Abstract

Carbon Emission Disclosure (CED) trends have been positive for several years. Unfortunately, studies focusing on the relationship between CED and the Cost of Debt (COD) still need to be made available, particularly in emerging countries. Addressing this gap, this study aims to analyze the relationship between CED and COD in Indonesia. We predict that firms can enjoy a lower COD by lowering asymmetry information and fulfilling public expectations through CED. Using the unique characteristic of Indonesian-listed firms that participated Public Disclosure Program for Environmental Compliance (PROPER) during 2015 to 2019, we confirmed our verdict. Our result is robust due to several endogeneity test checks. Our study is believed to be one of the pioneers in analyzing the impact of CED on COD in the emerging market. Moreover, this study sample is limited to firms that follow PROPER, and we believe this is one of the robust initiatives to minimize greenwashing practices in CED.

Plain Language Summary

This study explores how a CEO’s background as an auditor influences a company’s debt costs in Indonesia. We found that companies led by CEOs with an auditing background tend to have lower debt costs. This is because auditors have a better understanding of financial risks and are more effective in managing audits. We also compare our findings with previous studies to highlight the new insights we discovered. This study is important as it provides insights into how a CEO’s background can affect a company’s financial performance.

Introduction

Climate change and global warming have attracted much attention in recent decades and have become critical problems most countries face (Choi et al., 2013). Environmental issues are believed to be obstacles to a country’s economic development (Işık et al., 2019, 2021, 2022; Ongan et al., 2021, 2022). Some research suggests that excessive and arbitrary human activity is the leading cause of the rising carbon emissions, known as greenhouse gases, that escape into the atmosphere (Riebeek, 2010). Several studies have proved carbon emissions to be a common issue that must be addressed immediately if a country’s economic development is to be optimal (Işik et al., 2017; Sun et al., 2020). Therefore, firms as economic actors with industrial activities have a great opportunity to produce greenhouse gas emissions (Oktay et al., 2021). The survey results from Carbon Disclosure Project (CDP, 2017) show that the 100 largest corporates worldwide are responsible for more than 70% of the world’s carbon emission production. Moreover, the demand for firms to contribute to the SDGs is getting stronger (Tapos, 2017). These demands come from various stakeholders, both internal and external. Realizing this, many firms are starting to switch and consider presenting environmental-based information to their stakeholders (Aliyu, 2018).

Global regulations can provide solutions to the problem of global warming and climate change by giving confidence in each corporate entity to disclose greenhouse gas emissions. The international community’s response to the phenomenon of climate change occurs in many countries by signing United Nations Framework Convention on Climate Change (UNFCCC). Several countries, including Indonesia, have ratified the Kyoto Protocol through the Law of the Republic of Indonesia No. 17 of 2004 to implement sustainable development and intervene in efforts to reduce greenhouse gas emissions. Furthermore, the government has been enacting a regulation that mandates Indonesian-listed firms to publish a sustainability report, one of the components of carbon emission information. In 2017, the Indonesian government published Peraturan Otoritas Jasa Keuangan (POJK) Number 51 the Year 2017, which mandates every listed firm to publish sustainability reports starting in 2022. The firm must distribute information more openly about various activities that the firm does and its acts of accountability. Transparency and accountability are expected to continue to underlie the entity in conveying information in its annual report.

Undoubtedly, Carbon Emission Disclosure (CED) is a necessary disclosure for the firm. Prior studies document that carbon emission disclosure can enhance corporate value (Jiang et al., 2021; J.-H. Lee & Cho, 2021), financial performance (Alsaifi et al., 2020; Lu et al., 2021; Tahat & Mardini, 2021), and reducing firm’s total, systematic, and idiosyncratic risk (Alsaifi et al., 2021). Among all CED studies, one of the exciting areas is the cost of debt (COD). He (2017) argued that the firm’s debt rating is higher when the entity displays a profound CED. The COD is a fee that a firm must pay to collect funds through bank loans or issuing bonds (Kumar & Firoz, 2018). Lenders recognize that CED is necessary that affects lending strategies (Jung et al., 2018). Firms that issue CED and take proactive action on emissions reductions are seen to be signaling well by the market that they are sensitive to the environment, contributing to long-term business prospects (He, 2017). In addition, the research done by Jung et al. (2018) explained that carbon emissions are positively and significantly associated with COD levels. According to the study, firms with high carbon emission risks must bear higher borrowing costs and those risks are mitigated once the firms publish carbon disclosure based on CDP.

The study examining the relationship between CED and COD has been conducted by He (2017) and Jung et al. (2018). While both studies examine CED, this research focuses on COD, specifically on how companies optimize their debt structure and manage related risks. This is relevant in the context of debt management and long-term financial planning. In contrast, He (2017) focuses on Cost of Equity (COE), which concerns how companies retain equity investors. Both variables are components of the Cost of Capital (COC). In examining CED, this article employs a novel measurement approach by providing a score on each disclosure item using a dichotomous scale, with a maximum score of 18 and a minimum score of 0. This differs from Jung et al. (2018), who use the historical carbon risk profile, measured as the total annual greenhouse gas emissions of the year divided by the year’s sales revenue. The dichotomous score focuses more on the presence or absence of disclosure information, which is crucial for assessing basic compliance and transparency. On the other hand, the historical carbon risk profile emphasizes environmental performance and operational efficiency related to carbon emissions.

Based on the context outlined above, the purpose of this study is to obtain empirical evidence about the relationship between carbon emission disclosure on the cost of debt in Indonesia. We select Indonesia setting due to two rationales. First, CED studies in emerging markets, including Indonesia, are dominated by the ones that focus on its determinants (e.g., Hermawan et al., 2018; Nasih et al., 2019; Ulupui et al., 2020) or its impact on the shareholder’s reaction that reflected in firm value (e.g., Hardiyansah & Agustini, 2020; Hardiyansah et al., 2021; Kurnia et al., 2021). There needs to be more evidence in Indonesia on how CED could affect creditors’ perceptions proxied by COD. Unfortunately, this contradicts Azhgaliyeva et al. (2020) findings, where Indonesia is the top country among ASEAN countries in green bond issuance.

Moreover, Indonesia is known as a country with a consistently increasing trend of sustainable reporting in terms of quality and quantity (Harymawan, Putra, et al., 2020). Secondly, Indonesia has its instrument to assess firms’ environmental compliance and performance, including carbon emissions, named PROPER. PROPER evaluation will not solely rely on firms’ documents requested by the committee and public reports (e.g., annual report and sustainability report) but also conduct a series of site visits to ascertain the greenwashing risks are minimum. Therefore, environmental-related disclosure (including carbon emission information) of firms participating in the PROPER program has lower greenwashing risks compared to their peers not participating in the PROPER.

These justifications motivate us to select non-financial Indonesian listed firms from 2015 to 2019. We limit our sample to 2019 because COVID-19 is believed to be an exogenous shock that could disrupt CED and COD data distribution. Based on the results, we find that CED is an influential factor in lowering firms’ COD. This result confirms that carbon-related information is crucial for the lender to determine firms’ risk in the escalating green bond issuance setting. This result is robust due to Coarsened Exact Matching (CEM) and Heckman Two-Stage regressions.

The main contributions of this study are as follows. First, this study is one of the pioneer studies to examine the effectiveness of CED in lowering Indonesian firms’ COD. The result may significantly enhance our understanding of creditors’ response to firms’ carbon emissions issue, including, but not limited to, the emission amount and their carbon mitigation practice and outcome. Moreover, to our best knowledge, this study is one of the studies pioneering in CED and COD topics in the Indonesian context, which is a suitable setting for environmental-related debt studies. Second, greenwashing is one of the crucial issues within environmental-related disclosure, closely related to impression-management purposes (Guo et al., 2020; Harymawan, Nasih, et al., 2020). This phenomenon is in line with Yan et al.’s (2022) finding that not all environmental-related disclosure are favored by shareholders and creditors, mainly when government supervision of greenwashing practices is weak. Our findings in overall support this argument as we evidenced that for firms heavily supervised by the government through the PROPER program, their CED effectively diminishes the firms’ COD. Therefore, it would be favorable for the government to focus on developing PROPER and invite other firms as many as possible to join the PROPER program to diminish greenwashing activities. Last but not least, these findings also provide valuable insight on urgency of the quality of carbon emission disclosure, both to company management and to creditors.

The remainder of this paper is organized as follows. The literature review and hypothesis development are presented in the second section. It is followed by a section describing our research design, sample selection, and empirical models. Section “Results and Discussions” provides the empirical results, and Section “Conclusion, Suggestions, and Limitations” reports the conclusions, the study’s limitations, and possible avenues for future research.

Theoretical Framework and Hypothesis Development

Carbon Emission and Its Urgencies

As we all know, carbon emissions are dangerous for the sustainability of this world, and all parties agree to join the movement to reduce carbon emissions. Many governments, including the CEOs of many companies, are committed to achieving zero emissions by 2060. To achieve this, corporate carbon accounting is an essential tool for managing the resulting carbon emissions.

Studies related to carbon accounting have received much attention and have continued to develop over the last two decades (Ascui & Lovell, 2012). However, this development was also followed by various perspectives, which led to the emergence of several definitions, objectives, and methodologies in the context of carbon accounting. Sutantoputra et al. (2012) argues that carbon accounting requires a holistic approach and supports the principles of transparency and accountability. Proper use of carbon accounting will enable managers to comply with regulations, manage energy and material flows, and at the same time, support clean operations. One of the crucial keys of carbon accounting is quantifying the carbon emissions produced and absorbed. Quantification of carbon emissions is divided into three scopes, namely direct emissions (scope 1), indirect emissions but controllable by an entity (scope 2), and indirect emissions and uncontrollable by an entity (scope 3). Mostly, companies can only calculate scope 1 of carbon emissions, considering they are easier for management to track and measure. Even though conditions show that quantifying carbon emissions still needs improvement from the company’s point of view, this effort certainly deserves appreciation. It continues to be developed in the future.

Related to carbon emissions, several studies focus on matters that influence a company’s efforts to reduce its carbon emissions, often called the company’s carbon performance. Several studies argue that quality and regulatory support for managing carbon emissions is crucial in supporting carbon-reduction performance. Government regulations are believed to be a tool that can effectively incentivize management to be more serious about reducing corporate carbon (Xia & Niu, 2020). Hu and Wang (2020) also show that the stringency of environmental-based regulations is directly proportional to the carbon performance of companies. Several other studies have shown several other crucial factors that can affect carbon reduction performance, such as corporate governance (Narsa Goud, 2022), national culture dimensional (Luo & Tang, 2022), and issuance of green bonds (Wei et al., 2022).

Several other studies have focused on the benefits a company receives when it succeeds in reducing its carbon emissions. In the context of companies, this carbon emission reduction will generally be incorporated in the company’s carbon emission reporting, as company stakeholders are more able to process information than just carbon emission reduction data. In addition, the Carbon Emissions Disclosure (CED) also contains information on strategies, conditions, and challenges companies face in managing carbon emissions. Patel and Kumari (2021) explain how necessary carbon disclosure is by companies as a form of support for the stewardship theory for a sustainable future. Recent studies show that CED can significantly increase the value of companies in the United States, Brazil, Russia, India, and China (Jiang et al., 2021). Choi et al. (2021) study show that Australian listed companies tend to experience a decrease in company value along with the carbon emissions they produce. However, this penalty is imposed only on firms with low disclosure scores or poor carbon management performance. Another study by Adhikari and Zhou (2021) shows that information asymmetry in risk in capital markets as measured by the bid-ask spread can be minimized through the CED. These studies show that providing information on the number of carbon emissions companies produce is essential. However, reporting on the management process and the company’s carbon emission mitigation strategy is no less crucial. As part of sustainability reporting, disclosure of carbon emissions should be prepared by integrating various divisions within the company so that when the information presented is also a collaboration of various disciplines (Harymawan et al., 2022). In this study, we focus on Carbon Emission Disclosure (CED), as this topic provides information that is more comprehensive and easier to understand for stakeholders, especially providers of corporate capital.

Impression-Management Theory and Greenwashing

One of the main problems of CED, as well as problems in other corporate reporting, is the issue of window-dressing. This discretionary practice has been a topic discussed for a long time. This practice is motivated by the existence of legitimacy received by companies when they have a performance that satisfies stakeholders under the concept of legitimacy theory. The practice is explained in impression management theory, where companies tend to manage stakeholders’ perspectives about the company itself as much as possible. Impression management is how people present an image of how their audience wishes to see them face-to-face (Goffman, 1959). This management practice generally involves two processes, namely creating a front and then developing concealment, in which the two processes are often inconsistent with the reality that occurs (Solomon et al., 2013). In the context of accounting itself, this theory is also often used by financial managers, whom they tend to choose to present the company’s financial performance using certain graphs and charts to help improve the quality of the narrative explanations they provide to users of financial statements (Beattie et al., 2004).

Several studies have been conducted to see how far companies have carried out window-dressing activities for a long time. For example, Hillier et al. (2008) focused on window-dressing accounting practices in credit unions due to the introduction of new regulations in Australia. The regulations require that credit unions with capital ratios below a set minimum of 8% are forced to meet this level within a maximum period of 3 years and, meanwhile, face regulatory criticism and loss of operational control. The results of the analyst’s study show that risky credit union managers (equity ratio below 8%) are involved in accounting window dressing rather than applying efficiency improvements to meet the required capital reserves. Another study was conducted by Loughran et al. (2009), focusing on the ethical terms contained in the company’s 10-K reports. They found that companies that operate in “sinful” industries get sued and have low governance indexes tend to use more ethical terms than other companies. Indirectly, they have discovered that companies close to unethical activities deliberately focus on disclosing terms related to ethics to cover up their behavior. This is evidence that the practice of window-dressing, both in accounting and in terms of disclosure, has been carried out for a long time to meet certain expectations or express stakeholders’ perspectives.

With the growing need for an agreement on sustainability from companies on sustainability initiatives, window-dressing has developed into greenwashing. Although many people think that greenwashing is a term that has developed recently, in fact, this term first appeared in 1986 (Pearson, 2010) and became widely known thanks to the study of Greer and Bruno (1996). Greenwashing can be defined as “selectively disclosing positive information about a company’s environmental or social performance, without fully disclosing negative information on that dimension, thereby creating an overly positive corporate image” (Lyon & Maxwell, 2011). Greenwashing is the gap between symbolic and substantive training practices (Roulet & Touboul, 2015).

In a similar vein to window-dressing, greenwashing is also a significant concern for researchers, particularly those interested in the continuity between a company’s riot performance and what is reported in their riot reports. Oh et al. (2017) found that companies classified as “sinful” due to their controversial industry tend to have superior CSR activity advertising efforts compared to their competitors. While they found that “sinful” companies may indulge in this practice as their financial performance improves, the study also shows that this effort also has the potential to backfire against companies. Another study was conducted by Sikka (2010), which revealed that the motivation for CSR reporting is not a corporate commitment to support the global sustainability movement. Through the results of his study, he argues that CSR reporting is a corporate greenwashing practice to cover up their tax avoidance behavior, as tax avoidance is a practice that is contrary to the principle of sustainability (Bird & Davis-Nozemack, 2018). A recent study also documented the contradiction between practice and practice (M. T. Lee & Raschke, 2023), where companies with poor ESG performance tend to have superior ESG reporting compared to companies with good ESG performance.

As part of sustainability reporting, CED is also likely to be used by management companies as an opportunistic greenwashing practice. For this reason, various studies claiming that CED brings various positive benefits, such as higher firm value and lower information asymmetry, have limitations if they do not minimize the issue of greenwashing in their research. A recent study by Datt et al. (2022) shows that the demand to minimize greenwashing activities in carbon emissions disclosure mostly provided through assurance services, shows positive trends from an international perspective. Jiang et al. (2022) suggest that firms tend to greenwash carbon information and use carbon disclosure as a legitimizing tool, as CED offers significant incentives. Starting from this gap, this research focuses on identifying the benefits of CED in reducing the cost of debt of Indonesian companies, which have minimized their greenwashing practices thanks to their participation in the PROPER program.

PROPER Program

PROPER is one of the Indonesian government’s initiatives to assess the firm’s environmental performance, which cover the compliance area, mainly based on the other local environmental-related regulation, and the beyond-compliance area, primarily based on the global and national best practices. PROPER’s participation scheme is mandatory and voluntary. For the firms selected by the Ministry of Environment and Forestry, provincial government, or city/district government due to their significant impact on the environment, they must participate in the PROPER program. On the other hand, firms that are not selected can also participate voluntarily. These unique mechanisms ensure that firms with operations heavily related to the environmental issue and, commonly followed by stakeholders interested in environmental issues, are less incentivized to adopt greenwashing activities. This mixed mechanism is also supported by Gatti et al. (2019) where one of the efforts to minimize greenwashing from companies is the application of a combination mechanism of voluntary and mandatory for sustainability-based reporting. In addition, involving the legal side where the sustainability reporting oversight mechanism is seen as part of the regulation is seen as effective in encouraging companies to carry out sustainability-based activities, not as an effort to fulfill stakeholder expectations alone (Sheehy, 2015).

The value determination in PROPER is also determined not only from their environmental reporting but also from their compliance with relevant regulations in the environmental sector that apply in Indonesia. All reported documents and activities are audited directly by the Ministry of Environment and Forestry by visiting the firm’s operational locations. This makes all information related to the environment that is disclosed accountable, ultimately reducing the potential for greenwashing for firms participating in the PROPER program. Firms participating in PROPER are less likely to engage in greenwashing activities as they are provided assurance services by the government.

Carbon Emission Disclosure and Cost of Debt

It is believed that level of corporate disclosure can minimize information asymmetry, thus lowering the risk borne by the firm (Putra et al., 2020). The positive impact of the disclosure will be more profound if there is external and internal pressure to disclose the information, specifically for carbon emission disclosure (Tang et al., 2020). He (2017) argued that firms that expose carbon emission disclosure broadly would pay a lower cost of debt. Botosan (1997) stated that greater disclosure of carbon emissions would increase stock market liquidity and reduce the firm’s cost of debt. Based on He (2017) research, firms that expose carbon emission disclosure broadly will be a superior attraction and a good signal for lending institutions. Firms participating in the signing of CDP are considered to be more aware of the firm’s external environment and have better preparation for potential adverse environmental events. Francis et al. (2008) also stated that lenders and equity issuers are motivated to accept fully and work with firms that disclose carbon emission disclosures broadly to lower capital costs. This rationale also supported Bui et al. (2020) finding that carbon emission disclosure effectively decreases the cost of equity.

Firms that expose carbon emission disclosures broadly pay attention to the amount of energy used and reduce emissions as much as possible by running various emissions reduction programs. In addition, firms actively involved in emissions reductions may signal that management is committed to low-risk environmental strategies (Bauer & Hann, 2012). Firms’ awareness of carbon emissions risks allows them to identify potential risks and take steps to address those carbon emission risks.

H1: Carbon emission disclosure negatively impacts the cost of debt.

Method of Research

This study used quantitative data types with secondary data sources. The secondary data used were in the form of annual reports, sustainability reports, and PROPER rating reports (Corporate Performance Rating Assessment Program in Environmental Management) from 2015 to 2019. In this study, we limit our sample up to 2019 in order to minimize COVID-19’s exogenous shock that begins in 2020 (Ahmad et al., 2021; Irfan et al., 2022). The total sample used in this study is 216 firm-year observations, detailed in Table 1. Moreover, we limit our sample only to non-financial Indonesian listed firms that participate in the PROPER program. This criterion was selected based on the PROPER capability in minimizing greenwashing potency, which commonly became a limitation for environmental-based disclosure studies (M. T. Lee & Raschke, 2023; Zharfpeykan, 2021).

Sample Selection Criteria.

PROPER is one of the Indonesian government’s initiatives to assess the firm’s environmental performance, which cover the compliance area, mainly based on the other local environmental-related regulation, and the beyond-compliance area, primarily based on the global and national best practices. PROPER’s participation scheme is mandatory and voluntary. For the firms selected by the Ministry of Environment and Forestry, provincial government, or city/district government due to their significant impact on the environment, they must participate in the PROPER program. On the other hand, firms that are not selected can also participate voluntarily. These unique mechanisms ensure that firms with operations heavily related to environmental issues and commonly followed by stakeholders interested in the environmental issue are less incentivized to adopt greenwashing activities.

The value determination in PROPER is also determined not only from their environmental reporting but also from their compliance with relevant regulations in the environmental sector that apply in Indonesia. All reported documents and activities are audited directly by the Ministry of Environment and Forestry by visiting the firm’s operational locations. This makes all information related to the environment that is disclosed accountable, ultimately reducing the potential for greenwashing for firms participating in the PROPER program.

Operational Definition

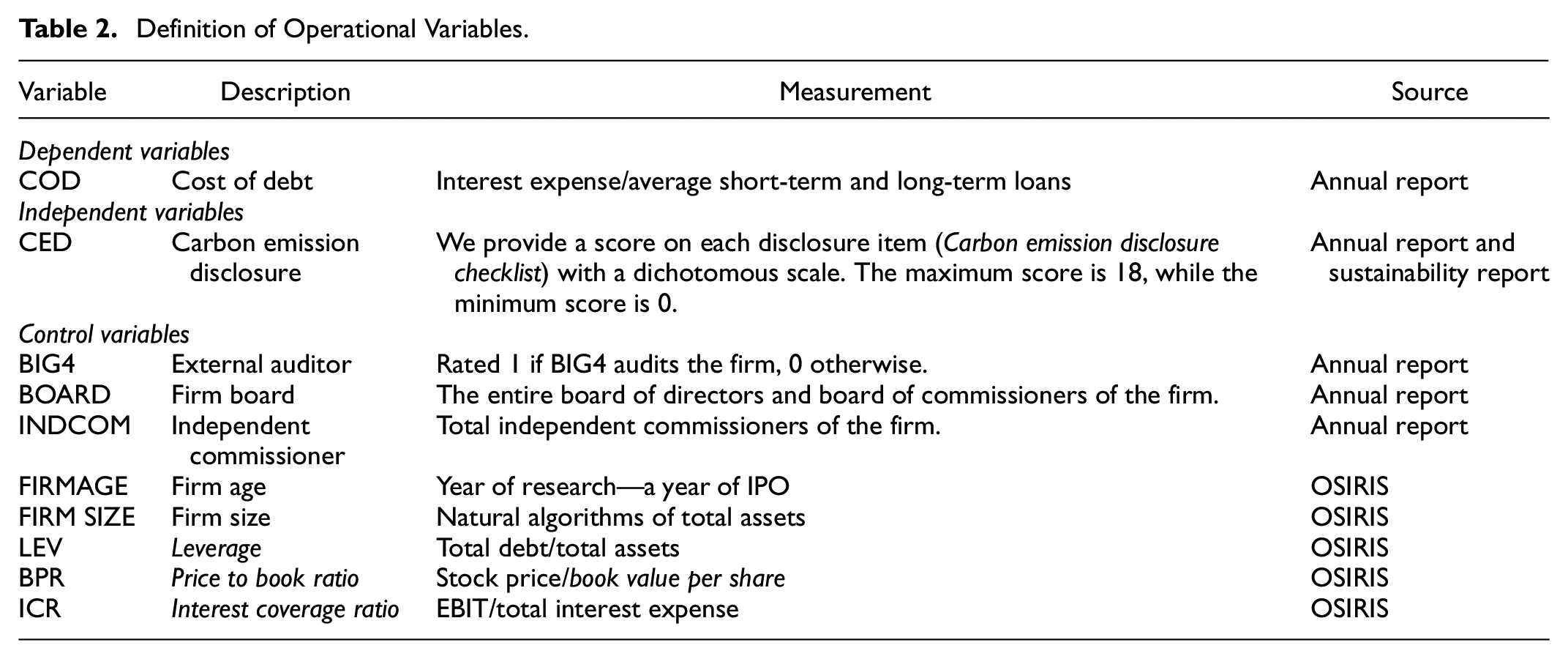

Carbon emission disclosure is a type of environmental disclosure that includes greenhouse emissions intensity and energy use, corporate governance, and strategies designed to deal with the impacts of climate change. This variable is calculated by providing a score on each disclosure item (Carbon Emission Disclosure Checklist) with a dichotomous scale. The maximum score is 18, while the minimum score is 0. The cost of debt is the rate of return creditors require when giving funding to a firm (Fabozzi, 2007). This variable is measured by the interest expense formula divided by the average short- and long-term loans.

The control variables used in this study are as follows: Auditor size (BIG4) as the auditor quality is believed as one of the essential proxies for the creditors in determining the firms’ risk. The entire board of directors and commissioners (BOARD) is generally a larger board size representing a greater level of corporate governance, resulting in a lower risk. Total independent commissioners of the firm (IND COM) are included because they represent independent individuals with supervisory functions crucial for corporate governance—the firm’s age (FIRMAGE) represents the firm’s experiences in handling the business environment. Natural algorithm of total assets (FIRM SIZE) included as large firms are well-known for their easiness in obtaining debt, including a low COD. Leverage (LEV) proxied by total debt divided by total assets is essential for creditors to assess risk. Stock price divided by the book value per share (BPR) represents shareholders’ perception. Last but not least, the interest coverage ratio (ICR) is commonly used to assess firms’ risk in adding additional loans. These control variables are commonly used in prior literature (e.g., Putra et al., 2020; Yan et al., 2022). The operational definitions of each of the 10 variables are listed in Table 2.

Definition of Operational Variables.

The data used in this study were pooled cross-sections using samples of firms listed on the IDX and participating in the consecutive PROPER rankings in 2015 to 2019 that published sustainability reports and annual reports. The selection of samples used in this study was made by reducing firms that did not disclose carbon emissions in the sustainability report or annual report, as many as 38 firms. Therefore, the final sample in this study is up to 216 firms. The sample selection from this study is summarized in Table 2.

Technique of Analysis

This study uses quantitative analysis techniques in which the data can produce the information needed for the analysis. The techniques of analysis used in the study are descriptive statistics, Pearson correlation tests, and simple regression tests with STATA software. The authors used fixed-effect regression. The following is a specification of regression equations that have been adapted to the hypothesis proposed by the authors:

Results and Discussions

Descriptive Statistics

The descriptive statistics analysis shows the mean, median, maximum, and standard deviation values from the variables in this study. For example, from the results of descriptive statistics, the COD variable has a maximum value of 45,277 at Adaro Energy Inc., Plc, in 2015 and a minimum value of 0.001 at Semen Baturaja Inc., Plc, in 2017 and 2015. In addition, the mean is 0.726, and the median is 0.060. Meanwhile, variable CED has a maximum value of 0.933 at Unilever Indonesia Inc., Plc in 2017 and a minimum value of 0.050 at Gunawan Dianjaya Steel Inc., Plc in 2018, and Tirta Mahakam Resources Inc., Plc in 2018. The mean and median values of 0.483 dan 0.500 indicate that nearly half of the firms in the sample disclosed carbon emissions. Furthermore, the information regarding descriptive statistics can be seen in Table 3 below.

Descriptive Statistics.

Pearson Correlation Test

The Pearson correlation test is a test that measures the strength of the linear relationship between two variables denoted by r (Pearson correlation coefficient; Table 4). It was historically used as the first formal correlation measure and is still one of the most widely used relationship measures.

Pearson Correlation Test.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

The table shows that CED has a negative and significant relationship with COD at the significance level of 1% and a coefficient value of −0.267. The results show that the higher the value of CED, the lower the firm’s cost of debt. Meanwhile, FIRMSIZE has a negative and significant relationship with COD at the significance level of 1% and a coefficient value of −0.239. The results showed that the larger the firm’s size, the lower the firm’s cost of debt. FIRMAGE and LEV have a negative and significant relationship with COD at the significance level of 5% level and coefficient values of −0.155 and −0.138, respectively. The results showed that the higher the value of FIRMAGE and LEV, the lower the firm’s cost of debt. On the other hand, BPR is associated significantly and positively with COD at 5% and a coefficient value of 0.149.

Baseline Regression

This study uses OLS regression with fixed effect analysis to test the relationship between independent and dependent variables. The regression test results showing the relationship of variable CED on the COD are found in Table 5.

Results of Regression Test on Carbon Emission Disclosure (CED) and Cost of Debt (COD).

Note. t statistics in parentheses.

p < .1. **p < .05.

Based on Table 5, regression analysis results showed that CED has a statistically significant and negative relationship with COD (coef. = −2.896, t = −1.84), concluding that the hypothesis is accepted. In addition, we also document a sufficient explanatory power (0.210) which implies our model can predict changes in COD by 21%. Compared to Putra et al. (2020), utilizing COD as the dependent variable in Indonesian listed firms, which documents adjusted R2 only .044, this study’s equation model has a more promising performance in the context of explanatory power.

Mounting studies have been documenting carbon emissions intensity in line with the cost of capital level, both for the cost of equity (e.g., Bui et al., 2020; Trinks et al., 2022) and cost of debt (e.g., Kumar & Firoz, 2018; Palea & Drogo, 2020). On the other hand, some other studies that emphasize CED instead of the carbon emission amount are, regrettably, dominated by the one that focuses solely on the cost of equity through minimalizing information asymmetry in capital markets (Adhikari & Zhou, 2021). For instance, Li et al. (2019) show that CED negatively affects the cost of equity. Another study by Jin et al. (2021) shows that the negative relationship only applies if the company has CED quality above a certain threshold. Unfortunately, as far as our observations are concerned, CED studies on the cost of debt still need to be expanded. However, when compared, our findings that CED is effective in reducing COD align with the findings of these studies in reducing the cost of equity.

One study that approaches the rationalization of the relationship between CED and COD is by S.-Y. Lee and Choi (2021). They examine the participation of Korean companies in government programs to reduce carbon emissions, where they are required to communicate to external stakeholders regarding their carbon information, such as actual emissions and reduction, carbon policy, strategy, and investment. They found that the companies that took part in the program, which required them to provide quality CED, consistently had lower COD based on various tests conducted. This result is in line with the findings of this study in which companies with a quality CED will enjoy benefits in the form of a lower COD.

Another related study that approaches rationalizing the finding of a negative relationship between CED and COD in this study is the study of He (2017). He (2017) developed a hypothesis and found that CED has a negative relationship with the cost of equity as CED is part of the fulfillment of legitimacy theory and stakeholder theory. Furthermore, He (2017) also found that companies with a quality CED tend to have a higher debt rating. This shows that creditors see companies with CED that are better than their competitors as having a lower risk, so the loans issued are seen as having minimal risk of not being repaid. In other words, creditors must bear the risk when providing loans to these companies is low. Another study that found similar results was by Jung et al. (2018). Jung et al. (2018) revealed that companies that respond to carbon information questionnaires by CDP and those that publish carbon-related information voluntarily gain certain benefits. The advantage is that the positive relationship between the number of carbon emissions and COD can be mitigated effectively. In other words, companies have intentions and carry out reporting actions related to their carbon emissions, appreciated by creditors so that borrowing costs incurred can be minimized. Although a study by Jung et al. (2018) is not fully representative of this study because Jung’s version of CED was measured using a dummy approach, which scored one if responding to the CDP questionnaire or had a carbon report and scored 0 otherwise, in general, the negative results of the relationship between CED and COD documented by this study have the principle the benefits of CED are the same as findings by Jung et al. (2018).

Another conclusion that can be drawn from the results of the baseline regression analysis of this study is related to the control variable. As shown in Table 5, the only control variable that has a statistically significant relationship is company leverage. Even though, in general, when the company’s leverage level is higher, it is directly proportional to liquidity risk, so it tends to increase COD. However, this relationship only sometimes occurs in all contexts. Our prediction of a negative relationship between leverage and COD is based on two rationalizations. First, the sample used in this study is a company that publishes carbon emission reporting based on the CDP framework and participates in the PROPER program. The two sample criteria indirectly show that the companies included in this study sample have a profound environmental concern, specifically concerning carbon emissions. That concern is not just greenwashing practices as closely monitored by the government. This encourages creditors to keep charging companies a low COD, despite their high level of leverage. The second rationalization is that a capital structure with high debt levels can also show that the company has the trust of various other creditors. This can encourage creditors to provide loans with low-interest rates, as the behavior of an entity is a reflection of the behavior of its competitors (Nani, 2016).

Analysis of Robustness Testing

Endogeneity is an issue that will arise in every business and accounting study. This study used the Coarsened Exact Matching (CEM) test to test the model’s durability and results. Table 6 presents the results of CEM analysis to find that the research model built will remain consistent with the primary analysis and to answer the endogeneity issues. The authors conducted CEM testing in this study by breaking down control variables into three strata by grouping each stratum with the same characteristics against independent variables. Table 6, panel I, show a summary of the sample breakdown when using CEM. In Table 6, panel I, 84 out of 103 observations have good carbon emission disclosure, and 108 of 113 observations have good carbon emission disclosure (below the median).

Results of CEM Analysis.

Note. t statistics in parentheses.

p < .05. ***p < .01.

Table 6 Panel II shows that the results from CEM testing are consistent with the primary regression of this study. This state suggests that the relationship between carbon emission disclosure (CED) and cost of debt (COD) showed significant negative results (coef. = −1.693, t = −2.31). This result confirms that our baseline regression results in Table 5 are robust.

In addition, we also added the Heckman two-stage regression test as a specific additional test to minimize the issue of unobserved variables in endogeneity. To carry out this test, we chose instrumental variables as these variables have the potential to affect CED and COD. This is also reinforced where CED is a variable that cannot be separated from the issue of self-selection bias, where companies can freely choose their level of CED quality. In the spirit of Harymawan et al. (2021), corporate reporting and benefits are two variables that can influence each other, especially considering the value from last year. The current CED level is likely influenced by last year’s COD level, although it will impact the current year of COD. Based on this, we select lagged COD as an instrumental variable. In the first-stage Heckman regression requirement, we transform CED into a dummy variable (D_CED) valued at one of the CED values that is more than the CED median value and 0 if otherwise. The Heckman two-stage regression result is provided in Table 7.

Heckman Two-Stage Regression.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

As seen in Table 7, we failed to document a significant relationship between lagCOD and CED in first-stage regression (coef. = 0.028, t = 1.27). This result confirms that last year’s COD did not impact the current year’s CED, which implies that simultaneity and reverse causality issues between COD and CED may not present, as it is a common issue in corporate reporting studies (Harymawan et al., 2021). Particularly, to re-affirm reverse causality issue is minimized, we also retest equation model 1 with lagCOD as an additional control variable. Our untabulated result shows CED and COD relationship has a negative result (coef. = −3.565, t = −1.96. These results affirm that simultaneity and reverse causality issues for lagged COD are unlikely to present between CED and COD.

The second regression stage shows that CED and COD have a statistically significant negative relationship (coef. = −2.385, t = −2.19). On the other hand, the MILLS variable shows a statistically insignificant relationship with COD. These outcomes imply two suppositions. First, compared with the baseline regression result, we document a more significant result, as the initial regression results show only a significance level of 10%. This conclusion is crucial as after considering lagCOD effect represented in MILLS, the negative relationship between CED and COD became clearer. Secondly, these results also conclude that lagCOD does not affect the relationship between CED and COD. This conclusion is also supported by our untabulated regression, where lagCOD shows an insignificant relationship with COD (coef. = 0.021, t = 0.88)

Conclusion, Suggestions, and Limitations

This research discusses the impact of Carbon Emission Disclosure (CED) on the Cost of Debt (COD) of companies in Indonesia. Global attention to climate change and global warming, which are considered to hinder economic development, has placed a spotlight on industrial activities of companies as a major source of carbon emissions, with increasing demands for companies to contribute to the Sustainable Development Goals (SDGs). This study focuses on how carbon emission disclosures made by companies can influence creditors’ perceptions and, consequently, the companies’ cost of debt. In the Indonesian context, regulations such as POJK No. 51 of 2017 mandate companies to issue sustainability reports that include carbon emission information. The PROPER program is also used as an evaluation tool for corporate environmental performance to minimize the risk of greenwashing. The study uses data from non-financial companies listed in Indonesia from 2015 to 2019, employing Coarsened Exact Matching (CEM) and Two-Stage Heckman regression methods to ensure robust results. The main findings indicate that CED significantly reduces COD, sending a positive signal to creditors about the company’s commitment to the environment.

Overall, recent publications highlight several gaps regarding carbon emission disclosures and cost of debt. While documenting the benefits of carbon emission disclosures on equity costs, the discussion on its impact on the cost of debt remains limited, without considering the quality of the reporting. Existing studies have rarely explored the benefits of carbon emission reporting on the cost of debt in Indonesia, which contradicts the fact that Indonesia has the highest green bond issuance in Southeast Asia. Greenwashing issues in carbon disclosures also remain unresolved, leading to significant limitations. There is a growing consensus that decarbonization is crucial for cleaner production. All these unresolved issues can hinder the stability and development of cleaner business models.

This paper bridges the gaps in research on carbon emission disclosures and the cost of debt. The findings enhance the understanding of the benefits of carbon emission disclosures for companies, particularly in reducing the cost of debt, even though research on the quality of disclosures remains limited, especially in developing countries. The paper also addresses greenwashing issues to guide research design and interpret empirical results. There is consensus that sustainability disclosures are often linked to impression management under stakeholder pressure. To reduce greenwashing, this study uses a sample of companies participating in the government’s PROPER program, which is expected to minimize such practices. Thus, this paper provides insights into how carbon emission disclosures reduce the cost of debt and highlights the importance of control mechanisms to reduce greenwashing in sustainability disclosures.

This study has important implications for investors, policymakers, and corporate management. The findings help sustainable creditors to use mechanisms such as company participation in the PROPER program or assurance services to minimize greenwashing practices in carbon emission reporting. For corporate executives, high-quality carbon emission disclosures are necessary to meet stakeholder expectations, including creditors and NGOs like the CDP. This also encourages increased green investment and carbon management capacity to enhance resilience against the impacts of global warming. The study’s results are beneficial for regulators in adopting appropriate policies. Currently, listed companies are required to issue sustainability reports that include carbon emission information, but specific regulations to manage carbon emissions from the private sector in Indonesia are still unclear. Plans to implement carbon taxes in certain industrial sectors have been repeatedly delayed, causing companies to report carbon emission management without clear guidance from the government. This study emphasizes the importance of formulating specific regulations on corporate carbon emission management. The PROPER program, which combines voluntary and mandatory participation, should publicly disclose the participation model of each company. This information is valuable for future researchers to conduct more in-depth analyses of PROPER and for stakeholders to analyze potential greenwashing and make better investment decisions.

One limitation of this study is that the sample only includes companies participating in the PROPER program, which may not apply directly to all companies. The decision to choose this sample may introduce sample bias, making it difficult to generalize the results to all companies. Although using this sample is an advantage of this study as it minimizes greenwashing issues, we acknowledge that the results cannot be generalized to all companies. Therefore, future studies are recommended to use all companies, both those participating in the PROPER program and those not, to compare the benefits of carbon emission disclosures in companies that participate in PROPER and those that do not. Additionally, future research should consider the mechanism of company participation in PROPER, which lies between voluntary and mandatory, as a sub-sample analysis or as an interaction and/or control variable. This can enhance the contribution of research focusing on greenwashing issues in companies participating in sustainability assessments like PROPER. Another limitation of this study is that we did not consider the impact of COVID-19. Although this study limits the sample of companies to 2018, given that company reports for 2019 were compiled in early 2020 when COVID-19 began to affect Indonesia, it is suggested that future studies use the latest years to see the potential impact of COVID-19 on corporate carbon emission disclosures.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was funded by Riset Mandat 2022 research scheme No. 225/UN3.15/PT/2022.

Ethical Approval

This study does not contain any studies involving animals and human participants performed by any of the authors.

Data Availability Statement

The research data supporting the findings of this study are available upon request from the corresponding author.