Abstract

Management accounting is an important technical and methodological system embedded in organizations for predicting variability and making business decisions, and it plays a positive role in promoting enterprise value creation. This study examined the influence of the application of management accounting tools on enterprise value creation from a value chain perspective. Data were obtained from a questionnaire survey, and hypothesis testing was conducted using structural equations. The research results show that the application of different management accounting tools in different links of the value chain have different impact on the value creation of the company’s internal operations and the enterprise customers. There is a significant positive correlation between value creation in Internal operation, value creation in customers, and value creation in finance.

Keywords

Introduction

Management accounting tools refer to all models, technologies, and processes used in the application of management accounting, such as strategic maps, rolling budget management, activity-based cost management, cost–volume–profit analysis, and balanced scorecards (Ministry of Finance, 2016). Management accounting tools have been used for a long time to adapt to contingent organizational environments (Rigby & Bruno, 2009). With a wider application of management accounting tools, whether the management accounting tools applied by enterprises create value for them has always been one of the most important topics in the research and application of management accounting in China.

Empirical studies conducted in China and abroad support the application of management accounting tools to create value for enterprises. For example, activity-based costing proposed by plays a role in shortening the production cycle and improving product quality, thus reducing enterprise costs. In an economic consequence test of the application of management accounting tools, Du et al. (2008) found that newer management accounting tools were gradually replacing traditional management accounting tools and that the use of most management accounting tools could improve enterprises’ value creation. However, according to Vărzaru et al. (2022), the application of corporate management accounting tools may not necessarily be used to enhance the creation of corporate value. This may be because companies seek legitimacy or synchronize with contemporary management accounting and innovative means. Therefore, whether the application of management accounting tools creates value for enterprises, and examining what kind of value it creates, requires further data support and empirical testing. Simultaneously, the application of management accounting tools to enterprises requires a certain carrier. The value chain, as the value carrier of business activities, reflects the dynamic process of value creation by enterprises (S. B. Wen et al., 2023) and provides a platform for the application of management accounting tools. Therefore, using a value chain platform, this study employed a questionnaire to analyze and explore the relationship between the application of management accounting tools and enterprise value creation.

The exploration of the above issues in this study not only answers fundamental questions in the field of management accounting tools research but also provides theoretical support for enterprise practice, promotes the application of management accounting tools, enriches the research results of management accounting, and broadens the research perspective of management accounting, which is of great significance and value. The main contributions of this study are as follows. (1) It helps to expand the research perspective of management accounting tools. This study breaks through the limitation of previous studies that mostly focused on the management accounting tools at a specific “point” of need, and systematically examines the application of management accounting tools and their value creation from a “chain” perspective. (2) It contributes to improving the theoretical system of management accounting. The application system of management accounting tools based on the value chain constructed in this study enables the maximization of the effectiveness or value creation of management accounting tools, enriches the research content of the discipline of management accounting, and improves the construction of the theoretical system of management accounting. (3) It is conducive to guiding enterprises to reasonably select and apply management accounting tools. This study embeds management accounting tools into the business processes of enterprises, forming a more efficient management system, effectively matching management accounting tools with enterprise value creation activities, and enhancing the value creation capabilities of management accounting tools application in the value chain.

Theoretical Analysis and Hypothesis Presentation

Application and Value Creation of Management Accounting Tools Based on Value Chain

The goal of management accounting is to use management accounting tools to participate in and provide useful information for the organization’s planning, decision-making, control, and evaluation activities to promote strategic planning. Management accounting tools are an important means for achieving the objectives of management accounting (Ministry of Finance, 2016). With the continuous improvement in enterprise management demands, many management accounting tools have been introduced and implemented by Chinese enterprises. Simultaneously, with the historical evolution of management accounting, management accounting tools have become a stage of creating value through the effective use of resources.

Based on contingency theory, scholars have focused on the proper use of management accounting tools in different environments to create value for enterprises (Pan et al., 2010). Value chain analysis involves dismantling an enterprise’s business into strategy-related activities to understand the behavior of costs and potential sources of variance, effectively optimizing the use of limited resources (Otley, 2016). With the help of each link in the value chain, the value-added effect of management accounting tools can be studied to reflect the operational status of enterprises in real time. The operational effect brought about by different strategic decisions can be reflected through the functions of prediction and evaluation to give full play to the maximum effect of management accounting tools. Based on the resource-based theory, the full combination of management accounting tools and value chains can form a comprehensive and in-depth management system, which makes management accounting more capable of exerting and evaluating the strong power of value creation.

With the help of value chain management accounting tools, it is possible to achieve the unity of the value stream and operation flow of the enterprise management and improve the ability to create value for the enterprise, such as homework cost management from the origin of resource consumption, reduce non-value-added work, optimize business processes (Yu & Sang, 2014), improve process speed and output (Mao & Li, 2012), and reduce the total cost value chain (Ge & Cao, 2014). Embedding management accounting tools into the enterprise value chain can reduce the complexity of internal processes, process changes, corporate costs, and help to improve internal operating efficiencies. It can enable companies to produce more products that meet corporate customer requirements. Regarding R&D, J. B. Zhang and Bao (2010) considered that the target cost method could be applied to the R&D stage of enterprise products, and the R&D cost of enterprises could be reduced through the planning of R&D target costs. In the procurement phase, Jack (2013) used budget management to provide the basis for project bidding and cost tracking, to effectively control the procurement cost of the enterprise, and to improve the competitiveness of the enterprise. W. F. Zhang and Ji (2013) studied the application of activity-based costing in the production process, and the control and management of surplus production capacity. Song et al. (2020) and Guimarães et al. (2012) believed that budget management in the production process can effectively plan the production process, improve market competitiveness, and reduce the internal production costs of enterprises. At the sales stage, Yu et al. (2014) defined the conditions applicable to the traditional budgeting method based on sales. In the logistics sector, Fu and Yuan (2010) considered the requirements of different enterprises in China for logistics cost management and the differences in the application of comprehensive budget management and constructed the budget management system for budget cost management of enterprises in China to control the logistics cost of enterprises in China. Hensher (2015) applied benchmarking management to enterprises’ after-sales services, standardized after-sales services, conducted effective contract management, and improved customer satisfaction.

In summary, based on the contingency theory, the application of different management accounting tools to different links in the value chain is a scarce and valuable resource that is difficult to replicate and can increase the value created within the company’s internal experience and customers’ ability. Because enterprise value creation is relatively backward in the financial aspects of the value creation of the index (Wen et al., 2014), management accounting tools in enterprise value creation are ultimately reflected in the results of the financial dimension indicators. However, its value creation directly performs mainly through the enterprise’s Internal operation and customer management implementation in the process of creating.

Based on the above analysis, Hypothesis 1 was proposed:

H1: Application of management accounting tools based on value chains has a significant positive effect on enterprise value creation.

H1a: Application of management accounting tools based on value chains has a significant positive impact on internal operation value creation.

H1b: Application of management accounting tools based on value chains has a significant positive impact on customer value creation.

Internal Structure Relationship of Multi-Dimensional Value Creation

Value creation is a collection of business activities that provides a market with products or services that meet customer needs (Grossi et al., 2022; H. Zhang et al., 2020). Based on resource theory, value creation is understood as how companies can obtain resources that are difficult to replicate and have competitive advantages. In today’s global business environment, companies are under significant pressure to improve their productivity. Organizational resources are an element of modern organizational design and a manifestation of strategic entrepreneurship (Hitt et al., 2011). To meet these challenges, enterprises need to utilize all internal resources, improve resources’ utilization rate, gradually become customer oriented, and invest in quality products at competitive prices to improve their financial indicators.

Value creation on the corporate side helps increase value creation on the customer side. The value chain theory believes that by continuously improving and optimizing the “value chain” of the company’s internal operations, maximizing the “customer value” as much as possible is the key to improving the competitive advantage of the company. These include the potential and embedded value in products or services obtained by customers from enterprises (Grönroos & Gummerus, 2014). Embedded value in products is mainly generated by the internal business activities of enterprises, whereas the service value obtained by customers is generated by customer satisfaction and other customer indicators. The improvement of value creation in the internal operations of an enterprise (such as the reduction of product defect rate, shortening of product production cycle, and advance of delivery time) can improve product quality, customer satisfaction, and expand market share, thus improving the market performance of the customer dimension. For example, Grönroos and Ravald (2011) from the perspective of suppliers and customers, analyzed the five service logics of creating value for customers by enterprises themselves, transformed the services of enterprises to customers into valuable processes, and realized common value creation.

Internal value creation can improve financial value creation. Management accounting is mainly used to provide financial and non-financial information; financial information is the dependent variable, and non-financial information is the independent variable (Yu, 2017). Therefore, the value generated by a company’s internal operations as non-financial information will eventually be reflected in the company’s financial indicators. For example, He (2018) argued that the improvement of internal operational value creation (such as the reduction of product defect rate, shortening of the product production cycle, and advance of delivery time) can reduce the external loss cost of the total cost, and then directly improve financial value creation and indirectly improve financial value creation by improving customer financial value creation.

Improvement in value creation on the customer side can effectively expand the market share of the enterprise and increase revenue, thus contributing to an improvement in value creation on the financial side. Although the value creation of enterprise finance is a lagging value-creation index (Wen et al., 2014), it is eventually reflected in the enterprise’s financial index. For example, Ikramuddin (2021) believe that with the improvement of customer satisfaction, customer loyalty will also increase, which will reduce the marketing cost of the enterprise and ultimately increase the creation of corporate financial value. Xia et al. (2016) believed that the improvement of customer satisfaction can affect the financial value creation of enterprises by improving the product or service quality to gain recognition and trust from customers, reduce customer complaints and dissatisfaction, improve customer loyalty, and enhance the attraction to new customers.

Based on the above analysis, Hypothesis 2 was proposed:

H2a: Internal operation value creation has a significant positive impact on customer value creation.

H2b: Internal operation value creation has a significant positive impact on financial value creation.

H2c: Customer value creation has a significant positive impact on financial value creation.

Research Design

Design and Withdrawal of the Questionnaire

Questionnaire Design

All the data used in this study were obtained from questionnaires. In the process of compiling and revising the questionnaire, to ensure validity and rationality of the questionnaire, this paper refers to the research of Churchill and Churchill (1992) and other scholars on the design process of the questionnaire. The specific steps for the design of the questionnaire are as follows: First, sort out relevant literature at home and abroad. After consulting a large amount of domestic and foreign-related literature on enterprise value chains, management accounting tools, value creation, and so forth, the relevant measurement items of the questionnaire are set to form the initial questionnaire items. Second, ask for the opinions of the academic team, aiming at the modification opinions provided by the experts and team members on the items and wording of the questionnaire, reduce the possibility of words failing to reach the meaning, unclear expressions, and ambiguity, and form the second draft of the questionnaire. Third, ask for the opinions of the senior managers of the enterprise. Through in-depth communication with senior managers of the enterprise, the rationality of the questionnaire questions, test contents of variables, whether the questionnaire reflected the real situation of the enterprise, and other issues are discussed, and related items in the questionnaire are revised. Finally, it is the preliminary test questionnaire. After the questionnaire is completed, through a questionnaire test of 30 Master of Business Administration (MBA) students, the measurement items and related wording of the questionnaire are revised again, and finally, a formal questionnaire is formed.

The questionnaire used in this study is divided into three parts. The first part is the basic collecting of sample companies, and the second part is the investigation of the degree of application of management accounting tools at the nodes of the value chain. A 5-point Likert scale was used to investigate the degree of application of management accounting tools in the value chain. The third aspect is value creation. If the respondents chose specific management accounting tools, they are considered the subjects of this study.

Data Collection and Statistics

Data Collection

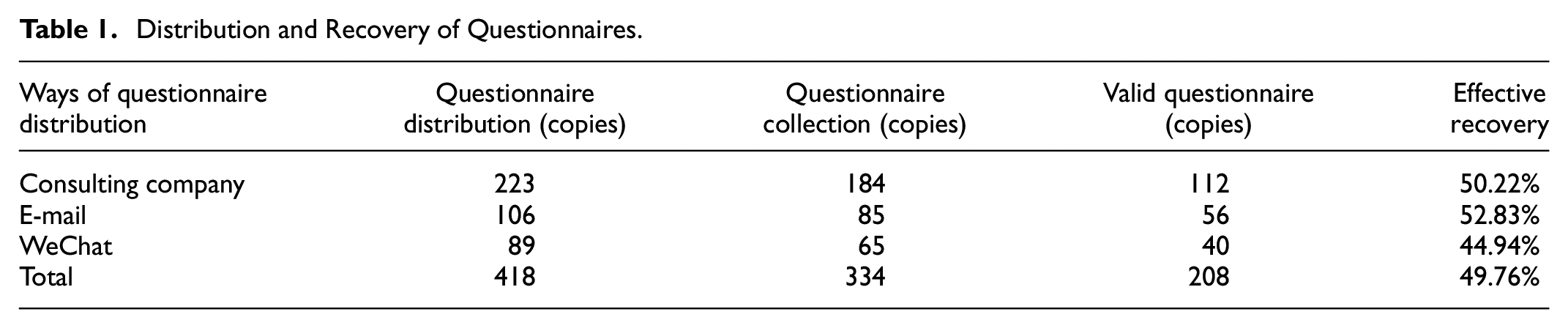

This paper used a total of 418 questionnaires, of which 334 were returned, the deficiency in eliminating obvious random fill, or options, after all of the same questionnaire form effective questionnaire 208, the effective recovery rate is 49.76%. We put forward the effective recovery rates greater than 45% of the standard questionnaire. Statistics on the distribution and recovery of questionnaires are presented in Table 1.

Distribution and Recovery of Questionnaires.

According to Table 1, there were three main ways of questionnaire distribution in this study: first, through cooperation with Dalian Seiwajyuku Consulting Company, the author sent 223 copies to the training site of Dalian Seiwajyuku Consulting Company in paper form and recovered 184 copies, of which 112 were valid questionnaires, with an effective recovery rate of 50.22%. Second, the questionnaire was made available through network link, 106 copies of which were distributed by e-mail to the students of MBA, Executive Master of Business Administration (EMBA), and Master of Professional Accounting (MPAcc); 85 copies were recovered, of which 56 copies were valid, with an effective recovery rate of 52.83%. The university has more working MBA, EMBA, and MPAcc classes, and graduated MBA, EMBA, and MPAcc students come from all over the country, so there are convenient conditions for issuing questionnaires. Third, the network link of the questionnaire was sent to friends engaged in financial accounting in the form of WeChat, and 65 copies were collected, with 40 valid questionnaires and an effective recovery rate of 44.94%.

Sample Distribution

This study provides statistics on the basic information of the surveyed enterprises and respondents. Table 2 presents the descriptive statistics of the questionnaire’s basic information.

Descriptive Statistics of the Basic Information of the Questionnaire (N = 208).

Note. The sample industries were divided into 15 sectors, such as industry, construction, wholesale, retail, and transportation, as well as the broad category of the social work industry. The sample size was categorized as large enterprises, medium-sized enterprises, and small enterprises according to a comprehensive examination of the industry, number of employees, and business income.

From the distribution of the property rights of the sample enterprises, the sample size of state-owned enterprises was 50, accounting for 24.04% of the effective sample size. The sample size of private enterprises was 106, accounting for 50.96% of the effective sample size. The sample size of Chinese-foreign joint venture enterprises was 22, accounting for 10.58% of the effective sample size. The sample size of wholly foreign-owned enterprises was 21, accounting for 10.10% of the effective sample size. From the perspective of the sample industry distribution, the sample size of industrial enterprises was 102, accounting for 49.04% of the effective sample size, and the sample size of the construction industry was 38, accounting for 18.27% of the effective sample size. The other sample size for industries was 68, accounting for 32.69% of the effective sample size. From the scale distribution of the sample enterprises, the sample size of medium- and large-sized enterprises was 59.62% each. Small enterprises accounted for 40.38% of the sample size. According to the distribution of the sample enterprises’ years of establishment, samples that were established for 10 years accounted for 69.71% of the effective samples. Based on the overall distribution of the sample enterprises, the sample of effective questionnaires has a certain representativeness.

Among the valid samples, the position distribution of respondents was as follows: 12 were chairmen, accounting for 5.77% of the valid sample; 18 were general managers, accounting for 8.65% of the effective sample size; and 23 were deputy general managers, accounting for 11.06% of the effective sample size. Fifty-five came from the Chief Financial Officer, accounting for 26.44% of the effective sample size. There were 48 middle financial managers, accounting for 23.08% of the sample. The average number of General Finance Staff members was 52, accounting for 25.00% of the sample size. Managers at the middle level and above accounted for 75% of the respondents, ensuring the quality of the questionnaire. The distribution of working years among the respondents to the questionnaire was as follows: 62 people within 5 years of work, accounting for 29.81% of the effective sample size; 60 people from 6 to 10 years, accounting for 28.84% of the effective sample size. The number of people within 11 to 15 years of work in the annual interval was 53, accounting for 25.48% of the effective sample size; 22 in the 16 to 20 years interval, accounting for 10.58% of the effective sample size; and 11 people over 20 years, accounting for 5.29% of the effective sample size. The average working life of the respondents was close to 10 years, with rich work experience, which improved the questionnaire quality.

Variable Setting

Application of Management Accounting Tools Based on Value Chain

In this study, the determination of the value chain node’s main reference to Porter put forward the idea of the value chain, given that the main auxiliary activities are auxiliary to the main activities to create value for the enterprise. This study selected the principal activities of the value chain as the research object, combining the actual situation of the enterprise interview at the same time, considering the procurement and development of two areas in the modern enterprise. The importance of the value chain was divided into R&D, purchasing, production, marketing, logistics, and customer service.

To determine management accounting tools, this study used the method of Zhou et al. (2009), based on the theoretical deduction of the definition of concepts in domestic and foreign social science research, combined with the characteristics of strong management accounting practices. It adopted two methods: mainstream management accounting textbooks and management accounting practice research literature. Simultaneously, it was supplemented by the Basic Management Accounting Guidelines issued by the Ministry of Finance of China in 2016, the 22 Management Accounting Application Guidelines issued in 2017 on the issue of Management Accounting Application Guide No. 100-Strategic Management, and regulations issued in 2018. Letter of soliciting opinions on seven management accounting application guidelines (draft for comments), including Management Accounting Application Guide No. 202-Zero-Based Budget and Management Accounting Announcement issued by the United States in 2012 were also used. The management accounting tools examined in this study mainly include comprehensive budget management, standard cost method, target cost method, activity-based cost method (ABC), marginal analysis, Key Performance Indicator (KPI), cost–volume–profit analysis (CVP analysis), benchmarking management, economic value added (EVA), and risk matrix. Considering the variable based on the application of value chain management accounting tools, this study adopted the method of principal component analysis of management accounting tools in the application of value chain dimension reduction for each link, and each link of the value chain management accounting tool kit was investigated based on the value chain management accounting tools used to create enterprise value. Table 3 presents the principal component analysis table formed using the management accounting toolkit for each link in the value chain.

Principal Component Analysis Table Formed by the Management Accounting Toolkit of Each Kink of the Value Chain.

According to the criteria given by the statistician Kaiser, a KMO value >0.6 is suitable for principal component analysis. In this paper, the KMO test and Bartlett’s sphere test were conducted on the sample data of management accounting tools in each link of the value chain, and the KMO values of management accounting tools in each link of the value chain were 0.904, 0.897, 0.885, 0.864, 0.927, and 0.826. The statistical value of the sphere test had a significance probability of .000 and a significance level was 1%, which further indicates that the data structure is suitable for principal component analysis. Therefore, this study used the method of great variance to rotate the factor loading matrix and took a factor eigenvalue greater than 1 as the criterion to determine the final number of factors to be extracted. Furthermore, management accounting tools with certain correlations between variables were packaged to reduce the dimensionality of the variables of management accounting tools in each link of the value chain in the form of a management accounting toolkit to study the relationship between the application of management accounting tools and enterprise value creation.

Value Creation

Based on the concept of diversified value creation adopted by D. H. Wen et al. (2009), and Du et al. (2008), this study divides enterprise value creation into financial and non-financial evaluations. Among them, non-financial value creation refers to D. H. Wen et al. (2009). O'Cass and Sok (2013) divide non-financial value creation into value creation within a company’s internal operations and customer value creation. Simultaneously, D. H. Wen et al. (2009), such as the division of value creation theory of explorative factor analysis, is based on a single aspect, and the results show that the content of the 13 questions that there are three principal component factor loads three principal component factor of each topic and the paper about Internal operation value creation, customer value creation in exact accordance with the classification of financial value creation, show that the dimensions of value creation are reasonable. The variable design table for enterprise value creation is presented in Table 4.

Variable Design Table of Enterprise Value Creation.

Reliability and Validity Test

Reliability Test

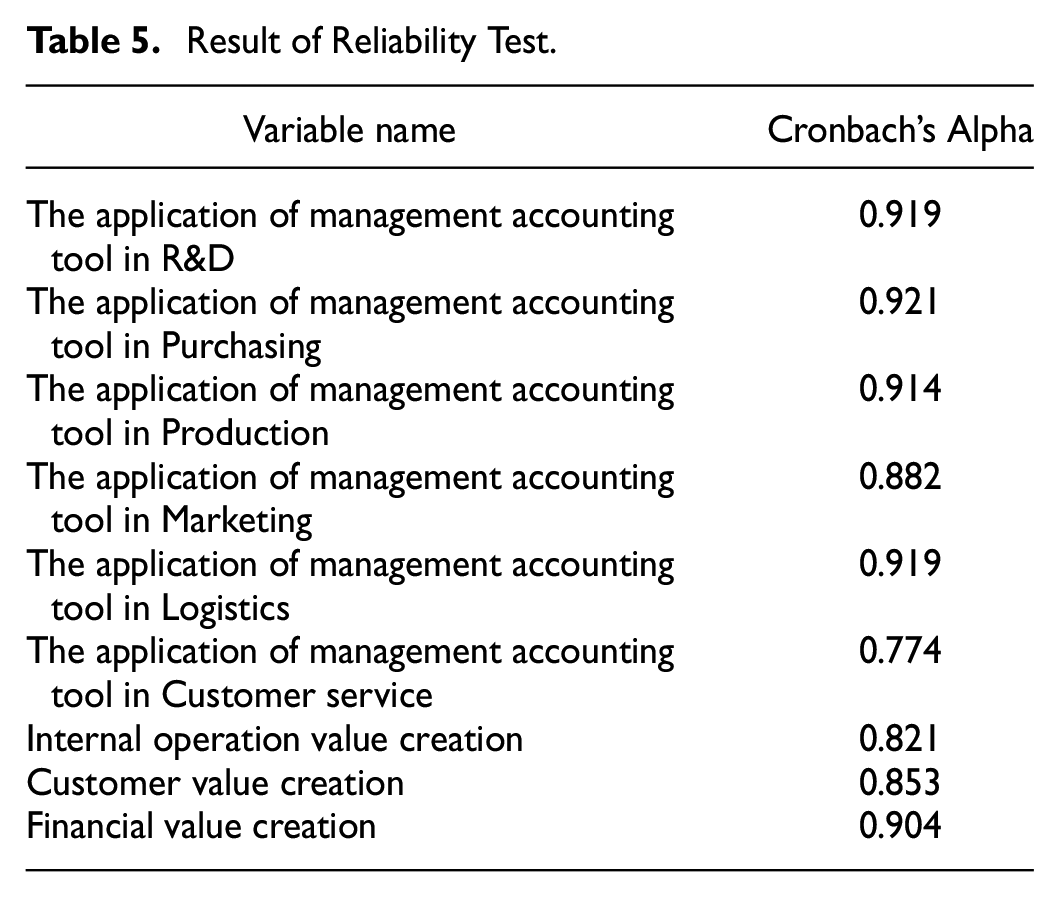

Reliability refers to the consistency and stability of the results obtained using a test tool. The greater the reliability of the scale, the smaller is the standard error of the measurement (Wu, 2010). This study used the Cronbach’s alpha coefficient to test the variables. If Cronbach’s alpha is greater than or equal to .700, the sample data have high reliability (John, 2016). The reliability test results are listed in Table 5.

Result of Reliability Test.

According to Table 5, the Cronbach’s alpha of the management accounting tools investigated in this paper is 0.774 at least and 0.921 at most in each link of the value chain; the Cronbach’s alpha of the management accounting tools used in each link of the value chain is >0.700; Cronbach ’s alpha for the internal operation value creation is 0.821, customer value creation 0.853, and financial value creation 0.904. All values were >0.700, indicating the high reliability of the questionnaire variables.

Validity Test

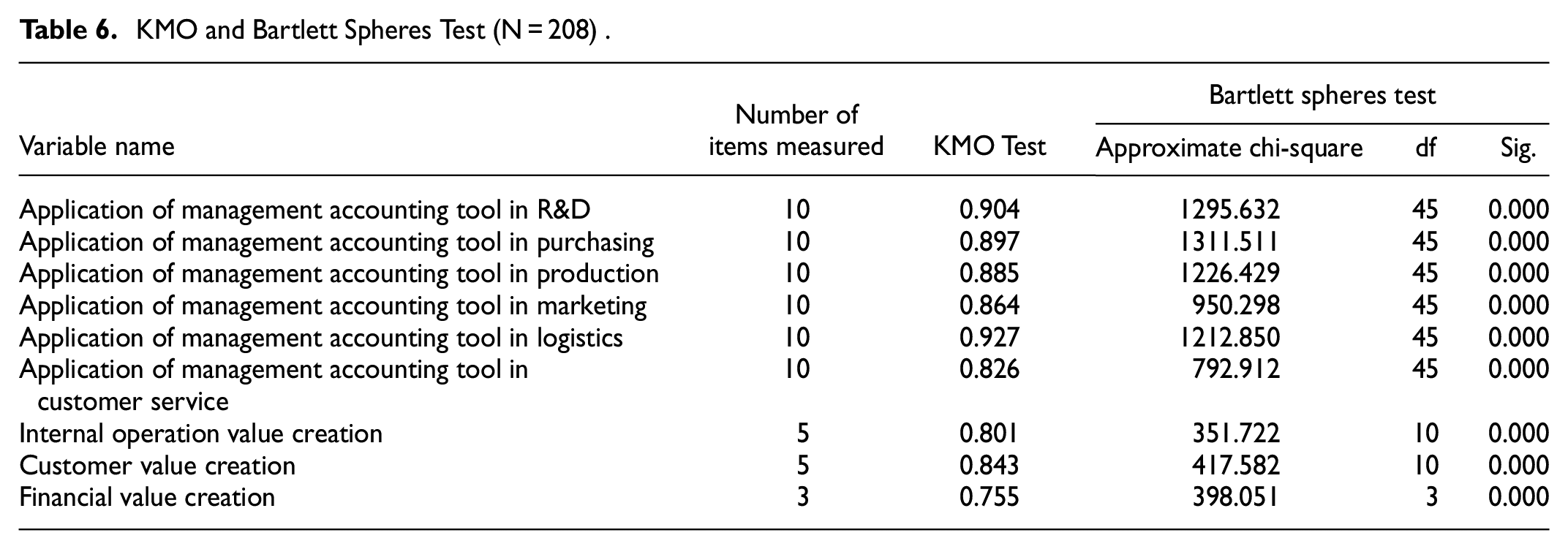

The validity analysis method used in this study mainly adopted construction validity. First we used SPSS17.0 software for each link of management accounting tools based on value chain applications, Internal operation, value creation, customer value creation in terms of value creation, and financial aspects of exploratory factor analysis, a survey questionnaire with a single-dimension validity. If the KMO and Bartlett test (Bartlett) sphere test value was >0.600, the questionnaire had good single dimensions of validity (Wu, 2010). Table 6 shows the exploratory factor analysis of value creation, which was used to test the single-dimensional validity of value creation in three aspects.

KMO and Bartlett Spheres Test (N = 208) .

Table 6 shows that the KMO inspection value of the management accounting tools applied in each link of the value chain is >0.800, indicating that the application of management accounting tools in each link of the value chain has higher validity. The KMO values for internal operation value creation, customer value creation, and financial value creation were 0.801, 0.843, and 0.755, respectively, indicating that the questionnaire has high single-faceted validity.

Analysis of Empirical Results

Correlation and Collinearity Analysis

Correlation Test

This study used Pearson’s and Spearman’s (upper-right) two-tailed tests to test the correlation between management accounting tools and value creation. Table 7 presents the Pearson (lower left) and Spearman (upper right) two-tailed test results for the latent variables of the model.

Model Latent Variables for Pearson’s (lower left) and Spearman’s (upper right) Two-Tailed Test.

Note. ** Indicates Significant at 0.05 level.

As shown in Table 7, the correlation coefficient between the application of Pearson’s (lower left) management accounting tools and value creation is .183 (p < .05), and the correlation coefficient between Spearman’s (upper right) double-tail test management accounting tools and value creation is .196 (p < .05), which preliminarily supports hypothesis H1, that is, the application of management accounting tools can improve enterprise value creation.

Collinearity Test

Table 8 presents the collinearity test results for the model. Generally, when the tolerance of the model latent variables is <0.10, or the variance inflation factor (VIF) is >5, it indicates that there is multicollinearity between the model latent variables, which affects the correct estimation of the regression model.

Multicollinearity Test of the Model Latent Variables.

Table 8 shows that the tolerance of management accounting tools is 0.89 (>0.10) and the variance inflation factor (VIF) is 1.13 (<5). The tolerances of value creation in internal operations, value creation in customers, and value creation in finance were 0.75, 0.64, and 0.68, respectively, all of which were >0.10. The VIF of the three aspects of value creation are 1.33, 1.56, and 1.47, respectively, all of which are <5, indicating that there is no multicollinearity in model management accounting tools, value creation in internal operations, value creation in customers, and value creation in finance.

Establishment of Structural Equation Model

This theoretical model is composed of multiple linear regression equation. The traditional path analysis is only applicable to test the relationship between the specific indicator variables, and structural equation model can simultaneously test more direct observation of the relationship between the latent variables. At the same time, to estimate the factor, the relationship between the structure and factor and model can provide the overall diagnostic information. Therefore, the structural equation is among the most effective test methods for the hypotheses proposed in this study.

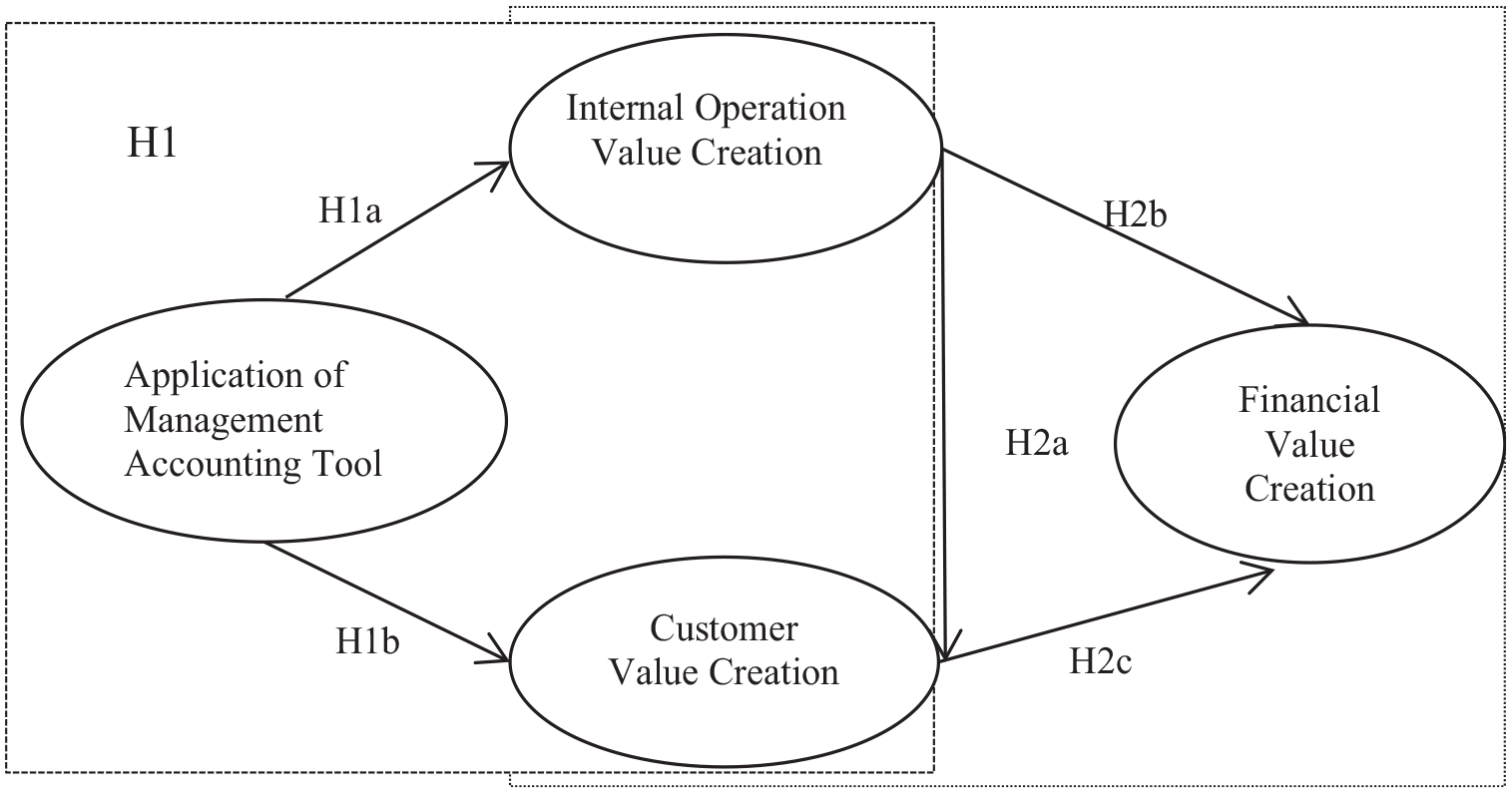

Referring to the relevant literature on management accounting tools, value chains, and value creation, this study established a structural equation model that reflects the application of management accounting tools and enterprise value creation in the value chain, as shown in Figure 1.

Structural equation model reflecting the application of management accounting tools in the value chain and enterprise value creation.

Measurement and Result Analysis of Initial Structure

Goodness-of-Fit Evaluation

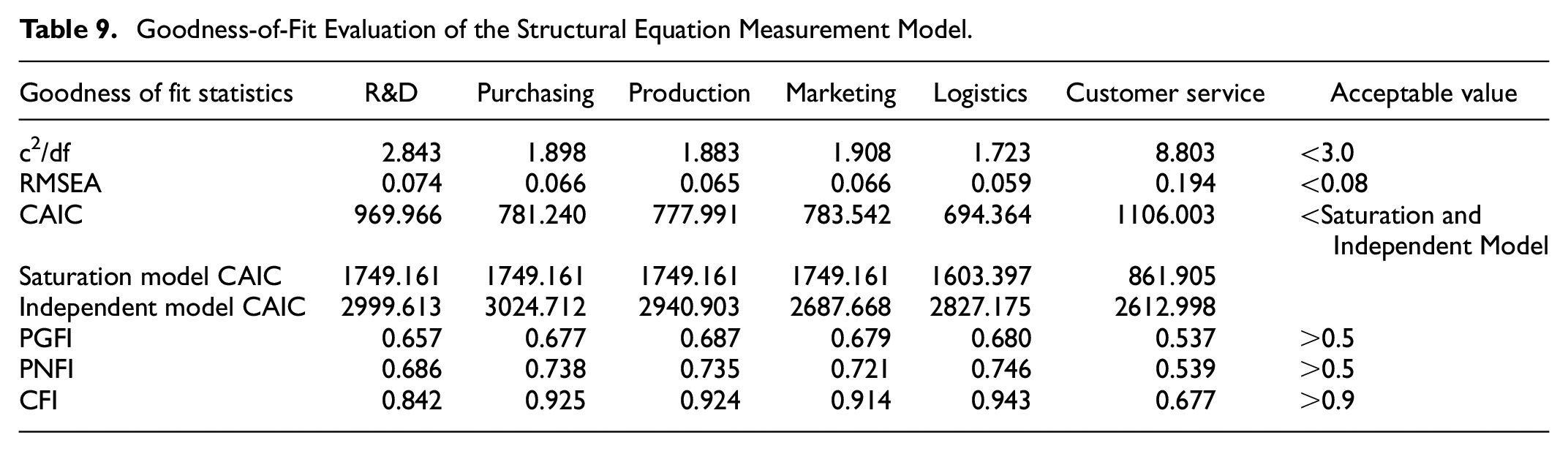

In this study, following D. H. Wen et al. (2009) and Wen et al. (2014), the chi-squared degree of freedom ratio (c2/df), root mean square error (RMSEA), Akaike Consistent Information Index (CAIC), Economical Fitting Goodness Index (PGFI), economical fitting normative fitting index (PNFI), and relative fitting index (CFI) were used. Table 9 shows the goodness-of-fit evaluation of the structural equation measurement model based on the application of management accounting tools and enterprise value creation.

Goodness-of-Fit Evaluation of the Structural Equation Measurement Model.

Columns 2 to 6 of Table 9 show the six goodness-of-fit index values for R&D, Purchasing, production, Marketing, Logistics, and Customer service, respectively. The last column shows the acceptable range of an index. It can be seen from Table 9 that the goodness of fit indexes in the four value chain links of Purchasing, production, Marketing, and logistics are all within an acceptable range. This shows that the degree of fit between the measurement model and the data in the four value chain links is satisfactory. In the R&D process, except for the CFI index of 0.824, which was slightly lower than the acceptable level of 0.900, the other goodness-of-fit indicators were within an acceptable range, indicating that the degree of fit between the measurement model and the data in the production process was satisfactory. In the Customer service, the chi-square freedom ratio (8.803), RMSEA (0.194), CFI (0.677), CAIC (1106.003), and other indicators are not acceptable, which indicates that the measurement model and data in the after-sales service are not well matched; therefore, this path should be deleted.

Measurement Results and Correction of Initial Structural Equation Model

Based on the goodness of fit of the model, this section uses AMOS 17.0 software to estimate the parameters of each path of the structural model. Table 10 presents the results of the standardized estimates of the initial measurement model.

Results of the Standardized Estimates of the Initial Measurement Model.

Note. *** Indicates Significant at 0.01 level.

The SEM was modified based on the initial measurements of the model. There are two directions for model modification. One is to simplify the structural equation model, that is, to delete or restrict some paths in the model so as to simplify the model. The second is to extend the structural equation model, that is, to relax the path restrictions in some models and improve the goodness of fit of the model (Yi, 2008). Due to the large number of variables studied in this study, a series of nested models were evaluated by using the method of deleting paths with insignificant coefficients according to Wang et al. (2022) . Through the nested tests repeatedly, the initial model test results with non negative coefficients were finally deleted to obtain the revised structural equation model measurement.

Analysis of Modified Structural Equation Results

Goodness-of-Fit Evaluation

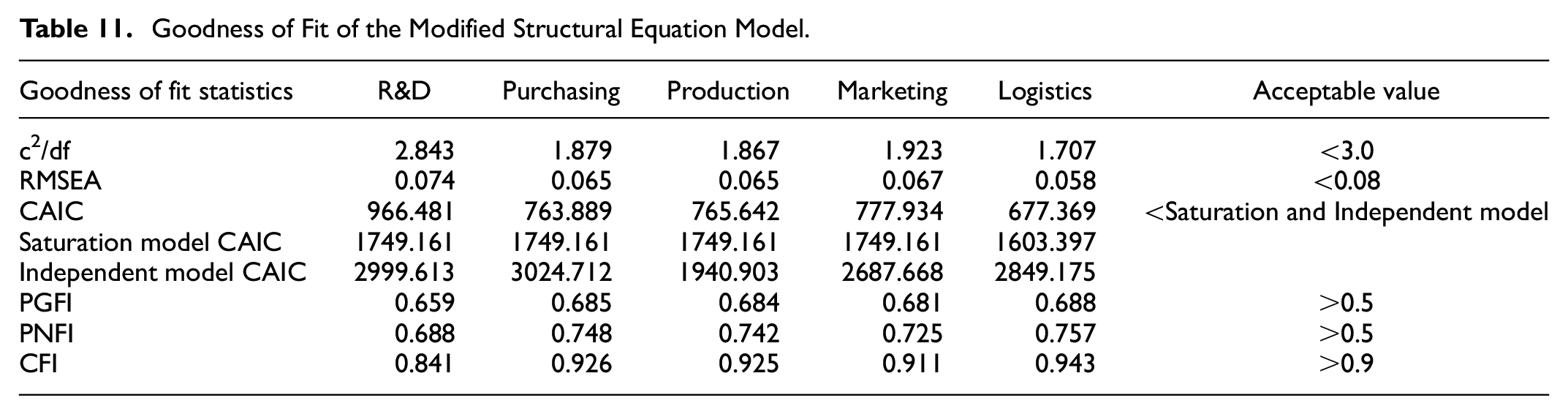

This study estimated the goodness-of-fit of the modified model. Table 11 shows the estimation results for the goodness of fit of the modified structural equation model.

Goodness of Fit of the Modified Structural Equation Model.

As shown in Table 11, the revised structural equation model for the Purchasing, production, Marketing, and logistics link card side ratio of degrees of freedom, RMSEA, CAIC, PGFI, PNFI, and CFI various goodness-of-fit indices in the range of acceptable values; only research and development of CFI values slightly less than 0.900 and 0.841 shows that the revised measurement model and data fitting degree of satisfactory, the presented model is reasonable.

Path Result Analysis

This study reevaluated the parameters of the revised model. Table 12 presents the measurement results of the revised structural equation model.

Measurement Results of the Revised Structural Equation Model.

Note. *** Indicates Significant at 0.01 level.

Impact analysis of management accounting tools based on value chain enterprise value creation.

Impact Analysis of Management Accounting Tools Based on Value Chain Enterprise Value Creation

Different tools have varying impacts on value creation at different stages. The following is an analysis of the impact of different management accountants applied to different value chain nodes on value creation. As Table 12 shows, the results of the model checking for value creation applied by management accounting tools at various links in the value chain are as follows.

In R&D link, marginal analysis, risk matrix, KPI, CVP analysis, benchmarking, and the application of economic value-added in the R&D section of enterprise value creation have significant positive influences on customer value creation.

In the procurement link, the KPI, benchmarking management, comprehensive budget management, CVP analysis, and target cost method application in purchasing links have a significant positive influence on customer value creation.

In the production link, total budget management and KPI had a significant positive impact on customer value creation.

In the sales link, comprehensive budget management, KPI, risk matrices, and application of benchmarking in the sales link have significant positive influence on customer value creation.

This study considered the logistics link of an enterprise as a process of planning, implementing, and controlling the efficient storage of goods, services, and related information from the place of production to the place of consumption to meet the needs of customers. In the logistics sector, enterprises mainly focus on budget control, performance assessment, and operational analysis, whereas risks and costs have a positive impact on the value creation of internal operations and customers; however, this was not significant.

Internal Structure Relationship Analysis of Multi-Dimensional Value Creation

The coefficients of the three paths of value creation from internal operations to customer value creation, from internal operations to financial value creation, and from the customer side to financial value creation were all positive. The two paths of value creation from internal operations to customers and from customers to financing were significant at the 1% level, whereas the paths of value creation from internal operations to financing are significant at the 10% level. This indicates that the value creation of Internal operation has a significant positive effect on the value creation of customers, the value creation of Internal operation has a significant positive effect on the value creation of finance, and the value creation of customers has a significant positive effect on the value creation of finance, which is verified by hypothesis H2a, H2b, and H2C.

Research Conclusion and Prospects

Based on management accounting tools as the research object, the empirical test, and analysis of the application of management accounting tools in every link of the enterprise value chain of enterprise value creation, it was concluded that the application of different management accounting tools in different links of the value chain has different impact on the value creation of the company’s internal operations and the enterprise customers. For example, marginal analysis, risk matrix, and KPI in the R&D link have significant positive impacts on customer value creation, whereas total budget management and KPI in the production link had a significant positive impact on customer value creation. There is a significant positive impact between internal operation value creation, customer value creation, and financial value creation.

This study begins by deriving the impact mechanism of the application of management accounting tools on enterprises’ value creation through an empirical test of questionnaire data. Although the author strives to achieve perfection and rigor, it also attempts to comprehensively study the various aspects of management accounting tools in the value chain. The impact of link application on corporate value creation. However, due to the limitations of certain sampling conditions, the number of effective questionnaires collected in this study was limited. Examining whether the research conclusions are universal requires further conceptual analysis and demonstration. Simultaneously, this study covers only the application of value chain management accounting tools “dot” type. For the effective value creation functions of management accounting tools, the enterprise should combine their own property rights, industry, and scale to choose scientific and reasonable management accounting tools and solve problems in enterprise value chain, break through the limitations of traditional “dot” type of management thinking, throughout the whole process and across the organization management process, and shape a new competitive advantage. How to give full play to the synergistic effect of management accounting tools in the application of enterprise value chains and how to excavate the value creation path of management accounting tools will be one of the important research topics for future studies.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.