Abstract

In the context of China’s dual objectives of carbon peaking and carbon neutrality, fostering the green transformation and sustainable growth of Chinese enterprises has become a crucial societal focus. This study utilizes resource-based theory and dynamic capability theory as theoretical foundation, and drawing upon secondary data from China’s A-share listed companies spanning 2008 to 2022, empirically examines the impact of green intellectual capital (GIC) on enterprise green transformation (EGT) and its mechanism. The findings reveal that GIC has a significant positive impact on EGT. Furthermore, GIC accelerates the process of EGT by influencing absorption capability, adaptive capability, and innovation capability; and higher levels of green management innovation are conducive to strengthening the role of GIC on EGT. Additional findings reveal that the impact of GIC on EGT exhibits heterogeneity, with heavily polluting and manufacturing enterprises being more sensitive to GIC, and enterprises with better ESG performance and regions with stricter environmental regulation demonstrate a more significant promoting effect of GIC on EGT.

Keywords

Introduction

With the rapid development of industrialization, issues such as environmental pollution, resource waste, and ecological degradation have intensified, posing significant challenges to global society (Yang et al., 2023). Consequently, green transformation has emerged as a global consensus. Particularly, China even though has achieved substantial economic growth, its historically resource-intensive development model has led to critical issues in resource scarcity and environmental degradation, creating barriers to sustainable economic and social progress (Sun & Feng, 2023). In response, Chinese society has increasingly recognized the urgency of transitioning from a growth model focused on short-term gains at the expense of ecological well-being to one that supports comprehensive green transformation (Yang et al., 2024).

Existing research on enterprise green transformation (EGT) has mainly examined its external drivers such as government policies and environmental regulations (Ge et al., 2023; Liang et al., 2024; Lu et al., 2022; Shen et al., 2020; X. Wu et al., 2022). Few studies focus on factors such as organizational culture, executive leadership characteristics, and corporate governance structures (Kar et al., 2015; Quan et al., 2021; W. Zhang et al., 2023). As a systematic process, internal support mechanisms within enterprises are equally important to advancing EGT. It is imperative to seek the intrinsic momentum of EGT from the perspective of enterprises’ resource advantages. Therefore, exploring the relationship between enterprises’ resources and green transformation has significant theoretical and practical implications.

In the context of escalating environmental challenges and heightened regulatory scrutiny, green intellectual capital (GIC) has emerged as a pivotal resource for enterprises, increasingly recognized as a critical driving force in the pursuit of EGT. For instance, Huawei’s green data centers facilitate innovations in sustainable technologies and management strategies, aiming for efficient energy use and reduced carbon emissions. Likewise, as a digital platform operator, Alibaba focuses on technological and model innovations to collaborate with its value chain in achieving carbon reduction goals, backed by robust governance frameworks and green resources. However, few studies have explored the impact of GIC on EGT from the perspective of enterprise resources.

Resource-based view (RBV) emphasizes that resources are foundational to generating competitive advantages, enabling enterprises to pursue long-term and sustainable development (Wernerfelt, 1984). As a key resource for enterprises, GIC encompasses the total of intangible assets, knowledge, abilities, and relationships associated with environmental protection and green innovation, bringing more competitive advantages to enterprises (Chen, 2008). GIC promotes sustainable development by integrating environmental knowledge and concepts into enterprises (Yusliza et al., 2020). Studies suggest that effective integration, configuration, and utilization of enterprise resources and the cultivation of core capabilities are crucial for driving organizational transformation and advancement (Sirmon et al., 2007). Under the dual drive of green innovation and economic efficiency optimization, enterprises achieve green transformation, realizing the organic integration of environmental protection and economic development (Ferguson, 2015).

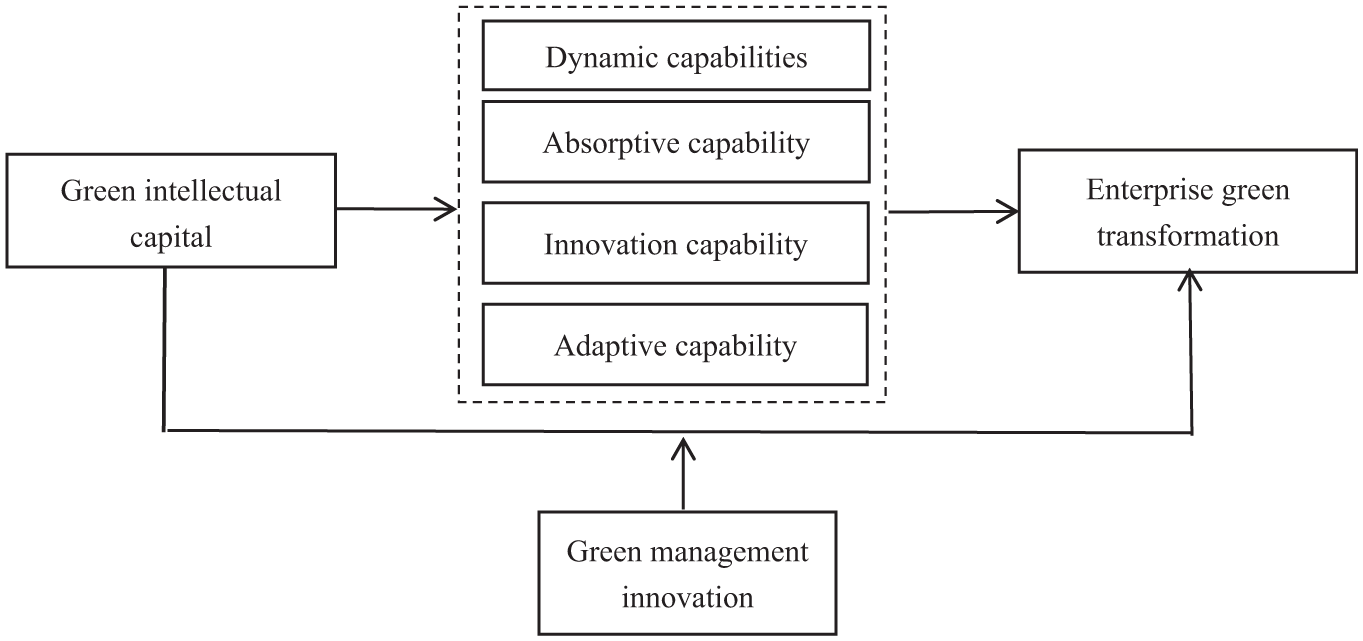

Current research confirms that GIC can improve enterprises’ extent of green innovation (Asiaei et al., 2023) as well as green performance of manufacturing enterprises (Shehzad et al., 2022). However, the mechanisms through which GIC facilitates green transformation remain underexplored, leaving a gap in understanding the pathways through which GIC supports enterprise-wide green transformation. Meanwhile, organizational transformation is inherently complex, requiring more than internal resources alone. To effectively leverage resources and capitalize on emerging opportunities during the process, cultivating key organizational dynamic capabilities (DCs) is essential (Teece, 2016; Y. Zhang et al., 2022). Based on the dynamic capability theory (DCV), the unique DCs derived from environmental changes is the key and guarantee for the smooth implementation of enterprise transformation and upgrading (Ghosh et al., 2022). Thus, understanding how DCs interact with GIC to support EGT has become an essential area of inquiry in this study.

Green management is recognized as a key driver for the transformation of green innovation into corporate green performance (Przychodzen et al., 2020). In a complex and dynamic environment, green management innovation (GMI) enables enterprises complete resource allocation, improve resource utilization, and stimulate the vitality of enterprises (Ma et al., 2018). It also plays an important role in promoting sustainable development of enterprises and environmental protection (Shu et al., 2016). However, how GMI moderates the relationship between GIC and EGT remains unclear, warranting further exploration in this domain. Accordingly, this study addresses three questions: (1) How does GIC influence EGT? (2) Do DCs (absorption, adaptation, innovation) mediate the relationship between GIC and EGT? (3) How does GMI moderate the impact of GIC on EGT?

This study aims to explore the mechanisms through which GIC drives EGT from a resource-capability perspective utilizing a sample of A-share listed companies from 2008 to 2022. By integrating the RBV and DCV, we focus on clarifying how DCs—absorption, adaptation, and innovation—act as mediators in the GIC-EGT relationship, revealing the “intellectual capital—capability accumulation—transformation practice” pathway. Additionally, we introduce GMI as a key moderating variable to explain how internal management practices strengthen GIC’s effectiveness. This study also examines how industry-specific factors (e.g., high-pollution sectors, manufacturing) and external pressures (e.g., ESG performance, environmental regulations) shape heterogeneous pathways for EGT. Ultimately, we propose a “resource-capability-internal/external context linkage” framework to support tailored strategies for green transformation.

The structure of this study is as follows. Section of literature review and hypothesis development provides a literature review and formulates the research hypotheses. Section of research methodology details the data sample, sources, variables, and methodological model employed in the study. Sections of empirical findings and further analysis present the empirical findings, followed by robustness checks, endogeneity assessments, and heterogeneity analyses to ensure the reliability and validity of the results. Sections of discussion and conclusion offer a discussion of the findings, highlighting theoretical contributions, practical implications, study limitations, and suggestions for future study.

Literature Review and Hypothesis Development

Drivers of EGT

EGT refers to shifting from an economic model characterized by high carbon emissions, pollution, and resource waste to a low-carbon, clean, and sustainable one (Z. Wang et al., 2024). It aims to mitigate adverse environmental impacts, enhance resource efficiency, and promote sustainable development (Deng et al., 2024).

From the external drivers of EGT, the government’s regulatory behavior has become a core issue in academic research in recent years. On the one hand, based on the formal institution, the government can effectively guide enterprises to implement green behaviors, enhance their environmental protection awareness, and promote the research and development of low-carbon emission technologies. As Lu et al. (2022) pointed out that the government’s green financial policies can intensify financing constraints and increase the cost of debt financing, thereby stimulating green innovation in highly polluting enterprises and forcing them to shift to green development models. In addition, Shen et al. (2020) found an inverted “U” relationship between the intensity of environmental regulation and the level of enterprise green technological innovation; as the local environmental regulation intensifies, the level of enterprise green technological innovation first increases and then decreases. Further research indicates that due to the differences in regional economic development level and corporate resource endowment, heterogeneous environmental regulation has a particularly significant role in promoting enterprise green technological innovation (L. Wang et al., 2022), thus driving the green transformation and upgrading of China’s manufacturing enterprises. On the other hand, informal institutions such as green subsidies (Bi et al., 2017) and energy-saving consumption incentives (X. Zhao et al., 2014) can help alleviate the environmental pressure brought about by regulation and enhance enterprises’ willingness to explore green transformation practices.

Regarding the intrinsic motivation for EGT, existing studies mainly focus on organizational culture and values, executive characteristics, and enterprise governance. Firstly, Kar et al. (2015) pointed out that enterprise green economic behavior is constrained by their level of environmental concern and the development of green concepts. The higher the attention paid to green development, the stronger the driving force behind promoting green economic behavior, thus facilitating the smooth progress of EGT. Through empirical research, Deng et al. (2024) found that increased awareness of carbon risk leads to alleviating the financing constraints and promoting the growth of enterprises, thus promoting the process of EGT. Meanwhile, improving enterprise governance levels plays a significant role as one of the intrinsic driving forces for enterprise transformation. For instance, W. Zhang et al. (2023) demonstrated that digital investment can drive enterprises to enhance their technical level and optimize their factor structure, thereby improving the green productivity of manufacturing enterprises and providing support for EGT. And Z. Wang et al. (2024) incorporated ESG performance into the research framework of green transformation, noting that ESG performance of enterprises has a positive impact on green innovation and total factor productivity of enterprises, which is conducive to EGT. It is worth noting that GIC can also be regarded as a key internal driving force in the process of EGT (Z. Wang et al., 2024).

Direct Effects of GIC and EGT

GIC signifies the intangible assets of enterprises, constituting the aggregate reservoir of diverse intangible resources, knowledge, competencies, and relationships centered around environmental conservation, spanning both individual and organizational strata (Chen, 2008; Huynh Mai Tram & Hoang Ngoc, 2024). In the green economy era, sustainable development and environmental preservation have emerged as pivotal directions (Dantas et al., 2021; X. Li et al., 2022; Mpofu, 2022; Yan et al., 2024). GIC differs from the traditional intellectual capital, emphasizing factors of sustainable development and environmental protection, which can be used to promote the development of the green economy and address environmental challenges. Presently, this concept is widely embraced by the international academic community, and more and more scholars have begun to research GIC (Asiaei et al., 2023; Huynh Mai Tram & Hoang Ngoc, 2024; Van Vo & Nguyen, 2023; C. H, Wang & Juo, 2021). RBV asserts that heterogeneous resources are essential for enterprise growth (Wernerfelt, 1984). As a scarce and non-imitable intangible resource, GIC will gradually replace the tangible resources and become the driving factor of the heterogeneous growth of modern enterprises. This study refers to the three dimensions of green human capital, green structural capital, and green relational capital proposed by Chen (2008) to measure enterprise GIC. Under the green transformation context, GIC can be regarded as the key strategic resources for the enterprises.

As a key element of GIC, green human capital involves the talent, skills, and knowledge in an organization that are related to environmental management and sustainable development. Employees, recognized as the driving force behind EGT, contribute significantly to the organization’s development (Gerhart & Feng, 2021). Green human capital, abundant in knowledge resources, facilitates the formulation of green strategies and cultures, shapes the enterprise’s environmental protection value orientation, and propels EGT. Meanwhile, green human capital enables enterprises to acquire a deeper understanding of environmental issues and cutting-edge green technology, identify and leverage the opportunities presented by environmental protection and green innovation, and provide technical and management support for EGT (Munawar et al., 2022). That is, the employees with environmental knowledge and technical skills can develop new products in line with market and environmental trends, such as renewable energy equipment, biodegradable materials or low-carbon transport.

Secondly, the development of green structural capital enables enterprises to acquire innovative ideas and knowledge from both internal and external sources, fostering the creation of innovative products, services, or business models (Delgado-Verde et al., 2014). It would promote the enhancement of information flow efficiency, facilitates the sharing and transmission of green knowledge, and contributes to creating a green innovation environment, providing robust support for EGT. Lastly, EGT depends not only on its autonomous efforts but also on the collaboration and support from external stakeholders, including suppliers, partners, and customers. Existing research has demonstrated that green relational capital assists enterprises in establishing green supply chains and partner relationships, thereby advancing the green transformation of the entire supply chain (Xi et al., 2022). So, this study proposes:

Mediating Effects of DCs

During the early stage of a company’s development, learning and integrating resources can be applied to enhance the organization’s competencies (Sirmon et al., 2007). Existing literature indicates a significant relationship between knowledge and capabilities (Khan & Tao, 2022; Mikalef et al., 2021). In the burgeoning green economy era, GIC, as an essential knowledge collection of enterprises, enables companies to more effectively cope with environmental changes, enhance competitiveness, and improve sustainable development capabilities (Yusliza et al., 2020). The DCV explains how an enterprise can obtain sustainable competitive advantages through its resources, and emphasizes the formation of dynamic adaptability based on specific resources, systems, and processes (Yusliza et al., 2020). In the process of transformation, the enterprise’s original core capabilities will be continuously stripped away due to environmental and strategic changes. Enterprise must evolve DCs to adapt to new strategies by expanding and combining internal and external resource elements to ensure the realization of transformation goals (Yusliza et al., 2020).

First of all, GIC significantly enhances the company’s absorptive capability, underscoring the strong correlation between the two variables. By accumulating and possessing a wealth of knowledge reserves, companies can better absorb and integrate external new knowledge into their own knowledge system (Engelman et al., 2017). Absorptive capability constitutes a prerequisite for a company’s green transformation. Against the backdrop of green transformation, companies need to actively acquire and implement knowledge and technologies associated with environmental conservation and sustainability to accomplish their green transformation goals. A company possessing a strong absorptive capability can proactively seek, acquire, and select knowledge and technologies related to green transformation (Albort-Morant et al., 2018) and apply them to actual green practices, thus promoting its green transformation. And it enables companies to stay apprised of cutting-edge green technologies and trends, offering indispensable support and guidance for their green transformation (Aboelmaged & Hashem, 2019).

Secondly, GIC contributes to enhancing enterprise adaptive capability. GIC enables enterprises to identify and comprehend the trends and impacts of environmental changes, allowing them to modify their strategies and operational models accordingly (Dang & Wang, 2022). With the support of GIC, enterprises can better adapt to environmental changes, including fluctuations in market demand, legislative changes, and changes in consumers’ environmental awareness (Shah et al., 2021). Green transformation, a dynamic process encompassing technological, policy, and market changes, necessitates strong adaptive capability (H. Li et al., 2019) and may pose new requirements for an enterprise’s organizational structure, processes, and culture (Poulsen & Lema, 2017). Therefore, based on market demand and technological advancements, enterprises can flexibly adjust the application of GIC, timely adjust strategies, resource allocation, and organizational structure, assisting enterprises in coping with uncertainties and risks during green transformation (Y. Zhang et al., 2021).

Finally, GIC guides enterprises to enhance their innovation capability. GIC provides enterprises with innovative resources such as environmental protection technology, knowledge, and experience, enabling them to develop and implement environmentally-friendly products, services, and solutions (Delgado-Verde et al., 2014). With the support of GIC, enterprises can constantly generate new ideas, develop environmentally oriented products and technologies, and improve their innovation capability (Marco-Lajara et al., 2022). Existing studies have shown that by accumulating and applying GIC, enterprises can enhance their innovation capability and achieve sustainable innovation and competitive advantages in environmental protection (Bombiak, 2023). Innovation capability plays a pivotal role in facilitating enterprise transformation. EGT necessitates innovation and improvement in various aspects, including products, services, and processes, to minimize adverse environmental impacts (Xie et al., 2019). Therefore, this study proposes:

Moderating Effects of GMI

GMI refers to the introduction or application of new low-carbon and environmental-friendly management methods and measures in the production and operation process within the firm to improve resource efficiency and protect the environment (Ma et al., 2018). Through introducing eco-friendly technologies and changes in management approaches, GMI aims to enhance resource efficiency, reduce waste emissions, and minimize environmental impacts, thereby achieving sustainable development and performance improvements (Huang & Li, 2017).

Under low-level GMI, companies may need more awareness of the significance of environmental issues and the potential benefits of green transformation. Consequently, enterprises may not take the initiative to adopt green transformation measures and will not pay attention to the cultivation and application of dynamic capabilities. On the contrary, under a high level of GMI, enterprises have recognized the urgency of environmental issues and actively implemented various green transformation measures. In this case, the degree of impact of GIC on the EGT may be more significant. On the other hand, high level of GMI implies that companies possess advanced technological and managerial capabilities in environmental protection, resource utilization, energy conservation, and emission reduction (Ma et al., 2018). That enables them to meet governmental and societal demands for environmental protection, leading to benefits like tax incentives and specialized environmental funding from the government, further promoting green transformation. High-level GMI also contributes to establishing robust stakeholder relationship networks (Yu et al., 2021). Based on these considerations, this study proposes the following hypothesis and Figure 1 illustrates the hypothesized relationships.

Conceptual framework.

Research Methodology

Sample and Data Collection

Since 2008, China and other developing and emerging economies have successively introduced green economic stimulus plans aimed at promoting the transformation of the traditional economy into a green economy. Therefore, this study focuses on China’s A-share listed companies from 2008 to 2022 as the research sample, as they are at the forefront of these green transformation efforts. A-share companies represent a diverse and dynamic group, offering a rich set of data on how firms in China are responding to the development of greener practices. To ensure the reliability of variable data, the following processing is carried out: (1) exclude the samples of listed companies that were ST (ST*) and PT in the current year; (2) exclude financial industry samples; (3) exclude samples with incomplete or severely missing data; (4) exclude anomalous observations, such as observations with asset-liability ratios outside the (0, 1) interval. To avoid the influence of extreme values, all continuous variables were winsorized at the 1% and 99% quantiles. Among them, the data on GIC is obtained using content analysis, mainly from the annual reports of listed companies and CSR reports. The data used for other variables were obtained from the Wind and CSMAR databases.

Variable Measurement

Dependent Variable

EGT: Some literature has undertaken measurements regarding EGT by constructing a comprehensive evaluation framework. For instance, C. Peng et al. (2023) developed an assessment system for EGT based on eight dimensions: green culture, green strategy, environmental information disclosure, environmental certification, green responsibility, green innovation, green emissions, and green governance. In that measurement approach, specific indicators within these dimensions are sourced from CSR reports, overlapping with the core explanatory variable, the measurement of GIC, as discussed in this study. To avoid that situation, this study draws inspiration from Hu et al. (2023) to measure EGT from the perspectives of green innovation and efficiency optimization. Specifically, green innovation (which is marked as GPA in analysis) is measured by the natural logarithm of the sum of total authorizations for green patents for listed companies plus one (Lai et al., 2022). Efficiency optimization is measured by the total factor productivity of enterprises (Hu et al., 2023). Since the OP method can effectively handle endogeneity problems and sample selection bias, this study adopts the OP method to measure enterprises’ total factor productivity (which is marked as TFP_OP in analysis).

Explanatory Variable

GIC: Current research on measuring GIC primarily focuses on two methodologies: questionnaire surveys (Nisar et al., 2021) and content analysis (Nikolaou et al., 2024). Due to the challenges of gathering data through questionnaire surveys, often resulting in limited sample sizes, and the preference of listed companies in China for textual descriptions when disclosing their GIC, this study is inspired by the studies of Abeysekera and Guthrie (2005), Beattie and Thomson (2007), Bozzolan et al. (2003), Pirogova et al. (2020), and Liu (2010), and measures the level of GIC of enterprises based on content analysis method. The specific steps are as follows:

Firstly, this study uses Python software to extract sentences related to green environmental protection in sample CSR reports and annual reports, and items related to environmental management or green innovation are reserved.

Subsequently, the frequency of keywords associated with “green human capital,”“green structural capital,” and “green relational capital” within these sentences was recorded as their respective scores. An additional point was awarded if specific data was disclosed within the items.

Finally, this study calculates the composite score (marked as GIC in analysis) as a measure of a company’s GIC level using the coefficient of variation method based on the scores for each dimension. The original data was dimensionless processed as

Key Words.

Mediation Variable

DCs: Following C. L. Wang and Ahmed (2007), this study examines the DCs of enterprises from three dimensions: absorptive capability (RD), adaptive capability (AVC), and innovation capability (IC). The measure of RD is calculated as the ratio of a firm’s R&D expenditure to its operation revenue (Tsai, 2009). AVC is evaluated using the coefficient of variation in a firm’s R&D, capital, and advertising expenditures for the current year (Y. Wang et al., 2023). To provide a more comprehensive assessment of IC, this study follows Y. Wang et al. (2023) who utilize the standardized total number of two indicators: R&D intensity and the proportion of technical personnel. This study then computes a weighted average of each sample firm’s RD, AVC, and IC for the current year to reflect the overall level of DCs.

Moderating Variable

GMI: According to X. Zhao et al. (2015), five indicators were designed to measure GMI. Considering the data availability, based on the disclosure of environmental information of listed companies in the CSMAR environmental database, indicators such as ISO14001 certification status, ISO9001 certification status, environmental management system, environmental education and training, and environmental protection particular campaigns were aggregated to obtain a composite score. The natural logarithm of the composite score plus one was used as a proxy indicator for GMI.

Control Variables

Referring to the existing research on the impact of factors related to EGT (Niu et al., 2022; C. Peng et al., 2023), the control variables include firm characteristics and governance structure levels. The firm characteristics level includes variables such as enterprise size (Size), debt-to-asset ratio (Lev), return on assets (ROA), cash flow level (Cashflow), firm age (Firmage), and ownership nature (SOE). The governance structure level includes variables such as board size (Board), board independence (Indep), and Shareholding Concentration (Top1). In addition, this study also sets up virtual variables for the year (year) and individual (enterprise). The specific definitions and calculation methods of the variables are shown in Table 2.

The Variables Used in the Study.

Model Construction

This study uses a two-way fixed effect model to explore the impact of GIC on EGT. The set measurement model is as follows:

Where,

The above theoretical analysis points out that GIC drives the EGT by enhancing their absorptive capability, improving their adaptive capability and innovation capability. To further clarify the impact mechanism of GIC on enterprises’ green transformation, this study adopts the intermediary effect model proposed by Mubarik et al. (2021) for further analysis and builds the following model (2) :

The above theoretical analysis points out that GMI can realize efficient utilization of enterprise resources and strengthen the driving effect of GIC on EGT by introducing green technology and innovative management methods. Therefore, to further investigate the moderating effect of GMI on the relationship between GIC and EGT, this study successively adds GMI and its cross-term with GIC (GIC×GMI) on the basis of the baseline regression model. To avoid the multicollinearity problem between the interaction term and explanatory variables, mean centralization processing is performed for both GIC and green innovation management indicators. As shown in Model (3):

Empirical Findings

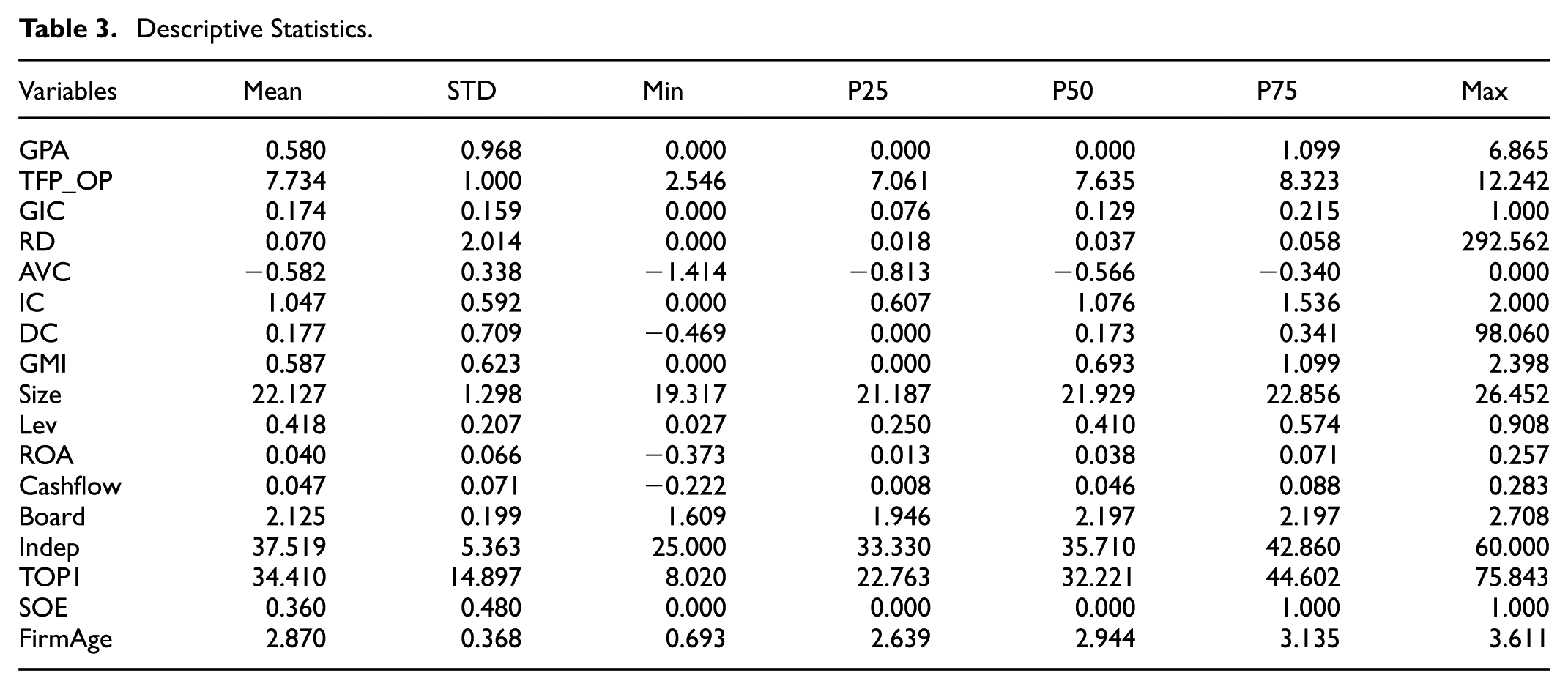

Descriptive Statistics

Table 3 lists the descriptive statistics of the main variables in this study. It can be seen from the table that the average value of the dependent variable GPA in the entire sample is 0.580, with a significant difference between the minimum and maximum values, indicating an imbalanced distribution. Another dependent variable TFP_OP also exhibits similar characteristics, with an average of 7.734, a standard error of 1.000, a minimum of 2.546, and a maximum of 12.242. This suggests that there are significant differences in the levels of green innovation and efficiency optimization between different enterprises, and the degree of green transformation is low. Therefore, it is still necessary to take measures to actively promote the green transformation. The descriptive statistics of the remaining variables are presented in Table 3.

Descriptive Statistics.

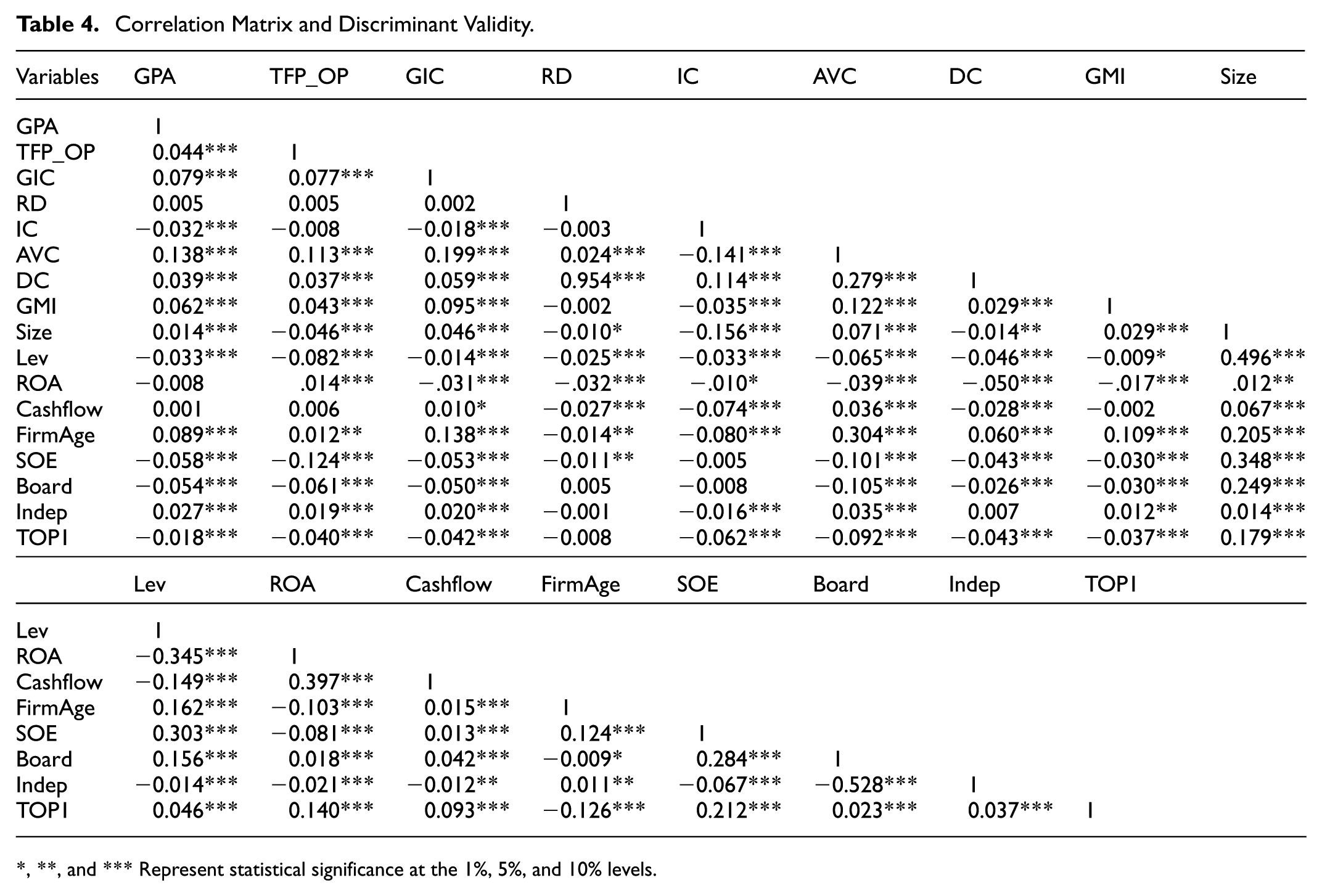

Correlation Analysis

Table 4 presents the correlation coefficient matrix between the main variables in this study. It can be seen from the table that enterprise green innovation (GPA) and efficiency optimization level (TFP_OP) are significantly positive with GIC at the 1% level, initially indicating that the degree of EGT is positively correlated with the level of GIC. Part of these results conform to theoretical expectations, laying a good foundation for the subsequent regression analysis.

Correlation Matrix and Discriminant Validity.

, **, and *** Represent statistical significance at the 1%, 5%, and 10% levels.

Multiple Regression Analysis

GIC and EGT

This study empirically studies the relationship between GIC and EGT using the above econometric models. The estimation results of the baseline regression model are presented in Table 5. Columns (1) and (3) of Table 5 represent the univariate regression results that only control for year and individual fixed effects, with the coefficients of GIC being significantly statistical. Columns (2) and (4) further add control variables at the corporate level. The result shows that the regression coefficient of GIC on enterprise green innovation (GPA) is 0.0923, which is significant at the 5% level, and the regression coefficient on total factor productivity optimization (TFP_OP) is 0.169, which is significant at the 1% level. That indicates that GIC significantly drives EGT, significantly improving enterprise green innovation and efficiency optimization levels, thus verifying H1.

Green Intellectual Capital and Enterprise Green Transformation.

** and ** indicate 1% and 5% level of significance respectively.

GIC, DCs, and EGT

Together, Tables 6 and 7 report the mediating effects of absorptive capability, adaptive capability, innovative capability, and overall DCs. In Columns (1), (3), (5), and (7) of Tables 6 and 7, the coefficients of GIC are significantly positive at the statistical level of 1% to 5%. It shows that the higher the level of GIC, the higher the enterprise’s absorptive, adaptive, innovative, and overall DCs. After adding the mediating variables in turn, in Columns (2), (4), (6), and (8) of Tables 6 and 7, the coefficients of absorptive capability, adaptive capability, innovative capability, and overall DCs are all significantly positive at the statistical level of 1% to 10%. In contrast, the coefficient of GIC is still significantly positive. It shows that improving the level of GIC can enhance the absorptive, adaptive, innovative, and overall DCs of enterprises. It has a positive impact on the EGT. Therefore, dynamic capability and its three dimensions play a specific mediating role in GIC’s impact on enterprises’ green transformation. H2 is confirmed.

Mediating Effect of Dynamic Capabilities-1.

**, **, and * Indicate 1%, 5%, and 10% level of significance.

Mediating Effect of Dynamic Capabilities-2.

**, **, and * Indicate 1%, 5%, and 10% level of significance.

GIC, GMI, and EGT

The regression results in Table 8 show that the coefficients of GIC on GPA and efficiency optimization (TFP_OP) are significantly positive at the statistical level of 1% to 5%. It shows that the GIC of enterprises can promote the level of green transformation. In addition, by introducing GMI and its interaction term (GIC×GMI) into the regression model for testing, the results show that, as shown in Columns (3) and (6), the coefficient of the interaction term is significantly positive at the level of 5%. The results show that with the continuous improvement of the GMI level, GIC plays a more significant role in promoting the EGT. Further, the GMI of enterprises significantly strengthens the driving effect of GIC on the EGT. H3 is confirmed.

Moderating Effect of Green Management Innovation.

**, **, and * indicate 1%, 5%, and 10% level of significance.

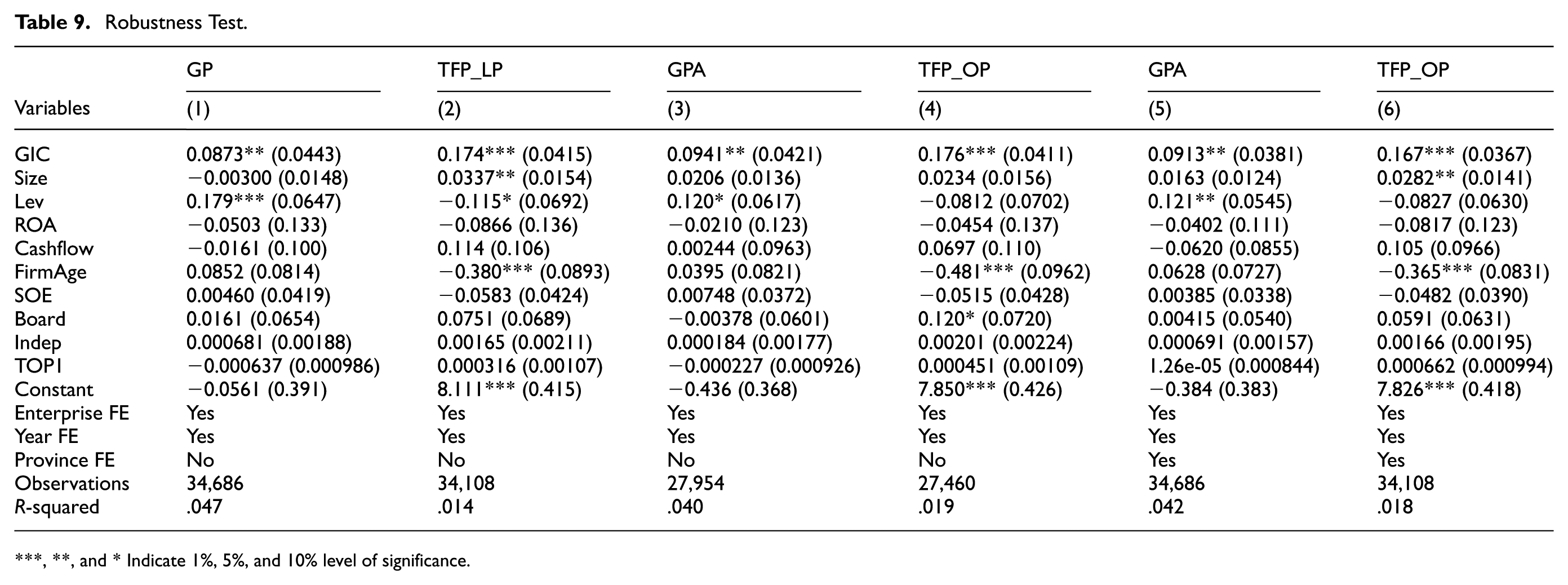

Robustness Test

Substituting the Dependent Variable

To test the robustness of the benchmark regression results, considering that the measurement of enterprise green innovation level might be affected by the cyclical and lagging effects of green patent authorization, this part uses the natural logarithm of the annual green patent application volume plus 1 (GP) of listed companies to measure the enterprise green innovation level. In addition, the total factor productivity (TFP_LP) measured by the LP method is used to measure the level of efficiency optimization in enterprises. The results, as shown in Columns (1) and (2) of Table 9, are consistent with those of the previous study.

Robustness Test.

**, **, and * Indicate 1%, 5%, and 10% level of significance.

Removing Samples From Directly Administered Municipalities

Considering that enterprises located in municipalities may be affected by uncertain factors such as policy and economy, this section tests the robustness of the benchmark regression by removing samples from directly administered municipalities. After excluding the sample of enterprises in the municipalities directly under the central government, the results are shown in Columns (3) and (4) of Table 9, where the coefficient of GIC is significantly positive at the statistical level of 1% to 5%. That indicates that after removing the samples from municipalities directly under the central government, GIC still positively impacts the level of green innovation and efficiency optimization of enterprises. Therefore, the conclusion that GIC positively impacts enterprises’ green transformation is robust.

Controlling More Fixed Effects

Considering that the degree of green transformation and the level of GIC of enterprises in different regions may differ, this part adds a provincial fixed effect to the original benchmark measurement model. As shown in Columns (5) and (6) of Table 9, the coefficients of GIC are significantly positive at the statistical level of 1% to 5%. Therefore, after controlling the influence of regional change, GIC still has a significant positive influence on the level of green innovation and efficiency optimization of enterprises. The validity of the benchmark regression results is demonstrated.

Endogeneity Test

Heckman Two-Stage Method

To further alleviate the endogeneity problem caused by sample selection bias, this paper adopts the Heckman two-stage method, and the control variables selected include enterprise scale, debt-to-asset ratio, return on assets, cash flow level, enterprise age, property rights nature, board size, board independence and equity concentration. The Probit regression is used to calculate the inverse Mills ratio (IMR). Furthermore, the IMR is further incorporated into the model to re-test H1. The results show that the research conclusions of this paper remain robust, namely, GIC is beneficial to promoting EGT. As shown in Table 10 Columns (1) and (2), the study’s findings still hold true.

Endogeneity Test.

**, **, and * Indicate 1%, 5%, and 10% level of significance.

Adjusting the Period of the Independent Variable

Considering that the cycle of EGT is relatively long, there may be a time lag in the impact of the current year’s GIC level on green transformation. Therefore, the explanatory and control variables are lagged by two periods (t-2 period) and re-introduced into the regression model. The results are shown in Columns (3) and (4) of Table 10, where the coefficient of GIC is significantly positive at the 5% statistical level. That indicates that GIC has a significant positive impact on the EGT over a long period. The benchmark regression conclusion remains reliable.

Instrumental Variable Method

To address reverse causality, this study uses the mean green intellectual capital (GIC) of firms in the same city and industry (excluding the sample firm) as an instrumental variable (IV) and employs a two-stage least squares (2SLS) approach. The IV is valid because: First, the GIC of firms in the same city and industry is highly correlated with that of the sample firms, as they face similar external environments (e.g., local policies and industry standards). Second, the instrumental variable satisfies the exogeneity condition, as it affects EGT only through the GIC of the sample firms, while the influence of any single firm on the overall industry level is limited, thereby mitigating reverse causality. Table 10 shows the first-stage (Column (5)) regression coefficients of the IV on GIC are significant, confirming relevance. In the second stage (Columns 6 and 7), GIC coefficients remain significant at 5% to 10%, aligning with baseline results and supporting its role in driving green transformation.

Further Analysis

Analysis of Heterogeneity of Pollution Levels

The enterprises’ green transformation process is closely related to the degree of pollution emission in their industries. According to the Guidance on Industry Classification of Listed Companies revised by the China Securities Regulatory Commission in 2012, 16 industries such as coal, mining, textile, and petroleum are classified as heavy polluting industries, and the rest are classified as non-heavy polluting industries for grouping regression. The regression results are shown in Columns (1) and (2) of Table 11. Compared with enterprises in non-heavily polluting industries, the GIC of heavily polluting industries plays a more significant role in promoting green innovation. In addition, the regression results of Columns (5) and (6) show that GIC has a significant positive impact on the efficiency optimization of enterprises in both heavily and non-heavily polluting industries. However, the incentive effect of GIC on the efficiency optimization of heavily polluting industry enterprises is relatively more significant. The possible reason is that, compared with enterprises in non-heavy polluting industries, enterprises in heavily polluting industries are often subject to stricter government supervision and more significant penalties, facing tremendous pressure of green transformation, and such enterprises have more vital willingness and motivation to improve the level of GIC to achieve green transformation. Therefore, the promotion effect of GIC on the EGT is greater than that of non-heavy polluting enterprises.

Heterogeneity Test Results-1.

**, **, and * Indicate 1%, 5%, and 10% level of significance.

Analysis of Industry Heterogeneity

This section classifies the sample listed companies according to whether they belong to manufacturing industries. As manufacturing enterprises are the main focus of government monitoring for environmental pollution prevention and control, their demand for green transformation is more urgent. Therefore, compared with non-manufacturing enterprises, the GIC of manufacturing enterprises has a more apparent driving effect on the EGT. Based on this, this study examines the industry’s heterogeneity of GIC in the EGT. Columns (3) and (4) of Table 11 show that, compared with non-manufacturing enterprises, the GIC of manufacturing enterprises has a more obvious promoting effect on the green innovation level of enterprises. In addition, Columns (7) and (8) show that the promoting effect of GIC on the optimization level of enterprise efficiency is more significant in manufacturing enterprises. The test results show that compared with non-manufacturing enterprises, the GIC of manufacturing enterprises can better drive enterprises to carry out green transformation activities because of the more substantial pressure of environmental regulation legitimacy and the more urgent demand for green transformation and upgrading.

Analysis of Heterogeneity of Enterprise ESG Responsibility

Under the concept of advocating green and sustainable economic development, enterprise ESG ratings have emerged as a timely response. ESG rating is an evaluation system that comprehensively scores the overall performance of enterprises in three aspects: environment, society, and enterprise governance. Enterprises with high scores pay more attention to resource conservation, environmental protection, and social responsibility in production and development, which can enhance enterprises’ social image and market competitiveness, improve resource allocation efficiency, and play a good supporting role in the EGT. As a result, the Sino-Securities index discloses a composite score of ESG performance that includes ESG performance. All samples are divided into high-ESG-performance companies and low-ESG-performance companies based on the median of annual enterprise ESG performance, and sub-sample regression is carried out. The results are shown in Columns (1), (2), (5), and (6) of Table 12. GIC with high ESG performance significantly promotes the EGT. GIC with low ESG performance has no significant impact on the EGT, which is in line with expectations. That means enterprises with a high ESG score pay more attention to environmental protection and sustainable development and create a good governance environment by increasing investment in green innovation, resource allocation, and employee efficiency. Such environmental awareness and practice make it easier for these enterprises to switch to green production and operation modes. Therefore, the GIC of enterprises with better ESG performance can more effectively promote the acceleration of EGT.

Heterogeneity Test Results-2.

**, **, and * Indicate 1%, 5%, and 10% level of significance.

Analysis of Heterogeneity of Regional Environmental Regulation Intensity

Due to the profit-seeking nature of enterprises, they tend to ignore the protection of the ecological environment while pursuing the maximization of interests. Environmental regulation initiated by the government with incentives or mandatory means is a meaningful way to curb the deterioration of the ecological environment and force enterprises to achieve green transformation and development. In areas with high environmental regulation intensity, enterprises will face more significant pressure and constraints, so they are more motivated to carry out green transformation, actively develop and apply green technologies, improve resource utilization efficiency, and reduce the negative impact on the environment. Conversely, companies may need more motivation and resources to drive a green transition in regions with weak environmental regulations. Government environmental regulation can influence the willingness and behavior of enterprises to carry out green transformation. Therefore, the driving force of enterprises’ GIC on green transformation varies with the intensity of regional environmental regulation. Referring to the method of Chen and Chen (2018), this study uses the natural logarithm of the number of relevant word frequencies in the government work report plus 1 to measure the environmental regulation intensity of each region. The sample of businesses was split into two groups based on each province’s average level of environmental regulation. One group had a lot of environmental regulations, and the other had few. That was done to see how the different types of GIC affected the green transformation. As can be seen in Table 12, the regression results are in Columns (3), (4), (7), and (8), which indicates that in regions with higher environmental regulation intensity, the driving effect of GIC on enterprises’ green transformation is more substantial.

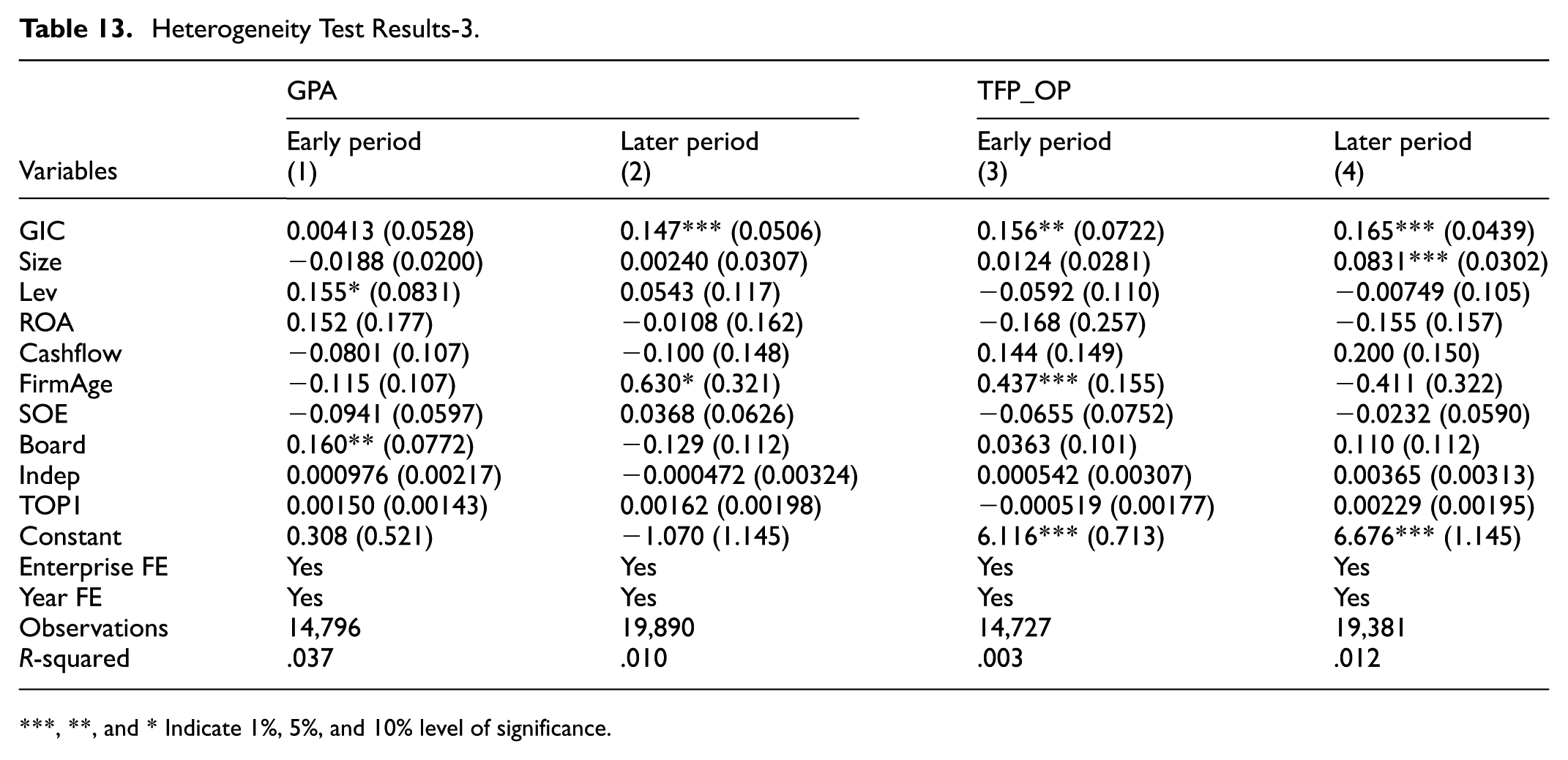

Analysis of Heterogeneity in Temporal Policy Contexts

The evolution of China’s environmental governance system exhibits distinct phased characteristics. During the early policy formulation phase (2008–2015), environmental regulations primarily served as mandatory constraints, with enterprises adopting passive compliance strategies that limited the effective utilization of GIC. However, since the implementation of the “Dual Carbon” goals, environmental regulation has transformed into a strategic driver for corporate development. The establishment of market-oriented mechanisms such as carbon emission trading and green financial systems has fundamentally altered the institutional logic of enterprise operations. To examine how temporal variations in policy systems affect the implementation effectiveness of GIC, this study conducts sub-period regression analyses based on major policy inflection points. We divide the research period into two phases: the early period (2008–2015) and the later period (2016–2022). The regression results in Table 13 reveal significant temporal heterogeneity: In the later period, the marginal effect of GIC on EGT increased substantially compared to the earlier phase. This amplification effect stems from the synergistic interaction between market-oriented environmental policies and corporate strategic cognition, where carbon pricing mechanisms and green technology subsidies enhanced the market value conversion efficiency of GIC. The findings confirm that the effectiveness of GIC in driving EGT depends on the maturity of environmental policy systems and the strategic adaptability of enterprises.

Heterogeneity Test Results-3.

**, **, and * Indicate 1%, 5%, and 10% level of significance.

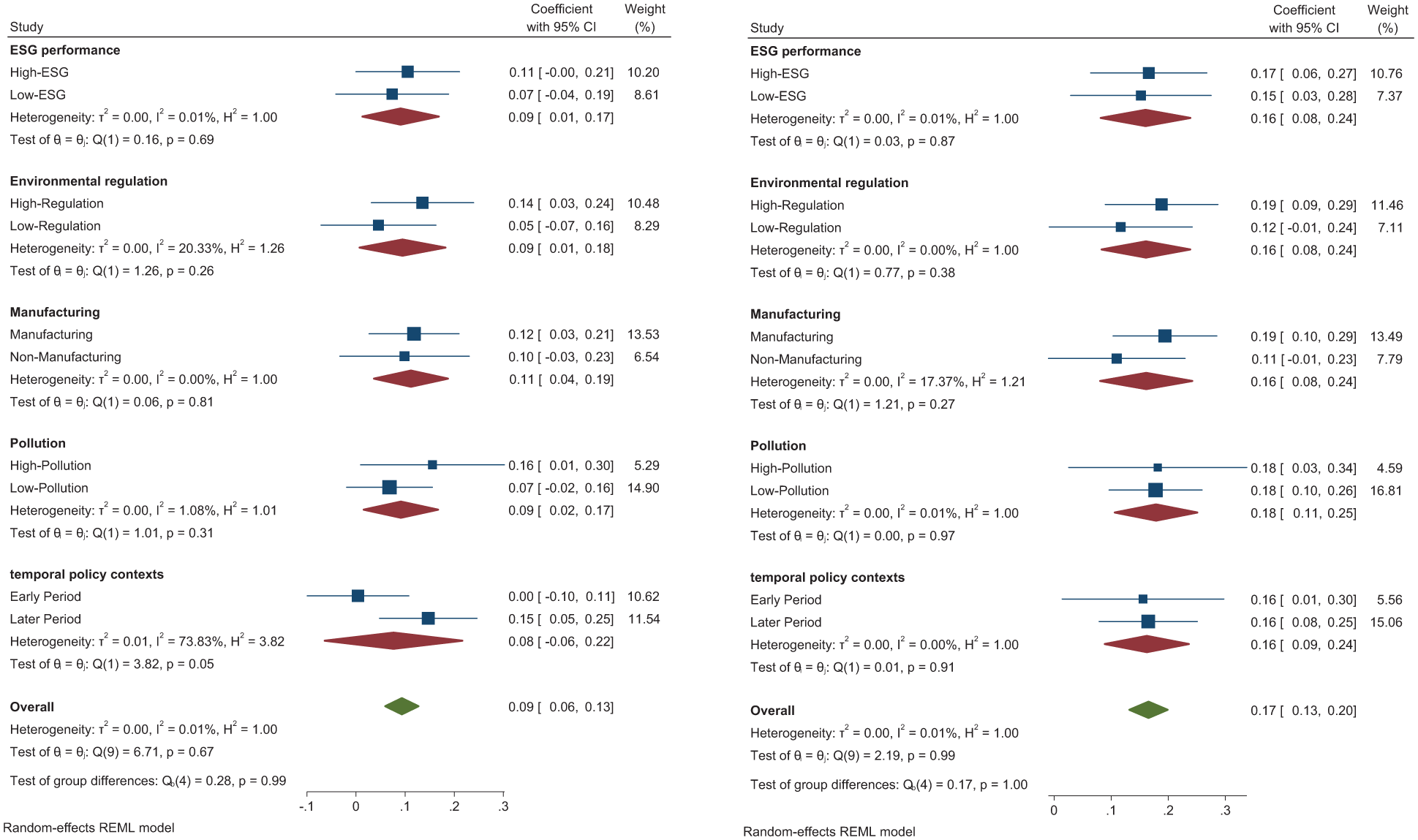

As illustrated in Figure 2, the forest plot analysis reveals multidimensional contextual heterogeneity in the effects of GIC on EGT. The results demonstrate that GIC exerts more pronounced impacts on high-pollution firms, manufacturing enterprises, firms with superior ESG performance, and those operating under stringent environmental regulations, with amplified effects observed in the post-policy reinforcement period. Heterogeneity test reveals that environmental regulation pressure, industry technological attributes, the ESG governance framework, and policy dynamics collaboratively drive the differentiated effects. The study suggests that green transformation policies should precisely target high environmental risk enterprises, enhance the technological transformation capabilities of the manufacturing sector, improve the ESG governance incentive mechanisms, and emphasize the temporal coordination between policy interventions and market mechanisms to fully unleash the governance potential of GIC.

Results of heterogeneous test.

Discussion

In this study, the panel data of A-share listed companies from 2008 to 2022 are selected as research samples to reveal the relationship between GIC and EGT. It tests the mediating effect of DCs and the moderating effect of GMI, reaching the following results:

Firstly, GIC has a positive impact on EGT. This result is different from the existing research on the EGT from external factors such as national policies and environmental regulations (Tsai, 2009), and it indicates that enterprises can significantly improve the level of green innovation and efficiency optimization by developing and utilizing internal resource GIC, hereby promoting the process of EGT. From the perspective of the firm’s own resource advantages, the results provide a theoretical basis for the intrinsic momentum of EGT, and also verify and supplement existing research. GIC has a relatively significant effect on enhancing enterprise’s production efficiency (Tsai, 2009), environmental performance (Mansoor et al., 2021), green image (Khan et al., 2023), and promoting enterprises to adopt sustainable development strategies (Feng et al., 2024), all of which are key to accelerating the pace of EGT.

Secondly, the research results have verified that DCs serve as a bridge for releasing the value of resources (Teece, 2007) and are key drivers of corporate transformation. By acquiring, developing, and effectively utilizing GIC, enterprises can effectively enhance their absorption capability, promote innovative and adaptive capability, and thereby continuously advance towards green transformation (Ye & Lau, 2022). This result validates and complements the existing studies (Tsai, 2009), and the more obvious mediating role of absorptive capability is a prominent finding in this study. Absorptive capability puts more emphasis on the identification, acquisition, and transformation of knowledge, and enterprises with strong absorptive capability are more inclined to choose green transformation-related technologies (Tsai, 2009). Therefore, the EGT can be promoted more effectively through GIC. In addition, for developing countries, EGT is still in the transitional stage, and the influence of absorptive capability on the breadth and depth of knowledge is more obvious, which also forms a response to previous studies (Tsai, 2009).

Additionally, this study reveals that GMI can strengthen the role of GIC in promoting EGT. In that case, it possesses superior technology and management capabilities in environmental protection, resource utilization, improving the relationship network of stakeholders, enhancing the support for corporate green culture (Tsai, 2009), energy conservation and emission reduction, achieving efficient resource utilization, and thus promoting EGT. Compared with technological innovation, the research on management innovation in the academic circle is still insufficient. Therefore, this study enriched the research on management innovation and provided support for how GMI can be transformed into enterprise performance (Przychodzen et al., 2020). In addition, different from previous studies, this study innovatively focuses on the regulatory role of GMI in promoting EGT by resources, and this result has enriched the research on GMI in promoting corporate sustainable development (Ma et al., 2018).

Finally, regarding industry heterogeneity, the promotional effect of GIC on EGT is more significant in heavily polluting and manufacturing industries. EGT can reduce production costs, improve resource utilization efficiency, and enhance corporate competitiveness (J. Wu et al., 2021). Therefore, enterprises in these categories have a stronger willingness to engage in green transformation (Y. Zhao et al., 2024). Different from the focus of previous studies, the results of this study propose: that heavily polluted enterprises and manufacturing enterprises are more urgently in need of support and guidance from GIC to address environmental challenges. Moreover, enterprises with good ESG performance usually advocate more strongly for green and environmental protection concepts, promoting the formation of low-carbon and circular operation modes, and leading enterprises to transform towards green development (Z. Wang et al., 2024). Enterprises operating in regions with solid environmental regulation face greater environmental pressure and regulatory restrictions. In such an environment, enterprises must assume more environmental responsibilities (Shen et al., 2020).

Conclusion

Theoretical Implications

This study significantly contributes to the existing literature. Firstly, by exploring EGT through the lens of the firm’s GIC, we propose a viewpoint that has thus far been overlooked. Although existing studies have investigated the important role of external means such as national policies and environmental regulations on enterprises’ green and low-carbon transformation (Lu et al., 2022; Shen et al., 2020), it remains unclear whether and how GIC, an important internal resource of firm, promotes EGT. Our study fills this gap. It shifts the focus to the enterprise resource level, expands the research scope of EGT, and provides a new perspective for further exploring EGT.

GIC, as an important resource for enterprises in the era of the green economy, can be combined with their own capabilities through effective organization and allocation (Al-Khatib & Shuhaiber, 2022) to promote enterprise transformation and upgrading. This study proposes an integrated theoretical framework based on RBV and DCV, and further elucidates the role of DCs as a mediating variable in the causal chain between GIC and EGT. This mechanism bridges the RBV and DCV paradigms and deepens our understanding of the “resource-capability-outcome” research framework, offering fresh insights for related field research on RBV and DCV.

Additionally, by exploring the boundary conditions affecting the effect of GIC on EGT, this study reveals the role of GMI as a moderating variable in the causal chain between GIC and EGT. We prove that GMI, as a peculiar subset of both green innovation and management innovation, as well as a combination of these two areas (Ma et al., 2018), is an essential conditional factor to fully utilize the effectiveness of GIC, thereby expanding the research in the field of green innovation and management innovation.

Lastly, this study also explores the differences between the enterprise industry, pollution level, ESG performance, and regional environmental regulation intensity on GIC to EGT, which lays a theoretical foundation for future research to further reveal the complexity of EGT under different backgrounds.

Practical Implications

In the era of the knowledge economy, enterprises relying on material resources will face severe limitations on their development prospects. Enterprises should actively transform their development model, change their past reliance on non-renewable resources, and develop GIC, relying on knowledge to drive enterprise development (Yusliza et al., 2020) to achieve EGT. It is worth noting that in promoting the accumulation of GIC and the green transformation of enterprises, China’s policymakers have played an important role as system designers and resource enablers. The policymakers can promote green innovation in enterprises by moderately strengthening environmental regulation (H. Peng et al., 2021). They have defined clear green transformation strategies for enterprises through national strategies such as the “dual-carbon” target and the 14th Five-Year Plan for Green Industrial Development; and reduced green innovation costs through special green funds and R&D subsidies (e.g., exemption of vehicle purchase tax on new energy vehicles). During the period of economic transformation, institutional system construction is an important guarantee and support for promoting EGT (Xu et al., 2023). In order to incentivize enterprises to invest in GIC, policymakers have set up demonstration zones for the application of green technologies (e.g., the Ordos-envision net-zero industrial park), which provide enterprises with technology verification scenarios and reduce the risk of market promotion; they have also set up additional carbon-neutral disciplines in colleges and universities, and set up joint enterprises with practical training bases in green technologies to cultivate more green talents.

Under the context of ESG performance becoming the core competitiveness of enterprises, firms need to deeply integrate ESG goals with carbon neutrality and national sustainable development goals through systematic strategic design. To achieve that goal, enterprises can cultivate green knowledge-based employees through regular green knowledge training and the establishment of knowledge-sharing mechanism, so as to form a top-down green culture (Yeşiltaş et al., 2022). Furthermore, enterprises should develop standardized CSR reports and disclose them publicly on a regular basis to enhance information transparency. Such transparency is vital in facilitating the public’s comprehensive understanding of the enterprise’s internal operations and environmental impact, which, in turn, aids in the construction of a positive corporate image (Hengboriboon et al., 2022).

Additionally, enterprises should focus on enhancing DCs, and the synergy between GIC and DCs to adapt to the changing environment and market demand (Farzaneh et al., 2022). In the green transformation, based on the DCV, enterprises should cultivate relevant environmental awareness talents or relevant mechanisms, aiming to be able to quickly and accurately identify policy, market, and technology trends. Specifically, enterprises can establish an internal knowledge management system to centrally store environmental protection knowledge and best practices, encourage employees to study, transform, absorb, and utilize new thinking in the field of environmental protection, and promote green innovation. By establishing a robust market monitoring mechanism and regularly releasing market analysis reports, enterprises should gather key information through market surveys and competitive analyses to promptly understand market needs and competitive trends. This information can guide the strategic development of environmentally friendly products or services and enhance the appeal to new customer segments.

Lastly, companies should strengthen GMI, improve the green management system through innovative green management technologies and methods, integrate existing management processes with environmental requirements, regularly evaluate and optimize, strategic planning and integrate resources to improve efficiency (Ma et al., 2018). At the same time, cross-departmental cooperation between different departments is encouraged to promote the integration of resources and find the best environmental protection solutions. By setting up a specialized green management department, clarifying responsibilities, and establishing a clear organizational structure and workflow, companies can ensure the effective implementation of green transformation and achieve sustainable development goals.

Limitations and Future Research Direction

Firstly, the scope of this study is limited. Due to data availability, this study only examined the situation of Chinese listed companies, and did not include small and medium-sized enterprises and companies from other developing countries. Future research can expand the sample size to enhance the generalizability of the findings. Furthermore, different industries may face different challenges and opportunities in green innovation and environmental management. Future research could explore GIC’s performance in different industry contexts, such as manufacturing, high-pollution industries or emerging technology industries, and understand the characteristics and impact of GIC in each industry, to further reveal its green transformation path, and expand the depth of research.

Secondly, although this study investigated the mechanism of DCs and GMI in the relationship between GIC and EGT, other factors may also influence this relationship. It is essential to recognize the complexity of the EGT path and the diverse characteristics of influencing factors, and to consider other potential variables that may lead to EGT. Future research can be based on factors such as firm characteristics and government behaviors to gain a more comprehensive understanding of this relationship.

In addition, GIC amalgamates three distinct facets, green human capital, green structural capital, and green relational capital, into a singular measure in our framework. However, our comprehensive approach to measuring GIC may not fully capture the unique characteristics and impacts of each individual dimension. Subsequent studies could explore breaking down the GIC construct into its constituent dimensions to gain a more in-depth understanding of their respective contributions to the phenomenon being studied. By separating these dimensions, a more detailed analysis could be conducted, enhancing the theoretical and practical implications of the research. Meanwhile, this study only uses secondary data disclosed by listed companies to test the theoretical model. Future studies can adopt case studies and questionnaire surveys to collect data for non-listed companies to test the theoretical model.

Footnotes

Author Contributions

Li-Yuan Wang: conceptualization, validation, investigation, resources, funding acquisition, methodology, project administration. Chun-Liang Yao: writing—reviewing and editing, validation, supervision, project administration. Dong-Yi Yan: conceptualization, methodology, software, formal analysis, data curation, writing—original draft preparation, visualization.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was funded by the Science Research Project of Hebei Education Department (BJ2025264), Hebei Collaborative Innovation Center for Urban-rural Integrated Development Research Project (2023JXYB02), and the Soft Science Research of Hebei Provincial Science and Technology Program (25357629D).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The supporting data for this research’s conclusions can be obtained from the corresponding author, subject to a reasonable request.