Abstract

Digital finance plays a crucial role in enhancing financial inclusion and decreasing income inequality within developing countries. Given the digital and financial attributes that characterize digital finance, digital financial literacy (DFL) is a critical factor that influences the extent to which this function can be exploited. There is relatively little empirical evidence linking DFL to rural income inequality. Based on the 2017 and 2019 China Household Finance Survey data and two-way fixed effect panel model, this study focuses on rural China and examines the effect of DFL on income inequality. Meanwhile, this study also explores the mechanism of this effect from the perspectives of financial asset allocation and entrepreneurship. The empirical results show that (1) increasing DFL within rural households contributes to decreasing income inequality; (2) DFL can decrease income inequality by enriching the variety of household financial assets and enlarging the proportion of risky financial assets in rural households; and (3) improving DFL can ameliorate rural income inequality by increasing the probability of entrepreneurship. The study’s findings put forward fresh empirical evidence for understanding the relationship and mechanism that exist between DFL and income inequality, and more significantly, provide new suggestions for designing and enhancing financial policies that aim to decrease income inequality in developing countries.

Keywords

Introduction

The incomes of Chinese farmers have continued to rise since the reform and opening-up policy was implemented. However, this income increase has been accompanied by substantial income gaps. The Gini coefficient of rural China is approximately 0.35 2019, approaching the internationally recognized warning line of 0.4 (Huo & Chen, 2021). The widening income gap in rural areas hinders economic development, reduces welfare-generated incomes, and even brings about social instability (Neaime & Gaysset, 2018).

Although many studies have confirmed that digital finance (DF) is conducive to improving financial inclusion (Ahmad et al., 2020; Batista & Vicente, 2020; Ozili, 2018), there is no consensus on whether DF can narrow the income gap. For example, Demir et al. (2020) suggest that DF is the most promising financial innovation for alleviating income inequality. Similarly, N. Yu and Wang (2021) show that DF is beneficial for reducing the urban-rural income gap. By contrast, some scholars find that the development of DF is not conducive to the alleviation of income inequality. Yue et al. (2022) posit that the DF can increase the likelihood that low-income households fall into debt traps. The study by Mohd Daud et al. (2021) examines the relation between DF and income inequality in 54 countries from a nuanced perspective, concluding that DF widens the income gap.

Reflecting our belief that digital financial literacy (DFL) should be taken into account when examining effect of DF on income inequality, many previous studies note that it is difficult for people who lack DFL to master it (Kass-Hanna et al., 2022). For example, Lo Prete (2022) finds that investment efficiency is low for people who could enter financial markets with a lower level of DFL. Setiawan et al. (2020) state that people are more rational in their saving behavior if they have a higher DFL. Leong et al. (2017) posit that people who lack DFL are not informed about the risks of DF. According to Gabor and Brooks (2017), financial literacy is key to decreasing the risk of DF.

Motivated by these studies, we analyze the role of DFL in alleviating income inequality and make three main contributions. First, this study develops a system for evaluating rural households’ digital financial literacy and measures their DFL by employing the principal component factor analysis method (PCFA), which expands prior research. Existing research either measures the financial literacy or measures digital literacy of rural households (Twumasi et al., 2022; L. Zhao et al., 2022), but there are few studies that assess both financial and digital literacy together. The second contribution of this study is that it explores the impact of DFL on rural income inequality. The majority of previous research has focused on the impact of digital literacy (Ma et al., 2018; Siaw et al., 2020) and financial literacy (Lusardi et al., 2017) on farmers’ income. This study combined these two aspects for analysis. Finally, this study presents a detailed analysis of the mechanism through which DFL affects rural income inequality. We clarify the importance of financial asset allocation and household entrepreneurial participation as channels of the influence of DFL on income inequality. Although there has been considerable research on the impact of DFL on financial asset allocation (van Rooij et al., 2011) and entrepreneurship (Oggero et al., 2020), this study conducted on the effect of these two channels on rural income inequality.

In the remainder of this article, we will follow the following structure. Section “Literature Review and Research Hypothesis” provides a review of existing literature on the research topic and presents a theoretical analysis of the effects and mechanisms of DFL on income inequality. Based on this analysis, research hypotheses are proposed. A description of the data and methodology is provided in Section “Data and Variables.” Section “Econometric Model” presents the econometric models used in this study. A discussion of the empirical results and the results of the mechanism analysis is presented in Section “Empirical Analysis”. Section “Conclusions and Policy Implications” concludes and proposes policy implications.

Literature Review and Research Hypothesis

The Impact of Digital Financial Literacy on Rural Income Inequality

Scholars have conducted extensive research into the meanings and implications of financial literacy. The original definition of financial literacy was focused on an individual’s ability to allocate and manage their wealth rationally, with the goal of making effective decisions (Noctor & Stradling, 1992). Subsequent scholars have expanded on the definition of financial literacy to include knowledge, application, and awareness as well (Bayar et al., 2020; Hung et al., 2009; Huston, 2010; Lusardi & Mitchell, 2008, 2011). At the same time, there has been a lot of literature analyzing the financial literacy of rural households. For example, Chang et al. (2022) measured the level of financial literacy among rural households in China’s relatively poor areas, using indicators such as understanding of basic financial concepts, savings and investment planning, financial risk identification, and investment in financial education and training. Twumasi et al. (2022 measured the financial literacy of Ghanaian rural farmers across seven aspects including interest rate, inflation, risk diversification, loan decisions, time value of money, money illusion, and insurance. Unlike other scholars, Tan et al. (2022) assessed the financial literacy level of the farmers surveyed by utilizing a set of 13 qualitative questions instead of quantitative calculation problems.

As digital financial products and services such as mobile payments, digital credit, and digital investment continue to rapidly develop, the conventional definitions and measurement indicators of financial literacy have become insufficient in depicting the unique features of digital finance. Consequently, a growing number of scholars posit that there is a need to conduct additional research on financial literacy within the framework of financial digital transformation (Lyons & Kass-Hanna, 2021; Ravikumar et al., 2022; Stephen, 2022). Regarding the definition of digital financial literacy, the majority of scholars define it as the acquisition of knowledge, skills, attitudes, and behavioral habits that individuals require to effectively participate in financial transactions and utilize digital financial services via digital devices (Azeez & Akhtar, 2021; Saini, 2019). Currently, a lot of scholars are really focused on figuring out how to measure digital financial literacy, and most of them are working hard on developing new and better measurement indicators. Lyons and Kass-Hanna (2021) have proposed a conceptual framework for digital financial literacy that includes five key dimensions: basic financial and digital knowledge, awareness of positive financial attitudes and behaviors, ability to make digital financial transactions, ability to make appropriate financial decisions, and self-protection. To define and measure these aspects, they suggest using metrics such as compound interest calculation, inflation, and risk diversification, as well as the ability to handle digital payments and so on. Prasad et al. (2018) have identified four dimensions of digital finance literacy, which are basic knowledge, practical experience, risk awareness, and financial skills. Si et al. (2022) attempted to measure digital financial literacy by adding content such as digital payments, digital wealth management, and digital lending on the basis of compound interest calculation, inflation, and risk diversification. While previous research has established a strong theoretical foundation and empirical basis for this study, these studies have not delved fully into the digital financial literacy status of rural households. Given the ongoing spread of digital finance in rural regions, it’s worth highlighting that digital financial literacy can have a major impact on the economic outcomes that digital finance can generate for the local economy.

Currently, scholars have mainly explored the impact of financial literacy on farmers’ income, while research on the impact of digital financial literacy on farmers’ income is not enough. Most scholars view financial literacy as a human capital element and they argue that the improvement of digital financial literacy can improve the accessibility of financial services to farmers and thus contribute to their income levels (Lusardi & Mitchell, 2014; Twumasi et al., 2022). It has been shown that lack of financial literacy leads to poor or incorrect investment and borrowing decisions by rural households, which in turn reduces the household’s ability to generate income (Berry et al., 2018). At the same time, a higher level of financial literacy can help farmers reduce the financial risks associated with investing or borrowing, and thus reduce the negative impact of financial risks on income (Banks et al., 2020; Lusardi & Mitchell, 2017). Some scholars have also empirically tested the poverty reduction effect of financial literacy and found that it is more conducive to improving rural low-income households, thus proving the significant poverty reduction effect of financial literacy (Tan et al., 2022; H. D. Xu et al., 2023).This study suggests that digital financial literacy can be defined as the understanding, analysis, management, and communication of digital finance issues. Reflecting our belief that the level of DFL in rural families is heterogeneous, Setiawan et al. (2020) note that DFL is affected by socio economic standing. Rural families with higher educational attainment and higher financial asset holdings tend to have higher DFL. These families usually have a high wealth (Lusardi & Mitchell, 2014; Prasad et al., 2018). As the DF grows, financial markets become increasingly accessible to rural households. However, owing to the heterogeneity of DFL, the development of DF may mainly improve the income of families with high initial wealth. In this context, the improvement of DFL will mainly improve the efficiency of DF use in low-income families, and thus narrow the income gap between them and high-income families. This leads to the following hypothesis:

Hypothesis 1. The improvement of digital financial literacy narrows the rural income gap.

Digital Financial Literacy, Financial Asset Allocation, and Rural Income Inequality

Fewer studies have examined the impact of digital financial literacy on rural household financial behavior, but many studies have analyzed the role of financial literacy. For example, Sayinzoga et al. (2015) found that the number of savings and loans among Rwandan smallholder farmers increased significantly after they were trained in financial literacy. Murendo and Mutsonziwa (2017) further explored the impact of financial literacy on the savings structure of rural households and found that as the level of financial literacy increased, the share of formal savings (savings with formal financial institutions) increased. On the other hand, Schoofs (2022) pointed out that financial literacy did not have a significant impact on farmers’ saving behavior, but only changed their borrowing behavior, causing them to shift from informal to formal borrowing. Raza et al. (2023) reached similar conclusions after studying the relationship between farmers’ financial literacy and credit availability in Pakistan. In studying the impact of rural e-commerce development on farmers’ digital financial market participation, L. L. Su et al. (2021) found that farmers with higher financial literacy were more able to actively participate in the digital financial market (e.g., digital payments, digital wealth, etc.). Gaurav et al. (2011) empirically analyzes the impact of financial literacy training on rainfall insurance adoption by farmers in India. And the study revealed that financial literacy training increases rainfall insurance adoption from 8% to 16%.

Unlike traditional financial service models, recent financial digitization in emerging economies has led to the rapid introduction of new financial products, which is more evident in their rural areas. The lack of financial literacy may slow the adoption of these products. DFL is helpful in lowering entry barriers and enabling low-income rural households to access more readily to diversified financial markets. It is well known that DF has lowered the entry threshold of the financial market, such as the bank wealth management products, fund, and stock markets (He & Li, 2020; Jia et al., 2021). However, in the process of using DF, low-income rural households may be excluded from digital finance because they are presumed to have quite limited DFL compared to high-income households who have developed considerable financial literacy under the traditional finance model (Guo et al., 2022). DFL is an important determinant of a household’s capability to collect and process financial information and to make appropriate financial resource allocation decisions. Low-income rural households with high DFL can skillfully use digital finance to diversify their financial assets, which reduces risks and increases property returns (Chu et al., 2016). This is helpful in alleviating the income inequality between them and high-income households. Given these assumptions, we propose the following second hypothesis:

Hypothesis 2. DFL can alleviate rural income inequality by optimizing the financial asset allocation of rural households.

Digital Financial Literacy, Entrepreneurial Probability, and Rural Income Inequality

With respect to the relationship between financial literacy and entrepreneurship, many scholars have conducted extensive and in-depth investigations. Some scholars found that digital financial literacy has significant and positive influence on entrepreneurial performance. Some scholars assert that financial literacy has significant and positive impact on households’ entrepreneurial probability (R. Li & Qian, 2019; Luo et al., 2021; Sayinzoga et al., 2015). The explanation they give is that with increased financial literacy, households would have easier access to and efficient use of credit, their risk tolerance would increase, which in turn would increase the likelihood of starting a business (S. Liu et al., 2023; Oggero et al., 2020; Riepe et al., 2022). In addition, some scholars have researched the impact of financial literacy on household entrepreneurial performance. Luo et al. (2021) found that there was a positive effect of financial literacy on business ownership and business innovation after analyzing data from 38,556 households in China. After analyzing the impact of financial literacy training on entrepreneurial performance of African entrepreneurs, Brixiova et al. (2020) concluded that the training is more conducive to improved entrepreneurial performance of male entrepreneurs. Tian et al. (2020) explored the impact of executive financial literacy on innovation in small and medium-sized enterprises in China and found that the executive financial literacy can significantly improve firm innovation.

It is generally acknowledged that the ability to obtain financing is an important part of entrepreneurial capability (Chang et al., 2022). Compared to high-income families, low-income rural families need more support from external funds when starting ventures (Burgess & Pande, 2005). However, many low-income rural households with entrepreneurial abilities may not have the enough digital financial literacy to acquire funding to start a venture (C.-W. Liu, 2020; Muhammad et al., 2017). Meanwhile, owing to low initial wealth and lack of risk management skills, rural households with low incomes are more averse to the risk of entrepreneurial failure than high-income households. Meanwhile, there is already evidence to suggest that improving financial literacy can have a greater impact on the entrepreneurship of lower-income populations. Chang et al. (2022) confirm the positive impact of financial literacy on self-employment entrepreneurship among poor rural households. Luo et al. (2021) show that the improvement of DFL can particularly benefit vulnerable populations, particularly those living in rural or less-developed areas.

While few studies explore how DFL impacts rural income inequality through entrepreneurship, we suppose there might be a mediating effect of entrepreneurship. DFL can help low-income farmers start businesses in two ways to narrow the income gap with high-income families. As DFL improves, rural low-income households are likely to acquire a better understanding of digital finance and, thus, have better access to finance services to support their entrepreneurial activities. On the other hand, DFL can reduce the risk aversion of low-income farmers and equip them with better risk-management skills, making them willing to accept new things to improve the possibility of entrepreneurship. In this way, we suggest a third hypothesis.

Hypothesis 3. DFL can alleviate rural income inequality by improving rural households’ entrepreneurial probability.

Data and Variables

Data

We derived our data from the 2017 and 2019 China Household Finance Survey (CHFS) conducted by the Southwestern University of Finance and Economics (SWUFE). This survey gathered detailed information at the micro level about various aspects of household finances and economic activity (Gan et al., 2016). This survey provides a wealth of information that fits well with the topic of our research. This database has been proven by much of the literature to be highly authoritative in the study of income inequality (R. Li et al., 2023; Wan et al., 2021; C. Zhang et al., 2014). According to the needs of this study, data from rural sample households who received the questionnaire in both 2017 and 2019 were extracted from this paper. To avoid errors due to outliers and missing values, we removed households with missing values and applied a 1% tailing process to the outliers. After the processing, we finally obtained the sample data of 7,946 rural respondent households. These households are distributed across 29 provinces and 365 counties. In addition, the provincial control variable data were obtained from the China Socio-Economic Development Statistical Database.

Dependent Variable

We refer to the existing literature examining household inequality (Carpantier et al., 2018; Firpo et al., 2009; Schneck, 2020) and use the value of the Gini recentered influence function (Gini-RIF) for each rural household as the dependent variable. The calculation process for this value consists of two steps. First, we calculate the influence of each rural household on the income Gini coefficient based on their total household income per capita and income distribution, which is the influence function calculation. Gini coefficient influence function is defined as a function of income y and the income distribution function Fy and is defined as

where G(Fy) is the Gini coefficient for the income distribution function Fy. Hyi is a distribution that takes a value only at yi.

Second, we calculate the value of the recentered influence function (RIF) for each rural family, Gini-RIF, which is a function of one family income yi and the given distributional statistic G(Fy) in equation (1). The Gini-RIF can be defined as follows:

where RIF(yi,G(Fy)) is the Gini-RIF. Obviously, the RIF for the Gini coefficient is the Gini coefficient, G(Fy), and the influence function for this statistic is IF(yi,G(Fy)).

Core Independent Variable

We take the level of digital financial literacy among rural households as the core independent variable. As mentioned in the previous literature review, there is no consensus on the indicators for measuring the level of digital financial literacy among rural households. We believe that digital financial literacy covers not only financial knowledge and financial skills, but also emphasizes the digital skills of residents in using financial products.

First, referring to Prasad et al. (2018) and Lyons and Kass-Hanna (2021), three major questions were selected to measure the respondents’ financial literacy in terms of interest rate calculation, inflation calculation and risk. Following Lusardi and Mitchell (2011), due to our belief that incorrect answers represent a different level of financial knowledge than those who cannot calculate or do not do any calculations, two dummy variables were created for each question. It indicates whether the question is answered correctly in the first dummy variable, and whether it is answered directly in the second dummy variable. Second, three indicators are selected to measure the financial skills: whether rural households have stock accounts, whether they hold funds, and whether they hold credit cards. Third, three indicators are selected to measure rural households’ digital skills in using financial products: whether they hold internet wealth management products, whether they choose computers or mobile terminals such as cell phones to make payments, and whether they conduct internet borrowing for daily life activities such as production and business and purchasing a house or car. Thereby, the DFL was divided into 12 indices. Detailed evaluation indexes for DFL are shown in Table 1.

The Evaluation Index System of DFL.

Following N. Xu et al. (2020), the above 12 variables were subjected to principal component factor analysis (PCFA) to calculate the composite score, which was used to measure the level of digital financial literacy of rural households. Validity and reliability tests show that KMO value is 0.6319 and Bartlett’s test is significant. These tests imply that the 12 indices are suitable for constructing a composite indicator using factor analysis. After factor rotation, the result of the PCFA is reported in Table 2. Based on the rule that the eigenvalue is greater than one, we selected the principal component. As presented in Table 2, the 11 tertiary indices (see Table 1) were regrouped into four principal components explaining 54.05% of the total variance. Meanwhile, we present the PCFA components loadings in Table 3.

Total Variance Explained.

Note. Extraction method is principal component analysis. Rotation method is Varimax with Kaiser normalization.

Rotated Factor Loading Matrix.

Note. Extraction method is principal component analysis. ***indicates significance at the 1% level.

Mechanism Variable

The previous theoretical analysis suggests that digital financial literacy can reduce the income gap among farmers by optimizing the allocation of financial assets and increasing the probability of entrepreneurship. According to earlier studies (Schoofs, 2022; Setiawan et al., 2020), digital finance can change the financial behavior of rural households and enrich the variety of their financial assets. Meanwhile, an increase in digital financial literacy levels may improve rural household investment strategies by enhancing their allocation of high-risk financial assets. Accordingly, we use two indicators to reflect the allocation of financial assets of rural households: the variety of financial assets and the ratio of risky financial assets. Among them, the variety of financial assets of rural households includes term deposits, wealth management products, funds, stocks, bonds and so on. The ratio of risky financial assets is reflected by the proportion of risky financial assets such as wealth management, stocks, funds, and financial derivatives owned by households to financial assets.

As for the variable reflecting the probability of entrepreneurship, referring to existing studies (R. Li & Qian, 2019; Muhammad et al., 2017; J. Zhao & Li, 2021), we measured it by the respondent’s answer to the question, “Is your household currently engaged in commercial and industrial production projects, including self-employment, renting, transportation, online stores, and running a business?” If the head of the household answers “yes,” the household is considered to have started a business and the variable is assigned the value of 1, otherwise it is assigned a value of 0.

Control Variable

Additionally, we take measures to minimize the potential impact of omitted observable factors on our estimation results by carefully controlling as many relevant variables as possible. We select them by drawing upon the existing literature on rural income (Altunbaş & Thornton, 2020; Ding et al., 2023; Khan et al., 2021; M. Li & Xiong, 2018; Mitra et al., 2020; Morduch & Sicular, 2000; G. Yu & Lu, 2021). Specifically, individual characteristics of the head of rural household mainly include the age and its squared term, gender, marital status, education, party, and Hukou. Household characteristics mainly include family population size, dependency ratio, housing demolition, and the number of houses owned. To account for province-level heterogeneity, we control for the province characteristics, including the logarithm of the GDP per capita in the province where the rural household is located, and government intervention that is reflected by the ratio of total government fiscal expenditure to GDP.

Variables Descriptive Statistics

Table 4 provides an overview of the selected variables through their descriptive statistics. It can be observed that the mean value of the logarithm of Gini-RIF is −0.803, the minimum value is −1.849, and the maximum is 4.509. To further illustrate the income disparity situation of rural households, we calculated the Gini coefficient of total per capita household income based on the sample data. The results show that the Gini coefficients for 2017 and 2019 are 0.583 and 0.551, respectively. Although the Gini coefficient decreased by 0.032, it is still higher than the international Gini coefficient warning line (0.4), which indicates a large income gap in rural areas.

Variable Definitions and Descriptive Statistics (N = 7,946).

In terms of DFL, the average value of DFL index was 0.010. Its minimum and maximum values are −2.350 and 2.581, respectively. Further analysis showed that on average, each rural household could answer only one of the three questions about financial knowledge correctly. Regarding to financial skills, only 7% of households have used credit cards. As for digital financial skills, among the sample households, while the percentage of households using digital payments is high (19.2%), the percentage of households holding digital investment products and using digital credit is low (about 3%). The above data indicate that the level of DFL in rural families is low. Furthermore, from the descriptive statistics of the channel variables, each rural household owns 1 to 2 financial assets on average, the average ratio of risky financial assets held by rural households is 0.6%, and 9% of the sample households have started a business.

With regards to control variables, the average age of householder is 58.648 years, 88.4% are male, 90.3% have a spouse, while the average education level among them is only between primary and secondary school, indicating that most householders have low education level. In addition, 10.5% of household heads are CPC members, and the proportion of urban Hukou is only 5.6%. There are 3 to 4 people in each rural family. The mean dependency ratio is 35.4%, which is generally consistent with the data in other studies (Ma et al., 2022). A total of 3.9% of surveyed rural households has experienced demolition. Averagely, each rural household owns 1 to 2 houses. On average, the value of the logarithm of the GDP per capita of the province where the sample households are located is 10.946, and the ratio of total government fiscal expenditure to GDP is 24.9%.

Econometric Model

A major challenge in estimating the effects of DFL on rural income inequality is the omission of potential confounding factors that affect both. To mitigate the adverse effects of confounding factors on the regression results, this study attempts to adopt a two-dimensional fixed-effects model. The baseline regression equation can be provided as follows.

Where the subscripts of i and t denote the rural household and the survey time, respectively. As mentioned earlier, the dependent variable lnrifgini is logarithm of the value of the Gini recentered influence function (Gini-RIF) for each rural household, and the core independent variable dfl is the level of digital financial literacy of rural households calculated based on principal component factor analysis. Control refers to a set of control variables including the household and province characteristics. Moreover, α0 represents the intercept term in the equation. The parameters that need to be estimated are α1 and β. If the coefficient of α1 is significantly negative, it means that the increase in digital financial literacy helps to reduce the Gini coefficient and achieve a reduction in the income gap. γ i represents the household-fixed effect. δ t represents the time-fixed effect. Additionally, there is an independent and identically distributed random error term, ε, which captures any other factors that could affect a household’s value of the Gini recentered influence function.

However, DFL may be endogenous. It is possible that DFL is improved by narrowing the income gap. For example, low–income households actively improved their DFL to reduce income disparities with high–income households. In addition, DFL and income inequality may be correlated with some unobservable factors. To address the endogenous issues mentioned above, we used the instrumental variable method and estimated the coefficients using a two-stage least squares method. The equations are as follows.

Where Z is instrument variable, and

As analyzed in the previous theory, DFL may reduce the rural income gap through two channels: optimizing financial asset allocation and increasing the probability of entrepreneurship. To verify the above conjecture, we constructed the following two models:

Where typefin represents the types of financial assets, and entre represents the entrepreneurship.

Empirical Analysis

Effect of DFL on Rural Income Inequality

Table 5 presents the benchmark results of DFL on rural income inequality based on equation (3). To investigate the effects of DFL, we perform the entire estimation process in a stepwise regression approach. Out of these results, the first column displays an estimate result that does not consider any control variables. Columns (2) to (4) build upon the column (1) by sequentially incorporating householder, household, and province characteristics in the presentation of the results. According to the estimates obtained from columns (1) to (4), the DFL variable is consistently found to hold negative significance with 1% confidence levels. Furthermore, regardless of whether additional observable factors are considered or not, its estimated coefficients remain stable at approximately −0.02. This implies that a one-standard-deviation improvement in DFL is associated with a decrease of 2.012% (−0.02 × 1.006) in rural Gini coefficient. The above evidence confirms that an improvement in DFL is conducive to alleviating rural income inequality and strongly reveals the important role of digital financial literacy in alleviating rural income disparities.

DFL and Rural Income Inequality: Benchmark Regression.

Note. The robust standard errors are shown in parentheses. To provide more accurate estimates, we present robust standard errors for each household level, which are shown in parentheses.

, **, and * indicates significance at the 1%, 5%, and 10% levels, respectively.

With respect to the control variables, the estimation results are shown as an example in column (4) of Table 5. The estimated coefficient of the age of the household head is significantly negative while the estimated coefficient of the age squared term is significantly positive, indicating a u-shaped relationship between age and income disparity. With the increase in age, farmers accrue experience in their work, leading to a reduction in the income gap caused by initial differences in ability. However, as they reach elderly age, several studies show that differences in pensions will cause an increase in their income gap (Hanewald et al., 2021; Zhan et al., 2021). The education level of the householder appears to have a negative and statistically significant impact on Gini-RIF, suggesting that the improvement of educational levels benefits the narrowing of income disparities in rural areas. The possible reason for this may be that farmers with longer years of education have greater knowledge to prosper and more proficiency in financial skills, and thus lead to more pronounced “spillover effects” of DFL. This finding is highly aligned with C. L. Chen (2016) and Campos et al. (2016). The hukou variable is positively and significantly correlated with the Gini-RIF. Rural families with urban hukou enjoy more benefits, such as state subsidies and better education for their children (Wang & Schwartz, 2018). This allows them to accumulate wealth faster than households with rural hukou only. This can further widen the rural income gap. The estimated coefficient of family size is −0.055 and statistically significant at the 1% level. Greater household membership is associated with higher levels of labor income, which facilitates a narrowing of income disparities between these households and those of greater affluence. In contrast, the estimated coefficient of dependency ratio is significantly positive, implying that higher family dependency ratios are not conducive to closing the income gap due to the increase in family burden. The estimated parameter of demolition is negative and statistically significant, suggesting that demolition in rural areas has alleviated income inequality. The Chinese government has adopted a policy of relocation to rural areas in poor regions (M. Li & Xiong, 2018; L. Zhang et al., 2023). These low-income rural families often receive some compensation after experiencing demolition and relocation, which helps to narrow the income gap between them and wealthy families. The per capita GDP of the province where the rural household is located appears to have a significantly negative impact on Gini-RIF. This may be explained by the trickle-down effect of economic growth, which holds that the first rich group will lead the low-income group to become rich along with the economic growth, and then achieve common prosperity (Chroufa & Chtourou, 2022; Shin, 2012).

Robustness Checks

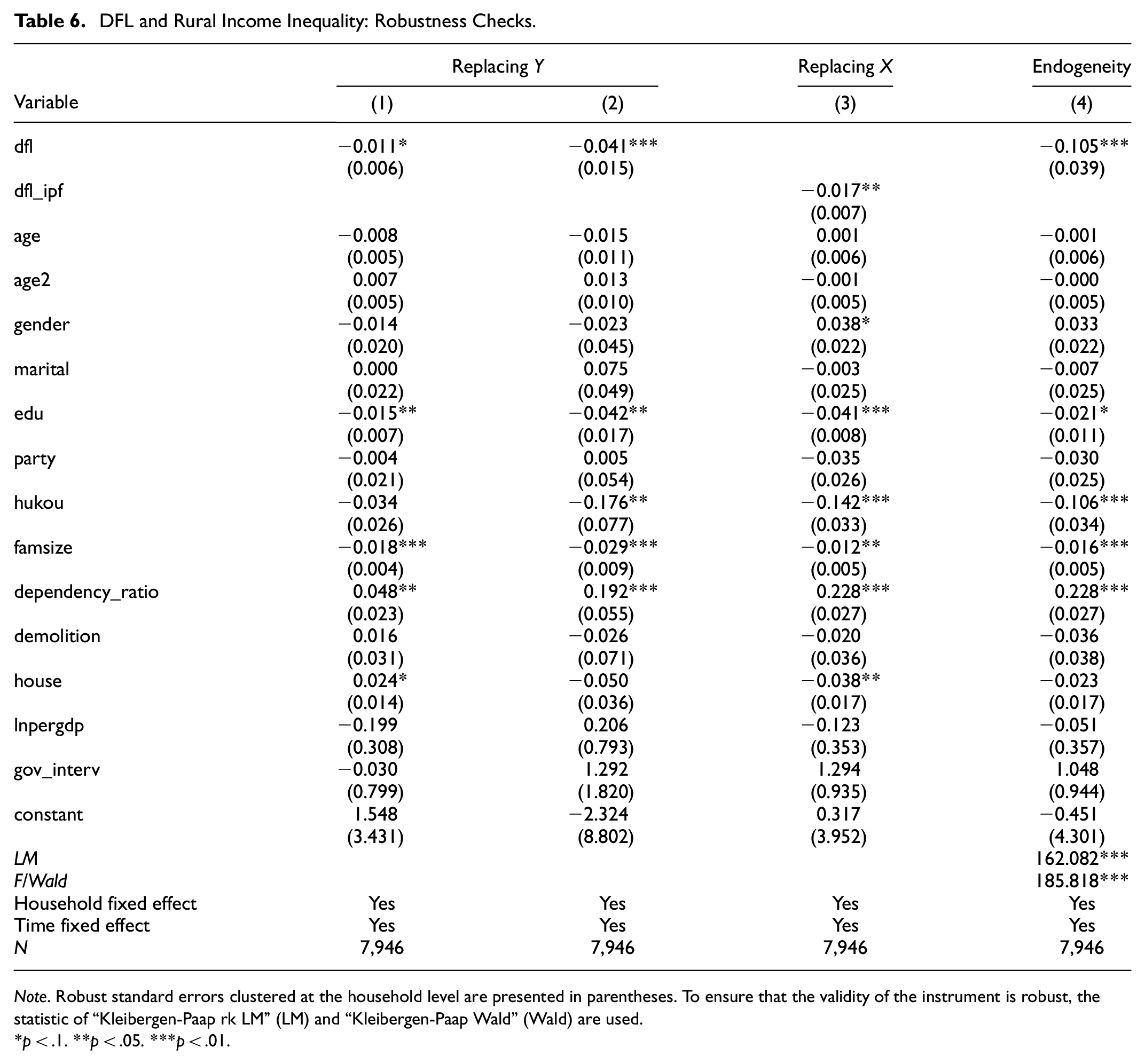

To ensure the robustness of our estimates, we conducted a set of robustness checks that include the replacement of dependent and key independent variables, as well as alternative estimation methods. The pertinent empirical results can be found in Table 6.

DFL and Rural Income Inequality: Robustness Checks.

Note. Robust standard errors clustered at the household level are presented in parentheses. To ensure that the validity of the instrument is robust, the statistic of “Kleibergen-Paap rk LM” (LM) and “Kleibergen-Paap Wald” (Wald) are used.

p < .1. **p < .05. ***p < .01.

First, we estimate the degree of income inequality by replacing the Gini coefficient with the Atkinson and Theil index, and recalculate the recentered influence function values based on the Atkinson and Theil index, respectively. The Atkinson Index is more sensitive to inequality at the bottom of the income distribution, while the Theil index is more sensitive to the top of the income distribution (De la Vega & Volij, 2013; De Maio, 2007). As shown in column (1), we redefine the dependent variable as the logarithm of the value of the Atkinson recentered influence function (Atkin-RIF). Meanwhile, we use the logarithm of the value of the Theil recentered influence function (Theil-RIF) as another dependent variable in column (2) of Table 6. The results presented in column (1) and (2) of Table 6 indicate that DFL still significantly reduces the income inequality, suggesting that both measures support the previous conclusions.

Second, to provide a more comprehensive assessment of the levels of digital financial literacy within rural households, we recalculate DFL using iterative principal factor analysis (IPFA) based on the 12 indicators in Table 1 to obtain the variable dfl_ipf. Then we use it as the core independent variable in column (3) of Table 6. As shown in column (3), the dfl_ipf variable is negative significant at the 5% level and the coefficient of it is −0.017, which again supports the conclusion that DFL mitigates rural income inequality.

Third, to further lower reverse causality errors, this article estimates causal relationships between DFL and rural income inequality with IV, as shown in Column (4) of Table 6. It is possible that DFL is improved by narrowing the income gap. For example, low–income households actively improved their DFL to reduce income disparities with high–income households. In addition, DFL and income inequality may be correlated with some unobservable factors. To address the endogenous issues mentioned above, we used the instrumental variable method. This study uses the average level of household DFL at the community level as an instrument for a household’s DFL. Households were excluded when calculating the instrument variable. The DFL of one family can be affected by that of other families (Lusardi & Mitchell, 2014). Meanwhile, the DFL of others is regarded as exogenous to a family’s financial decision making. Therefore, this instrumental variable was valid. Using this method, we were able to obtain consistent estimates of the impact of DFL on income inequality in column (4).

Mechanism Analysis

Given the significant and negative impact of digital financial literacy on rural income inequality, the crucial question that follows is how it affects this inequality? The following two aspects are the mainly focus of our exploration. As mentioned earlier, we first examine the effect of digital financial literacy on the allocation of financial assets in rural households, which is measured as the variety of financial assets and the ratio of the risky financial assets. Second, we investigate the effect of DFL on the entrepreneurial probability, which is represented by whether rural household currently engaged in commercial and industrial production projects, including self-employment, renting, transportation, online stores, and running a business (0 = no; 1 = yes).

The test results for the rural household financial asset allocation mechanism are presented in column (1) and (2) of Table 7. Column 1 presents the regression results on the variety of financial assets. Since the variable of the variety of financial assets held by rural households is a non-negative integers, to improve the validity of the estimation, we choose a panel Poisson regression model to estimate the effect of digital financial literacy on the variety of household financial assets. As shown in column (1), the coefficient of DFL is 0.137 and is significantly positive at 99% confidence interval. According to the characteristics of Poisson distribution, this means that, after DFL increases by one unit, the number of financial asset types held by the household will be 1.147 (e0.137) times that of before. This significant impact implies that increased digital financial literacy can alleviate the rural income gap in reverse. The potential explanation is that the reduction of the rural income gap needs to be achieved through the increase of financial inclusion (Das & Chatterjee, 2022; Qian et al., 2022). One of the direct effects of digital financial literacy on financial inclusion is to improve farmers’ ability to get financial products from the demand side. Yet this ability is sorely lacking among low-income rural households (S. J. Chen et al., 2022). As digital financial literacy increases, the variety of financial assets of low-income households will increase more than that of high-income households. This leads to a stronger income enhancement effect for low-income rural households (Meikle et al., 2020). From column (2) of Table 7, we observe that DFL significantly increase the ratio of the risky financial assets of rural households. The main reason is that digital financial literacy can increase farmers’ awareness of risky financial products and reduce their risk aversion (Long et al., 2023). In this case, farmers will increase the proportion of risky financial assets held through digital channels. At the same time, risky financial assets have high returns, which can help low-income farmers achieve rapid wealth accumulation and thus narrow the income gap with high-income farmers. Thus, Hypothesis 2 is verified.

DFL and Rural Income Inequality: Mechanism Test.

Note. The robust standard errors are shown in parentheses.

, **, and * indicates significance at the 1%, 5%, and 10% levels, respectively.

The column (3) of the Table 7 shows the test result of the mechanism of digital financial literacy to narrow the income gap by improving rural family entrepreneurship probability. Given that the dependent variable is a binary discrete variable, we opted to employ a panel logit fixed-effects model to evaluate the impact of digital financial literacy on the probability of entrepreneurship. According to column (3), the coefficient for digital financial literacy is positive and significantly different from zero in terms of average marginal effects. Further, we find that the value of the coefficient of DFL is 0.005, indicating that for an increase of 1 unit in DFL, the probability of rural households starting a business will increase by 5%. Digital financial literacy can mitigate rural income inequality in this way. It can be explained by the income-generating and spillover effects of entrepreneurship. On the one hand, low-income rural households achieve an increase in income through entrepreneurship (Ding et al., 2023; Kimhi, 2010); on the other hand, the employment of low-income rural households driven by entrepreneurship will likewise increase the income of low-income households. With these two effects, rural entrepreneurship will greatly increase the income of low-income households, and thus narrow the income gap between them and wealthy households (Janssens et al., 2019; Y. Su et al., 2023). Accordingly, Hypothesis 3 is verified.

Conclusions and Policy Implications

Conclusions

Globally, the digital transformation of finance is accelerating, which provides opportunities to increase the degree of financial inclusion. For the world’s largest developing country, China’s financial digital transformation can lead to economic growth, but also provide support to alleviate income disparity. However, the financial digital transformation has placed higher demands on the financial literacy of the population, and the concept of digital financial literacy has been introduced. In this context, more and more studies have begun to focus on the importance of digital financial literacy to the development of digital finance. Nevertheless, little attention has been paid to the important role of digital financial literacy in achieving shared prosperity by examining the link between digital financial literacy and rural income disparity, especially in the context of China. To narrow the research gap, this article exploits a recentered influence function approach, and a two-way fixed effect panel model to investigate the impact of digital financial literacy on rural income inequality by leveraging nationally representative household-level data from the 2017 and 2019 CHFS.

Empirical results reveal that digital financial literacy contributes to the reduction of income inequality in rural areas. This conclusion remains valid after a series of robustness checks such as replacing the dependent variable, replacing the independent variables, and accounting for endogeneity issues. The mechanism test found that the above effect is mainly achieved by enriching the variety of household financial assets, increasing the proportion of risky financial assets, and improving the probability of rural household entrepreneurship.

Policy Implications

The conclusions drawn from our research have important policy implications for not only China, but also other developing countries seeking to narrow the income gap in rural areas through the utilization of digital financial transformation. Firstly, it is also crucial for the government to improve digital financial literacy when it promotes the development of digital finance to achieve common prosperity. Governments and financial institutions can work together to popularize digital financial knowledge to low-income groups in rural area. Secondly, supporting the development of the investment consulting industry should be a priority for the government. When rural households invest through digital financial channels, timely investment advisory services can help them optimize household financial asset allocation. Third, the government should create a good entrepreneurial environment and actively support rural low-income groups to start business. By introducing policies to support entrepreneurship, the government can maximize the impact of digital financial literacy in decreasing the income gap by increasing the probability of entrepreneurship in rural households.

Limitations and Future Research Directions

Because this article is limited by the availability of data, there are some shortcomings that could be addressed in further studies. Specifically: (1) considering the representativeness of the database, this study measured the value of the recentered influence function of rural household income gap based on the national sample, and future studies can measure this value from a regional perspective to explore the differences in the impact of digital financial literacy on regional income gap; (2) the relationship between digital financial literacy and rural income disparity may be influenced by the village environment in which the farmers live, and future research can further explore the impact of digital financial literacy on rural income disparity by controlling for village characteristics variables; (3) due to the dynamic nature of the relationship between DFL and rural income inequality, future studies can use long-term tracking panel data to further explore this relationship.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Social Science Foundation of China (grant number: 23BGL185), and the Shandong Provincial Natural Science Foundation (grant number: ZR202103020652).

Data Availability Statement

The research for this paper utilizes data sourced from the China Household Finance Survey (CHFS), a comprehensive and longitudinal study that encompasses a wide range of Chinese communities, households, and individuals. The CHFS is dedicated to delivering to scholars an extensive and superior dataset that reflects the current state of China. Interested parties can access this data through the CHFS official website, which is available at the provided link (![]() ). Additionally, the specific dataset and related programs referenced in this paper can be made available upon request to the paper’s corresponding author.

). Additionally, the specific dataset and related programs referenced in this paper can be made available upon request to the paper’s corresponding author.