Abstract

The green credit policy has become a key measure for addressing pollution issues and promoting economic green transformation. This study uses the difference-in-differences model to examine the impact and mechanisms of the Green Credit Guidelines on the green transformation of high-polluting enterprises, using A-share listed companies in China from 2007 to 2021 as the sample. Our comprehensive performance evaluation of enterprise green transformation is based on pollution emissions, financialization, and total factor productivity. The results show that the green credit policy significantly enhances enterprises’ emission reduction effectiveness while reducing financialization and suppressing total factor productivity. Mechanism analysis indicates that the green credit policy primarily stimulates green innovation and mitigates financialization by imposing increased financing constraints; however, it also crowds out overall R&D investment, thus harming economic performance. The results support the “extrusion effect” rather than the “Porter effect.” Heterogeneity tests demonstrate that the green transformation of non-state-owned, low endogenous financing, eastern region, and strong socially responsible enterprises is more pronouncedly influenced by the policy. Further, the level of green finance development and the intensity of environmental regulations exhibit differential moderating effects on the policy’s outcomes. This study examines the effect of the green credit policy from multiple dimensions and highlights the contradiction between emission reduction and sustainable development, providing insight into the green transformation of high-polluting enterprises.

Plain language summary

The green credit policy has become an important tool for addressing environmental issues and promoting green economic transformation. This study examines the impact of green credit on the green transformation of high-polluting enterprises and evaluates the performance of green transformation from three dimensions: pollutant emission, financialization, and total factor productivity. Using A-share listed companies in China from 2007 to 2021 as the sample, we found that the green credit policy significantly enhances enterprises’ emission reduction effectiveness while reducing financialization and suppressing total factor productivity. Mechanism analysis shows that the green credit policy stimulates green innovation and mitigates financialization through increasing financing constraints; however, it also crowds out overall R&D investment, thus harming total factor productivity. Heterogeneity tests demonstrate that the green credit policy is more pronounced in non-state-owned, low endogenous financing, eastern region, and strong socially responsible enterprises. Further, the development level of green finance and the intensity of environmental regulation have different influences on the effect of green credit policy. This study not only examines the effect of green credit policy from multiple dimensions but also reminds enterprises to pay attention to the contradiction between emission reduction and sustainable development.

Keywords

Introduction

The global focus has intensified on environmental degradation and climatic alterations stemming from carbon emissions. Rapid urbanization and industrialization cause environmental problems and pose challenges to economic growth (Y. Lu et al., 2022; Niu et al., 2022). China’s economy has grown rapidly while becoming the foremost contributor of global carbon dioxide emissions (C. Wang et al., 2017). Environmental issues have become a key factor restricting the high-quality development of the Chinese economy (Zhao & Luo, 2018). Balancing environmental protection and economic development has become an urgent issue that must be resolved in all countries. Therefore, China has announced its dual carbon goals (Xi, 2020) and regards green credit policy (GCP) as an important measure to promote economic green transformation (Wen et al., 2021). Green credit has emerged as a fundamental instrument used by the global community to manage environmental pollution. GCP adjusts the flow of funds between “green” and “brown” enterprises by offering favorable interest rates or increased lending specifically for environmental protection initiatives, thereby fostering enterprise green transformation (EGT) (X. Xu & Li, 2020). Given the rapid progress of green credit applications, conducting a comprehensive study on the efficacy of green transformation among high-polluting enterprises (HPEs) within the confines of the GCP holds immense importance. This endeavor can contribute to uncovering strategies for attaining a global green and low-carbon economic transformation.

The essence of GCP lies in fulfilling the resource allocation role of the financial system and directing financial capital toward environmentally sustainable, low-carbon, and green innovation projects. However, for HPEs, the existing green financial policy system lacks incentive measures, serving more as an “environmental regulation” means to constrain their pollution emissions by reducing funding supply, forcing them to carry out pollution reduction and green transformation. After the policy’s implementation, Reghezza et al. (2022) observed a decline in bank loans extending to high-emissions industries, accompanied by an increase in associated loan interest rates. Chava (2014) points out that when enterprises encounter environmental issues, the credit funds provided by banks come with higher interest rates. Concurrently, HPEs frequently occupy a pivotal position in the national economy, and the successful execution of their green transformation has become the cornerstone of facilitating a smooth low-carbon transition throughout the economy. Hence, the green transformation of HPEs necessitates a reduction in carbon emissions and enhancement of their sustainable development capabilities. The essence of EGT revolves around transforming the existing production and operational framework, thereby attaining both environmental gains and economic prosperity for the enterprise while advancing the fundamental mandate of fostering the growth of the real economy (Ding et al., 2022; R. Li & Chen, 2022; Tian et al., 2022).

Studies suggest that GCP harms the financing costs and term structure of HPEs with substantial financial penalty effects. This influences the environmental, economic, and investment performance of enterprises through financing channels. Regarding environmental performance, Fan et al. (2021) discovered that, after the implementation of GCP, the pollution emissions of environmentally non-compliant enterprises decreased considerably, but the specific emission reduction methods varied by enterprise size. GCP has the potential to redirect capital flows away from energy-intensive and environmentally detrimental industries toward burgeoning and technology-forward sectors, thereby fostering the growth of green industries while concurrently curbing emissions from polluting industries (Tian et al., 2022). However, Bartram et al. (2022) observed that financial constraints can incentivize companies to shift their pollution-intensive production to other regions, leading to no overall improvement in environmental performance. Q. Xu and Kim (2022) also point out that, under the pressure of financing constraints, HPEs will weigh the cost of pollution control against environmental fines and choose to continue emitting toxic gases. Regarding economic performance, GCP has a certain degree of negative impact on enterprises’ production and operation (Yao et al., 2021), forcing enterprises to diversify their operations (R. Li & Chen, 2022), or it can temporarily improve enterprises’ economic performance, but it lacks a lasting or significant impact in the long run (Ding et al., 2022). Further, it has been recognized that GCP can stimulate green innovation within enterprises (Gao et al., 2022; G. Hu et al., 2021; Y. Lu et al., 2022; Z. Xu et al., 2023). However, whether GCP can promote an enterprise’s overall technological innovation and thus elicit the “Porter effect” remains unclear (Ding et al., 2022). In terms of investment decisions and promotion of the real economy’s development, GCP will restrain HPEs’ investments and reduce employment opportunities (Xue et al., 2023) but may also help enterprises focus on real economic sustainable development by reducing HPEs’ financialization (G. Hu et al., 2023). In summary, existing research remains controversial regarding how GCP affects corporate operations. More importantly, there is still vast research potential in comprehensively examining the impact of GCP on EGT from multiple dimensions such as environmental performance, economic outcomes, and investment decisions.

Accordingly, this study redefines “the green transformation of enterprises,” examining it through the lenses of environmental benefits, economic performance, and promoting the real economy. It uses carbon emission intensity, total factor productivity (TFP), and enterprise financialization as indicators to measure pollution reduction, productivity, and de-financialization and comprehensively examines the impact of green credit on the effectiveness of EGT. This study may contribute in the following ways: (1) Most literature examines the micro-level perspective of the impact of GCP on enterprises individually from a single dimension, such as environmental performance, productivity, technological innovation, investment, and financing. Few studies have addressed multiple dimensions of EGT, and they fall short of conducting a thorough examination of the interrelationships among various dimensions and the systematic identification of causal effects. This study comprehensively evaluates the effects of GCP from multiple critical dimensions, including pollution reduction, productivity, and de-financialization. Based on the pathway of “financing constraints–green innovation–overall R&D investment,” we explore whether HPEs exhibit an “extrusion effect” or a “Porter effect” during their green transformation process. Specifically, we examine whether economic performance is suppressed while enterprises improve environmental performance and reduce financialization levels, thereby investigating whether GCP creates a contradiction between emission reduction and sustainable development for enterprises. (2) Drawing on the nature of property rights, endogenous financing, regional location, and corporate social responsibility, we demonstrate the micro-mechanisms and heterogeneous effects of GCP from multiple perspectives. (3) We also explore the policy coordination effect between the level of green finance development and the intensity of environmental regulation in the regions where enterprises are located and GCP, further supporting and deepening the logical relationship between GCP and EGT.

By 2012, China’s carbon footprint had increased, constituting almost 30% of the global footprint (Y. J. Zhang & Da, 2015). China attaches great importance to promoting green transformation and development with green financial instruments. After many years of development, China has emerged as the world’s leading country in terms of green credit issuance (Y. Wang & Mao, 2022). Compared with other firms, A-share listed firms in China have greater influence and guidance and are more affected by GCP. Based on the above situation, we take green credit guidelines (GCGs) issued by the China Banking Regulatory Commission (CBRC) in 2012 as an exogenous policy shock and employ the difference-in-differences (DID) model to analyze the impact of GCP on the green transformation of Chinese A-share listed firms. The reason for adopting GCGs as an exogenous shock lies is that the GCGs promulgated in 2012 represent a significant milestone in China’s GCP framework. The period before and including 2011 marked the initial phase of China’s GCP, which transitioned into a systematic implementation stage only after the issuance of the GCGs. GCGs require banking financial institutions to determine reasonable credit authority and approval process according to the nature and severity of environmental and social risks faced by customers; customers whose environmental and social performance is not compliant shall not be granted credit. Moreover, the government has issued a series of supporting regulatory measures to ensure the smooth implementation of this policy, making it the most influential policy instrument within China’s green financial system (Gu & Qiao, 2024). Besides, the DID model can better evaluate the implementation effects of GCP and the causal relationship between these policies and EGT. Through the DID model, this study supports the “extrusion effect,” which provides important insights for policymakers, enterprises, and other stakeholders. Specifically, during the green transition process, special attention must be paid to the short-term trade-offs between emission reduction and sustainable development.

The rest of this study is organized as follows: Section “Literature Review and Theoretical Analysis” presents the literature review and research hypotheses; Section “Research Methodology” describes the research methodology and data selection; Section “Empirical Analyses” analyzes the empirical results, including benchmark regression, robustness tests, mechanism analysis, and extended analysis; Section “Conclusions and Recommendations” discusses the findings, concludes the paper, and proposes policy recommendations.

Literature Review and Theoretical Analysis

Definition and Measurement of EGT

EGT is a sustainable development paradigm in which enterprises prioritize resource-efficient utilization and environmental compatibility, focus on green innovation, and consistently adopt green production methodologies throughout the manufacturing cycle, thereby achieving a balance between economic and environmental performance. It fosters enhanced ecological environment quality along with robust societal development and economic growth (Y. Zhang, Li, & Xing, 2022). Research on EGT is predominantly centered on two primary dimensions: investigating the promotional or suppressive impact of diverse policies and factors on EGT, including environmental regulations (Shen et al., 2020; Zhai & An, 2020), digitalization (Y. Liu & Song, 2023; Miao & Zhao, 2023; J. Wang et al., 2023), carbon emissions trading pilot policies (Ge et al., 2023), and taxation systems (Su et al., 2023); and examining the models and value-creation pathways of EGT, including diversification management (R. Li & Chen, 2022) and mergers and acquisitions (Y. Zhang, Sun, et al., 2022). Few studies have conducted systematic analyses on how green credit affects EGT.

Simultaneously, the existing literature has proposed various measurement methods for EGT. First, the substitution method often employs green TFP (Niu et al., 2022) or the number of green enterprise patents (Y. Lu et al., 2022) as proxy indicators. Second, the comprehensive index method streamlines EGT measurements by constructing an evaluation framework with various indicators, assigning weights, and aggregating them to determine the overall EGT levels (L. He et al., 2021). Third, the text analysis method gauges EGT by selecting relevant keywords from corporate annual reports and calculating their frequencies using Python-based technologies (Wu & Lai, 2022). However, both the comprehensive index and text analysis methods have limitations. Weight determination in the comprehensive index method is relatively subjective. In the text analysis method, information about EGT may be biased or overstated in the preparation of annual reports, and keywords related to EGT may also be incomplete and biased. To comprehensively reflect the level of EGT, this study defines it from multiple dimensions based on its connotation. Accordingly, the literature review and theoretical analysis of this study will focus on the relationship between GCP and various dimensions of EGT, namely emission reduction and sustainable development. Among these, enterprise sustainable development is further divided into enterprise financialization and TFP.

The theoretical mechanism of the GCP in EGT is shown in Figure 1.

Theoretical framework of this study.

GCP and Emission Reduction of HPEs

According to classical externality theory, as a public good, the environment exhibits large externalities. The fundamental issue lies in the fact that polluting enterprises fail to adequately compensate for the negative externalities generated by their emission behaviors, resulting in private marginal costs being lower than social marginal costs. This problem cannot be resolved by the market itself, leading to a deviation of resource allocation from Pareto optimality (Fu et al., 2021; Hanna & Oliva, 2015; Q. Xu & Kim, 2022; Zivin & Neidell, 2012). Therefore, the key to improving enterprise pollution emissions is “internalizing external costs,” which means incorporating the growth of social marginal costs into the private marginal costs of enterprises. This can usually be achieved by clarifying property rights or performing external interventions. GCP is a financial innovation tool to alleviate environmental problems and is a rewarding policy for non-HPEs; however, for HPEs, it is a punishing policy similar to environmental regulations, which can achieve the effects of “internalizing external costs” and reducing emissions (X. Liu et al., 2019).

The GCP regulations exclude HPE from the catalog that support green innovation and environmental projects, thereby increasing their financing costs (X. Liu et al., 2019). HPEs are motivated to implement pollution control measures to alleviate their financing constraints. By implementing specific emission reduction plans, enterprises can increase the loans or preferential loan interest rates they receive from banks. From an “internal governance” perspective, good emissions reduction performance helps enterprises consolidate their brand status and obtain commercial credit financing more easily. In addition, enterprises’ active emission reduction activities are conducive to gaining competitive advantages, helping enterprises obtain more government subsidies and external investment (Nguyen et al., 2021). From an “external supervision” perspective, enterprise emission reduction behavior can mitigate information asymmetry, highlight the correct business philosophy of enterprises, and alleviate financing constraints. Moreover, external supervision can pass enterprise information to capital markets through rating agencies, analysts, and other information channels (N. Li et al., 2021; H. Liu et al., 2024), making it easier for them to obtain financing or investment and alleviate financial pressures. It is evident that GCP tightly couples the environmental expenses incurred by an enterprise’s pollution discharge with its financing costs, compelling HPEs to scrutinize their societal and environmental obligations and encouraging them to proactively integrate environmental considerations into the constraints that guide their production functions.

Green innovation serves as a crucial tool for GCP to advance pollution-reduction efforts and foster EGT (Cai et al., 2020). Green innovation empowers enterprises to conserve energy and reduce emissions. According to externality theory, green innovation possesses the same favorable externality of knowledge spillover as traditional innovation while also exhibiting a positive environmental spillover externality. However, limited private marginal benefits coupled with the substantial investment costs and risks may result in insufficient motivation for enterprises to embark on green innovation initiatives (Chen et al., 2023). Under the punishment mechanism of GCP, HPEs may actively implement green innovation and improve pollution reduction effectiveness to mitigate their financing constraints (F. Liu et al., 2024).

Hence, we propose the following hypothesis:

GCP and Sustainable Development of HPEs

We define “sustainable development” for enterprises as the enhancement of their productivity while simultaneously fostering the growth and advancement of the real economy. For this purpose, two indicators—TFP and enterprise financialization—were used to measure the sustainable development of HPEs.

Regarding the shift of enterprises from the virtual economy to the real economy in recent years, in an environment where the return on net assets in China’s real economy falls below that of financial investments, a considerable number of enterprises have sought to attain short-term profitability goals by directing their capital toward sectors such as finance and real estate. These investments do not favorably contribute to the growth of the real economy (Davis, 2017; Díez-Esteban et al., 2016; Jin et al., 2022). External credit is the primary source of funding for enterprises investing in financial ventures (Kliman & Williams, 2015; X. Xu & Xuan, 2021). Hence, as the financing pressure on enterprises intensifies, liquidity scarcity acts as a constraint, hindering the extent of their financialization. Given that most Chinese enterprises rely on indirect financing, GCP has increased their financing costs and required them to bear more environmental responsibilities (X. Liu et al., 2019; D. Zhang et al., 2019; M. Zhang et al., 2022). These requirements discourage short-term speculative returns, which can negatively impact the financialization level of HPEs. Therefore, we postulated the following hypothesis:

Economic growth theory underscores technological progress as the driving force behind its enhancement. Therefore, advancements in TFP reflect enterprises’ contribution to economic growth. Technological innovation requires substantial and stable investment in R&D; therefore, whether TFP can be improved depends on whether enterprises can ensure sufficient investment in R&D. Based on neoclassical economics, under the constraints of GCP, the financing cost of HPEs increases. HPEs also need to dedicate greater resources to pollution control endeavors, potentially leading to the displacement of R&D investment originally intended for their core business domains (Petroni et al., 2019). Given the decline in overall R&D investment by enterprises, there will inevitably be an “extrusion effect” on overall technological innovation, thus suppressing TFP. First, GCP for HPEs is equivalent to an environmental regulation measure, leading to a decrease in enterprise funding availability. This prompts enterprises to adjust their investment budgets and reduce their overall R&D investment. Second, GCP urges enterprises to prioritize environmental performance, amplify investment in green innovation and pollution control, and lower investment in other areas. This also means that the reduction in enterprises’ financialization levels stems primarily from tightened financing constraints rather than from the voluntary allocation of more funds to the real economy.

Unlike previous studies, research based on the “Porter effect” posits that the connection between environmental protection and innovative development is not one of mutual exclusivity but rather a push-pull relationship (Porter & van der Linde, 1995). GCP promotes intensive production processes, reduces excess capacity, guides enterprises’ R&D innovation, and ultimately enhances TFP. In addition, GCP improves the environmental performance of enterprises, which can increase market competitiveness (Pástor et al., 2022). This, in turn, facilitates access to financing from banks, capital markets, and governments, thereby providing ample financial support for R&D endeavors and further productivity gains. If GCP suppresses the financialization of enterprises and enhances TFP in HPEs, it implies that GCP is conducive to enterprises focusing on the sustainable development of the real economy. Thus, a clear controversy exists in the existing literature regarding whether GCP has an “extrusion effect” or a “Porter effect.” Hence, we posit the following two competing hypotheses:

Research Methodology

Model Specification and Identification Strategy

Given the important position of the GCGs in China’s GCP system, this study considers the GCGs as an exogenous shock event for implementing the GCP. We ascertained the causal influence of GCP on the green transformation of HPEs using a fixed-effects DID model. The DID model is an econometric method used for policy evaluation and causal inference, which estimates the net effect of a policy by comparing the differences between the treatment group and the control group before and after policy implementation. Its core principle relies on eliminating time trends and inter-group differences through double differencing, with the key assumption that the treatment and control groups must satisfy the parallel-trends condition. Within the framework of DID estimation, this study classifies non-HPEs as the control group and HPEs as the experimental group, based on the varying degrees of green credit restrictions imposed on diverse industries following the implementation of GCGs.

According to the previous analysis, we examined the effects of GCP on the green transformation of HPEs in three dimensions: emission reduction benefits, economic performance, and promotion of the real economy. The baseline model is established as follows:

In this study, i represents the enterprise, and t represents the year. The explanatory variable Gtranit represents the three dimensions of EGT: pollution intensity, TFP, and financialization level. xit signifies the collection of control variables at the enterprise level. ϕt is a time-trend term that replaces Postt to comprehensively control possible increasing or decreasing trends that may exist but have not been fully covered by xit and γi. γi represents an individual fixed effect that replaces Treati to comprehensively control for the impact of unobservable individual-level characteristics on the explanatory variables. εit is a random disturbance term. The coefficient β1 reflects the net effect of the implementation of GCP on HPEs’ EGT. A negative coefficient indicates that GCP has promoted the emission reduction effectiveness and de-idealization of HPEs but suppressed their TFP, with a negative impact on their transformation and development. A positive coefficient indicates the opposite situation.

In the benchmark regression, the coefficient estimation conducted cluster adjustments for individual entities to acknowledge the potential for temporal convergence among identical enterprise characteristic factors. Further, to mitigate the effects of macroeconomic system factors operating at the regional and industrial levels, this study meticulously controls for city and industry-fixed effects during robustness assessments and additionally provides coefficient estimates with cluster-robust standard errors tailored to the year–city–industry combination.

Data Source

Given the issuance of GCGs in 2012 and the aim of conducting a more precise analysis of the influence of implementing GCP on EGT, this study adopts a sample of Chinese A-share listed firms from 2007 to 2021. In 2021, the Chinese government incorporated the “dual carbon” goals into the national 14th Five-Year Plan and successively issued policies such as the “Guidance on Fully, Accurately, and Comprehensively Implementing the New Development Philosophy to Achieve Carbon Peak and Carbon Neutrality” and the “Action Plan for Carbon Peak Before 2030.” Since then, implementation plans for green transformation in key sectors and industries such as energy, industry, construction, and transportation have been released sequentially. The green transformation environment for Chinese enterprises has undergone major changes after 2021. To ensure the validity of the DID model’s causal identification, this study did not include samples after 2021. Further, the samples are screened by excluding financial insurance firms, those with abnormal trading statuses (e.g., ST, ST*, and PT), and those with incomplete data.

The data were categorized into four main sources: enterprise characteristics and financials from the China Stock Market & Accounting Research database, innovation data from the China National Research and Development Survey, regional financial and environmental regulation data from authoritative institutions (NBS, PBC, CESY, and CFY), and pollution discharge data manually compiled from corporate reports and disclosures. This study aligns the categorized numerical data on invention and utility model patents held by A-share listed companies with the “International Patent Classification Green List” promulgated by the WIPO in 2010, specifically identifying and extracting green patent information belonging to these listed enterprises. After matching all of the above data, 21,839 enterprise-year observations were obtained. To maintain the robustness of the data analysis, this study applies a 1% winsorization treatment to the tails of significant continuous variables and transforms certain variables by taking their natural logarithms.

Variable Measurements

Dependent Variables

Regarding the explanatory variable, from the essence of EGT and existing research results, we decompose the development of EGT into three dimensions: pollution discharge, TFP, and the promotion of the real economy.

Pollution discharge. Based on the standards established by the internationally accepted Greenhouse Gas Protocol, we measure the proportion of a company’s carbon emissions to its overall market value (lnctotalratio). A company’s carbon emissions encompass four categories: combustion and fugitive emissions, emissions arising from production processes, waste-related emissions, and emissions stemming from land-use alterations. In addition, in robustness testing, we further focused on the company’s production process emissions and end-of-pipe waste emissions.

TFP

Referring to Dong et al. (2025) and Xiong et al. (2025), this study employs the Levinsohn-Petrin and Olley-Pakes methods to measure TFP, defined as TFP_LP and TFP_OP, respectively, for benchmark regression and robustness tests.

Financialization

The definition of enterprise financialization allows for two ways to measure a company’s involvement in financial investment activities: First, enterprises with higher levels of financialization tend to hold a larger proportion of their financial assets (Demir, 2009). Second, a large portion of enterprises’ overall profits originate from financial investments (Song et al., 2024). Based on these definitions, we use the following two measures to assess enterprise financialization, which are used for benchmark regression and robustness testing, respectively.

Independent Variable

The core independent variable is Treati*Postt, where Treati represents the virtual variable that identifies the experimental group, assigning the value 1 to HPEs and 0 to others; Postt represents the dummy variable for the implementation of GCP, assigning the value 1 before 2012 and 0 after 2012. For the division of enterprise samples, we refer to GCGs and the Environmental Protection Verification Industry Classification Management List of Listed Companies issued by the Ministry of Environmental Protection of China in 2008. Companies operating in industries such as coal, steel, and so on are classified as HPEs, whereas all other enterprises are categorized as non-HPEs.

Control Variables

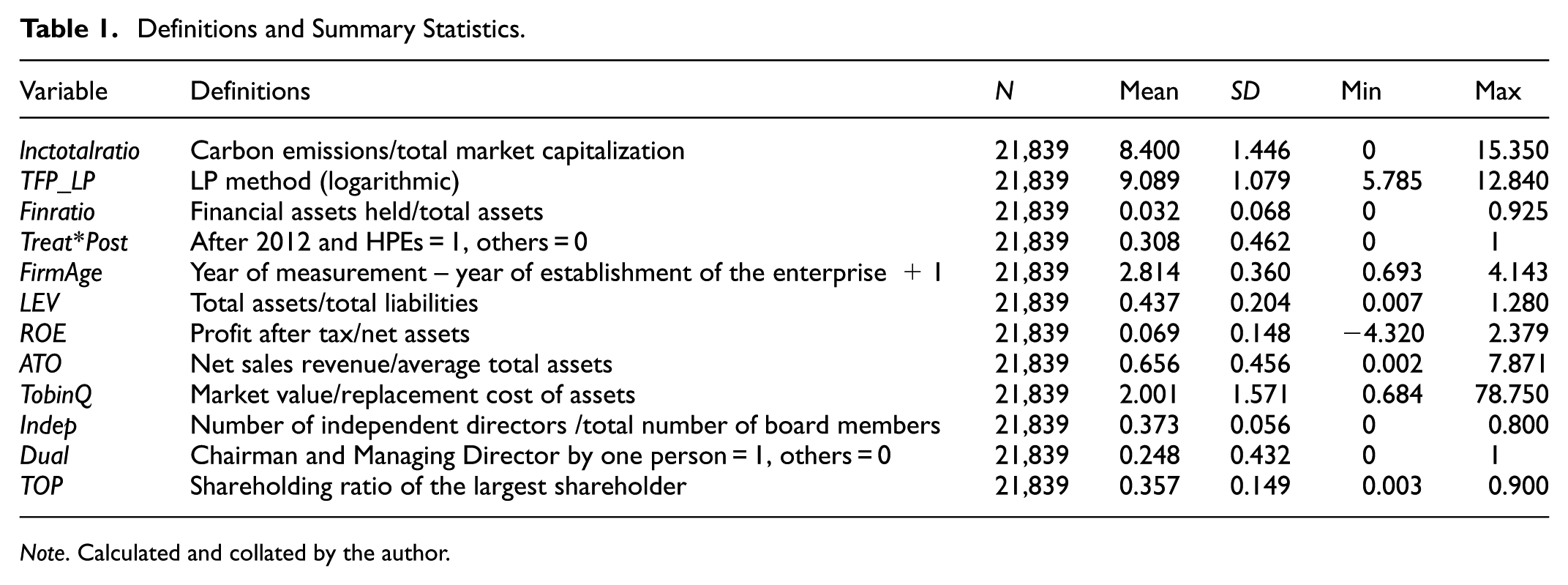

Regarding the control variables, we focused on corporate finance and governance characteristics, as identified in prior research, which potentially impact the process of green transformation. By adding these control variables, the potential influence of other factors on the test results can be somewhat reduced. The specific variables are FirmAge, LEV, ROE, ATO, TobinQ, Indep, Dual, and TOP. Table 1 presents the definitions and descriptive statistics of these variables. The average value of lnctotalratio is 8.400 with a standard deviation of 1.446; the mean of TFP_LP is 9.089 with a standard deviation of 1.079; the mean of Finratio is 0.032 with a standard deviation of 0.068, indicating that all variables exhibit certain fluctuations. The average value of the core explanatory variable is 0.308, indicating that the experimental group accounts for 30.80% of the total sample. The values of other control variables are consistent with previous studies.

Definitions and Summary Statistics.

Note. Calculated and collated by the author.

Empirical Analyses

Benchmark Regression

Table 2 displays the outcomes derived from Model (1), with the explanatory variables organized as follows: pollution emission intensity in columns (1) and (2); TFP in columns (3) and (4); and financialization in columns (5) and (6). Columns (1), (3), and (5) exclude the control variables, and all regression equations account for firm and year-fixed effects.

Benchmark Regression Results.

, and *** represent the 10%, and 1% significance levels, respectively; all regressions are robustly clustered by enterprise.

Table 2 reveals that all coefficients of the key explanatory variables exhibit statistical significance at the 1% level, with negative values. The inclusion of control variables has little effect on the coefficients. These benchmark regression findings suggest that, after the enforcement of the GCP, HPEs significantly outperformed non-HPEs in terms of enhancing their emissions reduction efficiency. However, their level of financialization has undergone a decline, and their TFPs have been subject to restraint. This means that the implementation of the GCP through credit channels has imposed substantial constraints on the environmental governance, investment decisions, and economic performance of HPEs. Constrained by GCP, HPEs prioritize environmental stewardship and social responsibility, proactively engaging in emission reduction efforts to mitigate their pollution output.

Further, from a sustainable development standpoint, GCP has dual implications: it fosters a decrease in the financialization of HPEs, facilitating “de-virtualization and realization”; concurrently, it exerts a certain negative influence on the TFP of these enterprises.

This may imply that the “de-virtualization” generated by GCP mostly stems from policy exacerbating the financing constraints faced by HPEs, leading to a lack of resources for investing in the virtual economy rather than substantially increasing investment in the real economy. Moreover, the constraints imposed by the GCP may incentivize HPEs to allocate more of their resources to green innovations focused on emission reduction, which in turn may lead to a diversion of overall R&D investments, ultimately resulting in a decline in their TFP. Whether through any of the aforementioned impact mechanisms, this implies that under the current constraints of the GCP, there exists a certain contradiction between low-carbon emission reduction and sustainable development for HPEs.

Robustness Tests

Parallel-Trend Tests

Satisfying the parallel-trend hypothesis is crucial for effectively employing the DID model. To test this hypothesis and examine dynamic policy effects, this study adopts the event study methodology (Borusyak et al., 2021; Rambachan & Roth, 2023). This study requires that before and after the implementation of the GCP, the differences in pollution emission intensity, TFP, and financialization degree between HPEs and non-HPEs become significant and insignificant. First, if the differences in each explained variable between the two types of enterprises are already significant before the implementation of the GCP, HPEs have learned about the policy’s implementation and its potential impact in advance, thus adjusting their investment and operational decisions ahead of time. This may change the enterprise’s pollution emission intensity, TFP, and degree of financialization, leading to biased estimation results from the DID model. Second, if the differences in each explained variable between the two types of enterprises become significant after the implementation of the GCP, it demonstrates that the policy has a significantly different impact on HPEs than on non-HPEs. To specifically analyze the hypothesis and policy dynamic effects, we construct the following econometric model:

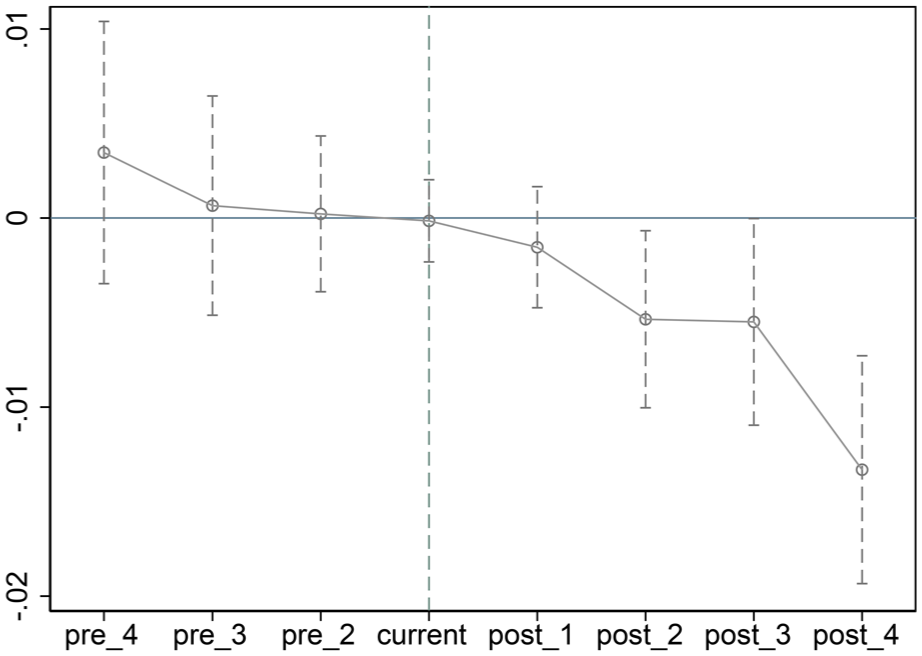

Timek is a temporal virtual variable that takes the value 1 when the sample corresponds to year K and 0 otherwise; all other terms retain their original meanings, as defined in Equation (1). Moreover, to avoid multicollinearity, we set the reference period as 2011 (i.e., K = −1). The parallel-trend hypothesis test and policy dynamic effect analysis are illustrated in Figures 2 to 4, respectively, through the utilization of lnctotalratio, TFP_LP, and Finratio as explanatory variables.

Parallel trend test (lnctotalratio).

Parallel trend test (TFP_LP).

Parallel trend test (Finratio).

The figures show that the coefficients and significance of the interaction terms βk in Equation (4) fluctuate. Before 2012, the interaction coefficients of the three explanatory variables were not significant. This means that there was no change in the differences in pollution emission intensity, TFP, or degree of financialization between non-HPEs and HPEs before the implementation of the GCP, validating the parallel-trend hypothesis. This also indicates that enterprises had not begun adjusting their green transition strategies before the implementation of the policy. Concurrently, after 2012, the interaction coefficients for all three explanatory variables decreased annually and changed from non-significant to significant. This signifies that, after the enforcement of the GCP, HPEs’ pollution emission intensity, TFP, and degree of financialization decreased more than in non-HPEs. Interestingly, these policy effects exhibit a certain time lag and gradual increase.

Placebo Tests

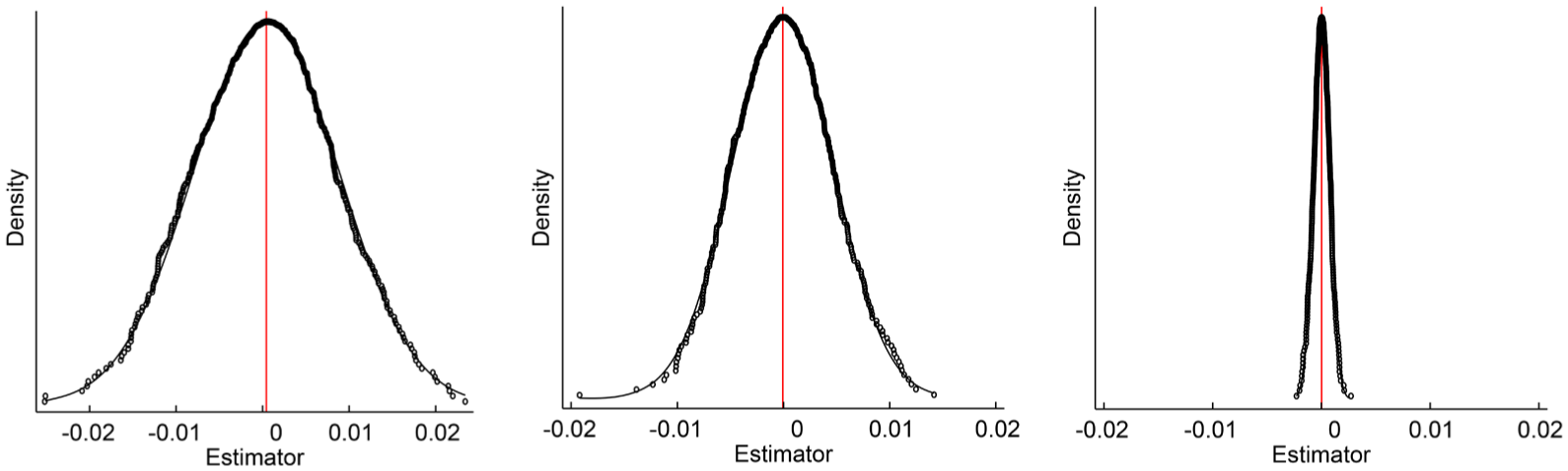

This study continued to conduct placebo tests by randomly selecting experimental group samples to prevent the confounding effects of unobservable factors that are synchronous with GCP (Sun, 2025). We randomly select enterprises within the sample, creating both a random experimental and a control group guided by the number of experimental groups defined in the benchmark regression. Additionally, we randomly determined the year of policy implementation to reevaluate the coefficients associated with the core explanatory variables (Q. Lu et al., 2024). In the placebo test, the core explanatory variables were randomly generated; thus, their influence on the explanatory variables did not yield statistically significant results. Figure 5 shows the distribution of coefficient estimates when lnctotalratio, TFP_LP, and Finratio were used as explanatory variables after repeating the above process 500 times.

Placebo tests.

This figure shows that the mean of the coefficients is concentrated around zero, which is consistent with the predictions of the placebo tests. When lnctotalratio, TFP_LP, and Finratio serve as explanatory variables, the benchmark regression yields estimated coefficients of −0.090, −0.070, and −0.009 for their respective interaction terms. Figure 5 illustrates that these estimated coefficients align with a low-probability event, suggesting that the benchmark regression outcomes are not attributable to unobservable extraneous factors. This finding reinforces the validity of the conclusions drawn in this study.

Alternative Measurement of Explained Variables

To evaluate EGT in the benchmark regression, this study adopts three key metrics: the total carbon emissions to total market value ratio for pollution intensity, TFP measured through the LP method for economic performance, and the proportion of financial assets to total assets for the financialization level. To further verify the robustness of the previous results, this study focuses on the generation process emissions (lnproduce_c) and end-of-pipe waste emissions (lnend_c), encompassing solid waste incineration emissions and sewage treatment-related emissions, uses the OP method to measure the TFP (TFP_OP), and employs the ratio of financial investment returns to total profits (Finratio2) as a metric to quantify the financialization level of enterprises. As presented in Table 3, altering the measurement approach for the explained variables did not significantly influence the regression outcomes. The GCP still promotes enterprise emission reduction effectiveness, reduces the degree of financialization, and suppresses TFP. An intriguing observation from columns (1) and (2) of Table 3 is that, compared with generation process pollution control, enterprise pollution emission reduction is more focused on end-of-pipe treatment. This means that enterprise emission reduction behavior may be more inclined to “cater” to policy requirements to quickly alleviate policy pressure.

Robustness Tests: Alternative Measurement of Explained Variables.

, **, and *** represent 10%, 5%, and 1% significance levels, respectively; all regressions are robustly clustered to enterprises.

Consideration of Model Self-Selection Problems

Enterprises could become highly polluting or non-highly polluting firms because of certain inherent characteristics, leading to sample self-selection issues. To validate the accuracy of identifying the policy impacts presented in this study, a PSM-DID approach was used to regress the model (Yang et al., 2020).

First, all control variables are utilized as covariates for the sample-matching process, employing logit regression to estimate the likelihood of an enterprise qualifying as an HPE. Second, a nearest-neighbor matching approach was applied to pair the most comparable enterprises between HPEs and non-HPEs, ensuring that no statistically significant disparities existed between the two groups in terms of covariates. Finally, the DID method was used to estimate the net effect of GCP on fostering green transformation within enterprises. Table 4 presents the results of the balance hypothesis test, which indicates that the average values of the various covariates across the two groups were approximately equivalent. The standard deviations were generally less than 3. Additionally, after the matching process, the disparities in the covariates between the two groups diminished, rendering them insignificant. Columns (1)–(3) of Table 5 present the PSM-DID regression outcomes, which align with the benchmark regression findings and affirm the robustness of the analysis.

Robustness Tests: Balanced Hypothesis Testing.

Robustness Tests: PSM-DID.

, and *** represent the 10%, and 1% significance levels, respectively; all regressions are robustly clustered by enterprise.

Exclusion of Other Policy Effects

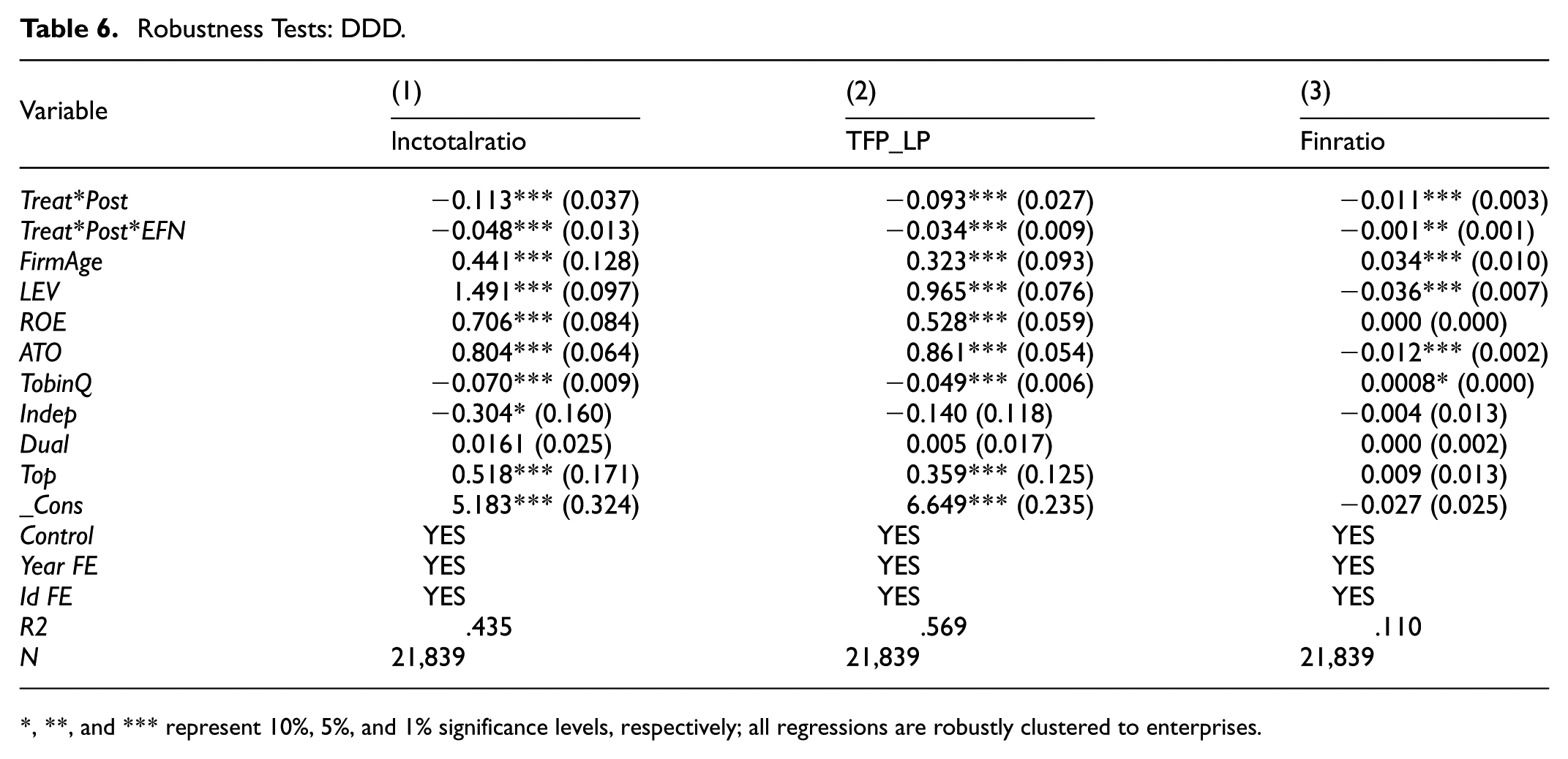

During the research period, the Chinese government promulgated environmental regulation policies that may have impacted EGT. To further exclude other factors that could potentially disrupt the accuracy of the estimation outcomes, this study uses a triple-difference estimator (DDD or TD) and constructs a third-level difference based on the differences in the roles of GCP and other disruptive policies. We consider enterprises’ external financing needs (EFN) as the third-level difference (Durnev & Kim, 2005). The reason is that the higher the external financing needs of an enterprise, the greater its impact from GCP; however, the strength of an enterprise’s external financing needs is not influenced by the impact of environmental regulation policies.

External financing demand is measured as the difference between the growth in capital demand and increased retained earnings. Enterprises are grouped into high and low levels of external financing needs and introduced into the benchmark regression model in the form of cross-items. Table 6 showcases the regression outcomes, revealing that for the explanatory variables encompassing pollution emission intensity, TFP, and the financialization level of enterprises, the coefficient associated with the interaction term between the core explanatory variable in the benchmark regression and EFN is negative. This finding aligns with the benchmark regression results, suggesting robust confirmation of the previous findings.

Robustness Tests: DDD.

, **, and *** represent 10%, 5%, and 1% significance levels, respectively; all regressions are robustly clustered to enterprises.

Controlling the Effect of Systemic Factors

Given the nationwide implementation of GCP, local governments and related industries may also introduce corresponding policies to support green transformation. To exclude the impact of time-variant macro-system factors at regional levels and characteristic factors at industry levels on the estimation outcomes, we further extend the benchmark regression by incorporating city and industry-fixed effects. The detailed regression outcomes are presented in Table 7, which demonstrates that the coefficients of the core explanatory variables remain consistent with those observed in the benchmark regression. In addition, the regression R2 after controlling the systemic factors improves significantly, reflecting an increase in the interpretability of the model.

Robustness Tests: Controlling the Effect of Systemic Factors.

, and *** represent the 5%, and 1% significance levels, respectively; all regressions are robustly clustered by enterprise.

Mechanism Analysis

Based on the above analysis, it is found that the GCP can not only effectively promote enterprise emission reduction and mitigate financialization but also suppress TFP. Under policy constraints, the green transition of enterprises faces a contradiction between low carbon emission reduction and sustainable development. To help enterprises solve this contradiction and assist them in a smooth transition, it is necessary to further explore how GCP produces the micro-transformation effects mentioned above. Inspired by relevant studies, GCP can enhance enterprise emission reductions through green innovation (Y. Zhang et al., 2020). Nonetheless, financial constraints may lead to the displacement of R&D investment in other areas through emission reduction innovation (Yu et al., 2021), thus negatively impacting TFP (G. He et al., 2020). Therefore, the virtual-real transformation brought about by green credit is a helpless move for enterprises under financing constraints rather than a substantial transformation to the real economy.

The mechanism analysis in this study did not adopt a traditional three-step model. As Jiang (2022) pointed out, the three-step mediation effect test is overused and biased. A more appropriate method involves proposing one or several mediating variables, denoted as M (e.g., green innovation, financing constraints, and R&D investment in this context), which can elucidate the channels through which GCP affects EGT based on economic theory. Since the impact of M on EGT has been confirmed by theory and research, the focus of regression modeling in our mechanism analysis was to examine the causal relationship between GCP and the mediating variable M.

First, we analyze the mechanism of enterprise emissions reduction under GCP constraints. GCP compels enterprises to embark on green innovation by increasing their financing constraints (Y. Lu et al., 2022). To quantify the total extent of green innovation (GP), the number of green invention patent applications (GP1) and green utility model patent applications (GP2) were aggregated (Kong et al., 2021; J. Liu et al., 2022). To address the issue of right-skewed distribution in green patent application data, this study applies the natural logarithm of the green patent application count plus one, resulting in LnGP, LnGP1, and LnGP2. In Table 8, columns (1)–(4), verifies that GCP intensifies enterprise financing constraints while concurrently spurring green innovation. This incentivizing effect motivates enterprises to enhance both the quality and quantity of their green innovations, which subsequently manifests in improved emission reduction outcomes, thus confirming Hypothesis 1.

Mechanism Analysis.

, **, and *** represent the 10%, 5%, and 1% significance levels, respectively; all regressions are robustly clustered by the enterprise.

Second, we analyzed the decision-making mechanism of sustainable enterprise development under the constraints of GCP. According to the benchmark regression results, GCP reduces the degree of enterprise financialization but suppresses TFP. If enterprises truly achieve definancing in the virtual economy, they will benefit by concentrating their resources on operations and reducing investments in the virtual economy. However, it is also possible that, after facing stronger financing constraints, enterprises’ available resources may further shrink, forcing them to reduce investment in the virtual economy. As columns (1) and (5) of Table 7 show, while GCP increases enterprise financing constraints, it crowds out enterprise R&D investment. Considering Table 8, columns (2)–(4), under stronger financing constraints, enterprises must invest limited resources in green innovation and attempt to mitigate long-term financing constraints by improving the effectiveness of emissions reduction. Therefore, under the constraints of GCP, enterprises do not make substantial transformations toward the real economy; rather, they have no more resources to invest in the virtual economy. Enterprises must use their limited resources for green innovation and inevitably crowd out overall R&D investment and total innovation, negatively affecting TFP. This confirms Hypotheses 2 and 3b. This result presents the internal decision-making process of HPEs under the pressure of GCP: policy constraint, financing pressure, resource redistribution, green innovation consuming overall R&D investment, total innovation decreasing, and damaged TFP, thus supporting the “extrusion effect” rather than the “Porter effect.” This logical chain emphasizes that the short-term compliance behavior of enterprises may lead to long-term productivity loss.

Expanded Analyses

According to the benchmark regression and mechanism analysis, GCP can affect green innovation and overall R&D investment through financing constraints, which in turn affects the effectiveness of EGT. This study further verifies the above logic from two perspectives: heterogeneity and coordination effect analyses.

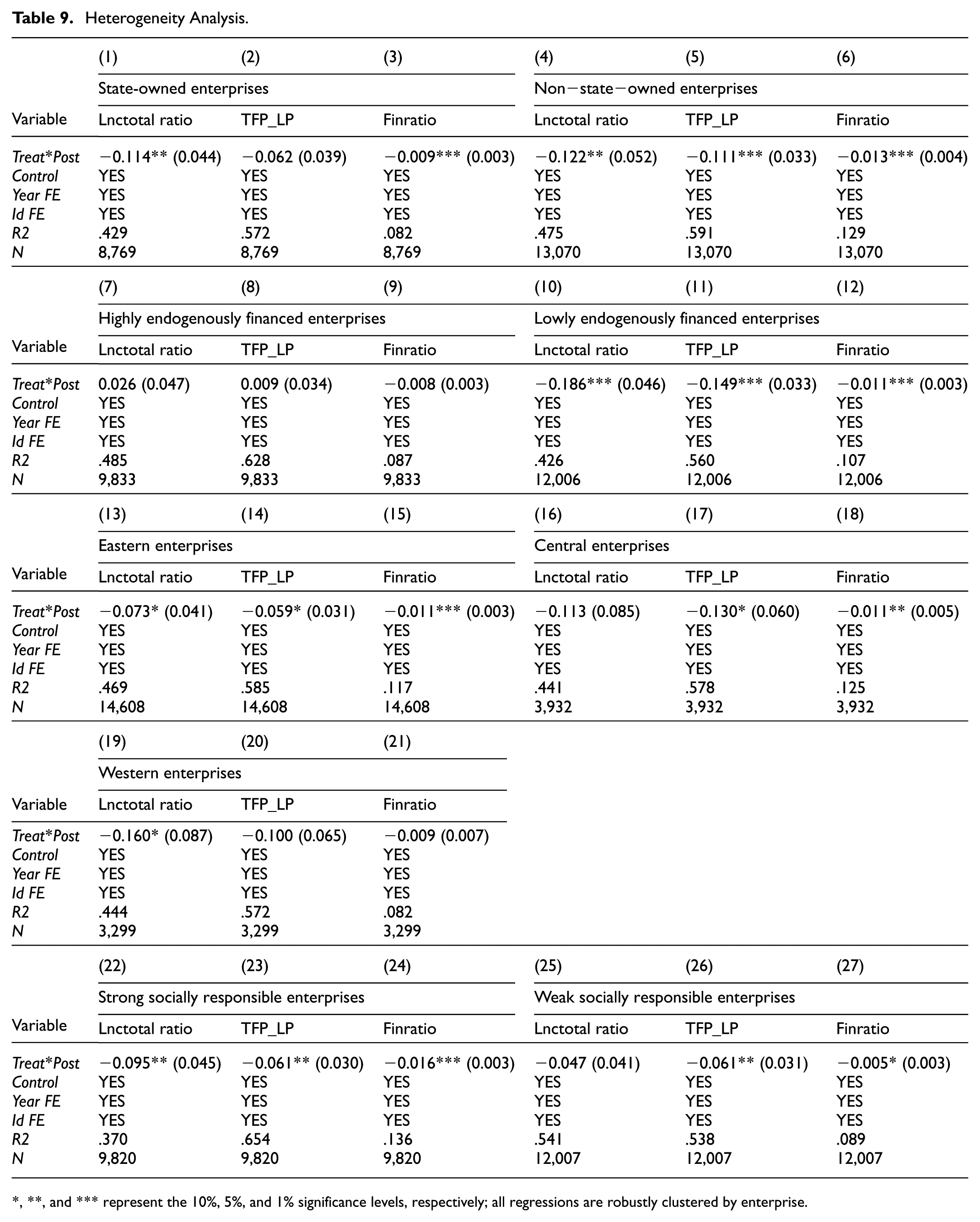

Heterogeneity Analysis

Because of implicit guarantees and alternative financing, different enterprises face different levels of financing constraints and varying degrees of influence that GCP exerts on the green transformation of HPEs compared with non-HPEs. Moreover, because of differences in enterprise awareness of environmental governance and social responsibility, even under the same financing constraints, the degree of crowding out green innovation by R&D investment may vary among different types of enterprises, thus affecting the effectiveness of their green transformation. Considering this, we conducted a heterogeneity analysis of the relationship between GCP and EGT from aspects such as the nature of property rights, endogenous financing levels, location, and corporate social responsibility.

Nature of Property Rights

State-owned enterprises have an advantage in implicit guarantees; therefore, debt financing is only one of their numerous financing channels. Forecasts indicate that GCP exerts minimal influence on the financing costs incurred by highly polluting state-owned enterprises, thus showing different innovation behaviors, investment decisions, and green transformation effects from those of non-state-owned HPEs (Wen et al., 2021). This study conducted a heterogeneity analysis of GCP effectiveness by introducing an interaction term between corporate ownership (SOE) and the core explanatory variable in the benchmark regression. Table 9, columns (1)–(6), displays the detailed regression outcomes, with SOE serving as a dummy variable to designate the ownership status of the enterprise. The value 1 signifies that the sample is state-owned, and the value 0 indicates otherwise. The table shows that, within the confines of the GCP, no disparity exists in emission reduction effectiveness or the degree of financialization between the two types of enterprises. However, there are pronounced differences in TFP, implying that both types of enterprises are influenced by the financing constraints imposed by the GCP, thereby incentivizing them to pursue emissions transformation efforts. Nevertheless, owing to differences in other financing constraints across these two types of enterprises, GCP pressure does not significantly affect the TFP of state-owned enterprises.

Heterogeneity Analysis.

, **, and *** represent the 10%, 5%, and 1% significance levels, respectively; all regressions are robustly clustered by enterprise.

Endogenous Financing

Debt financing is only one of many financing channels for enterprises; therefore, the reduction in bank loans and increase in loan costs caused by GCP are not necessarily conducive to increasing financing difficulties for enterprises. Internal financing of enterprises themselves is an important alternative financing solution for HPEs under credit restrictions. It can be predicted that higher internal financing will lead to a lower impact of GCP on HPEs, with less impact on their emission reduction efficiency, financialization level, and TFP. We quantified the extent of alternative financing by employing the ratio of total profit to main business income as a metric (Huang & Ritter, 2021).

As demonstrated in Table 9, columns (7)–(12), the regression coefficients for the total ratio, TFP_LP, and Finratio are significant only for enterprises with low internal financing, suggesting that GCP exerts its influence specifically on the emissions reduction efficiency, financialization level, and TFP of these enterprises with limited internal funding. For enterprises with high internal financing, GCP has no substantial effect on their financing constraints and does not provide sufficient incentives to reduce pollution under loose financing conditions. Owing to their ample funds, the financialization level and TFP of enterprises with high internal financing are not affected by GCP. This means that a single GCP is not sufficient to stimulate emission reduction efforts among enterprises with high internal financing, and other financing policies must be adopted to motivate them.

Location

Based on the varying economic and social developments across China’s regions, the nation has been categorized into three distinct economic zones. These zones exhibit disparities in their levels of marketization, financial environments, and natural resource endowments, potentially contributing to regional variations in the relationship between GCP and EGT. The empirical findings, presented in columns (13)–(21) of Table 9, indicate that the influence of GCP on enterprises’ emission reduction effectiveness, financialization level, and TFP is most pronounced in the eastern region, with the western region experiencing the least impact and the central region falling in between. There are two possible reasons for this: First, most of the eastern region is economically developed and densely populated; thus, the implementation of GCP is stricter, leading to a greater policy impact. Second, the central and western regions have abundant natural resources, but enterprises’ adverse use of resources is more serious, resulting in insufficient motivation for green transformation, leading to less feedback from enterprise behavior on policies.

Corporate Social Responsibility

The strength of corporate social responsibility reflects enterprises’ execution of sustainable development. Under the same policy constraints, enterprises with stronger social responsibility are more likely to make efforts toward pollution control and green transformation. Hence, this study undertakes a heterogeneity analysis to explore the varying strengths of corporate social responsibility; detailed regression outcomes are presented in Table 9, columns (22)–(27). Under the influence of GCP, the differences in green transformation between these two types of enterprises lie mainly in their emission reduction effectiveness. This may be due to two reasons: First, enterprises that demonstrate strong social responsibility are more readily acknowledged by others, thereby imposing a stricter social responsibility constraint upon them. This recognition encourages enterprises to continue to fulfill their environmental and social obligations. This intangible “constraint” serves as a catalyst, motivating enterprises to engage in green innovation and pursue low carbon emission reduction efforts. Second, when enterprises undertake social responsibility, they are more likely to attract attention from external organizations such as environmental protection groups, which helps promote information sharing. Enterprises can make full use of external information to compensate for their internal knowledge shortages, provide support for green innovation, and promote emissions reduction.

Analysis of Environmental Coordination Effects

This study examines the influence of various enterprise characteristics on the interplay between GCP and EGT. Apart from enterprise characteristics, external factors, including the degree of green finance development and the stringency of environmental regulations, can form a coordinated effect with GCP, thereby adjusting the effect of GCP on EGT.

Coordinated Effect of Green Financial Development

The level of green finance development can alleviate the financing pressure exerted by GCP on HPEs to a certain extent, thereby reducing the TFP loss under GCP pressure. To examine the synergistic effect between the level of green financial development and GCP, this study initially established an index system to measure the level of green financial development across various cities. This index was measured using the entropy value method, and its comprehensive evaluation system included the development levels of green credit, investment, insurance, bonds, support, funds, and equity. To ensure data comparability between cities at all levels, green financial development indicators were standardized. Subsequently, the benchmark regression model incorporates an interaction term that captures the interplay between an enterprise’s green financial development level and its core explanatory variable. Table 10, columns (1) to (3), presents the regression results.

Analysis of Environmental Coordination Effects.

, **, and *** represent the 10%, 5%, and 1% significance levels, respectively; all regressions are robustly clustered by enterprise.

According to the regression results, the level of green financial development alleviates the detrimental effects of GCP on enterprises’ TFP, exacerbates their financialization, and reduces the pollution reduction effect. A robust level of green financial development can help enterprises secure more external funding, thereby mitigating the financing constraints imposed by the GCP and potentially diminishing enterprises’ incentives to engage in pollution reduction efforts. This means that promoting substantial green transformation requires synergy between GCP and the level of financial development to effectively guide enterprises.

Coordinated Effect of Environmental Regulation

Environ-mental regulation also has coordinated effect. In contrast to the level of green financial development, environmental regulations further strengthen the binding pressure of GCP on HPEs. To test the coordinated effect of environmental regulation intensity and GCP, this study first measured the environmental regulation intensity in each region using the ratio of investment in wastewater and exhaust gas treatment projects completed by the enterprise’s location to industrial added value. The benchmark regression model incorporates an interaction term that captures the interplay between the intensity of environmental regulations and the core explanatory variable. Table 10, columns (4) to (6), reports the corresponding regression results.

Environmental regulation intensity contributes to promoting pollution reduction effects and reducing financialization levels but exacerbates the negative impact of GCP on TFP. Strict environmental regulations increase expenditures for HPEs in terms of environmental protection taxes, and pollution penalties intensify the financing constraints for enterprises. This leads to further crowding out R&D investments and the suppression of TFP from pollution reduction. This means that environmental regulation policies have a strong synergy with GCP and exacerbate the contradiction between emission reduction and the development of HPEs.

Conclusions and Recommendations

Discussion and Conclusions

Using Chinese A-share listed firms as the sample, this study examines the GCGs issued by the CBRC in February 2012 as an exogenous shock event for the implementation of the GCP. A comprehensive representation of EGT effects is based on the pollution emissions, TFP, and financialization levels of enterprises. Using a DID model, this study identified the influence of GCP on HPEs’ green transformation and the mechanisms of HPEs. The findings indicate the following:

(1) After the implementation of the GCP, compared with non-HPEs, HPEs have significantly improved emission reduction efficiency, while their financialization level has weakened significantly, but their TFP has been suppressed. Following a comprehensive suite of robustness tests, including parallel-trend analysis, placebo tests, alternative measurement approaches, addressing model self-selection issues, excluding confounding policy effects from the same period, and controlling for systemic factors, the aforementioned policy effects remain consistent and valid.

(2) The mechanism analysis clarifies the emission reduction and development decision-making mechanisms under GCP constraints. Under the constraints of the GCP, HPEs’ financing constraints are tightened, which encourages them to enhance the quality and quantity of green innovation, ultimately reflected in their emission reduction efficiency. Moreover, although the financialization level of enterprises decreases, it does not lead to substantive transformation of the real economy but to less investment in virtual economies because of limited resources. As enterprises allocate scarce resources to green innovation, it compels them to direct a greater portion of their R&D investment and overall innovation efforts toward this endeavor, ultimately hurting their TFP. The results support the “extrusion effect” rather than the “Porter effect.”

(3) Given the differences in financing constraints and green transformation motivation, non-state-owned, low endogenous financing, eastern region, and strong social responsibility enterprises were more significantly affected by GCP. In addition, the degree of green finance development and the intensity of environmental regulations in areas where enterprises are located have different directions of coordination effects on the effectiveness of GCP.

Overall, this study contributes to the existing literature by providing firm-level empirical evidence on how the implementation of GCP affects green transformation. For example, Guo et al. (2024) pointed out that green credit can curb the emissions of polluting industries and promote the green transformation of industries. However, existing research has not yet addressed the relationship between green credit and various dimensions of EGT. The findings highlight the importance of implementing the GCP and inherent tension between emission reduction and sustainable development that enterprises must navigate during their green transition. More importantly, the root cause of this “extrusion effect” is that, under the influence of GCP, enterprises need to reallocate capital and rapidly adapt to green transition requirements in the short term. Therefore, the conclusions of this study are not only applicable to China’s specific institutional context but also represent the universal challenges faced by EGT under green credit constraints.

Policy Implications

The findings of this study show that green financial instruments, including GCP, play a significant role in facilitating EGT. The following recommendations can be proposed to further enhance the effectiveness of green finance in promoting the green transformation of HPEs and alleviating the conflict between emission reduction and sustainable development:

First, the implementation mechanism of the GCP should be improved. To enhance the environmental information disclosure system for HPEs, we recommend unifying the content and format of disclosures, including emission reduction targets, transition implementation paths, environmental and social benefits, and related risk factors. Enterprises should clearly articulate their green transformation pathways, enabling them to correlate their pollution control performance with credit financing constraints, thereby fully leveraging the stimulatory effect of GCP on green innovation. Moreover, financial institutions can regularly conduct risk stress tests of EGT, comprehensively evaluating key dimensions such as environmental, economic performance, and “greenwashing” risks. Differentiated GCPs can be implemented for enterprises with different ownership types, endogenous financing levels, geographical locations, and corporate social responsibility performance, allowing enterprises to resolve the contradiction between emission reduction and development. For instance, special attention should be paid to the impact of GCPs on the economic performance of non-state-owned enterprises, ensuring sufficient funding support for their overall R&D efforts.

Second, the synergy of policy support measures needs to be valued. Beyond green credit, other aspects of the green financial system must be continually refined to expedite innovation in green financial products. For instance, prioritizing the growth of green bonds can diversify enterprise financing avenues, empowering them to actively pursue green innovation while ensuring adequate capital for business expansion beyond pollution control measures. This approach mitigates the potential adverse effects of GCP on TFP. Further, harmonizing the interplay between environmental regulations and the GCP prevents policy duplications. For example, by conducting policy effect simulations and pilot implementations, we can avoid the amplification of the inhibitory effect on enterprises’ TFP caused by the overlapping of multiple policies. In addition, the degree of financialization must be monitored and safeguards reinforced under an economic deleveraging policy. Enterprises should be inspired to direct more funds toward their primary operations by imposing curbs on excessive financial asset allocation. To promote EGT, efforts must be made to revitalize the real economy, optimize the business environment, and strengthen financial institutions’ capabilities in preventing “greenwashing” risks.

Third, an innovative financial system that meets the long-term needs of green transformation requirements of HPEs should be developed. Apart from the green financial system, diversified financial instruments must be used to provide the most direct financial backing for HPEs’ transition toward low-carbon and zero-carbon emissions, essentially establishing a “transitional finance” framework. On the one hand, the rapid standardization of transitional finance is crucial, involving the recognition of green transition activities and the emphasis on sectors worthy of transitional finance support. Driving product innovation in transitional finance is essential, proactively seeking loans, bonds, and other instruments tied to sustainable development, while also making use of the central bank’s carbon reduction incentives and clean coal financing programs. On the other hand, the loan interest rate and amount should be correlated with enterprises’ emission reduction efforts and ESG performance. By constructing a targeted “transitional finance” system, a long-term mechanism is built to facilitate the smooth green transition of high-pollution enterprises.

Limitations and Directions for Future Research

This study has some limitations. The first are endogeneity issues. This study employs the DID model and a series of robustness tests to ensure that the research findings are not affected by endogeneity problems. Specifically, EGT is a micro-level variable, while the implementation of GCP is a macro-level variable and not determined by the enterprises themselves; thus, the reverse causality issue in this study is minimal. Although this research has also incorporated control variables and fixed effects following existing studies, certain unobserved omitted variables may still exist. Overcoming potential bias in the relationship between GCP and EGT requires further attention in future studies. Second, because of limitations in data accessibility, we employed alternative indicators as proxies to gauge EGT performance. In the future, with improvements in enterprise information disclosure standards, more accurate and complete information on green transformation may be obtained from annual reports using techniques such as text analysis. Third, many interesting topics related to EGT under policy pressure are not fully covered in this study. Particularly, as environmental issues have garnered increasing attention, countries have introduced green transformation policies targeting HPEs. Future research should focus on the actual impact of these policies on the effectiveness of EGT. This leaves broad scope for follow-up research on this topic.

Footnotes

Acknowledgements

I would like to express my deepest gratitude to all those who have supported and guided use throughout the completion of this work. I extend my sincere thanks to reviewers and editors for their invaluable insights and expertise, which have significantly shaped the direction and quality of this research.

Ethical Considerations

Not applicable.

Consent to Participate

Not applicable.

Consent for Publication

Not applicable.

Author Contributions

Huiying Cui completed the paper alone, including conceptualization, data curation, formal analysis, funding acquisition, investigation, methodology, project administration, resources, software, supervision, validation, visualization, and writing (original draft, review & editing).

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was funded by National Social Science Fund of China [grant number 23BJL023].

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data are available from the corresponding author on reasonable request.