Abstract

This study attempts to examine the impact of service quality on customer loyalty and customer satisfaction using the SERVQUAL model for four main Islamic banks in the Sultanate of Oman. This is a quantitative nature of a study, which involved a structured, self-administered questionnaire based on a convenience sampling method gathering data from 120 customers of Islamic banks in Oman. The study data were analyzed using SPSS, and the reliability coefficient (Cronbach’s alpha) was established. The correlation analysis examined the significant relationships among the study variables. The impact of service quality dimensions on customer satisfaction was captured through regression analysis. The key findings of the study revealed that the respondents showed on average an “Agree” response in the five areas, namely, tangibles, responsiveness, reliability, assurance, and empathy. The correlation results depicted a significant relationship between the three variables: service quality, customer satisfaction, and customer loyalty. Similarly, regression results demonstrated that empathy and responsiveness dimensions have a significant positive impact on customer satisfaction. It is, therefore, recommended that banks should focus more on empathy and responsiveness considering the significant relationship of these two variables on customer satisfaction. However, banks should not neglect the importance of other variables such as reliability, assurance, and tangibles that are revealed as important by responses of the participants for the bank’s provisions.

Introduction

The significance and the role of Islamic banking have been gaining worldwide attention for the last two decades although its financial strength is at initial stages as compared with the conventional banking sector. According to the statistics provided by Islamic Financial Services Board (2018), Islamic banking sector has already crossed US$1.5 trillion, and it is further estimated that the size of Islamic assets in the banking industry will reach US$3.2 trillion at the end of 2020. The Middle East, which is the center of Islamic banking, has contributed 80% of the amount, whereas 20% is shared by the rest of the world. Islamic banking growth outlook continues to be positive, growing 50% faster than the overall banking sector in several core markets. In Saudi Arabia, the market share of Islamic banking assets is now more than 50%. In addition to the contribution of the Gulf Cooperation Council to Islamic banking, several Arab markets have launched Islamic banking services.

Islamic banking is a recent addition to the financial sector of the Sultanate of Oman although it has existed for a long time in other Islamic countries. Officially, the issuance of license to launch Islamic banking was made in 2012 through Royal Decree 69/2012 that paved the way toward the establishment of Islamic banks and other financial institutions based on Islamic law (Shariah). Islamic banks in Oman started operations in 2013 and few in 2014. As of the beginning of 2020, two full-fledged Islamic banks and Islamic windows of a majority of commercial banks have been operating in Oman since then.

The perceptions from the supporters of this banking concept assert that Islamic banking will have a bright future and rapid growth because of its uniqueness that emphasizes interest-free, business partnership solely based on profit–loss sharing and noncharging loan services, thereby making it distinct from the conventional banking industry.

Considering that Islamic banking is a new endeavor in the country, questions were still proliferated about the extent of service quality that will be extended by the banking sector and how to gain customer loyalty and achieve customer satisfaction with the needed quality service provision that the clients demand or perceive from the industry? Moreover, the quality service delivery of products and services in Islamic banking is still in a developing stage as compared with conventional banking. The objective of the study is to evaluate the extent of service quality provided by Islamic banks to customers and establish the linkage between service quality to other variables such as customer loyalty and customer satisfaction. This will help stakeholders to get insight into the sector and improve the service quality provided by them to potential customers. To the extent of our knowledge, this is the first endeavor in this area to answers some of the above questions.

Literature Review

This section overviews the existing literature, case studies, and pieces of evidence about the elements of the SERVQUAL model, namely, the dimension of service quality, customer satisfaction, and customer loyalty.

Service Quality

The concept of service has been defined since the 1980s by Churchill and Surprenant (1982) together with Parasuraman et al. (1985), who popularized the customer satisfaction theory through measuring the firm’s actual service delivery in conformity with the expectations of customers, as defined by the attainment of perceived quality, and that is meeting the customers’ wants and needs beyond their aspirations. With this premise, Parasuraman et al. (1988) later expanded the concept of service into the five dimensions of service quality that comprised tangibles, reliability, responsiveness, assurance, and empathy. Further evaluation of the concept has developed other dimensions of service quality as described by Lehtinen and Lehtenin (1982) and Groonroos (1984), where the former stressed that service quality might be divided into three main dimensions, namely, the physical quality, corporate quality, and interactive quality. Furthermore, Groonroos (1982), explained that the concept of service quality could be evaluated by corporate image, functional quality of service encounter, and the technical quality of the outcome. This had been earlier identified and evaluated by Parasuraman et al. (1988) who introduced the service quality model known as SERVQUAL, which was first applied in the service industry specifically for restaurants.

According to this model, service quality has been described with the help of five quality dimensions. These dimensions include five areas, namely, tangibles, reliability, responsiveness, assurance, and empathy, even though definitions relating to these variables have been modified by different authors. The tangibles dimension of service quality has been referred by Fitzsimmons and Fitzsimmons (2014) as the tangibility of the provided services, and it includes the firm’s materials and equipment and physical facilities, the physical environmental conditions, materials used for communication, and the like. Davis et al. (2003) have also affirmed that the service quality has a significant impact on higher education service providers as well.

However, the reliability dimension encompasses the ability of the enterprise or the business to delivery what was promised (Parasuraman et al., 1988). They added that reliability had played a significant role in the functioning of the traditional service operators as it consists of the following: accuracy of billings, quotations, records, and commitment to fulfill orders. Korda et al. (2010) have tested how reliability could be applied in the banking sector of transition economies in Europe, considering the concept of perceived quality and customer satisfaction, and results showed that the perceived value has the potential to be a mediating variable between perceived quality and customer satisfaction.

Another dimension of service quality is responsiveness, which usually measures the ability of the company or firm to respond to customers with willingness and the promptness of the service (Parasuraman et al., 1988). This definition has been modified by Johnston (1997) to include the timely delivery of services with speed to counter the problems of long queues and waiting periods. Furthermore, in this dimension, the concept of how quick the workers should respond to the customer’s needs and complaints is addressed. The fourth dimension of service quality is empathy, which was defined by Parasuraman et al. (1985) as the company’s ability through its employees to provide due care to the customers as well as address their individual and personal concerns and understand their needs. These elements have been applied in the study of Ananth et al. (2011), and findings showed a positive relationship to customer satisfaction as applied to banks in the private sector. Johnston (1997) has also supported the concept by defining empathy as the employees’ willingness to welcome customers and to take care of their specific needs. The last dimension is the assurance dimension that demonstrates to provide security and safety to the customers so that it will lessen their state of worries and anxieties with regard to the services provided to them. In other words, it is the assurance or making sure that they will receive positive benefits by availing the services based on what they desire without negative implications.

Customer Satisfaction

The term customer satisfaction and its importance were defined by Zeithami et al. (1996) as, to achieve continuous success of companies in the long run, the need to emphasize customer satisfaction is a key consideration. In other words, satisfaction can only be met when the performance generated by companies exceeds customer expectations. In this context, various authors and researchers have accentuated the importance of customer satisfaction as well as dissatisfaction as related to the company’s achievement of success and the incurrence of failures in the aspect of meeting the expectations of both the customers and the company (Chidambaram & Ramachandran, 2012; Kheng et al., 2010). Lau and Cheung (2013) specifically explained that meeting the expectations of the customers will not only provide customer satisfaction but also develop customer loyalty that will then lessen the cases of customer loss rates or improve the retention rate. Service quality delivery is considered an important factor to consider in establishing customer satisfaction and the relationship that will be developed between the company and the customers (Amin & Isa, 2008).

Customer Loyalty

There are various definitions of customer loyalty, and one of those refers to the behavior developed by the customer, which is called repurchase behavior, thereby accounting for all the experiences that customers have encountered throughout the usage of the products and services from providers. The use of loyalty strategy has proved to increase customer retention level while reducing marketing costs (Stan et al., 2013). Accordingly, in the study of Pasha and Waleed (2016), findings revealed that perceived value, service quality, and brand have a significant impact on customer quality in the Pakistan banking sector. Many other studies have been developed to determine the antecedents of customer loyalty considering that customer loyalty may vary based on many predictors. Yee et al. (2011) revealed that service quality, customer satisfaction, and employee loyalty have a positive influence on customer loyalty, especially in the high-contract service industry. Moreover, Otaibi and Yasmeen (2014) attempted to study perceived service quality and customer satisfaction, which affect Saudi customer loyalty, and reviewed relevant previous studies that investigated the relationships among the said three variables.

Service Quality and Customer Satisfaction

Many studies have established the relationship between service quality and customer satisfaction. Companies and organizations strive hard to achieve high customer satisfaction, especially those companies that consider a long-term relationship with customers as an asset. However, understanding the service quality components remains to be a subject of discussions and arguments. For instance, in the retail banking sector, customer satisfaction has become a key consideration for successful business operations although identification of service quality characteristics may not be fully understood (Belás & Gabčová, 2016; Chavan & Ahmad, 2013). So, the model introduced by Parasuraman et al. (1982) has been accepted by many authors to be a predictor variable of customer satisfaction, which was utilized by the Herington and Weaver (2009) study, where they established the relationship between service quality dimension and customer satisfaction was regarded as a positive relationship. As a result, perceived service quality has been widely considered as an antecedent of customer satisfaction and previous studies have ascertained its relationship (Naik et al., 2010; Yee et al., 2011).

However, there are still arguments and disagreements on the causal relationship between the two variables as applied in different settings. Three major possibilities had been explored by Brady et al. (2002) regarding the relationship: First, service quality is the antecedent of customer satisfaction; second, customer satisfaction is the cause of service quality (Bitner, 1990); and third, there is no significant relationship between service quality and customer satisfaction (Dabbolkar, 1995). These three positions may have a varied impact on the results of the study and other studies, although in general consensus, many researchers have found the relationship between the two variables where the service quality served as an antecedent to customer loyalty in a dominant position as applied to the service industry context such as the banking sector (Akhtar et al., 2011; Cameran et al., 2010).

Customer Satisfaction and Customer Loyalty

Evidence showed that there is a significant relationship between customer satisfaction and customer loyalty (Leninkumar, 2017). Customer loyalty is considered a result of customer satisfaction, when customers who have good experiences with the service of the company will continue to deal with the company viewing it as less risky, thereby making them loyal and rational in decision-making. In fact, many authors have advocated that customer satisfaction is one of the determinates of customer loyalty, especially in the service industry (Belás & Gabčová, 2016; Coelho & Henseler, 2012). According to Munari et al. (2013), satisfaction and loyalty are the components of ultimate loyalty, and satisfaction is the starting point of loyalty.

Furthermore, it can be assumed that the relationship between customer satisfaction and customer loyalty is nonlinear. Suggestions from Heskett et al. (2008) pointed out the importance of firms to increase the level of customer satisfaction if they want to sustain the level of customer loyalty. As evident, previous studies have already confirmed the significant positive relationship between service quality and customer loyalty by utilizing customer satisfaction as the mediating variable (Chodzaza & Gombachika, 2013; Chu et al., 2012). Moreover, in the banking industry, the same results have been identified: that customer satisfaction mediates the relationship between service quality and customer loyalty (Hassan et al., 2013; Lee & Moghavvemi, 2015).

Framework of Analysis

Five dimensions of service quality and loyalty were discussed in the previous section. This section presents a diagrammatic illustration of the theoretical framework. The conceptual framework (Figure 1) was developed following various empirical and theoretical studies such as Agus et al. (2007), Caruana (2002), and Khan and Fasih (2014). In a diagrammatic format, it shows the predictor variable, the five service quality dimensions, namely, tangibles, reliability, responsiveness, assurance, and empathy, whereas the customer satisfaction will serve as the mediating variable. Customer loyalty will be the dependent variable. The relationships among customer satisfaction, customer loyalty, and service quality dimensions will be examined by the correlation analysis, and the impact of service quality on customer satisfaction will be analyzed by the regression analysis.

Conceptual framework of the impact of service quality on customer loyalty and customer satisfaction.

There is a significant positive relationship between customer satisfaction and service quality (Muyeed, 2012; Ndubisi & Wah, 2005). Similarly, service quality enhances customer loyalty in a direct way where customer satisfaction variable plays a mediating role (Kaura et al., 2015).

Research Method

A quantitative research approach was utilized in this study with the well-structured survey questionnaire to test the SERVQUAL model. The quantitative approach was applied to assess the relationship between service quality, customer satisfaction, and customer loyalty. It also measures the relationship between the service quality variables and customer satisfaction through regression and correlation analyses.

Sampling Design and Sample Size

This study primarily utilized convenience sampling with 120 questionnaires and were distributed equally to the customers of the four main Islamic banks in Oman, namely, Bank Nizwa, Alizz Bank, Maisarah Islamic Banking Services, and Al-Yusr Islamic Bank. The use of convenience was done because of the accessibility of the respondents and the proximity to the researcher.

Research Instrument

In this study, the survey questionnaire is divided into two parts. Part 1 consists of the demographic profile of the respondents such as respondents’ age, gender, monthly income, level of qualification, and the present service offering by the respondent banks. However, Part 2 comprises the customers’ perceptions on the extent of agreement in the application of service quality dimensions, the level of agreement on customer satisfaction, and customer loyalty of the Islamic banking service providers in Oman. Five Likert-type scales were utilized to address the questions in Part 2 to determine the extent of responses with numerical equivalent and interpretation (Jalagat et al., 2017): 1 = strongly disagree, 2 = disagree, 3 = neutral, 4 = agree, and 5 = strongly agree.

Data Analysis Method

The data collected from the sample were analyzed using descriptive statistics, SPSS Version 22. The respondents’ profiles such as age, gender, monthly income, level of qualification, and the present service offering by the respondent banks were analyzed using the frequency and other numerical descriptive statistics. In dealing with the relationship between the three variables, namely, service quality, customer loyalty, and customer satisfaction, the correlation coefficient will be used. Finally, regression analysis will be applied to determine the relationship between the five service quality dimensions and customer satisfaction.

Research Validity and Reliability

To test the validity, the questionnaire was examined for content from a pool of experts to ascertain that all components that should be measured will be considered, and pretesting has been done to make sure that the questionnaire attends to the degree of fairness and accuracy. While determining whether the instrument is reliable, Cronbach’s alpha was used to measure the total number of 38 items distributed to service quality dimensions, customer satisfaction, and customer loyalty, and the result shows .937, which is beyond the .70, as the considered acceptable reliability (Nunnally, 1978). Hence, the instrument is highly reliable.

Data Analysis and Interpretation

This section presents the data analysis and interpretation of the data collected. It shows the statistical tools to be used such as the frequencies and tables, weighted mean standard deviation, correlation, and regression analyses.

Demographic Profile of the Respondents

Table 1 depicts the classification of respondents according to age. Most of respondents or 48% (N = 58) belong to age bracket 31 to 40 years, whereas 33% (N = 40) are aged 21 to 30 years. About 17% of the respondents are within 41 to 50 years of age, and the least is shared between ages below 20 years and above 50 years, with 0.8% each. This can be interpreted as Islamic banking has gained more interest in the age group 31 to 40 years old. The data imply that more respondents who participated in the survey are male with 70.8% (85 out of 120), whereas females comprised only 29.2% (35 out of 120).

Age of Respondents.

Table 2 shows the distribution of respondents in terms of their monthly income. From the table, it is clearly revealed that the highest percentage of respondents (37.5%) received salaries between RO1,000 and RO1,499 and this is followed by those respondents (30.8%) who are paid within RO500 and RO999. Very close to this rating are respondents who are having RO1,500 and more as salaries at 28.3% and, finally, only 3.3% responded that they receive only RO0 to RO499 monthly.

Monthly Income of Respondents.

Figure 2 reflects the services currently offered by the respondent banks. Results displayed that banks are using both online (36.7%) and mobile (36.7%) banking with the same rating. This is followed by an automated teller machine (ATM)/cash deposit machine (CDM) services with a 24.2% rating, and finally, traditional banking with 2.5%. This can be interpreted as the services of a bank are upgraded in line with the advances of technology and provide the customers with comfort and convenience.

Banking tools of current services.

Results from Table 3 indicate that the respondents mostly agree that the respondent banks have enough tangibles as the results are within 3.50 to 4.49 = agree interpretation, except for statement number 5 that says “The bank has enough availability for customer parking,” which has a “Neutral” response, with a mean rating of only 3.10. Specifically, the highest mean rating is 4.03, which means that the respondent banks have enough tangibles, followed by 3.98 mean ratings that the banks are equipped with good facilities, well arranged, and spacious. There is also evidence of signage, cleanliness, and the like (3.96), and pleasant and enough lobby (3.84), whereas the parking space is not agreeable to the respondents with “Neutral” responses. This may indicate that the respondent banks have taken due consideration of the physical requirements in serving their customers.

The Extent of Agreement in the Application of Service Quality Dimensions—Tangibles.

Table 4 displays the extent of application of service quality dimensions in terms of reliability. Generally, all responses to these statements agree within (3.50–4.49) mean ratings. First, respondents agreed that the bank is physically secured with monitoring devices (3.95), followed by the response to the statement that customers’ transactions and records are kept with confidentiality (3.90). The bank staff is prompt in service delivery (3.79) and service with accuracy (3.67). Finally, the banks have observed and maintain an error-free service to their customers (3.62). These results may imply that the services provided by the respondent banks are reliable with good trust ratings. Furthermore, the banks have also set the preference for security measures to ensure the safety of the customers and their deposits.

The Extent of Agreement in the Application of Service Quality Dimensions—Reliability.

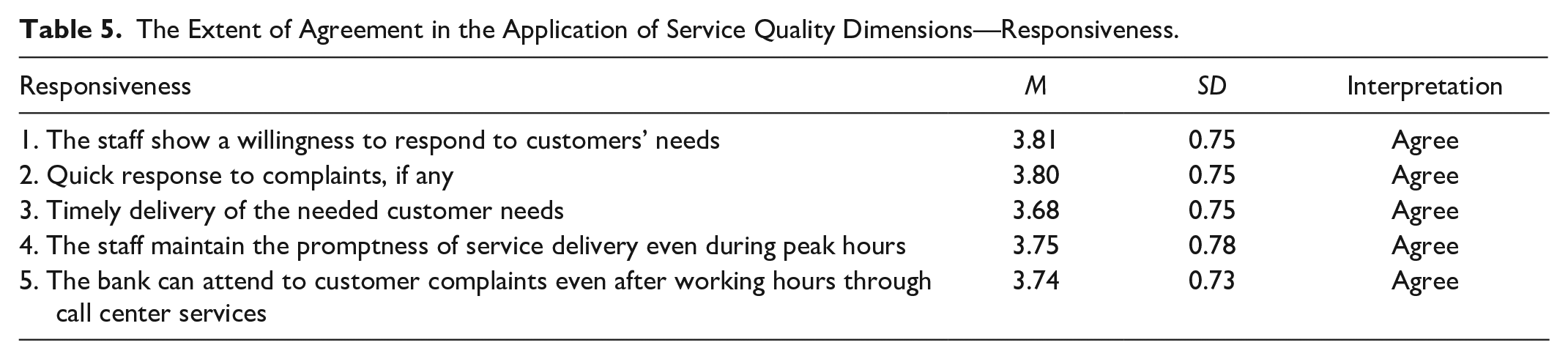

Table 5 reflects the extent of responsiveness of the respondent banks to its customers as a service quality dimension. In general, all remarks are agreed to the five statements mentioned. Individually, topping the list is the statement, “The staffs show a willingness to respond to customers’ needs” (3.8167, mean rating), followed by the quick response to complaints with a mean rating of 3.8000. The staff also maintain promptness in service delivery (3.7500) as well as attend to customer complaints even after working hours (3.7417). Last in the list is the timely delivery of customer needs (3.6833). These findings show the responsiveness of the respondent banks to customer needs on time, with promptness and willingness to act for the benefits of the customers.

The Extent of Agreement in the Application of Service Quality Dimensions—Responsiveness.

Correlation and Regression Analysis

The statistical tools, namely, the correlation and regression analyses, were utilized in this study to test the hypothetical assumptions among the three variables: service quality, customer satisfaction, and customer loyalty. Regression analysis, however, was used to determine the relationship between service quality dimensions and customer satisfaction. According to Rumsey (2010) and as cited in the study by Jalagat et al. (2017), the interpretation of correlation coefficient (r) measures the strength of the relationship between variables, where the value of r is between +1 and −1. Accordingly, −1 suggests a perfectly downhill negative relationship, whereas +1 is a perfectly uphill positive relationship; −.70 signifies a strong downhill negative relationship, whereas +.70 is a strong uphill positive relationship; −.50 means moderate downhill negative relationship, and 0 means no linear relationship. However, regression analysis is tested at .05 level of significance.

Table 6 depicts the correlation analysis between the three variables. From the result, it is clearly shown that there is a positive relationship between the variables, namely, service quality, customer satisfaction, and customer loyalty, at p < .01 level of significance. Specifically, there is a strong positive relationship between service quality and customer satisfaction with r = .652 at p < .01, whereas there is a moderate positive relationship between service quality and customer loyalty (r = .488). However, between customer satisfaction and customer loyalty, there is also a strong positive correlation at r = .602. The findings reject the null hypothesis that there is no relationship between these variables. This implies that these three variables should be continuously emphasized by the respondent banks in their operation because of their significance to the possible growth of Islamic banking in the country. These results were also consistent with previous studies that affirmed the relationship between service quality and customer satisfaction (Jalagat, et al, 2017; Parasuraman et al., 1988). Moreover, it also agrees with the findings of the study done by Hamzah et al. (2015) for Malaysia that service quality has a direct and positive relationship with customer satisfaction.

Correlation Analysis of the Relationship of Variables: Service Quality, Customer Satisfaction, and Customer Loyalty.

Correlation is significant at p < .01 (two-tailed).

However, the relationship between customer satisfaction and customer loyalty was also supported by many studies, thereby demonstrating a positive relationship by considering customer satisfaction as one of the most popular determinants of customer loyalty (Flint et al., 2011; Tsai et al., 2010). In fact, many studies have affirmed that customer satisfaction is one of the important variables for customer loyalty (Gillani & Awan, 2014; Hall, 2011).

In Table 7, the model summary of the regression analysis shows r = .695 and r² = .483, and with a standard error of 0.40110. This entails that according to the r² value, about 48.3% of the independent variables of service quality dimensions explain the variation of the dependent variable, which is customer satisfaction. This is considered moderate considering the relatively limited number of respondents in this study. However, in determining the adequacy of the model, the analysis of variance (ANOVA) results with a value F = 21.31 and significance at p < .010. Surprisingly, of all the service quality dimension variables, only empathy and responsiveness significantly related to customer satisfaction with p < .010 and p < .10, respectively. This means that the variables, namely, tangibles, reliability, and assurance, do not significantly affect the provision of service quality as applied to the respondent banks in this study. In order of preference, empathy has the highest significance, followed by responsiveness. This finding contradicts various studies that concluded that empathy has the lowest significance to customer satisfaction (Devi Juwaheer & Lee Ross, 2003; Jonsson & Klefsjö, 2006).

Regression Analysis Between Service Quality Variables and Customer Satisfaction.

Predictors: (constant), empathy, tangibles, reliability, responsiveness, assurance. b Dependent variable: customer satisfaction. c Predictors: (constant), empathy, tangibles, reliability, responsiveness, assurance. d Dependent variable: customer satisfaction.

However, in the study conducted by Siddiqui (2010) on the banking industry in Bangladesh, the result is consistent with the study where empathy has the highest correlation and followed by responsiveness and assurance. This may indicate that in service industries, empathy and responsiveness are more important than other variables. In a study on the Malaysian banking industry, empathy is also proven to have the highest influence on customer satisfaction (Kheng et al., 2010). Finally, Mengi (2009) also concluded that responsiveness is more significantly related to customer satisfaction. In summary, although service quality significantly relates to customer satisfaction, in this study, only two variables are significant, which are empathy and responsiveness that vary from other previous study findings.

Conclusion and Recommendation

This study investigated the impacts of service quality on customer satisfaction and customer loyalty for selected main Islamic banking institutions in Oman using the SERVQUAL model. Based on the findings, it has been revealed that the application of three important factors, the service quality, customer satisfaction, and customer loyalty variables, significantly relate to each other. The affirmation from previous studies conducted on their relationship still holds, with emphasis that as the service quality increased, the levels of customer satisfaction and customer loyalty also increased (Flint et al., 2011; Gillani & Awan, 2014; Hall, 2011; Mittal & Kamakura, 2001; Tsai et al., 2010). The mean values from the results described the level of service provided by the respondent banks, which mostly solicited an agree response, which means that the respondents are satisfied with the current service provision. However, the outcome from regression analysis divulges that empathy and responsiveness are the two variables that need preferable attention by the respondent banks, whereas other variables may be given second priority (Kheng et al., 2010; Mengi, 2009; Siddiqui, 2010). Although these variables are not significant in the study, it does not mean that the respondent banks should neglect their importance as many other studies have confirmed their significance.

Based on the findings and conclusion of the study, the following recommendations can be presented.

The respondent banks should try to improve their current services to at least a very satisfactory level considering that the responses from customers posit only agree responses. Considering the significant relationship between service quality, customer satisfaction, and customer loyalty, more emphasis on improvement will further enhance the customers’ favorable feedback.

The utmost priority of the respondent banks should rest on empathy and responsiveness, considering the significant relationship of these two variables on customer satisfaction. However, they should not neglect the importance of other variables such as reliability, assurance, and tangibles because mean ratings suggest that the respondents agree on the bank’s provision in these three dimensions.

The provision and availability and parking space have been identified in this study as a problem. There is a need for the respondent banks to consider this on an urgent basis as it will also affect the service quality provided to the customers. Likewise, continuous improvement is recommended for current services particularly online and mobile banking services to make them accessible and convenient for customers.

Considering that Islamic banking in Oman is relatively new and future studies could be conducted considering benchmarking wherever applicable to other service industries, a comparison of conventional banking and Islamic banking and applying the SERVQUAL gap model for the industry is needed.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.