Abstract

Previous literature shows mixed evidence on the effect of discretionary accruals and auditing on the cost of debt. We hypothesize that, in the SMEs setting, auditing can act as a substitute for accruals quality, and thus audits may mitigate the effect of discretionary accruals on the cost of debt. Using a sample of Spanish SMEs, we find that auditing is negatively related with the cost of debt, while higher discretionary accruals are related with a lower cost of debt. Nonetheless, this effect is lower than that one observed for audits. When considering the combined effect of both variables, the effect of discretionary accruals is replaced by that of auditing. These results suggest that, among SMEs, discretionary accruals do not have a relevant effect on the cost of debt when companies are audited, supporting the hypothesis that there exists a substitution effect between discretionary accruals and auditing.

Introduction

Previous literature shows that there exists a theoretical discussion about the effect of accounting quality on the cost of debt, which relies on the potential association between discretionary accruals and information risk, and the empirical evidence is mixed. In that sense, most of previous literature shows that companies reporting lower discretionary accruals have lower financing costs, what is theoretically supported by the hypothesis that discretionary accruals are associated with earnings management with opportunistic purposes and thus the information risk is increased (Bhojraj & Swaminathan, 2009; Carmo et al., 2016; Shen & Huang, 2013; Vander Bauwhede et al., 2015).

Nevertheless, some papers find that discretionary accruals are negatively related with the cost of debt (Aldamen & Duncan, 2013; Orazalin & Akhmetzhanov, 2019), what authors attribute to either a signalling role of discretionary accruals for performance information (Guay et al., 1996), or effective earnings management activities with opportunistic purposes (Orazalin & Akhmetzhanov, 2019). On the other hand, part of the previous research does not find a significant association between discretionary accruals and the financing cost (Gill de Albornoz Noguer & Illueca, 2007; Gray et al., 2009), what may be attributable to a lower relevance and credibility of accounting information, because of a closer monitoring and a privileged access to private information.

Closely related with accounting quality is the role of financial audits. Financial audits have the purpose of examining and assessing a company’s financial statements in order to guarantee that they are a fair representation of the company’s actual situation and performance. For this reason, audits are considered to improve their clients’ accounting quality, and audited financial statements are considered as more reliable and credible than the unaudited ones (Cassar, 2011). Indeed, prior literature has examined the relationship between auditing and the cost of debt, but it also shows mixed evidence: while some papers find that voluntary audits help companies to get upgrades in their financial ratings (Lennox & Pittman, 2011) and to reduce their financing costs (Kim et al., 2011), other studies do not find significant differences (Cassar et al., 2015; Huguet & Gandía, 2014).

In spite of the close association among auditing, accounting quality and the cost of debt, the empirical research examining how financial audits affect the association between discretionary accruals and the financing cost is rather scarce. To date, only Carmo et al. (2016) have examined if the effect of earnings quality on the cost of debt is different when companies are audited, and their results show that the effect of earning quality on the cost of debt is higher among audited companies, supporting the idea that financial audits increase the credibility of earnings quality, acting as complementary goods (Cassar, 2011; Kothari et al., 2010; Minnis, 2011). Nevertheless, we have to note that they assume the general view that discretionary accruals increase the information risk and are associated with a higher cost of debt. However, when discretionary accruals are associated with a lower cost of debt (Aldamen & Duncan, 2013; Orazalin & Akhmetzhanov, 2019), the effect of audits on the association between accounting quality and the cost of debt is an open question.

In that sense, we have to note that differences between the public and the private setting with regard to the motivation for earnings management activities, their risk structure or their financing opportunities, may affect the users’ perception of discretionary accruals and their effect on the cost of debt. In the Small and Medium Enterprises (SMEs) setting, we assume that companies use discretionary accruals with opportunistic purposes and they have a negative effect on the cost of debt because earnings management is effective in this setting. Under this view, and considering that the role of audits is guaranteeing the reliability of accounting information and lenders rely on their work, we hypothesize that audits and discretionary accruals may act as substitute goods, because lenders place more weight to the assurance role of auditors than to the information provided by the financial statements, and thus the effect of discretionary accruals is moderated by the effect of auditing. Therefore, the aim of this paper is to test whether audits affect the relationship between discretionary accruals and the cost of debt in the SMEs setting.

To do so, we use a sample of Spanish SMEs. The data have been collected from Orbis, and the sample is composed of 156,144 observations of audited and unaudited companies for the period 2013 to 2019. Controlling for other characteristics that affect the cost of debt, we perform a fixed-effects regression analysis in which we examine the effect of audits and discretionary accruals on the cost of debt. An interaction term between audits and discretionary accruals is also included to test whether audits have an effect on the association between discretionary accruals and the cost of debt. Several alternative measures of discretionary accruals are used to test the robustness of the results, and additional analyses are carried out to test differences based on the audit characteristics.

SMEs provide a unique setting to test the role of audits, because part of them are not required to be audited, so it lets us compare unaudited observations with audited ones (Huguet & Gandía, 2016; Kim et al., 2011), as well as the comparison of mandatory and voluntary audits. Moreover, the Spanish case is an interesting setting to examine the effect of audits and accruals quality on the private setting. Firstly, because of the relevance of SMEs in Spain (Huguet & Gandía, 2014); secondly, because of the relatively short tradition in the use of financial information and auditing (Carrera & Carmona, 2013), resulting in audits often not being demanded, but considered a legal obligation (Navarro & Martínez, 2004). For this reason, the role of audits in the Spanish SMEs setting is unclear, and more research is needed.

We find that auditing is negatively related with the cost of debt; results show that, in line with Aldamen and Duncan (2013), the association between discretionary accruals and the cost of debt is negative and thus companies with higher discretionary accruals have a lower cost of debt. These results support the hypothesis that SMEs use discretionary accruals with opportunistic purposes and these earnings management activities are effective, contributing to the reduction of the cost of debt. We also observe that audits have a negative effect on the cost of debt, and this effect has a more economically significant impact than that one observed for discretionary accruals. When we consider the combined effect of both variables, the effect of discretionary accruals is compensated by auditing, what suggests that, in the SMEs setting, discretionary accruals do not have a relevant effect on the cost of debt when companies are audited. These results suggest that, in the Spanish SMEs setting, auditing may act as a substitute good for discretionary accruals. Therefore, audits limit the use of discretionary accruals with opportunistic purposes in two ways: first, because audits restrict earnings management activities (Huguet & Gandía, 2016), and secondly, because the effect of earnings management on the cost of debt is not significant when SMEs are audited.

The paper contributes to the existing literature about the effects of auditing and earnings quality on the cost of debt in the following ways: first, the paper supports recent literature which questions the common view that higher discretionary accruals increase the firms’ cost of debt (Aldamen & Duncan, 2013; Orazalin & Akhmetzhanov, 2019). Secondly, it also extends the rather scarce evidence about the effect of auditing on the association between discretionary accruals and cost of debt (Carmo et al., 2016; Orazalin & Akhmetzhanov, 2019). In that sense, although Orazalin and Akhmetzhanov (2019) examine if the effect of earnings management on the cost of debt is affected by audit quality, they do not examine if there are differences among audited and unaudited companies. On the other hand, results complement those of Carmo et al. (2016) and contribute to the discussion about the role of audits on the credibility of accounting information, showing that auditing has a moderating effect on discretionary accruals when they have a negative association with the cost of debt. In that sense, this paper is the first one that provides insights into audits and accounting quality acting as substitute goods, rather than complementary goods, as they have been commonly treated in previous literature (Cassar, 2011; Kothari et al., 2010; Minnis, 2011). Finally, it extends previous research on auditing among private firms, and specifically among SMEs (Gandía & Huguet, 2018a; Sundgren & Svanström, 2013).

The rest of the paper is structured as follows: in Section 2 we develop our theoretical framework and describe the institutional setting; Section 3 is devoted to the description of the sample and research design; Section 4 reports the results of our analyses; and in Section 5 we present the conclusions and highlight the limitations of the study.

Theoretical Framework

Discretionary Accruals and the Cost of Debt: Information Versus Opportunism

Previous literature about the relationship between discretionary accruals and the cost of debt generally shows a positive association between them (Bharath et al., 2008; Bhojraj & Swaminathan, 2009; Shen & Huang, 2013; Vander Bauwhede et al., 2015). Its explanation relies on the expected effects of accounting quality on the cost of debt. In that sense, accounting quality is considered to reduce the information asymmetries and uncertainty for users (Arnedo et al., 2012; Minnis, 2011); therefore, increases in accounting quality reduce the information risk and hence the cost of debt. Considering that discretionary accruals have been commonly interpreted as a sign of low earnings quality, because of opportunistic earnings management, a positive association between discretionary accruals and information risk is expected, and thus higher discretionary accruals are associated with a higher cost of debt.

Nevertheless, some authors argue that discretionary accruals may have information content, and thus increase accounting quality and reduce the information risk faced by users (Francis et al., 2005; Guay et al., 1996). In that sense, Aldamen and Duncan (2013) find a negative association between discretionary accruals and the financing cost in a sample of public Australian companies. These results support the arguments by Guay et al. (1996) that discretionary accruals signal information about the performance and reduce information risk, compensating the positive effect of innate accruals.

In a more recent paper, Orazalin and Akhmetzhanov (2019) also find that higher discretionary accruals are negatively related to the cost of debt in a sample of listed companies from Kazakhstan. Their results are similar to those of Aldamen and Duncan (2013), but their conclusions are different: they consider that discretionary accruals are a consequence of earnings management activities, and thus their negative association with the cost of debt may imply that earnings management is effective.

Despite the empirical findings on the public setting, the literature on the private setting is rather scarce, with mixed evidence. Gill de Albornoz Noguer and Illueca (2007) do not find a significant relationship between accruals quality and the cost of debt in a sample of Spanish SMEs, results in line with those of Gray et al. (2009). The authors suggest that the lack of significance may be due to a matter of credibility of the accounting information, and thus banks prefer the use of alternative information sources. These results are different to those of Vander Bauwhede et al. (2015), who find a significantly negative association between accruals quality and the cost of debt in a sample of Belgian SMEs. In a more recent paper, Carmo et al. (2016) also find evidence of a negative relationship between earnings quality and the cost of debt.

We have to note that differences between the public setting and the private setting, which are more noticeable among SMEs, may affect both the use of discretionary accruals and the association between discretionary accruals and the cost of debt. With regard to the use of discretionary accruals, motivations for earnings management are different among public and private companies (Coppens & Peek, 2005). Among listed companies (Callao & Jarne, 2021), motivations for managing earnings upwards (executive compensation, capital market incentives purposes, debt covenants) seem to be stronger than motivations for managing earnings downward (political costs, taxation). Among private companies, however, agency conflicts between shareholders and managers are less common; furthermore, SMEs are inherently riskier and their financing opportunities are more limited, basically bank credit and supplier credit (Vander Bauwhede et al., 2015), so their main motivation for managing earnings upwards would be linked to debt capital. If this motivation is stronger than tax incentives for managing earnings downwards will depend on the influence of tax regulation on financial accounting (Coppens & Peek, 2005).

With regard to the association between discretionary accruals and the cost of debt, there are also differences among listed and private companies. While discretionary accruals among public companies may have a signalling value to reduce the information risk (Aldamen & Duncan, 2013; Cho et al., 2017), private companies would use them mostly with opportunistic purposes. Since the assessment of accounting quality is costly, private lenders prefer other mechanisms to reduce their information risk, such as relational banking, or asset pledges as collateral (Gill de Albornoz Noguer & Illueca, 2007). Under this view, discretionary accruals may help SMEs to feign a better performance and financial situation, thus contributing to a reduction on the cost of debt. Therefore, we formulate the first hypothesis as:

H1: There is a significantly negative association between discretionary accruals and the cost of debt on SMEs.

Auditing and the Cost of Debt

Auditors are considered to have a basic role to ensure the reliability and credibility of accounting information, because: (i) the revision process performed by auditors enhances the information reliability, reducing the information risk (Huguet & Gandía, 2016; Kausar et al., 2016) and (ii) the revision is carried out by an independent professional, who accepts responsibility for the verification of this information, and thus the credibility of accounting information is improved.

With regard to the effects of auditing on the credibility of accounting quality, that is, the “perceived” accounting quality, auditors assume an information role: audits, through the revision of the accounting information and the issuance of the audit opinion, ensure the reliability and integrity of the financial statements (Cassar, 2011; Cho et al., 2017; Dedman & Kausar, 2012; Kothari et al., 2010; Lou & Vasvari, 2013; Mansi et al., 2004). Cassar (2011) states that audited financial information is considered more reliable and credible than unaudited financial information, and Kothari et al. (2010) argues that, due to the incentives to manage accounting information, it would not be credible without the safeguard of audits. Moreover, Minnis (2011) states that audits help to “harden” the accounting information, which could be considered rather subjective without the revision carried out by auditors.

Considering this information role, previous literature has tested whether audits help to reduce financing costs, and results are mixed. Kim et al. (2011) and Minnis (2011) find that voluntarily audited companies have a lower financing cost of debt as compared to unaudited companies. On the contrary, Allee and Yohn (2009) and Cassar et al. (2015) do not find a significant association between audits and the financing cost, while Huguet and Gandía (2014) only find a significant effect for mandatory audits, suggesting that differences in the financing cost between unaudited and audited firms are associated with a “punishment” for those firms that avoid the audit requirement, instead of a “reward” for those firms that decide to be voluntarily audited. Since we expect that audits, through their information role, help to reduce information risk and the cost of debt, we formulate the second hypothesis as:

H2: The cost of debt for audited SMEs is significantly lower than the cost of debt for unaudited SMEs.

Combined Effect of Auditing and Discretionary Accruals on the Cost of Debt: Strengthening Versus Moderating Effect

Examining the combined effect of auditing and discretionary accruals lets us the opportunity to test whether the association between discretionary accruals and the cost of debt is different for audited and unaudited companies. We can expect either a strengthening or a moderating effect. On the one hand, we have to note that auditors provide additional credibility to financial statements, and thus lenders may place more weight on accruals information when estimating the interest rate. Therefore, considering that discretionary accruals are negatively related with the cost of debt, the effect of discretionary accruals on the cost of debt should be more pronounced among audited companies, so discretionary accruals and audits would act as complementary goods.

On the other hand, audits may have a moderating effect on the association between discretionary accruals and the cost of debt, rather than a strengthening one, to the extent that auditing and discretionary accruals can be considered as substitute goods. In that regard, we have to note the differences on the motivations and usefulness of discretionary accruals among public and private companies that we have stated in Section 2.1: since accounting quality is costly to assess, lenders in the private setting place more weight on other alternative information sources that may reduce information risk (Gill de Albornoz Noguer & Illueca, 2007), audits among them.

In this line, lenders may consider audits as a guarantee, being more relevant than the information provided by the financial statements, and the effect of discretionary accruals is moderated, if not replaced, but the effect auditing. Consequently, audits would act as a substitute good for discretionary accruals in the SMEs setting. If this is true, SMEs could reduce their cost of debt choosing between two clashing accounting decisions: (i) using discretionary accruals with opportunistic purposes or (ii) opting to be audited, what both limits the SMEs’ ability to manage earnings because of the audit work (Huguet & Gandía, 2016) and the effect of earnings management on the cost of debt.

Therefore, since we expect that they are substitute goods, and thus audits have a moderating effect on the association between discretionary accruals and the cost of debt, we formulate our third hypothesis as:

H3: The effect of discretionary accruals on the cost of debt for audited SMEs is lower than the effect of discretionary accruals on the cost of debt for unaudited SMEs.

Institutional Context: Accounting and Auditing in Spain

The hypotheses we have formulated in the previous Sections depend on the institutional context that affect the role of both accounting and auditing. In that regard, the SMEs setting provides a unique setting to test the role of audits, because part of them are not required to be audited, a comparison that is not possible when examining listed companies or large private companies (Huguet & Gandía, 2016; Kim et al., 2011).

Furthermore, the Spanish case provides an interesting to examine the effect of audits and accruals on the private setting. Besides the relevance of SMEs in the Spanish economy, we have to note the institutional features that affect the use of accounting information. First, Spain is a code-law country characterized by a less-developed stock market, more concentrated structures and a bank-oriented financial system (García-Teruel et al., 2014a). These characteristics involve that the main agency conflict is that between shareholders and creditors; given the preference for other alternative information sources by lenders, the role of accounting information seems to have less relevance (Gill de Albornoz Noguer & Illueca, 2007).

With regard to accounting in Spain, the promulgation of the Decree 1514/2007 that approved the 2007 General Accounting Plan involved an in-depth reform of Spanish General Accepted Accounting Principles (GAAP), whose purpose was the convergence towards the International Financial Reporting Standards (IFRS) in the preparation of the individual financial statements, although significant differences exist between them yet (Gandía & Huguet, 2018b). If this reform has involved a higher relevance of accounting information is an open question: although several authors have examined the effect of accruals quality on the financing structure (García-Teruel et al., 2010, 2014a, 2014b) and the cost of debt (Gill de Albornoz Noguer & Illueca, 2007) among Spanish SMEs, these studies use samples from the years previous to the accounting reform.

Regarding the Spanish auditing environment, and similarly to the rest of the European Union (EU), private companies have to be audited when they exceed a certain size for two consecutive years. In that sense, The Directive 2013/34/EU states that small companies (i.e., companies which on their balance sheet dates do not exceed at least two out of the following thresholds: €4,000,000 for the total assets; €8,000,000 for the net turnover; and 50 employees) are not required to be audited. However, Spain, like most EU countries, applies lower Statutory Audit Thresholds (SAT): companies are mandatorily audited by size when they meet two out of the following criteria: €2,850,000 for total assets; €5,700,000 for net turnover; and 50 employees. Therefore, an important number of Spanish SMEs, which are considered small companies under the Directive, are required to be audited.

It is worth noting that Spain does have a relatively short tradition in the use of financial information and auditing (Carrera & Carmona, 2013), resulting in audits often not being demanded, but considered a legal obligation (Navarro & Martínez, 2004). Therefore, the role of audits in the Spanish SMEs setting is unclear, and more research is needed.

Empirical Study

Sample and Descriptive Statistics

Financial data have been gathered from ORBIS, while auditing data have been collected from SABI. The sample period runs from 2011 to 2019. First, we select private Spanish companies which are below at least two out of the three following thresholds: €20 million in total assets, €40 million in turnover and 250 employees. These limits coincide with those established by the Directive 2013/34/EU to consider a company is medium-sized. We use this restriction to reduce differences in the company size and thus to get a more homogeneous sample than if we had included larger companies.

Moreover, in order to get a more homogeneous sample with more comparable accounting numbers, we exclude the observations of micro-firms as defined by Directive 2013/34/EU (companies that do not meet two of the following thresholds: (i) €350,000 in total assets; (ii) €700,000 in net turnover; and (iii) less than 10 employees). We also exclude observations from companies having unlimited liability, firms from the financial and insurance industries, and companies with share participation by public entities. After these exclusions, the original sample is composed of 442,260 observations from 44,226 companies. Observations that have no information to calculate the cost of debt as explained in Section 3.2 are eliminated, so the sample is reduced to 285,465 observations. The calculation of discretionary accruals and the rest of control variables, which are one period lagged with regard to the cost of debt, reduces the sample to 227,766 observations. Finally, after trimming the continuous variables, the final sample is composed of 156,144 observations from 33,310 companies for the period 2013 to 2019.

We have to note that, as explained in Section 2.4, Spanish SAT are lower than those established by the Directive 2013/34/EU. Since the Spanish SAT are lower than our selection sample criteria, the sample includes companies above SAT (which have the audit requirement) and companies below SAT (which does not have the audit requirement because of size) and companies above Spanish SAT (i.e., required to be audited).

Panel A of Table 1 shows that the final sample has 156,144 firm-year observations from 33,310 companies, with 29,259 observations from audited companies (3,775 below SAT and 24,704 above SAT and thus mandatorily audited because of size), and 126,885 observations from unaudited companies (123,525 of them are from observations below SAT and 864 are observations from companies that breach the audit requirement). Given that firms must meet the SAT for two consecutive years, 3,276 observations (780 from audited companies and 2,496 from unaudited companies) are not classified in either range.

Sample Distribution by Audit Status.

Table 2 shows the descriptive statistics of the continuous variables, which are defined in Section 3.2. We can see that audited companies have on average a lower cost of debt than the unaudited ones; they also report higher absolute discretionary accruals, are larger and more profitable, have more leverage and less liquidity and tangibility, have a lower growth and a lower solvency ratio, but they have a higher interest coverage and are older.

Descriptive Statistics of Continuous Variables.

Research Design

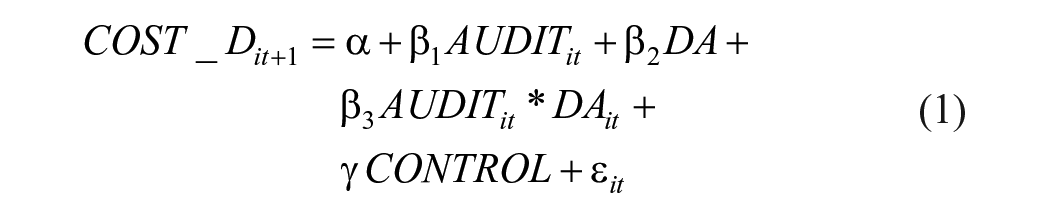

In order to test our hypotheses, we use the following regression model:

The dependent variable is the cost of debt (COST_D). Given that the cost of debt is not directly observable, we use the ratio of interests paid to the average financing debt between the beginning and the end of the period. Although this definition is commonly used in the literature, its use involves several limitations (Cassar, 2011; Huguet & Gandía, 2014). Firstly, this definition is a noisy proxy because it considers the average debt instead of specific loans. Although this limitation is hardly avoidable because of the lack of information, it can be mitigated by the elimination of outliers, thus we trim the variable in percentiles 5 to 95 (Vander Bauwhede et al., 2015).

On the other hand, we have to note that part of the observed interest rate is due to past contracts. In order to mitigate this problem some authors include the same variable lagged one period as a control variable (Cano Rodríguez et al., 2016; Huguet & Gandía, 2016), but problems with this inclusion may arise when using fixed-effects estimations (Angrist & Pischke, 2009; Nickell, 1981). For this reason, we do an additional analysis by including the cost of debt lagged one period.

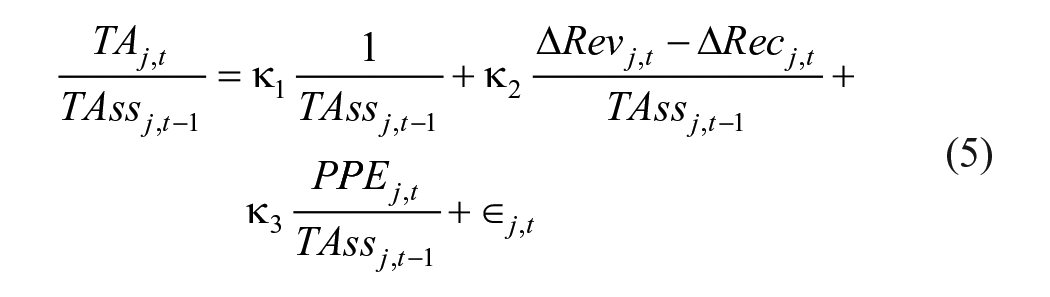

Model (1) includes DA as our measure of discretionary accruals, which we use to test Hypothesis 1, that is, the effect of discretionary accruals on the cost of debt. Considering the hypothesis that discretionary accruals are used with opportunistic purposes and are effective to reduce the cost of debt, we expect a negative coefficient for DA. The discretionary accruals models assume that accruals that are not explained by innate factors are a measure of the level of earnings management. We estimate discretionary accruals using the Jones Model (1991), which is one of the most common measure used in previous literature.

As we can see in equation (2), Jones (1991) classify accruals into non-discretionary accruals (NDA) and discretionary accruals (DA). NDA depends on two components (equation 3): (i) the growth of the sales (ΔRev), which controls for short-term accruals and (ii) the amount of Property, Plant and Equipment (PPE), which controls for the long-term accruals. Discretionary accruals are calculated as the difference between total accruals and non-discretionary accruals (equation 4). Although previous literature has commonly employed the absolute value of this measure (|DA|), some studies (Dedman & Kausar, 2012; De Fuentes & Porcuna, 2019; Francis & Wang, 2008; Tsipouridou & Spathis, 2012) use the signed discretionary accruals. In that sense, we have to note that auditors have preference for accounting choice that decrease earnings over those choices that increase earnings (Choi et al., 2010; Gandía & Huguet, 2020), so we regress the model using both the absolute and the signed measure. Moreover, we also regress the model separately for positive and negative accruals. On the other hand, in order to test if results are sensitive to the discretionary accruals measure, we do an additional analysis using for alternative measures, whose results are reported in Section 4.3

Model (1) also includes AUDIT, a dummy which equals 1 when companies are audited and 0 otherwise. This variable is used to test Hypothesis 2. We expect a negative association between AUDIT and COST_D. We have to remark that SABI may present some problems with the identification of audited companies (Huguet & Gandía, 2014): blank data may be either unaudited observations or missing values, and thus some audited observations may be erroneously considered unaudited. To overcome this limitation, we replace some of these “blank data” observations to “audited” observations with the following procedure (Huguet & Gandía, 2014, 2016): considering that the shortest auditor tenure in Spain is 3 years, if: (a) a company is audited in t − 1 and t + 1 and (b) is above the statutory audit thresholds in t, we consider the company is audited in t. After the implementation of this procedure, 926 “blank data” observations were replaced by “audited” observations.

Finally, in order to test Hypothesis 3, we also include the interaction term between AUDIT and DA. According to the theoretical framework from Section 2.3, two effects can be expected from this interaction: a strengthening effect of auditing on the association between the cost of debt and accruals, and a moderating one. With regard to the strengthening effect, we should expect the coefficient of the interaction to have the same sign as DA, to the extent that the effect of discretionary accruals on the cost of debt should be more pronounced when companies are audited.

Nevertheless, a moderating effect may be observed instead of a strengthening one, since auditing would act as a substitute good for discretionary accruals and thus the effect of discretionary accruals on the cost of debt may be mitigated when companies are audited. Therefore, the coefficient of the interaction should have the opposite sign of DA: if the coefficient of DA was negative, the interaction term would mitigate its effect, thus auditing would replace the effect of DA.

The Model includes a set of control variables used in previous empirical research. In line with previous literature (Huguet & Gandía, 2014; Kim et al., 2011), the test and control variables are lagged one period with regard to COST_D. Firstly, as larger firms are considered to bear a lower risk than the smaller ones, reducing the cost of debt (Gill de Albornoz Noguer & Illueca, 2007; Vander Bauwhede et al., 2015), company size (LNASS) is included. Also, more profitable firms are expected to have a lower cost of debt (Kim et al., 2011), so we include ROBA in order to control for firm profitability. With regard to the leverage, Huguet and Gandía (2014) document a non-linear effect on the cost of debt, so we also include leverage (LEV) and its squared term (LEV_SQ). More liquid companies are expected to have a lower information risk, so we include the liquidity ratio (LIQ) to control for its negative association with the cost of debt (Cano Rodríguez & Sánchez Alegría, 2012; Lennox & Pittman, 2011). Moreover, a higher level of PP&E is expected to be negatively related with COST_D (Kim et al., 2011), thus we include TAN, which we defined as the ratio of Property, Plant, and Equipment (PP&E) to total assets.

We include company growth (GROWTH) to control for its potential effects on the financing cost (Cano Rodríguez & Sánchez Alegría, 2012). We also include the solvency ratio (SOLV) to control for financial problems affecting the cost of debt. The interest coverage ratio (COV) is included to control for its negative association with COST_D (Francis et al., 2005; Lennox & Pittman, 2011). Additionally, since older companies are considered less risky, we include the age of the company (AGE) (Lennox & Pittman, 2011; Pittman & Fortin, 2004; Vander Bauwhede et al., 2015). Finally, year dummies are included to control for unobserved and time-specific effects common to all the companies.

In line with other audit-based studies, we have to note the potential endogeneity problems related with OLS estimations (Huguet & Gandía, 2014). Although previous literature has used the Heckman approach (Cano Rodríguez et al., 2016; Pittman & Fortin, 2004), recent papers show that its results lack on robustness, and they are even more unreliable than OLS estimations (Clatworthy et al., 2009; Larcker & Rusticus, 2010; Lennox et al., 2012). For this reason, we use a (firm) fixed-effects estimation (FE), which has been suggested by Francis (2011), Lennox et al. (2012), and Wintoki et al. (2012), and it has been used in previous literature (Huguet & Gandía, 2014, 2016; Karjalainen, 2011; Kim et al., 2011). On the other hand, the fact that test and control variables are lagged on period can also mitigate endogeneity problems (Wintoki et al., 2012).

Empirical Results

Main Results

In this Section we present the results of the main analysis. First, Table 3 shows the correlation matrix in order to examine potential multicollinearity problems. A high value is also observed for the correlation between AUDIT and LNASS (.5955), which is due to the fact that most of the audited observations belong to the mandatory setting, that is, they are mandatorily audited because of size. High correlations are also present between LIQ and SOLV (.6692) and between ROBA and COV (.3042), which are partially explained by the estimation of these variables, with common components. Nevertheless, the correlations are below .80; following Firth (1997), we do not expect collinearity problems.

Correlation Matrix.

Note. Coefficients in bold denote statistical significance at 5% level.

We then run the regression model. Table 4 reports the results obtained. Column 1 reports the results when using |DA|, whereas Column 2 shows the results using signed DA; Columns 3 and 4 shows the separate regressions for positive and negative DA (+DA and −DA). Although the R2 seem somewhat lower, we have to note that we have used a FE estimation, and thus they correspond to the within-R2. On the other hand, regarding the significance of the control variables, with the exception of TAN when using +DA, and COV in the −DA regression, all the control variables are highly significant.

Fixed-Effects Regression Results.

Note. Table 4 reports the FE regression results of the main analysis. Coefficients of year dummies are not included for parsimony. ***, **, and * denote statistical significance at 1%, 5%, and 10% level.

With regard to Hypothesis 1, we can observe in Column 1 that the coefficient of DA is significantly negative; the coefficient remains significantly negative when using signed DA. Although results are contrary to those of Vander Bauwhede et al. (2015), results are in line with Aldamen and Duncan (2013) and Orazalin and Akhmetzhanov (2019), who find a significantly negative association between discretionary accruals and the cost of debt in a sample of public companies. When we separate positive and negative accruals, we can observe that the coefficient of +DA is significantly negative, while become insignificant for −DA. Results support Hypothesis 1 and suggest that users consider that the use of discretionary accruals with opportunistic purposes is effective when companies use them to manage earnings upwards, that is, they achieve to feign a better performance and financial position. The lack of a significant effect of −DA may be due to the use by lenders of other mechanisms to reduce their information risk, such as relational banking, or asset pledges as collateral (Gill de Albornoz Noguer & Illueca, 2007), which compensate the potentially negative signal of −DA.

Regarding Hypothesis 2, we can see that AUDIT is significantly negative in the four regressions, the sign of the coefficient being in line with previous studies (Huguet & Gandía, 2014; Kim et al., 2011). These results support our Hypothesis and suggest that audits help to reduce the information risk faced by users. Nevertheless, examining whether this effect is homogeneous among audits, regardless the audit characteristics (voluntary/mandatory audit, auditor size, audit fees, audit opinion) is an open question, which we examine in Section 4.6.

Finally, with regard to Hypothesis 3, results show that the interaction term between AUDIT and |DA| is significantly positive; results remain significant when using +DA but are not significant for signed DA and −DA. Considering that results for signed DA may be affected by those for −DA, it seems that the potential effect of using discretionary accruals with opportunistic purposes (managing earnings upward in order to reduce the cost of debt) is mitigated by its interaction with AUDIT. This suggests that, in the SMEs setting, the benefits of managing earnings on the cost of debt are limited by audits. Considering that, as shown by previous literature, audits restrain earnings management activities among SMEs (Huguet & Gandía, 2016), these companies can reduce their cost of debt choosing between two clashing accounting decisions: using discretionary accruals (which impair accounting quality) or opting to be audited (that limits their ability to manage earnings and improves accounting quality). We explore in more detail how differences between audited and unaudited SMEs affect the impact of discretionary accruals on the cost of debt in Section 4.5.

Inclusion of the Cost of Debt Lagged One Period

Cassar (2011) states that the cost of debt measure suffers from staleness, in the sense that part of the observed cost of debt is due to past contracts. The inclusion of the variable lagged one period as an additional control variable in the regression model helps to mitigate this limitation (Cano Rodríguez et al., 2016; Huguet & Gandía, 2014). Since the use of lagged variables in fixed-effects estimations is not recommended (Angrist & Pischke, 2009; Nickell, 1981), we do an additional analysis running OLS regressions which include the cost of debt lagged one period. Results are reported in Table 5. Results show that the R2 is higher than those shown in Table 4, what is due for two reasons: (i) the use of OLS estimations rather than FE estimations and (ii) the inclusion of COST_D lagged one period as a control variable.

OLS Regression Results (Inclusion of COST_D_LAG).

Note. Table 5 reports the OLS regression results after including COST_D_LAG. Coefficients of year and industry dummies are not included for parsimony. ***, **, and * denote statistical significance at 1%, 5%, and 10% level.

We can see that the variable is significantly positive and has a high economic significance, suggesting the importance of previous debt contracts on the cost of debt, as stated by previous literature (Cano Rodríguez et al., 2016; Cassar, 2011). With regard to the test variables, the sign and significance of their coefficients remain unchanged for |DA| and +DA; when using signed DA, the coefficient of AUDIT remains significant at 10% level, and it only becomes insignificant when using −DA. Considering results as a whole, they are in line with those from Section 4.1: increasing discretionary accruals and audits are effective to reduce the SMEs’ cost of debt, having a compensatory effect between them; however, when discretionary accruals are negative, neither accruals nor audit have an effect on the cost of debt, what can be due to the use of other mechanisms by lenders.

Alternative Discretionary Accruals Measures

To test if results are sensitive to the measure of discretionary accruals we used, we do an additional analysis using four alternative measures. First, we use the Modified Jones Model (Dechow et al., 1995). This model, which has been used in recent literature (De Fuentes & Porcuna, 2019; Houqe et al., 2017; Orazalin & Akhmetzhanov, 2019), assumes that changes in credit sales result from earnings management activities (equation 5):

Secondly, we also use the model proposed by Dechow and Dichev (2002) modified by McNichols (2002). In this model, as shown in equation (6), accruals depend on cash flow from operations in years t – 1, t, and t + 1, as well as the change in sales, and PPE; therefore, this model is a combination of the Jones Model and the Dechow-Dichev Model (Carmo et al., 2016; Francis et al., 2005).

We also use two measuressss not based in the Jones Mode, particularly those used by DeFond and Park (2001) and Francis and Wang (2008). DeFond and Park (2001) use a linear model in which abnormal short-term accruals are calculated as the difference between short-term accruals and predicted accruals, which depend on a firm’s prior year ratio of current accruals to sales (equation 7). Francis and Wang (2008) complement this model by including the long-term component via the prior year’s ratio of depreciation to PPE (equation 8).

Table 6 shows the results for these alternative measures, and results are qualitatively similar to those reported in Section 4.1.

Alternative Discretionary Accruals Measures.

Note. Table 6 reports the FE regression results of Model (1) using alternative discretionary accruals measures. Coefficients of year dummies are not included for parsimony. ***, **, and * denote statistical significance at 1%, 5%, and 10% level.

Non-Discretionary Accruals and Cost of Debt

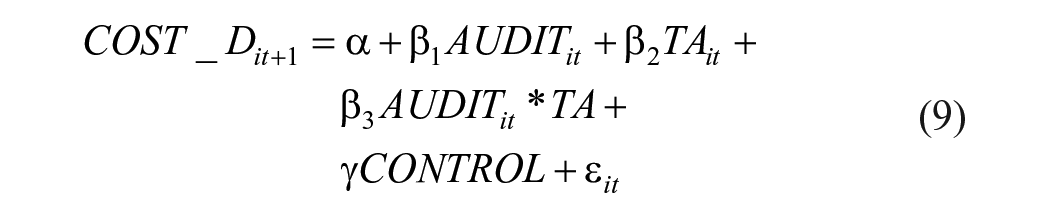

Although our main analysis is focused on the effect of discretionary accruals on the cost of debt, we have to note that the innate component of accruals may have also an effect. In order to explore the association between accruals and the cost of debt, we introduce the following modifications to Model (1):

Where TA refers to total accruals, and NDA refers to the estimated non-discretionary accruals using the Jones Model. As in Section 4.1, we use both signed DA and |DA|. Results are reported in Table 7. With regard to TA, we can see in Column 1 that its coefficient is significantly negative, but the interaction does not have a significant effect. With regard to NDA, as we can see in Columns 2, 3, and 4, its coefficient is significantly positive and has a higher impact than that of DA. These results are consistent with previous literature (Francis et al., 2005; Gray et al., 2009), and are consistent with the hypothesis that higher innate accruals increase information risk. In that sense, the negative coefficient of the interaction between NDA and AUDIT balances out the effect of innate accruals, suggesting that audits help to improve innate accruals credibility, and thus contribute to reduce the cost of debt. Finally, with regard to DA and its interaction with AUDIT, results remain qualitatively similar to those reported in Section 4.1.

Non-Discretionary Accruals and Cost of Debt.

Note. Table 7 shows the results of the FE regression considering the role of non-discretionary accruals. Coefficients of year dummies are not included for parsimony. ***, **, and * denote statistical significance at 1%, 5%, and 10% level.

Audit Versus No Audit

In order to examine the differences among audited and unaudited companies about the effect of discretionary accruals on the cost of debt, we exclude AUDIT and the interaction terms from Models (1) and (11) regress them separately for audited and unaudited companies, to assess if the effect of discretionary accruals on the cost of debt is different depending on the company is audited. Results are shown in Table 8 Panel A. We can see that although both DA and NDA are significant, the magnitude of their coefficients is higher for the sample of unaudited companies, being the difference statistically significant. These results show that audits have a moderating effect on the association between accruals and the cost of debt, thus supporting results from Section 4.1.

Audit Versus No Audit.

Note. Table 8 shows the results of separate regressions for unaudited and audited companies. Coefficients of year dummies are not included for parsimony. ***, **, and * denote statistical significance at 1%, 5%, and 10% level.

Audit Characteristics

As we explained in Section 4.1, the effect of audits on the cost of debt may depend on the audit characteristics. In order to assess how these audit characteristics may affect the association between discretionary accruals and the cost of debt, we do an additional analysis in which we include audit variables to Model (1) and regress it on the subsample of audited companies. The audit characteristics that we include in the Model are the following: the auditor size (Cano, 2007), auditor fees (Gandía & Huguet, 2021), the audit opinion (Karjalainen, 2011, and the voluntary/mandatory character of the audit (Huguet & Gandía, 2014).

The auditor size is proxied by two variables (Gandía & Huguet, 2018a; Sundgren & Svanström, 2013): LARGE, which equals 1 when a company is audited by Middle-Tier or Big 4 auditors; and BIG, a dummy which equals 1 when a company is audited by a Big 4 auditor (Cabal-García et al., 2019). In line with previous research (Boone et al., 2010; Sundgren & Svanström, 2013), we have considered BDO and Grant Thornton as Middle-Tier auditors. LARGE captures the differences between large auditors, while BIG captures the differences between Big 4 and Middle-Tier auditors. LNFEES is the natural logarithm of the audit fees paid by the companies. The auditor opinion is proxied by MOD, which equals 1 when the report has a modified opinion and 0 otherwise. Finally, we include VOL as a proxy for voluntary audits, which equals 1 when a company is below SAT and thus a priori voluntarily audited, and 0 when is above SAT and thus required to be audited by size.

We also include the interaction term of these variables with DA in order to test if the association between DA and COST_D is affected by the audit characteristics. We have to note that the effect of these audit characteristics on the cost of debt has been examined by Gandía and Huguet (2021), but they do not take into account the interaction of these characteristics with accruals information. Results are reported in Table 9. We can see that the sample is reduced as compared to the sub-sample of audited companies we use in Section 4.5, what is due to the availability of data regarding to audit fees. As we can see, DA is not significant when we examine the sample of audited companies, what is in line of auditing acting as a substitute good for discretionary accruals.

Audit Characteristics.

Note. Table 9 shows the FE regression results of Model (1) after the inclusion of audit characteristics, in a sample of audited SMEs. Coefficients of year dummies are not included for parsimony. ***, **, and * denote statistical significance at 1%, 5%, and 10% level.

With regard to the audit variables, we can see that only LARGE and LNFEES are significantly negative, what is in line with Gandía and Huguet (2021), showing that lenders value both the auditor choice and the signalling effect of audit fees to discriminate audit quality.

Conclusions

Previous literature on earnings management and accounting quality shows that there is a discussion on the effect of discretionary accruals on the cost of debt, with mixed empirical evidence. These mixed results are also present when examining the effect of auditing on the cost of debt (Allee & Yohn, 2009; Huguet & Gandía, 2014; Kim et al., 2011; Minnis, 2011). A potential explanation for the mixed evidence about the effect of earnings quality and auditing on the cost of debt is that few studies have considered their combined effect (Carmo et al., 2016). We have to note that differences between the public and private setting, and specially SMEs, with regard to the motivation for earnings management, their risk structure and their financing opportunities may affect the association between discretionary accruals and the cost of debt. In that sense, we hypothesize that discretionary accruals are used with opportunistic purposes in the SMEs setting, and auditing can act as substitutive goods, so the effect of discretionary accruals on the cost of debt is different among audited and unaudited companies.

Using a sample of Spanish SMEs, we find that discretionary accruals are negatively associated with the cost of debt, suggesting that managing earnings upwards is effective to reduce the financing costs. We also find that audited SMEs have a lower cost of debt than unaudited SMEs. Moreover, the interaction term between auditing and discretionary accruals shows a positive coefficient that compensates the effect of discretionary accruals, suggesting that audits and discretionary accruals may act as substitute goods in the Spanish SMEs setting. When we decompose the sample into positive and negative discretionary accruals, we can observe an asymmetric effect of discretionary accruals: companies that report increasing discretionary accruals have a lower cost of debt, while there is not a significant effect when using negative discretionary accruals. The lack of a significant effect for discretionary accruals may be due to the use by lenders of other mechanisms to reduce the information risk, such as relational banking or assets pledges. Results are robust to the use of other discretionary accruals measures and the inclusion of the cost of debt lagged one period as an additional control variable. Furthermore, an additional analysis considering non-discretionary accruals show that they have a positive effect on the cost of debt while discretionary accruals remain significant, what is in line with previous literature (Francis et al., 2005; Gray et al., 2009).

On the other hand, in order to examine in more detail de effect of auditing on the association between discretionary accruals on the cost of debt, we carry out separate regressions for audited and unaudited companies and find that the effect of discretionary accruals on the cost of debt is higher among unaudited companies, supporting our main analysis. Finally, we examine if the audit characteristics have an effect on the cost of debt, as well as if the effect of discretionary accruals is affected. Although auditor size and audit fees have a significant effect on the cost of debt, we do not find that the audit characteristics influence the association between accruals and the cost of debt.

The paper presents some limitations: first, audit-based studies may be affected by endogeneity issues. We have tackled them by using fixe-effects regressions, but these estimations cannot completely solve the endogeneity problems when the relationship between the dependent variable and the test variables is bidirectional. We have partially solved this concern using lagged values for the test and control variables, the dependent variable itself among them. Another problem is related with the comparability between the audited and unaudited companies, which we have tried to mitigate by focusing on these defined as SMEs. A last problem is related with the estimation of the discretionary accruals measure, which may involve errors of measure. In order to test the robustness of our results, we have used alternative measures, and they show similar results.

The study involves several implications for regulators and practitioners in the context of SMEs. For regulators, given that audits show that have a moderating effect on discretionary accruals with opportunistic purposes, and that previous literature has shown that audits are effective to deter earnings management activities (Huguet & Gandía, 2016), they should consider if the definition of mandatory audits should be revisited. With regard to the practitioners, given the conflict that may arise between auditing and the use of discretionary accruals, not only on the own use of them, but also on their effects, they should consider the other potential negative (positive) effects that discretionary accruals (auditing) have on their performance.

The paper presents several opportunities for future research. Firstly, the substitute effect of auditing on discretionary accruals should be examined in other companies belonging to the private setting, but larger than SMEs, to study if this effect is not only applicable to small firms but extensible to private companies. With regard to public companies, since differences between audited and unaudited companies cannot be examined, because all of them are audited, the analysis should be focused on differences among auditor characteristics other than the auditor size, in order to analyze if these characteristics affect the impact of discretionary accruals on the cost of debt.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors gratefully acknowledge the financial contribution of the Conselleria d’Innovació, Universitats, Ciència i Societat Digital (researchproject GV/2021/092).