Abstract

The debate on the implications of financial literacy (FL) on financial well-being (FWB) is at the forefront of global policy discussions. However, the literature often overlooks the mediating factors in this relationship and the characteristics of information that have not been thoroughly explored. This paper focuses on the level of information as a characteristic and investigates its mediating effect on the link between FL and FWB in the rural setting of Ghana. The study employed the Partial Least Squares Structural Equation model with a reflective-reflective higher-order construct to examine these linkages. Using an instrument adapted from existing studies and validated prior to administration, data were collected from 663 households in Ghana’s Upper West Region. The results show that financial literacy significantly impacts financial well-being. Moreover, financial literacy influences the extent of financial information individuals seek. Additionally, acquiring financial information is positively related to financial well-being, suggesting that access to and utilisation of financial information can improve financial well-being. Furthermore, the study reveals that the level of financial information partially mediates the relationship between financial literacy and financial well-being. This implies that while financial literacy directly enhances financial well-being, it also indirectly increases the level of financial information sought and utilized by individuals. The results emphasize financial literacy’s importance in promoting financial well-being, highlighting the need for comprehensive financial education programmes.

Introduction

Low financial literacy (FL) continues to threaten financial well-being (FWB) (Lone & Bhat, 2024) globally. Ghana’s financial literacy rate is reported to worsen from 32% in 2015 to 27% in 2023 (Klapper et al., 2015; Sarpong-Kumankoma et al., 2023). Rural areas have even lower literacy rates of around 12% to 13% (Szafranska, 2019), implying that lower-income and relatively less literate households in rural areas suffer from financial knowledge, affecting their financial well-being. In contrast, the Ghana demand side survey report 2021 indicates that access to financial services such as mobile money, credit and savings, and savings in other savings clubs has increased in rural Ghana from 51% in 2017 to 92% in 2021, while the national average in 2021 stands at 96% (GoG, 2021). Rural areas account for more than 80% of the country’s poverty rate (GSS, 2017), suggesting that households have limited resources and are likely not to put the highest benefits on the little they have due to low financial literacy.

As households assume a more prominent role in managing their financial lives (Qiu et al., 2025), it becomes essential that households possess an adequate degree of financial information. This responsibility becomes increasingly vital as households take on more significant roles in household financial resource management (Lusardi & Mitchell, 2017). Regrettably, numerous industrialized and emerging nations have acknowledged their citizens’ inadequate levels of financial information (Ahearne et al., 2004), which is necessary for making sound financial decisions. This deficiency can negatively impact households’ FWB. For instance, in Ghana, low FL and misinformation have led to growing scams, fraud, and the accumulation of high-interest debt among citizens (Asmah et al., 2020; Avortri & Agbanyo, 2020), thereby weakening FWB (Sarpong-Kumankoma et al., 2023). Sarpong-Kumankoma (2023) demonstrated this when he found that just about one-fourth of Ghanaians have the necessary information on financial products and services.

The financial information level (FIL) exposure in communities is essential for enhancing the role of FL in achieving FWB. However, the FIL, which can vary from household to household, may influence financial behaviour and contribute to FWB. The financial information households encounter shapes their financial behaviour, though the effect depends on their financial knowledge and needs (Houghton & Sheehan, 2000). This indicates that for households to apply financial knowledge and make well-informed decisions, they must have access to reliable, comprehensible, and pertinent financial information (Fernandes et al., 2014; Robb & Woodyard, 2011; Shim et al., 2012). Thus, lower or higher financial needs and knowledge may predict how financial information leads to FWB (Angrisani et al., 2023) through its effects on financial decision-making (Barbic et al., 2019; Fan, 2021). Although households’ financial knowledge may affect information consumption as a precursor to financial decisions that impact FWB, a thorough literature review revealed that the role of FIL in the relationship between FL and FWB remains unexamined. This gap is particularly evident in contextual factors that facilitate financial decision making, such as literacy education programmes and availability of financial information, which coexist with significant barriers, including sociocultural norms and low literacy levels. This dynamic is especially relevant in regions like the Upper West Region of Ghana, where the mediating role of financial information in this relationship requires empirical investigation.

The rest of the study is organized as follows: the

Literature Review

Theory and Hypothesis Development

Kamakia et al. (2017) questioned the adequacy of Prospect Theory (PT) as a standalone framework for explaining all dimensions of financial literacy in relation to financial well-being. Hillman and Dalziel (2003) similarly argued that no single theory is comprehensive enough to capture the complexity of the subject, advocating instead for a multi-theoretical approach. Recent empirical studies highlight a shift from examining the direct relationship between financial literacy and financial well-being to a growing interest in mediation- and moderation-based research (Richardson et al., 2022; Riitsalu & Murakas, 2019; Sehrawat et al., 2021; Xue et al., 2020). Indeed, mediators play a crucial role in understanding the impact of financial literacy on financial well-being.

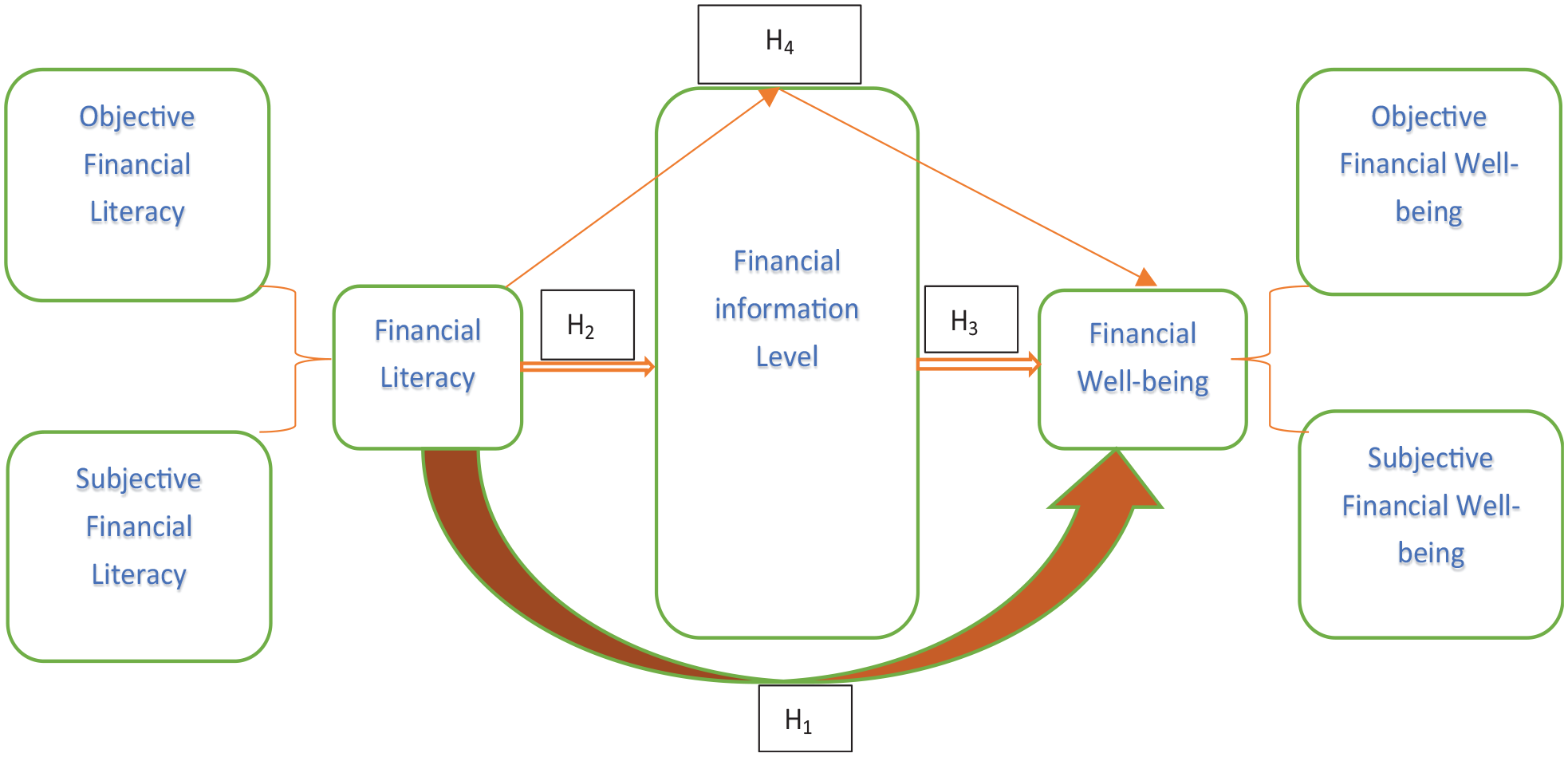

In line with this shift, the current study integrates the Resource Dependency Theory (RDT) by Pfeffer and Salancik (1978), Life Cycle Hypothesis (LCH) by Modigliani and Brumberg (1954), and Prospect Theory (PT) by Kahneman and Tversky (1979). These theories identify three key factors: knowledge, information, and well-being. Theoretically, rational households rely on information resources for decision making. The PT examines rationality in households’ choices and preferences, assuming that financial literacy underpins rational decision-making. The RDT emphasizes the role of information in guiding financial decision-making, while LCH focuses on how financial well-being will be achieved, building on insights from both PT and RDT. We propose that knowledge fosters information-seeking behaviour, and together, these elements contribute to financial well-being. Therefore, integrating these three theoretical views into a unified analytical framework, as illustrated in the Figure, represents a significant contribution to the literature.

FL and FWB

Households with higher FL are more likely to experience improved FWB. Research suggests that higher levels of financial literacy contribute to greater financial satisfaction (Koomson et al., 2023; Limbu & Sato, 2019; Zhang & Chatterjee, 2023). Chu et al. (2017) argue that households with advanced financial knowledge and skills are more likely to choose appropriate financial products and services that meet their financial goals, as well as adopt profitable investment strategies (Kramer, 2016) relevant to both current and future financial needs. This, in turn, is expected to increase financial returns and well-being (Xue et al., 2020).

A growing body of research highlights the positive link between financial literacy and financial well-being. For instance, Rutherford and Fox (2010) assert that young adults’ finances significantly influence their financial satisfaction and overall well-being. Likewise, Chu et al. (2017) demonstrate that enhanced financial literacy enables households to make superior investment decisions and attain favourable returns. Karki et al. (2024) emphasize that financial literacy enhances financial well-being, while Zhang and Chatterjee (2023) and Korankye and Pearson (2023) show that effective financial management strengthens household financial well-being. Collectively, these findings underscore the crucial role of financial literacy in promoting financial security and well-being, reinforcing the link between FL and FWB as illustrated in Figure 1. While some studies have documented this positive relationship in Ghana settings (Amidu et al., 2021; Matey, 2021), they do not focus on the link between financial literacy and well-being in the rural context. Hence, this study posits the following hypothesis.

Study’s analytical model.

FL and FIL

Few studies have examined consumer behaviour to assess the extent of information consumption in decision-making (Kim et al., 2022). Financial literacy plays a crucial role in shaping consumers’ judgment about the accuracy and reliability of financial information (Kienzler et al., 2022). The increasing volume of financial information available may be linked to the growing complexities of the financial market (Lusardi et al., 2017). A higher level of financial information acquisition can be facilitated through financial literacy (Obi-Anike et al., 2023). Households’ financial literacy shapes their financial behaviour, particularly regarding information consumption (Houghton & Sheehan, 2000). To effectively interpret and utilize financial information, households must first possess a foundational level of financial literacy. Prior research suggests that for households to apply financial knowledge and make well-informed decisions, they need access to and an increased level of financial information (Fernandes et al., 2014; Shim et al., 2012). Yet, no empirical evidence directly supports this claim. If a household’s financial knowledge has the potential to affect the level of information accessed, an essential precursor to financial decision-making, then financial literacy and financial information levels are expected to be positively related. Hence, the following hypothesis is proposed:

FIL and FWB

An earlier study argued that the FIL is critical in shaping people’s perceptions, opinions, and understanding of an issue (Lee et al., 2017). The impact of information can be either negative or positive, depending on the environment (Dessaint et al., 2024). Therefore, information consumption is a double-edged sword; it may improve or discourage well-being. For example, Summers et al. (2005) contend that greater financial information consumption can enhance saving behaviour, while others argue that excessive information consumption can result in information overload and deter savings (Li et al., 2024). Determining the influence of financial information on FWB thus requires an awareness of its attributes, including its level (basic, intermediate, or advanced). However, it does appear there is no empirical evidence to determine the effect of FIL on FWB. Whether it positively or negatively influences FWB is an empirical question; hence, there is a need to conduct a formal analysis of the effect of FIL on FWB. Given that advance information is expected to improve financial knowledge, hence in this study we speculate that FIL is expected to positively influence FWB.

Mediating Role of FIL in the Link Between FL and FWB

Financial information level is a crucial factor competent to explain the impact of FL on households’ FWB in rural settings. Consequently, in describing the link between FL and FWB, FIL may function as a mediator. Financial literacy is recognized as a crucial factor influencing participation in financial information consumption (Kuutol et al., 2024). Some studies emphasized how financial information plays a critical role in establishing a connection between FL and a range of financial outcomes, such as saving for retirement (Jappelli & Padula, 2013), building wealth (Koomson et al., 2023), and adopting sound financial practices (Mabula & Han, 2018). The literature suggests that the linkage between FL and FWB can be enhanced via mediating factors, including the dimensions of financial information. As such, earlier studies have called for intervening variables to explain the relationship (Tahir et al., 2021; Xue et al., 2020), yet this dimension of FIL is missing in current literature as a mediator. From this perspective, this study’s interest lies in the financial information level as a dimension of financial information to mediate the relationship. The discussion above suggests that a household’s financial well-being can be determined by the combined effect of FL and FIL. Thus, we hypothesize that:

Empirical Literature and Contribution of the Study

Prior work relevant to our investigation includes Akande et al. (2023), Chipunza and Fanta (2024), Timbile and Kotey (2022), Twumasi et al. (2022), Amidu et al. (2021), and Twumasi et al. (2021). Akande et al. (2023) assessed financial literacy and financial inclusion in rural Eastern Cape, South Africa, using variance-based structural equation modelling. Their findings indicate that financial literacy facilitates inclusion. Chipunza and Fanta (2024) assessed whether the relationship between financial inclusion and asset holding enhances consumers’ subjective well-being (SWB) in South Africa. They measured financial inclusion through credit, savings, and insurance, whereas multiple correspondence analysis was employed to compute an asset index that captured indicators of individual material possessions. The findings suggest that financial inclusion has an indirect positive impact on SWB through increased asset holding.

Twumasi et al. (2021), using data collected from rural areas in the eastern region of Ghana, found that households with higher income benefit more from access to financial services. In a related study, Twumasi et al. (2022) assessed the mediating role of access to financial services using data from 572 participants across the four regions of Ghana- Northern, Central, Eastern, and Brong Ahafo- where rural populations are more prevalent. Their findings indicate that access to financial services mediates the positive effect of financial literacy on income. Amidu et al. (2021) explored the relationship between financial inclusion and livelihood activities of people in Ghana, using a bivariate probit model to examine the relationship between financial inclusion and financial literacy. The study found that the interaction of financial inclusion with financial education improves the livelihood of households. Similarly, Timbile and Kotey (2022) assessed the impact of financial inclusion on household income in the Wa West district of UWR, using survey data from 373 households. Their findings suggest that greater financial inclusion improved households’ income. Our study differs from these prior studies in that they do not investigate the role of financial information, nor do they specifically address financial well-being and how it results from the interaction between financial literacy and financial information. This line of enquiry is particularly relevant in contexts where low literacy rates and sociocultural factors can hinder optimal financial decision-making. At the same time, these barriers coexist with enabling factors such as literacy education programmes and increased access to financial information through the internet and mobile phones. The next section discusses the Materials and Methods.

Research Material and Method

Study Site and Population

The study population consists of households in rural areas of Ghana’s Upper West Region (UWR). This region was selected due to its designation as the country’s poorest and its involvement in various FL and inclusion interventions since the Ghana Statistical Service (GSS) Report 2015. Understanding this population is crucial for formulating policies that address their specific needs, and the findings can be generalized to similar populations in comparable settings. According to statistics published by GSS 2021 Housing and Population Census (HPC), the UWR has a total of 190,761 households and a population of 878,824. Of these, 70.5% (134,487) of the households are in rural communities in the region (UWR Coordinating Council Report, 2021). Additionally, 73.6% of the UWR population resides in rural areas with a literacy rate of 46% (GSS, 2021).

In this study, we employ structural equation modelling-partial least squares (SEM-PLS) to explore interactions between FL, FIL, and FWB from the perspective of rural settings in the region. Figure 1 above illustrates the study’s primary focus, highlighting FIL’s mediating role in the relationship between FL and FWB (H4) as the central aspect of the investigation. The partial least squares structural equation modelling (PLS-SEM) method was selected for its distinctive advantages in managing complex models with several components and interactions, rendering it appropriate for exploratory and predictive research. For example, unlike covariance-based SEM (CB-SEM), which emphasizes theory validation, PLS-SEM prioritizes the maximization of explained variance in dependent components, consistent with the study’s objective to comprehend and estimate essential interactions within a complex framework. It supports both reflective and formative measurement models, manages relatively small sample sizes with substantial statistical power, and does not necessitate stringent assumptions regarding data distribution. These aspects augment the scientific rigour of the study, facilitating flexibility and robustness in the analysis of intricate linkages and the generation of actionable findings.

Sample Size and Data Collection

Determining an appropriate sample size is critical for research accuracy and ensuring a representative population depiction (Pirani, 2024). To establish the sample size, we used an online sample size calculator (www.surveyststem.com) to determine a suitable minimum sample size of 598. The sample size calculation adheres to established protocols, employing a 95% confidence level and a 4% margin of error, which are recognized benchmarks for obtaining reliable and generalizable results. However, according to (Pirani, 2024), the minimum sample size required for structural equation model-partial least squares is 10 times the number of items for most construct items. Pirani’s (2024) guideline for SEM-PLS analysis mandates a minimum sample size of at least 10 times the number of items per construct to provide sufficient statistical power for identifying relationships within the model. With 26 items and 3 constructs in this study, it gives us a minimum sample size of 260. But the calculated sample size significantly surpasses the minimum requirement, illustrating the robustness of the sample design and its conformity with recognized SEM-PLS standards. In the end, we collected data from 663 heads of households using a structured questionnaire.

Simple random sampling was employed after each district in the region was seen as a cluster from which to draw samples as a representative of the population. All 11 districts in the region were represented in the sample. Each district’s sample was representative of its rural household relative to the chosen sample size, ensuring a fair representation. Simple random sampling was selected for its straightforwardness and efficiency in obtaining a representative sample from the population. Stratified sampling may have yielded more accurate estimates by considering district-level variances; nevertheless, it was considered unnecessary due to the largely uniform characteristics of the rural population in the region. Furthermore, the absence of dependable and current data regarding district-level socioeconomic attributes rendered stratification unfeasible. District population statistics were sourced from the HPC, 2021, offering a dependable and uniform data source on which each district was assigned a minimum sample size. The sample size for each community was determined by using the combined population of all the selected communities within the districts relative to its assigned sample size.

Survey Instrument

Structured questionnaires were adopted for data collection in this study, offering a standardized approach to obtain consistent and similar replies. The questionnaire was developed using known measures and literature, guaranteeing its conformity with the study’s objective. To augment reliability, it was culturally tailored to the rural Ghanaian in the Upper West region via translation and alteration to include local vocabulary and subtleties. A pilot test was conducted in a representative rural community to evaluate its clarity, relevance, and reliability, leading to small modifications to enhance understandability and response precision. Following Blumberg et al. (2014), they suggested a sample size of 25 to 100 subjects for a pilot study that produces accurate results. These measures validate the questionnaire’s efficacy and dependability within the study’s setting, guaranteeing the acquisition of significant data. The pilot study for this study used 64 respondents to assess the research instrument’s credibility. It was noted that two of the indicators adopted were not loading properly in the rural context; therefore, those questions were simplified for greater clarity. See Appendix A, the adopted and modification of question

Biases Mitigation

To mitigate potential biases, various procedures were implemented. Non-response bias was mitigated by visiting homes to promote participation and earlier participation in community meetings. The survey questionnaire underwent pilot testing to guarantee cultural sensitivity and clarity, hence minimizing the potential for item non-response bias. Additionally, data weighting methods were utilized to correct for any residual biases, guaranteeing that the final sample accurately represented the rural population. These initiatives resulted in a substantial response rate of 97%, substantiating the assertion of unbiased and thorough representation.

Empirical Strategy

We utilized partial least squares structural equation modelling (PLS-SEM) with SmartPLS 4, in line with the recommendations of Hair et al. (2019), to analyse the interrelationships among various constructs as outlined in the analytical framework. PLS-SEM is a second-generation statistical method that integrates the advantages of multiple regression and factor analysis, allowing for the simultaneous examination of both direct and indirect effects of exogenous and endogenous variables. To assess statistical significance, we employed a bootstrapping procedure with 10,000 resamples.

Response Rate

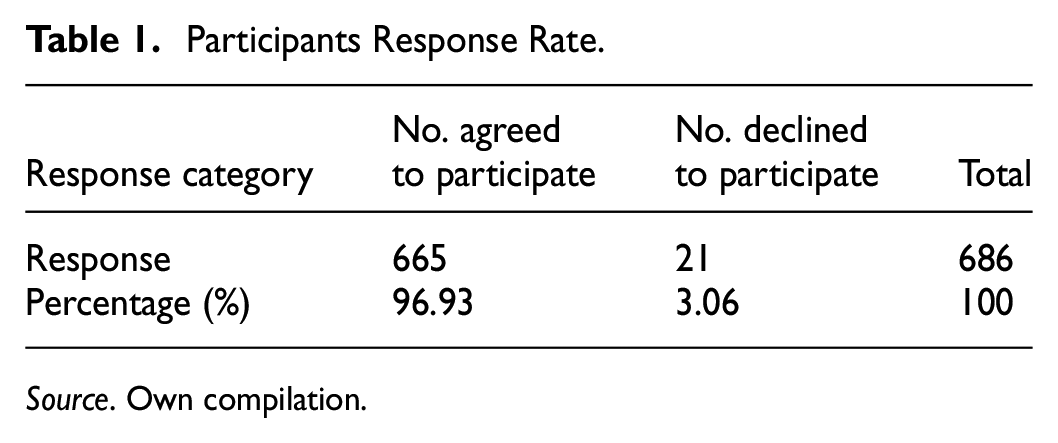

As mentioned earlier, the target population was the heads of households living in rural settings, as defined by the Ghana Statistical Service in the UWR of Ghana. Two major questions were asked when a household was randomly selected to judge exclusion or inclusion into the sample. These questions were “Are you a head of the household?” If yes, the next question follows: “Are you 18 or older?” If yes, include the person in the survey; otherwise, exclude. Neither of the two questions disqualified the person from participating in the survey. Due to high illiteracy levels in the rural region, researchers used research assistants to administer questionnaires through random household interviews, ensuring participant understanding and accurate data collection. Out of 684 heads of household contacted, 21 declined, and the remaining 663 gladly participated. The average response rate employing a traditional survey data collection method was 58.68% (Beehr et al., 2024). So, 96.93% of the results achieved in this study are proactively high response rates. Table 1 shows the response rate.

Participants Response Rate.

Source. Own compilation.

Data Analysis and Results

From Table 2, the overwhelming majority, representing 95.6%, were male, while the remaining 4.4% were female. This indicates a gender imbalance in household leadership positions in rural settings. Due to gender role ideology, attitudes, socialization, and cultural circumstances, the female gender is denied household leadership responsibilities in the region as leadership and responsibility are seen as exclusively male pursuits. The finding confirms that African women are underrepresented in leadership roles (MacLean et al., 2020). The low female representation suggests a genuine disparity in female representation in household leadership. The respondents’ ages are distributed over various age groups, making them quite diverse. The 30-39 age range comprises the largest age group, suggesting a higher likelihood of this cohort’s participation in family leadership. The survey sample appears to include a wide range of ages, as indicated by the significant proportions observed in other age categories. Over 80% of the respondents are in the active labour force bracket. This further improves the generalizability of the results.

Respondents Demographic Characteristics.

A significant portion of the surveyed population has relatively large families, as evidenced by the distribution of biological child counts, which shows a wide range of family sizes among respondents. The presence of respondents with 5 to 6 biological children suggests a subset of the population with particularly large families, which may have implications for resource allocation, family dynamics, and societal support systems. The most common category is having 3 to 4 biological children, followed closely by 1 to 2 children. Similarly, according to the data, adopted children were less common in the sample population than biological offspring.

The fact that most respondents do not have adopted children suggests that adoption is not as widespread in this demographic. Notwithstanding, a sizable percentage of respondents—especially those in the 1 to 2 adopted children category—have children of their own. This suggests that the surveyed group has some degree of adoption openness or interest.

The distribution of housing status offers information on the studied population’s housing circumstances. A sizable percentage of responders reside in their own homes, suggesting some degree of independence and ownership. A significant percentage of them living in their parents’ homes implies a dependence on cultural norms or family support for intergenerational living. The comparatively low proportion of respondents living in rental properties and homes provided by institutions suggests that the surveyed population prefers home ownership or family-based living arrangements.

Study Key Constructs

The study’s key constructs were also examined relative to the averages. Table 3 shows the outcome, indicating the various means score for the three main constructs.

Descriptive Statistics Constructs.

The findings indicate that, on average, respondents believed they possessed a somewhat higher than average level of financial literacy. This is supported by the higher mean score of 3.68/7. It might point to a tendency for people to underestimate how much they know about money (Huang et al., 2023) in rural settings. The evaluation of financial well-being in rural households resulted in a lower score of 3.26/10, highlighting diminished values recorded for financial well-being among most of the respondents. This could be due to economic, psychological, social, and personal factors contributing to reduced financial well-being. People’s quality of life and financial well-being can be enhanced by addressing these underlying causes through policy interventions and support services. The average financial information level is reported as 3.59/7 in the study context. This indicates almost a tie between financial literacy and financial information.

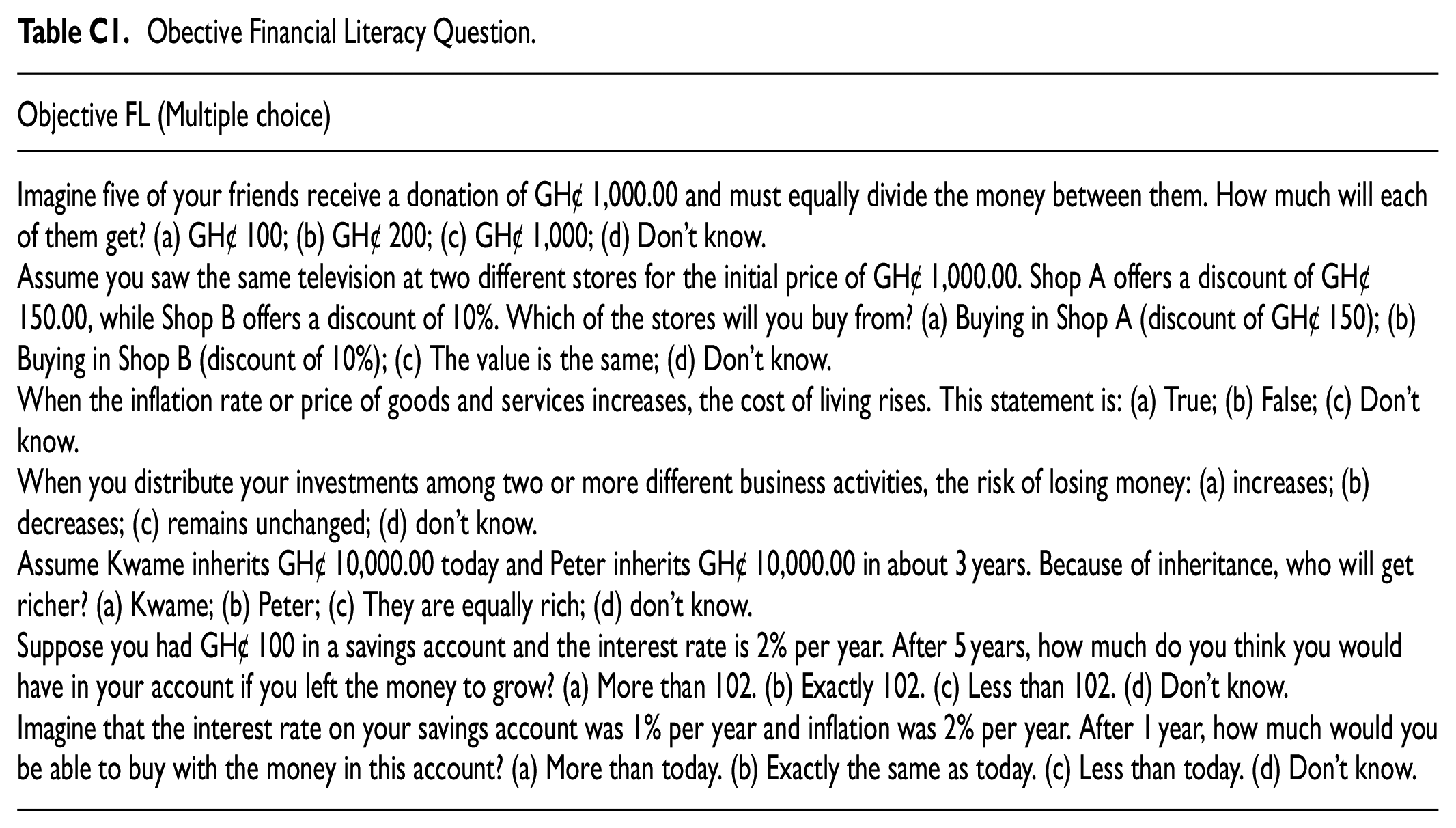

The objective financial literacy of study participants was evaluated by a seven-item questionnaire, consisting of quiz-style items frequently employed in the existing literature (Lusardi & Mitchell, 2011; Twumasi et al., 2022). The questions are shown in Appendix C. The score depends on the number of questions answered correctly.

Lower Order Construct (LOC)—Measurement Model Assessment

Reliability and Validity

The LOC are not the focus of the analysis; instead, it ensures that the scores generated for the HOC are reliable and valid. Table 4 shows the results of the factor loading, construct reliability, and average variance extracted (AVE) for construct validity, with factor loadings between 0.533 and 0.952. For an indicator to be reliable, it should have a factor loading of 0.7 or more (Hair & Alamer, 2022; Hair et al., 2019). However, for an indicator to be deleted from a construct, such an indicator should significantly impact the reliability and validity of the construct (Hair et al., 2019). Although three indicators, that is, the ability to identify the cost for taking credit (subjective financial literacy indicator), encountered payment problems monthly (objective financial well-being indicator) and living paycheck to paycheck (subjective financial well-being indicator), loadings fell short of the recommended threshold, they did not impact significantly on the respective constructs and hence were retained. Similar to Sehrawat et al. (2021), they did not delete indicators that fell short of the recommended threshold because such indicators did not negatively impact the validity and reliability of the constructs.

Reliability and Validity.

Note. α = Cronbach alpha; CR = composite reliability; AVE = average variance extracted.

Additionally, Table 4 shows that construct reliability via Cronbach’s alpha and composite reliability (CR) denotes satisfactory outcomes. Alpha and composite reliability values lie between .880 and .958, above a minimum threshold of 0.6 as recommended (Van Griethuijsen et al., 2015). For convergent validity to be established, the AVE value must be 0.5 or greater (Fornell & Larcker, 1981). Table 4 demonstrates that all the constructs have an AVE value above 0.50, indicating that convergent validity is established for all the constructs.

Discriminant Validity

Measurement of discriminant validity was based on Heterotriat-Monotriat (HTMT) and Fornell-Larker Criterion (FLC). Apart from Fornell and Larker’s Criterion and cross-loading, Hair et al. (2019) note that HTMT is one method used to assess measurement model discriminant validity. Discriminant construct validity measures how different a construct is from the other constructs in a model (Chin, 2009; Fornell & Larcker, 1981). HTMT is suggested in empirical studies to have superior outcomes over FLC (Henseler et al., 2015); thus, it is dominant in contemporary studies. For discriminant validity to be established in the case of HTMT, all pair constructs should have a value below 0.90 (Hair et al., 2019). In the case of FLC, the square of the AVE of any construct must be greater than the squared correlation of any two constructs. From Table 5, using HTMT to assess discriminant validity, the results indicate that no value is above 0.90, thus confirming discriminant validity. Equally, the square root of AVE is greater than all pair constructs, thus confirming discriminant validity.

Discriminant Validity.

Note. FLO = Objective Financial Literacy; FLS = Subjective Financial Literacy; FWBO = Objective Financial Well-Being; FWBS = Subjective Financial Well-Being; FIL = Financial Information Level.

Higher Order Construct (HOC) Assessment

After confirming the validity and reliability of the lower-order constructs, the construct scores were entered into a reflective model to produce the HOC reliability and validity, as shown in Table 6. Each of the HOC constructs of FL and FWB was evaluated for discriminant validity, convergent validity, and reliability as part of the validation of the higher-order construct measurement model (Hair et al., 2019). These metrics were subject to the same standards and limitations as the lower-order constructs. In that sense, the validity and reliability of these constructs were validated for this research. Indeed, the results similarly confirmed reliability and validity at the HOC level (Figure 2).

HOC Reliability and Validity.

Path model for HOC.

Structural Model and Testing of Hypotheses

Table 7 summarizes FL, FWB, and FIL model quality assessment metrics. The results indicate moderate explanatory power and good predictive relevance for the constructs, which exhibit a good model fit. Conversely, the FWB concept has a weaker model fit, lower explanatory power, and poorer predictive relevance than FIL. The VIF numbers suggest multicollinearity is not an issue for the FL or the FIL constructs. The model is generally more relevant and dependable for the empirical investigation.

Model Fit Assessment.

f2 indicates significance.

The SEM-PLS model exhibits diverse results. The SRMR score of 0.096 indicates a satisfactory fit of the structural model, albeit slightly below the acceptable threshold of 0.1 as proposed by Hu and Bentler (1999). A value of 0.610 d_ULS indicates a moderate to favourable fit. This indicates that the model is fairly accurate; however, there may be potential for enhancement. A d_G value of 0.567 indicates a decent fit. This suggests that the model is relatively accurate.

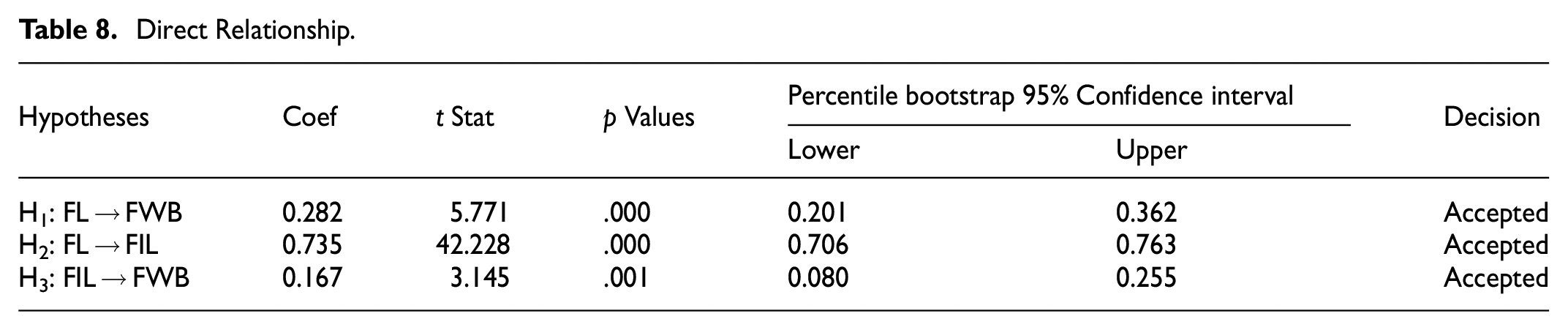

Following the validation of the measurement model for both HOC, LOC and model fit, it is certified that the models are appropriate for their intended use. To determine the relationships, the hypotheses that were put forth for this study were evaluated. The structural model results for the hypotheses under discussion are shown in Tables 8 and 9. Three direct paths and one indirect approach were assessed, as can be seen in Tables 8 and 9, to correspond to the different hypotheses of this study.

Direct Relationship.

Mediation: Mediating Role of FIL on the Relationship Between FL and FWB.

The first hypothesis assesses the assertion that FL influences FWB even in the presence of financial information level. As shown in Table 8, the finding indicates a significant positive relationship even in the presence of FIL (β = .282; p < .001). Hence, H1 is supported. A positive change in FL drives a significant positive change in the FWB of rural folks. The finding further revealed that FL is significant and positively related to the financial information level of consumption (β = .735; p < .001), supporting H2. As household head FL increases, so does the chance of increasing the level of financial information consumption.

Additionally, the level of financial information is positively related to FWB (β = .167; p < .05). This finding gives support to H3. This implies that the level of financial information consumption is a significant determinant of FWB.

The level of financial information is central to whether FL can affect FWB. Thus, it was hypothesized that financial information level mediates the relationship between FL and FWB in rural settings. Based on the information in Table 9, the study found a significant indirect relationship (β = .123; p < .05; t = 3.107) between FL and FWB through the financial information level. The finding thus signals partial mediation. The result points to the fact that FIL helps to explain the relationship between FL and FWB. However, not the only factor at play. While FL affects FWB directly, it might also pass through the level of financial information consumption to sufficiently affect FWB. Increasing FIL can help improve the positive effect of FL on FWB. Conversely, mediation could be absent in the relationship on three counts; (1) if the indirect effect showed insignificant, (2) if the direct effect of FL on FWB wasn’t significant without mediation variable, (3) if no significant total effect of FL on FWB including both direct and indirect. However, none of the thesis scenarios were present in the result, thus signalling a partial mediating role of FIL. Given the positive relationship in the specific indirect effect, the partial mediation is determined to be complementary.

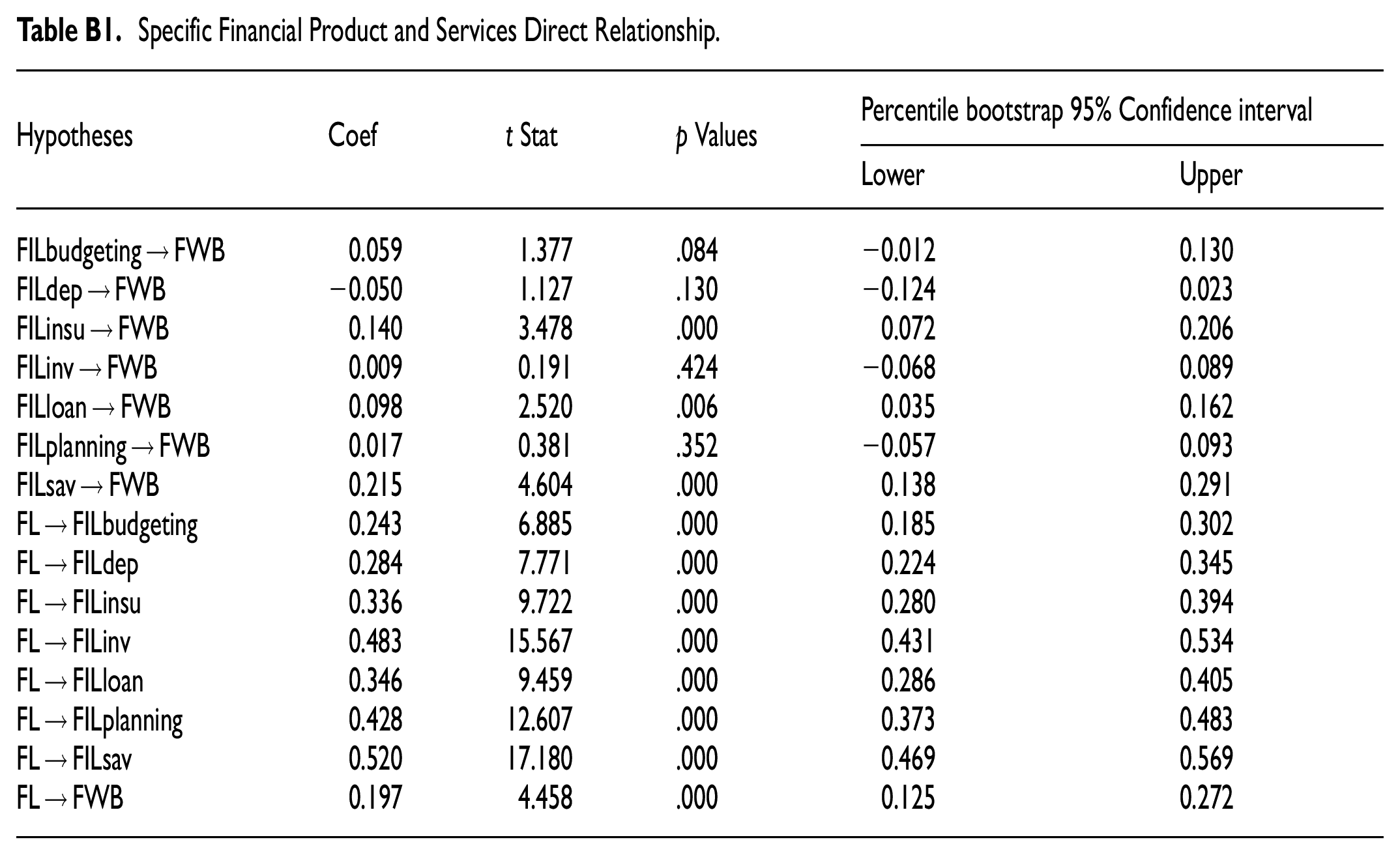

Critical financial products, regularly available to households, were chosen for further analysis to better understand the information level. The household level of information on the selected financial products was assessed and used as a mediator in the relationship shown in Appendix B. Table 10 shows that the increasing financial information level on specific financial products mediates the relationship between FL and FWB. The results show that FIL on savings (FILsav) mediate the relationship between FL and FWB (β = .112; p < .001). Furthermore, FIL on insurance (β = .047; p < .05) and FIL on loan (β = .034; p < .05) mediate the relationship between FL and FWB. These outcomes of the study indicate that increasing information on saving, insurance, and loans is one of the important mediums of FL to improve FWB. These findings establish the mediating role of FIL on savings, loans, and insurance, supporting hypothesis H4.

Mediation for Specific Financial Products.

Note. FILsav = FIL on savings; FILloan = FIL on loan; FILinsu = FIL on insurance; FILinv = FIL on investment; FILdep = FIL on deposit; FILplanning = FIL on financial planning; FILbudgeting = FIL on financial budgeting.

On the contrary, FIL on investment (β = .004; p > .05), FIL on deposit (β = −.014; p > .05), FIL on financial planning (β = .007; p > .05) and FIL on financial budgeting (β = .014; p > .05) are not important mediating factors in the relationship between FL and FWB. The non-significant relationships indicate that FIL on investment, deposit, financial planning, and financial budgeting has no discernible impact on the direct effect of FL on FWB. In this instance, there might be a more pronounced association between FL and FWB, and the mediating role is felt through FIL on savings, insurance and loans to explain the relationship more clearly. Therefore, the impact of FL on FWB does not require the transmission effect of FIL of these identified financial products. The findings on FIL on investment, deposit, financial budgeting, and financial planning on the mediating role in the relationship between FL and FWB did not support H4.

Using variance accounted for (VAF) to determine the strength of the indirect effect, the joint mediating effect of savings (0.112/0.402 = 0.28), insurance (0.047/0.402 = 0.12), and loan (0.034/0.402 = 0.08) account for (0.28 + 0.12 + 0.08 = 0.48) 48% of the total effect. This indicates partial mediation, and the mediating role is complementary. However, the impact of increasing financial information level on saving accounted for 58% of the joint effect.

Discussions

Low FL continues to be a significant global concern, weakening FWB and impacting societal and human development. Although substantial evidence links FL to FWB and its associated mediating factors, the role of FIL is less represented in the literature. This study focused on FILs in the relationship between FL and FWB, specifically in rural settings, addressing a research gap that has predominantly concentrated on urban areas. By examining rural settings in Ghana, our research aimed to provide more insights into how FL can impact FWB in developing economies and evaluate Ghana’s progress towards policy targets for marginalized populations. These insights are intended to inform better and potentially shift policy directions to achieve the Sustainable Development Goals (SDGs). The key questions addressed in this study are: (1) Are FL and FIL determinants of FWB? (2) What role does FL play in influencing FIL? (3) How does FIL affect the relationship between FL and FWB in rural settings?

First, the study found a significant and positive relationship between FL and FWB in rural settings, highlighting the function of FL in improving FWB. This discovery corroborates Hypothesis H1 and aligns with Prospect Theory, indicating that people’s financial decisions are shaped by cognitive biases and heuristics. In this setting, increased financial literacy empowers households to make better-informed decisions, reducing the influence of cognitive biases on their financial well-being. This finding is consistent with the Life Cycle Hypothesis, which posits that individuals’ household financial behaviour and well-being fluctuate over several life stages. In rural areas, increased financial literacy can enable these economic agents to make more informed financial decisions throughout their life cycle, thereby improving their financial well-being. Our study findings regarding H1 align with prior research establishing a positive and significant relationship between FL and FWB in rural settings (Akande et al., 2023; Amidu et al., 2021; Korankye & Pearson, 2023; Kuutol et al., 2024; Xue et al., 2020; Zhang & Chatterjee, 2023) across both developing and developed countries. For instance, Akande et al. (2023), investigating FL and financial inclusion for rural agrarian sustainable livelihood in South Africa using SEM-PLS, found that FL significantly and positively influences sustainable livelihood in the rural settings. These prior studies support the notion that achieving FL is crucial in improving FWB, particularly in rural settings. Our findings are consistent with those of earlier studies, highlighting that FL independently contributes to FWB in rural contexts. However, some studies offer contrasting views. For instance, Mugenda et al. (1990), Xiao et al. (2014), and Pak and Chatterjee (2016) found no significant relationship between FL and FWB. Xiao et al. (2014) found that high financial knowledge negatively impacted financial satisfaction, suggesting that excessive knowledge might not always translate into better satisfaction. Our study addresses this discrepancy by combining subjective and objective assessments of FL and FWB, providing clarity on their relationship.

Second, a significant positive relationship was observed between FL and FIL. This finding suggests that higher FL leads to greater financial information consumption. As household heads become more financially literate, they are more likely to seek and use financial information. These findings align with Prospect Theory, indicating that household heads are inclined to seek additional information when they anticipate a prospective gain or loss, and that those with greater financial literacy are more adept at recognising and pursuing financial possibilities. This link also aligns with Resource Dependency Theory, which asserts that people endeavour to obtain and utilize resources, such as financial information, to accomplish their objectives and mitigate uncertainty. As households enhance their financial literacy, they are increasingly able to see the significance of financial information as a resource, prompting them to actively pursue and utilize it to guide their financial decisions and reduce potential risks. These study findings align with Van Rooij et al. (2011), who demonstrated that FL enhances information consumption in the stock market, thereby improving financial resource management. This supports the view that FL increases the demand for and utilization of financial information, as confirmed by Swiecka et al. (2020), who argued that financial behaviour, attitudes, skills, and knowledge all contribute to financial information demand.

Third, the study’s result that financial information level (FIL) has a significant positive link with financial well-being (FWB) highlights its crucial role in enabling households to attain financial well-being. To improve FWB, increasing FIL is essential, making FIL a key factor in achieving financial well-being in rural settings. This link strongly corresponds with Resource Dependency Theory, which asserts that access to and control over essential resources such as financial information improve a household’s capacity to manage uncertainties. FIL provides households with the expertise to proficiently leverage financial services and products, including savings, loans, and investments, thereby diminishing vulnerabilities and fostering self-sufficiency. Moreover, the results align with the Life Cycle Hypothesis, which posits that people strategize their spending and savings patterns throughout their lifespan to maximize utility. An elevated FIL empowers rural folks to make informed decisions regarding savings and investments, hence promoting more consistent spending patterns and financial stability across various life phases. Collectively, these theoretical frameworks underscore the significance of FIL as a resource that not only improves immediate financial welfare but also fosters long-term financial resilience and sustainability in rural communities. The results regarding hypothesis H3 is also consistent with Meng (2023), who found that higher financial information and capabilities significantly improve FWB in China. Summers et al. (2005) noted that financial information consumption can be a double-edged sword, potentially improving or worsening FWB depending on the context. This supports our finding that FIL is crucial for enhancing FWB. Our study also concurs with Kuutol et al. (2024), who emphasizes the importance of financial information characteristics in achieving FWB. We observe that increased FIL leads to better decision-making, which aligns with Ching et al. (2022), who found that higher information consumption promotes sustainable decision-making.

Fourth, the study illustrates that FIL mediates the relationship between FL and FWB, stressing a cohesive theoretical framework that integrates Prospect Theory, Resource Dependency Theory, and the Life Cycle Hypothesis. Prospect Theory asserts that people’s financial actions, particularly in uncertain conditions, are shaped by their framing and perception of tomorrow. FIL augments this framing process by enhancing decision-making quality, enabling households to convert their financial literacy into actions that maximize outcomes through financial information. Resource Dependency Theory enhances this by identifying FIL as an essential resource that empowers people to proficiently obtain and employ financial knowledge, therefore manoeuvring through financial systems, both formal and informal, to attain increased control and stability. The Life Cycle Hypothesis elucidates this relationship, positing that financial literacy enables households to effectively modify their financial behaviour—such as saving and investing—throughout various life stages, hence stabilizing consumption patterns and improving financial security over time. Collectively, these theoretical perspectives emphasize that whereas financial literacy establishes the basis for financial competence, financial information functions as the means by which this information is applied, hence enhancing its crucial role in fortifying the connection between FL and FWB. This collaborative theoretical framework highlights the interrelation of cognitive framing, resource allocation, and life-stage planning in improving financial well-being in rural settings. Our findings corroborate the idea that the effect of FL on FWB may be indirect, with FIL serving as a significant mediator in this relationship, as supported by prior research (Lone & Bhat, 2024; Tahir et al., 2021; Xue et al., 2020). Consistent with several studies that applied mediating factors to explain the transition of FL to FWB (Amidu et al., 2021; Chipunza & Fanta, 2024; Selvia et al., 2021; Twumasi et al., 2022).

Furthermore, the results indicate that FL substantially affects FIL on savings, loans, and insurance to improve FWB; however, FIL concerning investments does not serve as a significant mediating factor. This gap can be ascribed to the urgent financial concerns and limitations encountered by rural folks. Rural households frequently prioritize short-term financial needs, including debt management, obtaining loans for immediate expenses, and acquiring insurance to reduce health risks, which are more closely related to their financial stability. Conversely, investments typically require long-term strategizing and entail greater perceived risks, which may appear less attainable or pertinent in an environment characterized by limited disposable income and mostly short-term financial objectives. Furthermore, limited exposure to investment opportunities and inadequate infrastructure in rural areas may contribute to lower engagement with investment-related information. Likewise, FIL concerning deposits, financial budgeting, and financial planning did not mediate the FL-FWB link, indicating that although these elements are essential for financial stability, they may not immediately result in quantifiable enhancements in FWB in rural contexts. This may arise from restricted access to formal financial institutions, cultural inclinations towards informal saving methods, or an absence of immediate recognized advantages from these practices.

In the context of rural Ghana, increasing financial information can significantly enhance perceptions of financial management and FWB. The findings emphasize that the level of financial information is not merely a choice but a critical component for securing financial well-being. This study provides empirical evidence that FL enhances financial information, and higher FIL improves FWB. Theoretical frameworks like Prospect Theory and Resource Dependency Theory support these relationships, suggesting that increased information level can lead to better financial decision-making and well-being. Engaging in FL education and increasing financial information consumption are essential steps for rural individuals to improve their financial future and overall well-being.

Conclusion, Implications, and Future Research

Conclusion

The study explores the volatile nature of the current informational world, focusing on the interplay between financial literacy (FL), financial information level (FIL), and financial well-being (FWB). Using the HOC reflective-reflective construct, the research empirically examines how these elements interact and the mediating role of FIL in the relationship between FL and FWB. The findings reveal that FL significantly enhances FIL and FWB, highlighting the critical role of financial information in achieving FWB. Specifically, the study found that increased financial information level on savings, insurance, and loans partially mediates the relationship between FL and FWB in rural Ghana. Financially literate households are better positioned to consume financial information and achieve healthy financial goals compared to those who are financially illiterate.

Implications

The study’s results provide significant insights for policy interventions in rural Ghana and broader theoretical implications. The findings highlight the crucial roles of financial literacy and financial information level in improving financial well-being, heightening the necessity for specialized financial education programmes that concentrate on practical and urgent financial matters, including savings, loans, and insurance, which directly influence FWB, while progressively fostering awareness and confidence in long-term investment strategies. This underscores the necessity for policymakers to develop accessible financial services and customized financial education initiatives that align with the distinct socio-economic conditions of rural folks rather than the current government blanket programme. The study theoretically consolidates and integrates concepts from Prospect Theory, Resource Dependency Theory, and the Life Cycle Hypothesis, demonstrating the interplay between financial knowledge and its application in shaping decision-making, resource allocation, and financial behaviour throughout various life stages. These observations underline the importance of integrating knowledge with actionable information to foster sustainable financial well-being, establishing a basis for future research to investigate context-specific solutions for enhancing financial literacy and resilience in marginalized communities.

Future Research Directions

The study acknowledges limitations, such as focusing solely on subjective measurements of financial information levels. Future research should incorporate objective measurements to conceptualize these characteristics better. Additionally, exploring other financial information characteristics like quality, source, and pattern can provide a deeper understanding of the FL-FWB relationship. Future research should also consider multigroup analysis to effectively influence policies targeting rural populations.

Footnotes

Appendix A: Path Model for LOC

Appendix B: Structural Path for Specific Financial Product and Services

Specific Financial Product and Services Direct Relationship.

| Hypotheses | Coef | t Stat | p Values | Percentile bootstrap 95% Confidence interval | |

|---|---|---|---|---|---|

| Lower | Upper | ||||

| FILbudgeting → FWB | 0.059 | 1.377 | .084 | −0.012 | 0.130 |

| FILdep → FWB | −0.050 | 1.127 | .130 | −0.124 | 0.023 |

| FILinsu → FWB | 0.140 | 3.478 | .000 | 0.072 | 0.206 |

| FILinv → FWB | 0.009 | 0.191 | .424 | −0.068 | 0.089 |

| FILloan → FWB | 0.098 | 2.520 | .006 | 0.035 | 0.162 |

| FILplanning → FWB | 0.017 | 0.381 | .352 | −0.057 | 0.093 |

| FILsav → FWB | 0.215 | 4.604 | .000 | 0.138 | 0.291 |

| FL → FILbudgeting | 0.243 | 6.885 | .000 | 0.185 | 0.302 |

| FL → FILdep | 0.284 | 7.771 | .000 | 0.224 | 0.345 |

| FL → FILinsu | 0.336 | 9.722 | .000 | 0.280 | 0.394 |

| FL → FILinv | 0.483 | 15.567 | .000 | 0.431 | 0.534 |

| FL → FILloan | 0.346 | 9.459 | .000 | 0.286 | 0.405 |

| FL → FILplanning | 0.428 | 12.607 | .000 | 0.373 | 0.483 |

| FL → FILsav | 0.520 | 17.180 | .000 | 0.469 | 0.569 |

| FL → FWB | 0.197 | 4.458 | .000 | 0.125 | 0.272 |

Appendix C

Obective Financial Literacy Question.

| Objective FL (Multiple choice) |

|---|

| Imagine five of your friends receive a donation of GH¢ 1,000.00 and must equally divide the money between them. How much will each of them get? (a) GH¢ 100; (b) GH¢ 200; (c) GH¢ 1,000; (d) Don’t know. |

| Assume you saw the same television at two different stores for the initial price of GH¢ 1,000.00. Shop A offers a discount of GH¢ 150.00, while Shop B offers a discount of 10%. Which of the stores will you buy from? (a) Buying in Shop A (discount of GH¢ 150); (b) Buying in Shop B (discount of 10%); (c) The value is the same; (d) Don’t know. |

| When the inflation rate or price of goods and services increases, the cost of living rises. This statement is: (a) True; (b) False; (c) Don’t know. |

| When you distribute your investments among two or more different business activities, the risk of losing money: (a) increases; (b) decreases; (c) remains unchanged; (d) don’t know. |

| Assume Kwame inherits GH¢ 10,000.00 today and Peter inherits GH¢ 10,000.00 in about 3 years. Because of inheritance, who will get richer? (a) Kwame; (b) Peter; (c) They are equally rich; (d) don’t know. |

| Suppose you had GH¢ 100 in a savings account and the interest rate is 2% per year. After 5 years, how much do you think you would have in your account if you left the money to grow? (a) More than 102. (b) Exactly 102. (c) Less than 102. (d) Don’t know. |

| Imagine that the interest rate on your savings account was 1% per year and inflation was 2% per year. After 1 year, how much would you be able to buy with the money in this account? (a) More than today. (b) Exactly the same as today. (c) Less than today. (d) Don’t know. |

Ethical Considerations

The paper literature used previously published works that were properly cited, and the raw data were gathered per ethical clearance obtained from the University of KwaZulu-Natal Research Ethical Board with approval number HSSREC/00006314/2023.

Consent to Participate

Informed consent was obtained from all subjects involved in the study. The consent was obtained either verbally or in writing, depending on the choice of the person.

Author Contributions

This article’s development and writing have benefited greatly from the contributions of each listed author.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: No organization provided the authors with funding support for the paper submitted.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The ethical requirements guided the data availability and are available from the corresponding author [Peter Kwame Kuutol] on request.