Abstract

The study examines the significant factors affecting the capital structure decisions for banks’ in MENA region. An unbalanced panel data comprising of 132 banks operating in fifteen different countries of the MENA region from 2012 to 2017, data was extracted from Bank Scope resulting in 891 bank year observations. Macroeconomic indicators and institutional characteristics data has been taken from World Bank and World Bank governance indicators database and financial freedom data has been collected from heritage foundation. We use the two-step system Generalized Method of Moments (GMM) to explore the relationship between dependent and explanatory variables. The regression outcome between profitability and leverage shows a negative and significant relationship. No significant association between tangibility and leverage is found. Earnings volatility is negatively and significantly related to leverage. The relationship between growth and leverage is negative and significant. Macroeconomic indicators GDP growth and inflation show a positive relationship with leverage. Finally, the institutional factors, that is, government effectiveness, political stability, and rule of law have positive association with leverage. The study results will lend a hand to bank managers to make value-maximizing financing decisions to achieve an optimal capital structure. It will also help the policymakers to articulate an effective regulatory framework in the region. As per our knowledge, this is the first study to explore the determining factors of capital structure for banks operating in the MENA region. Moreover, the findings from MENA region banks could also support the comparative study with other regional blocks.

Introduction

The debate on optimal capital structure, that is, mix of equity and debt, particularly the long-term, is inconclusive for a long in the existing corporate finance literature. The empirical literature reported contradictory findings not only for non-financial firms but also for financial firms in recent studies. This phenomenon is common for businesses operating in different developing and developed economies. In contrast to non-financial firms, very few studies have examined financial firms’ capital structure, particularly for banks. The banks’ removal was primarily due to the reason that the banks’ decision-making process is influenced by several domestic and international regulatory frameworks. Hence, the banks’ financing decisions not only depend on management discretion but also on the regulatory framework. Despite this contradiction, several studies such as a study on US banks by Diamond and Rajan (2000), a study on US and European banks by Gropp and Heider (2010), a study on Pakistani banks by Sheikh and Qureshi (2017), and Khan et al. (2021) study on Saudi banks have explored the factors affecting the financing decisions of banks. However, these studies also reported mixed results.

The capital structure debate has been started with the “debt irrelevance theorem” proposed by Modigliani and Miller (1958) in their seminal work. They proposed that the choice between debt and equity in frictionless capital markets is irrelevant. Later on, they introduced the tax advantage on the use of debt (see Modigliani & Miller, 1963). Centered on the tax shield assumption, Kraus and Litzenberger (1973) put forward the trade-off theory. Later on, Jensen and Meckling (1976) proposed agency theory and highlighted various agency costs and potential agency problems related to each source of financing. In continuation focusing on the role of information asymmetry pecking order theory emerged from the work of Myers (1984), Myers and Majluf (1984). It suggests that firms should initially use internal funds followed by debt and equity in last if external financing is desired. Jensen (1986) suggested that despite the threat of financial distress higher debt level contributes to the value of a firm, and named it the free cash flow hypothesis. Finally, the market timing theory proposed by Baker and Wurgler (2002) emphasized on the actual market situation for choosing debt or equity financing.

Traditionally numerous corporate finance studies explored the determining factor of non-financial firms’ capital structure, compared to financial firms. Therefore, Gropp and Heider (2010) stated that “what determines banks’ capital structure?” In response to this question, they borrowed the explanation from the empirical literature of non-financial firms’ studies to understand the factors affecting the capital structure choice of banks. Likewise, their study concluded that the similarities between the choices of non-financial firms and banks are likely to be more than previously assumed.

Based on different theories of capital structure various empirical studies have explored several other aspects of the financing choices of non-financial firms. Such as determinants of capital structure (see Booth et al., 2001; Frank & Goyal, 2009; Sheikh & Wang, 2013; Wald, 1999) capital structure and firms’ performance (see Dawar, 2014, Khan, 2022a; Sheikh & Wang, 2013) impact of ownership structure on firms’ capital structure (see Brailsford et al., 2002; Shoaib & Yasushi, 2015, 2016; Wahba, 2014).

The relative importance of optimal capital structure is of more concern to practitioners and researchers since the banks’ led financial crises in 2008. Theoretically, high leverage could take the firm into financial distress, and for banks, it could lead to bank runs. Moreover, the role of banks as financial intermediaries to match the supply and demand of capital in an economy is primary for the growth of various industrial sectors and the economy as a whole (see Ching et al., 2016). By considering the above-mentioned background, the exploration of factors affecting the capital structure of MENA region banks is of great importance since most of the economies have transformed from centrally planned economies to market-oriented economies during the last three decades.

This study focuses on exploring the factors affecting the financing choices of the banks operating in the MENA region, where the capital markets are less developed and banks are the dominant source of finance. The mixed findings from a handful of studies about the capital structure of banks around the globe (see Al-Hunnayan, 2020; Khan, 2022b; Khan et al., 2021; Sheikh & Qureshi, 2017) have encouraged the need for this study on the MENA region. Moreover, like the rest of the developing countries, the economies in the MENA region are also working on the liberalization of their financial sector to achieve their economic goals. Therefore, it is assumed that the current study not only helps to understand the banks’ capital structure of the MENA region but also will lend a hand to policymakers to evaluate different financial policies that could enhance the economic growth of the region. Hence, this study aims to strive for the answers to the following questions by adding empirical evidence of banks operating in the MENA region.

Q1. What are the determining factors of MENA region banks’ capital structure?

Q2. Do these components of the capital structure in MENA region banks are similar to other economies or different?

Overview of Banking in the MENA Region

The MENA region has strategic importance in the global economy, it has borders connected to European and Asian regions. It represents the oil-rich economies of the GCC (Gulf Cooperation Council) and Arab economies of the Near East and North Africa. The region’s population and wealth are also rapidly growing. According to World Bank, the collective GDP of the MENA region economies were 3.65 trillion US dollar in 2019, which is approximately 4.5% of the total world’s GDP. The region is categorized as a middle-income region and is enriched with natural resources. Nine out of 15 members of OPEC (Organization of the Petroleum Exporting Countries) belong to MENA region. Therefore, the region has significant importance and contribution to the global economic outlook.

According to World Bank Enterprise Survey, the financial sector in the MENA region on the supply side is dominated by banks. Where the credit is highly concentrated to fewer larger clients. According to Arezki and Senbet (2020), the financial system in the MENA region is highly bank centered compared to the stocks and bonds market. Moreover, due to the state intervention in several MENA region economies, there is very limited capital available for small and medium enterprises disposal. They further argued that the banking sector in the region is less diversified and follows a rent-seeking model, except in the GCC countries where the banking sector is relatively developed compared to other developing countries. According to World Bank, the capital markets and banking sector in the MENA region is significantly underdeveloped as compared to the developing world with few exceptions. For instance, the stock market capitalization in the MENA region is around 42% of the GDP where it is 179% of the GDP in the East Asian region (see Arezki & Senbet, 2020).

According to Olson and Zoubi (2011) banking sector in the MENA region is relatively young where most of the banks are established after the 1970s since then conventional and Islamic banking grows in the region with the presence of the largest Islamic banks. Therefore, this study explores the factors affecting the financing decision of conventional banks in the MENA region, to explore whether these factors are similar to the factors explored in other studies. Harris and Raviv (1991), suggested considering the firms’ local operating environment for future empirical studies on capital structure. Therefore, this study on MENA region banks’ data will add new empirical evidence to the current literature. To find out the determinants of banks’ capital structure in MENA region the study uses an unbalanced data set of 132 banks operating in fifteen countries of the MENA region, from period 2012 to 2017 with total of 891 banks year observations. The significance of the study is that its findings could help to understand the financing choices of banks’ which could contribute to the financial sector development of the region. Theoretically, it is assumed that financial sector development enhances the efficient allocation of capital through financial intermediation to various economic sectors. Moreover, the banks’ management will maximize the shareholders’ value by choosing the optimal capital structure. This will further contribute to the development of capital markets in the region.

Following the introduction and overview of banking in MENA region, the remaining paper follows the following structure. Section 3 provides the relevant literature review, data, and research methods are explained in section 4. The results of the study are presented in section 5 followed by the discussion on the results in section 6. Finally, section 7 presents the conclusion and future research recommendations.

Literature Review

Miller (1995) answered “yes and no” to the question “do M&M propositions apply to banks?” Likewise, Diamond and Rajan (2000, p. 2431) stated “does bank capital structure matter, and if so, how should it be set?” They suggested that for banks’ capital structure stylized facts from industrial firms cannot be used due to the fact that bank assets and functions are different from other firms. On the contrary, the study on 200 largest US and European banks by Gropp and Heider (2010) reported certain similarities between banks’ and non-financial firms’ financing structure. According to Rajan and Zingales (1995), the theories of capital structure have departed from the irrelevance proposition of Modigliani and Miller (1958) to its relevance for a firm’s value. Regarding the different provisional theories of capital structure, Frank and Goyal (2009) stated that “many theories of capital structure has been proposed only a few seem to have many advocates.” Among them, notable models are the trade-off model, pecking order theory, agency theory, and market timing hypothesis. Hence, there is extensive empirical evidence in relevance to these theories (see Frank & Goyal, 2009; Harris & Raviv, 1991; Rajan & Zingales, 1995; Sheikh & Wang, 2013). However, very little empirical evidence exists relevant to capital structure theories on banks’ data, even though theoretical assumptions do not differentiate between industrial and financial firms.

According to Flannery (1994), short-term debt due to its less risky nature plays an important role in US commercial banks’ financing choices, compared to other US financial intermediaries. While Diamond and Rajan (2000) observed the functions of bank and its’ capital for optimal capital structure. They further pointed the “three trades-off of capital, more capital increases the rent absorbed by the banker, increases the buffer against shocks, and changes the amount that can be extracted from borrowers” (Diamond & Rajan, 2000, p. 2433). Additionally, stated that a bank’s financing structure affects the credit creation and liquidity of a bank against its stability, and capital structure is largely determined by the asset side of the bank’s balance sheet. This infers that sound capital structures arise from stable asset structure. Allen et al. (2011) also endorsed this argument and stated that a bank’s capital structure is not affected by regulation.

The study by Amidu (2007) examined the Ghanaian banks’ capital structure and reported that bank size, growth, profitability, asset structure, and corporate taxes affect the financing decision of the banks in Ghana. In another study on large European and US banks, Gropp and Heider (2010) concluded that regulatory framework has secondary importance for banks’ capital structure decisions. Moreover, banks are highly leveraged than industrial firms and found no effect of deposit insurance coverage on banks’ capital structure. In the case of a developing economy, that is, Pakistan, Sheikh and Qureshi (2017) investigated the factors affecting the financing structure of conventional and Islamic banks. They stated that Islamic and conventional banks select capital structure in their own ways, but it is affected by the same variables that influence the choices of non-financial firms and reported profitability, tangibility, growth, and bank size as determinants of capital structure.

Al-Hunnayan (2020) investigated 12 Islamic banks operating in GCC region from 2005 to 2014. They also reported that growth opportunities, bank size, profitability, assets tangibility, and financial market development have material effect on the capital structure (leverage) of Islamic banks. As per their findings, GCC Islamic banks follow the pecking order theory hypothesis and use internal funds to minimize the transaction cost. Likewise, Khan et al. (2021) explored the determinants of 11 Saudi listed commercial banks and stated that Saudi banks’ capital structure is influenced by similar factors as of non-financial firms but unique in nature. In line with earlier studies, they also reported that profitability, growth opportunities, bank size, tangibility, and earnings volatility as determining factors of Saudi banks’ capital structure.

In summary, the factors that affects the banks’ capital structure decision reported by Amidu (2007) study on Ghana, Gropp and Heider (2010) on US and European banks, Sheikh and Qureshi (2017) on Pakistan’s Islamic and conventional banks, Al-Hunnayan (2020) study on GCC Islamic banks, and Khan et al. (2021) on Saudi commercial banks had similarity with factors of non-financial firms. All these studies reported banks’ book leverage is influenced by the same factors that were reported by Rajan and Zingales (1995) study on public firms of G-7 countries and Frank and Goyal (2009) study on US listed firms. The most significant factors that have a material impact on capital structure proxy i.e. leverage as reported by earlier studies (see De Jong et al., 2008; Frank & Goyal, 2009; Gropp & Heider, 2010; Khan et al., 2021; Rajan & Zingales, 1995; Sheikh & Qureshi, 2017) are profitability, firms’ size, tangibility (nature of assets), earnings volatility, and growth opportunities.

Profitability

The theories of capital structure are based on diverse prophecies that predict different nature of the relationship between firms’ profit and their financing choices. Trade-off theory advocates the use of higher debt levels for profitable firms to attain higher tax-saving benefits related to debt. Contrary to this, firms with no profit rely on equity financing. Hence, this theory assumes a positive association between profitability and leverage. Frank and Goyal (2009) suggested that considering the bankruptcy cost and tax benefits, profitable firms are likely to choose debt. Similarly, Jensen (1986) as per agency cost perception suggested the usage of debt as a discipline tool for profitable firms to avoid free cash problems. Pecking order theory based on information asymmetry advocates the use of internal funds followed by debt and finally the equity. It assumes that this way firms could avoid sending negative information to the market. Several empirical studies in line with the pecking order assumption reported a negative association between leverage and profitability. Such as Titman and Wessels (1988), Rajan and Zingales (1995), Wald (1999), Booth et al. (2001), De Jong et al. (2008), Viviani (2008), Frank and Goyal (2009), Sheikh and Qureshi (2017), Khan et al. (2021).

Like non-financial firms, empirical studies on banks’ capital structure reported mixed findings. Berger and Di Patti (2006, p. 1069) supported the agency cost hypothesis, that is, “higher leverage or a lower equity capital ratio in banking is associated with higher profit efficiency.”Amidu (2007) reported a negative association between profitability and leverage in the case of Ghana banks. Likewise, Gropp and Heider (2010) in the case of European and US banks and Sheikh and Qureshi, (2017) study on Pakistani conventional and Islamic banks also reported a negative relationship. Khan et al. (2021) and Al-Hunnayan (2020) also reported similar findings on the study of Saudi commercial and GCC Islamic banks respectively.

Bank Size

Existing theories and empirical literature consider the size of the firm as an influential factor in financing decisions. Basically, larger firms are assumed to be diversified with sufficient financial resources, hence less susceptible to financial distress or have lower default risk. Therefore, trade-off theory predicts a negative association between leverage and firm size. Likewise, agency theory suggests the usage of debt as a tool to mitigate the agency problems related to monitoring and free cash. Contrary to this, pecking order theory suggests the use of internally available funds, if available predicting a negative relationship between leverage and debt. However, advocating the use of debt if external funds are required. Thus theoretically, the nature of the relationship is mixed and inconclusive.

According to Rajan and Zingales (1995), firm size and debt are positively related and reported a positive association between a firm’s size and leverage in G-7 countries except for Germany. Moreover, the following studies have reported a positive association between size and leverage, Booth et al. (2001), Fama and French (2002), De Jong et al. (2008), Frank and Goyal (2009), Belkhir et al. (2016). Chen (2004) reported a positive but insignificant association between leverage and the size of Chinese firms. Likewise, studies on financial firms especially banks also reported mixed results. Amidu (2007) reported that short term debt and total debt are positively related to bank size and negative relationship between bank size and long-term debt. The following studies also reported a positive association between bank size and leverage, Gropp and Heider (2010), Sheikh and Qureshi (2017), Khan et al. (2021), and Al-Hunnayan (2020).

Tangibility

Nature of the assets owned by the firms particularly the availability of tangible/physical asset is also considered as one of the important firm’s specific factor that has an impact of financing decision. According to Frank and Goyal (2009), the outsiders of the firm can easily do the valuation of tangible assets (e.g. plant, property, machinery, etc.) compared to intangible and risky assets (e.g. goodwill) which can reduce the distress cost. Moreover, the usage as collateral for debt and higher value on liquidation properties of tangible assets, trade-off theory predicts firms’ physical assets inclines towards higher borrowing. However, Gropp and Heider (2010) stated that banks hold less collateral compared to non-financial firms. Pecking order theory postulate that tangible assets reduce the information asymmetry that results into lower cost of equity. According to Rajan and Zingales (1995, p. 1451) “If a large fraction of a firm’s assets is tangible, then assets should serve as collateral, diminishing the risk of the lender suffering the agency costs of debt (like risk shifting). Assets should also retain more value in liquidation.” This further increases the lender’s confidence which results into higher leverage. According to Long et al. (1992), collateralization of assets could reduce the moral hazard and adverse selection problems.

Like theories, empirical evidence also reports mixed results. Rajan and Zingales (1995) reported an increase in leverage with the increase of physical assets in G-7 countries. Titman and Wessels (1988), Wald (1999), Chen (2004), De Jong et al. (2008), and Belkhir et al. (2016) also reported the positive association. Empirical study on banks by Gropp and Heider (2010) found positive impact of nature of assets on book and market leverage. Amidu (2007) also reported positive association between leverage and tangibility in the case of Ghanaian banks. Contrary to this, Shibru et al. (2015) study on Ethiopian banks, Sheikh and Qureshi (2017) study on Pakistani conventional and Islamic banks, Khan et al. (2021) study on Saudi commercial banks, and Al-Hunnayan (2020) study on GCC Islamic banks found negative association between tangibility and leverage.

Earnings Volatility

Existing literature suggests that debt level decreases with the increase in earnings’ volatility for an optimal financing mix. Trade-off theory and pecking order theory predict a negative association between volatile earnings and leverage. Hence, stable earning firms are assumed to borrow more compare to volatile earnings firms. Moreover, firms with non-stable earnings may fail to meet the debt’s contractual obligations and fall into financial distress. According to Fama and French (2002, p. 5) as per the prediction of the pecking order theory, “firms with more volatile net cash flows are likely to have lower dividend payouts and less leverage.” Like other firm’s factors, empirical literature reported mixed findings.

Empirical evidence on the effect of volatile earnings on debt is also inconclusive. For instance, Titman and Wessels (1988) and Chen (2004) reported no effect on debt resulting from volatile earnings. Contrary to this Bradley et al. (1984) reported negative association between leverage and volatility. Likewise, Friend and Lang (1988) also reported negative relationship between the standard deviation of earnings and leverage. Amidu (2007) reported an inverse relationship between volatility and leverage in the case of banks. While Sheikh and Qureshi (2017) found positive association between volatility and leverage in conventional and no relationship in Islamic banks. Similarly, Khan et al. (2021) study on Saudi banks reported that earnings volatility is positively related to leverage.

Growth Opportunities

According to Myers (1984), companies with higher leverage ratios are likely to give up future investment opportunities, hence, the firms with growth opportunities should choose more equity. According to Titman and Wessels (1988, p. 4) “growth opportunities are capital assets that add value to the firm but cannot be collateralized and do not generate current taxable income.” However, empirically found no relationship. Trade-off theory proposes that firms with future growth prospects (intangible assets) are expected to borrow less compare to the firms with physical assets. The agency and pecking order theory also predict a negative relationship between leverage and growth opportunities. According to Lang et al. (1996) where capital markets do not recognize the future growth opportunities for firms, a negative association between leverage and growth opportunities has been found. On the other hand, Chen (2004, p. 1347) suggested that “under the signaling model generally predicts that the firms with the best earnings and growth prospects will employ the most leverage.”

Like other factors, empirical evidence on this factor also reported mixed results. Rajan and Zingales (1995) reported negative, while Chen (2004) reported a positive association between expected growth and leverage. De Jong et al. (2008) also found negative association and argued that firms with future opportunities try to keep lower leverage to capitalize the future investment opportunities. Following studies on banks, that is, Gropp and Heider, (2010), Shibru et al. (2015), Sheikh and Qureshi (2017), and Al-Hunnayan (2020) reported that growth opportunities are negatively associated with leverage. While Khan et al. (2021) found a positive relation of growth with leverage in the case of Saudi commercial banks.

Apart from above mentioned firm level factors which are used as explanatory variables, several studies have included country level economic variables. Following studies Gropp and Heider (2010), Belkhir et al. (2016), Bashir et al. (2017, 2020), and Khan et al. (2021), and so forth included GDP growth and inflation as macroeconomic variables to explore the capital structure determinants. Therefore, to capture the effect of overall economic and business activities, the study uses two macroeconomic indicators, that is, GDP growth and inflation of MENA region economies. Moreover, banks are vital economic players due to their role as suppliers and demanders of the capital (see Ching et al., 2016; Khan et al., 2021). According to Demirgüç-Kunt et al. (2004), Hussain and Bashir (2019), and Khan et al. (2016) country’s institutional characteristics significantly influence the banks’ business environment. Therefore, to control for country’s institutional characteristics study uses financial freedom, Government effectiveness, political stability, regulatory quality, rule of law indexes, which may have a direct or indirect effect on banks’ business activities.

Data, Variables, and Research Methods

Data

This study investigates the important factors that have an impact on banks’ capital structure decisions operating in the MENA region. Banks operating in Bahrain, Egypt, Iraq, Iran, Jordan, Kuwait, Lebanon, Morocco, Oman, Qatar, Saudi Arabia, Sudan, Syria, Tunisia, and United Arab Emirates (UAE) are included in the data sample. The financial data has been extracted from the Bank Scope database. The study uses the unbalanced data of 132 banks operating in fifteen different countries of the MENA region for the period of 2012 to 2017, resulting in 891 bank year observations. Macroeconomic indicators data has been taken from the World Bank. Additionally, institutional characteristics data has been taken from the World Bank governance indicators database, except data on financial freedom that has been collected from heritage foundation.

Variables

To have a meaningful comparison with the existing studies, the study adopted the variables’ definition from the existing literature. The variables are computed by following the studies of Gropp and Heider, (2010), Sheikh and Qureshi (2017) and Khan et al. (2021). Book leverage a proxy of capital structure is used as a dependent variable. These studies suggested the use of book values, since banks’ regulations are based on book values. To explore the impact on the dependent variable study uses following explanatory variables, profitability, bank size, tangibility, earnings volatility, and growth opportunities. In order to control for the impact of macroeconomic conditions on the financing choices, study employs two control variables, that is, the GDP growth rate and inflation rate. Moreover, to control for institutional characteristics study uses following five indexes as variables, that is, financial freedom, Government effectiveness, political stability, regulatory quality, and rule of law. The explanation of variables is presented in Table 1.

Definition of Variables.

Source. Author’s compilation based on Gropp and Heider (2010), Khan et al. (2016), Sheikh and Qureshi (2017), Hussain and Bashir (2019), and Khan et al. (2021).

Research Method

The final sample is panel data set, as it included banks over time. Hence in order to explore the relationship between dependent and explanatory variables, GMM methodology has been used to cope with various data issues. The econometric equation of the model is as below.

In the above equation the dependent variable (BLV) is the book to leverage for bank i at time t. The lagged dependent variable (

Empirical Results

Descriptive and Correlation Results

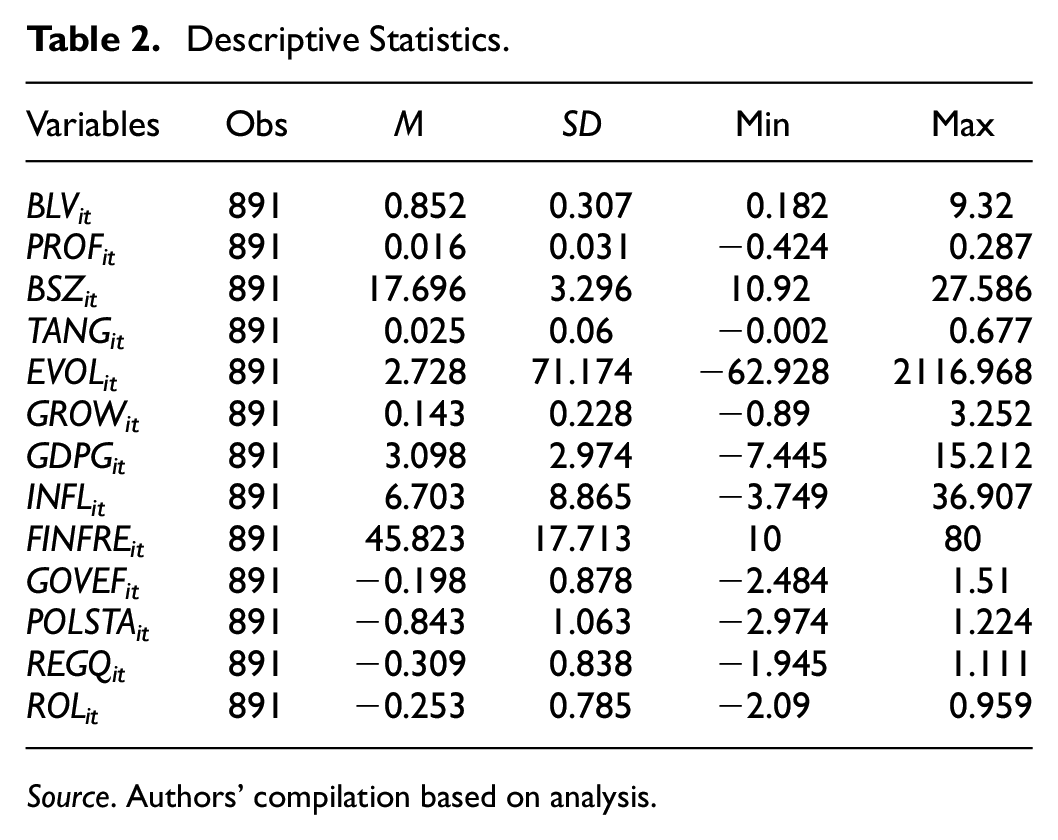

The descriptive statistics of the variables are presented in Table 2. The mean of book leverage shows that 85% of the assets of banks operating in MENA region are financed with leverage. The value of leverage is lower compared to the other studies on banks, for instance, Gropp and Heider (2010) study on Large European and US banks and Sheikh and Qureshi (2017) study on Pakistan. The mean of profitability is 1.6%, which means the profitability of the GCC banks is also lower compared to European and US banks. The mean of banks is 17.96. While the mean of earning volatility and tangibility are 2.5 and 2.78% respectively. The average GDP growth and inflation of the GCC regional economies increased at 3.09 and 6.70% annually on average.

Descriptive Statistics.

Source. Authors’ compilation based on analysis.

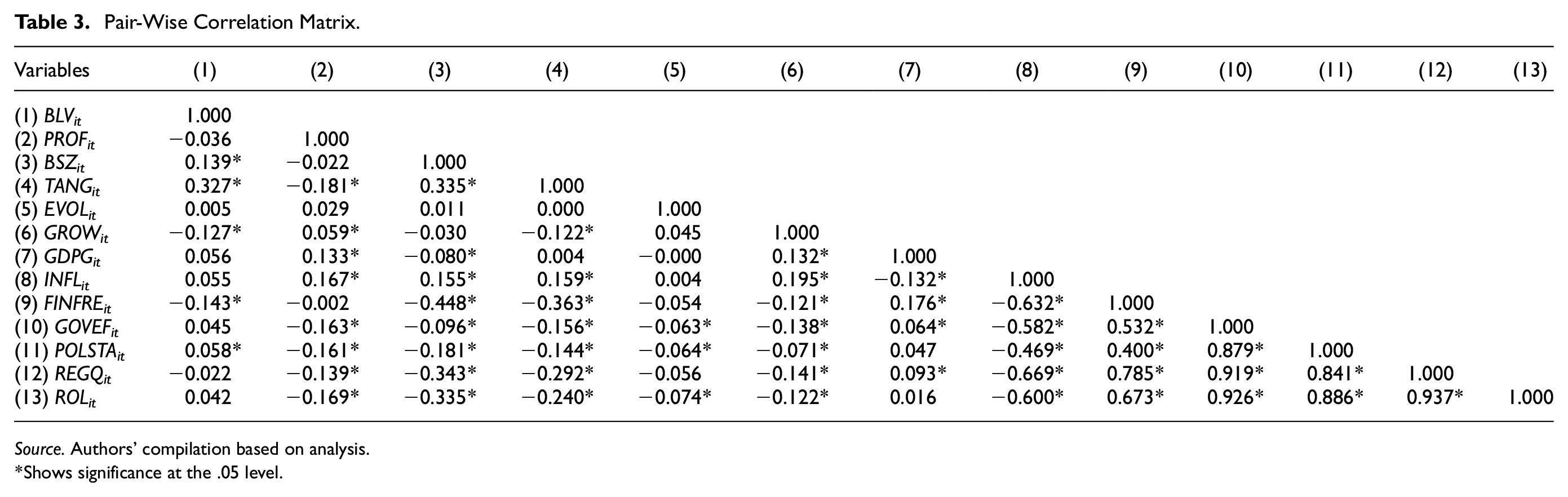

Variables Correlation

The pair-wise correlations matrix of variables is given in Table 3. Profitability is negatively correlated to book leverage and correlation is insignificant. Bank size and tangibility are positively and significantly correlated to book leverage, while both are negatively correlated to profitability but bank size correlation is insignificant and tangibility is significant. Earnings volatility is positively related to book leverage, profitability, bank size, and tangibility but the correlation is insignificant with all variables. Growth is negatively correlated to book leverage, banks size, and tangibility and correlation are significant with all except bank size, while it is positively correlated to profitability at a significant level and earnings volatility at an insignificant level. The values of variables’ cross correlations are small, hence the problem of multicollinearity among variables is negligible. In addition to this VIF (variance inflation factor) is also calculated for independent variables and mean of the VIF is 1.15, this also suggest there is no issue of multicollinearity among variables.

Pair-Wise Correlation Matrix.

Source. Authors’ compilation based on analysis.

Shows significance at the .05 level.

Regression Findings

We use dynamic panel estimation by using a two-step system GMM to examine the determinants of capital structure. The results are mentioned in Table 4. Various studies have used this method to deal with various data issues. This method can estimate unbiased results for a dynamic model and for data which has a large number of individual cross-sections and a small length of time periods which this method accommodates small (T), number of time periods, and large (N) number of cross-sections. Where explanatory variables are not strictly exogenous in nature and could be correlated with past or current terms of the error term. Dealing with issues of autocorrelation, heteroskedasticity, and time-invariant fixed effects. These types of issues are prevalent with financial data which are quite sufficient reasons for estimating our model with this methodology. This is also evident from the insignificant p-values of AR (2) in Table 4 depict no issue of serial correlation in all the estimated models and the Hansen test shows no identification issues overall, validating the econometric specification of all the models.

GMM Regression Results.

Source. Authors compilations.

Note. This table gives the estimation results using two-step system GMM as the dynamic model on the basis of bank characteristics and controlling for various macroeconomic conditions. The dependent variable is (BLEV) the measure for book leverage. Bank characteristics are given by (PROF) the profit after taxes to total assets, (BSZ) log of total assets, (TANG) Computed as ratio of fixed assets to total assets, (EVOL)is computed as ratio of (profit after taxes t − profit after taxest−1) to profit after taxest−1 to profit after taxest−1, and (GROW) ratio of market price per share to book value per share. GDPG is the gross domestic product growth rate, and INF is the CPI index measuring inflation. Financial Freedom, Government Effectiveness, Political Stability, Regulatory Requirements and Rule of Law control for country specific effects. Insignificant p-values of AR (2) depict no issue of serial correlation in all the estimated models and the Hansen test shows no identification issues overall, validating the econometric specification of all the models. Standard errors are given in parentheses.

, **, and *** denote statistical significance for p < .1, p < .05, and p < .01.

Results of the sample, while dropping the UAE and Egypt having more number of banking years in data are given in Table 5. Results are almost similar to the results of whole sample. Where there is a negative and significant association between profitability of banks and leverage. Contrary to profitability, bank’s size is positively related to leverage suggesting that larger banks’ rely on more debt compared to equity. The availability of tangible assets has a positive association with debt but the relationship is insignificant. Negative association between earnings volatility and leverage has been found but is only significant for whole sample. This suggests that variation in earnings has a material effect on banks’ debt. Growth opportunities are negatively correlated with book leverage and the relationship is significant. Results further indicate that macroeconomic indicators have positive and significant impact on the dependent variable book leverage. Among five institutional characteristic indexes government effectiveness, political stability and rule of law have significant effects on book leverage.

GMM Regression Results Dropping UAE and Egypt.

Source. Authors compilations.

Note. This table gives the estimation results using two-step system GMM as the dynamic model on the basis of bank characteristics and controlling for various macroeconomic conditions by dropping UAE and Egypt data. The dependent variable is (BLEV) the measure for book leverage. Bank characteristics are given by (PROF) the profit after taxes to total assets, (BSZ) log of total assets, (TANG) Computed as ratio of fixed assets to total assets, (EVOL) is computed as ratio of (profit after taxes t − profit after taxes t−1 ) to profit after taxes t−1 to profit after taxest−1, and (GROW) ratio of market price per share to book value per share. GDPG is the gross domestic product growth rate, and INF is the CPI index measuring inflation. Financial Freedom, Government Effectiveness, Political Stability, Regulatory Requirements and Rule of Law control for country specific effects. Insignificant p-values of AR (2) depict no issue of serial correlation in all the estimated models and the Hansen test shows no identification issues overall, validating the econometric specification of all the models. Standard errors are given in parentheses.

, **, and *** denote statistical significance for p < .1, p < .05, and p < .01.

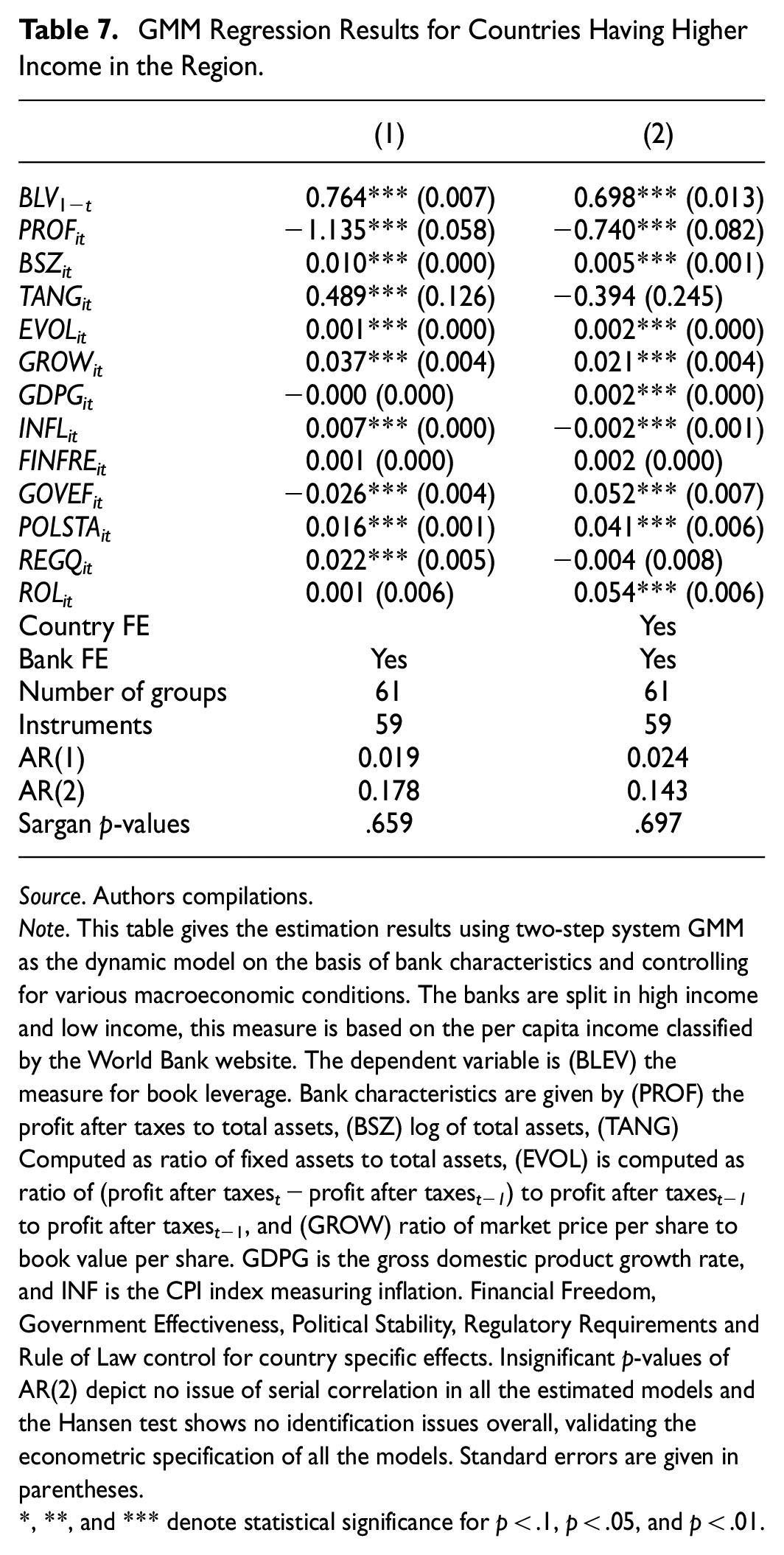

To check for robustness, the countries of MENA region are divided in to three categories based of per capita income level of the Work Bank, as shown in Table 6. Based on it analysis has been performed to explore the impact of independent variables on dependent variable on high income and low income countries. Above table is used for high low income analysis, the sample is divided as follows high income countries are grouped and rest of the countries including upper middle and lower middle and low income are grouped. The result of high income and low income countries are presented in Tables 7 and 8. The results are similar to the sample of all country except tangibility shows positive and significant relationship to book leverage. Also the earning volatility has positive and significant association with book leverage both in high income and low income countries, while it has negative association with the leverage in the case of whole sample.

Countries Classification as Per Income Level.

Source: Authors’ compilation based on World Bank’s country ranking.

GMM Regression Results for Countries Having Higher Income in the Region.

Source. Authors compilations.

Note. This table gives the estimation results using two-step system GMM as the dynamic model on the basis of bank characteristics and controlling for various macroeconomic conditions. The banks are split in high income and low income, this measure is based on the per capita income classified by the World Bank website. The dependent variable is (BLEV) the measure for book leverage. Bank characteristics are given by (PROF) the profit after taxes to total assets, (BSZ) log of total assets, (TANG) Computed as ratio of fixed assets to total assets, (EVOL) is computed as ratio of (profit after taxes t − profit after taxes t−1 ) to profit after taxes t−1 to profit after taxest−1, and (GROW) ratio of market price per share to book value per share. GDPG is the gross domestic product growth rate, and INF is the CPI index measuring inflation. Financial Freedom, Government Effectiveness, Political Stability, Regulatory Requirements and Rule of Law control for country specific effects. Insignificant p-values of AR(2) depict no issue of serial correlation in all the estimated models and the Hansen test shows no identification issues overall, validating the econometric specification of all the models. Standard errors are given in parentheses.

, **, and *** denote statistical significance for p < .1, p < .05, and p < .01.

GMM Regression Results for Countries Having Lower Income in the Region.

Source. Authors compilations.

Note. This table gives the estimation results using two-step system GMM as the dynamic model on the basis of bank characteristics and controlling for various macroeconomic conditions. The banks are split in high income and low income, this measure is based on the per capita income classified by the World Bank website. The dependent variable is (BLEV) the measure for book leverage. Bank characteristics are given by (PROF) the profit after taxes to total assets, (BSZ) log of total assets, (TANG) Computed as ratio of fixed assets to total assets, (EVOL) is computed as ratio of (profit after taxes − profit after taxes t−1 ) to profit after taxes t−1 to profit after taxest−1, and (GROW) ratio of market price per share to book value per share. GDPG is the gross domestic product growth rate, and INF is the CPI index measuring inflation. Financial Freedom, Government Effectiveness, Political Stability, Regulatory Requirements and Rule of Law control for country specific effects. Insignificant p-values of AR(2) depict no issue of serial correlation in all the estimated models and the Hansen test shows no identification issues overall, validating the econometric specification of all the models. Standard errors are given in parentheses.

, **, and *** denote statistical significance for p < .1, p < .05, and p < .01.

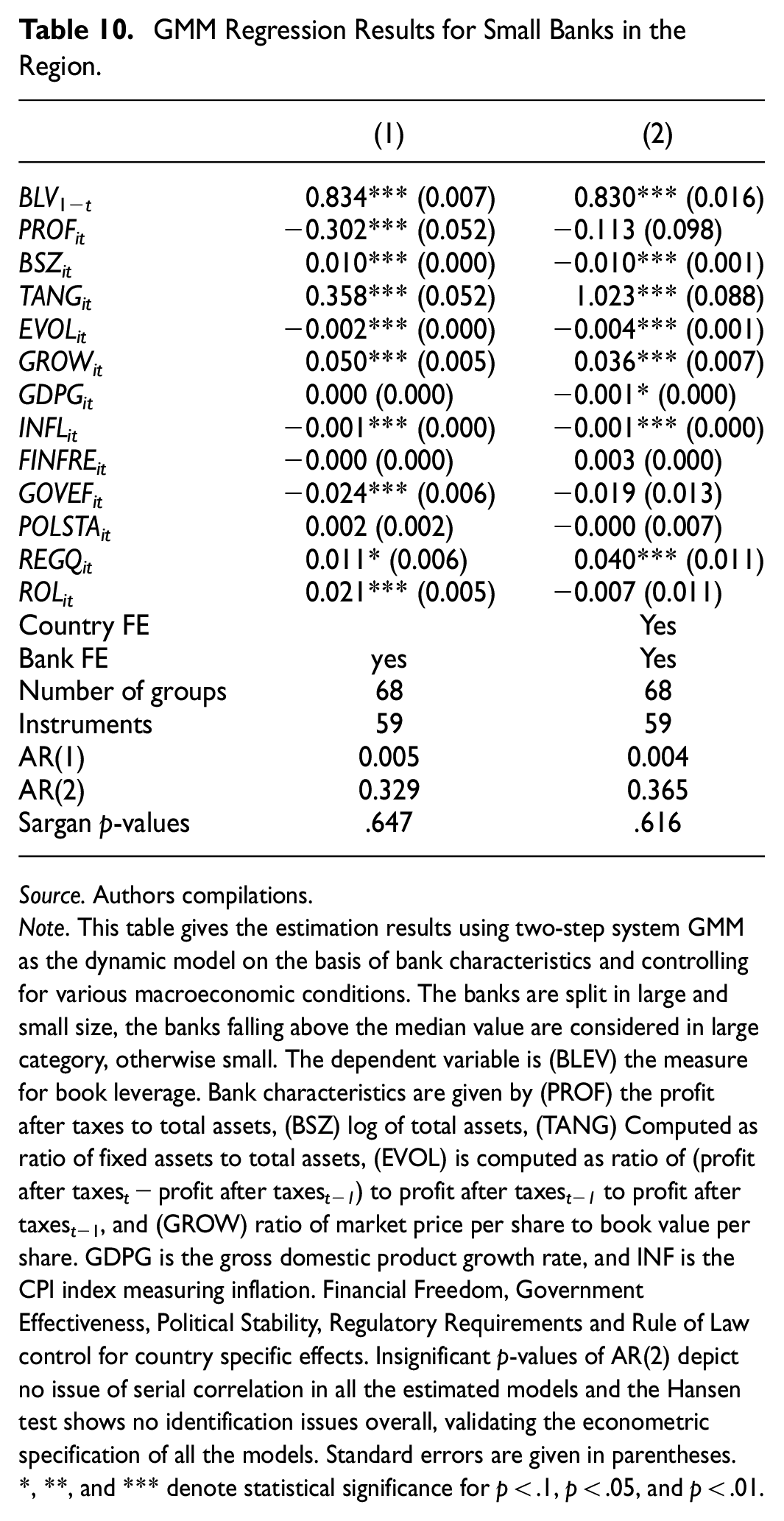

To further ensure the robustness of the results sample has been divided into two further sub sample, that is, sample of larger banks and smaller banks in the region. The banks are split in large and small size, the banks falling above the median value are considered in large category, otherwise small. The analysis results of largest and smallest banks are given in Tables 9 and 10. The estimation results of the large banks are similar to the results of whole sample except earnings volatility and tangibility. While smaller banks have similar association except the growth opportunities.

GMM Regression Results for Large Banks in the Region.

Source. Authors compilations.

Note. This table gives the estimation results using two-step system GMM as the dynamic model on the basis of bank characteristics and controlling for various macroeconomic conditions. The banks are split in large and small size, the banks falling above the median value are considered in large category, otherwise small. The dependent variable is (BLEV) the measure for book leverage. Bank characteristics are given by (PROF) the profit after taxes to total assets, (BSZ) log of total assets, (TANG) Computed as ratio of fixed assets to total assets, (EVOL) is computed as ratio of (profit after taxes t − profit after taxest−1) to profit after taxest−1 to profit after taxest−1, and (GROW) ratio of market price per share to book value per share. GDPG is the gross domestic product growth rate, and INF is the CPI index measuring inflation. Financial Freedom, Government Effectiveness, Political Stability, Regulatory Requirements and Rule of Law control for country specific effects. Insignificant p-values of AR(2) depict no issue of serial correlation in all the estimated models and the Hansen test shows no identification issues overall, validating the econometric specification of all the models. Standard errors are given in parentheses.

, **, and *** denote statistical significance for p < .1, p < .05, and p < .01.

GMM Regression Results for Small Banks in the Region.

Source. Authors compilations.

Note. This table gives the estimation results using two-step system GMM as the dynamic model on the basis of bank characteristics and controlling for various macroeconomic conditions. The banks are split in large and small size, the banks falling above the median value are considered in large category, otherwise small. The dependent variable is (BLEV) the measure for book leverage. Bank characteristics are given by (PROF) the profit after taxes to total assets, (BSZ) log of total assets, (TANG) Computed as ratio of fixed assets to total assets, (EVOL) is computed as ratio of (profit after taxes t − profit after taxes t−1 ) to profit after taxes t−1 to profit after taxest−1, and (GROW) ratio of market price per share to book value per share. GDPG is the gross domestic product growth rate, and INF is the CPI index measuring inflation. Financial Freedom, Government Effectiveness, Political Stability, Regulatory Requirements and Rule of Law control for country specific effects. Insignificant p-values of AR(2) depict no issue of serial correlation in all the estimated models and the Hansen test shows no identification issues overall, validating the econometric specification of all the models. Standard errors are given in parentheses.

, **, and *** denote statistical significance for p < .1, p < .05, and p < .01.

Discussion on Findings

The negative and significant association of profitability with dependent variable is found in all results, that is, whole sample, high income and low income countries sample, sample of largest and smallest banks of the region. It is in line with the prophecy of pecking order theory and in contradiction to trade-off theory. This infers that profitable banks do not need to borrow or take deposits, however, that could not be true in case of banks due to their primary nature of business. Secondly, banks may need to rely on external funds particularly in case of lower profitability. These findings are in line with the findings of Gropp and Heider (2010), Sheikh and Qureshi (2017), Ghosh and Chatterjee (2018), Al-Harby (2019), Al-Hunnayan (2020), and Khan et al. (2021).

Positive and significant association between bank size and book leverage is observed in all estimations. The result indicates that larger banks are incline to borrow more compared to small size banks. Theoretically these findings validate the trade-off theory hypothesis. This further endorse the argument that larger banks have higher credit ratings due to their diversified assets that result to lower cost of borrowings. Moreover, larger bank size means more branches or access to more customers which further enhance the banks’ capacity to collect more deposits and ultimately increase the capital base. These findings are also in line with the findings of Amidu (2007), Gropp and Heider (2010), Sheikh and Qureshi (2017), Bukair (2019), and Al-Hunnayan (2020).

No significant association between tangibility and leverage is found in whole sample and sample without the Egyptian and UAE banks. Small banks show. This is incongruent to trade-off and pecking order theory that suggests more tax benefits on collateralized borrowing and access to a higher levels of debt due to low information asymmetry. However, this endorses the fact about the banking industry, where depositors are less likely to consider the presence of tangible or more physical assets before depositing their money. Additionally, banks own more intangible assets (loans) compared to physical assets. Therefore, tangibility of the assets could not have significant effect on banks borrowing. But in small banks and high income and low income countries tangibility shows a positive association between tangibility and debt, suggesting that having more physical assets encourage the banks for collateralized borrowing.

Earnings volatility has a negative and significant association with leverage. These results endorse the predictions of trade-off theory. This negative association in the case of banks is similar to the assumption on relationship in the case of non-financial firms. However, results are contradictory to the actual nature of the banking business, where based on volatile earnings depositors do not stop depositing their money, unless bank meet their obligations.

The relationship between growth and leverage is negative and significant statistically. This validates the pecking order theory that recommends the growing firms to borrow less. The negative association also addresses the agency problems where managers may transfer the creditors’ wealth to shareholders by taking on risky projects. The results are congruent with Gropp and Heider (2010), Sheikh and Qureshi (2017) and Ghosh and Chatterjee (2018). Macroeconomic indicators GDP growth and inflation are likely to increase with an increase in economic activity hence, positive relationship with leverage is expected (see Jõeveer, 2013). Moreover, Demirgüç-Kunt et al. (2004) assumed a positive relationship between growth in the economy and business opportunities for banks, that is, increase in demand for capital.

Institutional characteristics have significant importance for financial sector, especially for credit lending institutions like banks in case of MENA region where banks are domestically centralized. For instance, banking activities flourish with financial freedom, by increasing the growth by increasing the loans. Government effectiveness, political stability and rule of law have a material effect on banks’ business environment and ultimately on the financing choices of the banks operation in MENA region. These institutional characteristics have an impact on the market structure that ultimately affect the banks’ business and their lending (see Hussain & Bashir, 2019, Khan et al., 2016).

To sum up, the findings contribute to the empirical literature by adding the evidence of MENA region banks. The empirical results are in line with earlier studies on banks’ capital structure and validate the trade-off and pecking order theory assumptions. It reports almost similar determinants of capital structure for MENA region banks, as reported by Gropp and Heider (2010), Sheikh and Qureshi (2017), Al-Hunnayan (2020), and Khan et al. (2021) studies on banks. The finding suggests that even though nature of business and regulatory environment is different compared to non-financial firms, the financing decisions of the banks are influenced by the same variables with few exceptions, resulted from the mentioned reasons. Hence, the banks’ capital structure choices are not the byproduct of the regulatory framework but also the managers’ choice to create the shareholders’ value.

Conclusion

This study examines the critical determinants of capital structure decisions for banks in the MENA region. The study employs an unbalanced panel sample of 132 banks operating in 15 countries from 2012 to 2017, resulting in 891 bank-year observations. The result indicates the similarity between the determinants of capital structure of financial and non-financial firms, even they both have different business and regulatory environments. The estimation outcome between profitability and leverage shows a negative and significant relationship. It supports the pecking order hypothesis and is in contradiction to trade-off theory. This infers that profitable banks do not need to borrow or take deposits, however, that could not be true in the case of banks due to their primary nature of business. The positive and significant association between bank size and book leverage specifies that larger banks are inclined to borrow more compared to small size banks. To check the robustness of the results, sample has been divided in to following categories, dropped the countries, that is, UAE and Egypt base on large number of banks observations, splitting the sample into larger and smaller banks of the region, dividing the countries into high and low income countries. It has been observed that mostly the effect of independent variables is same on dependent variable. Theoretically, these findings authenticate the assumptions of trade-off theory.

No significant association between tangibility and leverage is found. Earnings volatility is negatively and significantly related to leverage. It is congruent with the assumptions of trade-off theory. This negative association, that is, having volatile earnings, could not affect the intermediator’s role of a bank for the supply and demand of the capital. The relationship between growth and leverage is negative and significant. This is consistent with the pecking order theory assumption that recommends the less borrowing for growing firm. Macroeconomic indicators GDP growth and inflation are show a positive association that suggests the growth in macroeconomic indicators have a positive impact on overall economic activity that increases the demand of capital. Finally, the institutional factors, that is, government effectiveness, political stability, and rule of law are having positive association. Government effectiveness index refers to the fair public and civil service policies of a credible government. While the governance indicator including the political stability and rule of law are the outcome of efficient governance and regulatory system. These factors contribute to the establishment of a sound financial system with its impact on banks’ lending activities.

This study contributes to the inconclusive debate on an optimal structure by providing empirical evidence of banks operating in 15 economies of MENA region. A handful of studies have explored the factors of capital structure of firms operating in MENA region, particularly the financial firms. The findings of the study will lend a hand to the managers to formulate a value maximizing financing mix, also to regulators to establish investors’ friendly policies to tap on the regions’ economic potential and growth. Moreover, as most of the economies are moving away from oil export centered economies to diversified economies the stable and strong banking system could enhance the economic diversification objectives.

Lastly, this study provides a foundation for the understanding of capital structure choices of MENA region banks. Including banks from only 15 economies not from 19 economies of MENA region is a limitation for this study. Further studies including all the banks with the latest data from all the countries including the comparison among conventional and Islamic banks and comparative study with other regional economics blocks is recommended.

Footnotes

Acknowledgements

We are grateful for the comments given by the anonymous referees to include the robustness checks by dropping countries having higher number of banking years in data to ensure that bigger countries such as UAE and Egypt are not driving our findings the results can be seen.

Author Contributions

Conceptualization, Dr. Shoaib Khan, and Dr. Usman Bashir.; Methodology, Dr. Shoaib; Formal analysis, Dr. Usman and Dr. Khalid.; Data collection and sorting Dr. Hend Abdulhadi.; Writing—original draft, Dr. Shoaib and Dr. Usman.; Writing—review & editing, Dr. Khalid. and Dr. Hend. All authors contributed to revisions and approved the final submitted version.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.