Abstract

This study aims to investigate the mechanism for the combined influence of brand, quality, and corporate social responsibility management strategy on financial performance. These management concepts are positively used in agricultural small-medium enterprises as three research streams. However, because of resource limitations, the cost of brand management would be a burden or corporate social responsibility activities may lead to harmful performance. There are many conflicting findings in the existing research. This study analyzed data from 371 agricultural small-medium enterprises in China using fsQCA 3.0. The result reveals four solution pathways for achieving high financial performance and highlights the attributes of each solution pathway. The findings suggest that integrating brand, quality, and corporate social responsibility management, or combining brand and quality management are effective options for achieving high financial performance in agricultural small-medium enterprises. These results have significant implications for managers seeking to improve their firm’s financial performance by optimizing their management strategies.

Plain Language Summary

This study explores how the combined use of brand, quality, and corporate social responsibility management strategies affects the financial performance of small to medium-sized agricultural enterprises. These strategies have been seen as beneficial in the agricultural sector, but implementing them all can be costly due to limited resources. It is also uncertain whether corporate social responsibility efforts might negatively impact performance, as previous research has conflicting findings on this topic. To investigate this, we analyzed data from 371 small to medium-sized agricultural enterprises in China using a specific analytical tool. Our analysis unveiled four distinct approaches that lead to strong financial performance, and we provided details about each of these approaches. The findings indicate that integrating brand, quality, and corporate social responsibility management strategies, or combining brand and quality management, are effective ways for these agricultural businesses to achieve strong financial performance. These results are important for managers looking to enhance their company’s financial performance by making smart choices about how they manage their brand, quality, and corporate social responsibility efforts.

Keywords

Introduction

Nowadays, in the competitive environment, it is difficult for small-medium enterprises to adopt large enterprise practices because of resource limitations (Vo, 2011). Compared to other small-medium enterprises, agricultural enterprises face the most barriers, which are product differentiation of products, meeting high safety standards, and raising consumers’ ethical concerns (Grashuis, 2018; Wicaksono et al., 2021). Similarly, in the background of rural revitalization strategy in China, agricultural small-medium enterprises begin to underline the importance of effective management of brand, quality, and corporate social responsibility (CSR).

So far, agricultural small-medium enterprises are still grappling with the controversial question of which management strategy to adopt in order to achieve high financial performance (Giacosa et al., 2017). Brand management strategy has become increasingly pivotal, playing an essential role in developing long-term profit streams for these enterprises (Keller, 2008). It needs to meet the changing demands of the market and generate higher sales from a strategic perspective (Iyer et al., 2021). Meanwhile, to create a good brand image, most enterprises adopt a quality management strategy to focus on achieving sustainable high-quality and positively promoting the quality levels of their product. Consequently, quality management has emerged with success related to performance (Karia & Muhammad, 2006). Furthermore, for improving the brand image and enterprises’ reputation, CSR has gained significant attention in the academic fields. It has been identified as a strategic role in business. Especially for agricultural small-medium enterprises, they need to decide how to integrate CSR into their organizational strategy (Popoli, 2011). Some researchers take CSR as a cornerstone of brand management, playing an essential role in brand differentiation (Abid et al., 2020). Other researchers consider integrating CSR management into quality management, which can improve the image and maintain the organization’s sustainability (Frolova & Lapina, 2015). However, in this study, we take CSR as a different dimension of management, because CSR management extends more cost-benefit problems. Especially in the competitive market, for establishing a competitive advantage and increasing the enterprise’s marketing power, emphasizing CSR strategy has become considerable (Iaia et al., 2019; La & Choi, 2019).

Based on the discussion above, the market demand is influenced by the management of brand, quality, and CSR for enterprises (Mondal & Giri, 2021). Hence, brand management, quality management, and CSR could be simultaneously implemented by agricultural small-medium enterprises to develop a valuable enterprise strategy, which provides a sustainable competitive advantage.

However, according to previous research, when small-medium enterprises have invested in the management of brand, quality, and CSR, it is difficult to confirm which kind of management strategy has a positive impact on financial performance. As noted above, because of resource limitations, the cost of brand management would be a burden for small-medium enterprises (Keller, 2008). Also, if consumers prefer the product itself over the enterprise’s good deeds, CSR activities may cause consumers to draw adverse inferences and harm performance (Luchs et al., 2010). Furthermore, there is a shortage of literature on synthesizing brand management, quality management, and CSR to pursue a high level of financial performance from a configurational perspective. This study aims to merge three research streams, including brand management, quality management, and CSR, a management strategy of which has been adopted positively, further exploring the mechanism for brand management, quality management, and CSR combining effect on financial performance of the agricultural small-medium enterprises.

In this study, we address the following questions:

What are configurations of influencing conditions sufficient for producing a high level of financial performance?

What are the characters of each configuration for producing a high level of financial performance?

To examine these questions, we use a configurational approach with a fuzzy set qualitative comparative analysis (fsQCA). The fsQCA approach could help clarify the simple structure of the relationships between brand management, quality management, CSR, and financial performance. With this approach, we can capture combinations of conditions occurring simultaneously to be sufficient for an outcome (Pappas & Woodside, 2021). From a configurational perspective, we can explain complex causal relationships in social phenomena.

This study makes two significant contributions. First, given the importance of brand management, quality management, and CSR in strategic marketing theories and the lack of research on their impact on the agricultural small-medium enterprises’ financial performance, it is essential to examine how strategic management influences the agricultural small-medium enterprises’ performance. It represents the focus of this study. Second, while previous literature has focused on one or two management strategies affecting financial performance, this study emphasizes the configuration of brand management, quality management, and CSR. The application of the fsQCA approach extends the existing theory on management strategy. The results may have practical implications for the agricultural small-medium enterprises’ managers, who can develop the most appropriate orientation of strategic management configuration and enhance financial performance.

The following is the structure of this study. Combining with prior literature, we first discuss the impact of brand management, quality management, and CSR on financial performance respectively, to clarify the importance of a configurational approach. Then based on the literature, data, and measurement of this study will be described and chosen. Next, according to the process of fsQCA 3.0, we examined the results of configuration for high financial performance and robustness check. Last, the contribution of this result will be discussed, along with research limitations and suggestions for future research.

Literature Review

Brand Management and Financial Performance

Current knowledge shows that brand management capability and brand orientation alone are insufficient for enhancing financial performance (Lee et al., 2017). Notably, unlike general products, agricultural small-medium enterprises rarely use branding to pursue differentiation and competitiveness because of inherent constraints on agricultural food (Grashuis, 2018). However, there are still some scholars who find the relationship between brand management and financial performance. With regard to negative results, it is necessary to establish a better understanding of the brand management and financial performance relationship based on the characters of small-medium enterprises. Mainly due to resource limitations, brand management is probably not a priority for small-to-medium enterprises (Keller, 2008). By contrast, other researchers argue that the efforts of brand management have a positive effect on the financial performance of agricultural small-medium enterprises by the empirical analysis (Agostini et al., 2015; Grashuis, 2018).

Furthermore, in brand management, the factor of trademarks is recognized as a cumulative effect. In particular, the number of trademark registrations, which can enhance the ability of innovation for enterprises, has a positive impact on financial performance (Agostini et al., 2015). Thus far, because of the characters of small-medium enterprises, the contradictory point of the result for the effect of brand management on financial performance still exists.

Quality Management and Financial Performance

With the increasing concern for product quality, quality management has become a core element (Natarajan & Thiripurasundari, 2011). It can improve labor productivity and profitability and achieve quality goals to support managers in attaining quality improvement (Patyal & Koilakuntla, 2017). Previous studies have found that the efforts of quality management practices have a direct impact on financial performance (Nair, 2006; Parvadavardini et al., 2016; Sadikoglu & Olcay, 2014).

Within the context of the agricultural small-medium enterprises, for maintaining and increasing a company’s competitive advantage from a long-term perspective, quality management could impact on consumers’ perceptions (Giacosa et al., 2017). Especially for quality certification in quality management, it has been measured and proved that it positively contributed to the agricultural small-medium enterprises’ performance (Psomas & Kafetzopoulos, 2015).

Previous research suggested integrating CSR into quality management because this integration can help enterprises improve the overall process performance in the long term (Frolova & Lapina, 2015). Interestingly, a recent study found that the simultaneous implementation of CSR and quality management is less beneficial to financial performance than the isolated implementation of CSR due to the redundancy of different activities aimed at similar goals (Franco et al., 2020). Clearly, for enhancing financial performance, quality management has an essential position.

CSR and Financial Performance

In today’s competitive market environment, the content of CSR management is related to employment, environment, business practices with suppliers or consumers, etc. (Sheehy, 2015). Generally, agricultural small-medium enterprises start facing increasing pressure to engage in CSR activities (Kim & Bhalla, 2022). Many empirical studies have examined the relationship between CSR and financial performance, especially surrounding the benefits and costs of CSR. Regarding the positive impact of CSR on financial performance, many enterprises are increasingly drawing on CSR to improve their social image (Wicaksono et al., 2021). Using CSR information can not only positively influence the enterprise inside but also have a good effect on the market (Ramesh et al., 2019; Rhou et al., 2016). Consequently, for small-medium enterprises, the impact of CSR on financial performance could be significant in the long term (Choongo, 2017). Compared to other industries, agricultural enterprises’ commitment to CSR can be an important decision-making factor. CSR appears to have a positive impact on enterprise performance, either directly or indirectly, as a result of image and reputational effects (Luhmann & Theuvsen, 2016).

Nevertheless, on the other hand, some scholars do not think CSR can directly influence performances (Pai et al., 2015). Even sometimes, CSR is detrimental to financial performance because of the unnecessary cost incurred by CSR, or the expenses leading to an uncertain outcome (S. Park et al., 2017). Moreover, CSR may have a U-shape link on financial performance. Only when a solid relationship of enterprise inside has been formed, the cost of CSR will translate into a higher benefit (Franco et al., 2020). Thus, despite the increase in studies on CSR, the relationship between CSR and financial performance still needs to be clarified.

As discussed above, previous research findings into the contributions of brand management, quality management, CSR have been inconsistent and contradictory. The central contradiction is concentrated on the costs and benefits, especially for small-medium enterprises. Also, based on theory and research, much of the current literature pays particular attention to only one dimension of either brand management, quality management, or CSR, which can affect financial performance, respectively. However, in fact, these dimensions usually occur simultaneously, and it is hard to say which one can influence financial performance directly. As prior literature suggests, conditions mutually reinforce one another, and one condition can replace another in leading to an outcome. This concept is fundamental to a configurational approach (Misangyi et al., 2017). Under these circumstances, we need to understand how or why multiple conditions combine into different configurations to affect financial performance. Probably more than one configuration can lead to the outcome (Furnari et al., 2020). Hence, in this study, it is necessary to discuss that situation from a configurational perspective (Pappas & Woodside, 2021). In contrast to regression analysis on isolating net effects, fsQCA will be conducted to focus on the causal conditions combined (Fiss et al., 2013).

Methodology

Data

The data collection was conducted in China from November 19th to December 23rd in 2021, collaborated with the local economic and information commission of Chongqing City in China. The sample was randomly selected from the database of agricultural small-medium enterprises. In this study, we have selected the classification criteria for small, medium, and micro agricultural enterprises based on the guidelines provided by the Chinese government. These criteria include agriculture, forestry, animal husbandry, and fishery as the eligible sectors. Additionally, small, medium, and micro enterprises are defined as those with an operating income below 200 million yuan. At the beginning, we distributed survey questionnaires to each agricultural enterprise and then collected them after they had finished. Next, we scanned the survey questionnaire into electronic files. Last, the entire data was arranged into excel files. The whole process took 3 months. The survey recovered 493 copies, with 371 valid questionnaires. The sampling data is all from agricultural food processing enterprises that meet the following criteria. Each enterprise should enter their Unified Social Credit number. The Unified Social Credit number is issued to registered companies by the Chinese government (https://www.cods.org.cn/). This number serves as confirmation that all selected cases are genuine enterprises. Enterprise products should have at least one brand. Operating annual income is lower than 200 million yuan (small-medium enterprises standard). The established time for data collection ranges from at least 5 to 30 years. We eliminated 101 copies due to a lack of data and 21 by removing the extreme values.

The survey was designed by the following two parts: The first part contained items on: the purpose of this survey, established date, and what agricultural products were produced or processed. The second part asked the situation of the enterprises the management of brand, quality, CSR, and financial performance in 2020, which is the central part of data analysis in this study.

Analysis by fsQCA

As previously stated, we adopted a configurational approach employing fsQCA methodology, in order to analyze the relationships between brand management, quality management, CSR, and financial performance.

FsQCA is an approach grounded in the notion that causal relationships are often better comprehended through set-theoretic relations rather than correlations (Fiss, 2011). Particularly in the context of management strategies within organizations, this approach facilitates the exploration of interdependencies among the causal effects influencing organizational outcomes, aligning with configurational thinking (Greckhamer et al., 2018). Moreover, the application of fsQCA to large-N research stands to benefit significantly, as it allows for the incorporation of qualitative data and the exploration of causal patterns within specific configurations (Greckhamer et al., 2013). In this study, the sample size is sufficiently large for analysis, and the utilization of fsQCA enables the identification of combinations of simultaneous conditions that prove sufficient for generating a given outcome (Pappas & Woodside, 2021).

Measurement

In this study, we take three dimensions, including brand management, quality management, and CSR as the antecedents, and financial performance as the outcome condition. It was developed considering constructs that were measured using existing scale items in the literature as a reference.

In the enterprise, brand management is integrated into different organizational activities, including marketing, human resources, operations, etc. Here, we take three variables for measuring. The initial variable is the brand management department because it is necessary for the enterprise to have an individual department to manage its brand (Leijerholt et al., 2019). As a central condition, if this enterprise has an independent brand management department, it is coded by 1 and 0 otherwise. Second, the number of trademarks represents the value, which often indicates a company’s brand value, and is positively related to innovations that can improve company performance (Schautschick & Greenhalgh, 2016).

Similarly, we used 95% of the sample as “fully in,” and 5% were considered “fully out.” 50% value was used as the crossover point. The third variable is a trademark award, which is designed based on the background in China. Some brands are authorized as China Well-Known trademark, or Province Well-Known trademark, if the reputation of this brand is good. From the consumers’ perspective, brand reputation is equally essential for the enterprise and positively influences financial performance (Foroudi, 2019). Since brand reputation is related to the trademark award for the enterprise, we used code 1 if this enterprise got the trademark award and if not by code 0. As a result, brand management dimension is calculated by brand management department, the number of trademarks, and trademark award.

Quality management dimension is difficult to measure because companies use different quality standards and management methods, especially for agricultural enterprises. Several studies on quality management have been carried out and use whether a company has a quality certification (1) or not (0) as the main indicator (Franco et al., 2020; Levine & Toffel, 2010). Since the purpose of this study is to find combinations of influencing conditions for high financial performance, we use a dichotomous variable to measure whether this agricultural enterprise has quality certification (including ISO9001, HACCP) or not. If it has, we code 1 and if not, 0. In fact, some enterprises just have a quality certification but do not have an independent department to conduct and monitor, which is also a different level for quality management (Sadikoglu & Zehir, 2010). Therefore, in this study, we add two variables to measure quality management, namely whether this company has an independent quality management department and a full-time quality manager (1) or not (0). It is modified from the measurement of process monitoring and control (Parvadavardini et al., 2016). This measurement is more specific than considering only one condition of quality certification (Franco et al., 2020). Especially for agricultural small-medium enterprises, it is getting more convenient to stick to a precise plan. To sum up, the quality management dimension is measured by quality certification, quality management department, and full-time person in charge of quality management.

In developing the scale of CSR dimension, exploratory factor analysis has been performed, including community-oriented, natural environment-oriented, supplier-oriented, customer-oriented, shareholder-oriented, and so on. Among these, employee-oriented CSR has been focused because the employees in the enterprise would react strongly due to some irresponsible behaviors, and their commitment is related to organizational performance (El Akremi et al., 2018; Sheehy, 2015). Meanwhile, the unemployment issue is treated as one of the critical social problems. Especially for agricultural enterprises, it can raise credibility and authenticity by committing to job security and compliance (Luhmann & Theuvsen, 2016). Thus, we take absorb employment as one condition. In fact, for measuring the CSR dimension, a dichotomous variable is also often used, measured by whether this enterprise conducts CSR activities positively (1) or not (0) (S. Park et al., 2017). However, it is difficult to measure the difference in the magnitude of CSR activities. Especially for the background of rural revitalization strategy in China, most agricultural enterprises are trying to drive the farmers’ income. To quantify the degree of CSR dimension, we use two continuous variables, including driving farmers’ number and increasing the amount of farmers’ income to measure. Overall, in this study, the CSR dimension is measured by three conditions: absorb employment, drive farmers’ number, and increase the amount of farmers’ income.

Financial performance has been measured by prior empirical studies, including cost, expenses, income, profit, tax, etc. (Parvadavardini et al., 2016). It may be appropriate for structural equation modeling analysis because the chosen items need adequate and have a correlative relationship. In this study, since financial performance is the target outcome measured by fsQCA, we only need one variable to measure. Thus, we choose the value of the annual income in 2020 to indicate the financial performance of the agricultural enterprises. Then, we take the top 20% of highly annual income enterprises as high financial performance cases. We will explain that in the calibration part.

Calibration of fsQCA

According to the procedures, the first step in configurational analysis is data calibration (Ragin, 2008). Based on the linking of conditions, we transformed the original data into a fuzzy set membership score. For reflecting meaningful standards and capturing requirements directly relevant to the reality (Misangyi et al., 2017), according to the sample data’s frequency distribution (Douglas et al., 2020), we use the direct method of calibration, which chooses the values 0.95, 0.50, 0.05 to transform the data into the [0,1] range (Fiss, 2011). Nevertheless, since the data of financial performance in this study is skewed to the left, we use 80%, 50%, and 20% as the thresholds for is “fully in,”“fully out,” and somewhere in between (“crossover”) (Pappas & Woodside, 2021; Pappas et al., 2017). In detail, for the continuous value including financial performance, absorb employment, drive farmers’ number, increase the amount of farmers’ income, number of trademarks, we processed these data by SPSS to compute the values of 95%, 50%, and 5% as the three thresholds. Then using fsQCA software, the score of variables’ transformation is automatically computed on three membership which is “fully in,”“fully out,” and somewhere in between (“crossover”) by calibration (Pappas & Woodside, 2021). For the dichotomous values, including brand management department, brand award, quality certification, quality management department, and a full-time person responsible for quality management, we use 1 or 0 to represent whether this enterprise has met this condition or not (shown in Table 1).

Calibration (n = 371).

Process

According to the process for research practice by fsQCA 3.0 software (Pappas & Woodside, 2021), we should confirm necessary conditions first, and then construct the truth table algorithm to identify appropriate cases associated with outcomes based on the configurations of the causal conditions. Last, we examined the paths for the condition configurations to the high financial performance. To filter out configurations with stronger subset relationships and reduce the number of configurations, we chose the consistency threshold to 0.90 (Y. Park et al., 2020), greater than the 0.8 minimum recommended (Leppänen et al., 2019), and the PRI consistency to 0.71, greater than 0.5 significant inconsistency value (Greckhamer et al., 2018). We set the minimum acceptable frequency of cases with at least 1 case. In general, when a dimension is measured with multiple items, we need to compute one value per dimension (Pappas & Woodside, 2021). However, in this study, the individual effect of each condition needs to be considered (DiStefano et al., 2009), because for agricultural small-medium enterprises, each of the conditions could be operable on management strategy.

Results

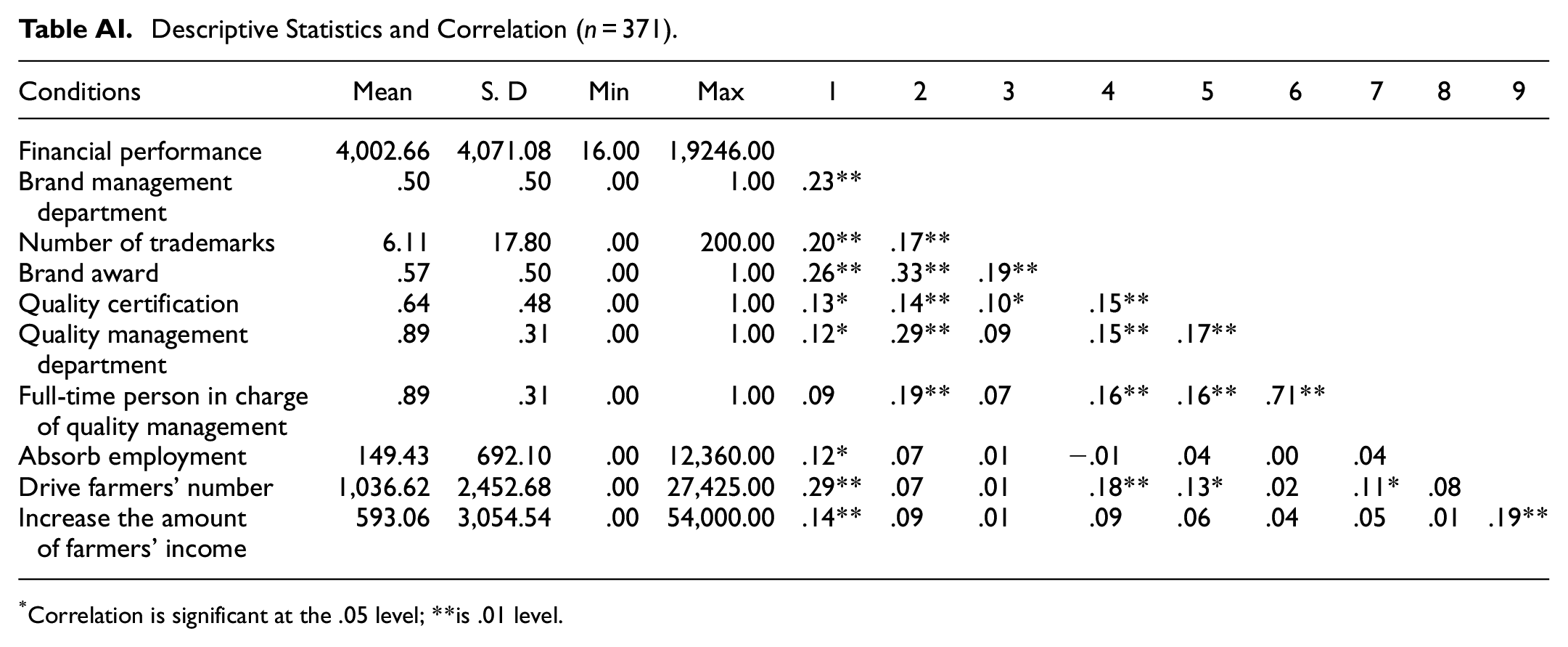

AppendixTable AI presents the description and correlations for all the conditions. We designed nine causal conditions for three dimensions to examine the high financial performance. Since the data is large-N, the number of conditions is appropriate (Greckhamer et al., 2013). In these three dimensions, the causal conditions are absorbing employment, driving farmers’ number, increasing the amount of farmers’ income, brand management department, number of trademarks, trademark award, quality certification, an independent quality management department. These conditions have the positive correlations with financial performance. Although there is no significant correlation between financial performance and a full-time person in charge of quality management, the latter condition positively correlates with the other conditions of quality management dimensions. Hence, we also take this condition into account. In detail, in each of different dimensions, brand award of brand management dimension, quality certification in quality management dimension and drive farmers’ number of CSR dimension has the highest correlations with financial performance. As the first step of the analysis, we can take these three conditions as relatively essential conditions.

Necessary Conditions

Before analyzing sufficient configurations for an outcome, we use the fsQCA 3.0 to determine the necessary conditions by the Necessary Analysis function. The necessary condition indicates that one individual condition is necessary for the target outcome. One condition with the value of consistency greater than 0.90 is used as a necessary condition (Ragin, 2008). As Table 2 reported, an independent quality management department and a full-time person in charge of quality management have the highest value of consistency, both of which are 0.92 greater than 0.90 but have non-trivial coverage (0.45 and 0.44). A possible explanation might be that most identified cases are not covered. From the aspect of the theory, recognizing these two conditions as necessary conditions is not meaningful. Since a significant claim of necessity is not only empirically consistent, but also empirically non-trivial, and theoretically meaningful (Schneider, 2018). Therefore, we do not take these two causal conditions as necessary conditions for high financial performance. A similar circumstance has been explained in previous literature (Douglas et al., 2020). Other values of conditions are ranged from 0.08 to 0.81.

Necessary Analysis for High Financial Performance.

~Indicates the negation of a condition.

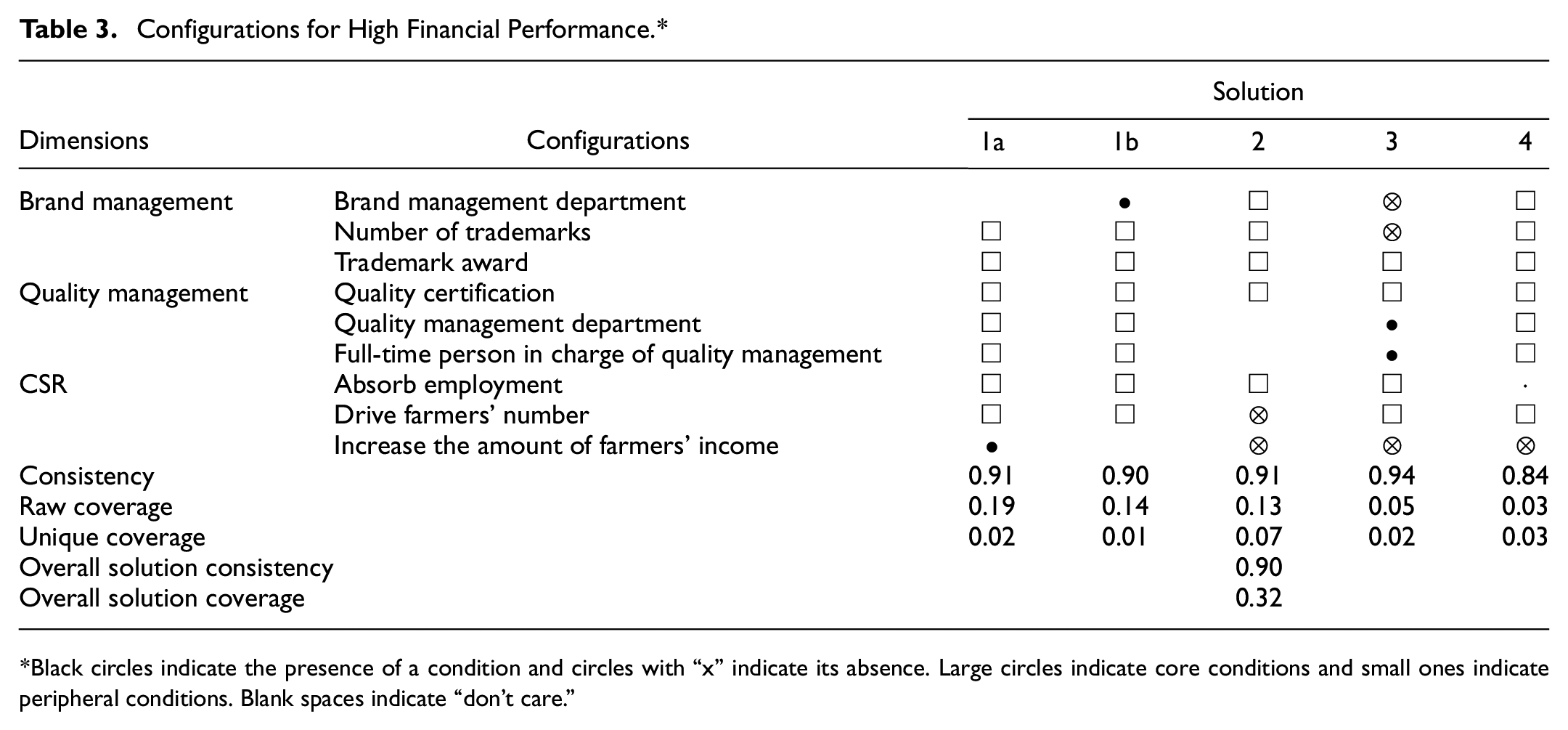

Configuration for High Financial Performance

Table 3 shows the configuration results for high financial performance, including the value of consistency and coverage for each individual solution and the overall solution. As the notation indicated introduced (Fiss, 2011), black circles mean that the presence of a condition, and circles with a cross-out mean their absence. Moreover, core conditions are used in large circles and peripheral conditions in small circles. Blank spaces indicate a condition may be present or absent. Compared with the parsimonious and intermediate solutions, core and peripheral conditions have been identified (Fiss, 2011).

Configurations for High Financial Performance.*

Black circles indicate the presence of a condition and circles with “x” indicate its absence. Large circles indicate core conditions and small ones indicate peripheral conditions. Blank spaces indicate “don’t care.”

Since there is no configuration comprised by a single condition, we can conclude that one single condition is not sufficient for high financial performance. This result shows that there are four main solution pathways for high financial performance. The overall solution consistency is 0.90, which exhibits acceptable consistency (≥0.80). The value of consistency means that these configurations are always sufficient for high financial performance. The coverage is 0.32, which explains about 32% of high financial performance can be covered by the identified solutions.

Overall, we find four solutions to high financial performance. Each of the configurations depends on the different core and peripheral conditions. In detail, three out of four solutions show the importance of brand management, especially for trademark awards. All the solutions have this core condition, which indicates that trademark award is very critical for high financial performance. Even though it is not the necessary condition at the prior examination, we can explain that in the 32% of high financial performance identified cases, and trademark award is the essential condition. This result examined the importance of brand reputation for high financial performance (Foroudi, 2019).

Similarly, the condition of absorbing employment is also taken as the core condition in most solution pathways except for solution 3. This result showed that most of the agricultural enterprises in China aim to solve the social problem of unemployment issue. By contrast, increasing the amount of farmers’ income is negation in three solutions and absent or peripheral condition in the other two solutions. Here, according to Pappas and Woodside (2021), we try to clarify the distinction between the terms of negation, absent and irrelevant (don’t care) condition. The possible explanation is that compared with driving farmers’ number, it would take much more cost to increase the amount of farmers’ income. With the current step of China’s rural revitalization strategy, this should be the next task to be accomplished in the foreseeable future. The following is to explain the characters of each solution pathway in detail:

The first solution pathway, including solution 1a and 1b to high financial performance, which we called the integration pathway, comprises all the dimensions, including brand management, quality management, and CSR as the core condition. The reason why we take solution 1a and 1b as one pathway is that both solutions have the same core condition. The consistency of this pathway is 0.91, 0.90, and the raw coverage is 0.19, 0.14, which is greater than the other pathways. It indicates that most cases belong to this pathway. Thus, strong evidence of this pathway was found when the agricultural enterprises focus on brand management, quality management, and CSR simultaneously, they would achieve high financial performance.

Regarding CSR, increasing the farmers’ income was not the core condition in this solution pathway but the “do not care” condition. We can explain that in the current rural revitalization strategy in China, it is necessary to drive the farmers to increase incomes. However, for high financial performance, it is not a core condition to pursue expanding the amount of farmers’ income. For the brand management, agricultural enterprises should focus on the number of trademarks and trademark awards. Meanwhile, having an individual brand department is taken as a peripheral condition.

Solution 2 indicates a second important path to high financial performance, which shows the critical existence of brand management, and quality certification is also the core condition. Hence, we called a branding-quality pathway. The consistency of this pathway is 0.91, and the raw coverage is 0.13. In this pathway, all the conditions of brand management dimension, including brand management department, number of trademarks, and trademark award are core conditions. In contrast, the conditions for CSR management should be absent except absorb employment. This result may be explained by the fact that CSR management occurs unnecessary costs sometimes, which could lead to a negative effect on high financial performance (S. Park et al., 2017). Regarding quality management, except quality certification, the other two conditions for high financial performance are present or absent. As mentioned above, quality certification is usually measured by the level of quality management in one’s own company, which needs to be given a lot of attention (Franco et al., 2020).

Solution 3 is the pathway that we can call the CSR-quality pathway. The core conditions are absorbing employment, drive farmers’ number, and quality management, in which quality certification is the core condition, and the other two are peripheral conditions. In detail, we found that the character of this pathway is concentrating on the vital condition, which is drive farmers’ number, trademark award, and quality certification in each of the dimensions. As correlation computed above, the values of these three conditions are larger than the other conditions in each of the same dimensions, which indicates that they have a stronger correlation with high financial performance. Consistency is 0.94, and raw coverage is 0.05 in this pathway, the second-lowest in the four solutions. In detail, CSR is similar as solution 3. The conditions for absorbing employment and driving farmers’ number are taken as the core conditions except increasing the farmers’ income. For brand management, trademark award is the core condition, whereas brand management department and number of trademarks are absent as peripheral condition. quality management conditions for an independent quality management department and a full-time person in charge of quality management are identified as the peripheral conditions.

Solution 4 can be called the CSR-branding pathway compared to solution 2, because driving farmers’ number in the CSR dimension is recognized as the core condition besides brand management. The consistency of this pathway is 0.84, and the raw coverage is 0.03. The value of this pathway is less than the other solutions, which indicates that the number of identified cases in the pathway is smaller than the others. Regarding quality management, as a peripheral condition, quality certification is absent, and the other two conditions in the quality management dimension are also blank. These findings consider the unimportance of quality management in this pathway.

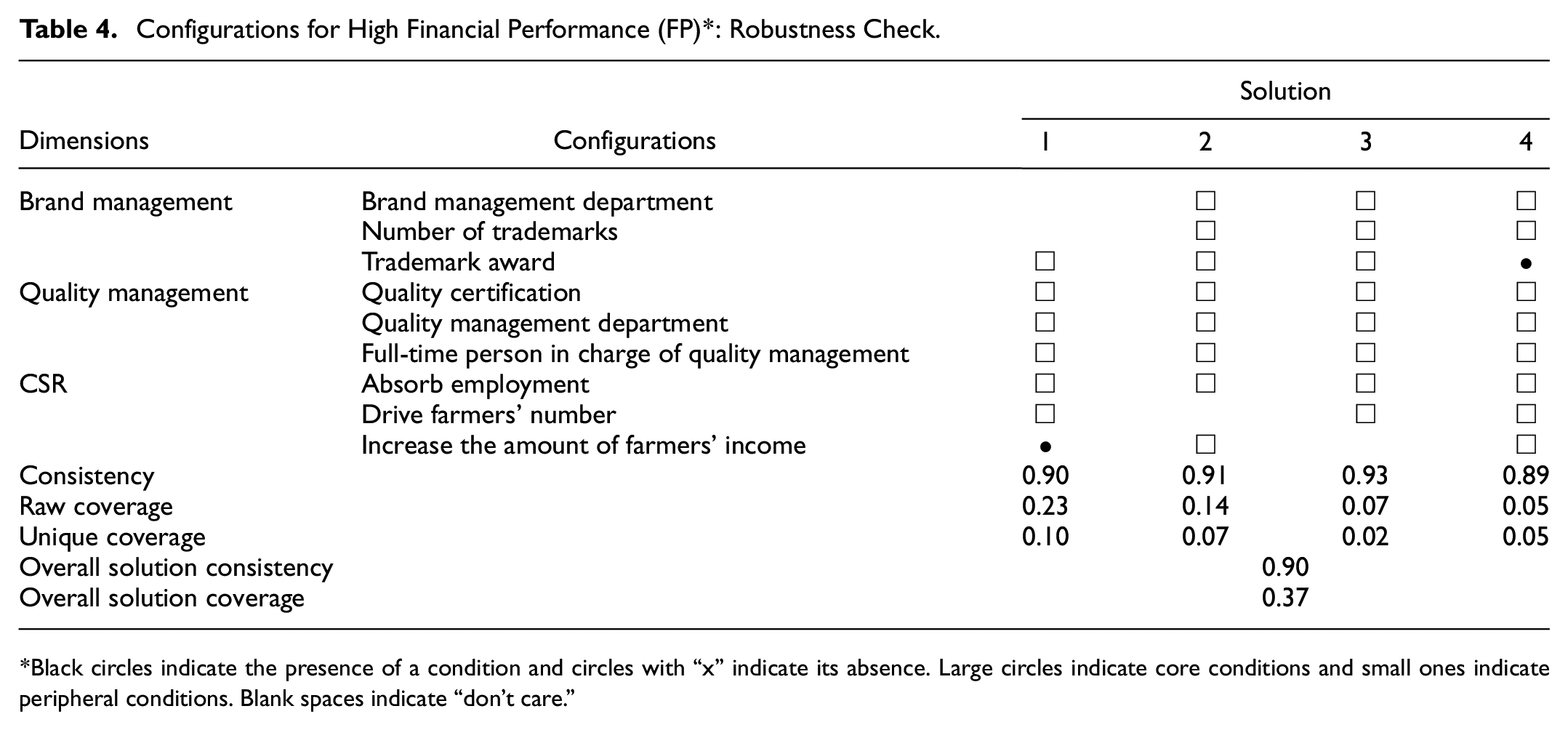

Robustness Check

Even though the solution pathways above have been simplified because of the high threshold, it is still easy to misunderstand the true meaning of solutions since we set a standard frequency threshold of 1 case. Hence in the robustness check, the analysis should be rerun with the different value of consistency threshold 0.89 and PRI 0.69 and adjusted to a criterion of at least 2 cases to obtain a more parsimonious superset of the original solution (Skaaning, 2011).

Table 4 shows that robustness check results in similar solution pathways, with the same consistency and slightly higher coverage from 0.32 to 0.37. Specifically, solution 1 has been integrated as one pathway, and solution 2 is still a branding-quality pathway. These two solutions are explained by most cases, which is also the main contribution of this study. Solution 3 is also similar to the original solution, but solution 4 cannot be called the CSR-branding pathway in the robustness check. Since the number of identified cases is the smallest, we conclude that this solution pathway is unstable. Moreover, the most striking result from the robustness check highlights the importance of an independent quality management department and a full-time person in charge of quality management, which is present in all the solutions as the core condition. Since these two conditions have a high value of consistency in the necessary condition analysis above, we need to reconsider the critical existence of these two conditions after raising to a criterion of at least 2 cases.

Configurations for High Financial Performance (FP)*: Robustness Check.

Black circles indicate the presence of a condition and circles with “x” indicate its absence. Large circles indicate core conditions and small ones indicate peripheral conditions. Blank spaces indicate “don’t care.”

Discussion and Conclusions

This study clarified on the relationship between brand management, quality management, and CSR, and their combined influence on financial performance for agricultural small-medium enterprises in China from a configuration perspective. This result could overcome the conflicting results found in previous literature (Franco et al., 2020; S. Park et al., 2017). In this study, we investigated the appropriate configuration of brand management, quality management, and CSR for high financial performance, using fuzzy set qualitative comparative analysis with the data from 371 agricultural small-medium enterprises in China. We assume that the agricultural small-medium enterprises face three kinds of management strategy, including brand management, quality management, and CSR. We design nine causal conditions in three dimensions for high financial performance, choosing the conditions of brand management, quality management, and CSR selected by prior studies. The result reveals four solution pathways for achieving high financial performance, and we explained the characters of each solution. The following are the critical points of the result in this study.

First, the most exciting finding of this study is that solution 1, the integration pathway, which shows the importance of focusing on brand management, quality management, and CSR simultaneously. This pathway was explained by a large part of the sample, indicating that the integrated management of brand management, quality management and CSR is the recommended way for achieving high financial performance. Compared with previous literature, although there is a risk of limited resources or cost spending for agricultural small-medium enterprises, pursuing improving the integrated management of brand management, quality management and CSR is still an effective strategy.

Second, compared to the integration pathway, the second effective solution is the branding-quality pathway. The result shows that combining brand management with quality management is necessary for achieving high financial performance. Especially in the necessary condition analysis and robustness check, we found the critical existence of an independent quality management department and a full-time person in charge. Comparing the findings with those of other studies confirms that quality management could be the foundation for integrating management (Sampaio et al., 2012). Additionally, from a configurational perspective, this study contributes to the existing theory in the field of branding that represents the importance of brand management on financial performance for agricultural small-medium enterprises (Agostini et al., 2015; Grashuis, 2018).

Third, the results of this study contribute to re-examining the relationship between quality management and financial performance (Parvadavardini et al., 2016). Particularly in solution 1, three conditions for quality management are the core conditions that are identified in most cases. As one of the most essential conditions, quality certification in quality management has been examined by other previous researches that need to be underlined (Psomas & Kafetzopoulos, 2015). Furthermore, to improve financial performance, clarifying the reason for quality certification can prompt managers to motivate employees to use these applications (Sadikoglu & Olcay, 2014).

Fourth, the results emphasize the critical role played by trademark award, which is a valid scale for measuring brand management affecting the financial performance of agricultural small-medium enterprises. This result explains that at the background of China, China Well-Known Trade Mark or Province Well-Known Trade Mark has already been admitted by consumers. The implication of this result is that company managers should focus on trademark award investments in brand management.

Lastly, regarding CSR, increasing the amount of farmers’ income is not a core condition for all the solution pathways. In general, with the background of rural revitalization strategy in China, it should be encouraged to solve social problems. However, this result indicates that only pursuing increasing the amount of farmers’ income maybe not a good choice for agricultural enterprises to achieve high financial performance. By contrast, conditions such as absorbing employment and driving farmers’ numbers need to be invested in by agricultural small-medium enterprises.

Implications

Theoretical Contributions

This study provides several theoretical contributions. First, this study verifies the relationship between brand management, quality management, and CSR to financial performance. Compared with one or two management strategies of influencing financial performance in prior literature, the perspective of this study focuses on the configuration for brand management, quality management, and CSR. We extend the existing theory on management strategy by the fsQCA approach.

Second, the result of this study shows four solution pathways for the configuration of brand management, quality management, and CSR that lead to high financial performance. Among these pathways, the integration pathway and branding-quality pathway identified in most cases, should be recommended in this study. After reviewing the impact of brand management, quality management, and CSR management on financial performance, respectively (Choongo, 2017; Grashuis, 2018; Parvadavardini et al., 2016), this study finds that all the three dimensions occurring simultaneously have a positive relationship with high financial performance. Compared to the prior literature, the contribution of brand management, quality management, and CSR may lead to contradictory results, because of the cost and resource limitation for agricultural small-medium enterprises (Keller, 2008; Vo, 2011). Thus, the result of this study not only confirms the existing theory, but also proposes the possibility for an integrated management.

Third, regarding the measurement of this study, we found the critical conditions in each dimension, which is trademark award in brand management, quality management department and full-Time person in charge of quality management in quality management, and absorb employment in CSR. Recent research has focused on the holistic effect of each dimension through structural equation modeling analysis (Gupta et al., 2021; La & Choi, 2019). The contribution of this study is to specify the conditions in each dimension and identify which conditions are necessary through the application of fsQCA. This approach implies that academics deal with the reality in the managerial field.

Managerial Implications

This study provides several managerial implications. First, the measurement of the relationship between brand management, quality management, and CSR to financial performance is critical for agricultural enterprises in competitive environments. The result shows that integrating brand management, quality management, and CSR or combining brand management with quality management should be a good choice for agricultural small-medium enterprises to achieve high financial performance. The results have practical implications for agricultural small-medium enterprises’ managers, who can develop the most appropriate orientation of strategic management configuration and enhance financial performance.

Second, to reflect reality, we expand two conditions to measure quality management, namely, an independent quality management department and a full-time person in charge of quality management (Parvadavardini et al., 2016; Sadikoglu & Zehir, 2010). These two conditions are taken as necessary conditions for high financial performance, which confirmed the positive impact of quality management practices on financial performance (Sadikoglu & Olcay, 2014). One implication of this result is the possibility that small and medium-sized farm managers understand a critical part of quality management. Notably, a quality management department needs to be established and necessary to set at least one full-time person in charge (Sadikoglu & Zehir, 2010).

Third, the result of this study highlights the importance of undertaking CSR activities for the agricultural small-medium enterprise, consistent with recent empirical studies (Halme et al., 2020; Iaia et al., 2019). While prior research has suggested that the isolated implementation of CSR is better than the simultaneous implementation of CSR and quality management for financial performance, this study shows that quality management and CSR strategy occurring simultaneously can be a potential source of sustainable competitive advantage.

Overall, the study underscores the importance of brand, quality, and CSR management for agricultural small-medium enterprises. However, resource limitations may hinder the implementation these strategies (Vo, 2011). Therefore, managers need to consider choosing the appropriate management strategy and provide more specific guidance for management strategy in the competitive environment.

Research Limitations and Suggestions for Future Research

This study has several limitations and suggests directions for future research. First, we identified nine causal conditions in three dimensions for high financial performance. While the number of conditions in this study is reasonable given the large N data, there may be other conditions that are also important and require further investigation. Additionally, further study is required to deep into the relationship between brand management, quality management, and CSR for the agricultural small-medium enterprises.

Second, this study took financial performance as the outcome variable. It could be related to the size of the enterprise. That is why we selected the enterprises with annual income and the established time limitation. However, we cannot ignore the fact that there is some error. Furthermore, financial performance is just one part of business performance (Sadikoglu & Zehir, 2010), because business performance encompasses many aspects, namely employee performance, innovation performance, organizational performance, and so on (El Akremi et al., 2018; Sheehy, 2015). A more holistic study needs to be conducted in the future.

Thirdly, the three dimensions of brand management, quality management, and CSR that we assumed in this study ultimately have no independent existence, and there maybe complex interactions between there. For example, CSR may positively influence brand development and preference, because it has emerged as central to brand development (Maon et al., 2021). Meanwhile, CSR communication with consumers has been seen as an effective strategy to boost brand image and foster brand admiration in the long term (Gupta et al., 2021; Lii et al., 2013). In particular, CSR performance can influence brand preference by perceiving brand quality (Tingchi Liu et al., 2014). Also, quality management may contribute to CSR satisfaction, because it may positively impact CSR in satisfying stakeholders (Quintana-García et al., 2018). Further study needs to consider the interactive relationship between these three dimensions and their impact on business performance.

Overall, this study highlights the importance of considering the integration of brand management, quality management, and CSR strategies in agricultural small-medium enterprises to achieve high financial performance. While these management strategies constitute internal characteristics of enterprises, it is important to acknowledge the relevance of external strategies, such as internationalization strategies, which also deserve consideration by managers (Giacomarra et al., 2021; Thrassou et al., 2020). Nonetheless, further research is required to fully understand the underlying mechanisms and to develop practical guidance for managers in the competitive environment.

Footnotes

Appendix

Descriptive Statistics and Correlation (n = 371).

| Conditions | Mean | S. D | Min | Max | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Financial performance | 4,002.66 | 4,071.08 | 16.00 | 1,9246.00 | |||||||||

| Brand managementdepartment | .50 | .50 | .00 | 1.00 | .23** | ||||||||

| Number of trademarks | 6.11 | 17.80 | .00 | 200.00 | .20** | .17** | |||||||

| Brand award | .57 | .50 | .00 | 1.00 | .26** | .33** | .19** | ||||||

| Quality certification | .64 | .48 | .00 | 1.00 | .13* | .14** | .10* | .15** | |||||

| Quality managementdepartment | .89 | .31 | .00 | 1.00 | .12* | .29** | .09 | .15** | .17** | ||||

| Full-time person in chargeof quality management | .89 | .31 | .00 | 1.00 | .09 | .19** | .07 | .16** | .16** | .71** | |||

| Absorb employment | 149.43 | 692.10 | .00 | 12,360.00 | .12* | .07 | .01 | −.01 | .04 | .00 | .04 | ||

| Drive farmers’ number | 1,036.62 | 2,452.68 | .00 | 27,425.00 | .29** | .07 | .01 | .18** | .13* | .02 | .11* | .08 | |

| Increase the amountof farmers’ income | 593.06 | 3,054.54 | .00 | 54,000.00 | .14** | .09 | .01 | .09 | .06 | .04 | .05 | .01 | .19** |

Correlation is significant at the .05 level; **is .01 level.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the Social Science Fund of Chongqing Federation of Social Science Circles [grant number 2019BS063]; the Science and Technology Research Program of Chongqing Municipal Education Commission [grant number KJQN202000627]; Humanities and Social Sciences Research Project of Chongqing Municipal Education Commission [grant number 22SKGH139]; Chinese Scholarships Council (CSC); and Ehime University Grant-in-Aid Research Empowerment Program (FY2023).