Abstract

Improving the financial well-being of people with disabilities is a pressing concern, given the documented lower levels of financial well-being among this population compared to the general population. Limited research, however, offers effective strategies for improving their financial well-being. This study investigates how financial knowledge and family financial socialization can be combined to enhance the financial well-being of people with disabilities. Using data from the 2016 National Financial Well-Being Survey, we employ multivariate analyses and propensity score matching techniques to test the robustness of our results and ensure our population comprised a nationally representative sample of people with disabilities. Our findings show that people with disabilities experience lower levels of financial well-being compared to those without disabilities. Furthermore, we find that self-assessed financial knowledge and financial socialization within the family context are positively associated with the financial well-being of people with disabilities. These findings have important implications for researchers and financial service professionals who work with people with disabilities. This study emphasizes the importance of tailoring financial education to the specific needs of people with disabilities and prioritizing financial education and financial socialization within the family context as critical mechanisms for enhancing their financial well-being.

Plain Language Summary

Improving the financial well-being of people with disabilities is a pressing concern, given the documented lower levels of financial well-being among this population compared to the general population. Using data from the 2016 National Financial Well-Being Survey, we employ multivariate analyses and propensity score matching techniques. Our analysis shows that people with disabilities experience lower levels of financial well-being compared to those without disabilities. While we acknowledge that systemic barriers faced by people with disabilities, such as the Medicaid infrastructure and wage-related laws, extend beyond individual impairments and play a significant role in employment prospects, we find a positive association between self-assessed financial knowledge and financial socialization within the family context and the financial well-being of people with disabilities. These findings are important for researchers and people who help with money matters for people with disabilities. They show that we should provide financial education that suits the needs of people with disabilities and also encourage families to discuss money matters with them. These steps can improve their financial well-being.

Keywords

Introduction

The term “disability” covers a broad range of impairments, activity limitations, and participation restrictions (Hemphill & Kulik, 2016). Additionally, the term includes those who may not currently have a disability but fall within the scope of having potential impairments, activity limitations, or participation restrictions (National Network, 2023). The World Health Organization (WHO, 2001) has defined disability in terms of three dimensions: First, disability encompasses impairment in a person’s body structure or any physical or mental function. These impairments may include the loss of a limb, vision, hearing, cognitive abilities, or memory. Second, activity limitations, such as difficulties in seeing, hearing, walking, or problem-solving, are considered disabilities. The third disability dimension involves participation restrictions in regular daily activities, such as working, engaging in social activities, and accessing healthcare and/or preventive services. Disabilities can vary in severity, ranging from mild to severe, and can be either constant or episodic (Goodman et al., 2017). Any individual, regardless of circumstances or demographic or economic characteristic, can experience a disability (Banister, 2006). In the U.S. about 26% of the adult population (61 million individuals), live with disabilities (Centers for Disease Control and Prevention, 2020).

The year 2021 marked the 31st anniversary of the Americans with Disabilities Act, which aims to eliminate discrimination against people with disabilities in various aspects of life, including employment, transportation, housing, communication, and access to government programs and services (U.S. Department of Labor, 2020). Significant strides have been made in the realm of disability rights to guarantee equal access to education and employment and to prohibit discrimination on the basis of disability (Rembis et al., 2018). Despite these advancements, individuals with disabilities continue to be disproportionately represented among the economically disadvantaged and undereducated populations in the United States (American Psychological Association, 2017).

People with disabilities face significant challenges concerning employment opportunities and achieving financial stability. Notable disparities exist in median income and education levels (U.S. Bureau of Labor Statistics, 2020). In fact, people with disabilities earn a median income of $5,796 less annually than their non-disabled peers. Approximately 40% of individuals with disabilities have a high school education or less, compared to 26% of those without disabilities (Goodman et al., 2017). These disparities in education and employment opportunities contribute to higher rates of poverty among people with disabilities. Labor force participation rates within the disabled population is significantly lower than for the general population. In fact, the labor force participation rate for people with disabilities was only 20.8% in 2019, compared to the rate of 68.7% for those without disabilities (Institute on Disability, 2020). Moreover, the disabled population demonstrates lower participation rates in various aspects of the traditional financial sector, such as banking, investment, and access to credit (Calderon, 2017) and experience higher rates of household poverty (Livermore & Honeycutt, 2015). Because of the significant discrepancies, several studies have examined the subjective financial well-being of people with disabilities. For example, Hadjar and Kotitschke (2021) found that individuals with disabilities do not have the same opportunities to achieve instrumental goals, such as being able to create a budget, as those without, ultimately, the inability to meet such goals negatively impacts their subjective well-being. As Van Campen and Van Santvoort (2013) demonstrated, this is a global problem. In their study of the disabled population in 21 European countries, they found that people with disabilities are in a disadvantaged position.

In addition to these challenges, it is crucial to recognize the systemic nature of the barriers faced by people with disabilities. Systemic reasons, such as the Medicaid infrastructure and laws concerning wages, extend beyond individual impairments and play a significant role in employment prospects. Historically, people with disabilities often have been locked into poverty to maintain eligibility for categorical Medicaid coverage because of restrictions on income and assets (Kennedy & Blodgett, 2012). Because additional earnings and savings could result in the loss of critically needed coverage, Medicaid has acted as a deterrent for many Americans with disabilities to seek employment (Hall et al., 2018). Furthermore, legal wage disparities persist, allowing individuals with disabilities to be paid less than their non-disabled peers in identical job roles, reinforcing economic inequality (Doucette, 2018). It is imperative to underscore that the employment and financial challenges faced by people with disabilities are deeply intertwined with systemic factors and structures within society.

Financial well-being is an important component of overall well-being (Consumer Financial Protection Bureau, 2015). It encompasses meeting present and future financial obligations, making informed choices that enhance one’s life, and feeling secure about future finances. Netemeyer et al. (2018) demonstrated that perceived financial well-being is a key predictor of overall well-being and comparable in magnitude to the combined effects of other life domains (job, physical health, and relationship satisfaction). Nguyen (2022) suggested that an improved understanding of the causes of financial well-being is needed to increase overall well-being. Yet, people with disabilities often face more financial challenges than the general population, making it crucial to examine the factors contributing to their financial well-being. Despite its importance, limited knowledge exists on the financial well-being of people with disabilities and how financial capability can improve their situation (McGarity et al., 2020). A greater understanding of ways to improve their financial well-being can assist people with disabilities and their financial advisors in managing their finances more effectively and developing a stable path toward overall wellness.

Review of Literature

To develop a comprehensive understanding of financial well-being among people with disabilities, a review of the relevant literature was conducted. The literature covered various aspects, including capability theory, family financial socialization theory, and financial well-being. In this study, we assume that individuals’ capabilities, rather than the resources or limitations they possess, have an impact on their well-being, with the capability theory as our foundational framework. While there are various ways to enhance an individual’s capabilities, our research particularly emphasizes the role of financial knowledge. Additionally, drawing upon the family financial socialization theory, this study examines how family financial socialization influences the financial well-being of people with disabilities.

Capability Theory

The increasing complexity of financial decisions, the greater diversity of financial products, and the instability of the global economy have strengthened the importance of equipping individuals with the necessary skills to make sound financial decisions (Lusardi, 2010; Sekar & Gowri, 2015). A person’s financial capability, which encompasses financial knowledge, confidence, and motivation to manage their finances effectively (Atkinson et al., 2007); the ability to apply the requisite skills or knowledge to various financial products (Johnson & Sherraden, 2007): and the application of appropriate financial knowledge and behaviors to improve their financial well-being (Xiao, 2016), is crucial to financial well-being. Enhancing financial capability may improve decision-making skills (Lusardi & Mitchell, 2014), which have significant implications and ultimately enhance overall well-being (Allmark & Machaczek, 2015).

Initially formulated in the 1980s by Amartya Sen and Martha Nussbaum, the capability theory has since undergone further development by various social science scholars (Robeyns, 2011). The capability theory is a theoretical framework that offers a comprehensive structure for evaluating individuals’ well-being. It emphasizes people’s potential to achieve goals rather than their possession of resources (Storchi & Johnson, 2016), grounding well-being in their “functionings” (Sangha et al., 2015). Based upon this theory, education plays a pivotal role in enhancing the quality of life and elevating financial capability, particularly among the most impoverished (Drèze & Sen, 2013), which has become a social policy goal for many Western governments (Allmark & Machaczek, 2015). Sen (2009) criticized the theory’s centrality focusing on the equality of resources as a political value and its assessment of well-being in this context and instead emphasized the importance of focusing on people’s capabilities—that is, what they are able to do and be, rather than on their resources or utility.

This approach redirects attention from the specific limitations or challenges posed by disabilities to the broader goal of ensuring that people with disabilities have the same opportunities as those without disabilities. Despite its popularity, only a few studies have explained the financial well-being of individuals with disabilities based on this theoretical foundation. Demonstrating the importance of financial education early in life, D’Aguilar (2019) found that the financial skills of young adults with disabilities fell below the average score of the general U.S. population. This highlights the urgency for improved financial education and resources to be provided to young adults with disabilities. Also stressing the importance of education, McGarity (2018) evaluated the influence of individual and institutional-level factors on the financial capability of a cohort of people with disabilities, identifying financial knowledge as instrumental in enhancing financial well-being.

Financial Socialization Theory

Enhancing the financial standing of people with disabilities is critical due to the substantial impact of financial difficulties on their general well-being. To examine the financial well-being of people with disabilities, this study employs family socialization theory. The family socialization theory is a process of acquiring values, norms, standards, attitudes, and behaviors that promote financial sustainability and individual well-being (Danes, 1994). According to family financial socialization theory, financial well-being is the result of multiple financial socialization processes within the family over time, as financial socialization is multifaceted and occurs in various settings, but the family being one of the most critical contexts (Gudmunson & Danes, 2011). Furthermore, family financial socialization during childhood and adolescence is directly associated with financial outcomes (Serido & Deenanath, 2016). Zhu (2018) found that parental socialization significantly influences the financial behavior of adolescents through financial learning outcomes and financial attitudinal variables, emphasizing the importance of sharing financial knowledge and teaching norms to adolescent children. More recently, Zhao and Zhang (2020) highlighted the significant impact of family financial socialization on financial outcomes, including financial well-being.

Although parents and other family members play a crucial role in shaping individuals’ financial behaviors, other sources of financial socialization, such as school-based financial education and workplace programs, are also valuable. Educational institutions can provide training in various formats to help those with disabilities develop healthy financial behaviors (Sinha et al., 2018). In the United States, some state-level mandates call for school-based financial education programs for adolescents (Lusardi & Mitchell, 2014) and some progressive colleges and universities have financial literacy/financial education centers (Danns, 2016) that offer programs to improve the financial wellness of their students (Alban et al., 2014). Also, many employers now offer workplace-based financial education training to their employees, which has been shown to positively influence financial behaviors (Lusardi & Mitchell, 2014). Similarly, Shim et al. (2010) showed that employed youths were likely to be more financially literate than non-employed youths. People with disabilities, especially adolescents or young adults, often rely on their parents for assistance and have limited involvement in the labor market (Goodman et al., 2017; Majola & Dhunpath, 2016).

Financial Well-Being

Financial well-being involves feeling secure and in control (Evans et al., 2023) of one’s financial situation and is a critical aspect of overall life satisfaction (Shim et al., 2009). Financial well-being involves several factors such as financial satisfaction, objective financial status, and financial attitudes and behaviors (Joo, 2008). It is a complex and multidimensional concept that cannot be assessed through a single metric. Previous studies have adopted a comprehensive approach to measure financial well-being, employing either objective or subjective measures. For instance, Xiao (2016) evaluated objective financial well-being considering various indicators such as income, expenditure, debt, assets, net worth, and debt-to-income ratio. Additionally, his study assessed subjective financial well-being, considering income satisfaction, savings, and other financial resources. Netemeyer et al. (2018) evaluated subjective financial well-being through two constructs: stress related to current money management and a sense of security concerning future finances.

The financial challenges faced by people with disabilities and their caregivers have been well documented. Given that most U.S. households rely on employment for income, it is not surprising that people with disabilities face difficulties in the labor market (Jabłońska-Porzuczek & Kalinowski, 2018) and are among the most financially disadvantaged (Pinilla-Roncancio, 2015). In addition, those who are employed tend to have low-wage or temporary jobs with less job security (Consumer Financial Protection Bureau, 2019). As a result, people with disabilities are more likely to live in poverty, as evidenced by the United States Census Bureau’s (2020) report detailing a poverty rate of 26.9% in 2018 for those with disabilities, compared to approximately 12.2% for others. The median income for households, including working-age people with disabilities, is also significantly lower than that of households comprised of people without disabilities (Erickson et al., 2019). In fact, 26% reported an annual income of less than $15,000, while only 15% reported an income of $75,000 or more (Goodman et al., 2017). The employment rates for persons with disabilities and those without were 19.3% and 66.3%, respectively, in 2019 (U.S. Bureau of Labor Statistics, 2020). This often forces people with disabilities to focus on short-term financial solutions rather than long-term financial security and well-being (Prosper Canada, 2015). These disparities highlight the urgent need to address the financial well-being of people with disabilities and their families.

Methods

Data and Analytic Sample

This study used the 2016 National Financial Well-Being Survey (NFWBS), which was conducted and managed by the Consumer Financial Protection Bureau (CFPB). The survey was conducted between October 27 and December 5, 2016, and a representative sample of 6,394 respondents from the U.S. adult population participated. The NFWBS provides a comprehensive range of individual and household characteristics, including income; employment status; financial experiences; behaviors, skills, and attitudes’ as well as savings and safety nets. For this study, an analytic sample of 6,203 respondents was used, with missing responses to selected variables excluded. Descriptive and multivariate results were weighted using the survey weight provided in the NFWBS dataset.

Research Hypotheses

Drawing from the theoretical framework and a comprehensive literature review, this study formulated the research hypotheses as follows:

Hypothesis 1: People with disabilities tend to exhibit a comparatively lower level of financial well-being compared with those without disabilities even after we control for various household characteristics.

Hypothesis 2: There exists a positive association between financial knowledge and financial well-being for people with disabilities.

Hypothesis 3: There exists a positive association between financial socialization and financial well-being for people with disabilities.

Dependent Variable: Financial Well-Being

In consultation with leading experts and drawing from existing literature on financial well-being, the Consumer Financial Protection Bureau (CFPB) developed a comprehensive and standardized definition of financial well-being. This definition posits that financial well-being is constructed by an individual’s ability to fully meet their current and ongoing financial obligations, feel secure in their financial future, and make choices that allow them to enjoy life (Consumer Financial Protection Bureau, 2015). To operationalize this definition, the CFPB constructed the financial well-being scale, which comprises four domains: (1) controlling daily and monthly finances; (2) being able to absorb financial shocks; (3) being on track to meeting financial goals; and (4) having financial freedom to make choices that allow enjoyment of life (Consumer Financial Protection Bureau, 2017). The CFPB financial well-being score is derived from ten questions, which are converted into a single score using item response theory (IRT) methods. The CFPB Financial Well-Being Scale scores are ranged from 0 to 100.

Focal Variables

Employment Status

The NFWBS survey includes a question regarding respondents’ current employment or work status, with eight possible categories for response. These categories include (a) self-employed; (b) full-time employment for an employer or the military; (c) part-time employment for an employer or the military; (d) homemaker; (e) full-time student; (f) permanently sick or disabled; (g) unemployed or temporarily laid off; and (f) retired. For the purposes of this study, the first three categories were combined into an “employed” group. Considering the study’s primary focus on people with disabilities, the “disabled” category was utilized as the reference group.

Financial Knowledge

We operationalized financial knowledge by examining it as either “quantifiable financial knowledge” and “self-assessed financial knowledge.” The quantifiable financial knowledge scale was based on Knoll and Houts’ (2012) nine-question scale, available in the NFWBS, where each multiple-choice question had a single correct answer. The questions covered topics such as (1) long-term returns on investments; (2) stocks, bonds, and savings volatility; (3) benefits of diversification; (4) stock market losses; (5) life insurance; (6) housing market losses; (7) credit card minimum payment; (8) the relationship of bonds prices and interest rates; and (9) mortgage term length on interest paid. We used the calculated scale score using the approach developed by Knoll and Houts (2012), which ranged from −2.05 to 1.27. For a detailed description of the IRT process and its contribution to measurement precision, see Knoll and Houts (2012). We evaluated self-assessed financial knowledge with a single question, “How would you assess your overall financial knowledge?” with response options ranging from 1 (very low) to 7 (very high).

Financial Socialization

The NFWBS includes a question on financial socialization: “While growing up at home, did your family do any of the following?” Respondents were able to report all relevant types of financial socialization activities they experienced, including (1) discussing family financial matters; (2) talking about the importance of saving; (3) discussing how to establish good credit; (4) teaching them how to be an intelligent shopper; (5) teaching them that their actions determine their success in life; (6) providing them with a regular allowance; and (7) providing them with a savings account. In this study, we created a summation score by adding up respondents’ agreement with all seven financial socialization questions, which ranged from 0 to 7.

Control Variables

The present study controlled for a set of variables in addition to the focal variables, namely: respondent age, categorized as 18 to 34, 35 to 44, 45 to 54, 55 to 61, 62 to 69, and 70 or older; gender, classified as male or female; marital status, categorized as married, never married, partner, and separated/divorced/widowed; education level, classified as less than high school, high school diploma, some college, bachelor’s degree, and post-bachelor’s degree; race/ethnicity, classified as Whites, Blacks, Hispanics, and Asians/others; homeownership status; banking status; household income, categorized as less than $30,000, $30,000 to $49,999, $50,000 to $74,999, $75,000 to $99,999, $100,000 to $149,999, and $150,000 or more; and census division.

Empirical Model Specification

We utilized ordinary least squares (OLS) regression models to investigate the factors that contribute to financial well-being. Furthermore, we conducted analogous analyses on a subset of major employment status groups to isolate the impact of financial knowledge and financial socialization within each subgroup. Specifically, Model 1 examined the relationship between financial well-being and employment status, financial knowledge, financial socialization, socioeconomic variables, and census division for the total sample. Model 2 focused on the relationship between financial well-being and financial knowledge, financial socialization, socioeconomic variables, and census division for the subsample of employment status. For Model 2, we conducted similar regression analyses across three selected groups, disabled, employed, and retired.

To reduce the potential for biased estimates of the association between disabled status and financial well-being, we employed a propensity score matching (PSM) analysis. The fundamental idea behind propensity score matching is to identify a counterfactual subgroup of households that possess comparable characteristics to those within the treatment group (Rosenbaum & Rubin, 1983; Rubin, 2001). The analytic sample was constructed by matching disabled respondents (treatment group) with non-disabled respondents possessing similar characteristics (control group). A one-to-one matching method without replacement was utilized as the matching algorithm in the PSM analysis. Under the matching algorithm, one-to-one nearest matching without replacement, the disabled were matched with the non-disabled using various socio-demographic variables of our regression analyses.

Results

Descriptive Results

Table 1 presents the descriptive statistics for financial well-being, financial knowledge, and financial socialization. The total sample had a mean financial well-being score of 54.30, while the quantifiable financial knowledge and self-assessed financial knowledge scores were −0.16 and 4.61, respectively. Respondents reported experiencing an average of 3.5 financial socialization activities. We also examined these variables across the three major employment status subgroups. Retired respondents demonstrated the highest levels of financial well-being, and quantifiable financial knowledge as well as self-assessed financial knowledge, while the employed group reported the highest score of financial socialization. T-tests indicated that the disabled group had lower scores for all four variables in comparison to employed and retired respondents. Characteristics of the sample are included in the Appendix.

Descriptive Statistics of Selected Variables, 2016 NFWBS.

Note. Weighted results. Standard errors in parentheses. T-tests were conducted for two pair-wise comparisons. Significance level: *p < .05. **p < .01. ***p < .001.

Multivariate Results

Table 2 presents the results of OLS regression models examining the factors associated with financial well-being. The results showed that disabled respondents had lower levels of financial well-being than the retired and employed groups. Specifically disabled respondents’ scores for financial well-being were 3.41 and 6.31 levels lower than employed and retired, respectively. There was no significant difference in the financial well-being of disabled and unemployed respondents. Moreover, both the quantifiable financial knowledge and self-assessed financial knowledge were positively associated with financial well-being scores, with one-unit increases in quantifiable financial knowledge and self-assessed financial knowledge yielding an increase in financial well-being by 1.06 and 2.86 units, respectively. Similarly, financial socialization was positively related to the level of financial well-being, with a one-unit increase in financial socialization yielding a 0.5 unit increase in financial well-being.

OLS Regression Results on Financial Well-Being, Total Sample, 2016 NFWBS.

Note. Weighted results.

We performed separate regression analyses for three employment status subgroups, namely disabled, employed, and retired, to identify the factors associated with financial well-being in each group, as demonstrated in Table 3. The quantifiable financial knowledge and self-assessed financial knowledge variables were positively associated with financial well-being in all three subgroups, except for disabled respondents, where only self-assessed knowledge was positively associated with financial well-being, and quantifiable financial knowledge did not show any significant association. Furthermore, financial socialization was positively related to the financial well-being for both disabled and employed groups.

OLS Regression Results on Financial Well-Being, Subsample of Employment Status, 2016 NFWBS.

Note. Weighted results. Significance level: *p < .05. **p < .01. ***p < .001. Reference category of age for retired group is 61 or younger.

Robustness Check: Propensity Score Matching Analysis

Table 4 shows the propensity score matching (PSM) analysis results. The sample of PSM analysis includes 226 pairs of units (a total of 452 respondents). As shown in Panel A, the mean score of financial well-being of disabled respondents was 12.67 lower than that of the non-disabled respondents. Panel B presents OLS regression results from the matched sample, which indicates that disabled respondents had a 5.59 lower score of financial well-being than the non-disabled group, after controlling for various socio-demographic factors and census division.

Propensity Score Matching (PSM) Analysis of Financial Well-Being, 2016 NFWBS.

Note. Significance level: *p < .05. **p < .01. ***p < .001. The propensity score matching is based on the one-to-one matching without replacement. The differences of propensity scores between matched peers do not exceed 0.001 in absolute value. In the process of the matching analysis, 38 observations were dropped.

Note. Weighted results. The size of matched sample is 452.

Control variables are the same as Table 2. Full results are available from the authors upon request.

Discussion and Implication

Improving the financial well-being of people with disabilities is both crucial and challenging. Previous studies have consistently highlighted significant barriers that people with disabilities face in achieving financial security, resulting in them trailing behind the financial well-being of the general population. Despite the pressing need for effective solutions, practical strategies to enhance their financial well-being remain conspicuously absent. By analyzing data from the 2016 National Financial Well-Being Survey, this study uncovered the key drivers of financial well-being within this group. The findings suggest that disabled respondents had lower levels of financial well-being than their non-disabled counterparts. This disparity persisted even when using the propensity score matching (PSM) technique. Our results not only validate the existing disparities but also emphasize the significance of personal financial knowledge and family-based financial education in enhancing the financial well-being of people with disabilities.

In line with our research objective of exploring the factors influencing financial well-being, we developed three hypotheses focusing on individuals with disabilities. Hypothesis 1 suggests that people with disabilities tend to exhibit a comparatively lower level of financial well-being compared to other demographic groups. This hypothesis found support in our findings, as the disabled group demonstrated lower scores in terms of financial well-being compared to other groups, even after controlling for various socio-demographic factors and census division. Grounded in capability theory, which emphasizes the significance of concentrating on individuals’ capabilities rather than their resources or utility, Hypothesis 2 posits a positive association between financial knowledge and financial well-being among people with disabilities. Our findings provided partial support for this hypothesis, revealing that only self-assessed knowledge was positively associated with financial well-being. In line with the findings of previous research, including Xiao (2016), our study also identified a positive association between financial knowledge and financial well-being among people with disabilities. This consistency across studies underscores the robustness and generalizability of this relationship within the context of individuals with disabilities. Drawing upon the family socialization theory, which posits a process of acquiring values, norms, standards, attitudes, and behaviors that promote financial sustainability and individual well-being, Hypothesis 3 suggests a positive association between financial socialization and financial well-being for people with disabilities. Our findings also supported this hypothesis. Consistent with prior research, including Zhao and Zhang (2020), and Serido and Deenanath (2016) our study found that family financial socialization is positively linked to the financial well-being of individuals with disabilities.

In summary, our results suggest that solely improving quantifiable financial knowledge may not be sufficient to improve financial well-being, particularly among financially vulnerable groups such as people with disabilities. Therefore, financial education programs should prioritize improving self-assessed financial knowledge. For this purpose, financial education programs must provide individuals with the information, skills, and confidence needed to address the complexities of personal finance. This knowledge empowers individuals to make informed decisions and manage their finances more effectively, ultimately leading to greater financial confidence and well-being. Moreover, since enhancing financial confidence is crucial to achieving financial well-being among people with disabilities, tailored strategies must be developed to strengthen their financial confidence. For instance, financial education materials and programs should be accessible to people with disabilities. This involves providing information in various formats, including Braille, audio, and enlarged materials, and ensuring that online resources are compatible with screen readers. The findings of this study suggest that financial socialization plays a vital role in the financial well-being of people with disabilities, highlighting the importance of discussing financial matters within families. We urge parents to engage in conversations about money management with their children, and schools to implement financial education programs that involve parents. By doing so, we can positively impact the financial futures of people with disabilities and empower them to achieve greater financial stability and success.

Improving access to financial education programs has been recognized as a crucial step to enhancing financial well-being, as indicated by previous empirical studies (e.g., Jin & Chen, 2020; World Bank, 2014). However, a one-size-fits-all approach is not practical, and financial programs must be tailored to support the financial well-being of people with disabilities, particularly in schools where financial education programs are scarce. Continuous evaluation and modification of financial education programs are necessary to meet the specific needs of this group. For instance, financial education tailored to people with disabilities can help prepare them for life after school. Inclusive education is essential to ensure the participation of young people with disabilities in school-based financial education programs. Better training for educational counselors in schools can address this deficiency and provide better access to employment, education, and training opportunities.

While we advocate for the implementation of school-based financial education programs for people with disabilities as one component of a broader strategy, it is crucial to recognize that these programs alone cannot fully address the systemic financial disparities faced by this population. The need for systemic changes remains paramount. School-based programs are valuable for providing essential financial knowledge and skills to individuals with disabilities within an educational context. Yet, they should be viewed as a starting point rather than a comprehensive solution. To achieve lasting improvements in the financial well-being of people with disabilities, systemic changes at the policy, societal, and institutional levels are still needed. These systemic changes may encompass policy reforms to ensure equal access to financial services, inclusive employment practices, and healthcare as well as insurance reforms.

This study is subject to certain limitations that are important to acknowledge. First, we acknowledge that a limitation of our study lies in its generalized approach. Due to the limited availability of data, the study did not explore the degree or nature of disability. Future research has the potential to delve into the specific challenges faced by individuals with distinct disability types, such as those with cognitive or physical impairments. The inclusion of a more comprehensive measure of disability status could enable researchers to undertake a more in-depth analysis of the subject matter. Second, despite focusing primarily on the impact of financial capability (i.e., knowledge and socialization) on the financial well-being of disabled individuals, the regression findings indicated that no single factor was responsible for determining their financial well-being. This suggests that further research is necessary to investigate other factors that may influence financial well-being, such as financial goals and priorities.

Footnotes

Appendix

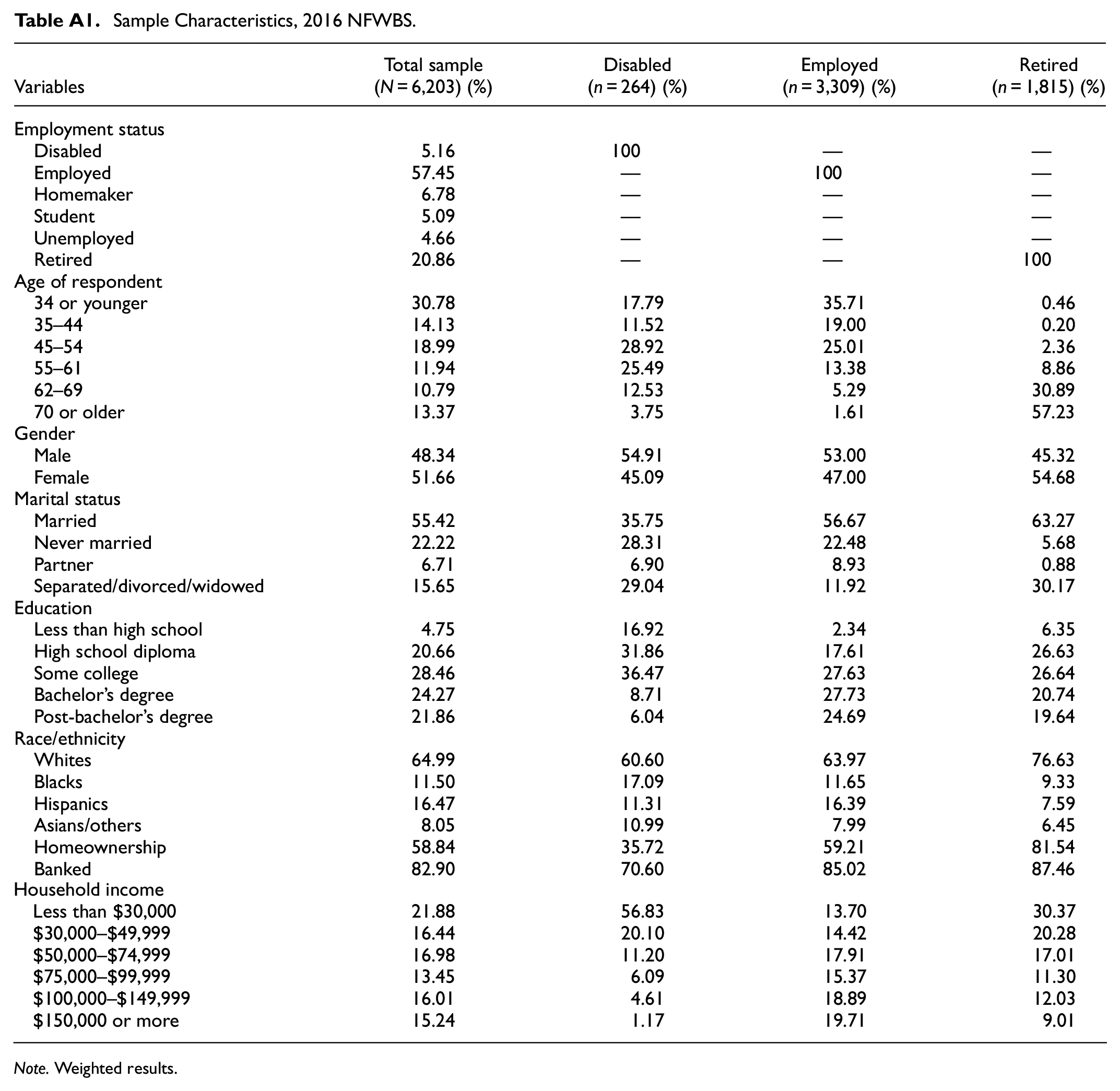

Sample Characteristics, 2016 NFWBS.

| Variables | Total sample (N = 6,203) (%) | Disabled (n = 264) (%) | Employed (n = 3,309) (%) | Retired (n = 1,815) (%) |

|---|---|---|---|---|

| Employment status | ||||

| Disabled | 5.16 | 100 | — | — |

| Employed | 57.45 | — | 100 | — |

| Homemaker | 6.78 | — | — | — |

| Student | 5.09 | — | — | — |

| Unemployed | 4.66 | — | — | — |

| Retired | 20.86 | — | — | 100 |

| Age of respondent | ||||

| 34 or younger | 30.78 | 17.79 | 35.71 | 0.46 |

| 35–44 | 14.13 | 11.52 | 19.00 | 0.20 |

| 45–54 | 18.99 | 28.92 | 25.01 | 2.36 |

| 55–61 | 11.94 | 25.49 | 13.38 | 8.86 |

| 62–69 | 10.79 | 12.53 | 5.29 | 30.89 |

| 70 or older | 13.37 | 3.75 | 1.61 | 57.23 |

| Gender | ||||

| Male | 48.34 | 54.91 | 53.00 | 45.32 |

| Female | 51.66 | 45.09 | 47.00 | 54.68 |

| Marital status | ||||

| Married | 55.42 | 35.75 | 56.67 | 63.27 |

| Never married | 22.22 | 28.31 | 22.48 | 5.68 |

| Partner | 6.71 | 6.90 | 8.93 | 0.88 |

| Separated/divorced/widowed | 15.65 | 29.04 | 11.92 | 30.17 |

| Education | ||||

| Less than high school | 4.75 | 16.92 | 2.34 | 6.35 |

| High school diploma | 20.66 | 31.86 | 17.61 | 26.63 |

| Some college | 28.46 | 36.47 | 27.63 | 26.64 |

| Bachelor’s degree | 24.27 | 8.71 | 27.73 | 20.74 |

| Post-bachelor’s degree | 21.86 | 6.04 | 24.69 | 19.64 |

| Race/ethnicity | ||||

| Whites | 64.99 | 60.60 | 63.97 | 76.63 |

| Blacks | 11.50 | 17.09 | 11.65 | 9.33 |

| Hispanics | 16.47 | 11.31 | 16.39 | 7.59 |

| Asians/others | 8.05 | 10.99 | 7.99 | 6.45 |

| Homeownership | 58.84 | 35.72 | 59.21 | 81.54 |

| Banked | 82.90 | 70.60 | 85.02 | 87.46 |

| Household income | ||||

| Less than $30,000 | 21.88 | 56.83 | 13.70 | 30.37 |

| $30,000–$49,999 | 16.44 | 20.10 | 14.42 | 20.28 |

| $50,000–$74,999 | 16.98 | 11.20 | 17.91 | 17.01 |

| $75,000–$99,999 | 13.45 | 6.09 | 15.37 | 11.30 |

| $100,000–$149,999 | 16.01 | 4.61 | 18.89 | 12.03 |

| $150,000 or more | 15.24 | 1.17 | 19.71 | 9.01 |

Note. Weighted results.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.