions and Discussion

Prior research shows that private firms in emerging markets face significant challenges in achieving sustainable development. While state ownership through reverse mixed-ownership reform has become increasingly prevalent, existing studies provide inconsistent evidence regarding its influence. Drawing on multitask theory, this study examines whether and how state ownership enhances the sustainable development of private firms.

Using data from Chinese A-share listed private firms over 2009 to 2022, the study finds that state ownership significantly enhances private firms’ sustainable development, with government agencies exerting stronger effects than SOEs. It reveals that this enhancement operates through increasing R&D investments and efficiency, as well as improving environmental information disclosure quality. These positive effects are more pronounced in firms characterized by greater financial constraints, severe principal-agent problems, and intense industry competition.

This study contributes to academic research in several ways. Firstly, this paper explores the effects of reverse mixed ownership reform (Guan et al., 2021; Gupta, 2005; K. Liu et al., 2023; Zhao & Mao, 2023), thereby extending the research scope of mixed ownership reform. Secondly, while prior literature focuses on the impact of state ownership on private firms’ short-term financial performance (Boubakri & Saffar, 2019; He et al., 2023; Song et al., 2016; Zheng et al., 2024), our study enriches the studies to addressing long-term sustainable development. Lastly, beyond the resource provision and monitoring roles of state ownership in existing research (Z. Xiao et al., 2022; Zhu et al., 2024), this study highlights the guiding role of state ownership from multi-task theory, offering a new theoretical perspective to understand how state ownership guide private firms toward sustainable development.

Beyond these theoretical contributions, this study also provides important practical implications for policy-making. First, the government should expand the scope of reverse mixed-ownership reform to private firms with severe financial constraints, weak corporate governance and insufficient external institutions. Second, differentiated policies are needed for government ownership and SOE ownership, given their varying effects on sustainable development. Third, the institutional framework needs to be revised to facilitate private firms’ sustainable strategies that emphasize innovation and information disclosure quality.

Based on China’s unique practice of reverse mixed-ownership reform, this study suggests that state ownership serves as an internal driver for more sustainable development, particularly in the context of inadequate external institutions. Future research could advance this line of inquiry: (1) examining these relationships in other emerging markets with different cultures and institutional environments, (2) investigating other potential moderating or mediating variables (e.g., strategic vs. non-strategic state shareholders), and (3) investigating how state ownership influences corporate culture, stakeholder relationships, and decision-making processes in private firms.

Footnotes

Acknowledgements

I wish to thank professor Chaohong Na for advice on experimental design.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Funding from the Social Science Foundation of China (Grant No. 20XGL004) is gratefully acknowledged.

Ethics Statement

This study did not involve human or animal subjects, and thus, no ethical approval was required.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.