Abstract

This paper investigates the effects of enterprise digital transformation on carbon performance, with a particular focus on both total carbon emissions and carbon emission intensity. It further examines how economic policy uncertainty (EPU) moderates these relationships. Drawing on panel data of Chinese A-share listed firms from 2011 to 2023, we construct firm-level indicators for digital transformation, carbon emissions, and EPU. The empirical results show that digital transformation significantly reduces carbon emission intensity by advancing green technological innovation and enhancing factor allocation efficiency. However, it also contributes to an increase in total carbon emissions due to the scale effect associated with production expansion. Moreover, elevated levels of EPU weaken the positive environmental impact of digital transformation by diminishing the marginal benefits of green innovation and resource optimization, thereby dampening improvements in carbon intensity and limiting increases in total emissions. Further heterogeneity analysis reveals that the impact of digital transformation is more pronounced in large enterprises, firms operating in high-carbon sectors, and those located in economically developed regions. In contrast, the moderating effect of EPU is significantly stronger among smaller firms, heavily polluting industries, and enterprises in less-developed regions. Overall, these findings provide novel insights into the dual effects of digital transformation on environmental outcomes and underscore the critical role of policy uncertainty in shaping these dynamics.

Plain Language Summary

The empirical analysis reveals that digital transformation significantly lowers carbon emission intensity by facilitating green technological progress and improving factor allocation efficiency. However, it also leads to an increase in total carbon emissions due to the scale effect of production expansion. Furthermore, heightened EPU weakens the effectiveness of digital transformation by reducing the marginal gains from green innovation and resource allocation, resulting in less pronounced improvements in carbon intensity and smaller increases in total emissions. Heterogeneity analysis shows that these effects are more prominent in large firms, high-carbon industries, and economically developed regions. In contrast, in smaller firms and less developed areas, the negative moderating role of EPU is more pronounced, further constraining the carbon performance benefits of digital transformation.

Keywords

Introduction

The intensifying environmental challenges brought about by global climate change have prompted governments worldwide to establish carbon emission targets aimed at mitigating global warming. As the world’s largest carbon emitter, China has proposed its “dual carbon” goals, which include achieving peak carbon emissions by 2030 and attaining carbon neutrality by 2060. In light of these national ambitions, a pressing research question arises: how can enterprises reconcile increasingly stringent environmental constraints with the pursuit of high-quality development? Within this context, digital transformation has emerged as a critical lever for promoting green transitions. However, its effectiveness may be highly dependent on the broader institutional environment, particularly the level of EPU. This study aims to explore the mechanisms through which digital transformation influences corporate carbon performance under varying degrees of policy uncertainty.

Prior studies have progressed along two primary dimensions. The first concerns the environmental impact of digital transformation. Existing evidence indicates that digital technologies reduce operational costs, enhance production flexibility, and foster innovation (J. Li et al., 2021; T. Zhang et al., 2022). More recently, their contribution to promoting green development and lowering emissions has attracted growing attention (Xie et al., 2024). However, most research focuses on total carbon emissions, while carbon emission intensity, which reflects technological efficiency, remains insufficiently explored. The second dimension examines the relationship between EPU and carbon emissions. According to real options theory (Myers & Turnbull, 1977), high levels of EPU raise the value of waiting, which causes firms to delay long-term investments that are essential for digital transformation, including green research and development and low-carbon equipment upgrades. These delays reduce the effectiveness of digital transformation in improving carbon performance and slow down the pace of green transition. Empirical studies provide further support for this mechanism. Baker et al. (2016) and Jiang et al. (2022) observed that EPU discouraged capital investment, particularly in projects involving technological innovation. Mirza et al. (2025) found that rising policy volatility led firms to postpone or abandon green innovation due to greater exposure to firm-specific risks and heightened managerial caution. EPU also influences emissions through structural channels. J. Yu et al. (2021) showed that unclear policy directions prolonged firms’ dependence on high-carbon energy sources, prompting them to rely on cheaper but more polluting fossil fuels. Furthermore, J. Wang et al. (2025) showed that increasing EPU weakened environmental governance. Firms facing greater uncertainty tended to reduce ESG engagement, often classifying environmental upgrades as non-essential and cutting related expenditures.

In summary, digital transformation is widely recognized as a key approach to improving resource utilization, streamlining production processes, and advancing green technological innovation. By integrating technologies such as intelligent manufacturing, data-driven decision-making, and energy-efficient management, firms are expected to enhance productivity while simultaneously reducing energy consumption and carbon emissions. Although digital transformation theoretically contributes to emission reduction, the presence of EPU may inhibit its green effectiveness. Elevated uncertainty can delay or distort the implementation of digital initiatives, thereby weakening their impact on both total carbon emissions and carbon emission intensity. However, the theoretical understanding and empirical investigation of this interaction remain limited in the existing literature.

Given these theoretical insights, China presents a particularly relevant empirical setting to investigate these research gaps. As the largest developing economy and global carbon emitter, China is actively promoting nationwide digitalization across various industries as part of its broader economic restructuring and innovation-driven development strategy. Simultaneously, China’s ambitious yet challenging “dual carbon” targets necessitate urgent improvements in corporate carbon performance. Moreover, China’s policy environment has undergone notable volatility in recent years, characterized by frequent shifts in industrial policy, regulatory standards, and incentive mechanisms. This inherently uncertain policy context provides an ideal testing ground for examining how EPU moderates the environmental dividends of digital transformation. In addition, the Chinese capital market, particularly its A-share listed companies, offers comprehensive and high-quality firm-level data disclosures, allowing rigorous empirical analysis and ensuring generalizability of findings.

Empirically, based on corporate disclosure documents, this paper employs textual analysis methods to construct firm-level indices for digital transformation and EPU, and adopts a fixed-effects panel regression model using data from China’s A-share listed companies spanning from 2011 to 2023. This methodological approach effectively controls for firm-specific, time-invariant characteristics and potential omitted variable biases, thereby ensuring robust estimation of the causal impacts of digital transformation and EPU on both total carbon emissions and carbon emission intensity. Furthermore, to ensure the robustness of the results and address potential endogeneity concerns, a series of robustness checks are conducted. These include alternative measurements of key variables, exclusion of observations during major economic shock periods, quantile regression, difference GMM and system GMM estimations, and instrumental variable (IV) approaches. In addition, mechanism tests are performed to clarify the internal transmission channels through which digital transformation affects carbon emissions, specifically focusing on green technological innovation, resource allocation efficiency, and scale expansion effects. Moreover, heterogeneity analyses are conducted across different firm sizes, industry types, and regional economic development levels, providing detailed policy implications.

Specifically, this study empirically explores three critical questions:

This study contributes to the literature in several ways. First, it identifies the dual effects of digital transformation on corporate carbon emissions and uncovers the underlying transmission mechanisms, thereby enriching the research on environmental outcomes at the firm level. Second, by incorporating EPU into the analytical framework, the study advances understanding of how policy volatility alters the environmental performance of digital transformation, expanding the scope of research on policy uncertainty. Third, the construction of a novel firm-level EPU index offers a replicable and quantifiable tool for future empirical analysis. Finally, the findings provide timely empirical evidence to support China’s dual carbon goals, offering practical implications for policymakers and enterprises to jointly foster low-carbon development amid increasing policy uncertainty.

The remainder of this paper is organized as follows: Section 2 reviews the relevant literature and presents the hypotheses. Section 3 outlines the research design. Section 4 reports the empirical results and robustness tests. Section 5 discusses the mechanisms and heterogeneity checks. Finally, Section 6 concludes this study.

Literature Review and Hypotheses Development

Literature Review

Economic Effects of Enterprise Digital Transformation

Enterprise digital transformation, which integrates big data, cloud computing, and artificial intelligence, has emerged as a critical driver of firm performance. By streamlining operational workflows, reducing information asymmetry, and optimizing the allocation of capital, labor, and energy, it significantly enhances production efficiency (Barua et al., 1995). Concurrently, digitalization fosters technological and business model innovation, strengthening firms’ capacity to develop new products and services (Hanelt et al., 2021) and improving financial outcomes through more efficient value chain and supply chain management (Bharadwaj et al., 2013).

Recent studies have extended this analysis to environmental outcomes. Digital technologies can lower energy consumption and carbon emissions by improving process controls and resource utilization (Kumar et al., 2023). However, Bieser and Hilty (2018) highlighted that these efficiency gains often spur production scale expansion, yielding a “rebound effect” that may offset some emission reductions. This dual impact underscores the need for detailed examination of the mechanisms by which digital transformation influences carbon emissions under varying conditions.

Economic Effects of EPU

EPU has increased markedly in recent years due to the pandemic, trade disputes, and geopolitical conflicts, with its impact on corporate investment and market expectations widely documented. By raising perceived risk, EPU dampens firms’ willingness to invest and innovate (Baker et al., 2016), thereby hampering economic growth and long-term development. Dixit and Pindyck (1994) argued that policy uncertainty leads firms to delay or scale back long-term projects in favor of short-term financial stability. This tendency is particularly evident in capital-intensive projects with long payback periods (Bloom et al., 2007), such as technological innovation and digital transformation (C. Xu et al., 2024). Moreover, Zhou et al. (2023) noted that heightened policy uncertainty amplifies firms’ risk aversion toward technological upgrades, making them more cautious in adopting new technologies and ultimately weakening the potential of digital technologies to enhance efficiency and reduce emissions.

EPU’s Impact on the Carbon Emission Effects of Enterprise Digital Transformation

Although current research directly examining how EPU affects the carbon emission reduction effects of digital transformation remains relatively limited, existing literature consistently demonstrates that EPU plays a crucial moderating role in this relationship. EPU primarily exerts its influence through the core channel of altering corporate investment behavior. Digital transformation typically requires substantial upfront investments in green technologies and low-carbon production processes. However, heightened policy uncertainty increases firms’ risk perception regarding these investments, prompting them to adopt a more cautious approach. Such risk-averse behavior may directly undermine the potential carbon reduction benefits of digital transformation, as enterprises may postpone or scale back investments in emission-reduction technologies (He et al., 2022). Furthermore, the conservative investment behavior induced by EPU is particularly pronounced in production expansion decisions. As noted by Leahy and Whited (1996), policy uncertainty significantly dampens firms’ willingness to undertake large-scale capital expenditures, with this effect being more prominent in high emission-intensity industries.

Hypotheses Development

Enterprise Digital Transformation, Production Expansion Effect, and Total Carbon Emissions

According to economies of scale theory, digital technologies such as big data, cloud computing, and IoT optimize production processes and expand firms’ production capacity, resulting in higher total carbon emissions due to increased output (Brynjolfsson & McAfee, 2014). Coelli et al. (2005) similarly argued that although efficiency improves, rising output leads to greater emissions. G. Li et al. (2023) confirmed that while digital technologies enhance efficiency in manufacturing, they also expand production scale and energy consumption. Financing theory posits that digital transformation improves information transparency and signaling, enhancing firms’ credibility and financing ability (Stiglitz & Weiss, 1981). Q. Li et al. (2023) showed that strengthened financing capacity facilitates capital acquisition for expansion, which raises total emissions despite efficiency gains. Liu and He (2024) further emphasized that digital transformation boosts resource allocation efficiency and optimizes financing channels, enabling production expansion. Overall, while digital transformation enhances capital access and operational efficiency, the associated production scale growth contributes to increased total carbon emissions, reflecting a production expansion effect where capacity growth directly escalates emissions. Based on this, we propose the following hypothesis:

Enterprise Digital Transformation, Resource Allocation Optimization, and Carbon Emission Intensity

From a resource-based perspective (Barney, 1991), digital transformation significantly enhances the efficiency of resource allocation within firms, thereby fostering sustainable competitive advantages. By improving the allocation of key production factors, including capital, labor, and energy, digital technologies reduce dependence on high-energy and high-emission resources while encouraging the adoption of cleaner, renewable energy sources. This shift leads to more efficient resource utilization, minimizes energy waste, and contributes to a substantial reduction in overall carbon emissions.

Moreover, digital transformation facilitates faster and more transparent information flow, allowing market mechanisms to reallocate resources toward low-energy, high-efficiency firms. As a result, market competition becomes more intense, leading to the gradual exit of inefficient, high-pollution enterprises, while environmentally friendly and efficient firms gain market share and expand their operations. This dynamic further optimizes resource allocation and reduces carbon intensity at the industry level. C. Zhang and Ji (2019) provided empirical evidence that digitalization enhances firms’ flexibility in resource deployment, lowering energy waste and emissions. Similarly, Lyu et al. (2023) stressed that accelerated information flows allow efficient firms to access resources swiftly, reinforcing market selection mechanisms and promoting carbon emission reductions.

Thus, we propose the following hypothesis:

Enterprise Digital Transformation, Green Technology Progress, and Carbon Emission Intensity

According to innovation theory, technological progress is a fundamental driver of productivity improvement and green development. Schumpeter (1934) argued that technological innovation not only promotes economic growth but also reduces carbon emissions by enhancing efficiency and optimizing resource allocation. Digital transformation, through technologies such as the Internet of Things, big data, and artificial intelligence, improves production processes, minimizes resource waste, and fosters green innovation, thereby making production processes more environmentally friendly and reducing carbon intensity. Bhagat et al. (2022) found that digital technologies like the Internet of Things significantly enhance production automation and intelligence, leading to lower energy consumption and reduced emissions. C. Xu et al. (2024) further highlighted that data-driven decision-making improves resource utilization efficiency, reduces unnecessary energy consumption, and facilitates green innovation.

Additionally, spatial spillover theory suggests that the diffusion of technology and knowledge across regions and industries promotes the widespread adoption of green technologies, enhancing green innovation at the societal level and further lowering carbon intensity (Porter & Linde, 1995). Digital transformation accelerates this diffusion, breaking spatial and industrial barriers to enable broader carbon reduction effects (Zeng et al., 2022).

Thus, we propose the following hypothesis:

EPU’s Impact on the Carbon Emission Performance of Enterprise Digital Transformation

According to investment decision theory and cost control theory, rising policy uncertainty encourages firms to adopt more conservative investment strategies, favoring short-term stability over long-term commitments (Dixit & Pindyck, 1994). Digital transformation is typically a long-term initiative that demands significant capital and technological inputs, particularly in areas such as technological upgrading and resource optimization. As policy uncertainty increases, firms become less willing to invest in digital transformation, slowing the pace of digitalization and limiting the realization of its potential to improve resource allocation and reduce carbon emissions. This investment caution delays digital transformation and weakens its effectiveness in curbing total carbon emissions.

From the perspective of innovation theory, uncertainty also hampers firms’ innovation activities. Under high levels of EPU, firms are less inclined to invest in green technologies, which are essential for reducing carbon intensity through cleaner production processes and more efficient resource use (He et al., 2022). Elevated policy uncertainty leads firms to rely more on conventional high-carbon production methods, thereby increasing carbon intensity. Additionally, policy uncertainty discourages capacity expansion investments. Although this may slow the growth of emissions, it also constrains the ability of digital transformation to deliver large-scale emission reductions through efficiency improvements.

Thus, we propose the following hypothesis:

Research Design

Data

Given that large-scale digital transformation of Chinese firms begins around 2010, this study focuses on A-share listed firms in China from 2011 to 2023. Carbon emissions data are sourced from the China Statistical Yearbook and the China Energy Statistical Yearbook, while financial data come from the China Stock Market and Accounting Research (CSMAR) database. Digital transformation data are extracted from company annual reports using textual analysis. Following Geng et al. (2024), the sample excludes the following: (1) delisted firms, to ensure data continuity; (2) companies designated as ST, *ST, or PT, due to their abnormal financial status; and (3) firms with missing values for key variables. This process yields a final sample of 23,119 valid observations.

Methodology

To address the two questions, this study adopts the empirical models set forth by Z. Li et al. (2024) as follows:

Where subscripts f and t represent firm and year, respectively. CE and CEI represent the total carbon emissions and carbon emission intensity, respectively. Dig denotes the level of digital transformation; EPU represents the perception of firms’EPU. X refers to the vector of control variables; V indicates the industry fixed terms, η indicates the year fixed terms, λ indicates the regional fixed terms; ε is the random error term.

Variables

Carbon Emission Performance

This study assesses firms’ carbon performance using two key indicators: total carbon emissions (CE) and carbon emission intensity (CEI). Reflecting China’s dual-control policy on both emission volume and efficiency, this dual-dimensional approach captures the scale and intensity of firms’ carbon output. As total emissions are not subject to mandatory disclosure in listed firms’ annual reports, direct data are limited. Accordingly, CE and CEI are estimated following the methodology proposed by Shen and Huang (2019), as outlined below:

where the carbon dioxide conversion coefficient of 2.493, as estimated by Xiamen University’s Energy Conservation Center, is used as the standard.

Enterprise Digital Transformation

Drawing on Han et al.(2024) and Acemoglu et al. (2021), this study uses textual data from the annual reports of listed firms and applies a machine learning-based “Term Frequency-Inverse Document Frequency” (TF-IDF) method to measure the level of digitalization (Dig) of enterprises. This method can effectively enhance the ability to identify digital-related keywords in text analysis, thereby reducing the underestimation of digital-related terms caused by the excessive presence of general vocabulary.

Where

Firms’ Perception of Economic Policy Uncertainty

In existing literature, the measurement of firms’ perception of EPU typically relies on national or regional indices (e.g., Baker et al., 2016). Drawing on the approach developed by Nie et al. (2020), this study constructs a firm-level indicator of EPU perception based on the textual analysis of annual reports.

The methodology consists of the following steps. First, each firm’s annual report in PDF format is converted into a text file using a document conversion tool. Using regular expressions, the content of the “Management Discussion and Analysis” section (also referred to as the “Board of Directors’ Report” in some cases) is extracted. All numbers, English letters, punctuation marks except periods, and special characters are removed. The cleaned text is then split into sentences using periods as delimiters, considering the syntactic characteristics of the Chinese language. Each sentence is treated as an individual unit of analysis.

Let Sft denote the set of sentences in the Management Discussion and Analysis section of firm f in year t. Each sentence is segmented into words using the Jieba package in Python, and stop words are removed simultaneously. To improve segmentation accuracy and avoid ambiguity, a customized dictionary is created. This dictionary includes full names and abbreviations of all A-share listed companies, accounting-related terms, uncertainty-related keywords, and terms associated with government or policy.

After segmentation, each sentence is represented as a sequence of words. If a sentence contains any uncertainty-related word, it is labeled as an uncertainty sentence s. If both uncertainty-related and policy-related words appear in the same sentence, it is further classified as a policy uncertainty sentence and assigned to set P. The firm-level EPU index is calculated as the number of uncertainty-related words ns in policy uncertainty sentences divided by the total number of words N in the Management Discussion and Analysis section. The EPU index is defined as shown in Equation 6, where the indicator function IP(s) equals 1 if sentence s belongs to set P, and 0 otherwise.

Control Variables

Following Song et al. (2022), this study incorporates several control variables to account for both firm-level and regional-level heterogeneity: (1) Firm age (Age): Older firms typically demonstrate greater operational stability, stronger reputations, and richer experience, which can enhance their capacity for environmental management and technological innovation, ultimately influencing carbon emissions. (2) Leverage (Lev): The leverage ratio reflects a firm’s financial structure and risk exposure. Higher leverage may limit a firm’s flexibility to invest in green technologies and energy-saving initiatives, thereby increasing carbon emission intensity. (3) Profitability (Profit): Firms with higher profitability are generally better positioned to support investments in environmentally friendly technologies, which may help reduce emissions. (4) Capital intensity (Capital): Capital intensity represents the amount of capital invested per unit of output. Firms with greater capital intensity often display distinct energy use profiles, which can affect their emission levels. (5) Government subsidies (Sub): Financial support from government sources can influence firms’ investment strategies, including their engagement in sustainable technologies. Subsidies may ease funding constraints associated with digital transformation and promote emission reduction. (6) Internet infrastructure (Net): The development of regional internet infrastructure reflects the local digital environment, which may shape the effectiveness of digital transformation in achieving emission reductions. (7) Environmental regulation (er): The strength of local environmental policies is proxied by the frequency of environment-related terms in prefectural government work reports. In regions with more stringent regulation, firms may have stronger incentives to adopt digital tools to enhance energy efficiency and reduce emissions. The model also controls for year-industry fixed effects and regional fixed effects to improve model fit and estimation efficiency. Additionally, variables with outliers have been winsorized at the top and bottom 1% to mitigate the impact of extreme values to address potential issues with heteroskedasticity and serial correlation. Table 1 provides detailed definitions for all variables.

Definition of Variables.

Table 2 reports the descriptive statistics of the main variables. The average value of total carbon emissions (CE) is 5.0252, with a standard deviation of 1.3708. The minimum and maximum values are 2.1695 and 8.7729, respectively. For carbon emission intensity (CEI), the mean is 0.3979, with a standard deviation of 0.3692, ranging from 0.0107 to 1.9281. These figures suggest substantial variation in carbon performance among firms. The mean value of digital transformation is 1.0862, with a standard deviation of 1.2075. The economic policy uncertainty (EPU) index ranges from 0 to 0.5023, indicating significant differences in firms’ perceived policy uncertainty. All other control variables fall within expected and reasonable ranges.

Descriptive Analysis.

Empirical Results

Baseline Results

Table 3 presents the baseline regression results. Columns (1) and (2) show that digital transformation significantly increases total carbon emissions, while columns (4) and (5) indicate that it significantly reduces carbon emission intensity. The interaction term between digital transformation and EPU in columns (3) and (6) suggests that EPU weakens both the positive impact of digital transformation on total carbon emissions and its negative impact on carbon emission intensity.

Baseline Results.

Note. Robust standard errors are shown in parentheses. “Yes” indicates that the corresponding variable has been included, and “No” indicates that it has not been included. The same applies to the table below.

, **, and *** represent significance at the 10%, 5%, and 1% levels, respectively.

These findings reveal a dual effect of digital transformation on carbon performance. On one hand, digital technologies enhance production efficiency and enable firms to scale up operations, thereby increasing total emissions (Du & Li, 2024). On the other hand, digital transformation improves resource allocation, fosters green innovation, and enhances operational efficiency, which collectively reduce carbon emission intensity (Han et al., 2024; Zheng & Zhang, 2023). These results align with existing literature, which argues that technological advancement, while improving process efficiency, may also lead to a rebound effect where increased efficiency encourages greater production and emissions (Z. Li et al., 2024).

The moderating role of EPU is reflected in the interaction term between digital transformation and EPU. The negative coefficients indicate that during periods of elevated policy uncertainty, firms tend to adopt more conservative investment strategies, particularly toward long-term initiatives such as digital transformation (Wen et al., 2021). This cautious behavior dampens both the emission-reducing effect of digital transformation and its expansionary effect on total emissions. These findings underscore the importance of a stable policy environment for enabling firms to fully leverage digital transformation to improve carbon performance.

The control variables exhibit heterogeneous effects on total carbon emissions and carbon emission intensity. Firm age, financial leverage, and capital intensity significantly influence both dimensions, whereas government subsidies and internet infrastructure display relatively limited explanatory power. Notably, while firm age and leverage are associated with lower carbon intensity, they are also linked to higher total emissions. In contrast, the stringency of environmental regulation contributes to reductions in carbon intensity but does not show a statistically significant impact on overall emission levels.

Robustness Tests

Alternative Measures of Core Variables

First, the measurement of digital transformation is refined. Following the approach of Zhao et al. (2021), digital transformation is remeasured along four dimensions: the application of digital technologies, the adoption of internet-based business models, the development of smart manufacturing, and the frequency of modern information systems usage. The corresponding results are reported in column (1) of Table 4.

Robustness to Variable, Sample, Model, and Policy Variations.

Second, the measure of EPU is adjusted. This study adopts the inter-provincial EPU index constructed by J. Yu et al. (2021) to capture firms’ perception of macro-level policy uncertainty. The results are presented in column (2) of Table 4. These findings remain consistent with the baseline results, confirming the robustness of the main conclusions.

Sample Adjustments

Next, the sample period is adjusted to address potential biases from major economic events. The 2015 stock market crash led to considerable volatility in the share prices of listed firms, which may have artificially increased the frequency of digital transformation-related disclosures in annual reports. Additionally, the COVID-19 pandemic introduced a range of political and economic interventions, creating confounding influences that may distort the estimation results. To mitigate these effects, observations from the years 2015 and 2020 are excluded. The estimation outcomes are reported in column (3) of Table 4.

Furthermore, to address potential industry-specific biases, firms operating in the software, information transmission, and information technology services sectors are removed from the sample. Given their intrinsic alignment with digitalization, firms in these industries may exhibit systematically different characteristics, which could distort the results. The corresponding findings are shown in column (4) of Table 4. The consistency of these results with the baseline model confirms the robustness of the core findings under alternative sample restrictions.

Alternative Model Specifications

To better address potential confounding effects from regional factors, this study incorporates time and region fixed effects to control for unobserved regional characteristics that vary over time. Robust standard errors are clustered at the firm level to ensure statistical reliability. The results, presented in column (5) of Table 4, remain consistent with baseline estimates, supporting the robustness of the conclusions.

Exogenous Policy Shock

In 2016, the Ministry of Industry and Information Technology selected 25 cities as national information consumption demonstration zones to promote upgrades in digital infrastructure and accelerate digital transformation. This policy is treated as an exogenous shock to local firms. Using 2016 as the implementation year, the corresponding regression results are presented in column (6) of Table 4. The consistent direction and significance of coefficients across this policy shock test further reinforce the reliability and external validity of the baseline results.

Alternative Estimation Methods

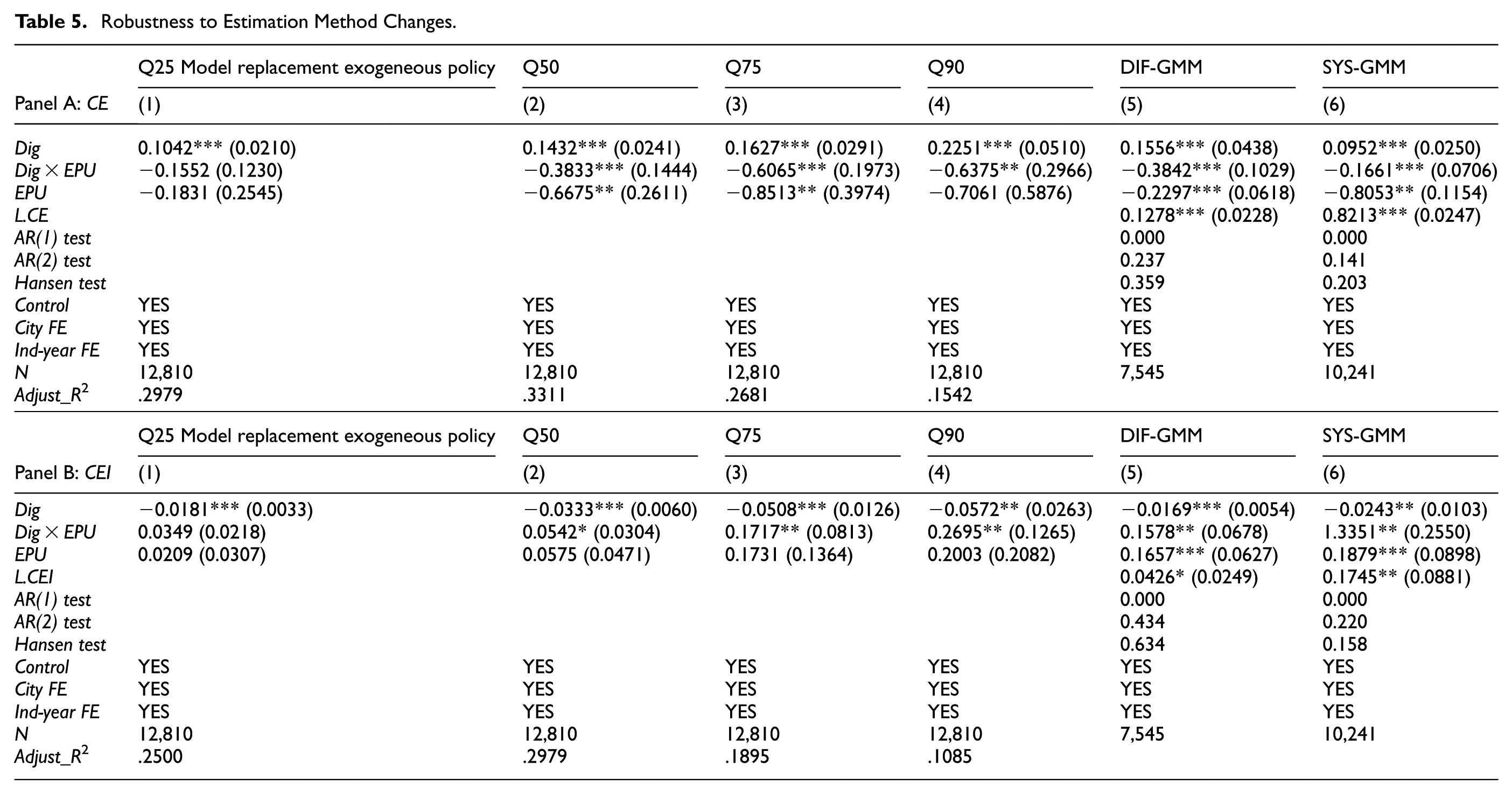

Given that OLS estimation is sensitive to outliers and may affect the robustness of the results, this study follows Koenker and Bassett (1978) and employs quantile regression as a robustness check. This method is less influenced by extreme values and performs better when the sample exhibits skewness or fat tails. As shown in columns (1) to (4) of Table 5, the estimates across different quantiles are consistent with the baseline results, supporting the robustness of the findings.

Robustness to Estimation Method Changes.

To further address potential dynamic characteristics and endogeneity issues, this study incorporates the lagged dependent variable and extends the model to a dynamic panel data framework for robustness testing. Both difference GMM and system GMM estimators are employed to ensure the reliability of the regression results. As reported in columns (5) and (6) of Table 5, the AR(1) test is significant while the AR(2) test is not, indicating the absence of second-order autocorrelation. The Hansen test supports the validity of the instruments. The coefficient on the lagged dependent variable is significantly positive, suggesting strong persistence in carbon emissions. Overall, the results are consistent with the baseline estimates, further confirming the robustness of the main findings.

Endogeneity Issues

This study recognizes that potential endogeneity may arise from both reverse causality and omitted variable bias. Firms with superior carbon performance are more likely to receive favorable policy support, such as government subsidies, tax incentives, or lenient environmental regulations, which in turn enhance their capacity to invest in and adopt digital technologies. This implies a potential reverse relationship, in which improved carbon performance may drive digital transformation, rather than digital transformation improving carbon outcomes. Additionally, unobserved factors such as managerial quality, firm-level development strategies, or broader economic conditions may simultaneously influence both carbon performance and digitalization progress, introducing estimation bias if left unaddressed.

To mitigate these concerns, the study employs the two-stage least squares (2SLS) method. Following the approach of Nunn and Qian (2014), an instrumental variable for digital transformation (IV1) is constructed by interacting the number of post offices in 1984 with the national internet penetration rate, capturing historical infrastructure endowment and its compatibility with digital adoption. In addition, drawing on Fisman and Svensson (2007), the average EPU perception among peer firms within the same industry, year, and province is used as an instrumental variable for firm-level EPU perception (IV2). Columns (1) to (3) in Table 6 include the instrumental variable for digital transformation, the instrumental variable for EPU, and their interaction term (IV3), respectively.

Endogeneity Issues.

Note. [] indicates the p-value, and {} indicates the critical value at the 10% level for the Stock-Yogo weak identification test.

Columns (4) and (5) report the second-stage results, which confirm that the effects of digital transformation and EPU on both total carbon emissions and carbon emission intensity remain consistent with the baseline regressions. The Kleibergen-Paap rk LM and Kleibergen-Paap Wald rk F-statistics indicate that the model does not suffer from problems related to under-identification, weak instruments, or over-identification, reinforcing the robustness of the instrumental variable approach.

Mechanism and Heterogeneity Tests

Mechanism Tests

The Production Expansion Effect of Enterprise Digital Transformation

To examine the mechanism through which digital transformation contributes to increased total carbon emissions via production expansion, this study uses two indicators: firm sales revenue and selling expenses. Considering the concept of cost stickiness, where costs tend to rise more rapidly during business expansion than they decrease during contraction, the expansionary effect of digital transformation is reflected not only in rising sales revenue but also in higher selling expenses. Therefore, both sales revenue (SR) and selling expenses (SC) are employed to comprehensively capture the production expansion mechanism.

As shown in columns (1) and (2) of Table 7, the coefficients on digital transformation are significantly positive at the 1% level, indicating that digital transformation significantly increases both sales revenue and selling expenses. These results confirm that production expansion serves as an important channel through which digital transformation leads to higher carbon emissions.

Mechanism Tests.

In addition, the coefficients of the interaction term between digital transformation and EPU are significantly negative. This finding suggests that economic policy uncertainty reduces the strength of the production expansion effect. When firms face elevated uncertainty, they tend to scale back capacity expansion and adopt a more cautious approach to production growth in order to manage potential risks. As a result, the increase in carbon emissions due to production expansion is also limited.5.1.2 The resource allocation optimization effect of enterprise digital transformation

The efficiency of resource allocation within firms reflects how proportionally and effectively various inputs and resources are utilized in the production process. In this study, the resource allocation mechanism is evaluated by assessing factor misallocation at the firm level. Specifically, labor misallocation (dist_l) and capital misallocation (dist_k) are used as proxies to capture the efficiency of a firm’s resource allocation.

Assuming that firms operate under a Cobb Douglas production function with constant returns to scale, labor and capital misallocation are calculated based on the following expressions, as shown in Equations 7 and 8:

Where

As shown in column (3) of Table 7, the coefficient of digital transformation is significantly negative at the 1% level, indicating that digital transformation reduces resource misallocation. This result confirms that improving resource allocation efficiency is an important channel through which digital transformation helps reduce carbon emission intensity. Furthermore, the interaction term between digital transformation and economic policy uncertainty is significantly positive at the 1% level, suggesting that rising policy uncertainty weakens the positive effect of digital transformation on resource allocation. When firms face heightened uncertainty, their willingness to invest in digital transformation declines, which slows the transformation process and limits its potential to enhance resource efficiency. As a result, the impact of digital transformation on reducing carbon intensity is significantly diminished.

The Green Technology Progress Effect of Enterprise Digital Transformation

The adoption of digital technologies enhances firms’ capacity to allocate resources efficiently toward green innovation, thereby motivating the development of environmentally sustainable technologies. In addition, green innovations often generate spillover effects that facilitate inter-firm and inter-industry diffusion of knowledge and technology. These spillovers accelerate the adoption and diffusion of green technologies, contributing to lower carbon emission intensity. To empirically assess this mechanism, the present study investigates the impact of digital transformation on green technological progress through two channels: green innovation and green technology spillovers.

Green Technology Innovation Effect

Patent counts are widely recognized as a comprehensive measure of a firm’s technological progress and innovation capacity from an output perspective. To more accurately capture green technological innovation, this study adopts two indicators: the number of green patent applications and the proportion of green patents. First, the natural logarithm of the total number of green patent applications, including both green invention patents and green utility model patents (Pat), is used to represent the output level of green innovation. Second, to control for unobservable heterogeneity and mitigate endogeneity concerns, a relative indicator is introduced: the proportion of green patents to total patent applications (Gre). Green patents are identified based on the International Patent Classification codes published in the Green Patent List by the World Intellectual Property Organization.

As shown in columns (4) and (5) of Table 7, the coefficients of Dig are significantly positive at the 1% level, indicating that digital transformation significantly enhances green technological innovation. This confirms that green innovation acts as an important mechanism through which digital transformation contributes to lower carbon emission intensity. Furthermore, the coefficients of the interaction terms Dig multiplied by EPU are significantly negative at the 1% level, suggesting that economic policy uncertainty weakens firms’ green innovation efforts. Under conditions of heightened uncertainty, firms tend to reduce investment in green and energy-efficient technologies, thereby limiting the ability of green innovation to reduce carbon emission intensity.

Green Technology Spillover Effect

To assess green technology spillovers, this study utilizes micro-geographical data on listed firms, green patent data, and a gravity model to construct a green technology spillover index. This index is used to test whether digital transformation enhances green technology spillovers, thereby reducing carbon emission intensity. The green technology spillover index is expressed as:

where Rj represents the R&D investment of firm j in a green industry; dfj represents the geographical distance between firm f and firm j. The stronger the spillover effect of green technologies from the surrounding green industries, the greater the firm’s ability to achieve green development and energy conservation.

As shown in column (6) of Table 7, the coefficient of Dig is significantly positive at the 1% level, indicating that digital transformation promotes green technology spillovers. Moreover, the coefficient of the interaction term Dig × EPU is significantly negative at the 1% level, confirming that EPU dampens the spillover effect of digital transformation. As perceptions of economic uncertainty rise, firms become less willing to engage in knowledge sharing and technology transfer, thereby diminishing the diffusion of green technologies and their effectiveness in reducing carbon emission intensity.

Heterogeneity Checks

Firm size Heterogeneity

In this study, firm size is proxied by total assets. Firms with total assets above the industry median in a given year are classified as large enterprises, while those below are classified as small and medium-sized enterprises (SMEs). Based on this classification, the sample is divided into two subsamples: large firms and SMEs. Table 8 presents the estimation results. The findings indicate that the effects of digital transformation on both increasing total carbon emissions and reducing carbon emission intensity are more pronounced among large firms than SMEs. Although no significant heterogeneity is observed in the impact of digital transformation on total carbon emissions across firm sizes, clear differences emerge with respect to carbon intensity. Large firms, due to their sustained investments in capital, labor, and technology, are better positioned to leverage digital transformation for improving carbon efficiency.

Firm Size Heterogeneity.

Furthermore, Table 8 shows that the moderating effect of EPU on the relationship between digital transformation and carbon performance also varies by firm size. The rationale is as follows: large firms, with stronger resource bases and more robust risk management capabilities, are better equipped to cope with uncertainties arising from policy volatility (Zhu & Qi, 2022). Although these firms may defer investments in non-core activities during periods of heightened policy uncertainty, they generally maintain long-term commitments to digital transformation and green technology development. Their substantial capital reserves and diversified financing channels provide greater flexibility in adapting to external shocks, enabling continued progress in reducing carbon intensity.

In contrast, SMEs are more susceptible to the adverse effects of EPU (Czarnitzki & Toole, 2013). With limited financial resources and weaker risk mitigation capacities, SMEs tend to prioritize short-term survival under uncertain policy conditions. As a result, they often scale back or delay investments in long-term digital transformation initiatives, especially those involving high costs related to green technologies. This decline in investment capacity hampers their ability to improve carbon efficiency through digital transformation, weakening its impact on carbon intensity reduction.

Industry Heterogeneity

For this study, firms are categorized into high-carbon and low-carbon industries based on the Ministry of Environmental Protection’s classification of heavily polluting sectors. Firms operating in heavily polluting sectors are classified as high-carbon industries, while those in other sectors are considered low-carbon. Table 9 presents the corresponding results. The findings reveal that digital transformation has a more pronounced effect in high-carbon industries, both in increasing total carbon emissions and in reducing carbon emission intensity. Due to their industry-specific characteristics, high-carbon industries possess greater potential to lower carbon intensity through digital transformation initiatives.

Industry Heterogeneity.

Additionally, Table 9 demonstrates that the influence of EPU varies considerably across industries. In high-carbon sectors, elevated EPU often leads to reduced investment in green technologies, thereby weakening the role of digital transformation in lowering carbon intensity. These industries are more vulnerable to policy fluctuations due to their dependence on high-emission production processes (Yang et al., 2022). Conversely, although firms in low-carbon industries may postpone digital transformation under policy uncertainty, the overall impact on emissions remains limited, given their already low emission levels. In such industries, digital initiatives are typically aimed at enhancing operational efficiency rather than reducing emissions. Investment priorities in response to policy uncertainty also differ by industry. During periods of heightened uncertainty, firms in high-carbon sectors often prioritize financial stability, deferring long-term investments in green technologies and digital transformation. In contrast, firms in low-carbon sectors are less affected, as their investments in digital transformation tend to be smaller in scale and less sensitive to policy fluctuations.

Regional Heterogeneity

For this study, China’s 31 provinces are classified into developed and underdeveloped regions based on indicators such as economic output, per capita GDP, industrial structure, and infrastructure development. The developed regions include Beijing, Shanghai, Guangdong, Jiangsu, Zhejiang, Tianjin, and Fujian. Based on this classification, the sample is divided into two subsamples.

As shown in Table 10, digital transformation in developed regions has a stronger effect on both increasing total carbon emissions and reducing carbon emission intensity compared to underdeveloped regions. Developed regions, which often serve as major production and export centers, generate considerable carbon emissions through their manufacturing activities, including emissions embedded in export goods. Moreover, the establishment and operation of data centers and digital infrastructure in these regions contribute significantly to carbon emissions. At the same time, developed regions possess greater research and development capacity and stronger technological innovation capabilities, enabling them to promote the development and adoption of green technologies. These technologies enhance energy efficiency and help reduce emissions during production, thereby lowering carbon emission intensity. Consequently, the effects of digital transformation on carbon performance show substantial variation across regions.

Regional Heterogeneity.

In addition, Table 10 illustrates that the impact of EPU on the carbon performance of digital transformation differs significantly between regions. Firms in developed regions generally have more sophisticated resource allocation systems and risk management mechanisms (B. Wang et al., 2024), which enable them to sustain digital transformation efforts even amid policy fluctuations. In contrast, firms in underdeveloped regions typically lack resilience to external shocks and are more likely to postpone or cut back on digital transformation investments during periods of uncertainty, especially in long-term green technology projects. This limits their ability to improve carbon performance. Furthermore, firms in developed regions tend to receive more policy support, such as government subsidies and tax incentives, while firms in underdeveloped regions often lack access to such resources (Chen & Guo, 2024; H. Zhang et al., 2023). These disparities further widen the regional gap in the effectiveness of digital transformation in improving carbon emission performance.

Conclusions

Conclusion

This study examines the impact of digital transformation on the carbon performance of China’s A-share listed firms from 2011 to 2023, with a focus on both total carbon emissions and carbon intensity. It also explores the moderating role of EPU. The empirical results indicate that digital transformation tends to increase total carbon emissions while simultaneously reducing carbon intensity. EPU acts as a negative moderator, dampening both the upward effect on total emissions and the downward effect on carbon intensity. Mechanism analysis reveals that digital transformation reduces carbon intensity by promoting green technological progress and improving resource allocation, while it contributes to higher total emissions through production expansion. Furthermore, EPU significantly weakens these mechanisms. Heterogeneity analysis shows that the positive effect of digital transformation on total emissions is generally consistent across firms, whereas its emission-reducing impact on carbon intensity varies. Specifically, digital transformation exerts a stronger effect in large firms, high-carbon industries, and economically developed regions—leading to both greater increases in total emissions and more significant reductions in carbon intensity. In contrast, the negative moderating effect of EPU is more pronounced in small firms, high-carbon industries, and less developed regions.

Policy Implications

Based on the findings, several policy recommendations are proposed:

First, the government should establish a dynamic dual control mechanism that addresses both total carbon emissions and emission intensity, thereby enhancing coordinated governance. As China enters the era of carbon peaking and neutrality, increasingly stringent carbon constraints demand an accelerated rollout of dual control systems. Environmental authorities should shift toward binding regulation of total emissions and improve quantitative carbon management to avoid the pitfalls of focusing solely on intensity reduction. Moreover, stronger inter-agency coordination is needed, with clear regulatory roles assigned to institutions such as the Ministry of Ecology and Environment, Ministry of Industry and Information Technology, and the National Development and Reform Commission. This will enhance the institutional coherence of carbon governance.

Second, a dual policy framework should be developed that integrates technological progress with energy transition to resolve the “carbon paradox” during the transformation phase. Digital transformation is a key enabler of green transition in Chinese enterprises. However, firms often face significant cost pressures in the early stages of transformation, leading to an urgent need to scale up production. This results in a temporary decoupling of rising total emissions and declining intensity. To address this, innovation-focused incentives should encourage firms to strengthen their technological capabilities and invest in green innovation. Simultaneously, green incentives should promote the optimization of factor allocation and improvement in resource efficiency. This approach will allow digital transformation to contribute simultaneously to technological upgrading and cleaner energy usage, thereby suppressing the growth in total emissions through enhanced reductions in intensity.

Third, policy stability should be prioritized to mitigate the adverse effects of EPU. Since EPU dampens the emission-reduction benefits of digital transformation, minimizing policy volatility is essential. Clear and consistent policies on environmental regulation, digital transformation, and green innovation will help maintain long-term investment confidence. In addition, the establishment of a policy uncertainty mitigation fund could offer transitional subsidies to enterprises whose digital projects are delayed due to policy shifts, helping ensure continuity in green technology development.

Fourth, a differentiated digital transformation support system should be designed based on firm-level heterogeneity. The carbon performance of digital transformation varies across firm types, industries, and regions, necessitating tailored policy responses. Governments should construct a tiered support framework that accounts for firm size, industry characteristics, and regional economic conditions. Large firms, emission-intensive industries, and leading enterprises in developed regions should receive priority support. This may include deploying real-time energy monitoring using IoT, applying blockchain for carbon tracking, and enhancing the dual control of total emissions and intensity. In less developed areas, pilot programs for digital transformation insurance funds targeting SMEs should be introduced, providing premium subsidies to firms facing transformation delays due to policy changes. This would reduce the long-term investment risks posed by regulatory uncertainty.

Limitations

While this study offers important insights into the relationship between enterprise digital transformation, carbon performance, and the moderating role of EPU, several limitations should be acknowledged.

First, the analysis is based on data from China’s A-share listed companies from 2011 to 2023. As such, the findings may not fully reflect the experiences of smaller or privately held firms, which are not publicly listed. These firms may face different constraints and opportunities in pursuing digital transformation and managing carbon emissions. Additionally, firm-level carbon emissions data are obtained from publicly available sources, which may limit the completeness and accuracy of the dataset.

Second, although this study considers both total carbon emissions and carbon intensity, it does not distinguish between direct and indirect emissions, nor does it account for potential emission offsets achieved through digital innovations. As a result, the analysis may not capture the full spectrum of carbon impacts associated with digital transformation.

Third, digital transformation is treated as a unified concept encompassing a range of technologies, including automation, artificial intelligence, and the Internet of Things. However, different types of digital technologies may have heterogeneous effects on carbon performance. Aggregating them into a single measure may obscure important variation in how specific technologies contribute to emission reductions or increases.

Future research should address these limitations by incorporating data from non-listed firms, disaggregating emissions by source, and examining the differentiated impacts of specific digital technologies. These directions will help build a more nuanced and comprehensive understanding of how digital transformation influences corporate carbon performance.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the Zhejiang Federation of Social Sciences Project [Project No. 2025N097], China.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data available on request from the authors.