Abstract

The “campus loans” crisis has highlighted the importance of financial literacy among Chinese college students. Based on an analysis of 2,266 valid questionnaires, this study utilized survey data and logistic regression to examine the correlations between demographic and behavioral factors and financial literacy among students. The results indicated that, compared to their international counterparts, Chinese students generally possess less financial knowledge. However, they exhibit stronger financial attitudes and behaviors. A significant gender disparity was observed, with female students outperforming male students in financial literacy. Students attending more prestigious universities, particularly those majoring in economics, management, science, and engineering, and those dedicating more time to financial education, showed higher levels of financial literacy. Additionally, positive social interactions were associated with enhanced financial literacy. The study also identifies a “Surrounding People Effect,” where the presence of financially knowledgeable peers, friends, and family correlates with improved financial literacy among college students. These findings offer critical insights for developing targeted policies to enhance financial literacy among Chinese college students.

Plain language summary

This study investigates how well Chinese college students understand and manage money, known as financial literacy. The research involved analyzing answers from 2,266 students to see what affects their financial knowledge, attitudes, and behaviors. The findings reveal that Chinese students generally know less about finances than students from other countries but have a stronger mindset toward handling money effectively. Notably, female students showed better financial understanding than male students. Students from top universities and those studying economics, management, science, and engineering also showed better financial skills. Moreover, more time learning about finances and having financially knowledgeable friends and family were linked to better financial skills. These insights are crucial for creating specific educational programs to improve money management skills among students in China.

Keywords

Introduction

Financial literacy (FL) encompasses the capability to acquire, comprehend, and utilize financial knowledge effectively and a positive attitude toward making prudent financial decisions that enhance one’s financial well-being (OECD, 2011). Given the increasing complexities of modern financial markets and the rising costs associated with longer life expectancies, a deep understanding of sophisticated financial instruments is essential for securing a stable financial future (Agarwalla et al., 2015; Lusardi & Mitchell, 2014).

Despite its critical importance, as highlighted by the OECD (2017), FL remains a widespread challenge across global financial markets, indicating a substantial need for improvement in this area (Lusardi & Mitchell, 2011). On a broader scale, FL plays a pivotal role in enabling individuals to manage everyday financial tasks, thus reducing the likelihood of economic downturns (Sohn et al., 2012; van Ooijen & van Rooij, 2016). On a more personal level, inadequate FL often results in poor financial choices, such as insufficient savings, unwise investments, and excessive borrowing, which can significantly undermine individual well-being (Mitchell, 2010; Reed & Cochrane, 2012).

Mobile banking platforms have transformed access to financial markets, especially for college students, facilitating their participation in financial activities. However, this demographic often displays limited financial knowledge, biased perceptions, weak risk awareness, and poor planning skills, which can lead to significant personal financial issues, as evidenced by the distressing outcomes of the “campus loans” crisis in 2016 (Liu & Zhang, 2021). These loans, known for their low entry barriers and high risks, have resulted in severe repercussions, including student suicides, highlighting the critical need for enhanced financial literacy among students.

While there is extensive literature on the financial literacy of various groups, including consumers, households, high school students, and adults, and its impact on their financial behaviors (Cole et al., 2011; Lusardi & Mitchell, 2017; Mouna & Anis, 2017; OECD, 2017; Rodrigues et al., 2019; Sohn et al., 2012), the specific financial literacy challenges facing Chinese college students have not been thoroughly examined (Wang & He, 2020). This study seeks to fill this gap by empirically analyzing FL among Chinese college students, assessing the relationship between demographic and behavioral factors with FL, and comparing these findings with international data. Considering China’s substantial student population and high higher education enrollment rate, gaining insights into this demographic’s FL is vital for shaping the nation’s future economic landscape and carries significant global implications. The findings from this study are intended to inform and guide policy strategies aimed at improving FL among college students.

This paper is structured as follows: Section 2 reviews relevant literature, develops hypotheses and outlines the research framework. Section 3 details the methodology employed. Section 4 evaluates the current levels of FL among college students, draws comparisons with OECD data, discusses findings from regression models, and performs robustness checks. Section 5 interprets logistic regression results, concludes the study, and discusses its limitations.

Literature Review, Hypothesis Development, and Research Framework

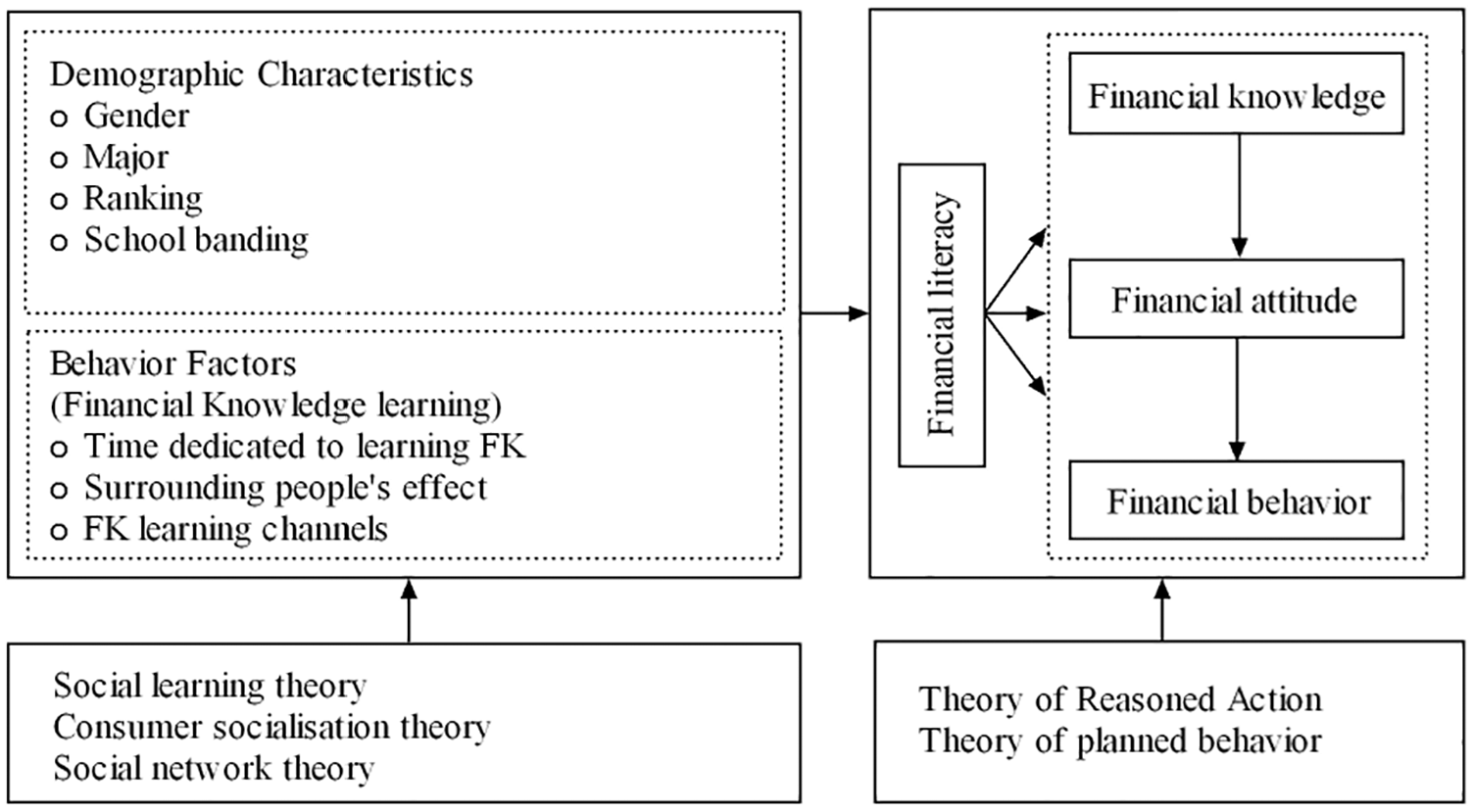

The literature highlights a variety of demographic factors associated with differences in financial literacy (FL), including gender, academic major, performance, and school banding (Ergün, 2018; Sohn et al., 2012). Ergün (2018) observed substantial disparities in FL among university students throughout Europe, reflecting the impact of varied educational systems and cultural contexts. Additionally, it is evident from the research that the channels through which financial knowledge (FK) is acquired, the financial behaviors of influential individuals, and the time dedicated to learning FK significantly affect students’ financial literacy.

Definitions of Financial Literacy

Financial literacy has been defined in various ways across studies, with each definition emphasizing the practical elements that are crucial for making informed financial decisions. Schagen et al. (1996) conducted a systematic survey in Britain focusing on young people and adults, highlighting financial planning, problem-solving, and decision-making as central elements of FL. Similarly, the Organization for Economic Cooperation and Development, International Network on Financial Education (OECD, 2011), defined FL as the combination of awareness, knowledge, skills, attitude, and behaviors necessary for making informed financial decisions, a definition consistently used in later reports (OECD, 2015, 2018).

Correlations Between Demographic and Behavioral Factors and Financial Literacy

Gender Disparities in FL

Notably, gender-related differences in FL have been extensively explored, with inconsistent findings. While some studies report lower financial knowledge among females (Agnew & Harrison, 2015; Karakurum-Ozdemir et al., 2019; Koh et al., 2020; Lusardi & Mitchell, 2011), others find no significant gender gap (Bucher-Koenen et al., 2017; Klapper & Panos, 2011; OECD, 2020b). These disparities often vary by age group and are associated with cultural and regional contexts.

Major and FL

The social learning theory (Bandura & Walters, 1977) and the consumer socialization theory (Moschis & Churchill, 1978) indicate that major categories significantly affect knowledge acquisition. Individuals majoring in finance or management should possess higher FL and have more access to FK from school (Ergün, 2018).

Academic Performance and Fl

The role of academic performance in FL has also been substantiated, with positive associations between students’ grades ranking and their financial literacy, suggesting that skills in areas like mathematics and foreign languages may enhance FL (Al-Bahrani et al., 2020; Bucher-Koenen and Lusardi, 2011; Erner et al., 2016).

School Banding and FL

Ho and Lee (2020) detected school banding influence on student FL acquisition in an FL curriculum and found students’ professional capital distinguished from school banding. Moreover, Lee and Chiu’s (2017) research indicated that how teachers teach and how students learn differs significantly with the specific banding of the school.

Different FK learning channels, surrounding people’s financial behavior, and the time dedicated to learning FL relate to student financial literacy. Social interactions within close-knit social groups significantly correlate with FL acquisition, as social network theory suggests. Key influencers like family members and peers are pivotal in enhancing FL through social learning mechanisms (Borgatti & Ofem, 2010; Haliassos et al., 2019; Li & Meyer-Cirkel, 2021; Moreno-Herrero et al., 2018; Zhu, 2019). Additionally, the channels through which students acquire financial knowledge—ranging from formal education to social media—play crucial roles. Significant relationships have been observed between media exposure and FL education attendance, both associated with variations in FL levels among students (Ergün, 2018; Tan et al., 2022).

From this comprehensive literature review, we propose the following hypotheses, illustrated in Figure 1.

The research framework.

This research not only aims to assess and compare the FL of Chinese college students with their peers internationally but also seeks to elucidate the factors associated with their financial literacy. By proposing enhancements based on these associations, this study aims to significantly contribute to the field of financial education.

Methodology

Sample

The sample for this study was collected during the preliminary rounds of a Financial Literacy (FL) competition held in Southwest China in 2020. The stratified sampling method was utilized to ensure a diverse participant profile, with a specific focus on inclusivity. The competition, organized by the Sichuan Provincial Education Bureau (SPEB) in collaboration with Sichuan University (SCU), targeted full-time college students across Sichuan Province at both undergraduate and graduate levels. The sampling strategy required participants to form teams of three to five members, with a restriction of no more than two members from economics and management majors per team, to encourage a mix of academic disciplines.

As authorized by SPEB, SCU promoted the competition extensively throughout the region using online (official websites, Class QQ, WeChat groups) and offline (face-to-face meetings) methods to ensure broad participation. This robust recruitment strategy aimed to gather a broad spectrum of students, contributing to a varied and comprehensive sample for the study. Eligible participants included all students who participated in the competition and completed the FL questionnaire. From November 1st to 5th, 2020, 2,280 students participated in the survey, of which 2,266 responses were valid after excluding 13 incomplete entries, yielding a high response rate of 99.4%.

Sample Rationality

The rationale for participant selection was to ensure representativeness and diversity, thus enhancing the study’s reliability and relevance. The sample’s demographic distribution closely mirrored national urban and ethnic demographics as reported in China’s seventh census in 2020. Approximately 54.6% of the respondents came from urban areas, closely approximating the national urban population of 63.9%. The ethnic composition was also representative, with 93.3% of respondents identifying as Han, compared to a national figure of 91.1%.

Moreover, the sample comprised students from various higher education institutions across Sichuan, home to various prestigious universities and colleges, including those designated as 985 and 211, and other local colleges. This diversity ensured that the sample reflected a broad cross-section of China’s student population, making it a microcosm of the country’s academic youth.

The comprehensive sampling approach and the broad engagement in the FL competition provided a strong foundation for understanding the financial literacy levels among college students in China. The detailed demographic and educational backgrounds of participants enhanced the depth and applicability of the research findings.

Descriptive Analysis

Table 1 presents detailed characteristics of the sample. Most respondents (93.3%) were of Han nationality, with a small minority (6.7%) from other ethnicities. Over half of the respondents (54.6%) were from urban areas, and a significant majority were female (74.6%). The majority of the participants (64.7%) attended ordinary universities. Regarding financial knowledge learning, 41.9% of the students spent <1 hour per week on this activity. Most sought financial knowledge from educational sources (51.6%) or media (58.9%), with about 30–50% reporting recent awareness of financial product purchases by peers or family.

Sample Characteristics.

The Han ethnicity, comprising 91.11% of China’s population, is the majority according to the 2020 census. The remaining 8.89% are minorities.

Established in 1958, the Hukou system regulates migration within China and is linked to social benefits like property and vehicle ownership in major cities.

In the realm of higher education, “985” and “211” universities are regarded as China’s elite institutions, with 39 “985” and 116 “211” universities, the latter encompassing all “985” universities. University rankings typically consider “985” institutions superior, followed by “211” and then ordinary universities.

Andreou and Philip (2018) research reveals a striking contrast in the participants’ financial literacy. Approximately 64% of the respondents demonstrated proficiency in financial awareness and behavior, a promising figure. However, <40% showed strong financial knowledge proficiency, indicating a potential area for improvement. These lower FK scores, however, were balanced by higher scores in financial awareness and behavior, reflecting an overall good financial literacy level among the participants.

Measurement Instruments

The survey instrument was divided into three sections: demographic information, behavioral factors, and Financial Literacy (FL) assessment (see Appendix). It underwent rigorous testing for clarity and feasibility with a randomly sampled group of 168 individuals who participated without compensation. The internal consistency of the instrument was confirmed through Cronbach’s alpha, yielding values of .637 for Financial Knowledge (FK), .639 for Financial Behavior (FB), and .669 for Financial Attitude (FA). Although these values are slightly below the ideal threshold of 0.7, they are still considered acceptable for exploratory research. Notably, the reliability of the FB section was enhanced to a Cronbach’s alpha of .802. This was achieved by refining Likert-scale questions, a process that involved careful review and adjustment of the wording and structure of the questions, which solidified the instrument’s overall reliability.

Analysis Method

The analysis employed logistic regression to explore the impact of demographic factors on the Financial Literacy (FL) of college students in China. This approach utilized a binary model to assess whether socio-demographic attributes influenced FL proficiency levels, focusing on respondents who correctly answered at least 67% of the questions, as guided by standards from Andreou and Philip (2018) and the OECD (2020a). Odds ratios were calculated to quantify the direction and magnitude of impacts on FL, where values above 1 indicated a positive effect and those below 1 indicated a negative effect. Additionally, the study implemented Cohen’s d to quantify the effect size, offering insights into the practical implications of the results while adhering to Cohen’s (2013) benchmarks for interpreting these sizes, as further detailed in Fernandes et al. (2014).

Results

Assessing FL of Chinese College Students Relative to OECD Standards

This section evaluates the financial literacy (FL) levels of Chinese college students in relation to their counterparts in 17 other countries, drawing on data from Tables 2 and 3, insights from our survey, and the OECD (2020a) dataset. The focus is on the 18 to 29 age group to maintain consistency in educational and experiential backgrounds across the sample.

Comparison Between China and Other Countries on Financial Literacy and Its Three Components.

The analysis is based on survey data and OECD (2020a) data. To ensure comparability, we only include individuals aged 18 to 29 in the OECD INFE surveys into comparison, reflecting a more homogenous group regarding education and experience.

Based on OECD (2020a) criteria, respondents achieving a high score meet the following thresholds: 5 or more for FK, 6 or more for FB, and >3 for FA. High FK, FA, and FB levels refer to the proportion of individuals who attained high scores in each financial literacy component.

High FK excludes Malta (Malta asked only four knowledge questions).

The actual average was inflated by multiplying it by 22/21 to match the maximum FL score of the OECD survey.

Comparison Between China and Other Countries on Each Financial Literacy Questions.

Note. The analysis is based on survey data and OECD (2020a) data. To ensure comparability, we only include individuals aged 18 to 29 in the OECD INFE surveys into comparison, reflecting a more homogenous group regarding education and experience.

The question we actually used as “Choosing financial products” referring to OECD (2015) tookit.

Overall Financial Literacy Scores

Chinese college students achieve an average FL score of 13.1, which is 12.1% above the average of the 17 countries surveyed but still below the OECD’s benchmark of 14. This suggests that while Chinese students generally exhibit solid financial understanding, there remains room for improvement in more complex financial areas. This gap highlights the need for targeted educational enhancements to deepen understanding of advanced financial concepts.

Financial Knowledge

With an average FK score of 3.7, Chinese students are slightly behind the 17-country average from the OECD 2020 study. However, only 33% of Chinese respondents demonstrated a high level of FK, as opposed to 42% in the comparative group. This presents a clear opportunity for improvement, particularly in key areas like interest calculations and risk diversification. By focusing on these areas, we can significantly enhance their overall financial literacy.

Financial Behavior

Chinese students exhibit strong real-world financial behaviors with an FB score of 5.8, outperforming the 17-country average of 4.9. Although this score is commendable, it also points to potential areas for enhancement, particularly in selecting financial products more judiciously than their international peers.

Financial Attitudes

The FA score among Chinese students is 3.0, aligning well with the 17-country average of 2.7. While their financial attitudes are generally positive, there remains potential for further development, especially when benchmarked against countries like Indonesia. Enhancing foundational understanding could significantly boost practical money management skills.

Comparison to OECD Target

While the overall FL score of Chinese students surpasses the average of the surveyed countries, it falls slightly short of the OECD’s target score of 14. This discrepancy underscores the importance of not only meeting but surpassing international standards in financial literacy. By doing so, we can ensure that our students are well-prepared to navigate the complexities of the global economic landscape.

These findings affirm the commendable FL levels among Chinese college students and emphasize the urgency of enhancing their grasp of complex financial concepts. This research underscores the importance of advancing financial education, addressing educational gaps, and leveraging financial-solid behaviors to effectively navigate the complexities of a dynamic economic landscape.

Correlation of Demographic and Behavioral Factors With Financial Literacy

Association of Demographic Characteristics With Financial Literacy (Hypothesis 1)

The logistic regression analysis indicates a significant association between demographic characteristics and financial literacy (FL) levels among Chinese college students (Table 4). Female students displayed a higher level of FL than their male counterparts, aligning with similar findings across several OECD INFE countries such as Bulgaria, Georgia, Poland, Indonesia, and the Czech Republic. Students majoring in economics and management, which typically emphasize financial knowledge, demonstrate higher financial literacy. Similarly, students from science and engineering backgrounds, who are generally more cautious in financial matters, show elevated levels of financial literacy. Compared to the students they were ranked in the top 10%, those ranked in the top 21–50%, and those ranked last (51–100%) exhibited lower FL. Most studies have found that student learning abilities are positively associated with the student’s FL. Furthermore, students attending prestigious universities exhibited enhanced FL, likely due to superior educational resources and a stimulating learning environment. These results substantiate

Correlation of Demographic and Behavioral Factors with Financial Literacy.

Association of Behavioral Factors With Financial Literacy (Hypothesis 2)

Behavioral factors, notably the time allocated to learning financial knowledge (FK), are strongly associated with variations in financial literacy (FL). Students who spend over 2 hours daily studying FK tend to show higher levels of FL. This observation underscores a significant association between the extent of dedicated study time and enhanced financial understanding. Moreover, the financial behaviors of peers and family members correlate positively with students’ FL, suggesting that interactions with financially literate individuals are linked with better financial literacy outcomes. These findings support

Role of Financial Knowledge Learning Channels (Hypothesis 3)

Our analysis highlights significant correlations between various financial knowledge learning channels and variations in financial literacy levels. Formal financial education and social media as channels for acquiring financial knowledge are notably associated with higher levels of financial literacy. The impact of peers and family members through their financial behaviors also plays a crucial role, indicating that practical experience and social interactions are instrumental in developing financial literacy. This finding supports

Model Accuracy and Summary of Findings

The logistic regression model exhibits good predictive accuracy based on sensitivity and specificity tests, providing reliable insights into the factors that correlate with financial literacy among college students. The logistic regression analysis utilized in this study provides a comprehensive view of how demographic factors, behavioral elements, and different FK acquisition channels correlate with FL among Chinese college students. The findings underscore the importance of a supportive learning environment, dedicated study time, active engagement with formal educational tools, and informal social learning opportunities to enhance financial literacy. These insights are crucial for developing targeted educational strategies and policies to improve FL levels. These results can inform policy interventions to enhance financial literacy through targeted educational strategies and the effective use of diverse learning channels.

This table presents logistic regression results, analyzing the demographic and behavioral factors associated with Financial Literacy (FL). The dependent variable, FL, is assigned a value of 1 for respondents scoring 13.4 or above (approximately 67% of the total 20 points) on the FL questionnaires and 0 otherwise. Independent variables include demographic and behavioral factors, as defined in the methodology section. Key statistics in the table include the mean and standard deviation (S.D.) of the dependent variable, along with a constant term in the regression models. For each model, we report the number of observations (Obs.), pseudo R-squared (Pseudo Rsq.), Wald Chi-Square test (Chi-sq.), and log pseudolikelihood value. The table also indicates the model’s ability to predict financial literacy proficiency (Sensitivity) and non-proficiency (Specificity). Significance levels are marked as follows: *** for 1%, ** for 5%, and * for 10%.

Robustness Check

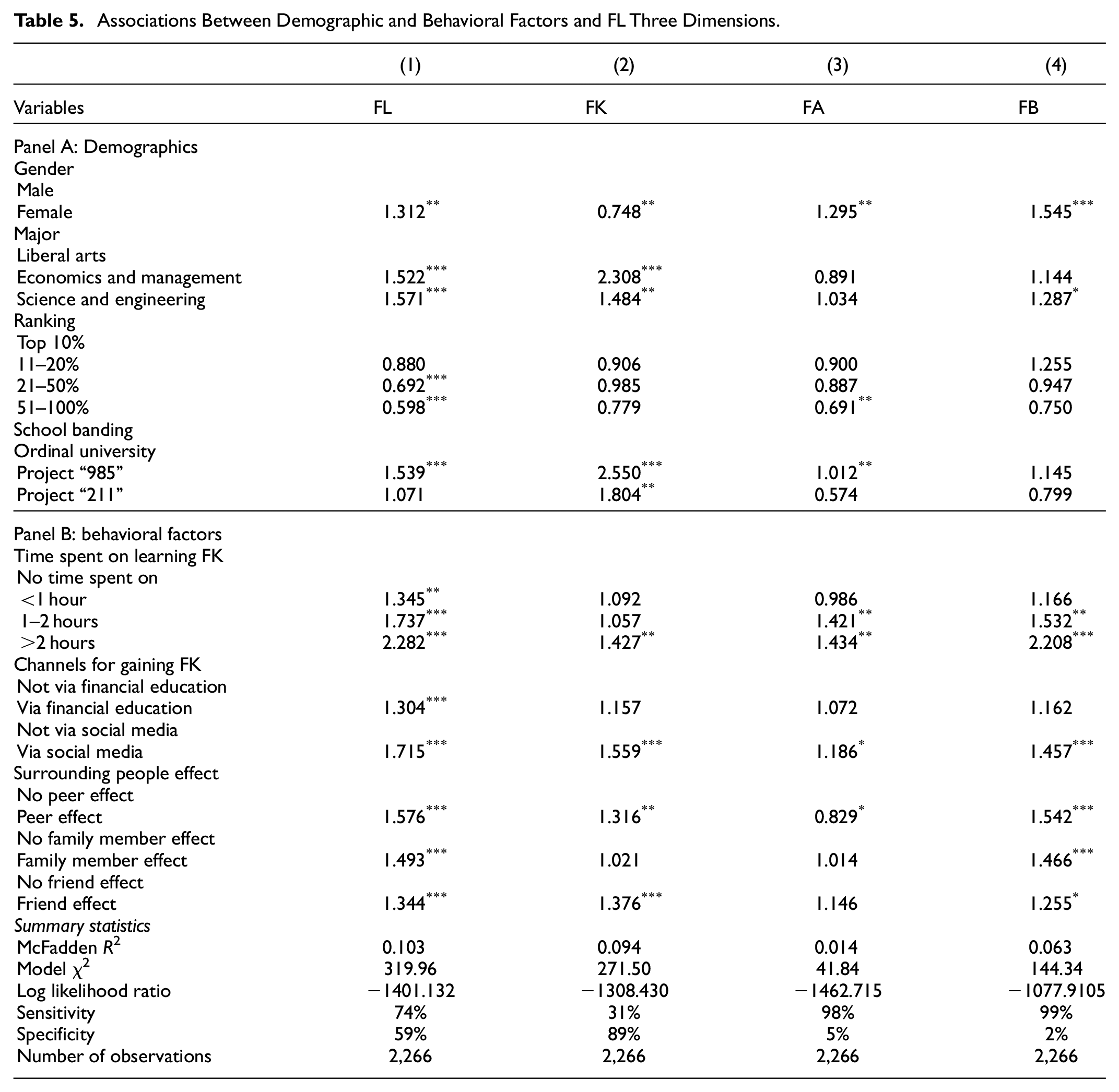

In this section, we conduct a rigorous analysis of the relationship between various demographic and behavioral factors and financial literacy (FL), focusing on its three components: knowledge, attitudes, and behaviors. We employ logistic regression to explore the associations of gender, academic major, ranking, school banding, and diverse financial knowledge (FK) learning methods with FL.

Initially, we define proficiency in FL as scoring above the mean. Supported by data presented in Table 5, our analysis shows that females exhibit a deeper comprehension of financial topics, which correlates with enhanced financial knowledge. Additionally, students majoring in economics, management, science, and engineering report higher levels of FL. A significant finding from our study is the association between university ranking and FL: students ranked in the middle (21–50%) and lower tiers (51–100%) exhibit FL scores that are 30% and 40% lower, respectively, compared to those in the top 10%.

Associations Between Demographic and Behavioral Factors and FL Three Dimensions.

The superior education offered at elite universities correlates with higher FL, likely reflecting better-quality instruction and a more stimulating peer environment. Moreover, varied methods of learning FK—ranging from peer interactions and social media engagement to intensive study—are significantly associated with FL, highlighting the critical role of diversified educational approaches.

Our analysis further reveals that the presence of financially savvy individuals, whether peers, friends, or family members, correlates with higher FL levels among college students, underscoring the importance of positive social interactions.

A secondary analysis focuses on the distinct dimensions of FL. Table 5 supports these findings, showing that factors such as female gender, majoring in economics/management or science and engineering, and extensive engagement in finance learning notably correlate with enhanced financial knowledge. The role of peers and social environments is especially significant, with attendance at elite universities and active peer interactions positively related to financial attitudes. Moreover, prolonged involvement in financial studies significantly strengthens these attitudes. Variables including peer interactions, social media use, and rigorous study play vital roles in enhancing financial knowledge, attitudes, and behaviors, demonstrating the importance of a broad and engaging educational environment in fostering comprehensive financial literacy.

The table outlines the logistic results of our financial literacy (FL) analysis. FK stands for financial knowledge, FA stands for financial attitude, and FB stands for financial behavior. Model (1) shows the odds ratio of logistic regression, where respondents scoring above 12.5 points (the average score) on FL questionnaires are assigned a value of 1 and 0 otherwise. Models (2) to (4) present logistic regression (odds ratio) results, assigning a value of 1 to respondents scoring 5, 3, 5, or above (about 67% of the FK, FA, and FB scores) in the FK, FA, and FB questions, respectively, and 0 otherwise. Independent variables in these models include demographic and behavioral factors, detailed in the methodology section. The lower section of the table shows for each model the number of observations (Obs.), pseudo R-squared (Pseudo Rsq.), Wald Chi-Square test (Chi-sq.), and the log pseudolikelihood value. The table also indicates the model’s ability to predict financial literacy proficiency (Sensitivity) and non-proficiency (Specificity). Significance levels are marked as *** for 1%, ** for 5%, and * for 10%.

Conclusions and Discussion

Discussion

This study evaluated financial literacy (FL) among 2,266 Chinese college students by examining its correlations with demographic variables and financial knowledge (FK) learning. Remarkably, Chinese students achieved higher average FL scores (13.1) compared to a 17-country average of 11.7, indicating a robust grasp of financial concepts. Nevertheless, there remains potential for further improvement, especially when compared to more advanced economies.

The analysis revealed notable gender differences, with female students outperforming their male counterparts across all FL dimensions. This finding diverges from prevalent trends but aligns with results from five OECD INFE countries. Furthermore, students from fields such as economics, management, science, and engineering demonstrated superior FL compared to those in liberal arts, corroborating findings from previous research (Andreou & Anyfantaki, 2021; Ergün, 2018; Mandell, 2008).

FL also varied according to academic standing and the prestige of the educational institution. Students from more prestigious universities typically showed higher FL levels, likely benefiting from enhanced educational opportunities and influential peer groups (Lee & Chiu, 2017; Miller et al., 2014; Moschis & Churchill, 1978; Mugerman et al., 2014).

Behavioral factors played a significant role in shaping FL. Extensive engagement in FK learning was positively correlated with increased FL, underscoring the value of sustained dedication and a proactive attitude toward financial education (Meier & Sprenger, 2013). Both formal financial education and the use of social media were positively associated with FL, highlighting the importance of educational environments and social interactions in facilitating knowledge acquisition (Borgatti & Ofem, 2010; Liu et al., 2020; Lusardi & Mitchell, 2014; Miller et al., 2014; Moschis & Churchill, 1978; Tan et al., 2022).

Additionally, peers, friends, and family members’ financial behaviors are significantly associated with students’ financial behaviors (FB). Observations of successful financial practices among acquaintances often inspired similar student behaviors, corroborating Bandura and Walters’s (1977) social learning theory and emphasizing the significant impact of social interactions (Borgatti & Ofem, 2010).

Management Implications

Our research underscores the importance of fostering a culture that emphasizes financial investment, excellence, and motivation among college students, particularly in light of the “surrounding people effect.” Given the observed correlation between school rankings and financial literacy (FL), parental and educational support should encourage students to aim for prestigious universities and excel academically. To enhance FL, we recommend collaborative efforts between parents and educational institutions to help students allocate more time to learning financial knowledge (FK), regardless of their major. This collaboration should guide students in accessing diverse channels for acquiring FK, applying it to develop financial plans, and exploring investment opportunities.

Furthermore, efforts to integrate FL into higher education curricula are essential to improve students’ understanding of fundamental financial concepts such as interest calculations and risk diversification. However, it is equally important to emphasize the practical application of this knowledge. Strengthening students’ social interactions within academic settings is also vital, as these can significantly enhance their financial education. By linking theoretical knowledge with practical application and supporting an environment conducive to financial learning, we can elevate the FL of Chinese college students, thereby equipping a future generation to make informed financial decisions and effectively navigate financial complexities. These measures are crucial not only for individual financial health but also for fostering a more financially literate society.

Limitations and Future Research

This study encounters several limitations that warrant consideration. First, the geographical specificity of our sample within China may limit the broader applicability of our findings. Although this represents the first extensive financial literacy survey among Chinese college students, including participants from diverse regions, the results should be applied cautiously to other contexts. Future studies should include a more diverse demographic profile to broaden the generalizability of the findings.

Second, the research design employed in this study is correlational and does not establish causality. This limitation underscores the need for future investigations to focus on determining causal relationships, especially examining how financial literacy impacts individuals’ capabilities to recognize and prevent financial fraud.

Third, our participant age range was limited to 18–29 years to match the experiential backgrounds with those from other countries, resulting in diverse sample sizes—from 141 in the Republic of North Macedonia to 431 in Peru. This age restriction and the varying sample sizes have limited our capacity to delve deeper into variations across different educational backgrounds, a factor that future research should consider.

Despite these limitations, this study’s results are crucial for understanding how financial literacy varies across different cultural and educational settings. They highlight the importance of adopting tailored approaches in future financial literacy research to address these nuances effectively.

Footnotes

Appendix: College Students’ FL Measurement

FK1 (Time value of money) Now imagine that you have to wait for 1 year to get 1,000 yuan, and the inflation stays at 5%. In 1 year’s time will you be able to buy:

FK2 (Interest on loan) You lend 500 yuan to your classmate, and he/her will pay you 500 yuan back three months later. Assuming that the bank’s annual loan interest rate is 4.35%, how much interest has he paid on this loan?

FK3 (Simple interest) Suppose you put 100 yuan into a savings account with a guaranteed interest rate of 2% per year. You don’t make any further payments into this account and you don’t withdraw any money. How much money would be in the account at the end of the first year, once the interest payment is made?

FK4 (Compound interest) Suppose you put 1,000 yuan in the bank with an annual interest rate of 2%. What is the balance of your account at the end of 5 years?

FK5 (Risk and Return) An investment with a high return is likely to be high risk

FK6 (Definition of Inflation) High inflation means that the cost of living is increasing rapidly

FK7 (Diversified investment) It is usually possible to reduce the risk of investing in the stock market by buying a wide range of stocks and shares.

FA1(Live for today) I tend to live for today and let tomorrow take care of itself:

FA2 (Spend than save) I find it more satisfying to spend money than to save it for the long term:

FA3 (Money is there to be spent) Money is there to be spent.

FB1 (Affordability) Before I buy something I carefully consider whether I can afford it:

FB2 (Bill payment) I pay my bills on time:

FB3 (Financial Monitoring) I keep a close personal watch on my financial affairs:

FB4 (Long-term planning) I set long term financial goals and strive to achieve them:

FB5-1 (Personal budget) Do you have a budget for daily consumption?

FB5-2 (Decision-making) Will you participate in the financial decision-making in your family?

FB6 (Actively savings) In the past 12 months have you been [individually] saving money, whether or not you still have the money?

FB7 (Choosing financial products) Which of the following statements best describes your choice about choosing financial products?

FB8 (Making ends meet) What did you do to make ends meet the last time this happened?

Acknowledgements

In addition, many thanks to the OECD/INFE Secretariat, which offers the OECD-INFE 2020 Survey data on Adult Financial Literacy.

Author Contributions

Jiuping Xu contributed to the conception of the study. Zhineng Hu and Yongge Niu contributed significantly to the data sources and manuscript preparation. Xiawei Tan performed the data analyses and wrote the manuscript. Zhineng Hu and Yongge Niu helped perform the analysis with constructive discussions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The National Natural Science Foundation of China [Grant Nos supports the work. 72072122,71572120], and General Project of Sichuan Key Research Base of Social Sciences–System Science and Enterprise Development Research Center [Grant No. Xq23C01], and the Talent Introduction Project of Xihua University, China [Grant number: RX2300000805].

Ethics Statement

We further confirm that any aspect of the work covered in this manuscript that has involved either experimental animals or human patients has been conducted with the ethical approval of all relevant bodies and that such approvals are acknowledged within the manuscript.

Consent

All participants in this study were informed about the purpose, procedures, and potential risks involved in the research. Written informed consent was obtained from all participants prior to their participation in the study. Participants were assured of the confidentiality and anonymity of their responses, and they were informed that their participation was voluntary and that they could withdraw from the study at any time without any consequences.

Data Availability Statement

The first author will make available the datasets used and analyzed in this study (the author’s survey data except for the OECD-INFE 2020 Survey data) upon reasonable request.