Abstract

In the contemporary landscape of corporate governance, where organizations are increasingly recognizing the importance of not only generating profits but also contributing to societal progress and environmental preservation, there arises a pressing requirement for a comprehensive financial index that accurately captures these multifaceted commitments. In this study, we introduce a novel sustainable finance index that utilizes the Grey Relational Analysis (GRA) method to comprehensively capture the three fundamental dimensions of sustainability: economic, social, and environmental aspects. The GRA methodology ensures a comprehensive and balanced consideration of each dimension, thereby providing a holistic perspective. The deployment of this index, which encompasses a wide range of criteria, on an extensive 11-year financial dataset (2010–2021) obtained from 21 prominent commercial banks, reveals fascinating and thought-provoking findings. Banks frequently demonstrate intermittent commitments, wherein their pursuit of short-term gains often takes precedence over the imperative of economic sustainability. While some banks have been notable champions of social endeavors, it is concerning to observe that environmental sustainability has unfortunately taken a backseat in the overall banking landscape. This index provides a meticulous assessment of sustainable financial paradigms, ensuring accuracy and reliability. It serves as a valuable resource, enhancing the quality of research and providing corporations with a sophisticated framework to evaluate and enhance their sustainable financial paths.

Plain language summary

We conducted a study with the aim of creating a comprehensive scoring system for businesses, allowing them to evaluate not just their profit-making abilities, but also their contributions to society and the environment. Using a method known as Grey Relational Analysis (GRA), we ensured that three primary areas: economic performance, societal contributions, and environmental protection, received equal emphasis in our scoring system. We then tested this on the financial records of 21 major banks, spanning 11 years from 2010 to 2021. Our findings indicated that while some banks excelled in specific areas, none consistently performed well across all three. For instance, a bank might be actively supporting societal initiatives but might lag in environmental conservation efforts. The significance of our work lies in its potential to guide banks and other businesses in identifying areas of improvement. Additionally, our scoring system can serve as a tool for researchers keen on delving deeper into the field of sustainable finance. However, it’s worth noting that our study has its limitations. Our focus was solely on large commercial banks within a specific timeframe, which means the results might not resonate with smaller banks or other business sectors. Also, while our evaluation method strives for balance, there’s scope for refining it further to cater to the evolving landscape of sustainable finance.

Keywords

Introduction

The Sustainable Development Goals (SDGs), adopted by the United Nations in 2015, require worldwide action to eradicate poverty, safeguard the planet’s environment, and promote prosperity and peace for every person by 2030 (Nino, 2015, p. 2). The public sector, private sector, and institutional capital are also required to achieve this agenda, as well as an extensive transformation of socioeconomic behavior, policies, and standards to achieve the stability and adaptability of societal livelihood. Otherwise, irresponsible production and consumption consequences will present the global community with sustainability challenges (Sachs et al., 2019). With the growth of technology, the business revolution will bring prospects for competitive advantage, revolution, security, progress, wealth, employment, maintenance of social stability, and influence on the environment (Rowledge et al., 2017). The financial sector can be crucial in structuring and allocating transitional resources. A practical and established financial sector requires a well-balanced structure of procedures, laws, and regulations and consideration of sustainability risks in financing and investment decisions. The financial sector may also play a role in mobilizing and channeling its financial assets, “moving the trillions” toward environmentally beneficial, resilient, and sustainable investments (Buch & Weigert, 2021). Financial investors, financial advisors, and the financial sector view this change as a financial opportunity and adjust their investment and financing plans as necessary. Today, in this competitive market, it is essential for businesses to accept responsibility for their actions, whether they are beneficial or harmful to society and the environment (Aggarwal, 2013) along with economic aspects. During investment selections, the investors grew more cognizant of the non-financial performance of the enterprises in addition to the financial performance (Ernst & Young, 2009).

Numerous governments, regulatory and financial bodies in the Asia-Pacific region are currently incorporating climate and environmental issues into their strategy frameworks and encouraging their financial institutions to integrate environmental, social, and governance (ESG) standards into their financing and investment decisions, as well as incorporating environmental and social risk management (ESRM) practices (Volz, 2019). In addition, most monetary, regulatory, and governing authorities in Asia-Pacific and other regions need more expertise in environmental risk management and sustainable finance (Durrani et al., 2020).

Sustainable Finance in Broader Policy Framework

People have been concerned about the impact of economic activities on social structures and the natural world for many years (Migliorelli & Dessertine, 2019). However, a universally accepted, adaptable, and workable definition of sustainable finance has yet to be available (Migliorelli, 2021). Because it directly impacts the standard of living, prosperity, development, and well-being of the population, sustainability is regarded as a crucial pillar in the survival and growth of an organization (Jilcha & Kitaw, 2017). The entirety of a company’s sustainability can be broken down into three components: economic sustainability, social sustainability, and environmental sustainability (Vallance et al., 2011). Therefore, to maintain the satisfaction of its internal and external stakeholders, the company must engage in various sustainable practices. Moreover, incorporating sustainable practices into a company’s regular business operations can provide that company with a competitive edge and the opportunity to enter new markets (Annunziata et al., 2018). Therefore, sustainable finance is the collective responsibility of all economic sectors, and it is based on all these sectors’ efforts to implement and enhance at least one aspect of sustainability (Migliorelli, 2021).

Globally, the financial industry has recently increased its focus on sustainable finance. Central banks and financial regulators can participate, and they can do so by progressively developing policies to reduce environmental risks and integrate sustainable finance (Dikau & Volz, 2021). Sustainable finance is exemplified by the Sustainable Banking Network (SBN) and the Network for Greening the Financial System (NGFS), a central bank organization. Network for Greening the Financial System is the name of this organization. Between 2017 and 2019, eight central banks developed NGFS, with 54 members (NGFS Annual Report, 2019). NGFS is an independent, consensus-based forum with the mission of promoting best practices, managing climate-related risk in financial institutions, and incorporating the development of a sustainable economy into the use of funds. NGFS was created to achieve these objectives (Durrani et al., 2020).

Administrative and regulatory bodies’ initiative is an additional indicator highlighting the importance of sustainable finance. Local governments and international organizations such as the G20 and the International Monetary Fund (IMF) have taken the initiative to allocate a portion of their limited resources to sustainable development (G20 Green Finance Study Group, 2017; IMF, 2019, 2020).

The United Nations formed the Sustainable Development Agenda 2030 to promote sustainable and comprehensive economic formulation and to engage central banks in developing sustainable financial strategies to accomplish the Sustainable Development Goals, often known as SDGs. UNO developed this agenda to support the Sustainable Development Goals, also known as SDG (Durrani et al., 2020). The Sustainable Development Goals (SDGs) are the benchmark by which the international community must gauge its progress in fulfilling its responsibilities to promote a sustainable environment and society (Migliorelli, 2021). Efforts have been made globally to adopt policies that will mainstream the flow of financial resources devoted to attaining Sustainable Development Goals (SDGs). The importance of sustainable finance is being recognized globally; Sustainability is about ensuring the commitment to meet the UN Sustainable Development Goals (SDGs) by 2030.

Research Objectives

Sustainable finance index provides operative systems for reporting and observing environmental and social situations that can be combined or enhanced to offer more effective guidelines to direct a transition towards sustainability.

Sustainable finance index is developed by independent action by proper research planning, assembling, analyzing and decision support for effective system development for adaptive administration, societal learning and investor’s decision making to evaluate the performance of different businesses.

Moreover, the current study focuses on all the three dimensions of sustainable finance that removes the literary gap by explaining the corporation’s responsibilities towards society and environment along with its shareholders.

The motivation behind importance of the study sustainable finance is to identify the factors those can generate the negative effect on environment sustainability such as fuel consumption, energy consumption, ozone destruction, air pollution, fossil resource exploitation those can influence wellbeing on human being and society.

The aim of the present study is that the sustainable finance index can be used as a benchmark to evaluate the corporate responsibilities towards social sustainability and environmental sustainability.

Literature Review

Sustainable Finance

In recent years, there has been a substantial focus on sustainable financing. Nevertheless, the precise meaning of the phrase could be more explicit (Dimmelmeier, 2021). Due to the ambiguity of the term sustainable finance, the policy development included other terminologies, such as socio-environmental finance, low carbon finance, and green finance. These phrases subdivide sustainable finance into its constituent parts (Forstater & Zhang, 2016). In addition, Haigh (2012) examined the critic’s perspective and concluded that sustainable finance is a “vague signifier.” Stakeholders believe that financial institutions and politicians use the term “sustainable finance” to describe their preferences and viewpoints.

Researchers concluded that most current financial models were created during an era of resource abundance, and a relatively small number of environmental concerns. When the irreversible depletion of natural resources and the environmental damage they cause is not being considered. However, industrial production and redundant competition also contribute to the universe’s movement towards an unhealthy natural environment. Consequently, environmental concerns are becoming the most challenging and complex ecological constraint (Camilleri, 2019). In addition, the rapidly expanding global population and their rapidly expanding wealth unquestionably contribute to a rise in the demand for finite and nonrenewable resources (Camilleri, 2020). But now, modern economic models are centered on reducing carbon emissions and conserving natural resources to overcome environmental obstacles. However, these models cause a decline in the value of businesses’ assets, reducing their profitability and productivity (Munir et al., 2022).

Kumar et al. (2022) defines sustainable finance as the combination of all those activities and factors that could create finance sustainable and contribute towards sustainability. Where the sustainability is defined by World Business Council for Sustainable Development (2002), as the obligation of the business toward sustainable economic growth, as well as the obligation to provide a healthy work environment for their employees, an improved living standard for their families, and a higher quality of life for both the local community and the international community. Therefore, sustainability refers to the notion that society should only use vital and replenishable resources and prevent wasting them excessively (Aras & Crowther, 2008). Similarly, organizational sustainability involves three distinct aspects: financial success, environmental conservation, and continuous societal support (Soto-Acosta et al., 2016). Moreover, corporate sustainability necessitates the implementation of economic, social, and environmental policies by business organizations to achieve sustainable stakeholder values. In conclusion, corporate sustainability is founded on the ideas and practices necessary to achieve long- and short-term economic objectives without compromising social and environmental concerns (Frempong et al., 2021). Ionescu (2021) applies the notion of sustainable finance to the environmental performance of businesses, the mitigation of climate change, and green innovation behavior.

According to Yilan et al. (2022), they may describe sustainable finance’s possible qualities using two components. The initial stage categorizes the numerous sustainability factors that managers could address. These factors may include the conservation of the natural environment, the maintenance of biological diversity, the defense against the negative consequences of climate change, the improvement of living conditions for the poor, and the provision of adequate food supply. The second component is to determine the role that each economic sector plays and the impact that its operations have on sustainability and improvement in the routine business activities that it engages in, or at the very least, to improve the significant sustainability features that it already possesses. At the absolute least, this will aid in recognizing the industries that require continued financing. These two elements permit the creation of a functional definition of sustainable finance. In this context, sustainable finance can be defined as the availability of funds for all activities in many sectors that contribute to achieving or improving sustainable finance’s characteristics. In other terms, sustainable finance relates to the availability of financial resources (Migliorelli, 2021).

Sustainable finance refers to the provision of financial resources to industries or activities crucial to achieving or enhancing sustainability’s economic, social, or environmental components (Migliorelli, 2021). In addition, when firms define their strategy, economic sustainability is the primary focus of their attention. An empirical study by Chen (2015) reveals that economic sustainability precedes environmental and social sustainability. To be successful, however, businesses must demonstrate their social and environmental responsibility (Caniëls et al., 2013). Therefore, sustainable finance is not centered on profit maximization; it requires value creation to serve the interests of all its stakeholders. Sustainable finance must accomplish this without jeopardizing the natural environment or societal obligations (Jyoti & Khanna, 2021).

Sustainable finance is the combination of three distinct dimensions, namely economic sustainability, social sustainability, and environmental sustainability, according to the discussion thus far (Schoenmaker & Schramade, 2018). Moreover, sustainable finance involves the financial infrastructure that incorporates sustainability practices into routine company activities to accomplish environmental and social integration without sacrificing economic objectives (Migliorelli, 2021). It is possible to assert that sustainable finance results in positive outcomes; consequently, the emphasis should be placed on challenging issues such as the provision of food security, higher quality housing, the availability of a healthy work environment, fair labor practices, and environmental protection (Camilleri, 2017)

Economic Sustainability

Regardless of its pivotal role, economic sustainability remains ambiguously defined. There is insufficient knowledge about which conditions are found as proper definition of economic sustainability (Qiu et al., 2019). Economic sustainability is defined by Chelan et al. (2018) as the generation of revenues for the different participants of society without destroying the capital and resources that in return stabilize the economy by generating circular effect. Economic sustainability refers long-term feasibility of economic processes, equity and equality of resource distribution, employment generation, revenue generation opportunities, and poverty alleviation (United Nations World Tourism Organization, UNWTO, 2004).

Economic sustainability of organization focuses on value creation and evaluate cost and income in the production and distribution of goods and services; thus, this dimension focuses financial and economic performance of the business (Braccini & Margherita, 2018).

Economic sustainability receives the most attention among the three pillars of sustainable finance, compared to environmental and social sustainability (Chen et al., 2015). Today’s businesses face economic challenges in the market and competition in the environmental and social spheres (Z. Wu & Pagell, 2011). Therefore, initiatives to maintain a better balance between the sustainability of the environment, society, and the economy are required.

The financial return is the primary motivator behind the adequate provision of funds, which generates value addition for businesses and society (Camilleri, 2020). The economic sustainability dimension of sustainable finance includes indicators such as sales, market share, revenues, operational efficiency, and progression (Jia et al., 2018). Moreover, tax payment is also an indicator with respect to economic sustainability (Baumgartner & Rauter, 2017). And economic dimension also consists upon earnings before interest and taxes (EBIT), net profit (Braccini & Margherita, 2018).

Social Sustainability

The notion of social sustainability is based on social analysis and evaluation, the encouragement of the acquisition of social opportunities, and the assurance of the mitigation of social issues and the reduction of social hazards (Social Development, 2013). According to McKenzie (2004), social sustainability is a strategy that assesses the social impact of company policies and practices, in addition to corporate organizations fulfilling their social commitments and attaining their social goals. According to Wagner (2007), business social sustainability strategies are intended to develop a better work environment to improve employee recruitment, retention, and satisfaction. They also control inter- and intra-business conflict; and improve the operations or objectives of various departments, internal and external stakeholders, shareholders, and management. It will automatically improve the company’s financial performance. Thus, social sustainability of sustainable finance refers to the enterprises approach towards reservation and development human and social capital of societies in which enterprise operate for value creation (Braccini & Margherita, 2018).

Consequently, social sustainability is the procedure that verifies the societal health and welfare of a company’s stakeholders (Tur-Porcar et al., 2018). Growing expectations of stakeholders from corporations to fulfill social obligations and achieve economic objectives are evident. Many investors and stakeholders demand that corporations fulfill their social and financial obligations. Stakeholders’ expectations have risen for firms to fulfill social responsibilities and achieve economic objectives (Matten & Moon, 2008).

Social issues may arise, for instance, poor working conditions are considered as the indicator of social sustainability (Baumgartner & Rauter, 2017). Moreover, the number of permanent employees is also included in social sustainability (Braccini & Margherita, 2018). Social sustainability dimensions are defined by Rajak and Vinodh (2015) in terms of a company’s citizenship, legal issues, donations, employee compensation, social safety, and health concerns. Indicators of social dimension incorporates aspects such as job satisfaction, work life balance, quality of life, solidarity, equity and fairness in the revenue distribution, and equal opportunities of training and development (Braccini & Margherita, 2018).

Environment Sustainability

Monitoring the impact of a firm’s operations on internal and external environments enables the company to continue offering environmentally friendly products and services to the local community (Adebambo et al., 2015). Environmental sustainability is a requirement of today, even though it may affect a company’s overall financial return. Corporations are now held accountable for the impact of their operations on the global environment. They must disclose these operations in their annual and sustainability reports (Aggarwal, 2013). Environmental dependability is a necessary environmental safeguard for preserving the environment and protecting the needs of future generations (Tur-Porcar et al., 2018). In addition, environmental sustainability refers to the efficient use of available resources and the environment’s ability to ensure the survival of humans (Norton, 2012). The environmental sustainability of sustainable finance emphasizes the compatibility among the trend of operations and renewable of these resources in nature. Moreover, the environmental dimension focuses on consumption of only those natural resources that can be regenerated from nature, and making emissions those can absorbed naturally in ecosystem (Braccini & Margherita, 2018).

The Global Reporting Initiative (GRI, 2011) defines the environmental dimension of sustainability as being conscious of the impact of an organization’s operations on living and nonliving natural systems. These natural systems consist of ecosystems, land, air, and water. It establishes GRI Environmental Performance Indicators, which include inputs such as material, energy, and water and outputs such as emissions, effluents, and waste, in addition to biodiversity and environmental protection. According to Vătămănescu et al. (2020), the current climate is characterized by a rapid rate of environmental change; therefore, managers must adopt business strategies to achieve an adequate level of performance in international companies.

The environmental effects on the natural environment are not related to socio-cultural or economic conditions, as it is based upon physical or chemical procedures (Baumgartner & Rauter, 2017). Environment dimension concentrates on energy consumption and usage of raw material during production process (Braccini & Margherita, 2018).

Although, the level of incorporation of these initiatives of sustainable finance and its three dimensions will ultimately plays a central role towards measurement of its indicators (Schumacher et al., 2020). But, current reviews remain limited because of disconnected insights presented by a subset rather than the complete corpus of sustainable finance (Kumar et al., 2022). To fulfill existing gap, this research aims to finalize the measurement of indicators of economic sustainability, social sustainability, environmental sustainability, and sustainable finance and develop the index by using Grey relational analysis (GRA) to evaluate the sustainable finance performance.

Theoretical Framework

Stakeholder theory is considered as the fundamental concept that explains the required improvement in corporations (Patrusheva et al., 2020). Firms with socially and environmentally responsible behaviors along with good economic practices would satisfy the interests of stakeholders, and thus, this would improve firm performance (Diab et al., 2019). This stakeholder theory found that more polluting corporations often select to sacrifice their environmental obligations to acquire their financial goals. Moreover, the larger the corporate size, the lesser the negative effect of environmental performance on economic performance (Hsu & Chen, 2023). Whereas the value-destruction theory and trade-off theory demonstrate that corporations involved in environmental and social responsibility mislay focus on financial performance and thus pursue satisfying stakeholders at the cost of shareholders.

Research Methodology

Research methodology consists upon two sections. Section “Sustainable Finance Indicators for the Development of Index” consists upon finalizing the indicators of economic sustainability, social sustainability, environment sustainability and sustainable finance for the development of index. Section “Sustainable Finance Index (SFA)” consists upon development of sustainable finance index by using Grey Relational Analysis (GRA).

Sustainable Finance Indicators for the Development of Index

To measure economic sustainability, social sustainability, environmental sustainability and sustainable finance, its performance should be evaluated by quantitative data so that comparisons can be done in an organized way. Indicators can be a reliable method to transform abbreviated and complex data into a simpler and measureable form. Assembling different indicators into single dimension according to underpinning model could simplify the calculation of multidimensional problems such as sustainable finance (Singh et al., 2009). Common trends can be found by using these Indices across various indicators (Nhemachena et al., 2018) and to compare the performance of several enterprises on composite grounds those cannot be measured directly (Becker et al., 2017). Thus, indices are the most appropriate tool to overwhelm complex issues regarding various aspects suggested by researchers (Cirstea et al., 2018).

A clearly defined underlying model is necessary for the construction of an index to formulate strategy for normalizing, weighting, and aggregating methods can be determined (Singh et al., 2009). Multi criteria decision making (MCDM) is most suitable methods to be used for complex and multidimensional sustainability (Bertoni, 2019). MCDM consists of different methods to deal with decision-making process in a multi criteria environment by evaluating a set of possible alternatives (Samira et al., 2019). MCDM methods help individuals in decision making processes that are based upon predetermined preferences. Grey relational analysis (GRA) introduced by Deng (1982) is one of the commonly used MCDM methods which is a quantitative analysis method based upon grey system theory (W. Wu, 2017). Thus, the current study uses Global Reporting Initiative (GRI) sustainability standard for assembling different indicators of economic sustainability, social sustainability, environment sustainability and sustainable finance in section “Sustainable Finance Indicators.” And after this Grey relational analysis (GRA) is applied to design an index of economic sustainability, social sustainability, environment sustainability and sustainable finance in section “Sustainable Finance Index (SFA).”

Sustainable Finance Indicators

A composite index is developed by collecting a whole set of variables; for this reason, the (Global Reporting Initiative) GRI sustainability standard makes use of the most accepted sustainability practices and an internationally recognized sustainability standard (Rashed et al., 2022). The researcher can break down the concept of sustainable finance into three categories, each of which can have a positive or negative impact on the long-term viability of an organization (Table 1). The entire economic value created and distributed by the companies is used to determine economic sustainability. In addition, the growth of banks is evaluated based on the total number of branch locations and automated teller machines (ATMs) (Stauropoulou & Sardianou, 2019).

Economic Sustainability Indicators.

The social dimension (Table 2) of sustainable finance is related to overall society’s well-being by directly spending as donations or indirectly by generating employment (Stauropoulou & Sardianou, 2019).

Social Sustainability Indicator.

Table 3 displays the environmental sustainability dimension, comprised of those indicators that can either directly or indirectly influence the natural environment. Some examples of such indicators include the consumption of copious amounts of fuel, stationery, and printers, which can have a detrimental effect on the natural environment (Stauropoulou & Sardianou, 2019).

Environmental Sustainability Indicator.

Sustainable Finance Index (SFA)

In the current study, the Grey Relational Analysis method is applied to calculate the sustainable financial performance of the banking sector of Pakistan.

Grey Relational Analysis (GRA)

GRA is a method used to examine and assess the relationship between the components of a matrix based on the variation of similarities or the variation of development trends among the matrix elements (Feng & Wang, 2000). It has been demonstrated that the grey system theory is appropriate for a technique when the information presented is inappropriate, partial, poor, or uncertain. Therefore, in making decisions, the term “grey” refers to a lack of information or an insufficient collection of information, an unknown link between variables, or an impact of variables on the entire system that is not defined (Doğan, 2013).

GRA includes the following steps.

The first step of GRA is to make the primary decision matrix zi(j), where i represent the n variables and j represents the m criteria.

Where i = 1, 2, 3, …, n and j = 1, 2, 3, …, m

In the initial decision matrix, the unit of measurement for each criterion is different, so in the normalization process, the values of the data set are adjusted as free of the unit. For this purpose, two transformation formula is used.

(1) For maximum is better transformation is

For minimum is better transformation

After the normalization process, all the values have been transformed into the maximum is the better type, with all the values ranging between 0 and 1.

With the help of normalized values calculated in step 2, the normalized matrix is constructed.

Where i = 1, 2, 3, …, n and j = 1, 2, 3, …, m

Δ0i(j) are the values that show the difference between normalized values with their respective reference value, and their difference matrix is represented below.

Co-efficient of Grey relational (

Where (

According to Hsiao et al. (2017), if all the variables in the decision matrix have equal importance, then the formula for the grey relational grade is as follows.

Sample Selection

For more than a decade, the banking sector in the country has been rapidly expanding (Khan et al., 2022). The current study’s sample comprises 21 banks from the country’s banking industry, including both public and private sector banks. Their performance is evaluated using economic, social, environmental, and sustainable financing variables from 2010 to 2021 (12 years). Data is gathered from bank financial statements retrieved from the banks’ websites. Firstly, data is collected from financial statements of the different indicators. Then GRA approach, as described above, is used from steps 1 to 6. Compare interbank economic sustainability, social sustainability, environmental sustainability, and overall sustainable financial performance by ranking the banks in different years. Furthermore, each year, the data for different banks are ranked and compared based on intra-bank economic sustainability, social sustainability, environmental sustainability, and overall sustainable financial performance.

Results and Discussions

In this section, data from 21 banks is studied, which can provide the economic sustainability, social sustainability, environment sustainability and sustainable finance of 21 banks by allocating equal weight to each dimension.

Economic Sustainability

Table 4 presents the economic sustainability scores of various banks over a span of 12 years, from 2010 to 2021. The economic sustainability of ABL bank commenced in 2010 with a value of 0.633. This score faced a decline until 2017. However, from 2018 onward, an upward trend was observed. A similar trend in economic sustainability across different years can be discerned by the other banks listed. An overarching observation is that there was a noticeable dip in economic sustainability scores across most banks in the earlier part of the decade. Nevertheless, post-2018, most of the banks exhibited an uptrend in their scores, indicating a positive shift in their economic sustainability. When delving into specifics, it’s interesting to note varying patterns. For instance, while the ABL bank shows a clear declining pattern until 2017 followed by a subsequent rise, others like JS Bank witnessed a peak in 2016 and then a decline. Some banks like Summit Bank even exhibited their highest sustainability scores in 2019. Overall, this data provides a comprehensive overview of the economic sustainability journey of these banks, highlighting periods of challenges and growth. Overall, it can be evaluated that in the first few years there was a declining trend in economic sustainability but, after 2018 almost every bank shows an increasing trend in the data of every bank.

Economic Sustainability from the Year 2010 to 2021.

Note. UBL = United Bank Limited; HBL = Habib Limited; ABL = Allied Bank Limited; MCB = Muslim Commercial Bank; BOP = Bank of Punjab; NBP = National Bank of Pakistan.

Social Sustainability

Table 5 provides a comprehensive summary of the social sustainability ratings attributed to 21 prominent commercial banks in Pakistan, covering the period from 2010 to 2021. The fluctuations in performance observed across different years for each bank suggest that their commitment to social sustainability was not consistently maintained, as their performances displayed annual variations. Despite this incongruity, it is worth noting that there has been a prevailing upward trend in the social sustainability ratings of most banks from 2019 to 2021. This phenomenon underscores the possibility of a renewed emphasis or heightened attention on societal responsibilities and initiatives by these organizations within the contemporary landscape.

Social Sustainability from the Year 2010 to 2021.

Upon closer scrutiny of the individual performances, it becomes apparent that banks, such as NBP, which initiated the decade with robust social sustainability metrics, have witnessed a gradual deterioration over time, culminating in a notably diminished score by the year 2021. However, it is noteworthy that numerous organizations, including Khyber Bank, have experienced a substantial metamorphosis. Commencing the decade with markedly low scores, the subject under scrutiny has exhibited a discernible upward trajectory, culminating in the attainment of an exceptionally high score by the year 2021. The captivating plot of the text is enhanced by the juxtaposition of these tendencies within the greater narrative. The banking industry, traditionally driven by a strong emphasis on profit growth, seems to be undergoing a notable transformation in its fundamental approach. The transformation mentioned above, as illustrated in Table 5, showcases a propensity to recognize and actively incorporate social factors into their corporate strategies. The concluding statements of the table serve to reinforce the perspective that banks are increasingly recognizing their societal responsibilities and are gradually integrating these commitments into their overarching goal of profit maximization. The incorporation of commercial interests and societal welfare in a comprehensive manner serves as a prime example of a changing perspective regarding the participation of commercial banks within the broader framework of societal advancement and well-being.

Environmental Sustainability

Table 6 presents the empirical findings pertaining to the environmental sustainability of various banks within the financial industry. The data encompasses the period spanning from 2010 to 2021. Upon closer analysis of the prevailing circumstances, a disquieting trend emerges, revealing a consistent decline in the environmental sustainability ratings across a wide array of financial institutions. The decline in performance raises immediate concerns for banking institutions, serving as a microcosm of the situation in a developing nation. These institutions are confronted with the imperative to redirect their attention towards embracing operational procedures that are characterized by enhanced environmental sustainability. Strategies, such as the adoption of renewable energy sources, as demonstrated by solar systems, and the curtailment of non-renewable resource consumption, particularly fossil fuels, hold promise in mitigating the adverse trajectory. Reducing the usage of printers and stationery holds the promise of enhancing their ecological footprint.

Environmental Sustainability from the Year 2010 to 2021.

One noteworthy observation extracted from the table is the occurrence of negative values for MCB during certain years, indicating the possibility of anomalies or discrepancies in data reporting or calculation. A comprehensive investigation of these incidents is essential, as they possess the capacity to introduce biases that could potentially influence the overall analysis and comparisons derived from the presented table. The observed decline in environmental sustainability, as identified within the context of the study on the development of a Sustainable Finance Index, is a matter of significant concern. This observation indicates a potential insufficiency in the banks’ commitment to corporate social responsibility in relation to the preservation of the environment. The abstract highlights the contemporary focus of the corporate sector on societal development and environmental conservation. This underscores the significance of aligning banks with these ideals, as evidenced by their decreasing inclination. Moreover, the incorporation of Grey Relational Analysis (GRA) in this investigation guarantees the impartial evaluation of economic, social, and environmental sustainability aspects. As a result, the potential impact of a decline in a particular aspect, such as the environmental component, on a bank’s overall sustainable financing score should not be underestimated. In summary, the findings presented in Table 6 provide a compelling rationale for banks to promptly act, emphasizing the importance of prioritizing environmental sustainability in their operational strategies. Through active participation in these actions, individuals can fulfill their societal responsibilities while also positioning themselves strategically within a comprehensive and robust sustainable financial framework, as substantiated by the findings of this study.

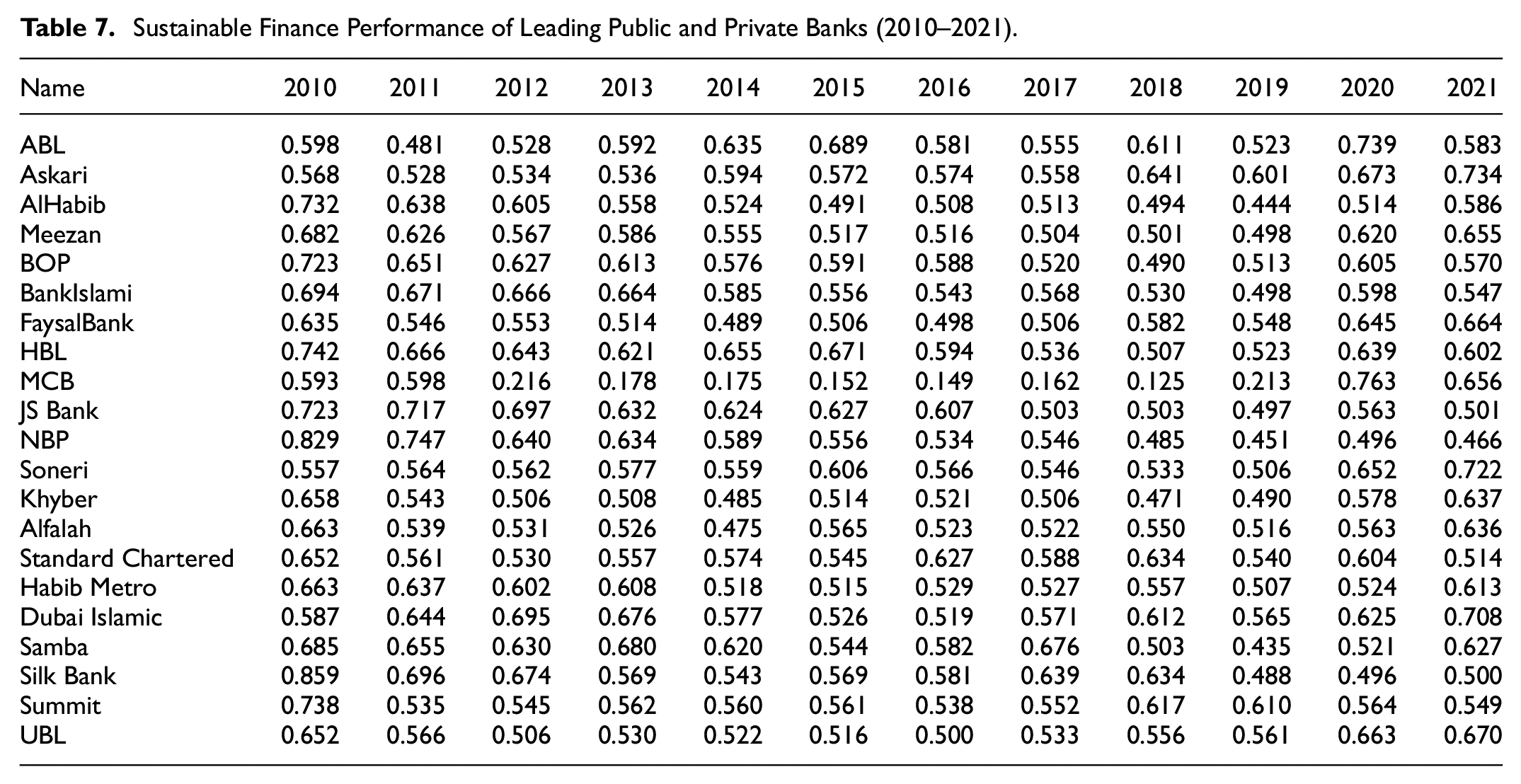

Sustainable Finance

Table 7 showcases a comprehensive examination of the sustainable financing performance exhibited by 21 prominent public and commercial banks throughout an extensive 11-year timeframe, spanning from 2010 to 2021. This essay emphasizes the importance of sustainable finance in the corporate realm, especially in response to the growing emphasis on societal advancement and environmental conservation, alongside the traditional goal of maximizing profits. In this study, we employ the Grey Relational Analysis (GRA) methodology to construct a comprehensive financial index that encompasses three fundamental dimensions, namely economic, social, and environmental sustainability. The Global Sustainability Assessment (GRA) offers a comprehensive evaluation of a bank’s sustainability performance, ensuring equitable consideration of all relevant factors.

Sustainable Finance Performance of Leading Public and Private Banks (2010–2021).

Upon careful examination of Table 7, it becomes apparent that a discernible mixed trend in sustainable finance performance is observed across different institutions. In this illustrative case, the performance score of ABL commenced at 0.598 in the year 2010. However, it experienced a decline in the subsequent year. Notably, in the year 2020, ABL demonstrated a significant recovery, with its performance score reaching 0.739. However, it is noteworthy that several banks, including MCB, experienced a notable decline in their rankings during the mid-2010s. However, by the year 2020, these banks demonstrated a commendable ability to recuperate and enhance their overall performance. The observed range of performance indicates that select banks have exhibited a consistent dedication towards incorporating sustainable objectives into their financial operations, whereas others have encountered challenges in this endeavor. In recent years, a discernible inclination has emerged within the banking industry, wherein there is a notable shift towards a heightened focus on sustainable financing. The insights mentioned above hold great potential in offering substantial benefits to stakeholders, academics, and policymakers in their pursuit of advancing sustainable finance objectives and attaining a comprehensive comprehension of the most efficacious strategies and potential challenges within the industry. The efficacy of the GRA-based index in offering a comprehensive evaluation of sustainable finance performance across different banks and time periods is underscored by the findings presented in Table 7. As a result, this enables the establishment of a more robust and exact framework for conducting sustainable financial research.

Intra-Bank Performance Evaluation

Table 8 zeroes in on the intra-bank performance evaluation from 2010 to 2021, providing a comprehensive breakdown of the 21 largest commercial banks in terms of their performance across the three sustainability dimensions. The table also highlights each bank’s peak and trough years for economic, social, environmental sustainability, and their combined sustainable finance performance. For instance, ABL bank recorded its highest economic sustainability in 2020 while marking its lowest in 2017. This pattern of highs and lows over the years is evident for each bank across all three dimensions. Such data is instrumental in capturing the progress, or lack thereof, in various areas of sustainability within individual banks. Several trends can be discerned from Table 8. Economic sustainability among banks has been on an upward trajectory, hinting at the growing financial robustness of these institutions. On the other hand, the consistent decline in environmental sustainability underscores the pressing need for these institutions to bolster their environmental conservation efforts. The variable performance in social sustainability further underscores its dynamic nature, affected by numerous socio-economic factors over the years. Given that each dimension is weighed equally in the index, the general improvement in overall sustainability performance is commendable. Nonetheless, the pronounced decline in environmental performance is a clear signal for regulatory authorities to step in and intensify their focus on environmental conservation within the banking sector.

Peak and Trough Years of Economic, Social, and Environmental Sustainability Performance for Major Banks (2010–2021).

Interbank Performance Evaluation

Table 9 compares the interbank economic, social, and environmental sustainability performance and combined sustainable financial performance of 21 banks in the country’s banking sector from 2010 to 2021. In the table above, the financial institution with the best overall performance in terms of economic sustainability, social performance indicator, environmental sustainability indicator, and overall sustainable finance performance is highlighted annually. Regarding economic sustainability, the MCB Bank had the worst performance for the period, while the Silk Bank had the highest performance in 2010. NBP displayed the highest level of social responsibility throughout 2010, while Dubai Islamic demonstrated the lowest level. Meezan Bank had the best performance in terms of environmental sustainability during the same period in 2010, while Standard Chartered Bank had the worst performance. Currently, Silk bank has the best performance in terms of sustainable financial ratings, whereas Soneri bank has the worst performance in these rankings. According to the preceding table, the bank with the most significant financial volume has average performance on each of the four parameters. It is owing to the bank’s size to create policies and implement them across all its branches. Although the bank is somewhat small, it has a lot of control over all its branches, allowing it to quickly design and implement policies across its limited branch network. In the interim, if the required attention is not provided, the performance of this small network branch network will be at its absolute worst in terms of its economic sustainability performance, social sustainability performance, environmental sustainability performance, and combined sustainable financial performance.

Interbank Performance Evaluation from the Year 2010 to 2020.

The lack of a universally agreed-upon definition for sustainable finance, as emphasized by Dimmelmeier (2021), becomes evident when examining the fluctuating performance metrics displayed by banks throughout different periods. The dynamic nature of comprehending and implementing sustainable finance practices within the banking sector is highlighted by this variability (Forstater & Zhang, 2016). In the study conducted by Chelan et al. (2018), the concept of economic sustainability is defined as the capacity to generate revenue while simultaneously avoiding the depletion of valuable resources. However, it appears that the adherence to this concept is not consistently observed by prominent banks, including HBL, MCB, BOP, and UBL. The observed fluctuation suggests that banks, driven by their focus on short-term profitability, may be disregarding the conservation of long-term resources, which is consistent with the conclusions drawn by Braccini and Margherita (2018) as well as Qiu et al. (2019). In the realm of social sustainability, the existing data offers a multifaceted depiction. McKenzie (2004) and Wagner (2007) underscore the profound societal implications stemming from a company’s actions. In line with the perspectives presented by Tur-Porcar et al. (2018) and Matten and Moon (2008), banks such as Meezan and FaysalBank are increasingly committing themselves to the advancement of societal well-being. In contrast, the declining scores of NBP indicate challenges in the continuity of social sustainability initiatives. Although the current body of literature does not explicitly delve into the topic of environmental sustainability, it is crucial to acknowledge the considerable emphasis placed on the responsible utilization of resources (Adebambo et al., 2015; Norton, 2012). Hence, it is crucial to undertake a thorough examination of the environmental indicators pertaining to financial institutions. In accordance with the perspectives presented by Jyoti and Khanna (2021) and Schoenmaker and Schramade (2018), the notion of sustainable finance necessitates a holistic and fair approach that incorporates economic, social, and environmental dimensions. The data derived from the banking sector reveals that despite some progress in the domains of economy and society, the widespread adoption of sustainable finance within the industry continues to be a distant goal. Considering Kumar et al.’s (2022) findings, it is evident that the successful resolution of these disparities and the advancement of a comprehensive sustainable finance framework will heavily rely on the integration of ongoing research.

Conclusion and Recommendation

In this study, we developed the sustainable financial performance of the country’s banking sector based on three dimensions: economically sustainable finance, socially sustainable finance, and environmentally sustainable finance. According to the facts reported in the preceding section, it is abundantly clear that banks focus primarily on their operations’ economic and social sustainability. In contrast, the environmental sustainability of their activities receives only a little attention. Problems with sustainability are challenging for ecosystems as well as for humans. Moreover, they have an impact on human behavior as well as human interactions. In this context, the problem should be addressed by regulators, who should seek acceptable and practicable remedies. Therefore, there is a significant need for financial regulators and financial organizations to incorporate economic, social, and environmental factors into their strategies. We will need investment capital from the public and private sectors and funds from domestic and international sources to achieve this objective. Therefore, investing in a sustainable system needs the creation of innovative strategies for the mobilization of long-term funding across all industries. If environmental and social obligations are incorporated into product development decisions and financing options, this is viewed as a first step toward making the financial system play its crucial role in transforming the regional economy into a more sustainable one. Moreover, financing efficient energy projects, renewable energy resources, and sustainable projects necessitates developing new financial instruments suitable for the current situation. For an organized framework, it is vital to have a sustainable banking network, sustainable tools, and suitable regulatory frameworks.

Theoretical and Empirical Implications

The current study acquires an important place in the theoretical domain as it has significant contribution about social sustainability and environmental sustainability in the existing literature. This study practically evaluates sustainable finance and its three dimensions, like economic sustainability, social sustainability, and environmental sustainability and the responsibilities of enterprises towards employees, environment, and society. Moreover, the findings of the present study have importance for businesses as it provides guidelines and motivation on how to acquire economic sustainability, social sustainability, and environmental sustainability to improve their business performance. It is feasible that future studies will incorporate these markers into their investigations. The evaluation of the sustainability performance of every financial institution enables regulatory bodies and financial institutions to play a significant role in the preservation of the natural environment, the continued existence of humans, and the availability of natural resources for future generations. In addition, financial institutions can set rules for environmentally responsible financing and restrict loan alternatives for businesses to those that engage in environmentally responsible business practices by evaluating the sustainable financial performance of the borrower using this index.

Government must establish comprehensive policies and promote social and environmental performance of companies by reward and punishment mechanism. For instance, green credit concession and tax rebates should be given to the enterprises according to social and environmental performance of enterprises and while less credit for companies with poor performance. Furthermore, the government can motivate the enterprises by financially compensating them for the short-term losses for adopting the social and environmental transformation. Furthermore, the enterprises must disclose their information regarding social and environmental performance so that they can get low cost financing benefits by revealing their good social and environmental performance.

The present study has different limitations as these can weaken the efficiency of the study. Due to the country’s developing economy, there is a need for more information available in its financial accounts. This is true regarding information about environmental indicators such as carbon emission, waste material recycling, water usage, and energy consumption. Moreover, employee turnover rate, electricity consumption, employee education, employee training hours per year, total paper consumption data, and many other factors directly have impact upon economic, social, and social sustainability.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The research data supporting the findings of this study are available from the corresponding author, Dr. Muhammad Irfan, upon reasonable request. Please contact Dr. Muhammad Irfan at