Abstract

Researchers have found that the accumulation of assets through savings may serve a vital function in enhancing mental health and well-being. However, the question of how the status of savings affects the level of depressive symptoms in homeless persons remains largely unexplored. This study examines the relationship between savings and depressive symptoms in homeless individuals by utilizing the 2016 National Survey on Homeless People. We employed propensity score matching to reduce selection bias and multivariate logistic regression to probe the effects of savings on depressive symptoms. We found that after taking into account the covariates, a lower level of savings was associated with a higher level of depressive symptoms. Our findings imply that an asset-based policy orientated toward those facing homelessness could have a significant effect on reducing depressive symptoms.

Background

Between 1970 and 1996, South Korea (hereafter Korea) underwent rapid economic expansion, which significantly increased the country’s capacity to deal with poverty. However, the 1997 financial crisis caused an unprecedented economic burst in Korea. This economic burst incurred massive bankruptcies for many corporations, eventually resulting in elevated unemployment rates. As such, homelessness emerged as one of the critical social problems (Nam, 2001). In response, the Korean government has provided social resources to help those experiencing homelessness to foster their self-reliance, including rehabilitation services, housing facilities for a set duration, and creating public jobs for homeless individuals (Lee et al., 2007, 2017).

Despite the existence of government aid, prior research found that a significant number of individuals experiencing homelessness had difficulty leaving housing facilities due to a lack of self-reliance and confidence in economic activities (Park & Han, 2014). Prior research also highlighted that homelessness was related to feelings of helplessness and passivity (Nam, 2009). A survey conducted in 2016 found that 51.9% of people experiencing homelessness showed symptoms of depression. More specifically, 69.0% of the street homeless, 82.6% of the residents in jjokbang (a tiny, rented room where only one person can stay in an urban area), and 27.7% of the homeless living in facilities were found to have symptoms of depression (Lee et al., 2017). These findings underscore the prevalence of depressive symptoms as a substantial social problem within the homeless population (Lee et al., 2017).

Previous research utilizing asset-effect theory has revealed that savings can help to attenuate symptoms of depression and form positive views about the future, underscoring the vital role of asset-building in positively influencing individuals’ lives (Kang & Han, 2017, 2018; McKernan & Sherraden, 2008; Sherraden, 1991; Ssewamala et al., 2009). Specifically, drawing on the institutional saving theory, it has been found that even those from low-income groups can reap benefits from saving through asset-based policies and thus enjoy the positive effects of savings (Han et al., 2009). Sherraden (1991) pointed out that the act of savings itself may be as important as the amount because such acts can promote individuals’ future-oriented attitude, which can positively impact their mental health and eventually give them confidence in dealing with poverty.

Despite the importance of savings suggested by previous research, there is a lack of empirical focus on the impact of savings among the homeless population. Two studies from Korea have suggested that homeless individuals often find themselves excluded from institutional opportunities to save through asset-based policies, hindering their ability to accumulate assets (Han, 2019; Kang & Han, 2018). An earlier study by Park and Han (2014) also examined the potential effects of savings on homeless individuals, using surveys from staff at homeless centers in Korea. This research discovered that those experiencing homelessness faced severe depression and were in dire need of financial support for savings. The noteworthy finding of the study is that a significant number of homeless individuals managed to save money when incentivized. This suggests that it is possible to encourage homeless people to participate in savings for asset accumulation, which can mitigate their mental health issues (Park & Han, 2014).

In sum, while existing research has revealed important insights into the positive effects of savings, the exploration of its relationship with the mental health of homeless individuals, particularly in relation to depression, is largely under-researched. To fill this gap, this study aims to investigate the extent to which savings may be inversely associated with depressive symptoms among those experiencing homelessness. The current study employs the 2016 National Survey on Homeless People data for statistical analysis. Based on the results, the study can provide policy implications, specifically focusing on the significance of comprehensive asset-based programs designed for the homeless population.

Literature Review

Definition and Living Conditions of Homeless People

The Korean legislation, “Act on Support for Welfare and Self-reliance of the Homeless (Act No. 10784),” defines homelessness as a state of residing without a fixed address over a substantial duration, utilizing homeless shelters or living in homeless facilities over a protracted period, or inhabiting a location where housing conditions are profoundly deficient over a significant length of time (Korean Law Information Center, 2021).This legislative definition allows for the classification of homelessness to include those who find their sleeping quarters in public spaces such as parks or streets, those residing in homeless shelters, and individuals living in deplorably substandard housing (referred to as jjokbang in Korea). The living situations of street-dwellers and jjokbang residents are markedly unstable, as these individuals often vacillate between staying in shelters and sleeping in public areas (Nam, 2009). In 2018, the homeless population in Korea was estimated to be around 16,500, with a significant majority residing in urban locales (Lee et al., 2019).

Depression in Homeless People

Depression, a prevalent and severe medical condition, is characterized by feelings of sadness, helplessness, and discouragement, often triggered by the frustration and despair experienced in the course of one’s life (Radloff, 1977). Depression has deleterious effects on mental health (Beck, 1995) and increases the risk of suicidal ideation and behaviors (Perkins & Hartless, 2002). Previous work found that individuals experiencing homelessness tended to exhibit elevated levels of social disaffiliation and learned helplessness resulting from the psychosocial trauma inherent in their circumstances (Goodman et al., 1991). Moreover, previous studies found that socioeconomic factors (such as income and indebtedness), health status, the extent of disability, educational attainment, and employment status play a significant role in predicting depressive symptoms among the homeless population (Choi & Lee, 2019; Han et al., 2011; Kim, 2008; Nam, 2009; Shin, 2009).

Effect of Savings

The concept of savings indicates the willingness of individuals and households to accumulate assets to prepare for unexpected future events (Beverly & Sherraden, 1999). Previous research underscored the struggles of low-income and vulnerable groups, including homeless individuals, in saving money, as opposed to the middle and high-income classes, who can derive additional income through savings (McKernan & Sherraden, 2008; Sherraden et al., 2005). As such, these studies highlight the importance of devising institutional mechanisms that enable disadvantaged groups to build their assets and reap the benefits of savings, as do the middle and high-income groups. Prior studies documented that asset-based policies with varied incentives and high matching rates can encourage savings among the lower-income group (Han, 2013; Sherraden, 1991). Specifically, according to institutional saving theory, economically marginalized groups can harness the benefits of savings via asset-based policies that incorporate institutional characteristics such as access, incentives, facilitation, expectations, and information (Han et al., 2009). Although promoting savings among homeless individuals has several challenges, such as housing instability, a low propensity to engage in income-generating activities, negative credit histories, and a lack of necessary identification documents, prior research found that some homeless individuals successfully saved money by participating in self-sufficiency programs that increased access and utilization of basic transaction and saving accounts (Kim, 2020).

Promoting the engagement of savings is particularly important among homeless individuals because saving behaviors can make people more future-oriented, and this can positively affect their emotional and mental health (Han, 2019). For example, Sherraden’s (1991) asset-effect theory posits that savings investment for asset accumulation empowers individuals to enhance their capabilities and improve their circumstances over the long term. In other studies, drawing upon the theory, asset-building programs exerted a positive influence on mental health and quality of life among low-income participants due to the promotion of future-oriented attitudes and behaviors, such as economic confidence (Han, 2019; Han & Rothwell, 2014; McKernan & Sherraden, 2008; Park & Han, 2014; Rothwell & Han, 2010; Sherraden et al., 2019; Ssewamala et al., 2009; 2010). In other studies applying the asset-effect theory to the homeless population, researchers have found that homeless individuals were more likely to engage in savings programs and build assets when provided with high incentives (Biggers, 2013; Linardi & Tanaka, 2013; Marco et al., 2015).

Contribution of the Study

Although a substantial body of research has investigated the link between mental health and savings, empirical studies explicitly exploring the impact of savings on depression amongst homeless individuals are relatively sparse. In response to this gap in the literature, this study, using a sample of homeless individuals in Korea, aims to examine the potential association between savings and depressive symptoms within the homeless population. This empirical investigation enables us to scrutinize the role of savings for those experiencing homelessness, thereby providing critical insights for policy implications. The hypothesis for this study is the following:

Hypothesis: There would be an association between higher savings and lower depressive symptoms among people experiencing homelessness.

Methods

Data and Study Sample

This study utilized data from the 2016 National Survey on Homeless People, conducted by the Korean Ministry of Health and Welfare, which provides a nationally representative sample of the homeless population. Point-in-time (PIT) counting was employed to identify study participants, pinpointing regions where street homeless individuals, facility dwellers, and jjokbang residents were likely to be residing as of October 2016. PIT counting is recognized as a systematic method for identifying specific populations, such as the homeless, at a given time (Lee et al., 2017). Interviews were conducted in October, mitigating potential weather effects — the possibility that residential conditions might change according to weather patterns, especially before and after the transition seasons (Lee et al., 2017). The survey garnered the participation of 2,032 homeless individuals: 219 street homeless, 1,511 living in housing facilities, and 302 jjokbang residents. After excluding entries with missing data, a total of 1,860 individuals were included in this study. The study utilized de-identified data, with approval granted by Statistics Korea (Approval No. 117098).

Measures

Dependent Variable

Participants’ depression symptom severity was measured by the Center for Epidemiological Studies-Depression (CES-D) scale (Kohout et al., 1993; Lee et al., 2017), which was coded with a four-point Likert-type scale (0 = barely (less than 2 days) and 3 = most of the time (10–14 days)). This study summed up 11 items (Kohout et al., 1993). The summated scores equal to or above 16 were considered as having depressive symptoms, while the scores less than 16 were regarded as not having such symptoms (0 = not depressed, 1 = depressed) (Kohout et al., 1993). The reliability score using Cronbach’s alpha was .86.

Independent Variable

This study employed the monthly savings of homeless people as a major independent variable. The savings unit is 1,000 Korean Won (KRW, approximately 0.80 US$), and the log transformation was applied to meet the normality assumption.

Control Variables

Socioeconomic factors affecting depressive symptoms among the homeless were recorded as control variables (Han et al., 2011; Kim, 2008; Nam, 2009). Included variables were housing status (0 = currently street homeless or jjokbang residents and 1 = living in housing facilities), education levels (0 = middle school or lower and 1 = high school or higher), logged debt status (total current debt, unit: KRW 10,000), logged monthly income (total average monthly income for the past year, unit: KRW 10,000), employment status (0 = unemployed and 1 = employed), gender (0 = female and 1 = male), age, self-rated health status (0 = poor, 1 = fair, and 2 = good), and degree of disability (0 = no disability, 1 = mild disability, and 2 = severe disability) (Choi & Lee, 2019; Shin, 2009).

Analysis

Specific analysis plans are as follows. First, descriptive statistics were conducted to observe the characteristics of the homeless population. Second, propensity score matching was used to balance the information on monthly saving status (either non-savers with zero savings or savers with savings greater than zero) and the covariates. Goodness-of-fit, χ2 test, and t-test were utilized to verify the matching status. Third, after the matching process, a bivariate correlation between study variables was conducted. Finally, a logistic regression analysis was employed to probe the influence of savings on depressive symptoms in homeless individuals.

Without using propensity score matching, it would be challenging to ensure equivalence between groups if the savings level for homeless individuals was simply used as an independent variable. This is due to the likelihood that the savings status is influenced by personal characteristics, potentially leading to selection bias, where savers and non-savers possess different attributes. If an ordinary least squares (OLS) regression analysis is performed with these inter-group differences, regardless of the controlled characteristics, it could lead to overestimation or underestimation of the results (Yoon et al., 2010). The propensity scores matching method, developed by Rosenbaum and Rubin (1983), is a tool that can alleviate selection bias and endogeneity (Rubin, 2001; Stuart & Rubin, 2008).

In implementing the propensity score matching analysis, this study employed a 1:1 nearest-neighbor matching without replacement and evaluated the matching quality via an overall balance test (Hansen & Bowers, 2008). The practice of using the same cases repeatedly for matching is referred to as matching with replacement, while the opposite is called matching without replacement. Generally, matching methods with and without replacement do not yield significantly different results (Bloom et al., 2002).

Results

Demographic Characteristics

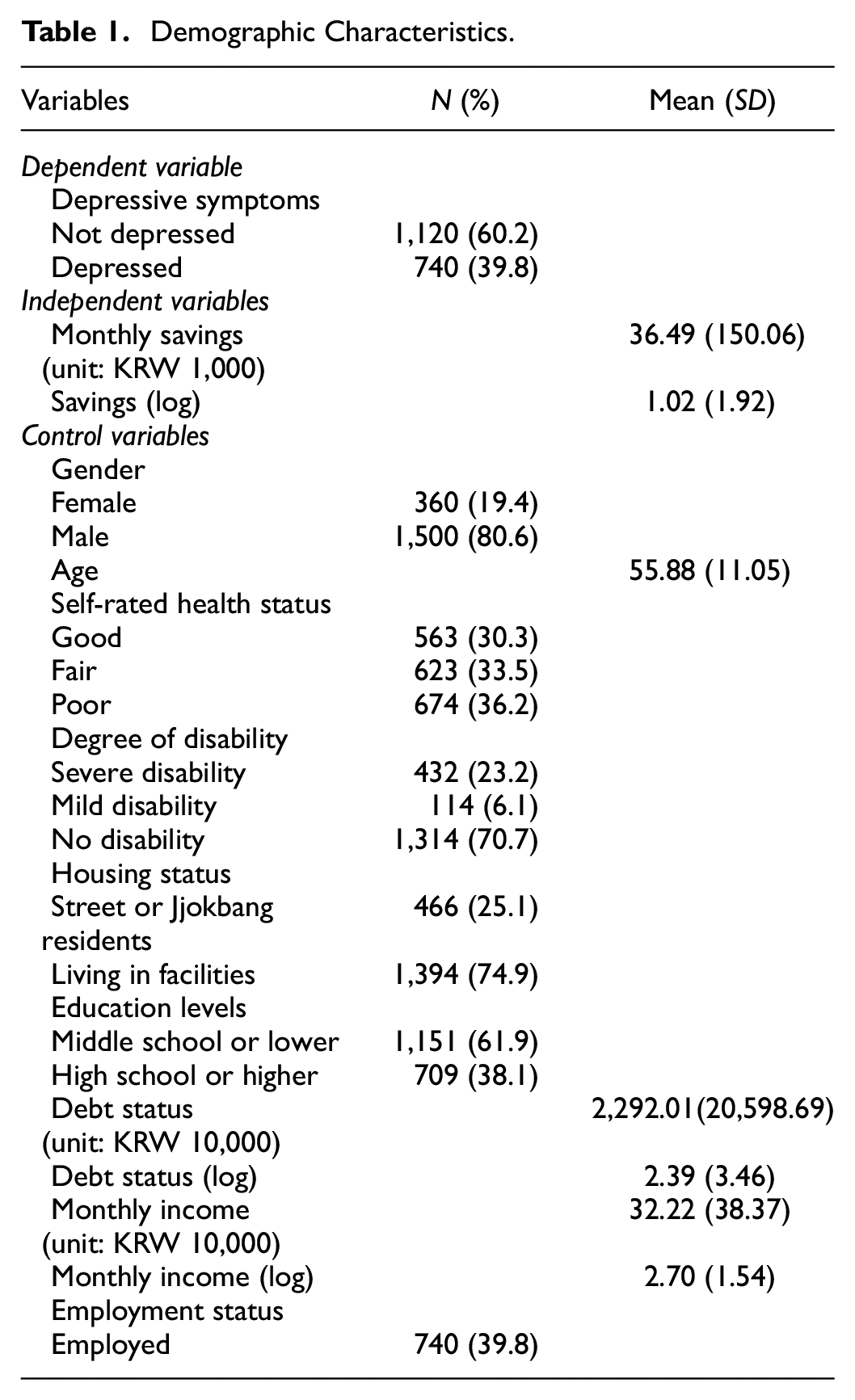

The descriptive statistics of study participants are presented in Table 1. This study found that 39.8% (n = 740) exhibited depressive symptoms. The average monthly savings were approximately KRW 36,490 (SD = 150.06), and most participants were males (80.6%, n = 1,500). Their mean age was about 55.88 years (SD = 11.05). About 30.3% (n = 563) rated their health as good, while approximately 36.2% (n = 674) rated their health as poor. Of the study sample, 23.2% (n = 432) had severe disabilities, and 6.1% (n = 114) had mild disabilities. About 61.9% (n = 1,151) were middle school graduates or lower, and 39.8% (n = 740) held a job. The average monthly income (the previous year) was KRW 322,200 (SD = 38.37), and the debt levels were KRW 22.92 million (SD = 20,598.69). Around 25.1% (n = 466) were on the street or lived in jjokbang, while 74.9% (n = 1,394) resided in homeless facilities.

Demographic Characteristics.

Propensity Score Matching

The monthly savings amount was used as a binary variable (non-savers and savers) for propensity score matching. The covariates for propensity score matching were the socioeconomic factors that influenced the savings of homeless people, including homeless shelter or housing facility status, education levels, debt status, monthly income, and employment status (Biggers, 2013; Park & Han, 2014). The covariates were also used as control variables in the logistic regression analysis.

This study confirmed the balance of matching using two steps. First, the matching quality was estimated using the relative multivariate imbalance measure L1, as Iacus et al. (2009) suggested. This index shows that a value closer to 0 indicates the acceptable distribution balance of two groups, and a value closer to 1 indicates the imbalance. In this study, the value was .585 before the matching, while the value decreased to .283 after the matching. Second, Hansen and Bowers (2008) suggest an overall balance test using the χ2 test to identify the overall imbalance between the treatment and control groups. If the null hypothesis were not rejected at a significance level of .05, the structure between the two groups would be similar. This indicates that the matching was conducted well. This study found the matching to be well-balanced (χ2 = 7.809, p = .167).

As Figures 1 and 2 depicted, the study found similar distribution patterns between non-savers and savers after the matching.

Distribution of propensity scores before and after matching.

Distribution of propensity scores.

Two statistical analyses (χ2 test and t-test) were performed to examine whether major study variables’ characteristics differed before and after the matching.

As shown in Table 2, significant differences were found before matching. To see housing status, non-savers were relatively more residing in street or jjobang than savers dominantly living in facilities (χ2 = 118.405, p < .001). In education levels, non-savers held lower education level than savers (χ2 = 9.807, p < .001). Non-savers had more debts (t = −2.524, p < .05) and earned less monthly income (t = 6.806, p < .001) than savers. Non-savers had higher unemployment rate (χ2 = 177.319, p < .001) and exhibited higher depressive symptoms (χ2 = 42.390, p < .001) than savers. After matching, these significant differences were not found. These findings suggest that the matching was conducted well.

Comparison of the Characteristics Before and After Matching.

p < .05, **p < .01, ***p < .001.

Correlation Between Major Variables After the Matching

The results of the bivariate correlation analysis are presented in Table 3. To see significant correlations between independent and dependent variables, this study found a significant negative correlation between savings and depressive symptoms (r = −.104, p < .01). This study also found that health status (r = −.180, p < .001) and residence type (r = −.235, p < .001) were negatively correlated with depressive symptoms. Correlation coefficients higher than 0.8 were not found, indicating that there may not be a multicollinearity issue in the dataset.

Correlation Between Study Variables After Matching (n = 882).

Note. 1 = Gender; 2 = Age; 3-1 = Self-rated health status—good (ref poor); 3-2 = Self-rated health status—fair (ref poor); 4-1 = Degree of disability—severe disability (ref no disability); 4-2 = Degree of disability—mild disability (ref no disability); 5 = Homeless shelter or housing facility status; 6 = Education levels; 7 = Debt status (log); 8 = Income level (log); 9 = Employment status; 10 = Savings (log); 11 = Depressive symptoms.

p < .05, **p < .01, ***p < .001.

Effect of Savings Level on Depressive Symptoms of Homeless People

Following the propensity score matching, a logistic regression analysis was utilized in this study to assess the relationship between the level of savings and depressive symptoms among the homeless population. Table 4 presents the key findings of the analysis. The logistic regression model after matching was found to be statistically significant (χ2 = 88.967, p < .001). Most importantly, this study found that homeless people with more savings showed lower levels of depressive symptoms (OR = .908, p < .01). This indicates that homeless individuals engaged in savings were less susceptible to severe depressive symptoms in comparison to those without savings. This study also found that homeless individuals with good physical health were less likely to experience depressive symptoms (OR = .378, p < .001). Additionally, homeless individuals residing in shelters or facilities were found to be less prone to depressive symptoms than their counterparts living on the streets or in jjokbang (OR = .113, p < .001). The finding highlights the protective role of residing in shelters or facilities in depressive symptoms compared to living on the streets or in jjokbang.

Result of Logistic Regression Analysis.

p < .05, **p < .01, ***p < .001.

Discussion

This study examined the effect of savings on depressive symptoms of homeless people using nationally representative data in Korea. To mitigate selection bias that could potentially influence the research outcomes, propensity score matching was applied in the study design. Logistic regression analysis was performed after the matching. Our major findings can be summarized as follows. First, 23.7% of homeless people saved money; the average monthly savings was about KRW 36,490. Although the amount of savings was small, it is worth noting that some portion of homeless people did actually save. Most importantly, this study discovered a negative association between savings and depressive symptoms. While there are few studies examining the relationship between savings and depression among homeless people, the findings of this study are similar to previous research where assets and savings were significant factors in reducing depression among youth (Kang & Han, 2018) and older adults (Kang & Han, 2017). Drawing on our findings and prior research, it is possible that having savings could serve as a protective factor against depressive symptoms within the homeless population.

The findings of this study have several implications. First of all, the findings of this study report that homeless people, who are one of the most disadvantaged populations, can save and that savings matter for their depression. The significant link between savings and depressive symptoms strongly suggests that saving programs should be institutionalized to include homeless people. However, shelters and facilities for homeless people are reluctant to actively manage the saving of homeless people because of administrative issues and a shortage of workers at shelters and facilities. In this regard, the government needs to take action to implement saving programs targeting homeless people. In Korea, there are many matched savings programs (e.g., Hope Building Accounts for low-income workers, Tomorrow Saving Accounts for low-income youth, Dream Building Accounts for children, etc.) for low-income households (Han, 2013; 2019). A specialized matched savings program for homeless people is expected to help them move out of their lives (Park & Han, 2014).

Second, the current self-sufficiency programs for homeless people in Korea have allowed them to temporarily stay at facilities or make a living through the programs. However, the provision of homeless shelters and support for short-term rehabilitation are insufficient to help homeless people prepare for their financial independence and future (Lee et al., 2017). A previous study suggested that one of the main reasons for savings by homeless people was to prepare for housing (Park & Han, 2014). While many homeless people can get public housing from the government, many of them go back to the streets or facilities because of high living costs and utility costs. These findings suggest that savings of matched saving programs for homeless people to prepare for the future may increase the probability of independence as well as self-sufficiency.

Third, it is very important to design savings programs tailored to the conditions and needs of homeless people (Biggers, 2013). Many homeless people suffer from alcohol addiction, gambling, or mental health problems. In addition, many of them are credit defaulters who cannot open bank accounts with their ID cards. These situations may emphasize that saving programs should consider their conditions, needs, incentives, and restrictions together. Workers at shelters and facilities should be trained well to manage the saving program tailored to individual conditions and needs of homeless people. In this regard, saving programs can be implemented with additional programs such as emotional support, leisure activity, mental health treatment, or counseling programs. These collaborative efforts may increase the success of continuous saving, self-sufficiency, and positive mental health.

Fourth, programs helping homeless people that cope with diverse challenges may require coordination with mental health centers and self-sufficiency work programs with active case management (Marco et al., 2015). To manage the saving programs at the facility or center levels, it is necessary to educate social workers at the centers for the homeless about financial literacy, asset-building programs, and coping strategies against mental health problems. Their capacity and practice skills will be critical in implementing savings programs for the homeless and making them successful.

Fifth, this study found that the physical health status and residential status of people experiencing homelessness are significantly associated with depression. Since the strong association between physical health status and depression is supported by previous research (Choi & Lee, 2019; Han et al., 2018; Kim, 2008; Nam, 2009; Shin, 2009), the finding suggests that health promotion services are necessary to enhance the mental health of homeless people. The finding that homeless people living in shelters/facilities experience lower levels of depression can be explained by the services and programs they receive at shelters/facilities. Those institutions provide regular meals, health check-up services, employment assistance services, and case management services. Practitioners at the institutions need to think about how to enhance the quality of those services accordingly to help the homeless overcome depression.

Finally, the findings of this study are expected to build knowledge of asset-building literature in that savings have significant impacts on depression among homeless people. Asset building is related to capacity building (Han, 2019). Homeless people can be institutionalized to save in a specialized matched saving program. These ideas may contribute to knowledge building of Sherraden’s (1991) asset theory and evidence. In addition, the study findings may exert further discussion of the implementation of saving programs for homeless people in the future.

Despite these salient findings, our results should be interpreted with caution since there are several limitations. First, the study was not able to contain important factors influencing homelessness, such as the period of homelessness, alcohol use, and the status of welfare recipients, as control variables due to a lack of such information in the data. In this regard, we suggest that future research should include those factors in the analysis. Furthermore, the finding of the significant relationship between savings and depressive symptoms amongst the homeless population needs a cautious interpretation due to the use of cross-sectional data. Therefore, an examination of the causal link between savings and depressive symptoms through the utilization of longitudinal data would be a worthwhile objective for future research. Finally, our sample consisted solely of Korean adults, which might potentially limit the applicability of our results to other Asian or Western demographic groups. However, our findings align with previous studies conducted outside of Korea (Marco et al., 2015; McKernan & Sherraden, 2008), which suggests that the findings could still provide valuable insights for future investigations exploring the role of savings in the association between depressive symptoms and homelessness.

Conclusion

This research poses a significant contribution, emphasizing the potential benefits of savings programs tailored for homeless individuals. The programs could aid the homeless in attaining not only financial autonomy but also adequate mental health. Thus, we propose that the positive impacts of assets on mental health and psychosocial functioning can be extended to include the homeless population. Sherraden (1991) illustrated how institutional saving supports could enable low-income and vulnerable populations to save, thereby enabling them to experience the positive influences of savings. In this regard, savings programs designed for people experiencing homelessness should be explored as viable alternative initiatives that help reduce their depressive symptoms (Park & Han, 2014).

Footnotes

Authors’ Contributions

JC, SK, and C-KH contributed to the study concept and design. JC and SK performed data acquisition, analysis, interpretation of data, and drafting the article. JC, SK, and C-KH revised the article critically for important intellectual content and final approval of the version to be published. All authors read and approved the final manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethical Approval

The data was ethically collected and approved by the Korean Ministry of Health and Welfare.

Consent for Publication

Participants signed informed consent before participating in the study.