Abstract

This study constructs fixed-effects models based on a sample of Chinese A-share manufacturing companies listed from 2012 to 2021, to examine the impact and mechanisms of financial analysts’ attention on the quantity and quality of enterprise green innovation (EGI). The study draws the following conclusions: (1) Analysts’ attention positively promotes the quantity and quality of EGI. (2) The relief of financing constraints from information-revealing effects mediates the relationship between analysts’ attention and EGI quantity, while the external monitoring effect improves corporate Environmental, Social, and Governance (ESG) performance and mediates the relationship between analysts’ attention and EGI quality. (3) The relief of financing constraints has a masking effect on the relationship between analysts’ attention and the improvement of EGI quality due to executives’ short-sightedness. But the external monitoring effect of analysts’ attention can have a curbing effect on this. (4) In the heterogeneity test, it is found that for better performing firms, analysts’ attention promotes the improvement of the EGI quality. However, for poorer performing firms, the effect is not significant as the performance pressure effect is more pronounced. This study emphasizes the significant impact of analysts’ attention on external monitoring of EGI quality compared to other research. The findings support the need for relevant policies to guide and strengthen the external monitoring effect of analysts’ attention in practice, as well as the development of differentiated environmental regulation policies for firms with different characteristics.

Keywords

Introduction

With over 30 years of rapid development following the reform and opening up of China’s economy, the manufacturing industry in the country has made significant progress and achieved remarkable economic gains. However, the long-term reliance on factor inputs of economic growth makes environmental pollution problems increasingly prominent. In light of the increasing public consciousness regarding environmental conservation, it has become an unavoidable decision for China’s economic growth in both the present and future to shift the development approach of the manufacturing sector and encourage its transition to green practices (B. Yuan & Cao, 2022). Enterprise green innovation (EGI), which refers to firms’ green technology-oriented innovation, is regarded as a critical avenue to overcome the limitations posed by resources and the environment, ultimately achieving sustainable economic growth (Cheng et al., 2023). Therefore, how to stimulate firms’ enthusiasm to carry out EGI has also received extensive attention from scholars. The environmental regulation policy of administrative means and market incentives is an important means to reduce the pollution emission of enterprises and promote EGI (S. L. Hu et al., 2023; Q. Liu & Dong, 2022; P. B. Wang et al., 2021). Meanwhile, the development of EGI cannot be separated from the external supervision of the capital market, the media, and the public and so on (Lv & Li, 2021; F. Y. Wang et al., 2022).

As a powerful supplement to government supervision in developing countries, the capital market is called the “barometer of national economy” because of its sensitive response function, and its response is also considered to effectively improve the environmental behavior of companies (Gupta & Goldar, 2005). Among them, financial analysts are experts who evaluate and advise specific companies. They are considered to be important information transmitters in the capital markets, and they are also considered to be important external supervisors of companies (T. Chen et al., 2015). The impact of analysts’ attention on corporate innovative behavior has also received extensive attention from scholars. However, the existing studies did not give a unified conclusion, but gave two opposing hypotheses. On the one hand, some scholars have proposed the pressure transmission hypothesis, in which they argue that analysts’ attention and forecasts on earnings will bring short-term performance pressure to enterprises, resulting in short-sighted behavior of managers, and this pressure will inhibit corporate innovation (Edmans, 2009; He & Tian, 2013). He and Tian (2013) used data from the U.S. capital market to validate the conclusion. On the other hand, some scholars have proposed the information transmission hypothesis, in which they argue that analysts’ attention plays the role of information transmission and alleviates information asymmetry and financing constraints, thus promoting corporate innovation (Bai et al., 2023; P. Zhang & Wang, 2023). Many Chinese scholars have used Chinese data support the latter hypothesis, which they believe is related to China’s institutional and market environments. They argue that the ownership structure of Chinese listed companies is relatively concentrated, and the existence of major shareholders reduces the short-sighted behavior of management under market pressure. Meanwhile, the rule of law, property rights, and corporate governance in the Chinese market are not perfect, which makes the external supervision role of analysts more prominent (Aghion et al., 2013; Y. H. Wang et al., 2024; M. G. Yu et al., 2017). As the public’s awareness of environmental protection increases, realizing sustainable corporate development through EGI has become a strategic choice for firms to cope with strict environmental regulatory policies (L. Han & Jing, 2024). Recent research has also started to examine the influence of analysts’ attention on EGI and has discovered a positive correlation between analysts’ attention and EGI (M. N. Han et al., 2022; S. L. Hu et al., 2023).

However, existing studies on the impact of analysts’ attention on enterprise innovation and EGI are still not rich and sufficient. First of all, most studies still do not pay enough attention to the quality of innovation. Some of the literature only selects the number of patents to reflect firms’ innovation, without considering the quality indicators of innovation (Q. P. Yang & Liu, 2024; M. G. Yu et al., 2017). Second, although some literature has added EGI quality indicators on EGI quality, EGI quantity and EGI quality are usually studied as a whole in mechanism studies (S. L. Hu et al., 2023; M. N. Han et al., 2022). Existing studies have not discussed the impact mechanism of analysts’ attention on EGI quantity and EGI quality separately, and do not pay attention to the possible differences in the mechanism of action between them. Third, existing studies on the mechanism of the role of financing constraints in the effect of analysts’ attention on EGI quality are not clear. Since most of the studies do not distinguish between the mechanism of the impact of EGI quantity and EGI quality, they have generally concluded that relief of financing constraints plays a facilitating mediating role in the impact of analysts’ attention on EGI in their mechanism studies (Y. H. Wang et al., 2024; M. G. Yu et al., 2017). However, recent studies have found that some firms resort to strategic catering innovations or greenwashing in response to green finance policies, which may relieve financing constraints but are detrimental to EGI quality (Y. Hu et al., 2023; D. Y. Zhang, 2022). This raises the question of whether the relief of financing constraints does indeed contribute to actual improvements in EGI quality? If not, what will be the relationship between analysts’ attention, financing constraint mitigation, and EGI quality?

Therefore, considering the shortcomings and gaps of the above studies, the research objectives of this paper are as follows: (1) Our study needs to verify the effect of analysts’ attention on the respective quantity and quality of EGI, respectively. (2) Our study attempts to identify and distinguish the dominant mechanisms of action that influence the relationship between analysts’ attention and the EGI quantity as well as analysts’ attention and the EGI quality. (3) Our study attempts to further explore the relationships among analysts’ attention, relief of financial constraints, and the EGI quality. This needs to build on the reorganization of the relationship between financial constraint mitigation and EGI quality.

Our research investigates the influence of analysts’ attention on the quantity and quality of EGI and the mechanism of its action, using a sample of manufacturing firms in China’s A-share listed companies from 2012 to 2021. The contributions of this study are as follows. (1) Expanding the research on the mechanism of the impact of analysts’ attention on the quantity and quality of EGI. Unlike previous studies, we identify and differentiate the main mechanisms of their respective effects on the quantity and quality of EGI. We find that the information-revealing effect plays a dominant role in the impact of analysts’ attention on EGI quantity. While the external monitoring effect plays a dominant role in the impact of analysts’ attention on EGI quality. (2) We conduct a reorganization and analysis of the connections between analysts’ attention, relief of financing constraints, and EGI quality. Our findings indicate that while relief of financing constraints promotes the growth of EGI quantity, it hinders the improvement of EGI quality due to short-termism. This creates a masking effect in the relationship between analysts’ attention and EGI quality. However, we also find that sufficient external monitoring by analysts can effectively curb such myopia and promote the enhancement of EGI quality. (3) Our study also complements the differential impact of analysts’ attention on EGI quality across firms with different performance. We find that the external monitoring effect of analysts’ attention is more effective in promoting EGI quality in better performing firms. However, in firms with less effective performance, the performance pressure effect of analysts’ concerns is more effective, making the EGI quality improvement no significant. The findings provide the necessary support for us to formulate relevant policies to guide and strengthen the external monitoring effect of analysts’ concerns in practice, as well as to formulate differentiated environmental regulation policies for firms with different characteristics. Our findings highlight the significance of utilizing analysts’ external monitoring impact in practical applications and the necessity for tailored environmental regulations for various firm categories to steer corporate initiatives towards EGI.

Theoretical Analysis and Hypothesis Development

Policy Background

In response to the increasingly severe environmental issues, Chinese government places great emphasis on addressing environmental pollution and has implemented a range of environmental regulations and policies. These include administrative order-based regulation, which involves direct government oversight through the establishment of environmental laws, quota systems, licenses, etc. (P. B. Wang et al., 2021; X. P. Wang & Li, 2019). Additionally, market incentive-based regulation utilizes market mechanisms such as environmental taxes, pollution charges, government subsidies, pollution right emission trading policies, green financial policies and other market tools to promote environmentally friendly behavior (Jiang et al., 2023; Q. Liu & Dong, 2022; S. Luo & He, 2022). The “Green Credit Guidelines” issued by the China Banking Regulatory Commission in 2012 have played a significant role in promoting the implementation of environmental regulatory policies in the financial sector. This has led to increased financing constraints for heavy polluters at the capital market level while encouraging investment in innovative green enterprises and enhancing corporate disclosure of environmental information (Q. B. Chen, 2023). According to data from the People’s Bank of China, the balance of green loans in China reached 30.08 trillion yuan by the end of 2023, showing a year-on-year increase of 36.5%. This growth rate was 26.4 percentage points higher than that of all loans, and China’s green loan funds ranked first in the world (Ma et al., 2023). Following this, in 2016, the National Development and Reform Commission issued guidelines for green bond issuance, leading to China quickly becoming the world’s second largest green bond market (Q. Li et al., 2022).

The continuous increase of green finance policies and other environmental regulation policies has made corporate finance subject to environmental risks, and also made external stakeholders increase their attention to EGI. And analysts, as information intermediaries, play an important role in the transmission and supervision of EGI.

Information-Revealing Effect and the Quantity of Enterprise Green Innovation

First, according to the information transmission hypothesis, analysts’ attention has an information-revealing effect, which helps to reveal and transmit the information and value of EGI for external stakeholders, thus alleviating information asymmetry (Cohen et al., 2013; Manso, 2011; X. Zhang et al., 2023). The large investment expenses, high uncertainty and high specialization that characterize innovation activities exacerbate the information asymmetry between business and external stakeholders, which leads to the inability of investors and creditors to correctly evaluate the value of corporate innovation (D. Zhang & Jin, 2021). And EGI, as a fusion point of green development and innovation drive, it belongs to the category of enterprise innovation activities, so it not only has the basic characteristics of traditional innovation but also has stronger positive externalities, stronger uncertainty, greater investment risks and higher professional characteristics than traditional innovation (C. Wang et al., 2022). Therefore, EGI may expose firms to more serious information asymmetry problems, and it is even more necessary to exert the information-revealing effect of analysts to help external stakeholders understand the plan and value of EGI. On one hand, analysts are able to use their professional ability to analyze the disclosed information professionally due to their specialized financial training and rich industry knowledge (F. Yu, 2008). On the other hand, analysts are also able to dig deeper into the internal information such as business efficiency, innovation status and the strategic choice of enterprises through face-to-face exchanges or teleconferences with managers as well as on-site research on the enterprise, thus better conveying and revealing the information and value of the EGI activities to the capital market (Brauer & Wiersema, 2018; X. Liu et al., 2021). Meanwhile, analysts rely on their professional competence to analyze the environmental risks faced by enterprises, understand EGI information, and further understand the company’s sustainability-related activities and plans, which will help to better evaluate the future value of the company, and also improve the prediction quality and accuracy of analysis. It also helps enterprise stakeholders to form more accurate company value estimates (K. Luo & Wu, 2022; Rossi & Candio, 2023; Schiemann & Tietmeyer, 2022). Therefore, analysts’ attention can effectively improve the information environment of EGI, reduce information asymmetry, and promote the growth of EGI inputs and quantity.

Second, analysts’ attention to the alleviation of information asymmetry can effectively alleviate the financing constraints and reduce the cost of capital. In the context of green finance policies, corporate financing will be subject to environmental regulations in the capital market because of environmental risks (Y. Yang & Zhang, 2022). However, information asymmetry will make financial institutions and other capitalists have problems such as difficulties in recognizing environmental projects, thus further aggravating financing constraints (Q. Xie et al., 2022). While the information revealing effect of analysts helps external stakeholders to understand the plans and status of EGI faster and better, accelerates the dissemination speed and breadth the information of EGI, and reduces the cost of external interpretation of EGI (Ban, 2023; Z. J. Wang & Lv, 2022), thus contributing to the relief of financing constraints. Meanwhile, many related studies show that analysts’ attention can also help to improve corporate environmental information disclosure, thereby improving corporate reputation and promoting the relief of financing constraints (Fan & Yao, 2022; S. L. Hu et al., 2023). Analysts’ focus on easing firms’ financing constraints not only boosts cash flow, but also lowers the cost of capital. This, in turn, encourages greater investment in EGI (Derrien, 2013; M. G. Yu et al., 2017).

In summary, we believe that the information-revealing effect that analysts’ attention can exert alleviates the information asymmetry between firms and external stakeholders, promotes the relief of firms’ financing constraints, and thus contributes to the increase in the quantity of EGI. The mechanism of its action is shown in Figure 1. Meanwhile, we formulate the subsequent hypothesis.

Hypothesis 1a. Analysts’ attention can contribute to the quantity of EGI.

Hypothesis 1b. Analysts’ attention promote the increase in the quantity of gEGI by alleviating their financing constraints.

Mechanisms of the impact of analysts’ attention on the quantity of EGI.

External Monitoring Effects and the Quality of Enterprise Green Innovation

Analysts’ attention not only has an information-revealing effect, but also has an external monitoring effect on firms.

First of all, financial analysts are acknowledged as external monitors of firms, playing a role in curbing opportunistic behavior and promoting the enhancement of corporate internal governance (Bai et al., 2023; Lehmann, 2019; Tang et al., 2023). According to corporate governance theory, there are two types of agency cost problems in modern enterprises. The first type arises from the separation of ownership and management, leading to conflicts between management and shareholders. Shareholders and external stakeholders expect long-term benefits from innovation, while managers may prioritize short-term gains due to personal interests. This can result in decisions such as reducing green investments or engaging in opportunistic behaviors like strategic catering innovation or greenwashing (Y. Hu et al., 2023; Lin & Long, 2019; D. Y. Zhang, 2022). The second type involves conflicts between major shareholders and minority shareholders, which are exacerbated by the concentrated shareholding structure of Chinese listed companies. This can lead to self-interested actions by major shareholders that harm the interests of minority shareholders through related-party transactions, unfair dividend distribution, and internal borrowing (Yan & Ye, 2017). It makes the long-term motivation mechanism of EGI insufficient, thus affecting the input and quality of EGI. Nonetheless, the agency problems mentioned above can be mitigated by the external monitoring effect from analysts’ attention. Through their continuous tracking and professional analysis of firms’ disclosed information, analysts are able to promptly identify short-termist behaviors such as misappropriation of funds and reduction in long-term innovative investments. Their comments can also negatively impact a company’s stock price and credit rating, leading to potential penalties for managers from shareholders (X. Liu et al., 2021; Wei & Zeng, 2018). Therefore, analysts’ attention serves as an important external governance mechanism in scrutinizing the behavior of managers or major shareholders, effectively curbing short-termist behavior within firms (T. Chen et al., 2015; Jin et al., 2021).

Second, the external monitoring effect of analysts reinforces the reputational pressure on firms and promotes firms’ ESG performance, which in turn promotes the quality of EGI. Analysts’ attention is contagious and attracts external stakeholders such as investors, the media and the public (Dyck et al., 2010; Xiao & Shen, 2017). When a company’s business activities face extensive external attention and supervision, it will lead to a stronger incentive to establish and maintain its good reputation, which in turn will make the company more inclined to make business behavior decisions that are generally recognized by society (M. Zhang et al., 2015). Reputation theory suggests that corporate reputation is the result of constant monitoring and trust gained by a company over time, and is a reflection of the company’s overall competence (Nie et al., 2021). With the many problems caused by global warming, external stakeholders such as governments, investors, and the public are increasingly concerned about whether enterprises have taken appropriate actions in their business activities, so the performance of enterprises in ESG is regarded as an important indicator for evaluating the sustainable development of enterprises as well as reflecting the reputation of enterprises (L. Han & Jing, 2024). Enterprises’ investment in EGI can reflect their social and environmental responsibility and establish a good image of their green reputation. However, firms with less external monitoring tend to engage in low-cost and low-quality strategic catering investment of EGI, while firms with more external monitoring face more external attention and monitoring, and such symbolic behaviors, if revealed, can cause great damage to corporate reputation and stock price. Therefore, firms will reduce the speculative behavior of EGI based on the perspective of maintaining their own reputation, pay more attention to substantive EGI, and actively fulfill the ESG responsibilities of the firm, so as to ensure the quality and value of EGI (L. Han & Jing, 2024).

Therefore, analysts’ attention can exert its external monitoring effect to curb short-sightedness of firms, enhance corporate ESG performance, and ensure substantive EGI, thus contributing to the improvement of the quality of EGI. Therefore, we formulate the subsequent hypothesis.

Hypothesis 2a. Analysts’ attention can contribute to the quality of EGI.

Hypothesis 2b. Analysts’ attention are able to contribute to the quality of EGI by improving its performance on ESG.

Analysts’ Attention, Relief of Financing Constraint, and the Quality of Enterprise Green Innovation

Many studies have supported the role of relief of financing constraints in enhancing the quantity of EGI. However, there is a lack of research on whether the relief of financing constraints can promote the improvement of the quality of EGI.

The essence of green financial policies and other environmental regulatory policies is to guide the flow of capital to green environmental protection and EGI projects, to raise the financing constraints of polluting enterprises, and at the same time to alleviate the financing constraints of green transformation enterprises (Q. Liu & Dong, 2022). And their actual effects have also triggered discussions among scholars. Relevant studies have found that although green credit policy has a positive effect on the EGI quantity, the effect on the EGI quality is not significant (Xu, 2023). Influenced by managers’ short-sightedness, some firms may mislead investors and creditors by “greenwashing” behavior when facing green financial policies, and they selectively report positive green performance information while hiding negative information (D. Y. Zhang, 2022). And some firms will choose to conduct short-cycle, low-cost strategic catering innovation research such as utility model patents and design patents rather than long-cycle, high-cost substantive innovations such as invention patents (Guo & Chen, 2023; Y. Hu et al., 2023). Thus the effect of green finance policies on EGI quality is unclear, and similarly the effect of the relief of financing constraints on EGI quality is also unclear. Y. Wang et al. (2024) find that greenwashing behavior can ease the firm’s financing constraints, but faces financing inefficiencies. The study by S. R. Li et al. (2023), on the other hand, finds that an increase in financial geo-density similarly reduces the cost of capital and eases financing constraints, which contributes to an increase in the quantity of EGI, but results in a decrease in the quality of EGI. The explanation given by the authors is that the increase in financial geo-density increases the level of competition among banks, which negatively affects the quality of EGI. The above studies show that we do not have enough evidence to prove that the relief of financing constraints can promote the improvement of EGI quality. Conversely, when external oversight is insufficient, under the influence of short-termism, firms lack the motivation to engage in substantial green innovation, which can adversely affect the improvement of EGI quality.

So does analysts’ attention always curb short-termism? According to the “performance pressure hypothesis” school of thought, they argue that analysts’ attention does not always curb firms’ short-termism. On the contrary, analysts’ forecast reports increase short-term performance pressure on firms. This increases management’s short-sightedness by strategically catering to innovations or greenwashing, and contributes to the further aggravation of firms’ agency problems (Edmans, 2009; Z. Xie & Ai, 2014). Yan and Ye (2017) find that analysts’ attention can both alleviate financing constraints and reduce the second type of agency costs, but increase the first type of agency costs. They argue that analysts are more inclined to issue optimistic forecast reports and reduce the content of negative information to obtain resource support from listed firms, thus weakening the monitoring role of analysts on managers. It increases the incentives for firms to strategically catering to innovation or greenwashing. Because the disclosure of such strategic catering or greenwashing information can not only meet the requirements of environmental regulation, but also send a “pseudo-positive” signal of EGI to the outside world (Lin & Long, 2019).

To summarize, we argue that when management’s short-sightedness exists, the relief of financing constraints may have an adverse impact on the EGI quality, thereby weakening the positive impact of analysts’ attention on the quality of EGI. This situation is known as the masking effect (Wen & Ye, 2014). Meanwhile whether analysts’ attention can curb short-termism mainly depends on whether the external monitoring effect from analysts can be effectively exerted. When the external monitoring effect plays out prominently, analysts’ attention can promote EGI quality. On the contrary, it cannot. So we propose the following hypothesis.

Hypothesis 3a. The relief of financing constraints will have a masking effect in the channel of analysts’ attention on the quality of EGI due to the influence of management’s short-sightedness.

Hypothesis 3b. When the analyst’s external monitoring effect plays a dominant role, the analyst’s attention will promote the improvement of EGI quality; When the analyst’s performance pressure effect plays a dominant role, the analyst’s attention will not promote the improvement of EGI quality

Furthermore, Figure 2 illustrates the impact of analysts’ attention on the quality of EGI.

Mechanisms of the impact of analysts’ attention on the quality of EGI.

Data and Methods

Data Source

This study selects a sample of manufacturing companies listed in China’s A-share market, with data spanning from 2012 to 2021. Considering that the time point of China’s green finance policy implementation mainly starts from 2012, the data after 2012 is selected. Meanwhile, considering that China is a large manufacturing country, the green transformation and upgrading of manufacturing enterprises is crucial for China, so the manufacturing industry is selected as a sample. In addition, the data pertaining to green innovation and analysts’ attention in this research are sourced from the China Research Data Service Platform (CNRDS) database, while other data originate from the China Stock Market & Accounting Research (CSMAR) database. Meanwhile, the initial data were processed as follows: (1) excluding ST and *ST listed companies from the sample (ST refers to the stock that has been specially treated due to the loss of the company’s operation for two consecutive years, and *ST refers to the stock that has incurred loss for three consecutive years and has the risk of delisting); (2) excluding samples of listed companies with missing data on relevant variables; (3) mitigating the impact of outliers on the regression findings by subjecting all continuous variables to winsorization, both upward and downward, by 1%. The final total of unbalanced panel sample data for 1,565 companies with a total of 9,384 observations was obtained after processing.

Research Model

Benchmark Regression Model

We test hypotheses 1a and Hypothesis 2a by constructing a fixed effects model for the benchmark regression.

Model (1) is for testing Hypothesis 1a, while Model (2) is for testing Hypothesis 2a. Among them,

Mechanism of Action Analysis Model

We followed the stepwise test regression coefficient method to test the mediating and masking effects (Kenny & Judd, 1984; Wen & Ye, 2014).

First of all, in order to test Hypothesis 1b, we add Model (3) and Model (4) to Model (1) to conduct a three-step test. Among the models,

Secondly, in order to test Hypothesis 2b, we add Model (5) and Model (6) to Model (2) to conduct a three-step test. Among the models,

Thirdly, in order to test Hypothesis 3a, we test model (2) in the first step, model (3) in the second step, and at the same time, we add model (7) on the basis of these two models.

In addition, to further examine the overall indirect impact of “corporate ESG performance + relief of financing constraints,” we constructed Model (8), adding both mediating variables into the model, and used it to test Hypothesis 3b.

Variable Design

Dependent Variable

In order to reflect the actual effect of EGI, this paper adopts two variables of quantitative and qualitative indicators of EGI as explanatory variables. First, referring to most of the literature on the method of setting the indicator of the quantity of EGI and considering the lag of analysts’ attention on the impact of EGI, the natural logarithm is taken as the index to measure the quantity of EGI after adding 1 to the total number of green invention patents and green utility model patents applied for by enterprises in the later period (Du et al., 2022; Y. Hu et al., 2023). Second, referring to the practice of relevant research, we use natural logarithm as an index for measuring EGI quality by adding 1 to the average total number of other citations of green technology patents in the later period of enterprises (Q. Xie et al., 2022).

Independent Variable

The independent variable in this study is the attention of analysts. Consistent with previous research, we use the natural logarithm to represent analysts’ attention by adding 1 to the number of analysts following the listed company in the current year (He & Tian, 2013; Ye et al., 2019).

Analysts’ attention is taken as the independent variable. Referring to the practice of most previous studies, the natural logarithm is taken as an indicator to reflect analysts’ attention after adding 1 to the number of analysts following the firm in the current year (He & Tian, 2013; Ye et al., 2019).

Mediating Variable

Relief of financing constraints is utilized as a mediating factor to examine the correlation between analysts’ attention and the EGI quantity. Meanwhile, Corporate ESG performance is utilized as an mediating factor to examine the correlation between analysts’ attention and the EGI quality. Firstly, alleviation of financing constraints variable adopts the negative value of KZ index. KZ index refers to the studies of Kaplan and Zingales (1997) and Qian et al. (2017). The formula of KZ index is:

Secondly, the corporate ESG performance variable adopts the comprehensive score given in the ESG rating system launched by Shanghai Sino-Securities Index Information Service Company as the proxy variable (Huang et al., 2023). This ESG rating system is a three-level ESG evaluation embodiment based on the globally recognized ESG evaluation framework and combined with China’s market characteristics from top to bottom, focusing on evaluating the sustainable development ability of Chinese listed companies with nonfinancial information.

Control Variable

Based on the available literature, corporate age, corporate size, financial leverage, return on equity, Tobin’s Q value, proportion of independent directors, CEO duality, top shareholder, proportion of fixed assets and state of corporate ownership, which may affect the EGI output, are taken as control variables (Bai et al., 2023; Fu & Fan, 2023; Y. K. Yuan et al., 2023). Industry and year are also set as dummy variables as control variables. Table 1 displays the definition and elucidation of every variable.

Main Variable Settings and Description.

Empirical Results and Analysis

Descriptive Statistics

The main variables are presented in Table 2, displaying their descriptive statistics. First, from the index reflecting the quantity of EGI, the average value of LnQuantity is only 1.066. Converting LnQuantity into the quantity of EGI, the average number is only 3, indicating that the average number of EGI applications is low. Simultaneously, the standard deviation of LnQuantity reaches 1.066, the minimum value is 0, and the maximum value is 7.020, which is equivalent to the number of 1,118 green patent applications, indicating that there is a large gap among different samples. Meanwhile, the index reflecting the quality of EGI data also shows that the average number of citations of EGI is not high, and there is a large gap between different samples. Second, considering analysts’ attention, the average LnAC value is 1.661, which is approximately five analysts tracking each company on average. However, the standard deviation is 1.139, which shows that analysts’ attention to different companies is quite different. Meanwhile, it is observed that the average value of TOP reaches 34.766%. This suggests that the shareholding structure of the sample companies is relatively concentrated, which is in line with the basic condition that the information-revealing hypothesis is more applicable to China’s capital market, as mentioned in related studies (Aghion et al., 2013; M. G. Yu et al., 2017). A comprehensive depiction of the statistical analysis of the remaining variables can be found in Table 2.

Descriptive Statistics of Variables.

Regression Results

Table 3 demonstrates the results of the regression analysis of the impact of analysts’ attention on the quantity and quality of EGI. The findings from Model (1) presented in column (1) indicate that analysts’ attention has a significant contribution to the growth of the quantity of EGI. Each 1% increase in analysts’ attention leads to a significant increase of 0.060% in the quantity of EGI. This result supports Hypothesis 1a. Meanwhile, column (2) demonstrates the regression results of Model (2), which shows that analysts’ attention has the same significant contribution to the improvement of the quality of EGI. Each 1% increase in analysts’ attention leads to a significant increase in the quality of EGI by 0.068%. This result supports Hypothesis 2a. The above two results prove that against the background of China’s growing environmental protection demand, as the information transmitter and supervisor of the capital market, analysts’ attention to manufacturing enterprises can exert a positive influence on enhancing both the quantity and quality of EGI.

Benchmark Regression Results.

Note. Standard deviations in parentheses.

*p < .1. **p < .05. ***p < .01.

Robustness Test

Propensity Score Matching (PSM) Test

Analysts’ attention to enterprises can itself be influenced by the financial characteristics of enterprises, which can also have an impact on the quantity and quality of EGI, so this may lead to endogeneity issues such as self-selection bias in the sample as well as mutual causation. In this study, the propensity score matching (PSM) method (Rosenbaum & Rubin, 1985) is used to construct a counterfactual framework for the impact of analysts’ attention on the quantity and quality of EGI to correct the possible problem of sample self-selection bias. First, we transform the core explanatory variable “LnAC” into a dummy variable “LnAC*.” The sample is categorized into two groups based on the median analysts’ attention: a group with high analysts’ attention and a group with low analysts’ attention. For analysts’ attention above the median value, LnAC* is assigned as 1, while for analysts’ attention below the median value, LnAC* is assigned as 0. At the same time, the group with high analysts’ attention was used as the treatment group, while the group with low analysts’ attention was used as the control group. Then the financial characteristics of the enterprises that affect both analysts’ attention and EGI were used as covariates (including all the control variables in the benchmark model). The samples were then matched 1-to-1 for propensity scores using the least nearest neighbor matching method. The standard deviation of the control variables in the treatment and control groups decreased substantially after matching, and the t-test showed no significant difference between the two groups, satisfying the parallelism assumption of PSM.

Table 4 represents a comparison of the PSM pre-matching and post-matching regressions. The first two columns show that analysts’ attention significantly and positively affects both the quantity and quality of EGI in the pre-matching regression. The last two columns show that after correcting the sample self-selection problem through propensity score matching, the regression using the matched sample still has a significant positive effect of analysts’ attention on both the quantity and quality of EGI, and all these results pass the significance test at the 1% level. The findings align with those of the benchmark regression analysis, suggesting that the results are reliable and consistent.

Results of the Propensity Score Matching Test.

Note. Standard deviations in parentheses.

*p < .1. **p < .05. ***p < .01.

Replace Variable Test

To guarantee the reliability of the results, we additionally employed the approach of substituting variables in the testing methodology. In this paper, the number of research report coverage (RC) of the enterprise in the current year is selected as the substitute variable of analysts’ attention (AC), and the number of research report coverage is also treated with a natural logarithm, so the core explanatory variable after replacement is LnRC. The regression results after substituting variables are shown in columns (1) and (2) of Table 5. It can be seen that research report coverage has a significant positive impact on the quantity and quality of EGI. Every 1% increase in research report coverage will increase the quantity of EGI by 0.047% and at the same time improve the quality of EGI by 0.060%. The findings align with the outcomes obtained from benchmark regression, indicating the robustness of the results.

Results of the Variable Replacement Test.

Note. Standard deviations in parentheses.

*p < .1. **p < .05. ***p < .01.

Other Robustness Test

There may be a reverse causal relationship between analysts’ attention and EGI. That is, enterprises with higher EGI may be more likely to attract analysts’ attention. Therefore, when constructing Model (1) and Model (2) in this paper, we adopt the treatment of lagging explanatory variables by one period to solve the problem of reverse causality. Furthermore, we consider that only one year’s analysts’ attention value may be affected by specific events in that year, and the effectiveness of EGI will be affected by analysts’ continuous attention. Therefore, we used the average of analysts’ attention in the last 3 years (t, t−1, and t−2) and took natural logarithm treatment as the substitute variable of the original core explanatory variable, and LnAC3 was the core explanatory variable after replacement. Columns (3) and (4) of Table 5 show the regression results after replacing variables. It can be seen that analysts’ attention in the last 3 years has had a notable favorable impact on the quantity and quality of EGI. Every 1% increase in analysts’ attention in the last 3 years increases the quantity of EGI by 0.102% and at the same time improves the quality of EGI by 0.108%. From the results of the coefficients, the coefficients after adopting the index that can reflect analysts’ continuous attention (LnAC3) as a substitute variable have a larger regression coefficient value than that of the original explanatory variable (LnAC), which suggests that analysts’ continuous attention will have a better effect on the improvement of the quantity and quality of EGI. This result proves the robustness of the main regression results.

Mechanism Analysis

Analysts’ Attention, Relief of Financing Constraints, and the Quantity of EGI

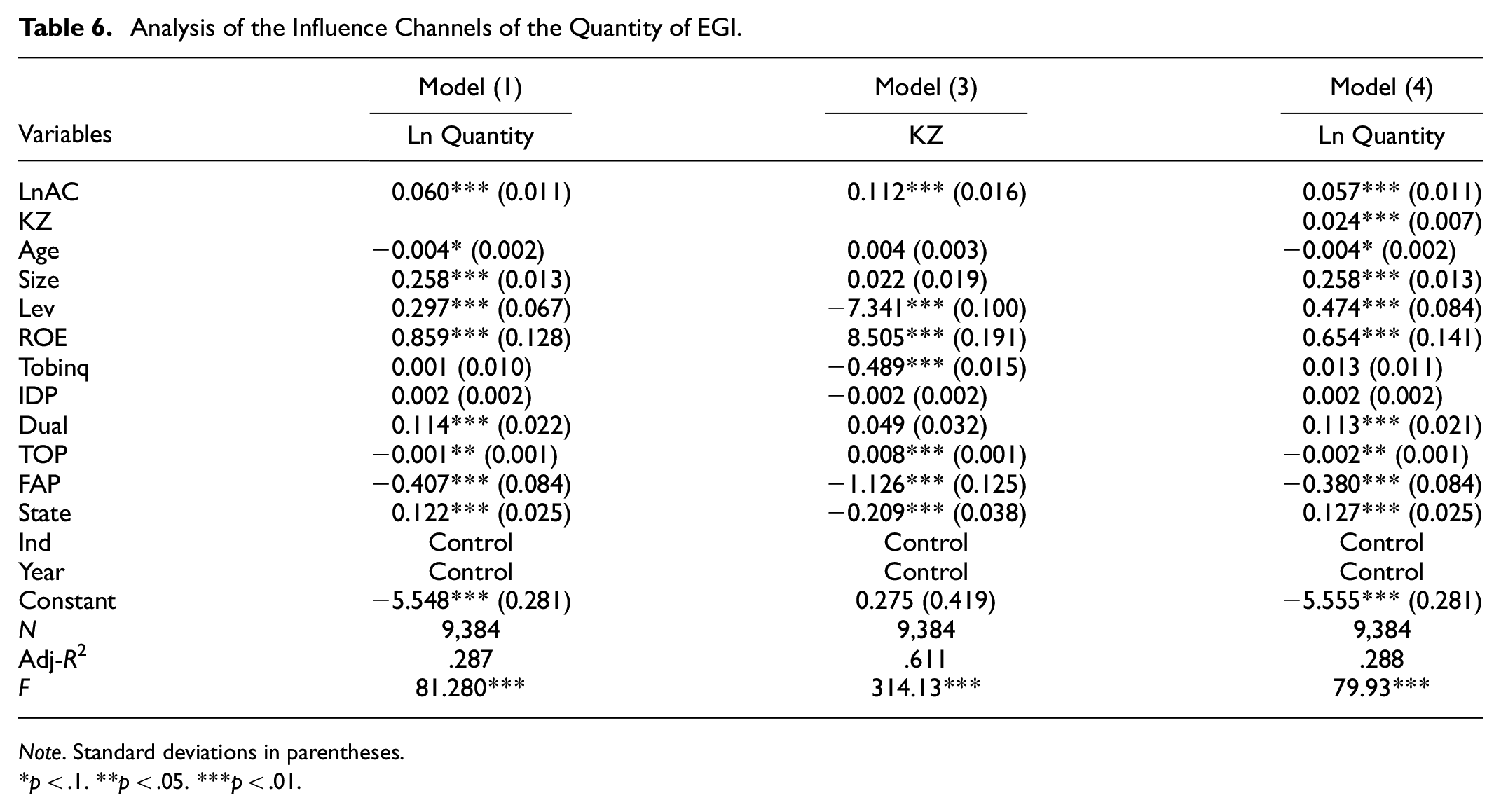

In order to test whether analysts’ attention has an impact on the quantity of EGI through the channel of “analysts’ attention → relief of the financing constraints → the quantity of EGI,” we add Model (3) and Model (4) to Model (1) to test the mediating role of financing constrains. Table 6 shows the results of the impact channel test. First, the results of Model (1) show that the impact of analysts’ attention on the quantity of EGI is significantly positive, and the total effect of the impact is 0.060. Second, the results of Model (3) further tests the influence of analysts’ attention on financing constraints. The findings indicate that analysts’ attention has a significant positive impact on the relief of financing constraints; that is, the increase in analysts’ attention relieves corporate financing constraints. Then, the Model (4) includes two variables, relief of financing constraints (KZ) and analysts’ attention (LnAC), to examine the impact on the quantity of EGI. The results show that after controlling for the impact of relief of financing constraints, the direct effect of analysts’ attention on the quantity of EGI is 0.057, so the indirect effect of the relief of financing constraints is 0.003. This indicates that the relief of financing constraints play a partial mediating role in the link between analysts’ attention and the quantity of EGI. It shows that the channel of influence of “analysts’ attention → relief of financing constraints → the quantity of EGI” is established. This result supports Hypothesis 1b. The findings indicate that the relief of financial constraints acts as a mediator in the connection between analysts’ attention and the improvement of EGI quantity, primarily driven by information effects. This finding is consistent with the findings of M. G. Yu et al. (2017) and X. Zhang et al. (2023), who also support the analysts’ attention on the important role of information in alleviating financing constraints and promoting firms’ innovation.

Analysis of the Influence Channels of the Quantity of EGI.

Note. Standard deviations in parentheses.

*p < .1. **p < .05. ***p < .01.

Analysts’ Attention, Corporate ESG Performance, and the Quality of EGI

In order to test Hypothesis 2b, we add Model (5) and Model (6) to Model (2) to examine the mediating role of ESG performance. The test results are presented in columns (1)-(3) of Table 7. First, the results of Model (2) indicate that the analysts’ attention has a significantly positive impact on the quality of EGI, with a total effect of 0.068. Second, the results of Model (5) demonstrate that analysts’ attention positively influences corporate ESG performance, with a coefficient of 0.125, indicating that it promotes the improvement of corporate ESG performance. Then, column (3) of Table 7 shows the results of Model (6). In this model, both analysts’ attention (LnAC) and corporate ESG performance (ESG), are included to investigate their influence on the quality of EGI. The findings show that after controlling for the influence of corporate ESG performance, the direct effect of analysts’ attention on the quality of EGI is 0.059 and indirect effect through corporate ESG performance is 0.009. This suggests that corporate ESG performance plays a partial intermediation role in the impact of analysts’ attention on the quality of EGI. It shows that the channel of influence of “analysts’ attention → corporate ESG performance → the quality of EGI” is valid. This result supports Hypothesis 2b. This result confirms the mediating role of corporate ESG performance, while demonstrating the important role of the external monitoring effect played by analysts in promoting EGI quality. The role of external monitoring by analysts in promoting EGI quality has not been separately explored and emphasized as a mechanism of action, although it has been mentioned in the literature (M. N. Han et al., 2022; S. L. Hu et al., 2023). The result therefore provides additional arguments for this.

Analysis of the Influence Channels of the Quality of EGI.

Note. Standard deviations in parentheses.

*p < .1. **p < .05. ***p < .01.

Analysts’ Attention, Relief of Financing Constraints, and the Quality of EGI

In order to further examine Hypothesis 3a, we conducted stepwise regression analysis using Model (2), Model (3), and Model (7) to test the impact channel of “analysts’ attention → relief of financing constraints → the quality of EGI.” The results are presented in Table 7. The regression coefficients for the independent and mediating variables in all three models show statistical significance. In Model (2), analysts’ attention has a significant positive influence on EGI, with a total effect size of 0.068. Model (3) shows a significant positive correlation between analysts’ attention and relief of finance constraints, with a coefficient of 0.112. Model (7) incorporates both analysts’ attention and relief of financing constraints into the model simultaneously. The coefficient for analysts’ attention on the quality of EGI is 0.072, indicating a direct impact effect of 0.072. The coefficient for the relief of financing constraints on the quality of EGI is −0.033, suggesting that it hinders improvement in EGI quality. The indirect effect between analysts’ attention and EGI quality was calculated to be −0.004, which is the result of multiplying the regression coefficient 0.112 with the regression coefficient −0.033. The indirect effect sign differs from the direct effect sign, indicating that the relief of financing constraints have a masking effect in the relationship between analysts’ attention and EGI quality. This result supports Hypothesis 3a. That is to say, the relief of financing constraints does not result in high-quality EGI, but rather hinders the improvement of EGI quality due to short-sighted behavior and other reasons. The decomposition results of various effects in this impact path are shown in Table 8. The result that relief of financing constraints have a negative impact on EGI quality, which aligns with the conclusions drawn by S. R. Li et al. (2023). It also possesses logical consistency with the findings of Yan and Ye (2017), who argued that analysts tend to issue optimistic forecast reports and reduce negative information to gain support from listed companies, thus easing firms’ financing constraints, but this can weaken their supervisory role and increase managiiiers’ short-termist behavior. Our analysis also believes that the adverse impact of financing constraint mitigation on the quality of EGI is due to the impact of short-sightedness under the circumstances of insufficient external supervision.

Decomposition of Each Effect of Analysts’ Attention on the Quality of EGI.

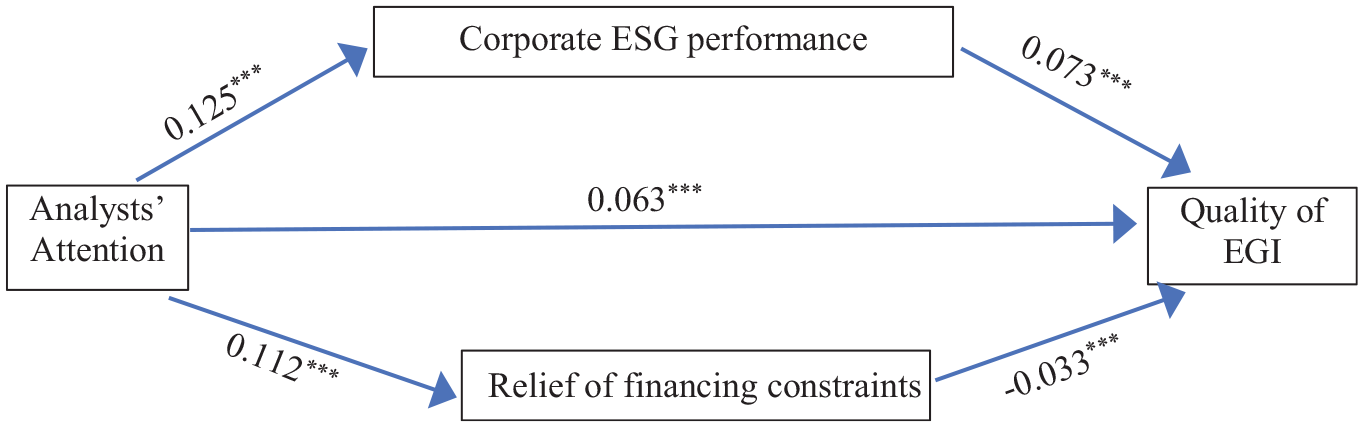

Further, we include both mediating variables in Model (8) to examine the overall effect of the two influencing channels on the quality of EGI. The test results are displayed in column (6) of Table 7. The results show that the direct effect of analysts’ attention on the impact of the quality of EGI is 0.063, and the total effect is still 0.068 in Model (2). Therefore, the total indirect effect of “corporate ESG performance + relief of financing constraints” is 0.005. According to the previous analysis, corporate ESG performance exerted a mediating effect of 0.009, while the relief of financing constraints produced an masking effect of −0.004. These results show that the external monitoring effect from analysts’ attention plays a more critical role in improving the quality of EGI and mitigates the adverse effects of financing constraints under short-termism. This finding supports Hypothesis 3b. The decomposition results of various effects in each impact path of analysts’ attention on the quality of EGI are shown in Table 8, while the specific mediation model relationship paths are organized as shown in Figure 3.

Pathways of analysts’ attention to the quality of EGI.

The results above once again highlight the significant impact of external monitoring on the connection between analysts’ attention and EGI quality. This indicates that simply easing financing constraints is not enough to improve EGI quality, but easing financing constraints under effective external monitoring can enhance EGI quality.

Further Discussions

To further investigate whether the adverse effects of easing financing constraints on the quality of EGI is due to the management’s short-sightedness, we categorize the sample into two groups: one with short-sighted and one with non-short-sighted. We adopt the method of Hu et al. (2021) as a reference, and take the chapter contents of “Management Discussion and Analysis” (MD&A) in annual reports of publicly traded companies as an object, and use text analysis and machine learning techniques to construct the short-sightedness indicator of managers, and calculate the frequency of occurrence of the term “short-term perspective” in MD&A. The short-sighted group refers to the samples with short-sighted word frequency ≥4 times, and the non-short-sighted group refers to the samples with short-sighted word frequency <4 times. The influence of the relief of financing constraints on EGI quality in the two groups was investigated respectively. The results are presented in Table 9. In the short-sighted group, relief of financing constraints has a notably adverse effect on EGI quality, indicating that relief of financing constraints is instead detrimental to the improvement of EGI quality. In contrast, the non-short-sighted group showed no significant impact on EGI quality when financing constraints were relieved. This finding supports our previous analysis, suggesting that the adverse influence of financing constraints on EGI quality is linked to short-sighted behaviors such as short-term, low-cost strategical innovation or greenwashing practices by company executives.

Heterogeneity Analysis Based on Executives’ Short-Sightedness.

Note. Standard deviations in parentheses. The short-sighted group refers to the samples with short-sighted word frequency ≥4 times, the non-short-sighted group refers to the samples with short-sighted word frequency <4 times.

***p < .01.

Meanwhile, to further test Hypothesis 3b, we group the sample based on firm performance. We use the variable “return on equity” (ROE) to measure firm performance, and categorize samples with ROE ≥ 4% into a high performance group and samples with ROE < 4% into a low performance group. Separate regressions are run for the two groups of samples. The results of the analysis are presented in Table 10. In the high performance group, analysts’ attention significantly improves EGI quality. This suggests that the external monitoring effect dominates since the impact of performance pressure is relatively small. However, in the low performance group, the external monitoring effect of analysts’ attention fails to outweigh its performance pressure effect, making the final result of the effect of analysts’ attention on EGI quality insignificant. This result also supports Hypothesis 3b, and underscore the significance of external monitoring and the varying roles of analysts in diverse settings.

Heterogeneity Analysis Based on Firm Performance.

Note. Standard deviations in parentheses. The high performance group refers to firms with ROE ≥ 4%, and the low performance group refers to firms with ROE < 4%.

p < .05. ***p < .01.

Conclusion and Policy Recommendations

Conclusion

Based on an analysis of data from Chinese manufacturing companies listed between 2012 and 2021, this research investigates how analysts’ attention affects the quantity and quality of EGI, and presents the following findings.

Firstly, the findings indicate that analysts’ attention has a beneficial effect on enhancing both the quantity and quality of EGI, and these results have been confirmed through robustness testing. This result is generally consistent with the findings of previous studies.

Second, the findings suggest that the information revealing effect plays a dominant role in the positive influence of analysts’ attention on the quantity of EGI, where the relief of financing constraints resulting from the information revealing effect plays a mediating role in both. We also find that the external monitoring effect plays a dominant role in the positive influence of analysts’ attention on the quality of EGI, where the enhancement of firms’ ESG performance resulting from the external monitoring effect plays a mediating role in the relationship.

Third, the study finds differences in the role played by financing constraints in the relationship between analysts’ attention to EGI quantity and EGI quality. Although the relief of financing constraints is able to exert a positive mediating effect in the relationship between analysts’ attention and EGI quantity improvement, it has a masking effect in the relationship between analysts’ attention and EGI quality improvement. Further tests find that executive myopia is the main cause of the adverse effect of financing constraint mitigation on the quality of EGI. However, analysts’ attention can help curb myopia and ultimately improve EGI quality through external monitoring.

Fourth, the study finds heterogeneity in the effect of analysts’ attention on the quality of EGI. While there is a significant positive effect of analysts’ attention on EGI quality in better performing firms, in worse performing firms, the performance pressure effect comes to the fore, causing the significant effect of analysts’ attention on EGI quality to disappear.

This study makes significant contributions to theory and practice in several ways. First, it extends the theoretical perspective on how analysts’ attention affects the quantity and quality of EGI, emphasizing the external monitoring effect of analysts’ attention on EGI quality. It also finds that relief of financing constraints negatively impacts EGI quality due to short-termism, and that the effect of analysts’ attention on EGI quality varies among firms with different performance levels. Secondly, from a practical perspective, it highlights the importance of utilizing and strengthening the external monitoring role of analysts to promote EGI quality. The findings also prompt further consideration on how to balance the external monitoring effect of analysts with performance pressure through differentiated policy formulation for better utilization of each effect.

Policy Recommendations

The above empirical results reveal the improvements and recommendations that can be made by external capital market monitoring to incentivize EGI.

Firstly, to enhance the monitoring of EGI, it is important to strengthen the role of financial analysts. They play a crucial role in transmitting information about capital markets and external monitoring. The government and China Securities Regulatory Commission should encourage analysts to report on and pay more attention to EGI, in order to improve its quantity and quality effectively. This will also attract more attention from investors, media, and the public, thereby strengthening the effects mentioned above.

Secondly, we need to strengthen external supervision of green fund usage. Improving the quality of EGI is crucial for green transformation. Green financial policies can encourage funds to flow into EGI, but without effective external supervision, their impact on improving ESG quality is unclear. Therefore, implementation of green financial or subsidy policies should involve not only superficial information disclosure but also field visits and continuous monitoring to ensure the substance and quality of EGI investments. Policy guidance can be used to strengthen the supervisory role of professional analysts and third-party organizations, and to ensure that green funds are invested in high-quality projects by conducting continuous tracking and supervision, improving investment efficiency and promoting the EGI quality.

Furthermore, tailored environmental regulations and green financial policies should be developed based on the diversity of enterprises. While alleviating financing constraints remains crucial for promoting EGI growth, it’s important to recognize that different companies have varying motivations and capabilities for EGI due to performance pressures and environments. A one-size-fits-all policy may lead to excessive EGI speculation and is not suitable for meeting the diverse needs of companies. Therefore, it’s essential to propose appropriate environmental regulations and green financial policies according to the actual characteristics of heterogeneous enterprises.

Limitation

There are still certain limitations in this study. Firstly, this study only uses the number of citations to green innovation to reflect the quality of EGI. Although this indicator can reflect the quality of EGI to a certain extent, it is not comprehensive enough. Because the number of citations may be affected by many other factors, it does not fully reflect the quality of EGI. Future research could consider adding other indicators to offer a more thorough evaluation of EGI quality. Secondly, since the focus of this study is on the impact of analysts’ attention on EGI, there is no way to comprehensively and systematically discuss the negative impact of financing constraint mitigation on the quality of EGI found in the study. However, the findings reflect issues that we may have overlooked in our current research, and how to ensure that the relief of financing constraints promotes the improvement of EGI quality, or how to ensure that green finance funds flow correctly to substantive green innovation, is a topic that deserves to be further explored.

Footnotes

Author Contributions

Li Li: Conceptualization, Methodology, Data curation, Software, Writing—original draft preparation. Senwei Huang: Writing—review and editing, Supervision. Junjie Lin: Funding acquisition, Validation. Jing Cui: Funding acquisition, Validation.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was support by the National Social Science Foundation of China (No. 22CGL003), the Project of Social Science Planning in Fujian Province, China (No. FJ2022BF047).

Data Availability Statement

Data on green innovation and analysts’ attention in this study were obtained from the China Research Data Service Platform (CNRDS) database at https://www.cnrds.com/Home/Login. Other data were obtained from the China Securities Market and Accounting Research (CSMAR) database at ![]() .

.