Abstract

This study investigates the impact of uncertainties on the non-performing loans/ finance (NPL/NPF) of conventional and Islamic banks in the MENA region using data from 2005 to 2022. Based on inclusion and exclusion criteria and the purposive sampling technique, 92 banks were selected from 13 MENA countries, 42 of which are Islamic and 50 of which are conventional banks. The study used two estimation methods: Augmented Mean Group (AMG) and two-step Generalized Method of Moments (GMM) to estimate the relationship between uncertainty and NPL/NPF. These estimation methods were chosen for their ability to provide unbiased results in the presence of cross-sectional dependence and deal with endogeneity. The study revealed that world pandemic uncertainty had a negative and significant influence on the NPL of conventional banks while showing a positive and significant influence on the NPF of Islamic banks. US trade policy uncertainty was found to have a negative and significant influence on the NPL of conventional banks. In contrast, it exhibited a positive and significant influence on the NPF of Islamic banks. We discovered a positive and significant influence of US sovereign debt risk uncertainty on the NPL/NPF of conventional and Islamic banks in the MENA region. The findings revealed a negative and significant influence of oil price uncertainty on the NPL/NPF of conventional and Islamic banks in the MENA regions. These findings reassure us that bank in the MENA region should adopt and tailor risk strategies based on sector-specific responses, engage in proactive risk monitoring, and maintain loan quality amid economic uncertainties.

Plain language summary

This study investigates the impact of uncertainties on non-performing loans (NPLs) in conventional and Islamic banks across the MENA region using data from 2005 to 2022. Through a purposive sampling technique, 92 banks were selected from 13 MENA countries, of which 42 are Islamic and 50 are conventional banks. Two estimation methods, Augmented Mean Group (AMG) and two-step Generalized Method of Moments (GMM), were used to estimate the relationship between uncertainty and NPLs. These methods were chosen for their ability to handle panel data and their robustness in estimating dynamic models. The study revealed that world pandemic uncertainty had a negative and significant influence on the NPLs of conventional banks while showing a positive and significant influence on the NPLs of Islamic banks. US trade policy uncertainty was found to have a negative and significant influence on the NPLs of conventional banks. In contrast, it exhibited a positive and significant influence on the NPLs of Islamic banks. We discovered a positive and significant influence of US sovereign debt risk uncertainty on the NPLs of conventional and Islamic banks in the MENA region. The findings revealed a negative and significant influence of oil price uncertainty on the NPLs of conventional and Islamic banks in the MENA regions. These findings reassure that bank in the MENA region can adapt, tailor risk strategies based on sector-specific responses, engage in proactive risk monitoring, and maintain loan quality amid economic uncertainties.

Introduction

Financial institutions are pivotal in promoting economic development and stability in the Middle East and North Africa (MENA) region ( Neaime & Gaysset, 2018). They effectively use savings to assist businesses and individuals in driving economic growth. They expertly manage risk to preserve deposits and system integrity, reassuring stakeholders. To generate a lively atmosphere, they optimize processes, enhance client satisfaction, and launch new financial products using their financial operations knowledge (Fasnacht & Fasnacht, 2018). They promote economic variety and regional cooperation, easing trade and investment. Due to their importance, financial institutions in MENA provide safe savings accounts and personal and commercial loans to individuals and corporations. This enables corporations to receive loans for their business activities, contributing to their growth. These financial institutions promote regional stability, job creation, and economic growth by providing public sector finance and treasury services for infrastructure and economic development. Individuals, organizations, and governments benefit enormously from the banks’ contributions. They also help governments fund vital infrastructure and public services, improving society (Fisch et al., 2019).

Despite their valuable contributions, banks in the MENA region grapple with significant non-performing loans/finance (NPL/NPF; Jarbou et al., 2024; Khalaf & Awad, 2024). These issues affect the bank’s profitability by reducing interest income and increasing operational costs by setting aside some of their earnings to address them. However, they also hinder a bank’s growth by limiting lending capacity and damaging its corporate image due to perceived risk management issues. These result in regulatory scrutiny and concerns about capital adequacy, which can impact financial stability and investor confidence in the banking sector (Alaoui Mdaghri, 2022; Alnabulsi et al., 2023; Mohamad & Jenkins, 2021). Dealing with NPL/NPF is crucial for banks to ensure long-term profitability, foster economic growth, and uphold a positive regional reputation (Alshebmi et al., 2020).

Addressing the causes of NPL/NPF involves a proactive approach from banks and governments. It requires looking at internal factors within banks, such as credit standards, risk management, and loan diversification. These issues can be effectively tackled by implementing diligent care and improved risk assessment procedures (Mwithi, 2012; Tarchouna et al., 2021). Factors related to the country, such as economic instability and weak legal frameworks, can affect borrowers’ ability to repay and may necessitate government intervention by implementing effective economic policies and strengthening legal frameworks (Tshuma, 2018). External factors, such as global economic conditions and natural disasters, are beyond the control of banks and governments. However, banks should implement risk management strategies to minimize the impact of these factors on loan performance (Bessis, 2011; Klomp, 2014). Understanding and managing these factors are essential for banks and policymakers to effectively handle NPL risks and maintain the financial system’s stability (Naili & Lahrichi, 2022).

Numerous studies have delved into the impact of global economic policy uncertainties on NPL/NPF (Botshekan et al., 2021; Deng & Li, 2024). Global economic policy encompasses a variety of factors and uncertainties that can influence economic conditions and financial markets worldwide (Sharif et al., 2020). Its components include economic policy uncertainty, oil price volatility, sovereign debt risks, geopolitical risk, world pandemic uncertainty, and US trade policy uncertainty.

Examining the impact of global policy uncertainties on NPL/NPF without considering the specific impact of its components on NPL/NPF does not provide clear insights into the overall scope of global policy uncertainties. This is because global policy uncertainty components have unique and diverse impacts on banks’ financial stability and operational conditions. While the effect of economic policy uncertainties on NPL/NPF has been investigated by Karadima and Louri (2021), Ozili (2022), and Hamdi and Hassen (2022), these studies were not carried out in the MENA region, making it difficult to understand how macroeconomic factors globally affect banks in MENA. The other global policy uncertainties remain underexplored in the literature, with a specific focus on the MENA region, which highlights the need for research to fill these significant knowledge gaps. Also, how the other components impact NPL/NPF on conventional and Islamic banks has not been explored.

The world pandemic uncertainty affects industries that play a vital role in the region’s economic growth, including trade, tourism, and energy demand, which impede development and deter foreign investment (Pianta, 2021). The U.S. trade policy uncertainty significantly impacts the MENA region’s commerce, particularly crude exports, which causes economic instability and revenue fluctuations (Hnainia & Mensi, 2024). The sovereign debt uncertainty, a global credit condition, limits the funding availability for MENA regions and escalates borrowing costs (Gatti et al., 2021). The oil price uncertainty is particularly pronounced due to the immediate effects of price variations on government revenues and economic stability, given that oil is a major export. Geopolitical risks are significant because they frequently cause economic disruptions and affect energy security, investor confidence, and trade (Bouoiyour et al., 2019). These factors shape the MENA regions’ economic condition, resulting in an environment of unpredictability.

To address these gaps, this study investigates the influence of oil price uncertainty, sovereign debt risk, geopolitical risk, world pandemic uncertainty, and US trade policy uncertainty on NPL/NPF in conventional and Islamic banks across the MENA region. The study seeks to answer the question: Do oil price uncertainty, sovereign debt risk, geopolitical risk index, world pandemic uncertainty index, and US trade policy uncertainty influence NPL/NPF in conventional and Islamic banks across the MENA region? The answers will provide valuable insights into the factors influencing NPL/NPF in the MENA region, contributing to a deeper understanding of banks’ financial stability and operational conditions.

This study contributes to the existing body of knowledge by examining the influence of oil price uncertainty on the NPL/NPF of both conventional and Islamic banks in the MENA region. The research underscores the crucial impact of oil price volatility on the financial stability of banks, particularly in oil-dependent MENA nations. It delves into how fluctuations in this vital economic variable affect the banks’ well-being. This contribution aids in understanding the contrasting effects on conventional and Islamic banks, considering their unique operational principles and risk management techniques.

Our study investigates how sovereign debt risk affects the NPL/NPF of both conventional and Islamic banks in the MENA region, thereby adding to the existing body of literature. This contribution elucidates the practical implications of sovereign debt risk on bank loan performance, specifically focusing on how it influences countries’ creditworthiness and fiscal stability. Understanding the economic interdependencies within the MENA region can provide valuable insights for assessing risks and creating policies for both conventional and Islamic banks. These banks may have varying levels of exposure and responses to the risk of government debt, and this study will equip them with the needed knowledge to make informed decisions.

This study contributes to the existing body of knowledge by examining the influence of geopolitical risk on the NPL/NPF of both conventional and Islamic banks in the MENA region. Geopolitical risks, such as political instability, conflicts, and diplomatic tensions, can affect economic stability and financial systems. These contributions shed light on the unique capabilities of different banking regimes to withstand and recover from external political shocks, providing a fresh perspective on risk management in the banking sector.

This study adds to the existing body of literature by investigating the impact of global pandemic uncertainty on the NPL/NPF of both conventional and Islamic banks in the MENA region. The COVID-19 pandemic has highlighted the significance of comprehending the financial ramifications of worldwide health problems. This contribution considers the distinct features of conventional and Islamic banks, which may have varying levels of risk exposure and ways of managing risks in unusual circumstances.

This study contributes to the existing literature by examining how US trade policy uncertainty affects the NPL/NPF of conventional and Islamic banks in the MENA region. The trade policies of the United States can have significant and far-reaching impacts on global markets, particularly those in the MENA region. This contribution emphasizes the consequences of international trade dynamics on local banking sectors by examining trade policy uncertainty. This contribution is essential as it assists in identifying the precise vulnerabilities and adaptive capabilities of both conventional and Islamic banks regarding global trade fluctuations and policy changes.

This study is vital for banks to devise focused strategies and implement risk mitigation measures. By analyzing these factors in light of evolving global economic conditions, banks can make well-informed decisions regarding loan portfolios, capital allocation, and risk assessment. This study connects theory to practice by offering banks practical insights to effectively navigate challenges and enhance their performance in the ever-changing MENA banking sector.

Literature Review

Theoretical Perspective

Using the theory of financial distress can provide practical insights into how uncertainty impacts NPL/NPF in the MENA region. According to the theory, economic uncertainty, including factors like oil price fluctuations, geopolitical risk, and US trade policy, can directly impact businesses and individuals in the MENA region (Selmi et al., 2020). When experiencing higher uncertainty, businesses may encounter difficulties maintaining consistent revenue streams or obtaining necessary financing (Basu & Bundick, 2017). In periods of oil price volatility, companies in oil-dependent economies may struggle to maintain profitability and meet their debt obligations.

Businesses grapple with increasing loan defaults, directly impacting banks and lenders operating in the region. These loans become non-performing when borrowers cannot repay or fulfill their financial obligations due to economic difficulties (Naili & Lahrichi, 2022). Financial institutions in the MENA region diligently track economic indicators and geopolitical risk to evaluate the credit risk associated with their loan portfolios (Almualla & Al-Gasaymeh, 2023). Financial institutions have the authority to change lending practices, credit standards, and loan structures to minimize the effects of uncertainty on NPL/NPF (Anastasiou, 2023).

The theory highlights the significance of banks’ proactive risk management. These involve performing comprehensive credit assessments, analyzing loan portfolios under various economic conditions, and working closely with borrowers to identify solutions during challenging economic periods (Aymanns et al., 2018). By implementing these practical strategies, banks demonstrate their preparedness to mitigate the negative impact of uncertainty on NPL/NPF and uphold financial stability in the MENA banking sector (Alaoui Mdaghri, 2022).

Asymmetric information theory suggests that disparities in the information accessible to borrowers and lenders can affect NPL/NPF (Rundo & Di Stallo, 2019). According to this theory, borrowers possess superior knowledge regarding their capacity to repay loans compared to lenders, resulting in issues of adverse selection and moral hazard. Within NPL/NPF, lenders cannot precisely evaluate the likelihood of borrowers defaulting, leading to increased NPL/NPF.

The market discipline theory emphasizes the influence of market forces in governing bank conduct. This theory posits that the market enforces discipline on banks using processes such as depositors’ responses and the bank’s stock price performance (Min, 2014). By comprehending and using these market dynamics, the banking industry can successfully mitigate banks’ hazardous conduct, potentially diminishing NPL/NPF and fostering trust in the industry’s self-regulation and resilience.

Hypotheses Development

The Influence of World Pandemic Uncertainty on NPL/NPF

World pandemic uncertainty impacts the level of NPL/NPF within the MENA region. This quantifies uncertainty regarding the global economic repercussions of pandemics such as the COVID-19 pandemic. During periods of heightened pandemic uncertainty, several critical factors come into play that directly affect the performance of loans and credit portfolios (Dunz et al., 2023).

Pandemic-induced disruptions can lead to an economic slump characterized by reduced economic activity, business closures, and interruptions in the supply chain (Moosavi et al., 2022). These disruptions can decrease income and liquidity for organizations and individuals across various industries. When borrowers encounter financial difficulties due to these conditions, they may struggle to fulfill their debt obligations, leading to increased loan defaults and a higher NPL/NPF for banks and financial institutions (Zaki et al., 2011).

The uncertainty surrounding the duration and severity of the pandemic causes market fluctuations and investor anxiety. These uncertainties can significantly influence investor confidence, potentially impacting asset prices and market stability (Khan, 2022). This volatility exacerbates challenges for borrowers and lenders, affecting loan performance and credit quality (Palmer, 2015).

The world pandemic uncertainty serves as an indicator of economic uncertainty and risk. This uncertainty is subject to change based on evolving pandemic conditions and corresponding government responses, potentially signaling future challenges for borrowers, lenders, and financial institutions (Feyen et al., 2021). During heightened uncertainty, banks may adopt a more cautious approach to lending, resulting in reduced credit access and stricter loan conditions. The world pandemic uncertainty impacts NPL/NPF by reflecting economic disruptions, market instability, and investor sentiment associated with global pandemics (Matkovskyy, 2014). This underscores the interplay between economic conditions and loan performance, highlighting financial institutions’ challenges in effectively managing lending risk during uncertain times.

Olorogun (2020) investigated the impact of the COVID-19 pandemic on NPL/NPF in Turkey’s agricultural sector and its repercussions on the banking system. The study utilized the Diebold and Yilmaz index to assess interconnectedness using monthly data from December 2004 to April 2020. Johansen and Juselius’s cointegration analysis was employed to identify long-term effects. The results indicated a significant correlation between variables, with COVID-19 spillover effects impacting the agricultural sector, subsequently affecting the return on equity (ROE) across different sectors. The Johansen cointegration analysis revealed persistent transmission of the pandemic’s effects across other sectors, highlighting the profound and far-reaching impacts on the Turkish economy.

Fakhrunnas et al. (2022) examined the asymmetrical relationship between macroeconomic factors and NPL/NPF in Indonesia before and during the COVID-19 outbreak. They employed a nonlinear autoregressive distributed lag (NARDL) model for their analysis. They discovered evidence of asymmetric impacts, with stronger correlations observed among Islamic banks before the epidemic, which subsequently shifted during the pandemic period.

H1: World Pandemic Uncertainty positively and significantly influences NPL/NPF in the MENA region.

The Influence of US Trade Policy Uncertainty on NPL/NPF

The US trade policy uncertainty directly influences global commerce dynamics, especially for countries in the MENA area with substantial economic connections to the United States (Kowalski et al., 2015). Trade policy uncertainties, such as tariffs, trade agreements, or trade restrictions implemented by the US government, disrupt international trade flow and supply chains (Handley & Limão, 2015). This uncertainty results in economic volatility and impacts the well-being of enterprises operating in the MENA area. Trade policy uncertainty poses issues for businesses in estimating demand, managing manufacturing costs, and obtaining crucial supplies (Souza, 2014). These firms may face difficulties fulfilling their financial responsibilities, such as repaying loans, leading to a rise in NPL/NPF.

The impact of US trade policy uncertainty extends beyond direct trade disruptions. It also influences investor sentiment and market volatility, resulting in stock market volatility, currency exchange rate fluctuations, and commodity price fluctuations (Broda & Romalis, 2011). These fluctuations influence firms’ profitability and cash flows, affecting their ability to repay obligations and potentially resulting in higher default rates and NPL/NPF. US trade policy uncertainty also impacts macroeconomic conditions in the MENA area, leading to economic slowdowns, decreased investment inflows, and a higher cost of capital, worsening financial strain for enterprises and individuals. Consequently, this can result in elevated levels of NPL/NPF for banks and financial institutions in the region.

To reduce the impact of US trade policy uncertainty on NPL/NPF, policymakers and financial institutions must adopt risk management measures. This includes closely monitoring trade developments and preparing for potential causes (Stark et al., 2014). By reducing the effect of trade policy uncertainty for NPL/NPF in the MENA area, we can promote economic diversification, strengthen regional trade agreements, and develop stable diplomatic ties (Chau & Oanh, 2023).

H2: US trade policy uncertainty positively and significantly influences NPL/NPF in the MENA region

The Influence of US Sovereign Debt Risk Uncertainty on NPL/NPF

The US sovereign debt uncertainty influences global financial markets and investor sentiment, particularly in countries exposed to US debt or financial instruments (Bhattarai et al., 2020). This uncertainty increases instability in bond markets and stock exchanges, affecting the valuation of financial assets held by institutions and impacting financial well-being. During heightened uncertainty, investors typically exhibit greater risk aversion, leading to capital flight from emerging economies, especially those in the MENA region (Shah & Albaity, 2022).

Fluctuations in US sovereign debt uncertainty affect interest rates globally. According to McCauley et al. (2015), the increased risk associated with US sovereign debt prompts investors to seek higher returns on US Treasury securities, resulting in adjustments to global interest rates. These rate changes affect the interest rates that firms and individuals in the MENA region must pay when borrowing money, potentially making it more challenging for borrowers to meet their obligations and increasing NPL/NPF (Gatti et al., 2021). US sovereign debt uncertainty directly influences exchange rates, impacting import costs, export competitiveness, and economic stability. Currency rate fluctuations pose risks to firms, affecting their profitability and ability to repay loans (Chui et al., 2016).

The influence of US sovereign debt uncertainty on economic sentiment and investor confidence cannot be overstated. Increases in perceived sovereign debt uncertainty have reduced firm investment, decreased consumer spending, and caused an economic slowdown. This profoundly impacts businesses and individuals’ financial well-being, potentially increasing loan defaults and NPL/NPF (Bocola, 2016).

Boumparis et al. (2019) examined the relationship between sovereign ratings and macroeconomic/financial factors using a multivariate Panel Vector Autoregressive (PVAR) methodology. Their research investigated the interdependence between sovereign ratings and bank credit risk, considering a reciprocal relationship with NPL/NPF. The study used generalized impulse response functions (GIRFs) and found significant impacts of sovereign ratings on NPL/NPF, underscoring the importance of this relationship.

Keddad and Schalck (2020) analyzed the risk transmission from the government to domestic financial institutions using credit default swap (CDS) spreads during the European debt crisis. The researchers employed a Markov-switching model with time-varying probabilities to assess the impact of heightened sovereign risk on bank CDS spread volatility. Their study focused on 14 European countries and 30 banks, revealing that increased sovereign risk affected changes in bank CDS spreads, indicating greater risk aversion and subsequent implications for bank financing conditions due to the increased likelihood of domestic sovereign default.

H3: US sovereign debt risk uncertainty positively and significantly influences NPL/NPF in the MENA region.

The Influence of Oil Price Uncertainty on NPL/NPF

Fluctuations in oil price uncertainty impact the number of NPL/NPF in the MENA region through multiple interconnected pathways. MENA countries, which rely heavily on oil exports for revenue, face economic challenges during oil price instability or unpredictability (Vandyck et al., 2018).

One significant consequence is the effect on government revenues. Decreased oil prices reduce revenue streams for oil-exporting nations, affecting their ability to finance public expenditures and investments (Koh, 2017). This decline in government income can have far-reaching economic repercussions, including reduced economic growth, decreased corporate activity, and potential job cuts. In challenging economic conditions, businesses may struggle to generate income and meet financial obligations. Consequently, borrowers may encounter difficulties fulfilling debt commitments, increasing NPL/NPF (Suárez & Sánchez Serrano, 2018).

Oil price uncertainty directly and immediately impacts industries reliant on oil, such as the energy, industrial, and transportation sectors. Reduced oil prices put immediate pressure on enterprises’ profitability and cash flow in these sectors. The financial strain on businesses results in immediate challenges for borrowers in repaying debts, contributing to increased NPL/NPF in the banking industry.

Oil price uncertainty also affects investor sentiment and market conditions. Uncertainty in oil markets can lead to increased market volatility and greater risk aversion among investors (Gao et al., 2022). Market volatility can impact the valuation of financial assets held by banks, potentially leading to deteriorating balance sheets and overall financial health. Declining asset quality and uncertain market conditions may challenge financial institutions in managing and recovering loans, potentially necessitating more extensive provisions to cover bad loans and resulting in increased NPL/NPF (Chryses, 2020). Oil price uncertainty contributes to economic instability, reduced company performance, and financial difficulties for borrowers, all contributing to a higher NPL/NPF in the banking sector of the MENA region (Atichasari et al., 2023).

H4: Oil price uncertainty positively and significantly influences NPL/NPF in the MENA region.

The Influence of Geopolitical Risk Index on NPL/NPF

Geopolitical risks encompass a range of issues, including political instability, conflicts, trade disputes, and regulatory changes, which can adversely impact economic stability and corporate operations (Althaqafi, 2024). Geopolitical risks disrupt company operations, supply chains, and investment activity. Political instability or regional conflicts lead to business closures, reduced customer demand, and corporate operational challenges (Bartik et al., 2020). Such disruptions can hinder the financial performance of firms, making it more difficult for them to repay loans and increasing the likelihood of NPL/NPF.

Geopolitical risks often trigger economic fluctuations and uncertainty. Shifts in geopolitical risk cause abrupt fluctuations in currency exchange rates, interest rates, and stock markets (Duan et al., 2021). Market disruptions impact the financial well-being of firms and individuals, impairing their ability to meet debt obligations and contributing to NPL/NPF. Heightened geopolitical risk dampens investor sentiment and confidence. Political instability or geopolitical conflicts can deter international investments and capital inflows (Fania et al., 2020). Reduced investment and capital inflows constrain economic growth, creating financial pressures for enterprises and debtors, ultimately leading to increased NPL/NPF.

Geopolitical risks elevate the level of credit risk faced by banks and financial institutions (Phan et al., 2022). Increased uncertainty may prompt banks to exercise greater caution in lending, resulting in stricter credit terms. This can limit funding availability for firms and individuals, particularly in industries vulnerable to geopolitical risks, exacerbating financial difficulties and NPL/NPF. Geopolitical risks often trigger changes in regulations and policy measures (Hemrit, 2022). Regulatory changes or trade policy shifts impact firm operations and profitability. Compliance with new regulations requires additional resources and investments, potentially affecting cash flows and loan repayment capabilities.

H5: Geopolitical risks index positively and significantly influences NPL/NPF in the MENA region

Methodology

Sample and Data

The MENA region, a significant area encompassing the Middle East and North Africa, has been chosen for this investigation. This region is of particular importance due to the substantial challenges it faces related to NPL/NPF, which have a profound impact on banks’ profitability, liquidity, and financial health (Abu Khalaf & Awad, 2024; Almualla & Al-Gasaymeh, 2023). The high levels of NPL/NPF in this region not only constrain lending capacity but also have a ripple effect, negatively affecting economic growth, job creation, and the depletion of essential capital reserves during economic downturns or crises (Tölö & Virén, 2021). By analyzing these countries, the study aims to deepen the understanding of the regional challenges banks face and develop effective risk management strategies for ensuring financial stability. Banks in the MENA region play a pivotal role in the financial system, providing essential services and contributing significantly to economic development and stability (Allouche & Hijazi, 2024).

The study meticulously selected 13 countries from the MENA region, based on the Global Peace Index Institute for Economics and Peace’s (2020) ranking of 21 countries in the MENA region. These selections were based on inclusion and exclusion criteria and a purposive sampling technique. The inclusion criteria stipulated that the countries should be included in the Global Peace Index Institute for Economics and Peace (2020) ranking and that the banks in those selected countries should have complete data between 2005 and 2022. On the other hand, the exclusion criteria ruled out any country not ranked by the Global Peace Index Institute for Economics and Peace (2020) for the MENA region. The banks in the selected nations were further categorized into conventional and Islamic banks. Based on the inclusion and exclusion criteria, 92 banks met the criteria, comprising 42 Islamic and 50 conventional banks, chosen from 13 nations. Table 1 presents the selected nations, the banks within each country, and their classification as conventional or Islamic banks.

Selected Countries and Banks.

Data for this study was obtained from two data repositories. NPL/NPF data was obtained from Thomson Eikon Reuter DataStream, which was chosen for its comprehensive coverage and reliable information in banking and finance. Data on policy uncertainty were obtained from https://www.policyuncertainty.com/index.html. The data for the policy uncertainty had varying frequencies, including daily, monthly, quarterly, and yearly observations. The daily, monthly and quarterly data are transformed into yearly data to facilitate a comprehensive and manageable analysis of the relationship between policy uncertainty and NPL/NPF in the MENA region.

Dependent and Independent Variables

The variables for dependent, independent, and moderating variables are presented in Table 2.

Summary and the Sources of the Variables.

Dependent Variable

The study used NPL/NPF as the dependent variable, a loan where borrowers have defaulted on payments, usually by 90 days or more (Bholat et al., 2018). NPL/NPF are crucial metrics that provide insights into the financial well-being of institutions. They indicate the quality of the loan portfolio and the level of credit risk exposure. Elevated levels of NPL/NPF put pressure on a bank’s capacity to meet its financial obligations, diminish its ability to generate profits and undermine its capital strength. This highlights the potential risks and challenges NPL/NPF pose to a bank’s financial stability (Atichasari et al., 2023). Managing NPL/NPF effectively is critical to maintaining financial stability. Analyzing these metrics assists in evaluating the influence of economic uncertainties on the performance of the banking industry, thereby improving their ability to withstand unpredictable conditions.

Independent Variables

This study employed five independent variables to assess policy uncertainties. The initial variable used was the world pandemic uncertainty, which quantifies uncertainties associated with worldwide pandemics such as the COVID-19 pandemic (Salisu et al., 2021). This metric measures the economic disruptions and market instability resulting from pandemics, impacting borrowers’ ability to repay debts and the state of the economy (Mahajan, 2020). Uncertainties stemming from the pandemic directly influence enterprises and individuals, potentially increasing NPL/NPF (Kimani, 2023).

The second variable, US trade policy uncertainty, represents uncertainties arising from changes in US trade policies, such as tariffs and trade agreements. Changes in US trade policies disrupt the flow of goods and services between countries and impact business operations, which affects borrowers’ ability to meet financial obligations and repay loans (Huang et al., 2022).

The third variable, US sovereign debt risk uncertainty, quantifies uncertainties associated with fluctuations in the risk of US sovereign debt. This metric affects global financial markets, interest rates, and investor sentiment. They also indirectly impact borrower credit risk and NPL/NPF (Agoraki et al., 2022).

The fourth variable, oil price uncertainty, represents volatility in oil prices and its effects on countries reliant on oil exports in the MENA region. Oil price fluctuations impact government income, business profitability, and borrowers’ ability to repay loans, increasing NPL/NPF during oil price volatility (Idris & Nayan, 2016).

As the fifth variable, geopolitical risks represent uncertainties arising from geopolitical tensions and conflicts. Geopolitical risks disrupt financial markets, erode investor confidence, and disrupt economic activities in the MENA area. This influences borrowers’ behavior and increases credit risk (Mansour-Ichrakieh & Zeaiter, 2019). It contributes to rising NPL/NPF as organizations and individuals struggle to fulfill financial obligations due to geopolitical instability.

Moderating Variable

The size of the bank serves as a crucial moderating factor for this study, as it demonstrates the diverse effects of uncertainties on NPL/NPF contingent upon the bank’s size. The resources, risk management, and varied assets of larger institutions enable them to endure the impacts of uncertainty better (Arhinful et al., 2023a). This indicates that smaller banks may be more vulnerable to NPL/NPF and uncertainty, but larger banks may be less affected by similar challenges. Using bank size as a moderating variable elucidates the strategies various banks employ to navigate external uncertainty, providing insight into how small and big banks manage external shocks or uncertainties based on their size (Arhinful et al., 2024). This strategy explains the dynamics of NPL/NPF and uncertainty by acknowledging that external influences influence banks differently.

Pre-Estimation Tests

Table 3 presents the results of the cross-sectional dependence and heterogeneity tests conducted. The initial pre-estimation test was the cross-sectional dependence test, aimed at identifying interdependence or correlation among specific entities (such as countries or banks) within the panel dataset (Elhorst et al., 2021). The Breusch-Pagan Lagrange multiplier, Pesaran scaled Lagrange multiplier, and Pesaran CD were used to assess the presence of cross-sectional dependence across banks in the MENA region. The alternative hypothesis indicates the presence of cross-sectional dependence, and the null hypothesis indicates the presence of cross-sectional independence. Therefore, the alternative hypothesis was accepted based on the findings presented in Table 3, suggesting interdependence among the activities of the banks in the MENA region.

Cross-Sectional Dependence and Heterogeneity Tests.

p < .01. **p < .05. *p < .1.

Cross-sectional dependence implies that one bank’s performance and risk exposure may influence and potentially affect other banks in the same region or market (Kutan et al., 2012). The interconnectedness between institutions can lead to the transmission of financial risks and vulnerabilities, thereby contributing to systemic risk within the banking system (Andrieş et al., 2022). When a bank experiences financial distress or instability due to external factors, it could trigger a chain reaction affecting other interconnected banks, amplifying systemic risk and contagion effects during economic stress or financial shocks (Roncoroni et al., 2021). The interdependence of banks implies that any crisis or failure in one institution can rapidly propagate to others, impacting market confidence and stability.

The second preliminary test was the heterogeneity test, which identified disparities or distinctions in individual-specific impacts among the entities (countries or banks) within the dataset. The Pesaran-Yamagata test was employed to assess heterogeneity among the banks. The null hypothesis of this test posits that there is homogeneity, and the alternative hypothesis asserts that there is heterogeneity. The results presented in Table 3 indicated the presence of heterogeneity among these organizations, leading to the acceptance of the alternative hypothesis. Banks with diverse characteristics may encounter challenges in implementing uniform risk management techniques due to the necessity for tailored approaches to effectively assess and mitigate risks based on varied risk profiles (Kandasamy et al., 2020).

Choice of Regression Estimation

The cross-sectional dependence and heterogeneity test results show that this study needs robust and advanced regression estimation methods to give accurate estimates even though the datasets have cross-sectional dependence and heterogeneity. Therefore, the study selected the Augmented Mean Group (AMG) estimator to provide reliable estimation results in the presence of cross-sectional dependence and the two-step Generalized Method of Moments (GMM) estimation to deal with the issues of endogeneity, heteroskedasticity and auto-serial correlation associated with panel data (Arhinful et al., 2024; Mensah, Arhinful, & Bein, 2024).

The AMG estimator is a valuable technique for analyzing panel data, particularly in the presence of cross-sectional dependency and heterogeneity (Mesagan & Vo, 2023). This method is designed to accommodate individual-specific factors while capturing typical group dynamics. It allows for incorporating entity-specific effects into the model while acknowledging similarities or relationships among entities within the dataset. The AMG estimator tackles the issue of cross-sectional dependence by integrating a shared dynamic process across all entities in the panel data (Guzel & Okumus, 2020). This is achieved by incorporating variability in the slope coefficients and considering the influence of unobserved shared characteristics that can lead to interdependence across different data points.

The two-step GMM estimator, a robust and dependable approach, is well-suited for addressing issues in panel data analysis, such as endogeneity, serial correlation, and heteroscedasticity. This approach delivers accurate and dependable parameter estimates in settings involving cross-sectional dependence and heterogeneity (Arhinful et al., 2023b; Mensah & Bein, 2023). The framework provides a robust foundation for mitigating various forms of bias and inefficiency in panel data, ensuring the reliability and accuracy of regression findings.

Model Specification

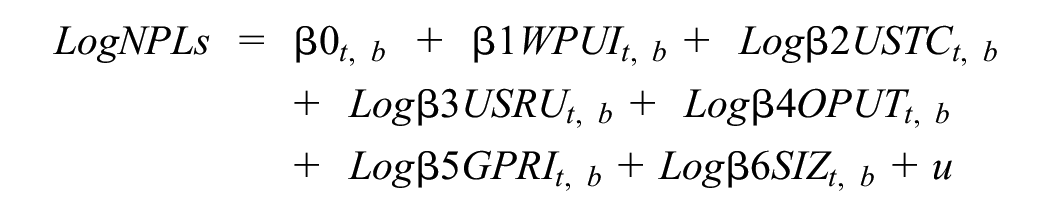

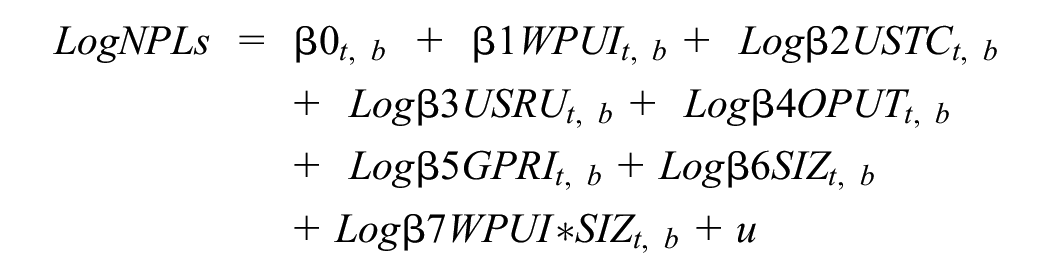

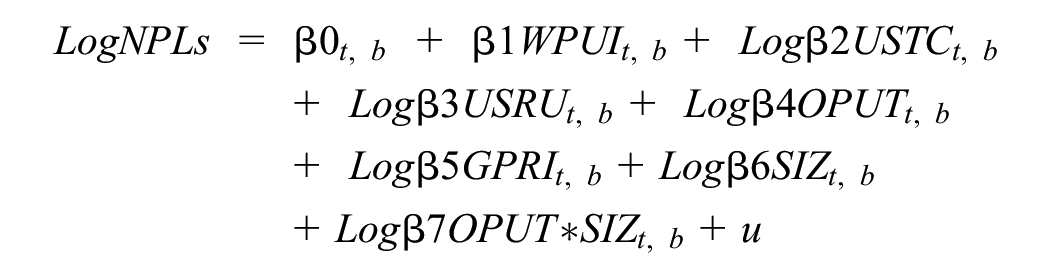

The study employed four models to investigate the influence of uncertainties on bank NPL/NPF in the MENA region. The first model examines the direct impact of various uncertainties on NPL/NPF, which contributes to the literature. Models two, three, and four explore the interaction effects between bank size and the world pandemic uncertainty index, US trade policy uncertainty, and oil price uncertainty on NPL/NPF. The four models are displayed below.

Where “t” denotes years and “b” denotes banks in MENA regions

Discussion and Results

Table 4 presents the descriptive statistics of the variables utilized in this study. The mean value for NPL/NFP suggests that, on average, the banks have a larger number of loans considered to be non-performing (Bholat et al., 2018). This indicates a notable amount of underperformance in the loan portfolio of the institutions examined, emphasizing possible difficulties associated with credit quality and risk management. The results highlight the high occurrence of NPL/NPF, indicating possible challenges in repaying loans and maintaining financial stability.

Descriptive Statistics.

The average mean for world pandemic uncertainty indicates a heightened level of uncertainty on aspects associated with the pandemic. This uncertainty could influence investment choices and market sentiment, impacting economic circumstances and financial markets. The average score for US trade policy uncertainty also indicates significant uncertainty regarding US trade, which can disrupt the dynamics of international trade, investment choices, and market sentiment, potentially leading to economic instability and affecting corporate operations. The mean score for US sovereign debt risk uncertainty indicates a substantial level of uncertainty linked to the risk of US sovereign debt. This uncertainty affects interest rates, global financial markets, and investor confidence, affecting borrowing costs and the MENA area’s financial circumstances.

The average score for oil price uncertainty indicates that oil price volatility can impact economies that depend on oil exports, affecting government income, fiscal policies, and investment choices in the energy industry. The average geopolitical risk indicates an increased perception of risk arising from geopolitical events and conflicts. These risks disrupt markets, trade flows, and investor confidence.

Amin and Cek (2023) and Mensah, Arhinful, & Owusu-Sarfo et al. (2024) used the variance inflation factor (VIF) to check if the independent variables in their studies have multicollinearity. The researchers asserted that VIF values below 5 indicate the absence of multicollinearity, and the VIF for all the independent variables in this study is less than 5. These findings indicate no problems with multicollinearity among the independent variables.

Table 5 presents the results of the correlation matrix, which was used to assess the presence or absence of multicollinearity among the independent variables. The results indicate the absence of multicollinearity, consistent with prior studies by Arhinful et al. (2023c) and Arhinful and Radmehr (2023a). The correlation values between the independent variables are all below the threshold of .70 (Arhinful & Radmehr, 2023b; Wooldridge, 2009), suggesting no significant correlation that would indicate multicollinearity issues. This finding supports the VIF results presented in Table 3.

Matrix of Correlations.

The results of unit root tests conducted using two methods, namely the Cross-sectionally Augmented IPS (CIPS) test and the Levin-Lin-Chu (LLC) test, are presented in Table 6. The IPS (CIPS) test is tailored explicitly to determine the unit roots test when cross-sectional dependence is present in panel data (Gregori & Giansoldati, 2020). This assessment determines whether variables remain stationary at levels or become stationary after the first difference. The LLC test identifies unit roots and evaluates the degree of integration (Zehirun et al., 2015). The unit root tests revealed that all the variables were stationary at the level and their first difference, leading to the acceptance of the alternative hypothesis. The presence of stationary variables simplifies parameter estimation and enhances statistical results’ reliability and interpretability.

Unit Root Tests.

p < .01. **p < .05. *p < .1.

Table 7 presents the results of AMG estimation for all banks and their categorization into conventional and Islamic banks in the MENA region.

Augmented Mean Group Estimation Results.

p < .01, **p < .05, *p < .1.

The Influence of Uncertainties on NPL/NPF (All the Banks)

The study revealed that world pandemic uncertainty had a negative and significant influence on NPL/NPF across banks in the MENA region, which supports the study’s hypothesis. Behavioral finance theory explains the impact of psychological factors and biases on financial decision-making, especially in situations characterized by uncertainty and stress (Zahera & Bansal, 2018). Amidst a pandemic, increased uncertainty and fear might result in more cautious financial conduct from borrowers and lenders. Individuals who borrow money may exhibit prudence in acquiring additional debt and give greater importance to settling current loans to prevent future financial hardship. Similarly, lenders may strengthen their credit standards, decreasing the likelihood of new NPL/NPF, when they notice a decrease in NPL/NPF during the pandemic.

These findings were because banks might have used more cautious lending strategies during periods of uncertainty, such as imposing stricter credit criteria and offering extra assistance to customers experiencing financial challenges (U. Khan & Lo, 2019; Ng et al., 2020). The heightened level of uncertainty may have also prompted borrowers to exercise more prudence, leading to enhanced repayment behavior and decreased rates of NPL/NPF (Ng et al., 2020). This result emphasizes the significance of implementing efficient risk management and cautious lending approaches during times of crisis to reduce loan defaults and uphold financial stability within banks (Taiwo et al., 2017).

From an economic perspective, numerous countries in the MENA region heavily depend on income generated from oil, which may be extremely unstable during global crises (Mensi et al., 2023). Throughout the pandemic, governments enacted fiscal support measures to stabilize their economies and assist people and companies, potentially mitigating the occurrence of defaults. The MENA countries have diverse levels of stability and political administration. Governments in politically and economically stable nations enact efficient policies to alleviate the economic consequences of the pandemic. This would have helped borrowers and kept NPL levels minimal (Hale et al., 2021).

Secondly, the study discovered that US trade policy uncertainty also had a negative and significant influence on NPL/NPF in MENA banks, supporting the study’s hypothesis. The rational expectations theory suggests that individuals and organizations make decisions by considering their reasonable perspective, the information they access, and their past experiences (Coibion et al., 2018). When confronted with trade policy uncertainties, borrowers and lenders anticipate probable economic disruptions and adopt proactive activities that will enable them to handle the uncertainty effectively. During increased trade policy uncertainty, such as alterations in tariffs or trade restrictions, companies may adopt a more cautious approach to their investment and expansion strategies, prioritizing preserving financial stability. To mitigate the risk of default, borrowers may prioritize the repayment of their current debts to prevent future financial limitations (Mayer et al., 2013). Similarly, lenders may implement stricter credit criteria to minimize possible risks, reducing new NPL/NPF.

Kim et al. (2009) indicated that banks improve risk awareness and adjust to changes in external trade dynamics. Banks modified their lending methods to address the potential risks arising from trade interruptions or shifts in market circumstances due to changing trade policy (Aday & Aday, 2020). The increase in trade policy uncertainty led banks to pursue safer lending procedures, resulting in stronger loan portfolios. It is crucial for banks to actively address external economic uncertainties to manage NPL/NPF and maintain financial resilience efficiently (Bastan et al., 2023).

From an economic perspective, countries in the MENA region that have robust commercial connections with the United States, either directly or indirectly, experience instability in their economic connections, causing banks to embrace more cautious financial strategies (Gilchrist et al., 2014). Exporters may encounter varying demands, impacting their creditworthiness and loan repayment ability. As a result, they may prioritize loan repayment to maintain ongoing access to credit. The MENA region exhibits different stability and policy predictability levels from a political standpoint. In politically and economically stable nations, governments are more likely to have the necessary resources and capabilities to enact policies that protect their economies from the negative impacts of international trade disruptions. This, in turn, helps firms in these countries to continue making their loan payments on time (Essers, 2013).

Thirdly, the study identified a positive and significant influence of US sovereign debt risk uncertainty on NPL/NPF in MENA banks, supporting the study’s hypothesis. The asymmetric information theory elucidates the adverse effects of uncertainty surrounding US sovereign debt on NPL/NPF by emphasizing the disparity in information between borrowers and lenders (Ioannidou et al., 2022). The heightened US sovereign debt uncertainty increases the risk inside the global financial system, complicating lenders’ ability to evaluate borrowers’ creditworthiness appropriately. The information disparity creates an information gap, so the lenders offer loans to borrowers with greater risk levels. In times of elevated sovereign debt risk, borrowers used financial misrepresentation to get loans, worsening the problem and raising the probability of defaults (Quail, 2011).

This highlights the interdependence between global economic risks and the results of local banks. Increased US government debt risk uncertainty led to economic instability, affecting borrowers’ ability to repay their debts and creditworthiness (Ahiadorme, 2023). During times of heightened sovereign debt uncertainty, banks faced increased risks of defaults. To minimize potential losses, banks conduct thorough risk assessments and diversify their portfolios (Jonasson & Papaioannou, 2018). The findings suggest that macroeconomic influences from outside the region impact the performance of local banks, highlighting the significance of proactive risk management and financial planning (Afshan et al., 2023).

US sovereign debt risk led to financial instability, and that caused a negative impact on global investment flows and economic growth. The instability has the potential to affect the MENA countries. Banks encounter greater challenges in effectively handling loan portfolios (Albaity et al., 2019). Countries with weak financial systems or inadequate regulatory oversight are more vulnerable to the adverse effects of asymmetric information, resulting in increased levels of NPL/NPF due to reduced ability to enforce loan conditions and evaluate borrower risk.

Additionally, oil price uncertainty was found to have a negative and significant influence on NPL/NPF in MENA banks, supporting the study’s hypothesis. The market discipline theory elucidates the adverse effects of oil price uncertainty on NPL/NPF by emphasizing the role of market dynamics and their implications on financial institutions. The fluctuating nature of oil prices puts financial pressure on borrowers in sectors heavily reliant on oil, hence raising the likelihood of loan defaults (Wang & Luo, 2020). As a result, lenders adopt stricter lending criteria to handle this increased level of risk effectively. They increase interest rates, require additional collateral, or impose credit restrictions, which lead to a decrease in loan acquisition. Although these restrictions effectively mitigate immediate risk, they can also restrict loan availability and impede economic growth. With the increase in defaults, banks may choose to raise their provisions for loan losses, which will further impact their financial health and result in higher NPL/NPF.

The decrease in NPL/NPF during oil price instability may indicate the ability of banks operating in countries heavily reliant on oil to withstand and recover from challenging conditions (Al-Harthy et al., 2021). Banks in these regions successfully protected themselves against oil price changes by using measures such as hedging or diversifying their loan portfolios to reduce exposure (Cavaliere et al., 2021). Decreased oil prices may favor economic stability and borrowers’ creditworthiness, reducing loan defaults (Nadalizadeh et al., 2019). The findings emphasize the significance of banks’ capacity to adjust to changes in commodity prices and economic instability to uphold loan quality and preserve financial performance (Acharya & Ryan, 2016).

From an economic perspective, fluctuations in oil prices lead to instability in regions that heavily rely on oil, which in turn impacts economic performance and raises the likelihood of borrowers in these areas defaulting on their loans (Wang & Luo, 2020). From a political standpoint, governments in countries that heavily rely on oil may encounter difficulties in upholding economic stability and assisting their financial institutions when faced with fluctuations in oil prices. This situation might worsen the NPL/NPF issue.

Furthermore, the study found that geopolitical risks had a negative and significant influence on NPL/NPF in MENA banks, supporting the study’s hypothesis. The asymmetric information theory explains the adverse effect of geopolitical risks on NPL/NPF by emphasizing the unequal distribution of knowledge between borrowers and lenders. Geopolitical risks, which encompass conflicts and political instability, amplify the challenge of acquiring precise information regarding the creditworthiness of borrowers (Khoo & Cheung, 2021). Uncertainty causes lenders to exercise greater caution, resulting in more stringent loan terms, higher interest rates, and the imposition of additional collateral requirements. Borrowers, particularly those in volatile regions or industries, encounter increased challenges in obtaining funding and undergo financial hardship. This strain results in elevated default rates and increased NPL/NPF. The economic consequences of geopolitical concerns, such as diminished consumer confidence and economic slumps, can intensify borrowers’ financial instability, raising the probability of defaults.

These findings indicate that although the region has inherent geopolitical risks, banks have successfully reduced these risks or diversified their operations to protect themselves from geopolitical issues (Ngo et al., 2024). The significance of strategic risk management and operational resilience within banks is underscored by their ability to maintain stable loan portfolios, notwithstanding geopolitical risks (Girling, 2022). The findings suggest that banks must navigate geopolitical environments while upholding financial stability and ensuring uninterrupted services to borrowers.

The Influence of Uncertainties on NPL/NPF (Both Conventional and Islamic Banks)

The study revealed that the world pandemic uncertainty had an impact on NPL/NPF among conventional and Islamic banks in the MENA region. Specifically, this uncertainty had a negative and significant influence on the NPL of conventional banks while showing a positive and significant influence on the NPF of Islamic banks, and these findings support the behavioral finance theory. This suggests that conventional banks have implemented more effective risk management strategies or adapted lending practices to mitigate pandemic-related uncertainties, resulting in lower NPL/NPF (Karkowska et al., 2023). The positive influence on NPF in Islamic banks could indicate different risk exposures or lending behaviors unique to Islamic banking principles during pandemic-related uncertainties (Rizwan et al., 2022). These findings underscore the importance of robust risk management strategies in the banking sector, particularly amid economic and geopolitical uncertainties.

The economic implications for conventional banks highlight the necessity of strengthening capital buffers and improving risk management measures to alleviate unforeseen circumstances. To assist banks in efficiently resolving crises, governments and regulators, through political support, may need to enforce more rigorous oversight and support systems, including regulatory modifications at times of heightened risk.

The economic implications suggest that Islamic banks possess significant potential, as their risk-sharing mechanisms offer enhanced stability during uncertainty. During economic upheavals, governments can politically advocate for Islamic banking as an essential element of the financial system by implementing legislation that fosters its growth and utilization as a stabilizing factor.

Secondly, the study uncovered contrasting effects of US trade policy uncertainty on NPL/NPF between conventional and Islamic banks in the MENA region. US trade policy uncertainty was found to have a negative and significant influence on the NPL of conventional banks. It exhibited a positive and significant influence on the NPF of Islamic banks. These findings support the rational expectations theory. The findings suggest that conventional banks may have responded more adversely to fluctuations in US trade policies, leading to higher NPL (Jiang et al., 2018). The Islamic banks may have demonstrated resilience or adapted their lending strategies differently in response to trade policy uncertainties (Chenet et al., 2021). Differences in business models or risk management approaches between conventional and Islamic banks could shape their vulnerability to external trade dynamics.

The economic implications suggest that conventional banks should diversify their income sources and rely less on markets affected by trade policy changes to reduce risk. This implies that enhanced government participation in international trade agreements may promote stabilizing the financial sector and diminishing uncertainty.

The economic implications for Islamic banks indicate they could exploit further opportunities in less vulnerable regions to trade policy instability. The region should politically promote Islamic banking as a more robust alternative and support the creation of legislation that facilitates its expansion in response to shifts in international commerce.

Thirdly, the study found a positive and significant influence of US sovereign debt risk uncertainty on the NPL/NPF of conventional and Islamic banks in the MENA region, supporting the asymmetric information theory. These results indicate that US sovereign debt risk uncertainty may have a more pronounced impact on banks, potentially due to their specific exposure to global financial markets or differences in asset-liability structures (Askari, 2012). The positive influence suggests that the banks may need to adopt tailored risk management practices to address sovereign debt risks effectively (Mülbert, 2015). These tailored practices could include more stringent credit risk assessments or the development of financial instruments that can hedge against sovereign debt risks. Unique characteristics of banking operations, such as their prohibition of interest and focus on risk-sharing, can influence their vulnerability to sovereign debt uncertainties.

The economic implications for Islamic and conventional banks indicate that managing exposure to sovereign debt requires heightened scrutiny. To reduce exposure, banks may need to modify portfolios and improve credit risk evaluations. Governments should aim to stabilize sovereign debt markets, implement laws that reduce uncertainty, provide a more stable environment for banks, and preserve the financial sector’s sustainability amid debt risk volatility.

Additionally, the study revealed a negative and significant influence of oil price uncertainty on the NPL/NPF of both conventional and Islamic banks in the MENA region, supporting market discipline theory. Oil price fluctuations directly impact oil-dependent economies’ economic conditions, affecting borrower creditworthiness and loan repayment capabilities across both conventional and Islamic banking sectors (Idris & Nayan, 2016). This underscores the importance of effective risk mitigation strategies and the diversification of loan portfolios to mitigate the impact of oil price volatility on NPL/NPF.

Considering the economic implications, conventional and Islamic banks must augment their resilience to oil price volatility. This results from their involvement in oil-dependent businesses, which may subject them to increased risk during fluctuations in oil prices. Diversifying investment portfolios and enhancing risk management measures for energy-dependent sectors is essential. To mitigate the detrimental impacts of oil price volatility on the financial sector, governments in the MENA should enact policies that stabilize oil markets and promote banks to diminish their dependence on oil-related enterprises.

Furthermore, the geopolitical risks exhibited a negative and significant influence on the NPL/NPF of both conventional and Islamic banks in the MENA region, supporting the asymmetric information theory. This finding suggests that geopolitical risks may not directly translate into increased NPL/NPF for regional banks. Robust risk management practices or diversified operations may have enabled banks to navigate geopolitical challenges effectively (Gamso et al., 2024). Geopolitical stability or effective risk management strategies can contribute to stable loan portfolios despite inherent regional risks.

The economic implications show that geopolitical stability lowers the likelihood of loan defaults, which benefits both conventional and Islamic banks. Banks should prioritize investments in sectors and areas less vulnerable to geopolitical risks. The regions should prioritize regional stability and strengthen diplomatic connections to avoid geopolitical risks. This will aid in stabilizing the banking system and ensuring sustained economic growth in the region.

Validating the Results of GMM

When the results from the AR (1) test are statistically significant and the AR (2) test results are statistically insignificant, affirm the validity of the model (Arhinful et al., 2024). The AR (2) results indicate no auto-serial correlation (Amin & Cek, 2023). Similarly, the Sargan-Hansen test assesses the model’s overidentifying restrictions. When the Sargan test yields insignificant results, it suggests the absence of such restrictions and the instrumental variables are exogenous. Hansen test values falling within the 10 to 30 range indicate the absence of overidentifying restrictions and that the instrumental variables do not correlate strongly with the error term. (Roodman, 2020).

Hansen test results falling below 10 or exceeding 30 signal potential issues with the model results. Values below 10 may indicate issues that require careful re-evaluation, while values exceeding 30 might suggest overfitting, necessitating a thorough re-evaluation of instrument validity and model (Roodman, 2020).

Table 8 presents the results of the two-step GMM estimation. The results in Table 8 are similar to those of the AMG findings in Table 7. Despite variations in the estimated coefficients and standard errors, the positive or negative significant or insignificant findings are consistent. This consistency confirms the robustness of the AMG findings and reaffirms the reliability and robustness of the original findings derived from the AMG estimation.

Two-Step GMM.

p < .01. **p < .05. *p < .10.

Conclusions

The study investigated the impact of uncertainties on NPL/NPF of conventional and Islamic banks operating in the MENA region. The study employed a purposive sampling technique to select 92 banks from 13 MENA countries, of which 42 were Islamic, and 50 were conventional banks, using data from 2005 to 2022. The study utilized two estimation methods, AMG and two-step GMM, to address potential cross-sectional dependence and endogeneity issues. These methods were chosen to provide robustness and reliability of the finding on how uncertainties impact NPL/NPF across different banking sectors in the MENA region.

The study revealed that world pandemic uncertainty had a negative and significant influence on the NPL of conventional banks while showing a positive and significant influence on the NPF of Islamic banks. US trade policy uncertainty was found to have a negative and significant influence on the NP of conventional banks. In contrast, it exhibited a positive and significant influence on the NPF of Islamic banks as observed. The investigation discovered a positive and significant influence of US sovereign debt risk uncertainty on the NPL/NPF of conventional and Islamic banks in the MENA region.

Policy Implications

For the Banks in the MENA Region

Banks in the MENA region must strengthen their risk management frameworks to address the problems provided by external uncertainties. To accomplish this, they must employ advanced scenario analysis and stress testing approaches tailored to address these risks. This approach will enhance banks’ ability to foresee and alleviate potential asset quality threats, securing a more resilient financial standing during turbulent times. To ensure financial stability, it is essential to incorporate these advanced risk management frameworks within the organization’s comprehensive plan.

Banks should focus on diversifying their revenue sources to alleviate the adverse effects of external shocks, such as fluctuations in oil prices and uncertainty in US trade policy. Expanding their operations beyond traditional sectors and the energy industry is a viable strategy. Moreover, banks can create and provide cutting-edge financial solutions to various clients and businesses. Geographic diversification can diminish reliance on markets more vulnerable to external issues by entering new markets within and beyond the MENA region. This strategy will protect banks against sector-specific declines and guarantee their profitability given the significant influence of uncertainty over US sovereign debt risk on NPL/NPF.

Banks must enhance their credit allocation and monitoring systems. By implementing more rigorous credit assessment protocols, banks can more accurately determine their customers’ financial conditions and ensure that loans are extended to clients with excellent creditworthiness. Moreover, diversifying loan portfolios to cover a wider range of businesses and consumer demographics can help mitigate government debt risk and maintain a broader, stable, balanced lending portfolio.

Enhanced liquidity and capital reserves are crucial for banks in the MENA region, especially considering the possible detrimental impacts of uncertainty on non-performing loans/non-performing financing. Banks must enhance their capital adequacy ratios and sustain sufficient liquid assets to align more closely with the Basel III standards. These reserves will enable banks to maintain normal operations during economic upheavals and to endure possible disruptions. This will bolster investors’ and customers’ confidence in the banks’ capacity to manage risk while safeguarding them from financial instability.

Investment in digital transformation is a crucial strategy for banks in the MENA region to improve their operational efficiency and agility in uncertain conditions. Banks can use digital banking systems and data analytics to improve their ability to evaluate risk and recognize and alleviate possible threats to their portfolios. Digitalization enhances customer service by enabling banks to provide more efficient and tailored services to their clientele. This will guarantee business continuity and expansion amid global economic turmoil by facilitating the acquisition and retention of existing customers.

For the Conventional Bank in the MENA Region

To improve risk management and reduce default probabilities, traditional banks should use advanced risk assessment methodologies and conduct stress testing to analyze the effects of uncertainty on loan portfolios. They must also diversify their income sources by creating alternative financial goods and services, such as green finance or digital banking solutions, which are less vulnerable to market and geopolitical changes. Augmenting capital buffers is essential to safeguard against potential disruptions from volatile economic conditions and preserve liquidity and stability during crises.

For the Islamic Banks in the MENA Region

Islamic banks should promote risk-sharing models by improving the development and marketing of financial products that offer stability during volatile economic situations and appeal to clients desiring security. Companies may concentrate on penetrating new markets or sectors less vulnerable to oil price volatility and geopolitical risks to expand their market presence and diversify their portfolios. Ultimately, establishing frameworks that promote the growth of Islamic finance would guarantee regulatory compliance and foster stability and financial inclusion by strengthening regulatory engagement through close cooperation with regulators.

Limitation of the Study and Directional Future Study

One limitation of this study is the restricted number of countries and banks included in the analysis. The countries were chosen based on data availability for banks within the MENA region. Despite the Global Peace Index Institute for Economics and Peace (2020) encompassing 21 countries, only 13 countries’ banks were utilized due to missing data in the Thomson Eikon Reuters database. This limited selection of countries and banks restricts the generalizability of the study’s findings.

Another limitation of the study is identifying a new gap in the existing literature, with limited studies conducted in those areas. This scarcity of empirical studies makes it challenging to gather enough comparative results to assess how this study’s findings align with or differ from prior research.

Furthermore, the study exclusively focuses on banks, neglecting other types of financial institutions. Future research should consider incorporating a broader range of financial institutions, such as insurance companies, to expand the scope of the analysis and attain a larger sample size. This approach would enhance the comprehensiveness and representativeness of the study’s results across the MENA region.

Footnotes

Author Note

This manuscript is new, has never been published before, and is not being looked at for publication anywhere else.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author, upon reasonable request.