Abstract

This study examines the association between the pricing efficiency of individual shares during the post-period and the pre-period of renames, substantive renames, and those with non-substantive renames. Based on a sample of 567 firms in the Chinese A-share market, this study finds that the pricing efficiency of individual shares is significantly higher during the post-period than during the pre-period of a renaming announcement. Moreover, the results are robust to controls. In addition, the results are consistent with the argument that the firms experiencing substantive renames are more inclined to involve the firm-specific information content.

JEL classification: M41, G32, G12, G34, M21

Plain Language Summary

This research looked at how the renaming of companies affects how accurately their stock prices reflect true value in the Chinese A-share market. We studied 567 companies and found that after they announce a name change, their stock prices tend to show a more accurate value compared to before the announcement. This was especially true for companies that made significant changes to their names. This suggests that these name changes might be linked to better information about the companies being available to investors.

Keywords

Introduction

Non-financial announcements become increasingly important in detecting useful information. The share name reflects the firm image and strategy. The renaming announcement of a firm reveals the direction of future development or conceals a negative image of the past. The information conveyed by the announcement is observed by investors and ultimately impounded into the share price, reflecting the pricing efficiency of the market. Previous literature examines the impact of name changes on share prices and price efficiency, mostly in developed countries but seldom in developing countries. This study examines the name changes in pricing efficiency in developing economies, especially China’s largest one.

A listed firm commonly selects the share name from its full name registered at the State Administration for Industry and Commerce in China and then can be renamed as long as the full name is changed. In China, share name changes can be classified as active and passive renaming. The first category refers to the approved name changes out of firm development, while the latter is commonly the signal of special treatment (“ST” or “*ST”) that is below discussed in this study. While certainly, in most cases, name changes are associated with substantial organizational events such as mergers and acquisitions as well as changes in the business focus, many times, the renaming occurs in the absence of substantial events but in an attempt to get rid of former deteriorating reputation or to spellbound investors with a name related to popular topics (Agnihotri & Bhattacharya, 2017; Akyildirim et al., 2020; Biktimirov & Durrani, 2017; Josev et al., 2004; Mathuva et al., 2016)

A notable example is SHANGHAI DUOLUN INDUSTRY CO., LTD.′s renaming homonymous to P2P on 14 May 2015. The announcement triggered a soaring share price in the following two consecutive trading days. To investors’ surprise, the firm ultimately confirmed that it had no intention to shift its business focus to Internet finance and provided neither relevant personnel information nor any feasible report when facing inquiries from the Shanghai Share Exchange. This preposterous renaming vividly implies that firm name changes may influence the share price, providing supportive evidence that capricious renaming announcements (without proper regulation) may induce investors to misevaluate a firm’s value due to information asymmetry (Long & Lin, 2020).

Previous studies explain the impact of renaming typically from the perspective of market reactions (Karim, 2011; Kot, 2011), firm value, and financial performance (Akyildirim et al., 2020; Berkman et al., 2011; Mathuva et al., 2016), and subsequent growth and prospects (Cole et al., 2015; Cooper et al., 2001). A renaming announcement has a certain but short-term influence on market reaction. Karim (2011) provides empirical evidence of a positive relation between the market reaction and a rename by the firms listed on the “Euronext Paris,” indicating the economic potential of a renaming announcement. However, some studies find little market reaction from investors due to a rename or only a short-term effect (Kot, 2011). Bicha (2009) finds only a long-term impact of a rename on the share price.

Firm value and financial performance can be improved by changing the share name. Berkman et al. (2011) adopt a standard event methodology and reveal that the value increases experienced by the Chinese listed firms with a rename result from substantial and successful operational changes. Mathuva et al. (2016) use the same methodology and find evidence supporting a consistent and positive relation between a rename and the subsequent financial performance. The name change immediately impacts the firm and has a long-term effect on future development. Cooper et al. (2001) point out that a renaming can influence the subsequent growth of the firm in the window period. Following Epermanis and Harrington (2006), the result of Cole et al. (2015) supports a significant and positive impact of the insurer renaming on the subsequent growth in premiums.

Most studies measure the impact of a rename on the share price movement, especially cumulative abnormal return, due to information of renaming being impounded into the share price. Lev (1983) and Roll (1988) propose that economic variables, industry information, and firm-specific events influence share prices. Roll (1988) points out that most of the impact of firm-specific information lies in the residual of the capital and asset pricing model’s market model, innovatively adopting R2 of the model to infer firm-specific information. Accordingly, this study utilizes

A sample of 567 listed firms with an active rename in the Chinese A-share market for which data are available from 1 September 2010 to 31 August 2020 is selected using the Wind Financial database. The sample firms are categorized into the substantive and non-substantive groups of a renaming announcement. The empirical results of this study reveal that the pricing efficiency of individual shares is significantly higher in the post-period than that in the pre-period of a renaming announcement and higher for firms with the substantive renaming than those with the non-substantive one. The firms in the post-period of a renaming announcement and with the substantive renames significantly stimulate the pricing efficiency of individual shares. In addition, this study finds that the institutional shareholding shares of listed firms are vital in the process of share pricing and the information content of share pricing, thus resulting in the higher pricing efficiency of individual shares.

This study contributes to the previous literature in three ways. First, this study discusses the impact of a rename on the pricing efficiency of individual shares, which has received little attention in the existing literature. Early studies by Howe (1982) regard share name changes as neutral events with little influence on share prices. But given that research related to share name changes has been improved with more diversified empirical data and prudential statistic methods, the impact of renaming on share prices and other factors can be discovered and examined more comprehensively. However, there is limited evidence on the relationship between renaming and pricing efficiency. The finding of this study suggests that substantive renaming can impound more firm-specific information into share prices, thus improving pricing efficiency.

Second, this study discloses institutional investors’ role by investigating institutional investors’ behaviors toward the renaming announcement and the moderating effect on the relation between renaming and the pricing efficiency of individual shares. The results show that institutional investors increase shareholdings in firms with substantive renames but decrease shareholdings in those with non-substantive renames, indicating that institutional investors can distinguish substantive renaming announcements from misleading ones. Thus, the findings justify the critical role that institutional investors play in ensuring the effective operation of the share market.

Finally, the findings of this study have implications for the goal of the Securities Regulatory Authority to better protect the interests of irrational investors by strengthening the oversight of a rename, especially concerning extreme renames with no substantive purpose. Although investors can distinguish substantive from non-substantive renames in the long run, there remains an overreaction to a renaming event. Therefore, this study provides the Securities Regulatory Authority of China and the administrative departments in other countries with important references to improve the renaming processing and approval policies.

The rest of this paper is organized as follows. The following section reviews the relevant firm identity literature and signaling theory to develop testable hypotheses. Section 3 presents a concise overview of the data used in this research, while Section 4 discusses the methodologies employed and provides some preliminary descriptive results. Section 5 presents the main results of the analysis regarding a rename and the robustness tests, while Section 6 concludes.

Literature Review and Hypothesis Development

Reason and Effects of a Rename

A rename creates a new name, term, symbol, design, or combination for a new brand to develop a different image in the investors’ minds (Borges & Branca, 2010). The primary goal is to create a favorable and differentiated image for the firm or convey information about substantive changes in shareholding structure, business focus, and legal status (Delattre, 2002; Einwiller & Will, 2002; Wu, 2010). Firms beset by unsatisfactory reputations and inappropriate names tend to change the share name. Wu (2010) suggests that a firm adopts a radically different name to disassociate from a poor reputation, but the renaming has little impact on share prices after the announcement. Some studies also propose that cognitive fluency positively influences short-term share price movement. Fluently named shares robustly outperformed shares with disfluent names in the short term (Alter & Oppenheimer, 2006; Green & Jame, 2013).

In most cases, however, non-substantive rename occurs when a highly speculated and believed-to-be-promising industry rises. The firm changes its share names to cater to investor mania. In the wake of millennia comes the “Internet boom.”Cooper et al. (2001) observe a positive long-term share price reaction to announcing firm name changes to Internet-related dot com names. Lin et al. (2016) find Canada’s positive but transitory impact of oil-related renames. Akyildirim et al. (2020) document that firms who partake in “crypto-exuberant” naming practices offer substantial and persistent share market premiums but suffer from unsatisfactory profitability and leverage in the short term.

Price Efficiency and R-Squared

Most studies adopt the event methodology to evaluate the economic consequence. Still, they have not agreed on the impact’s empirical results and magnitude. The majority of the studies show a positive relationship between a rename and the share price (Agnihotri & Bhattacharya, 2017; Biktimirov & Durrani, 2017; Cole et al., 2015; Gupta & Aggarwal, 2014; Kilic & Dursun, 2006; Ma et al., 2018; Mathuva et al., 2016). In addition, strong renaming can be established for years, thus creating higher margins, customer loyalty, and increased income (Gupta & Aggarwal, 2014; Keller, 2002). However, Bosch and Hirschey (1989) regard these valuation effects of name changes as modest and transitory. Other studies find little market reaction or only a short-term impact due to a rename (Bicha, 2009; Kot, 2011).

Indeed, the event methodology enables researchers to explore the impact of renaming on market reaction and individual firms via visual and tangible financial indexes such as cumulative abnormal returns (CAR) and return on assets (ROA) in a more straightforward and understandable approach. It meets its limitations when measuring the magnitude of systematic mispricing and price informativeness, defined as how share prices reflect the firm-specific information (see Morck et al., 2000; Roll, 1988). Lev (1983) and Roll (1988) argue that share price factors consist of pervasive economic variables, industry information, and firm-specific events. Roll (1988) further finds a weak relation between the first two factors and individual share prices. Furthermore, the price volatility of most individual shares is unexplained by firm-specific news. According to the market model of capital and assets pricing model (CAPM),

where

Signaling theory can explain the association between renaming reasons and subsequent economic results. Prior studies reveal that a rename can serve as a signal to the market of improved operational efficiency, attained investment goals, and substantive structural changes or business focus changes, indicating positive or brighter prospects for a firm (Cole et al., 2015; Ferris, 2011; Gupta & Aggarwal, 2014; Josev et al., 2004). The renaming of a firm sends a strong signal to the stakeholders regarding the business focus and direction (Josev et al., 2004). Deng and Zeng (2005) find that there also exists market overreaction in China when the listed firm announces technology-related name changes. Furthermore, investors tend to perceive the prospect of those firms with substantive rename highly. Kot (2011) demonstrates that investors positively react around the announcement date to a rename associated with changes resulting from a merger or acquisition, a reconstruction, or a change in business type. Cole et al. (2015) assert that a renaming announcement possibly results in a negative relation between a rename in prior years and an increased future reputation. Mathuva et al. (2016) provide empirical evidence supporting a continual positive relation between subsequent financial performance and a rename based on the appropriate strategies.

The signal conveyed through a rename was previously considered difficult to be imitated due to the association between the potentially high costs and the signal conveyed through the rename (see Ippolito, 1990; Koku, 1997). Nevertheless, recent empirical studies seem to provide positive evidence that a rename has become a shortcut to signal improved firm management falsely and business focus changes to the market, which raises concerns for irrational investment decisions of the market and thoughts of needed policy (Zheng et al., 2018). Thus, this study proposes the following hypothesis:

Research Design

Sample Selection and Data Sources

The basic model employed in this study to evaluate the association between a renaming announcement and the pricing efficiency of individual shares is well-accepted in the literature. Morck et al. (2000) document that the firm-specific risk is higher for developed countries or countries with advanced legal systems or lower systematic risk in the share market. Using Chinese listed firms as a sample, Gul et al. (2010) empirically find that there is a significant association between the R-squared and the firm-specific information content. A higher R-squared indicates that less firm-specific information content is involved in the asset pricing of investors. Therefore, fewer individual differences among firms result in the lower pricing efficiency of individual shares (Yu, 2008).

This study uses data on either the SHSE (the Shanghai Share Exchange) or the SZSE (the Shenzhen Share Exchange) from 1 October 2009 to 30 September 2021. This empirical study is restricted to firms announcing a rename for 3 years before and after the renaming announcement. The announcement information is obtained from the Wind Financial database, cninfo.com (an official designated platform for financial information disclosure in China), and press coverages. This study begins the analysis by developing a concise list of active renaming announcements of renames by omitting firms under special treatment. Next, this study establishes which of those firms undertake substantive rename by scrutinizing financial reports that reveal main product changes or merges and acquisitions.

Firms in the finance and insurance industry are excluded from this study because of the special accounting treatment and business scope. Special treated (‘ST” and “*ST”) firms are also excluded from this study. Failure to carefully screen the data (dependent and independent variables) could impose considerable biases and lessen the validity of the research. Other concurrent events are checked, such as earnings announcements, mergers, acquisitions, and major reorganizations. This leaves 567 firms with a rename and 445 announcements with detailed reasons for renaming.

Table 1 exhibits the distribution of renaming announcements of firms on the A-share market from 2010 to 2020. The distribution divergence indicates that, during the past decade, the number of rename announcements peaked in 2016 and then slowly decreased in the following years.

Renaming Announcement of Firms in the A-Share Market.

Variable Measurements

Independent Variables: A Rename (

The basic model used in this study to test H1 is as follows:

A rename (

To examine whether the pricing efficiency of individual shares is higher for firms with a substantive rename than those with a non-substantive rename, the model is estimated with the inclusion of a dummy variable for the period after a renaming announcement. This is reflected in the following equation:

where for firm i at time t, the variable

As a sensitivity test, the impacts of a substantive rename for the institutional investors and mergers or acquisitions on the pricing efficiency of individual shares are used as the alternative measures of a renaming announcement. These renaming announcements are directly related to the firm-specific information content. These measures are commonly considered in the information interpretations of share returns literature and are expected to yield significant results. Using these alternative measures of a renaming announcement to examine changes in R-squared values, the findings of this study are consistent with the above hypotheses.

Dependent Variables and Control Variables

In this study, the factors affected by a rename are analyzed and reflected in the pricing efficiency change of individual shares. This study selects several variables, including the firm scale, the proportion of outstanding shares, ownership concentration, the proportion of institutional shareholding, leverage ratio, share turnover, operating performance, capital structure, and dividends. Roll (1988) indicates that a larger scale for a firm results in a larger correlation between the firm and the share market. A share price violation reflects more firm-specific information. There is a significantly positive association between the firm scale and R-squared, indicating that firms’ share prices tend to incorporate more market-wide information. This study calculates the R-square from the model (1), using the monthly return rate of individual shares (

where

Moreover, Piotroski and Roulstone (2004) argue that firms can act as the leading market indicators by revealing or signaling macroeconomic events. The firm scale is defined as the natural logarithm of market capitalization at the end of the year. A larger scale indicates a lower unsystematic risk for a firm’s shares. Firms on a larger scale are more likely to be affected by systematic factors. Institutional investors’ trading has increased firms’ specific information and thus improved market efficiency (see Hou & Ye, 2008).

By contrast, better operating performance, a higher proportion of institutional investors, and higher share turnover indicate higher unsystematic shares risks for a firm. For firms with better operational performance, a higher proportion of institutional investors, and higher share turnover, share prices involve more firm-specific information content. Institutional investors are better able to analyze and gain information content professionally. As a result, institutional investors’ information content for the shareholding changes can be delivered to the share market. Consequently, the share prices can involve more information content (Chakravarty, 2001).

Furthermore, the higher share concentration and share turnover lead to a higher unsystematic shares risk. The systematic risk impacts firms with higher share concentration and share turnover. The ownership concentration helps mitigate the conflict of interests between the controlling and minority shareholders (see Demsetz, 1983; Grossman & Hart, 1980; Shleifer & Vishny, 1986). The controlling shareholders are more inclined to disclose credible and high-quality information for the benefit of minority shareholders (see Boubaker et al., 2014). Large shareholders are less inclined to conceal information when holding greater ownership in a firm.

Rather, the large shareholders have incentives to disseminate more and better firm-specific information content. Piotroski and Roulstone (2004) argue that the high ownership concentration facilitates access to the firm-specific information content and encourages informed trading, thus reducing the R-squared and increasing the pricing efficiency of individual shares. Since the controlling shareholders are more likely to disseminate more firm-specific information content (see Gul et al., 2010), this study expects that owning a large fraction of a firm’s shares increases the amount of firm-specific information content available to the market, which reduces the reliance on market-wide information, decreases R-squared of share price movements, and increases pricing efficiency of individual shares.

With less firm-specific information content available for pricing shares, the share returns of a firm embody more industry- and market-related information. A firm’s shares with a high leverage ratio have more optional features. Consequently, the firm is more sensitive to default risk, and the level of unsystematic risk related to firm-specific information content appears to be improved.

In addition, this study uses the Big 4 auditing firms as a control variable. In the Chinese context, the Big 4 auditors are defined as the joint ventures of the international Big 4 firms and local auditors (Gul et al., 2010). The Big 4, which have more effective facilitators of the firm-specific information content than other auditors, reflect more firm-specific information content and are therefore priced more efficiently.

Finally, an industry dummy controls the potential industry-fixed effects.

Variable Definitions.

Summary Statistics

Table 3 presents the summary statistics for the regression variables. The mean of R2 (rsq) is .2381, indicating that the economic factors systematically influence more than 20% of price volatility for the individual shares. The institutional investor shareholding rate is approximately 41.01% on average, whereas the firms with a renaming announcement due to a merger or acquisition constitute approximately 90%. A total of 8% of the sample firms are audited by one of the Big 4 international accounting firms. Approximately 38% of controlling owners are firms among all sample firms, and individuals control the remaining shares. The leverage ratio (Lev_it) is greater than 40% on average. The sample firms vary widely in size, as reported in Table 3.

Descriptive Statistics for Regression Variables.

Note. Variable definitions are provided in Table 2.

Table 4 presents the changes in firms’ performance and growth rate following a rename. EPS1 refers to the net income ratio (after subtracting preferred dividends) to the weighted average number of common shares outstanding, whereas EPS2 refers to the net income ratio (after removing preferred dividends) to the weighted average number of dilutive common shares outstanding. BPS indicates the net assets per share, and ROE is the return on equity. All variables are measured to assess the performance of the firm.

Comparison of Performance and Growth Rates of Firms Before and After a Rename.

Note. Variable definitions are provided in Table 2.

, **, and * denote significance at the 1%, 5%, and 10% levels, respectively.

The performance of firms is significantly improved after a rename for the substantive renaming group. Firm growth indicators include revenue growth and operating profit growth rates. Conversely, the growth rates decline sharply after the non-substantive renaming group renames. However, for the substantive renaming group, the EPS, growth rate, revenue growth rate, and net profit growth rate increased after a rename, while the operating profit growth rate declined slightly.

Table 5 compares share concentration, institutional investor shareholdings, and R-squared during the pre-period and post-period of a renaming announcement. The substantive renaming group’s share concentration and institutional investor shareholding rate increased the most among the groups, followed by the group of all sample firms. The share concentration and institutional investor shareholding rate of the non-substantive renaming group decrease slightly. The R-squared of the substantive renaming group decreases the most, followed by the group of all samples.

Comparison of Share Concentration, Institutional Investor Shareholdings, and R-squared Before and After a Rename.

Note. Variable definitions are provided in Table 2.

, **, and * denote significance at the 1%, 5%, and 10% levels, respectively.

Results

Impact of Renames on Pricing Efficiency of Individual Shares (H1)

The results for the tests of H1 in the first instance are reported in the first model of Table 6. The table highlights the pricing efficiency of individual shares for the post-period of a renaming announcement and the pre-period of a renaming announcement for all sample firms. The R2 is significant at the 10% level. The results from the estimation model provide support for H1 and reveal that a rename by a firm listed in the Chinese A-share market is associated with the high pricing efficiency of individual shares (p = .0000) in the subsequent year. Accordingly, there is evidence of a significantly negative association between the post-period of a renaming announcement and the pre-period of a renaming announcement.

Impact of Renames on Pricing Efficiency of Individual Shares.

Note. Variable definitions are provided in Table 2, and the p-value is in parentheses.

, **, and * denote significance at the 1%, 5%, and 10% levels.

According to the results, the listed firms in the A-share market that announce renames experience an

In addition to the test variable, model (1) results present similar findings for most control variables. According to the results, T10share seems to have a significant and negative association with the pre-rename announcements at the 1% level. The results suggest that the listed firms with higher shareholding concentrations are associated with the higher pricing efficiency of individual shares, with a significant coefficient of −0.00844 (p = .0000).

In contrast, there is a less significant association between the pricing efficiency of individual shares for the post- and pre-periods of a renaming announcement for the sample firms with non-substantive renames than substantive ones, with a coefficient of −0.268, as shown in the second model.

A question arising from the above results is whether the higher pricing efficiency of individual shares for the post-period of a renaming announcement is simply a consequence of a rename. This issue is addressed by including only substantive renaming firms in the sample, with the results reported in the third model of Table 6. According to the results, the post-period and pre-period of a renaming announcement seem to have a significant and negative association at the 1% level for these firms. The result provides more insight into the previous observation that the listed firms in the Chinese A-share market seem to be using arbitrary renames to enhance share prices. The renaming presents a new brand to the investors, especially given that the share prices of internet finance firms with the renaming announcements usually fluctuate widely. Accordingly, the results in Table 6 for all sample firms and the sample firms with the substantive renames are consistent with the firms that change names having a higher pricing efficiency of individual shares and a lower

In summary, across Table 6, there is evidence that the pricing efficiency of individual shares is higher for the post-period than for the pre-period of a renaming announcement, which is consistent with prior studies investigating renames (see Agnihotri & Bhattacharya, 2017; Biktimirov & Durrani, 2017; Liao, 2010; Mathuva et al., 2016). However, a point of distinction is that these earlier studies generally consider renames and utilize the revenue-cost structure to revalue investment risk. For these renames, there is separate evidence of relevance. In contrast, there is little consideration of the pricing efficiency of individual shares for the post-period and pre-period of a renaming announcement. The results reveal a consistent and negative association between a pre-period rename and a post-rename announcement.

Impact of Substantive and Non-substantive Rename on Pricing Efficiency of Individual Shares (H2)

An important issue is whether the above results, consistent with the firm-specific information content in the substantive renaming announcements rather than the non-substantive announcements, involve highly unsystematic factors that lead to higher pricing efficiency of individual shares. Evidence of the impact of the substantive and non-substantive renaming announcements on the pricing efficiency of individual shares is presented in Table 7.

Impact of Substantive and Non-substantive Renames on Pricing Efficiency of Individual Shares.

Note. This table reports the impact of substantive and non-substantive renames on the pricing efficiency of an individual share. The estimation of columns (1), (2), and (3) are the result of the primary model, model with control variables, and model with industry fixed effect, respectively. Variable definitions are provided in Table 2, and the p-value is in parentheses.

, **, and * denote significance at the 1%, 5%, and 10% levels.

The results in the third model of Table 7 reveal that the R2 is significant at the 10% level. It is worth noting that the Pricefficy of Subst_it is negative and significant in the period immediately after the renaming announcement (p = .0225). This result suggests that the substantive renaming announcements positively relate to information efficiency. The results support the second hypothesis in this study and indicate that the pricing efficiency of individual shares in the year following a renaming announcement is higher for firms with substantive renames than those with non-substantive renames. As a result, the listed firms with substantive renames in the Chinese A-share market are associated with high pricing efficiency for individual shares in the subsequent year.

Based on a sample of 567 listed firms with renaming announcements in the Chinese A-share market, the fundamental factors of individual shares with substantive renaming announcements significantly influence the process of share pricing and the information content of share pricing, which involves highly unsystematic factors. This leads to the higher pricing efficiency of individual shares. Consistent with previous studies, such as King (1966) and Durnew et al., the results reveal that the rate of individual share return is significantly associated with the rate of market return and the industry return. Share prices contain much relevant information for the market and the industry. A lower

The findings in Tables 6 and 7 on the impact of a rename on the pricing efficiency of individual shares add to the existing literature on the market reactions to a rename (see Agnihotri & Bhattacharya, 2017; Andrikopoulos et al., 2007; Biktimirov & Durrani, 2017; Josev et al., 2004; Mase, 2009; Mathuva et al., 2016). The findings provide additional insights into the negative association between a rename and the pricing efficiency of individual shares in the Chinese A-share market around the period of a renaming announcement. This study extends the analysis by Liao (2010) by focusing on the impact of a rename on the firm-specific information content involved in a developing country characterized by a vibrancy of the listed firms.

Although previous studies have documented the market’s reaction to a rename, those studies fail to discuss the impact on the share-pricing efficiency from the aspect of the firm-specific information content. This study fills this gap by examining the impact of a rename on the pricing efficiency of individual shares for the substantive and the non-substantive renaming announcements, which have been highlighted as factors explaining the firm-specific information content. More specifically, the results reveal a consistent and negative association between the pre-period and the post-period renaming announcements and the substantive and the non-substantive renames.

Robust Test

This study also conducts serval robustness tests, which are tested from the alternative method (i.e., PSM-DID) and alternative indicators to measure

Alternative Method (PSM-DID)

In addition to the industry fixed effects regression model specification, this study also conducts propensity score matching difference-in-difference (PSM-DID) tests among renamed and all A-share firms.

The propensity score matching (PSM) method was developed by Rosenbaum and Rubin (1983) to solve the problem of endogeneity of self-selection bias and correct for the bias due to confounding factors that may be found in the estimate of the renaming effect obtained by simply comparing the results between the firms that change names versus those that do not. Since this study has a panel of firms observed over time, the matching of firms in the second test is implemented year-by-year in light of the similar treatment by Heyman et al. (2007). This study can then conduct the DID method on the selected samples with PSM, which compares the difference in price efficiency between the treatment and control firms before and after the renaming event.

The first test classifies the samples into two groups by applying the PSM method: (1) the treated group, which includes firms with a substantive renaming announcement, and (2) the control group, which includes firms without such substantive renames. In the second test, (1) the treated group, which includes firms with a renaming announcement, and (2) the control group, which includes firms without renames. This study obtains propensity scores (PS), which measure the extent of matching the treated and control groups in multiple dimensions.

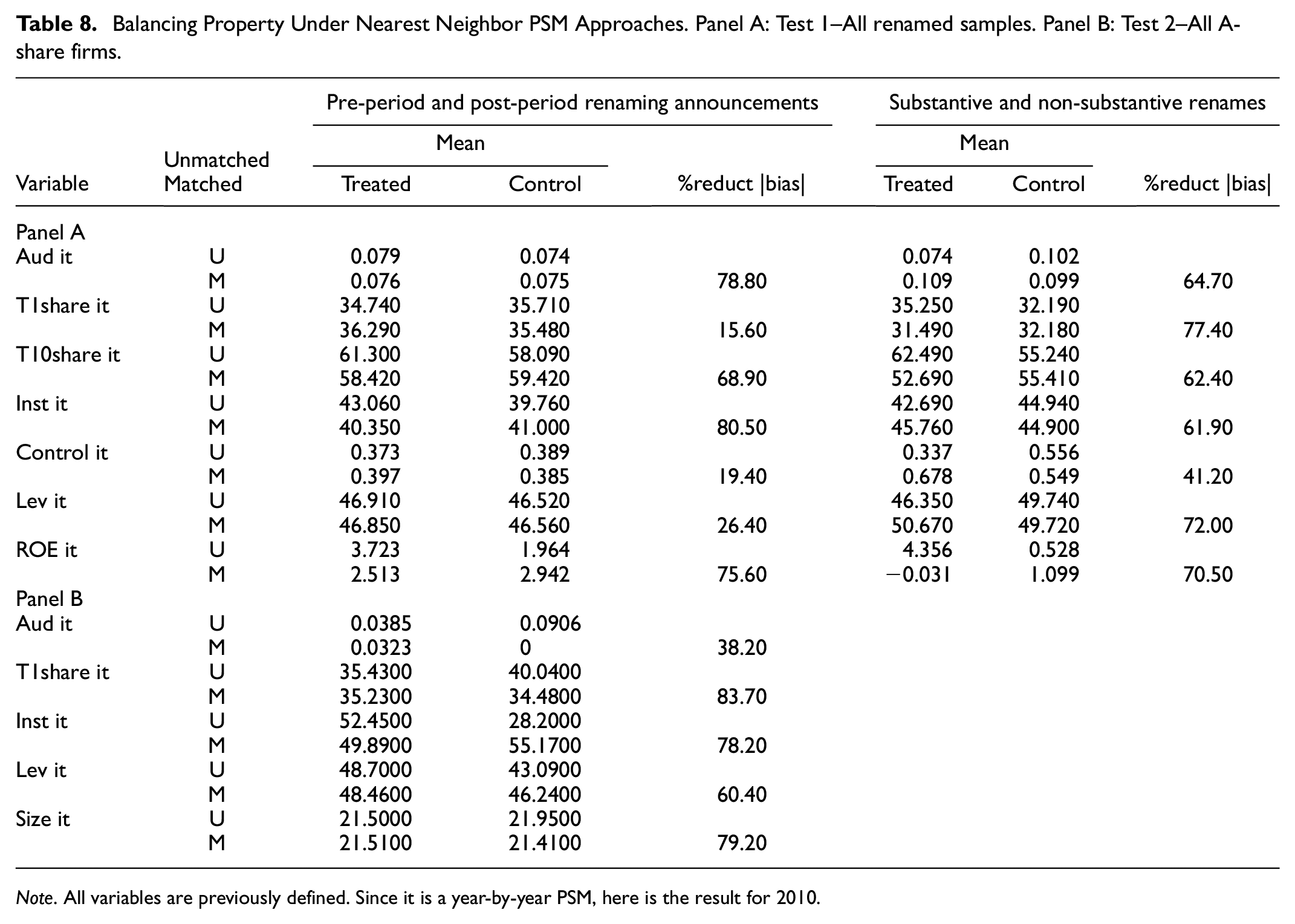

The results in panel A of Table 8 show the matching effect of pre-period and post-period renaming announcements, and substantive and non-substantive renames for test 1, by the nearest neighbor matching approach without a replacement method. The bias is significantly reduced. Furthermore, the untabulated results indicate an insignificant difference between the covariates within the two groups. This finding suggests that the equilibrium effect of each covariate becomes better under the matching approach. Finally, the results in panel B of Table 8 show the matching effect of renamed and non-renamed firms for test 2.

Balancing Property Under Nearest Neighbor PSM Approaches. Panel A: Test 1–All renamed samples. Panel B: Test 2–All A-share firms.

Note. All variables are previously defined. Since it is a year-by-year PSM, here is the result for 2010.

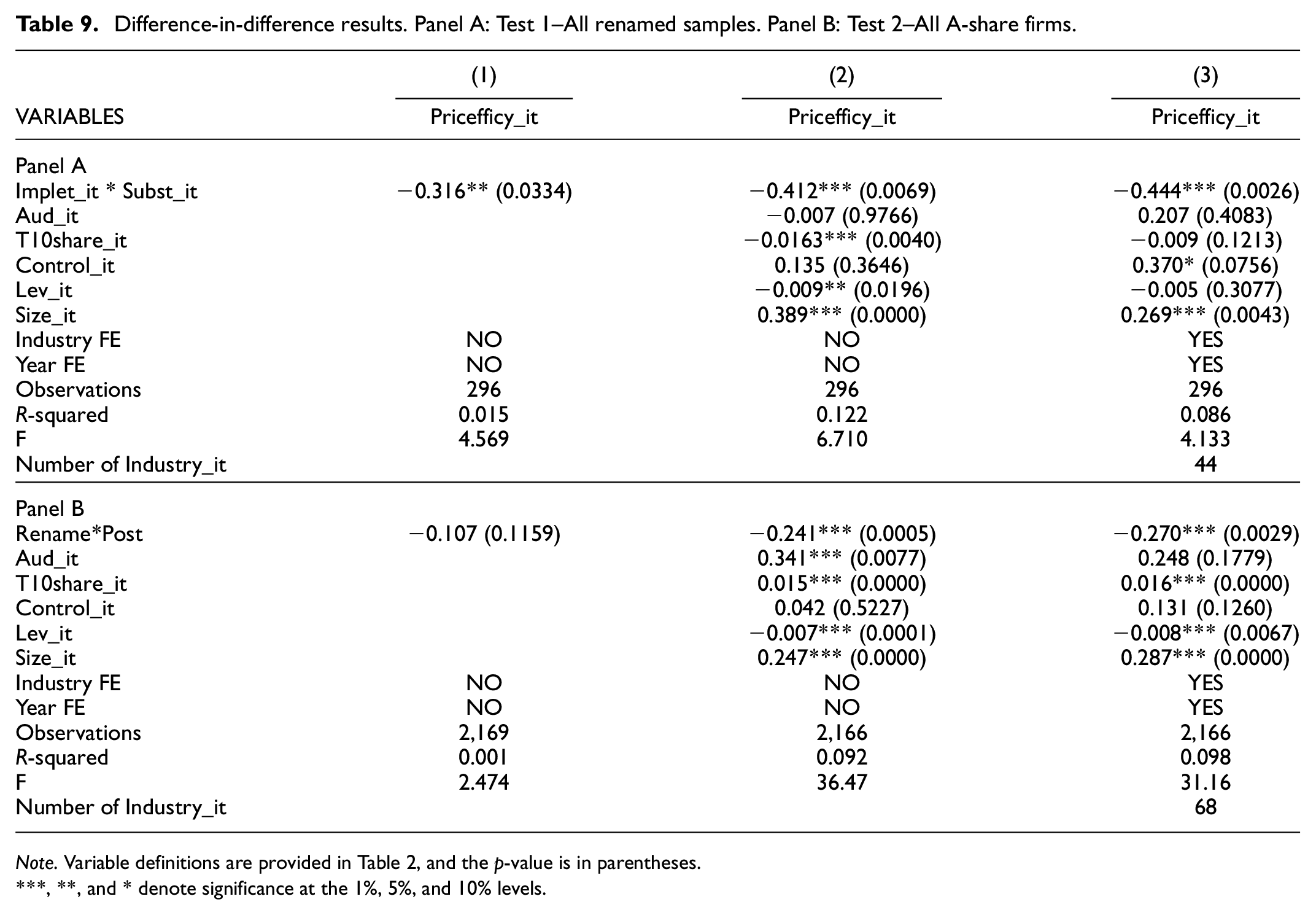

Panel A of Table 9 displays the result of the difference-in-difference for renamed samples. The coefficients of Implet_it * Subst_it are significantly negative under difference models, suggesting that substantive rename firms can significantly improve pricing efficiency after renaming. The results in panel B of Table 9 display the coefficients of Rename * Post are −0.107, −0.241, and −0.270 in a simplified model, a model with control variables, and an industry-fixed effect model. The last two coefficients are significant at a 1% level, indicating that firms that experienced a rename have higher pricing efficiency than unnamed firms. The results are robust.

Difference-in-difference results. Panel A: Test 1–All renamed samples. Panel B: Test 2–All A-share firms.

Note. Variable definitions are provided in Table 2, and the p-value is in parentheses.

, **, and * denote significance at the 1%, 5%, and 10% levels.

Alternative Measurement

Given that the approach of R-squared is controversial, this study uses more conventional methods to measure share pricing efficiency. Existing literature mainly measures asset pricing efficiency from two aspects. One is the information content of prices, that is, whether asset prices truly and fully reflect all market information, especially based on characteristic fluctuations at the company level. The other is information response speed, that is, whether asset prices can include new market information in a timely and accurate manner. Moreover, an important characteristic of efficient market prices is following a random walk. Under the random walk assumption, the higher the predictability of share price returns, the higher the possibility for investors to predict future share price trends based on past and present information. Thus, the lower the pricing efficiency.

Information Content of Prices: Cross-Autocorrelation

Through analyzing the linkage characteristics of individual shares in share markets in different countries, Morck et al. (2000) find that developed share markets contain more heterogeneous risks than emerging markets. The coefficient measures the pricing efficiency of individual shares and the market.

Bris et al. (2007) propose to measure the pricing efficiency of individual shares and the market by using the correlation coefficient between the return rate of individual shares in the current period and the market return rate lagging one period. The specific calculation formula is as follows:

where

Information Response Speed

Hou and Moskowitz (Hou & Moskowitz, 2005) propose to use the relative efficiency of the adjustment speed of asset prices to market information to measure pricing efficiency and construct a price lag index, which studies have widely used. If the market cannot timely and fully reflect the information into the share price, then this information will be involved in the subsequent time, thus forming a lag in price response. The delay of price response can be obtained through a regression model with a lagged market rate of return. The stronger the explanatory power of the lag variable, the longer the price will take to respond to information. Following Hou and Moskowitz (Hou & Moskowitz, 2005), this study runs a regression of each share’s monthly returns and 4 months of lagged returns on the market portfolio over the prior year:

where

Similar to the F-test, this measure captures the proportion of individual asset returns explained by lagged market returns. The smaller the value of D1, the lower the dependence of asset return on past market information, suggesting a shorter time required for assets to absorb market information (i.e., higher pricing efficiency).

In addition to the coefficient of determination of the regression equation, this study can also use the parameter of the independent variable in the regression equation to measure the dependence of the rate of return on individual assets on the lagged market rate of return and obtain the second indicator of price delay:

D2 captures the proportion of the regression coefficient of the lagging market rate of return in equation (6) among all the regression coefficients. The smaller its value, the higher the pricing efficiency. Since the sample period investigated in this study is only 6 years, if annual data are used to calculate the above indicators, the final sample will be too small. Based on the practice of Moïsé & Bris (2013), this study regresses each share’s monthly rate of return to the market rate of return on that month and the market rate of return lagging 1 to 4 months. After obtaining the price delay indicator of all shares on different trading months, calculate the average value of each share’s price delay indicators in different years.

Variance Ratio

In an efficient market, future share price trends cannot be predicted based on past share price performance and current information, and share prices accurately reflect all information related to share value (Rösch et al., 2017). Therefore, the financial market-related literature has developed many methods to measure market pricing efficiency, such as variance ratio.

Early market efficiency studies use variance ratios to test whether prices follow a random walk (e.g., (Barnea, 1974)). A random walk implies that the ratio of long-term to short-term return variances, measured per unit of time, equals 1. Like Boehmer and Kelley (2009), this study conducts a variance ratio test on the monthly return rate of each share, subtracts one from the result, and takes the absolute value |1 − VR|.

Runs Test

The run test is a non-parametric test method, which only considers the rise and fall of the price and tests the walk characteristic of the sample sequence by verifying the significance of the actual number of runs of the sample sequence deviating from the expected number of runs under random walk conditions. In this study, the rise and fall of individual share can be represented by the rise and fall of the sample sequence logarithmic rate of return:

where

Given a significance level α, when n is sufficiently large, the construction statistic

First-Order Autocorrelation

First-order autocorrelation is also a conventional method to measure pricing efficiency. As French and Roll (1986) argue, the absolute levels of these autocorrelations should be positively related to incomplete reactions or possibly overreactions by investors to new information. The smaller the autocorrelation is, the better the pricing efficiency of the stock. This study calculates every share’s annual first-order autocorrelation coefficient based on monthly return rates.

Results

Table 10 shows the robust results.

Robust Test for Alternative Measurements. Panel A. Robust Test results of Cross-autocorrelations and Response Speed. Panel B. Robust Test Results of Variance Ratio, Runs Test, and First-order Correlations.

Note. Variable definitions are provided in Table 2, and the p-value is in parentheses.

, **, and * denote significance at the 1%, 5%, and 10% levels.

Under the regressions using different price efficiency indicators, the coefficients of Imple_it in the group of sample firms with substantive renames are consistent with expectations in most tests. However, they are significantly negative, which are −0.224 (p = −.0304), −0.0358 (p = −.0364), −0.0185 (p = −.0951), −0.0181 (p = .0302) and −0.0262 (p = .0328) respectively. Although the results of the runs test are contrary to expectations, the results are not significant in the sample of substantial name changes. It shows that substantive renaming can reduce the synchronicity of share prices and significantly improve the efficiency of share pricing.

Additional Tests

In the hypotheses tested above, Imple_it and Subst_it are used to measure the pricing efficiency of individual shares. The results’ sensitivity to an alternative share-pricing efficiency measure and the interaction variable SubControl_it is considered. Concerning the impact of the largest shareholder, an independent variable (T1 share_it), which is the percent of the largest shareholding at the end of the year, is introduced in this study. The results are reported in column (1) of Table 10, and it is worth noting that the

The finding seems to be consistent with a study by Jin and Myers (2006), who argue that the lower transparency in a firm leads outside investors to realize less firm-specific information content, thus suggesting that R2 is lower. A lower R2 implies that more firm-specific information content involved in the asset pricing of investors enlarges the characteristic differences among firms. Accordingly, the firm’s post-rename announcement share-pricing efficiency is higher than personal shares.

To assess the robustness of the results, this study also controls for institutional investors and checks the impact of a rename on the pricing efficiency of individual shares. The results are reported in column (2) of Table 11. Concerning the impact of the institutional investors, the interaction variable SubInst_it is considered. The results in Table 11 reveal a significant and negative coefficient for SubInst_it. The finding suggests that a higher percentage of institutional shareholding leads to a higher unsystematic risk for the firm shares. The result implies that the firms with institutional shareholding shares strongly influence the process of share pricing and the information content of share pricing, thus resulting in a higher pricing efficiency of individual shares. The result is consistent with the institutional investors expecting more information sources and specialized analysis abilities. The information content for the share changes of the institutional investors is subsequently delivered through the share prices. Therefore, it leads to higher information content of share prices, as suggested by the prior literature (e.g., Chakravarty, 2001).

Additional Tests.

Note. Variable definitions are provided in Table 2, and the p-value is in parentheses.

, **, and * denote significance at the 1%, 5%, and 10% levels.

Column (3) of Table 11 reports the estimation results controlling for the effect of mergers and acquisitions. To control the impact of mergers and acquisitions, the interaction variable SubMer_it is introduced. Table 11 suggests a significant negative coefficient for the substantive renames for mergers and acquisitions at the 10% level (p = .0750). Thus, a firm with a substantive rename due to a merger or acquisition is associated with higher pricing efficiency of individual shares. The finding seems to suggest some contributions of a rename to the firm-specific information content for the listed firms with the substantive renames following the mergers and acquisitions. Similar results are reported for other tests. Accordingly, substantive renames are associated with higher pricing efficiency of individual shares involving more firm-specific information content after the business acquisitions.

Conclusion

The decision to rename an organization has associated costs and benefits, such as favorable market reactions and subsequent premium growth for the listed firms. This study aims to evaluate the pricing efficiency of individual shares for the pre-period and the post-period of a renaming announcement. Consideration is also given to whether the share-pricing efficiency is higher for a substantive rename than for a non-substantive rename.

Based on a sample of 567 firms in the Chinese A-share market, there is empirical evidence that the pricing efficiency of individual shares is higher for the post-period than for the pre-period of a renaming announcement. This initial finding illustrates that the renames involving the firm-specific information content are value-adding to improve the market’s reaction. The results are robust to various controls and indicate that the renames by the listed firms in the Chinese A-share market are associated with the higher pricing efficiency of individual shares that involve more firm-specific information content. The result applies regardless of whether the substantive and the non-substantive renames are controlled. The results are consistent with the firms experiencing a substantive rename being more inclined to involve the firm-specific information content. The results seem to suggest a significant and negative

Interestingly, the share-pricing efficiency after a renaming announcement is higher for the firm and personal shares. The results also demonstrate that the institutional shares of listed firms strongly influence both the process and information content of share pricing, thus resulting in higher pricing efficiency of individual shares. Finally, the results imply that a firm with a substantive rename is associated with higher pricing efficiency of individual shares involving more firm-specific information content after a rename.

This study focuses solely on the listed firms in the Chinese A-share market. The method may affect the generalizability of the findings. Therefore, more studies on the listed firms with a rename in the more developed economies would be useful. The results demonstrate that after a rename, the impact of the renames seems to have a strong influence on both the process and information content of share pricing, thus leading to higher pricing efficiency of individual shares. Further research could investigate the window during which the listed firms experience the positive impact of a rename through the point at which the effect becomes muted. Another area for future study would be examining a control group of the listed firms in the U.S. share market and assessing whether the results are comparable to those of the listed firms in the A-share market of China. The association between the renames and the pricing efficiency of individual shares is considered, but this is not extended to the accounting performance. Expanding the analysis to include this topic is anticipated and concerns the major economic cycles during the sample period.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Zhejiang Office of Philosophy and Social Science, Grant/Award Number: 23NDJC154YB. Study on the Course Module Design and Teaching Model Reform for Training Excellent Accounting Talents under the Convergence of ‘Dual Carbon’ Goals and ‘Digital Economy’–a Graduate Teaching Reform Project of the Zhejiang Province’s 14th Five-Year Plan. General Research Project of Zhejiang Provincial Department of Education (No. 2023-005) and the Zhejiang Graduate Education Society (No. 2023-005).

Data Availability Statement

The data supporting this study’s findings are available from the corresponding author upon reasonable request.