Abstract

The study examines the dimension of financial inclusion from the beneficiaries’ perspective (on the demand side). In addition, the present study seeks to determine the relationship between financial inclusion and the disposable income of Pakistani households. The results revealed four significant dimensions to predict financial inclusion (access, availability, usage, and cost). Furthermore, the results also revealed that financial inclusion significantly and directly and indirectly impacts disposable income. Thus, this research emphasizes that inclusion in the formal financial system can enhance the disposable income of low-income urban households and assist them in combating poverty. Further, this investigation is among the earliest to provide a demand-side perspective to measure the financial inclusion dimensions of the “most financially excluded” group (low-income urban households in Pakistan). Besides, this study advances the literature on financial inclusion and disposable income. It attempts to adequately bridge the gap in the literature by examining the relationship between financial inclusion and disposable income among low-income urban households by employing the structural equation modeling approach.

Keywords

Introduction

One of the grave challenges that have accelerated worldwide over the past 20 years is the breadth and scope of the financial system. It has been studied by the concept of financial inclusion (FI) or financial exclusion (Md Salleh, 2015). Financial inclusion is a contemporary issue and is outlined as fair access to financial products and services in an economy. It is crucial for poverty alleviation, income equality, and economic growth (Prabhakar, 2019). The relevance of financial inclusion in policy circles can contribute substantially to attaining sustainable economic growth and social cohesion. Several international financial institutions and financial development agencies have achieved significant strides in improving financial inclusion. To promote inclusiveness, various initiatives and regulations were announced at regular intervals by governments, central banks of developed and developing countries, and international organizations like the United Nations (Allen et al., 2016; Sarma, 2008). The United Nations policy document contains 17 crucial goals, with 169 specific targets, and financial inclusion is targeted in 8 out of the 17 primary goals (Ahmed et al., 2015). It is evident from the arguments that the realization of most of the Sustainable Development Goals SDGs rests, to a great extent, on inclusive finance.

Most of the extant studies (Allen et al., 2016; Arora, 2010; Beck et al., 2007; Li, 2018; Sarma, 2008; Vo et al., 2021) considered the data collected only from the secondary sources to determine the extent of financial inclusion, available at Financial Access Survey (FAS), The World Bank Group, International Monetary Fund (IMF), etc. Moreover, while predominately focusing on the supply-side perspectives, researchers have ignored the demand-side perspective. Thus, there is a dire need to investigate inclusive finance from the demand-side perspectives to multiply inclusive finance density. Besides, studies in the literature have discussed inclusive finance in rural and gender empowerment contexts (Bhatia & Singh, 2019; Lal, 2018; Nandru & Rentala, 2019). However, the literature on the state of financial inclusion among low-income urban households is mainly under-explored. Moreover, it is the first study, at least in our knowledge from the demand-side perspective in Pakistan, to determine the extent of financial inclusion and then evaluate its direct and indirect impact on disposable income. Thus in this scenario, the present study answers the questions. Does opportunity, growth, and distribution effect mediate between financial inclusion and disposable income?

The policymakers in both emerging and developing economies have grasped that financial inclusion is crucial if they intended to direct their economies and countries on the stimulated and all-inclusive growth trajectory. This is essential for a country like Pakistan, which is facing abysmal poverty about 24.3% of people are below the poverty line in Pakistan (Economic Survey of Pakistan, 2020–2021). Further, regarding urban poverty in various Pakistan provinces (Kedir et al., 2016) argued that the city expansions through urbanization increased poverty levels for its inhabitants. Another study by A. Iqbal et al. (2020) shows that the spatial extent of poverty is severest in Rajanpur, Muzaffargarh, and Dera Ghazi Khan. Besides, the population of this study is confronted with severe socio-economic and financial exclusion issues. Under these circumstances, the choice of the target population assumes great significance. Moreover, very limited and only supply-side studies are available concerning the financial inclusion status of Pakistan (Raza et al., 2019). From this perspective, the current investigation is positioned to address the gap. Furthermore, this research employs the structural equation modeling technique to evaluate the key determinants of financial inclusion and to investigate its direct and indirect impact on the disposable income of low-income urban households in Pakistan.

Literature Review and Hypothesis Development

Inclusive Finance for Inclusive Growth

The usage of the term “inclusive growth” dates back to the turn of this century. Presently, there is a broad agreement among economists that finance facilitates the economy to grow. Indeed, inclusive growth is fundamentally a multi-dimensional construct. Unfortunately, no deal has been reached in the policy discussions and literature on correctly measuring and defining it. One viable approach represents growth as inclusive if the economic growth benefits the lower-income groups more than or equal to the rest of the population (Ngepah, 2017). Similarly, George et al. (2012) postulated that inclusive growth primarily incentivizes deprived people, that is, growth that mitigates gender, ethnic, and regional inequalities. The author continued that for growth to be inclusive, it demands an extensive contribution from financial institutions. Moreover, according to White (2012) inclusiveness has been discussed in at least six different contexts: expanding opportunities for growth of emerging market economies; mitigating inequalities in educational, financial, and judicial systems; bridging the North-South divide; ensuring internalization of growth externalities; alleviating absolute poverty; and fostering income equality.

Inclusive finance can become a driving factor for equitable and inclusive growth by making people competitive in economic opportunities. Moreover, it provides access to affordable financial services to facilitate inclusive participation and improve people’s lives. Indeed, there are irrefutable shreds of evidence that suggest financially excluded people face severe challenges in assimilating into society and the economy (Krumer-Nevo et al., 2017). Besides, it also impairs people’s ability to attain the minimum living standard, thus pushing them to the margin of society (Cameron, 2006; Wang et al., 2020). Conversely, access to safe and affordable financial services through either a “supply leading” or a “demand-following” channel by the low-income and vulnerable groups or in lagging sectors is the prerequisite for accelerating inclusive growth.

Dimensions of Financial Inclusion

Seminal literature on inclusive finance accentuates that financial inclusion is a multi-dimensional construct. Many studies have measured the index financial inclusion using secondary sources (Allen et al., 2016; Fungáčová & Weill, 2015). To explore the various dimensions of inclusive finance, we first evaluate the following definitions. According to Sarma (2008), financial inclusion is “a process that ensures the ease of access, availability, and usage of the formal financial system for all members; of an economy.” However, Demirgüç-Kunt and Klapper (2013) present a more comprehensive definition as “inclusive financial system is a mechanism that warrants wide-ranging access to financial products and services without price barriers to the weaker section and other disfavored groups.” Based on these definitions, it can be deduced that the dimensions to assess the extent of financial inclusion comprising four primary factors: access, availability, usage, and cost of financial services.

Over the past two decades, much of the inclusive finance literature has clustered around how to measure and promote it (Prabhakar, 2019). Likewise, Sarma (2008) developed a multi-dimensional financial inclusion index by applying an approach similar to the one adopted in UNDP’s human development index (HDI) calculation. The author employed three dimensions that are banking penetration (accessibility) measured by the number of bank accounts per 1,000 population, usage measured by the volume of credit and deposit as a proportion of the country’s GDP, and availability of banking services measured by the number of bank outlets per 1,000 population. Similarly, following the dimensions presented by Sarma (2008) and Vo et al. (2021) constructed a financial inclusion index for 18 developing Asian economies using different dimensions of the inclusive financial system, for example, availability, accessibility, and usage. The result confirmed that financial inclusion alleviates poverty and income inequality.

To calculate a comprehensive financial inclusion index (Arora, 2010) applied supply and demand indicators to compute the financial access index. The author used three dimensions, namely demographic and geographic penetration, ease, and cost of transactions. According to the UNDP method, the author examined the degree of the inclusive financial system in developed and developing countries. Arora (2010) asserted that extended access to finance facilitates and supports economic development. The author continued that growth in the financial systems cannot be achieved unless finance is accessible to all and barriers to access are removed.

Other extant cross-country studies were conducted by Demirgüç-Kunt and Klapper (2013) for 148 countries and by Allen et al. (2016) for 123 nations. The authors examined the underlying characteristics of individuals and governments, related to accessibility and usage of formal financial services. These investigations uncovered that affordability (cost) and unrestricted access to financial services were positively associated with increased account use and ownership. They also established that personal income inequality affects the level of financial inclusion in all the countries. Furthermore, in line with Allen et al. (2016), Demirgüç-Kunt and Klapper (2013), and Fungáčová and Weill (2015), also conducted a cross-country study on BRICS countries to examine the individual-specific characteristics associated with access to financial services. The findings reveal that demographic characteristics (e.g., education, income, age, and gender) are significantly and positively related to the use of formal financial services (e.g., official account ownership and credit).

Very few existing studies have computed the comprehensive financial inclusion index from demand-side perspectives. To compute financial inclusion, Lal (2018, 2019) documented five dimensions (e.g., access, availability, usage, quality, and impact). These studies were designed to examine the impact of inclusive finance on poverty alleviation and rural development, respectively. The studies highlighted that financial inclusion directly and significantly affects poverty reduction and rural development, respectively (Lal, 2018, 2019). Similarly Nandru and Rentala (2019) conducted a study on Indian primitive tribal groups. They considered five dimensions (e.g., ease of access, availability, physical proximity, affordability, and usage) to measure financial inclusion and ascertain its effect on the socio-economic condition of the beneficiaries. The study reveals that financial inclusion positively and significantly impacts the socio-economic situation of its beneficiaries. Hence, this research hypothesized the following:

Financial Inclusion and Disposable Income

Inclusive finance is a contemporary issue essential for poverty alleviation, income equality, and economic growth. Its relevance in the political community can realize social cohesion and economic sustainability (Sarma, 2008; Sarma & Pais, 2011). It is a prerequisite for job creation and poverty reduction. An inclusive financial system revamps living standards and allows low-income communities to save and borrow to create assets and invest in their education and businesses (Mehrotra et al., 2015). Moreover, expanding access to credit for the poor helps them come out of poverty and enables them to invest in human capital and microenterprise, thereby reducing overall poverty by promoting economic growth (Li, 2018; Vo et al., 2021).

It is believed that access to finance can help overcome financial constraints. Therefore, it can be a significant factor for sustainable human and economic development (Raza et al., 2019). It provides much-needed financing for entrepreneurship, particularly for micro and small business development. This, in turn, allows them to make better business decisions, facilitating business expansion, creating jobs, and supporting economic prosperity. These arguments are in line with inclusive growth theory (Samans et al., 2015) and socio-economic theory (Bradshaw, 2007). Therefore, these theories have now become a policy requirement for governments around the world. Inclusivity has become a significant component of any effective growth strategy (Deblock & Haji, 2008). This vision captures the imaginations of those looking for alternative models of social and economic change (Adegbite & Machethe, 2020). Some studies highlight that inclusive finance can increase income and savings by allowing previously underserved people to invest in necessities such as financial risk management (Demirgüç-Kunt & Klapper, 2013). They continued that adequate financial services such as transfers, micro insurance, payments, loans, and savings could stimulate business activity and help increase household income. Hence, this research hypothesized the following:

The Mediating Role of Opportunity Effect

Opportunity effect is measured in terms of economic opportunity which is defined as the potential benefits an individual can take to thrive in a financial system (Demirgüç-Kunt et al., 2008). Inclusive finance is a means to an end, not an end in itself. A well-functioning financial system helps enrich the entire country and empowers individuals and households, especially vulnerable groups (Mehrotra et al., 2015). Access to various financial services has opened the door for individuals and households to build savings, smooth out their consumption, make investments, and equip them to meet emergencies. It enables businesses to grow, create jobs, and reduce inequality. Financial inclusion acts as a bridge between economic opportunity and outcome. It is essential for operationalizing policies that can sustain growth effectively and more efficiently (Zulfiqar, 2017).

A considerable body of work on inclusive finance postulated that expanding access to financial resources can ensure much-needed financing for education, daily consumption, and business activities. Besides, it guards customers in the face of adverse shocks. These opportunities make people more productive and efficient economic agents and ultimately lead to poverty alleviation and human development (Aghion & Bolton, 1997; Vo et al., 2021). An all-inclusive financial system fosters a range of efficient financial services that can amplify beneficiaries’ efficiency, welfare, and income level (Sarma & Pais, 2011). This is what inclusive growth brings forth, that is, reduction in inequality and expansion in economic opportunities, specifically social inclusion, health, and education, as an outcome of growth (Anand et al., 2013). Consequently, in the absence of an inclusive financial system, poor people and small businesses do not have any other option but to rely on personal wealth or domestic resources to invest in business and education or seize promising growth opportunities. Hence, this research hypothesized:

The Mediating Role of Growth Effects

In terms of inclusive growth, it is a process of extending the size of the economy by providing a level playing field to every individual without any discrimination (Ngepah, 2017). Therefore, for the socio-economic development of developed and developing nations compulsory access to financial services must be ensured. A well-developed financial system is crucial for growth and development (Sarma & Pais, 2011). Evidence from the seminal studies insinuates that unrestricted access to financial services plays a catalytic role in economic growth and development. A community with a well-inclusive financial system is a win-win situation for a country, economy, banking institutions, and most importantly, for low-income individuals. It can spur more robust and more balanced growth (Prabhakar, 2019).

Moreover, to assess the mechanisms linking finance and economic growth using cross-country and time-series analyses, Levine (2005) advanced that the services provided by financial markets and intermediaries exert a positive and first-order impact on the rate of long-run economic growth. Similarly, Demirgüç-Kunt and Singer (2017) noted that, once access to formal financial services improves, inclusion will bring multiple benefits to customers, regulators, and the economy as a whole. For example, existing studies show that improving the accessibility of financial services can facilitate empowering people to develop long-term consumption and investment proposals. Thus, it helps them participate in prolific economic activities (Li, 2018). Indeed, preliminary studies of financial inclusion have shown that greater accessibility to banking services significantly affects production and innovation and contributes to economic growth (Ayyagari et al., 2011; Levine, 2005). Likewise, recent literature also confirms that well-developed banking systems are closely linked to economic growth (Škare, et al., 2019; Uddin et al., 2013). Also consequently, through economic growth, there comes a significant improvement in poor people’s income level (Ngepah, 2017). The finance growth theory and inclusive growth theory correspond to these arguments (Anand et al., 2013; Rajan & Zingales, 1998). Hence, this research hypothesized:

The Mediating Role of Distribution Effects

The distribution effect in terms of inclusive growth is defined as a process of making benefits available directly to the beneficiary system (Demirgüç-Kunt et al., 2008). A growing body of empirical and theoretical evidence on financial inclusion argues that a well-structured financial system can serve low-income groups and assist in alleviating poverty (Beck et al., 2014; Dabla-Norris et al., 2015). Consequently, improving the availability of financial services is of enormous significance in improving the economic conditions of low-income households (Li, 2018). Because the role of finance in poverty reduction has always been valued, policymakers have sought to provide quality financial services to the poor on a broader scale (Hussain et al., 2019). However, certain social groups continue to be systematically disadvantaged because of discrimination based on their ethnicity, religion, caste, gender, age, disability, and immigration status (Prabhakar, 2019).

It is argued that financial inclusion helps solve the underlying problem of equitable growth by empowering individuals socially and economically (Adegbite & Machethe, 2020). It enables the poor to overcome poverty at all levels, improve their living standards, and stimulate growth and development through equitable distribution of wealth (Škare et al., 2019). But balanced growth will remain a mirage unless it includes all the sections of the society, reduces poverty, and generates employment opportunities for low-income and marginalized segments (Amponsah et al., 2021). Similarly, inclusive growth theory holds that balanced growth cannot be realized until all segments are placed on equal footing with other segments in reference to economic development. It broadens the development agenda and, above all, incorporates the major components of an effective poverty alleviation strategy (Anand et al., 2013).

Unfair distribution of economic opportunities through distribution channels can lead to significant income inequality and harm individual well-being (Atkinson & Bourguignon, 2014). For example, one of the main obstacles to the inclusiveness of vulnerable groups is the limited opportunity offered by financial institutions. It might be because they only seek profit and prevent the complexities of purveying services to the low-income group (Prabhakar, 2019). Likewise, when creditworthy borrowers are denied credit due to imperfect information and collateral, their lack of income or wealth limits their investment options (Adegbite & Machethe, 2020). Consequently, a lack of investment harms growth and causes income inequality. Therefore, improving and expanding the distribution of financial services without discrimination can enhance income and expedite the growth process by providing a level playing field for economic opportunities. Hence, this research hypothesized:

Methodology

Nature and Scope of Research

This research used a cross-sectional study design because it is efficient and capable of collecting larger data sets quickly and eliminating repetitive errors in the survey questionnaire. In addition, the study was both quantitative and descriptive. The scope of this research is limited to the three most impoverished districts of Punjab, namely Rajanpur, Muzaffargarh, and Dera Ghazi Khan (A. Iqbal et al., 2020). The population in this study is low-income urban households, which is justified by the argument (Honohan, 2008) that the poor also save, borrow money, and use other financial services throughout their lives.

The Originality of the Study

The relationship between inclusive finance and disposable income has unique implications for low-income households, but previous research has largely ignored these issues. Previous research on financial inclusion was mainly conceptual, and empirical research based on publicly available data is scarce (Khan et al., 2022). Some of those studies seem worthwhile and deserving of investigation with regard to low-income households. Due to a lack of rigorous research, there appears to be an empirical gap in the existing literature. Therefore, on these issues, an empirical investigation is important as it provides policy shifts to tackle poverty. Besides, there is not a single study till now which has attempted to test the empirical relationship between financial inclusion and disposable income. In addition, there is very little research conducted on demand-side perspectives of financial inclusion, that is, from the customers’ point of view. Also, the extent of financial inclusion is much more affected by the demand side factors as compared to the supply side factors, that is, factors from the perspective of financial institutions and their staffs (Kempson, et al., 2004). Hence, this research work has attempted to empirically determine the contributions, of financial inclusion from the demand-side perspective on disposable income.

Besides, existing demand-side studies specifically focused on rural contexts through cooperative banks (Lal, 2018, 2019; Nandru & Rentala, 2019) or based on gender empowerment (Bhatia & Singh, 2019). However, they ignored the urban perspectives and impact of commercial banks, which provide financial services to a vast population segment. Also, the extant studies have failed to address some contradictions in the previous research findings (Montgomery & Weiss, 2011; Swamy, 2014). Consequently, we have identified the existing evidence gaps in the previous research works which contradict in their findings. Furthermore, previous studies lack robust quantitative research methodology; therefore, we have identified a gap. In the present investigation, the researcher, therefore, seeks to establish a new inquiry using a better technique, that is, structural equation modeling (SEM). In order to estimate causal relationships, this technique is better as it estimates both direct and indirect relations at the same time. The researcher seeks to extend the literature by addressing all these gaps in new ways and with a better research methodology.

The other motivations for testing the aforementioned relationship are irrefutable and multifaceted. First, financial inclusion is very low in Pakistan, that is, 79% of adults in Pakistan are unbanked, and 13 have inactive accounts. Additionally, borrowings, pension, and insurance coverage are 3%, 7%, and 7%, respectively (Demirgüç-Kunt & Singer, 2017). Second, the government and SBP are trying to increase the number of banked adults, but their effects have not yet been evaluated. However, the literature on the state of financial inclusion among low-income urban households is mainly unexplored. Therefore, the current research is positioned to address all these gaps by estimating the financial inclusion of the urban poor and what impact does it have on disposable income.

Pilot Study

In the present study, a pilot test of the questionnaire involving 60 beneficiaries was carried out before the main study, with samples not used in the main study (Van Teijlingen & Hundley, 2002). All ambiguous, double barrel, negative worded, and abstruse items were deleted from the final survey questionnaire, as the simpler, the better. Ultimately, a questionnaire containing 53 items was finalized to collect the necessary information from the beneficiaries of the financial inclusion.

Scale Development

The responses for the current study were collected using a self-developed questionnaire. Since no research article witnessed a well-developed scale so after an extensive review of literature, discussions with the specialists and experts from the field, and following several rounds of suggestions and editing, a questionnaire containing 53 items was finally prepared for collecting the requisite information from the respondents. The final questionnaire was divided into two sections; section A collected demographic information of the respondents, and section B collected the information regarding various dimensions of financial inclusion, disposable income, opportunity effect, growth effect, and distribution effect. Out of 53 items, 7 items were related to demographic information and 46 related to the hypothesized relationship. The scale developed and the items are presented in Supplemental Appendices 1 and 2.

Sample Technique and Sample Size

The population of this research comprised 229,847 households residing in the three districts of Punjab (Pakistan Bureau of Statistics, 2021). Since the income level of the respondents was a chief criterion for their selection (belonging to different professions, e.g., worker, day laborer, maids, gardeners, drivers, etc.). Therefore, the purposive sampling technique was more feasible to use than any other. In addition, the criteria applied were availability and readiness to respond. Furthermore, a sample of 400 respondents was acquired using formulae recommended by Yamane (1973). The conceptual model of all hypothesized relationships is given below in the Figure 1.

Conceptual and empirical framework.

Data Collection

To meet the objective of the current study, heads of low-income households were chosen as our main inquiry unit. In aggregate, 1,050 respondents were contacted. Among them, 502 substantial responses were received. The collected responses were then analyzed and sanitized. Eighty responses were eliminated due to missing or incorrect responses and straight-lining (Y. Kim et al., 2019). Besides, 22 responses were treated as outliers in the initial screening using the Mahalanobis distance test which is used to identify aberrant responses. Therefore, they were removed. Thus the final sample arrived at 400 respondents with an effective response rate of 38.09%. This study adopted a seven-point Likert scale to collect data, where “7” implies “strongly agree” and 1 indicates “strongly disagree.” Table 1 represents the demographic profile of respondents. In this research, Helsinki’s declaration on research ethics was considered. Moreover, Skewness −0.985 to −0.085 and Kurtosis −1.391 to 0.259 indicate that the data is distributed normally.

Demographic Profile of the Households.

Data for the current study were cumulated in 6 months from December 2020 to May 2021 from the three districts of Punjab by three research assistants. The research assistants were hired from the same districts that were selected for the study. The research assistants so hired addressed the issue of nonresponsiveness caused by communication barriers and assisted the author in collecting data. The questionnaire was directed exclusively to the respondents through personal visits to their homes.

Common Method Bias

It reflects biasness in a data set which caused due to the instrument. For instance, employing a single method in data collection process, that is, through online survey. It can either inflate or deflate responses due to systematic response bias. A single factor in a study can explain most of the variance if a study has significant common method. To see if most of the variance is explained by a single factor the researcher used Harman’s single factor test in this study.

As the survey was done using single method (i.e., by personal visiting) and on the single group of society (i.e., low income unbanked adults). Thus, based on above argument the researcher have used Harman’s single factor test to find out if there exist common method bias in this study. The result reveals that percentage of variance explained by single factor was 41.215% which was less than the 50% (Podsakoff et al., 2003) threshold so there is no common method bias in this study.

Data Analysis

Exploratory Factor Analysis (EFA)

The technique of EFA is mainly adopted during the scale development process to specify construct dimensions (Reise et al., 2000). This technique primarily aims to simplify numerous inter-correlated measures into several representative factors (Ho, 2006). In this study, the exploratory factor analysis technique was performed using Principal Component Analysis and Varimax rotation. Two critical measures are used to test the appropriateness of factor analysis. First, a measurement that gives the adequacy of the overall sample is Kaiser–Meyer–Olkin (KMO) measure (Kaiser, 1974). KMO statistics range from 0 to 1. Second, another measurement is Bartlett’s test of sphericity.

The EFA results identified eight factors from the 46 items having factor loads between 0.55 to 0.91. The factor analysis presents variance explained at 87.12% for eight factors. The estimated values of Cronbach’s alpha for the eight factors ranged from .92 (OEffect) and .982 (Acc); all these values were above the threshold of .77 (Gordon & Narayanan, 1984), indicating high consistency. The value of Kaiser–Meyer–Olkin (KMO) measure arrived at 0.947 (more than the cutoff value 0.7), showing that sampling adequacy is good and Bartlett’s Test of Sphericity was statistically found significant with p-value <.05, that is, equal to .000 denoting a significant correlation exist amongst the factors under consideration as depicted in Table 2. The factors having an eigenvalue equal to or higher than 1 and factor loadings greater than 0.5 were held for further analysis, as described in Table 3. This entails that the measurement is good. The item loadings, Cronbach’s alpha, percentage of variance explained, and cumulative variance are presented in Table 3.

KMO and Barlett’s Test.

Exploratory Factor Analysis.

Confirmatory Factor Analysis (CFA)

CFA is used to test how well the observed variables represent smaller constructs (Byrne, 2010). The primary objective of employing CFA was to assess the reliability, validity, and model fit indices. To estimate the accuracy and validity of the measurement model, the statistical values of standardized factor loadings, composite reliability (CR), critical ratio, and average variance extracted (AVE) were examined.

To improve the measurement model (validity, reliability, and model fit) and particularly GFI value which was 0.667, seven items, namely OEff6 with loading 0.485, OEff7 with loading 0.456, GEff6 with loading 0.519, GEff7 with loading 0.505, DEff6 with loading 0.481, DI8 with loading 0.409, and DI9 with loading 0.430 were removed from the CFA model. The items having loadings equal to or greater than 0.7 were retained (Hair, Matthews, Matthews, & Sarstedt, 2017). Furthermore, removed items were less than 20% of the questionnaire (Hair, 2009; Hair, Babin, & Krey, 2017).

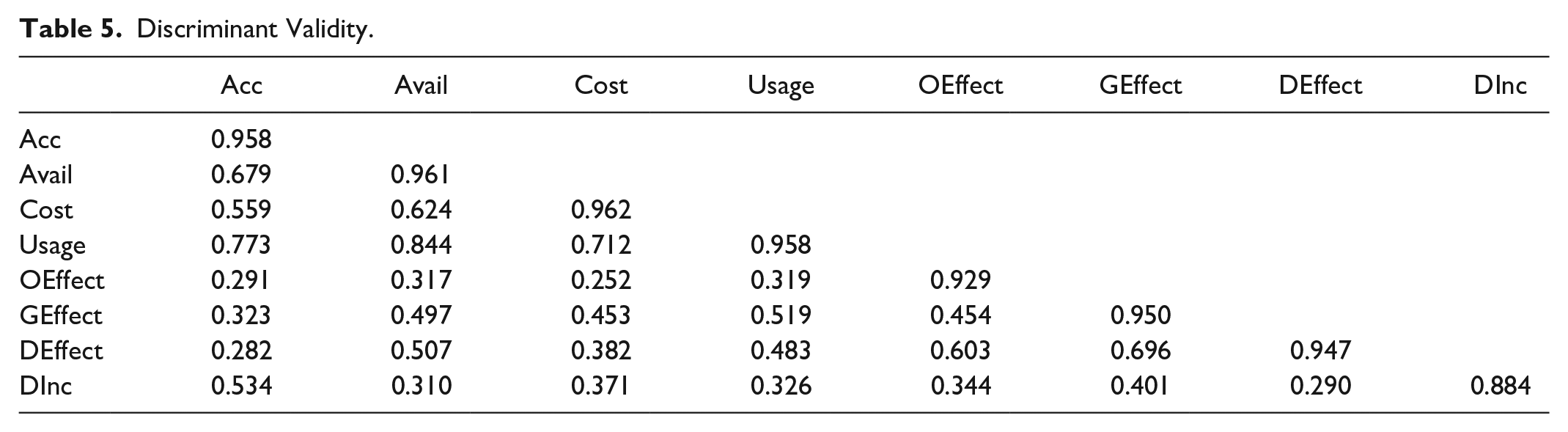

The CFA has been performed again on 39 items. The composite reliability for each factor exceeded the minimum level of .7 (Hair et al., 2011). It ranged from .961 to .982, as shown in Table 4, and the critical ratios are also more than the threshold value of 1.96 and statistically found significant at a p-value less than .001. The resulting values of AVEs were more than .5 and ranged from .782 to .926, implying convergent validity. The results in Table 5 indicated that there was no discriminant validity issue.

Confirmatory Factor Analysis.

Denotes the p-value significant at .001.

Discriminant Validity.

Hair (2009) advocated presenting three to four model fit indices to verify model fitness. Therefore, the results obtained through confirmatory factor analysis are χ2 = 1,298.243, CMIN/DF = 1.929, p < .05, goodness-of-fit index (GFI) = 0.86, root-mean-square error of approximation (RMSEA) = 0.048. Some additional fit indices such as average goodness of fit (AGFI) = 0.837, incremental fit index (IFI) = 0.976, comparative fit index (CFI) = 0.976, Tucker–Lewis index (TLI) = 0.974, normed fit index (NFI) = 0.952 as depicted in the Table 6. All factor loads were more than 0.50 and were statistically significant at p < .000 (Fornell & Larcker, 1981). Thus, the results confirm the fitness of the measurement model. The measurement indices are presented in Table 6.

Model Fit for Measurement Model.

Denotes the p-value significant at .001.

Structural Equation Modeling (SEM)

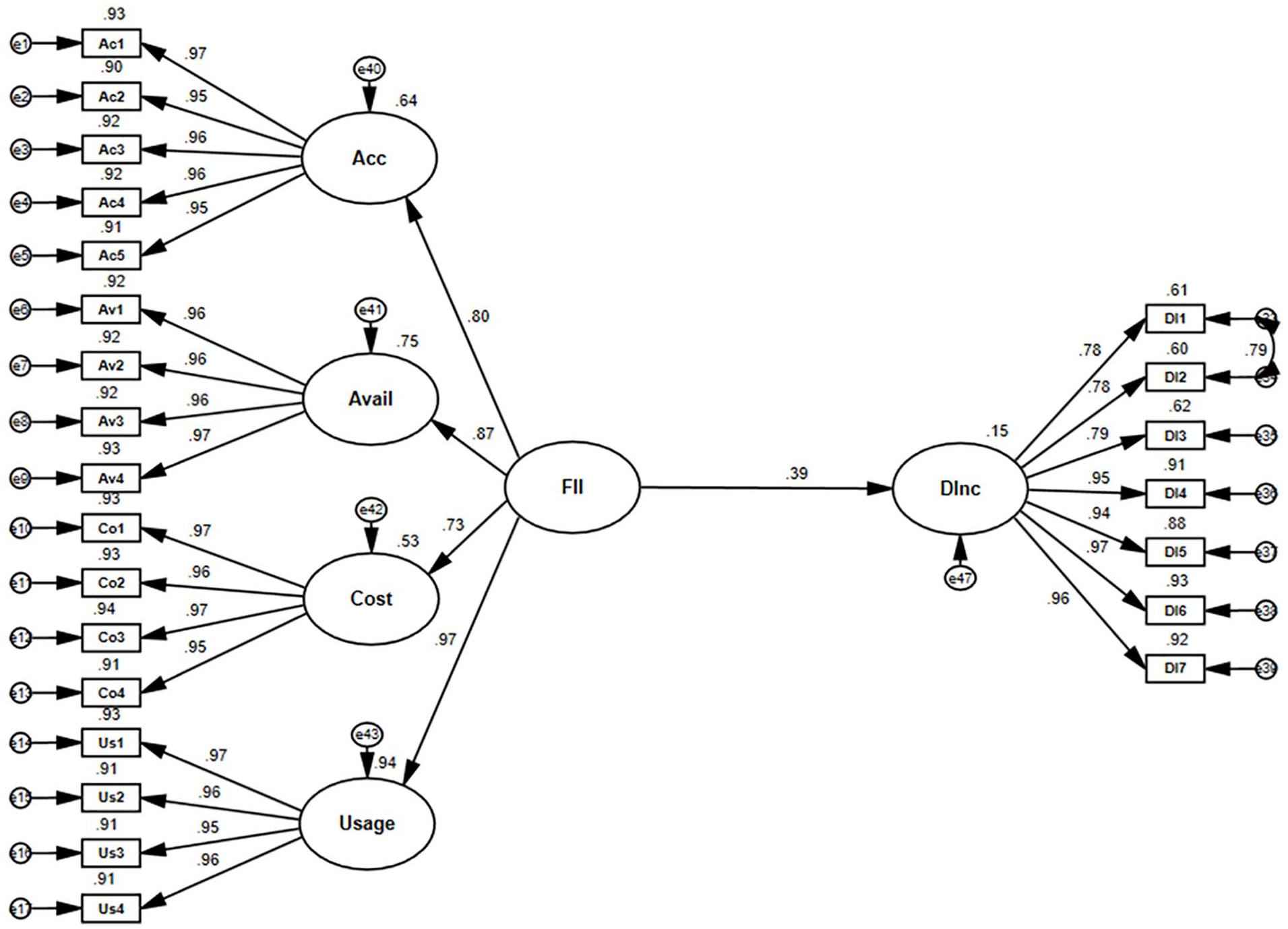

After administering confirmatory factor analysis CFA and verification of reliability, validity, and model fitness, SEM is performed to assess the fitness of the structural model and the proposed hypotheses of the study (Hair, 2009). In SEM, each item or indicator is linked to its underlying theoretical construct by single-headed arrows following the study’s hypotheses. The results from SEM affirmed that Usage, Avail, Acc, and Cost significantly predict financial inclusion, as reflected in Figure 2 and Table 7. Thus, H1a, H1b, H1c, and H1d stand accepted.

Structural model without mediation.

Direct and Total Effects.

Significance of estimates: ***p < .001. **p < .010. *p < .050.

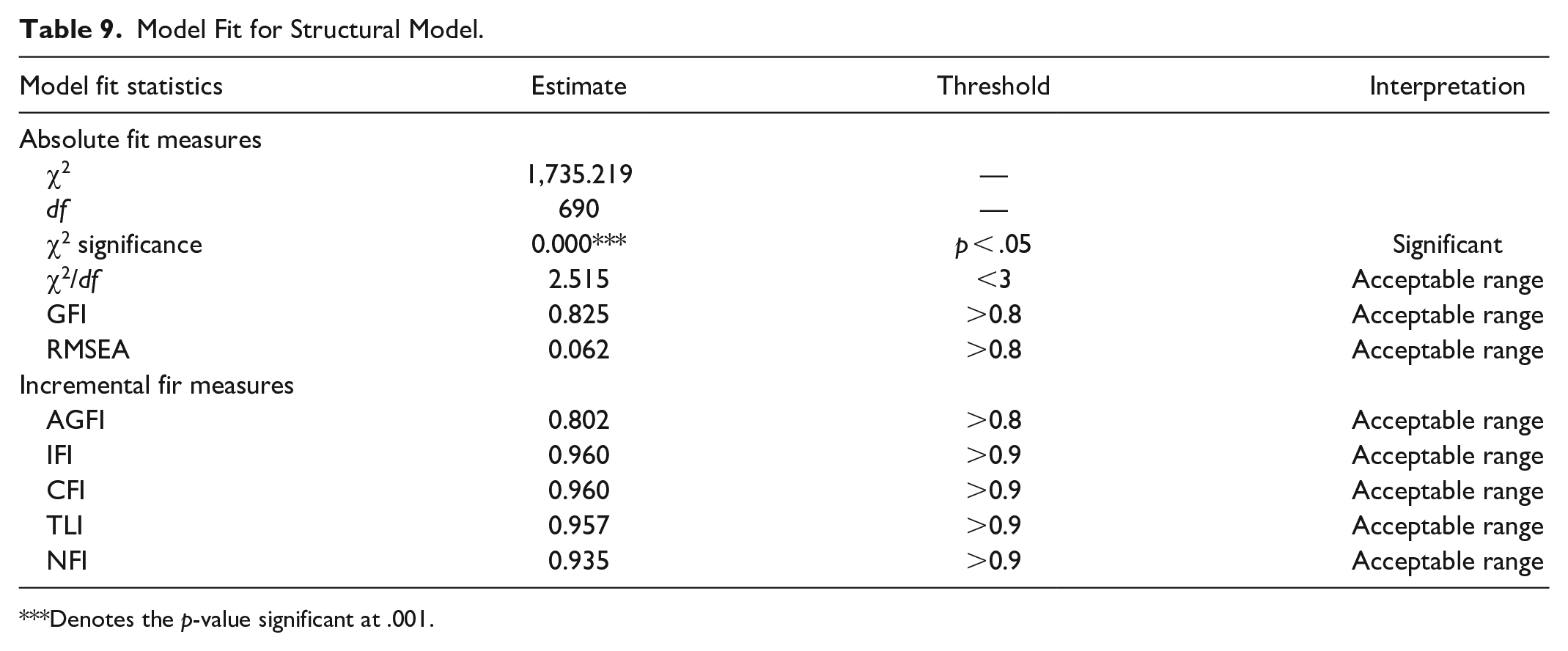

Overall, the current structural model contains (1) path from FII to OEffect, (2) path from FII to GEffect, (3) path from FII to DEffect, (4) path from FII to DInc, (5) path from OEffect to DInc, (6) path from GEffect to DInc, and (7) path from DEffect to DInc. The proposed model strived to identify the financial inclusion impact on the disposable income of low-come urban households. By using eight reliable and valid factors, the proposed model is tested in this section. The model fit indices of the proposed indirect structural model (χ2 = 1,735.219, CMIN/DF = 2.515, GFI = 0.885, RMSEA = 0.062. AGFI = 0.802, IFI = 0.960, CFI = 0.960, TLI = 0.957, and NFI = 0.935) indicated that all these fitness indices have acquired their threshold values (Byrne, 2010; Doll et al., 1994; Hair, 2009). These values are presented in Table 8.

Indirect Effects.

Significance of estimates: ***p < .001. **p <. 010. *p < .050.

Hypotheses Testing for Direct Relation

Based on SEM results, the framed hypotheses have been tested (Table 7), and the results are as under:

H1a: Access significantly predicts the FII.

H1b: Availability significantly predicts the FII.

H1c: Cost significantly predicts the FII.

H1d: Usage significantly predicts the FII.

It is evident from the results obtained through SEM (Figure 2 and Table 7) that Usage, Avail, Acc, and Cost significantly predict FII. Thus, hypotheses H1a, H1b, H1c, and H1d stand accepted. The results further depict that in order of precedence, usage with (β = .967) emerges as an important and most significant factor of financial inclusion. Subsequently, Avail (β = .867), Acc (β = .800), and Cost (β = .731) followed respectively.

H2: FII has a significant impact on disposable income.

H3a: FII has a significant impact on the opportunity effect.

H4a: FII has a significant impact on the growth effect.

H5a: FII has a significant impact on the distribution effect.

SEM results indicate that FII has a direct and significant impact on disposable income (β = .386, p = .000), opportunity effect (β = .379, p = .000), growth effect (β = .568, p = .000), and distribution effect (β = .540, p = .000). Therefore, hypotheses H2, H3a, H4a, and H5a are accepted, as stated in Table 7. The results also demonstrated that financial inclusion with (β = .386, p = .000) has a significant impact on the disposable income of the low-income in urban Pakistan. With this finding, it can be stated that an increase in the level of financial inclusion tends to raise the level of disposable income of low-income households.

H3b: The opportunity effect has a significant impact on disposable income.

H4b: The growth effect has a significant impact on disposable income.

H5b: The distribution effect has a significant impact on disposable income.

It is inferred from SEM results that opportunity effect (β = .221, p = .000) and growth effect (β = .265, p = .000), has significant impact on disposable income. However, distribution effect (β = −.161, p = .000) has significant but negative impact on disposable income. Hence, H3b, H4b, and H5b stand accepted as stated in Table 7. Based on these results, it can be concluded that an increase in the opportunity and growth effect leads to an improvement in the level of disposable income the low-income in urban Pakistan. In contrast, a change in distribution effect negatively affects disposable income (Figure 3).

Structural model with mediation.

The Mediating Role of Opportunity Effect, Growth Effect, and Distribution Effect

The mediation effect exists when a predictor variable affects the dependent variable through a mediator (Baron & Kenny, 1986). In the present study, the relationship between financial inclusion, opportunity effect, growth effect, distribution effect, and disposable income has been assessed. To evaluate whether there exist mediating effects between the independent and dependent variables or not, Baron and Kenny (1986) proposed four underlying conditions that must be met before performing the mediation test. These conditions are (i) the relationship between predictor and outcome variable must be significant, (ii) the relationship between predictor and mediator variable must be significant, (iii) the relationship between the mediator and outcome must also be significant, and (iv) when the mediator is entered into the equation, the relationship between independent and dependent variables becomes insignificant, which is according to Hair (2009) termed as full mediation. However, under condition (iv), if the predictor variable reduces but continues to be significant, this condition is termed partial mediation. In further detail, it signifies that the predictor variable impacts the outcome variable both directly and indirectly.

All of these conditions except (iv) have been tested and satisfied in the previous section, and the hypotheses H2, H3a, H3b, H4a, H4b, H5a, and H5b are accepted. Thereupon, to test the mediating effect, we added the mediating variables, that is, opportunity effect, growth effect, and distribution effect between FII and disposable income, in the last step. The result revealed that when the mediators as mentioned earlier are entered into the FII and disposable income equation, the relationship between FII and disposable income remains significant (β = 0.251, p = .000), which implies partial mediation as reflected in Table 9.

Model Fit for Structural Model.

Denotes the p-value significant at .001.

The SEM results also indicated that opportunity effect (β = .084; p < .05), growth effect (β = .150; p < .05), and distribution effect (β = −.087; p < .05) significantly mediates the relationship between financial inclusion and disposable income with bootstrap results as reflected in the Table 8. This implies that the inclusion of opportunity and growth in the relationship mentioned above boosts the impact of financial inclusion on the disposable income of low-income urban Pakistan by 8.4% and 15%, respectively. At the same time, it also established that the distribution effect is significantly but negatively linked in the relationship between financial inclusion and disposable income. Therefore, this confirms our hypotheses H3, H4, and H5. The figure indicating multiple paths for the hypothesized relationship is given below in Figure 4.

Multiple paths between financial inclusion and disposable income.

Findings and Discussion

Findings and Discussion

Recently, the government of Pakistan and the State Bank of Pakistan has taken several initiatives to increase the level of financial inclusion. However, to reap the maximum benefits of financial inclusion, it is essential to reach the low-income population, which has the tendency to remain excluded. Bearing this in mind, the researcher has performed an investigation to ascertain the role of financial inclusion on disposable income. The results of this study empirically confirmed the proposed model represented in the study. Therefore, it is now empirically established that financial inclusion can be estimated using its four factors, that is, access, availability, cost, and usage. Moreover, among the four factors of financial inclusion, based on significance level and standardized regression path coefficients, the strongest to lowest predictors are usage, followed by Avail, Acc, and Cost. This signifies that reaching the low-income urban households in Pakistan Usage is the major contributing factor of financial inclusion. It can, thus, be deduced that while many factors are significant, usage takes precedence within the frame of low-income urban households. Therefore, it is imperative to improve and encourage the usage of financial services among the low-income urban households in Pakistan. In addition, government, financial sectors, and policymakers should adopt a proactive approach in this regard. The results further depict that the relationship between financial inclusion and the disposable income of low-income urban households is statistically significant. With this finding, it can be stated that an increase in the level of financial inclusion tends to raise the level of disposable income of low-income households. This empirical result confirms the causality between financial inclusion and disposable income. This is in line with L. Li (2018), who argued that financial inclusion significantly enhances the income of poor households. Swamy (2014) also supported this view and postulated that taking part in inclusive financial systems has substantially increased the households’ income of women. However, Montgomery and Weiss (2011) used the difference with the control in their study in Pakistan. The author selected 1,454 Khushhali Bank clients and the same number of non-clients from the same village, and the results showed no impact on income growth. The results further show that the opportunity and growth effects have a significant and positive mediating relationship between financial inclusion and disposable income. However, the mediator distribution effect has a significant but negative relationship between financial inclusion and disposable income. Moreover, the growth effect is the strongest mediator in the relationship above. All these empirical results confirm the mediation between financial inclusion and disposable income. These findings also support the theory of inclusive growth and socio-economic theory.

In our study, the opportunity effect through inclusive finance significantly and positively affects the relationship between financial inclusion and disposable income. Based on these results, it can be concluded that an increase in the opportunity leads to an improvement in the level of disposable income of the low-income in urban Pakistan. This empirically confirms the causality of the hypothesized relationship. The results are in line with Brune et al. (2011), who argued that increasing opportunities to access various financial services in rural Malawi had facilitated the lives of poor households because they can use their savings for agricultural inputs. Ardic et al. (2011) also supported this view and asserted that access to a range of financial services by low-income households could empower them economically and socially and assist them in escaping from poverty. Besides, the growth effect through inclusive finance also has a significant and positive impact on the relationship between financial inclusion and disposable income. These results insinuate that an increase in the growth leads to an improvement in the level of disposable income of the low-income in urban Pakistan. Also, the growth effect is the strongest mediator among all; therefore, it has a great impact in affecting disposable income. This empirical result establishes the causality between financial inclusion and disposable income. This finding is congruent with D. W. Kim et al. (2018), who stated that improved access to financial services could expedite economic growth. The author continued that difficulties in accessing financial services in the least developed world are the leading causes of low earnings. Several authors also confirmed that well-developed banking systems are closely linked to economic growth (Levine, 1997; Škare et al., 2019). And consequently, through economic growth, there comes a significant improvement in poor people’s income levels (Ngepah, 2017).

In the current study mediator, distribution effect has a significant but negative relationship between financial inclusion and disposable income. Based on these results, it can be concluded that a change in distribution effect negatively affects disposable income. This empirical result establishes the causality between financial inclusion and disposable income. It might be due to multiple reasons, including socio-economic and political instability and concentration of wealth in few hands. This is compatible with the view, Z. Iqbal (1997) who affirmed that interest-driven financing leads to the income concentration in few hands. However, the principle of profit-and-loss sharing in the financial system leads to a more equitable distribution of economic opportunities in the long-run. Prabhakar (2019) argued that as more people become financially included in the economic system, there will be a higher level of investment in real or productive activities leading to higher output, income per capita, and, by extension, reducing income inequality. However, according to Global Findex, the state of financial inclusion in Pakistan is abysmal (Demirgüç-Kunt & Singer, 2017). Only 21% of adults have a formal account, and access to credit is also meager. Only 3% take loans from a traditional financial sector, leading to a low level of investment (Demirgüç-Kunt & Singer, 2017). Consequently), due to the low level of investment, employment creation adversely leads to a rise in income inequality (Dabla-Norris et al., 2015; Mitkov, 2020). The income of the privileged class tends to increase while the income level of the low-income group remains low.

There may be other reasons for the negative impact of the distribution effect as Haq (1973) postulated that the socio-economic setup of Pakistan primarily benefits the rich class at the expense of the poor. He continued that the capitalistic system of Pakistan is still the world’s most primitive one. The Chief Planning Commission of Pakistan in 1973 underlined that only 22 families had owned 70% of insurance, 80% of banking, and 75% of the industrial assets in Pakistan, which is the main obstacle in ensuring all-inclusive growth. Other reasons include political lending (Dinç, 2005; Saeed et al., 2015), which keeps the marginalized group excluded, and only the elite class could benefit from such services. Moreover, inflation, wealth accumulation in a few hands are also the major causes of concern. These views are supported by H. Li and Zou (2002), who conducted a systematic, cross-country analysis on how inflation affects income distribution. They found that, first, inflation worsens the distribution of income. Second, it increases the income share of the rich; third, it negatively affects the income shares of the poor and the middle class; and fourth, it reduces the rate of economic growth. Furthermore, Dao (2008) and Barrier (2017) substantiate this view and posit that a low level of economic development does not improve the income level of low-income groups. Kuznets’s (1955) findings also corroborate this perspective. In the early stages of economic growth, income distribution deteriorates due to wealth accumulation by the rich, and subsequently, improvements in income distribution occur (Kuznets, 1955). In addition, the unfair distribution can be attributed to financial instability as the financial system in Pakistan is still in its primitive stage and facing instability since its evolution. Y. Kim et al. (2019) uphold this argument that the instability in the financial system aggravates the distribution of income and engenders income inequality.

Conclusion

Considering financial inclusion, a most crucial challenge to the recent world, it can be construed that it is highly important to respond. Multiple techniques and approaches have been considered since its inception and identification. But any problem could only be addressed if we exactly know the current status of the problem. Though the current situation of financial inclusion is very poor in Pakistan, it is now acknowledged fact that it has the potential to transform the quality of life.

In the present investigation by using an alternative approach through primary data we were able to empirically establish that financial inclusion has a significant direct and indirect impact on disposable income. One of the main contributions of our research is that we combine financial inclusion with opportunity effect, growth effect, and distribution effect as mediators through the lens of inclusive growth. However, the distribution effect is proven to be a significant but negative mediator in the aforesaid relation. Evidence confirms that financial inclusion with opportunity and growth effects provides a better model for explaining the scope of financial inclusion for low-income urban households from the perspective of developing countries, focusing mainly on Pakistan. The study presents sufficient evidence to conclude that the opportunity effect and the growth effect increase the disposable income of low-income households. This implies that through an inclusive financial system, the disposable income of households tends to rise, especially in communities with strong opportunity and growth effects.

Since we have applied a more robust technique to get results, therefore the findings of this research are more compatible as compared to previous contradictory findings. Also, in this study, financial inclusion is empirically proven to be a significant contributor to enhancing disposable income. Therefore, we were able to substantiate that government and the SBP are on the right track to boost financial inclusion among the general population to combat poverty.

The findings of this research can serve as a guiding principle for policymakers and financial institutions. Moreover, the findings highlight that the banking sector should take necessary efforts to improve the level of financial inclusion and avoid if any constraints in the inclusion of low-income households. This could tend to increase the disposable income of low-income and underprivileged populations.

Research Implications

Results suggest that the inclusiveness of low-income households can enhance their disposable income. Therefore, policymakers, government, and practitioners should (1) draft provisions and regulations to ease the participatory process and facilitate the excluded segments of the society in using necessary financial products and services. (2) The government, through the SBP, should enhance inclusiveness through digital and non-digital means. (3) The authorities should direct their attention to encouraging digital and cashless transactions. This will improve the availability of essential financial services to the marginal sections at an affordable cost and, consequently, enhance the efficiency of the financial sectors. Furthermore, (4) arrange financial literacy programs near low-income households and broaden the scope of inclusive finance beyond the current horizons. Finally, since opportunity and growth are significant mediators, policymakers are cautioned not to underrate their relevance in the relationship between financial inclusion and disposable income.

Limitations of the Study

Despite implications and practical significance, the present research was conducted amidst few limitations too. First, this could not reflect the outlooks of other stakeholders, in particular business correspondents, bank staff, and non-government organizations (NGOs). Second, the in-depth analysis of this research was geographically limited as all the respondents belonged to the three districts only due to time and resource constraints. Third, though every care has been taken in data collection and interpretation, however, in some instances, the possibilities of subjective interpretation cannot be prevented. Forth, the study is based on a cross-sectional study design combined with quantitative data while ignoring longitudinal and qualitative data. Fifth, the study considered formal financial institutions (commercial banks) only, while semi-formal and informal financial institutions are entirely overlooked. Finally, data were collected only from the low-income urban households of Pakistan. Thus, limiting the results to low-income urban households may not be generalized to other groups, including middle and upper-income groups.

Future Research

First, the investigation can further be carried out to uncover various other dimensions of inclusive finance. Second, a similar study can be replicated by considering a larger sample and even more than three districts to produce a more generalized result on a national level. Third, consider other important vulnerable groups in the society, namely disabled persons, women, youth, refugees, and middle-income groups. Fourth, future research can use a longitudinal research design, qualitative approaches, or mixed methods to examine the hypotheses set under this research. Fifth, future research could consider the perception of non-beneficiaries of financial inclusion.

Contributions to Theory and Practice

Considering these worthwhile findings, it is now evident that this study has made multiple contributions to theory and practice. The findings advance toward a broader understanding of financial inclusion discourse, specifically concerning the importance of financial inclusion on households’ levels of income. The study advances the debate on the relationship between inclusive finance and the disposable income of low-income urban households within the scope of inclusive growth theory. The research has identified a dire need for developing a formal financial system that can increase the status of financial inclusion, affect household income, and thus reduce poverty.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440221093369 – Supplemental material for The Financial Inclusion Development and Its Impacts on Disposable Income

Supplemental material, sj-docx-1-sgo-10.1177_21582440221093369 for The Financial Inclusion Development and Its Impacts on Disposable Income by Salman Mahmood, Wen shuhui, Shoaib Aslam and Tanveer Ahmed in SAGE Open

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.