Abstract

Enterprises make charitable donations as one of the main means to fulfill their social responsibility, to explore the impact of religious beliefs and poverty experiences of private enterprise owners on corporate charitable donations, this paper takes the 2018 China private enterprise survey dataset as the research sample, and empirically examines the impact between private entrepreneurs’ religious beliefs, poverty experience, and enterprises’ charitable donations by using the Probit model and the Tobit model. The results of the study are as follows: First, the religious beliefs of the private entrepreneurs can encourage the enterprises to make charitable donations and have more strength in charitable donations. Second, the private entrepreneurs with poverty experience will be more active in making charitable donations and have more strength. This study enriches the literature on charitable donations by private entrepreneurs from the perspective of their characteristics, which has certain theoretical significance; the conclusions of this paper help the government guide private enterprises to make charitable donations, which has certain practical significance.

Plain Language Summary

First, the religious beliefs of the private entrepreneurs can encourage the enterprises to make charitable donations and have more strength in charitable donations; Second, the private entrepreneurs with poverty experience will be more active in making charitable donations and have more strength; This study enriches the literature on charitable donations by private entrepreneurs from the perspective of their characteristics, which has certain theoretical significance; the conclusions of this paper help the government guide private enterprises to make charitable donations, which has certain practical significance.

Introduction

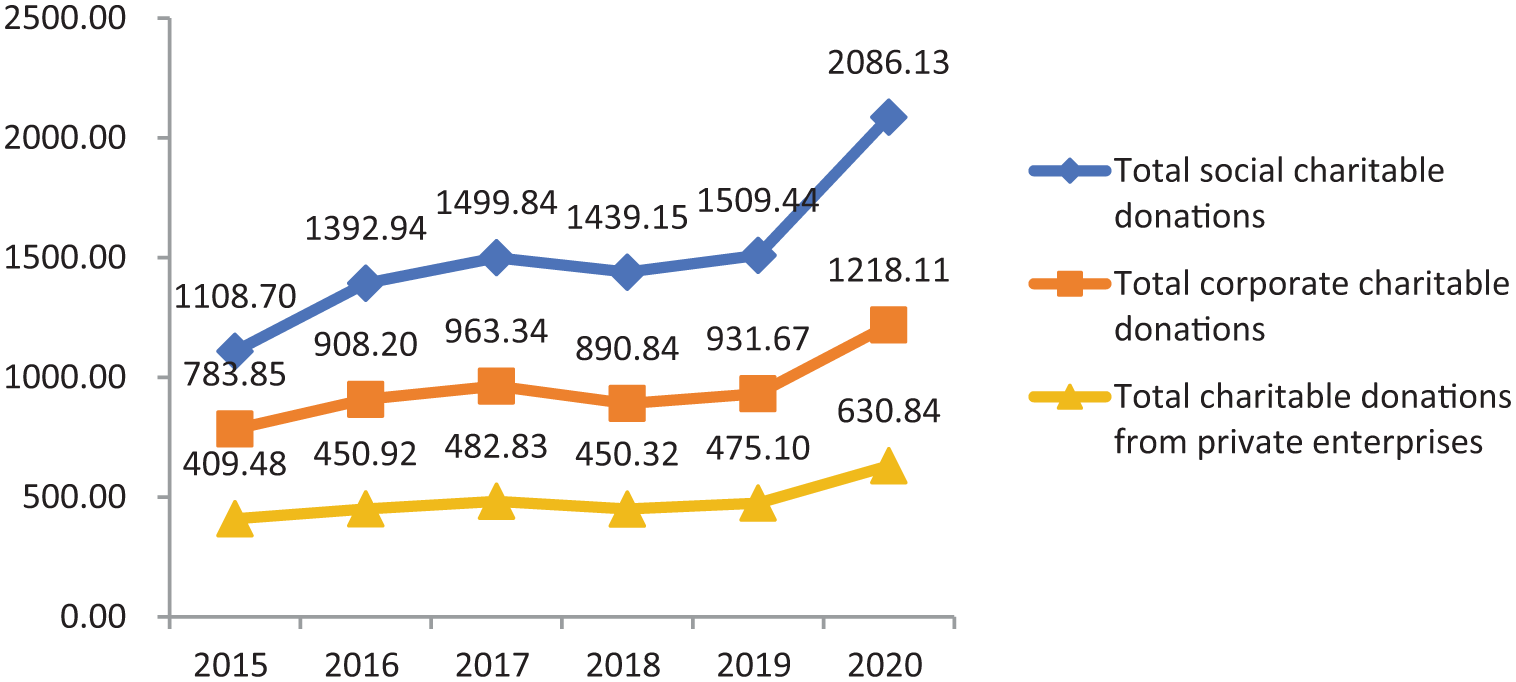

With the further increase in China’s total national economy, China’s charitable donations have started to gradually shift from relying on the government to private donations. According to the 2015 to 2020 China Charitable Donation Report (hereinafter referred to as the report) issued by the China Charity Federation, it is known that private enterprises in China have become the main force of social donations. Specific Chinese charitable donations, corporate charitable donations, and private enterprise charitable donations are shown in Figure 1, with charitable donations data from the China Charity Federation. As one of the important means for enterprises to fulfill their social responsibility, charitable donations can effectively improve their reputation, enhance their competitive advantages (Zhu & Gao, 2022), enhance the competitive advantage of enterprises (Feng & Wang, 2022), etc. It is also effective in solving public crises (Z. L. Li, 2023), health (H. P. Wang et al., 2022), environmental protection (J. H. Han & Yang, 2022), and public welfare education (J. L. Xu & Cheng, 2023) for the public welfare. At the same time, corporate charitable donations have also played a huge role in China’s battle against poverty (C. J. Liu et al., 2021).

2015 to 2020 China charitable donation data change chart.

In the existing literature, corporations make charitable donations mostly for corporate development (X. Y. Wang et al., 2024) and corporate value enhancement (Chu & Tian, 2023). Fewer scholars have explored whether the demographic characteristics of corporate managers affect corporate Charitable Donation. According to the top-echelon theory, the personal characteristics of corporate managers have an impact on corporate governance, investment decisions, and business performance. As for religious beliefs, which is one of the important personal characteristics, although there are current academic studies on the impact of corporate managers’ religious beliefs on corporate Charitable Donation, they are more focused on listed companies, the Du Yingjie’s study shows that religious factors positively affect the donation behavior and donation strength of enterprises (Du & Feng, 2014). Based on this, this paper hopes to explore the impact of private entrepreneurs’ religious beliefs and poverty experiences on corporate charitable donations through empirical research.

The study of private entrepreneurs’ religious beliefs and poverty experiences is based on the following four factors: first, the reason for taking private entrepreneurs as the object of study is as follows, although the object of study of the top-echelon theory is the enterprise managers, in the private enterprises, private entrepreneurs tend to have the dual roles of leaders and managers, so this study helps to enrich the existing literature on one hand, and on the other hand, it also helps to enrich the top-echelon theory. Second, private enterprises are selected as the main body of the study because as of January 2024, private enterprises in China accounted for more than 90% of the total number of enterprises, which is a huge number and has been a force to be reckoned with in the process of China’s economic development. Meanwhile, compared with State Owned Enterprises (SOEs), because the leadership and managers of SOEs are generally appointed by the government and the charitable donations of SOEs may be influenced by political factors to a certain extent, whereas private firms are less influenced by political factors, thus studying private firms in China can be helpful to the government’s policy making. Third, the religious beliefs of private entrepreneurs were chosen for the study because, as one of the important characteristics of private entrepreneurs, on the one hand, based on the top-echelon theory, religious beliefs may have an impact on the charitable donations of private entrepreneurs; on the other hand, based on the imprint theory, religious beliefs may make entrepreneurs make more charitable donations due to the influence of religious doctrines that are kind and charitable. Fourth, the reason for choosing the characteristic of poverty experience is that, based on the imprint theory, the early experience of poverty may make entrepreneurs more active in charitable donations after they can “feed” society. Therefore, by analyzing the religious beliefs and poverty experiences of private entrepreneurs, we explore whether the personal characteristics of entrepreneurs affect their charitable donations, and provide data support for the religious beliefs, early experiences, and charitable donations of private entrepreneurs.

Using the 2018 China Private Enterprise Survey dataset as a research sample, this paper empirically examines the impact of private entrepreneurs’ religious beliefs as well as poverty experiences on the charitable donations made by businesses. Compared with existing studies, the contribution of this paper may be threefold as follows:

First, the introduction of private entrepreneurs’ religious beliefs and poverty experiences into the decision-making behaviors of firms making charitable donations enriches the research related to the top-echelon theory.

Second, the religious beliefs and poverty experiences of private entrepreneurs are linked to corporate charitable donations, and through empirical research, it explores whether the religious beliefs and poverty experiences of private entrepreneurs affect corporate charitable donations, to provide empirical help for the government in guiding and promoting the further charitable donations of private enterprises.

Third, in the existing academic literature, it is found that there is no uniform result of the religious beliefs of corporate managers on the fulfillment of corporate social responsibility, S. R. Zhang (2016) argues that managers’ religiosity has no significant effect on social responsibility; Ni (2016) found that executives’ religious piety positively affects two types of corporate social responsibility behaviors. Therefore, this paper explores the impact of private entrepreneurs’ religious beliefs on corporate charitable donations to provide new evidence that religious beliefs affect corporate fulfillment of social responsibility.

Literature Review

Characteristics of Managers and CSR

Private entrepreneurs have a high degree of autonomy in decision-making in the process of enterprise management, so some of the characteristics of private entrepreneurs themselves (S. R. Zhang, 2016) will likely have an impact on the decisions they make in the process of enterprise management, thus affecting the fulfillment of corporate social responsibility. In the existing research literature, scholars focus more on managers’ characteristics in terms of managers’ education level, gender, academic characteristics, and occupational background. Taking listed companies in China as a sample, Huang Mingdong empirically analyzes and find that the education level of executives significantly enhances the likelihood of corporate social responsibility fulfillment (G. Yang & Huang, 2023). Shi Bowen et al. used empirical research to explore the impact of the educational background of the executive team on the fulfillment of corporate social responsibility and the results of the study showed that the level of education and liberal arts background of the executive team had an incentive effect on the fulfillment of corporate social responsibility, and that the corporate social responsibility score was positively proportional to the proportion of the number of people in the executive team who had the level of education and the liberal arts background (Shi & Xie, 2019). This study is consistent with the American scholar Manner, who found that CEOs with a bachelor’s degree in humanities performed better than CEOs with a bachelor’s degree in economics in fulfilling their social responsibility (Manner, 2010). Meanwhile, based on Xiang Rui’s study, it can be seen that the age, reputation, and education of scholarly sole directors all have a significant positive impact on CSR fulfillment (Xiang, Li & Li, 2020). In addition to the education level, the gender of executives and the political affiliation of the company will also have an impact on the fulfillment of corporate social responsibility. Lv et al. (2021) and Ma (2020) showed that female executives have a significant positive impact on CSR. Meanwhile, based on T. T. Wang (2021) found that the degree of gender diversity on the board of directors is positively related to the fulfillment of CSR, and that gender diversity on the board of directors has a greater positive impact on state-owned enterprises (SOEs) than on non-state-owned enterprises (NSOEs). However, Liang Qiang found that overall female directors do contribute to the fulfillment of CSR to a certain extent, but the result is not always the case. When the gender ratio of the board is relatively balanced, the participation of female directors has a positive effect on the fulfillment of CSR, and vice versa, it has a certain negative effect (Liang et al., 2022). The educational characteristics of corporate managers also have an impact on the fulfillment of corporate social responsibility. Y. K. Zhang et al. (2019) found that executives’ first degree, academic background, and the relationship between the first degree and the highest degree all have an impact on the fulfillment of corporate social responsibility.

In addition to managers’ education level, gender, and academic characteristics that affect the fulfillment of corporate social responsibility, recent studies have found that the political identity of managers also has an impact on the fulfillment of corporate social responsibility. Huang Yongjian found that the chairman of a private enterprise with Communist Party of China (CPC) membership will be more active in fulfilling social responsibility in his enterprise (Y. J. Huang & Liu, 2020). Dou et al. (2022) and G. F. Zhang and Zhang (2021) found that when executives have party membership, they are more actively involved in poverty alleviation, and their efforts to alleviate poverty are greater than those of executives who do not have party membership. H. H. Wang and Guo (2019), F. Han (2017), and W. H. Zhang et al. (2017) found that the political affiliation of executives has a significant contribution to the fulfillment of corporate social responsibility.

As scholars’ research on how the characteristics of executives affect the fulfillment of corporate social responsibility gradually deepens, the special experience of executives has also become a hot research topic in recent years. It is found that the chairman’s “overseas returnee” background is helpful for the fulfillment of CSR, and the overseas background is helpful for the disclosure of CSR information (X. F. Li et al., 2020) and that overseas background helps the disclosure of CSR information (Jiang & Lai, 2019). The study found that the chairman’s “overseas returnee” background is helpful for the fulfillment of CSR, and the overseas background helps the disclosure of CSR information. Meanwhile, executives’ military experience (Nasih et al., 2019), experience of poverty (S. Xu & Ma, 2021), and the experience of natural disasters during their adolescence (He et al., 2021) will have a positive impact on the fulfillment of corporate social responsibility.

Research on Charitable Donation by Enterprises

Charitable Donation is one of the ways for enterprises to fulfill their social responsibility, but the purpose of Charitable Donation by different enterprises is quite different, and scholars at home and abroad have had more results to explore the motivation of enterprises to make charitable donations. Many enterprises treat Charitable Donation as a strategic behavior of enterprise, such as C. M. Yang and Yang’s (2023) study found that tax incentives will have an impact on corporate Charitable Donation: after the proportion of Charitable Donation tax credits rises, the strength of corporate Charitable Donation and the tendency of Charitable Donation both increase significantly; Shao et al. (2022) and B. H. Zhang and Zhang (2022) found that corporate charitable donations have a significant positive impact on brand value through empirical research; Liao et al. (2021) found that corporate charitable donations help to reduce the costs incurred by enterprises in the process of debt financing. Cheng et al. (2020) found through empirical research that enterprises can obtain more government subsidies through charitable donations than enterprises without charitable donations, J. Q. Liu and Yang (2021) and H. P. Wang et al. (2022) et al. have similar conclusions. Similarly, the market environment also has an impact on corporate Charitable Donation, as Zheng (2021) found that the rise of economic policy uncertainty significantly reduces the willingness of enterprises to donate; W. Huang and Wang (2020) showed that the greater the financial pressure on local governments, the greater the probability and amount of charitable donations made by private enterprises in their jurisdictions; Z. W. Lu and Chen (2020) and other scholars empirical analysis found that: the institutional environment will have a certain impact on the enterprise’s charitable donations.

In summary, scholars have found that the characteristics of managers will have a significant impact on the fulfillment of corporate social responsibility. In the study of corporate charitable donations, although scholars at home and abroad have abundantly demonstrated the motivation of corporate charitable donations, they are more centered on the level of corporate development, and there are still fewer studies focusing on the impact of managers’ characteristics on corporate charitable donations. In the existing literature, although there is also an analysis of the impact of corporate managers’ religious beliefs on corporate Charitable Donation and the impact of managers’ poverty experience on corporate social responsibility, there is no literature that simultaneously incorporates both the religious beliefs and poverty experience of corporate managers into the research framework at the same time. Based on this, this paper adopts an empirical approach to explore the role of private entrepreneurs’ characteristics in enterprises’ charitable donations and incorporates private entrepreneurs’ religious beliefs, poverty experiences, and charitable donations into the research framework to analyze the impact of private entrepreneurs’ religious beliefs and poverty experiences on private enterprises’ charitable donations.

Theoretical Analysis and Research Hypothesis

CEO Religious Beliefs and Corporate Charitable Donation

In 1984, Donald and Phyllis innovatively put forward the top-echelon theory, the top-echelon theory believes that the cognitive ability and values of managers will affect the strategic choices of the enterprise, thus affecting the enterprise decision-making, that is, the characteristics of managers will affect the decision-making of the enterprise, and the characteristics of managers (cognitive ability and values, etc.) and the characteristics of the demographic background have a close relationship. The characteristics of business managers include education level, academic characteristics, political identity, gender, etc. Religious beliefs are also one of the significant characteristics of managers. In the existing studies, scholars have found that education level, academic qualifications, and political identity, which are the salient characteristics of managers, have a certain impact on the fulfillment of corporate social responsibility. As one of the ways for enterprises to fulfill their social responsibility, charitable donations are inevitably affected by the characteristics of managers.

The motives for charitable donations may vary greatly from enterprise to enterprise, but the promotion of love and charity contained in charitable donations is worth recognizing, and the promotion of love and charity is consistent with the teachings of religions such as Buddhism, Taoism, Islam, Christianity, and so on. Due to the inclusiveness of Chinese civilization, which is characterized by acceptance and seeking common ground while reserving differences, these religious teachings will have an important impact on thoughts, perceptions, and values due to the existence of the stigma theory (Iannaccone, 1998). The imprint theory is the reason why these religious teachings will have a significant impact on thoughts, perceptions, and values. Therefore, for enterprises, managers with religious beliefs, under the influence of the “brand” of “religious teachings,” will have a higher possibility to take more social responsibilities when making decisions under the influence of the teachings. In addition to pursuing legitimate profitability, the enterprise will also take into account the interests of the social environment, including environmental protection, internal employees and investors, external upstream and downstream enterprises, the government, and customers.

First of all, influenced by the religious doctrine of charity, religious beliefs will have an important impact on the values of managers, on the one hand, this value will prompt them to pay more attention to social information about charitable donations; on the other hand, by the influence of the values will also push them to be more active in charitable donations. Second, as a corporate manager, the corporate culture of the enterprise will be influenced by the personal characteristics of the corporate manager to a certain extent, and influenced by religious beliefs, the enterprise will be more active in fulfilling its social responsibility within the enterprise because of this characteristic of the manager’s religious beliefs. At the same time, because altruism and religion have a complementary relationship, such as “benevolence,”“compassion,”“love,” etc., managers with religious beliefs will have a higher level of altruism. Therefore, enterprise managers with religious beliefs will have a higher level of altruism, which will be more conducive to the promotion of the fulfillment of corporate social responsibility by the enterprise managers and will also be helpful to the decision of the enterprise to make charitable donations. Finally, since this paper takes private enterprises as the research object, private entrepreneurs have a higher voice in enterprise management, so the personal characteristics of managers will also have a more significant impact on enterprise charitable donations.

Therefore, to summarize, based on the top-echelon theory, this paper argues that business executives with the trait of religious affiliation will be more likely to make charitable donations. Therefore, the following hypotheses are proposed:

Managers’ Experience of Poverty and Corporate Charitable Donation

Enterprise managers are the social image of the company, and they are the makers and distributors of important decisions. Based on the stigma theory, it can be seen that the values of managers are influenced by the environment they grow up in and the experiences they have later on in life, which in turn affects their behavior and decision-making (Batson et al., 1991). Batson found that managers’ early experiences shape their sense of value and have an impact on the fulfillment of corporate social responsibility. Tan and Li (2023) based on the empirical research to explore the impact of the chairman’s early poverty experience on corporate poverty alleviation, the empirical results show that the chairman’s early poverty experience has a significant positive impact on corporate poverty alleviation.

In existing studies, scholars have found that the poverty experience of executives has a significant impact on the shaping of executives’ outlook. Because the growth environment is in the poor area, the poverty experience will become part of the individual’s outlook in the process of personal growth, and then gradually affect the individual’s behavioral pattern and value orientation. Existing research has shown that the values of corporate managers will have a certain impact on the fulfillment of corporate social responsibility (Zhao et al., 2015). The existing studies have shown that the values of corporate managers have a certain impact on the fulfillment of social responsibility by enterprises.

Therefore, in summary, it is believed that managers with experience of poverty are more likely to show understanding and empathy when faced with disadvantaged groups who suffer from poverty, natural disasters, illness, and other causes of poverty. Therefore, managers with experience of poverty are more likely to make charitable donations and to do so more vigorously.

Therefore, the following hypotheses are proposed:

Based on the above theoretical analysis, this paper proposes a theoretical mechanism as shown in Figure 2.

Theoretical mechanisms.

Empirical Research Design

Data Sources

This article uses the 2018 survey dataset of private enterprises in China as the research sample, which is derived from the 13th National Sample Survey of Private Enterprises carried out by the Private Enterprise Research Group in 2018. The project was completed under the auspices of the Private Enterprise Research Group. As the survey not only covers 31 provincial-level administrative regions but also requires enterprises’ industries and scales, the data of the survey is highly representative. At the same time, the survey data set includes not only information about enterprises but also certain personal information of Private entrepreneurs, such as gender, year of birth, education level, political status, experience, fulfillment of social responsibility, religious beliefs, etc. There are a total of 5,037 data in 2018, and a total of 3,628 samples were screened to obtain complete data. Meanwhile, to avoid the influence of abnormal values on the results, continuous variables were Winsorized in this study.

Definition of Variables

Explained Variables

This paper focuses on the impact of Private entrepreneurs’ religious beliefs and poverty experience on private enterprise charitable donations, so the explanatory variable in this paper is enterprise charitable donations. This paper measures the situation of enterprises’ charitable donations by setting two variables, the first is whether charitable donations are made; according to 2018 China’s private enterprise survey data centralized disclosure of the relevant situation, if the enterprise has made charitable donations in the year of the survey, it is assigned a value of 1; conversely, it is assigned a value of 0. The second is the strength of the enterprise’s charitable donations; the strength of the enterprise’s charitable donations is the total amount of charitable donations plus 1 and then the natural logarithm.

Explanatory Variables

Religious beliefs of private entrepreneurs: the motivation of enterprises to make charitable donations was selected in the questionnaire form of the thirteenth national survey of private enterprises in 2018, and since the vast majority of religions currently have the teachings of urging people to be good and assume certain social responsibilities, no distinction is made between religious denominations in this study, and if a private entrepreneur selects religion in the selection of motivations for donating behaviors, it is assumed that the Private entrepreneur has a religious belief, the value is assigned to 1; vice versa, the value is assigned to 0.

Poverty experience of private entrepreneurs: we can obtain the poverty experience of entrepreneurs more accurately through interviews, questionnaires, etc., but due to the difficulty of obtaining data, this paper draws on the definitions of domestic scholars of poverty experience to measure the poverty experience of private entrepreneurs according to the context of China’s economic development at that time: if the entrepreneur’s birth year is within the range of 1945 to 1953 (Zeng & Mao, 2018) or born in a national-level poverty-stricken county (Dou et al., 2022), then the private entrepreneurs is considered to have a poverty experience, and is assigned a value of 1; otherwise, the value is 0.

Control Variables

To reduce the impact of other variables on the empirical test, this paper controls for the following variables, drawing on existing research:

(1) Gender of managers. Some scholars have argued that gender is also an important factor that can influence managers to make charitable donations (L. Y. Wang, 2023). The manager’s gender is also considered to be an important factor in influencing managers’ Charitable Donations. Therefore, this paper controls for the manager’s gender, which takes the value of 1 if the private entrepreneurs’ gender is male, otherwise it is 0. (2) Age. Private entrepreneurs of different ages may have different approaches to Charitable Donation. (3) Political identity. In general, private entrepreneurs who may have political identity will be more inclined to make charitable donations (Gao et al., 2011). (4) Party membership (Y. J. Huang & Liu, 2020). In the existing literature, it is found that business executives with party membership can fulfill their social responsibilities more actively. (5) Corporate Gearing. In the existing research, the results of the study on the impact of the gearing ratio on enterprises to make charitable donations have not been unified. However, in general, enterprises with low gearing ratios have a relatively high likelihood of making charitable donations. (6) Corporate profitability. The reason for selecting this variable is the same as that of corporate gearing ratio. (7) Enterprise size. Generally speaking, the larger the scale of enterprise operation, the more it will consider the interests of society, the environment and the public. Therefore, the total assets of the enterprise business are introduced as an indicator of enterprise size. (8) Enterprise industry. Private entrepreneurs in different industries may have different approaches to Charitable Donations. (9) Annual salary of entrepreneurs (C. Lu et al., 2023). Lu’s empirical study found a significant association between managers’ compensation and Charitable Donation by enterprises.

The main variables are detailed in Table 1.

Definition of Variables.

Modeling

In order to examine the impact of religious beliefs or poverty experiences on private entrepreneurs’ Charitable Donation, this paper empirically tests the Probit model:

To examine the impact of religious beliefs or poverty experiences on the strength of private entrepreneurs’ Charitable Donation, this paper uses the Tobit model for empirical testing:

Analysis of Empirical Results

Descriptive Statistical Analysis of Variables

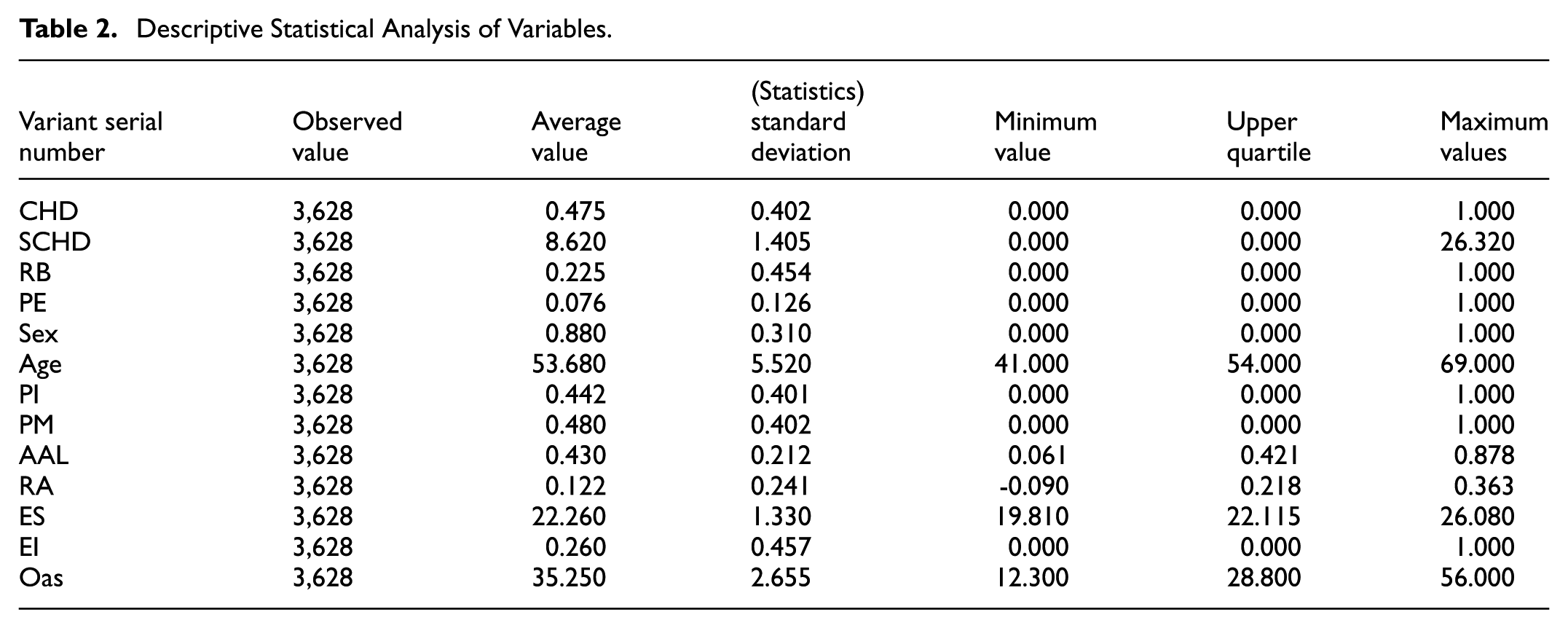

The results in Table 2 show the mean, standard deviation, maximum, minimum, and median of the main variables. It can be seen in the 3,628 observations that 47.5% of the study sample made charitable donations during the survey period; 22.5% of the private entrepreneur in the sample companies participating in the survey had religious beliefs, and the average age of the private entrepreneurs were at 53.68 years old. The data show that 44.2% of private entrepreneurs are or have been serving in the National People’s Congress, the Chinese People’s Political Consultative Conference, or relevant government departments, and 48% of private entrepreneurs are members of the CPC, indicating that it is more common for private entrepreneur to have a political identity or to be a party member; however, out of the 3,628 valid samples, the share of private entrepreneur with experience of poverty is 7.6% today.

Descriptive Statistical Analysis of Variables.

To test the enthusiasm of private entrepreneurs with religious beliefs and private entrepreneur without religious beliefs in the enterprise to make charitable donations and the strength of charitable donations, this paper divides the sample enterprises into groups with religious beliefs and without religious beliefs, and carries out the t-test of the mean and the median test on whether the enterprises make charitable donations and the strength of the enterprises to make charitable donations, which is shown in Table 3. The results of the test show that private entrepreneur with religious beliefs. Both enthusiasm of enterprises for charitable donations and the strength of charitable donations are significantly higher than those without religious beliefs, indicating that religious beliefs to a certain extent will make the enterprise owners have more enthusiasm to invest in charitable donations and the strength of charitable donations is also higher, which preliminarily supports the hypothesis H1a.

Mean Differences and Median Differences in Corporate Charitable Donation.

Note. *p < 0.1, **p < 0.05, ***p < 0.01.

Analysis of Regression Results

The Impact of Religious Beliefs and Corporate Charitable Donation

According to the regression results in Table 4, it can be seen that the regression coefficients of both the Charitable Donation situation as the dependent variable and the strength of corporate charitable donations are significantly positive and significant at the 1% confidence interval, which indicates that private entrepreneurs with religious beliefs will be more active in charitable donations and the strength of charitable donations will be higher compared with those without religious beliefs, and the hypothesis H1a of this paper can be supported, that is, religious beliefs of the private entrepreneurs will be more active in charitable donations and the strength of charitable donations is higher. In terms of control variables, age, political identity, enterprise size, and annual salary of private entrepreneurs are positively correlated with charitable donations by enterprises.

Regression Results on the Relationship Between Religious Beliefs of Private Entrepreneurs and Corporate Charitable Donation.

Note. *p < 0.1, **p < 0.05, ***p < 0.01.

Private Entrepreneurs’ Experience of Poverty and Corporate Charitable Donation

Table 5 shows the regression results related to the relationship between private entrepreneurs’ poverty experience and Charitable Donation, and the regression coefficients of the two sets of dependent variables are both significantly positive and significant at the 1% confidence interval, which suggests that private entrepreneurs with poverty experience have a greater likelihood of making charitable donations and the amount of charitable donations invested will be significantly higher than that of private entrepreneurs who do not have poverty experience. Therefore, the regression results in Table 5 support the hypothesis H2a of this paper, that is, private entrepreneurs with poverty experience, the enterprise is more likely to make charitable donations, and charitable donations are more powerful.

Private Entrepreneurs’ Experience of Poverty and Charitable Donation.

Note. *p < 0.1, **p < 0.05, ***p < 0.01.

In terms of control variables, the gender of private entrepreneurs, age, political identity, party membership, return on assets, business size, and annual salary of private entrepreneurs have a significant effect on enterprises making charitable donations and the strength of enterprises making charitable donations. Unlike the effect of religious beliefs on enterprises’ charitable donations, for private entrepreneurs with poverty experience, the gender of the private entrepreneurs affects whether the enterprise makes charitable donations or not. For businesses, return on assets significantly affects the decision to make charitable donations.

Robustness Test

To test the stability of the above regression results, this paper draws on the work of Gao et al. (2011) and W. L. Wang et al. (2015), to re-select the sample of enterprises, and selects the enterprises in the sample in which the private entrepreneur has more than 50% of the equity, to avoid that the private entrepreneur is unable to independently make decisions on charitable donations due to the lack of management rights. The new sample of enterprises totaled 2,132, of which 1,088 enterprises had made charitable donations at the time of the questionnaire survey. Using the data from the new sample, regression analyses were conducted to analyze the charitable donations made by enterprises as well as the strength of charitable donations made by enterprises.

The results of the robustness test show that in the new sample, both corporate Charitable Donation and the strength of Charitable Donation are significant, in which the religious beliefs of private entrepreneur have a positive correlation with corporate Charitable Donation and the amount of Charitable Donation, and the results of the rest of the variables are also consistent with the results of the previous study (Table 6).

Robustness Test Results.

Note. *p < 0.1, **p < 0.05, ***p < 0.01.

Conclusion and Discussion

Using the 2018 China Private Enterprise Survey dataset as a research sample, this paper selects the religious beliefs and poverty experiences of private entrepreneur to analyze the impact of the above two factors on the charitable donations of private enterprises. The study finds that private entrepreneur with religious beliefs may be more active in Charitable Donation and have greater Charitable Donation. Second, this paper explores the impact of entrepreneurs’ poverty experience on corporate charitable donations and charitable donations, and finds that entrepreneurs with poverty experience are more willing to participate in charitable donations and make larger charitable donations than entrepreneurs without poverty experience. The above conclusions are still significant after the robustness test.

The white paper “China’s Policy and Practice of Guaranteeing Freedom of Religious Belief,” publicly released by the State Council Information Office in 2018, mentions that at present, there are nearly 200 million Chinese residents who believe in all kinds of religions, and the number of believers is growing at a relatively fast rate, and the influence of religion on the society should not be ignored, so it is inappropriate for the research field of corporate governance or social development to neglect the influence of religion on the enterprise. This paper analyzes the influence of private entrepreneurs’ religious beliefs and poverty experiences on enterprises’ charitable donations, examines the causal relationship between religious beliefs, poverty experiences, and charitable donations, and provides a supplement to the top-echelon theory, which has certain theoretical significance. At the same time, by analyzing the motivation of corporate charitable donations, it helps the government to guide and promote corporate charitable donations, which is beneficial to the “threefold distribution” advocated by China, and promotes the development of the society, which is of practical significance.

Based on the findings of the study, the following two policy recommendations are made:

First, relevant government departments, such as the Ministry of Civil Affairs and the Ethnic and Religious Affairs Commission, should correctly recognize the positive influence of religious beliefs in the charitable donations made by entrepreneurs, actively guide entrepreneurs with religious beliefs to make charitable donations, and give full play to the initiative of government departments.

Second, the Ministry of Civil Affairs and the Ethnic and Religious Affairs Commission should recognize that religious beliefs can promote charitable donations by private entrepreneur, and similarly religious beliefs may, to a certain extent, also be able to promote charitable donations by individuals, so that through charitable donations made by residents and businesses together, a good social climate can be formed and a more harmonious development of society can be promoted, thereby realizing the common prosperity of China.

Analysis of Limitations

Although there are some innovations in this study, there are still limitations. First, due to the difficulty in obtaining data on the variable of religious belief, this study uses data related to the 2018 China Private Enterprise Survey dataset, which has poor data currency, so in future research, questionnaire survey method and interview method may be used to obtain first-hand data, so as to improve the conclusions of the existing study. Second, this study did not differentiate between the religious beliefs of private entrepreneurs, but simply differentiated private entrepreneur by the presence or absence of religious beliefs, and did not explore in depth the impact of different religions on the charitable donations made by private entrepreneurs. In the next step of the study, the religious beliefs of private entrepreneur will be carefully divided, and the impact of different religious beliefs on corporate Charitable Donation will be analyzed in a targeted manner. Finally, limited to the actual situation, the poverty experience of private entrepreneur can only be defined simply by age and place of birth or growth, without more in-depth analysis, which also concludes the study flawed, and in the future research, the questionnaire will be used in the hope that through the questionnaire survey, more detailed data can be obtained, so as to improve the conclusion of the study.

This study used the 2018 Private Enterprise Survey dataset to investigate the impact of business owners’ religious beliefs and poverty experiences on corporate charitable donations. Due to data availability, this study can only use 2018 for the time being, but it still supplements the theories of high-level echelons and branding. The reason is as follows: Starting from the branding theory, the branding theory believes that the effect of branding is irreversible, and the branding theory believes that once the human branding phenomenon is formed, it is difficult to change it. Therefore, although this study used data from 2018, based on the branding theory, the impact of past experiences on private business owners is long-lasting. Secondly, based on the reality, we can see that the impact of stigma on residents is lifelong. For example, the impact of major public health events (COVID-19) on adolescents may appear in the next 10 years. These adolescents who have received help from the government, enterprises, or ordinary residents in major public health events (COVID-19) may also show goodwill and help others in some future events.

Footnotes

Acknowledgements

Useful suggestions given by Dr QI are also acknowledged.

Author’s Note

XiFeng Yang

Research Areas: Corporate Governance, Regional Economic Studies, Agricultural Economic Development

MeiHui Qi

Research Areas: Enterprise Valuation, Agricultural Economics

Ethical Considerations

Not applicable

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The authors will supply the relevant data in response to reasonable requests