Abstract

There is a growing awareness of the importance of financial education and literacy in personal economic success, yet not many Generation Z are proficient in this area. The lack of understanding can lead to consequences such as not recognizing the need for greater retirement savings, making poor spending decisions, or when overpaying off high-interest debt. In addition, many of the studies on financial education and literacy among Generation Z remain untapped in the context of China. As a result, the researcher emphasizes the evidence by mining data from the Web of Science database and analyzing the data using bibliometrics and content analysis. Contemporary research on financial education and literacy in the web of science has discovered that it is trending strongly across fields like environmental science, healthcare, energy, and economics, according to bibliometric data. Further investigation has uncovered the important writers, journal sources, and universities in China that are creating such knowledge. Subsequently, the content analysis on the focused area has yielded results related to recent findings from key authors, and how their studies describe the socio-demographic and psychological behavior of Generation Zs. As an implication, China’s academic research reveals that Generation Zs’ subjective and objective financial education may be absorbed into their financial self-beliefs, which affects how they handle their finances. Thus, financial education is instrumental to help them set clear financial goals and plan for the future.

Keywords

Introduction

Financial literacy is the ability to obtain useful financial information and skills necessary to make wise decisions and manage one’s money. It includes using complex financial tools, understanding the financial system, evaluating investment options, and making informed choices (Ghasarma et al., 2017). Financial literacy can be defined as knowledge of the general concepts of personal finance—such as saving, borrowing, and budgeting—and the specific tools necessary to effectively manage money. To achieve a healthy financial lifestyle, individuals must demonstrate their knowledge and ability in different aspects of finance. The factors that contribute to financial literacy are numerous and vary by individual.

On the other hand, people born between 1996 and 1997 are considered members of Generation Z (also known as the iGen, Centennials, etc.). They are currently between 9 and 24 years old in terms of age group. While more and more young people are interested in improving their finances, this new generation’s concern about their wealth requires more exploration in their financial management behavior. According to the US National Association of Plan Advisors (NAPA), Gen Z has the lowest level of financial literacy, with only 28% of questions being answered correctly on average. P-Fin Index findings show that financial wellness and financial literacy are linked across all five generations—a constant conclusion, the research states (Godbout, 2021).

From other studies, it is found that there is still the majority of young generation Zs are financially vulnerable, despite their daily efforts to cope with life’s economic challenges (Kovács et al., 2021). The rising cost of living and inflation has made it more difficult to pursue long-term goals. This proposal discusses the importance of financial education for young people about financial literacy which eventually will help stabilize their state of personal finances (Becerra, 2018).

For generation Zs, the ability to make well-informed financial decisions at the personal, household, and macroeconomic levels depends on having a good grasp of financial literacy (Bharucha, 2019). The goal of this study is to determine the relationship between financial education and financial literacy, as well as their impact on society and macroeconomic stability. As judged by many financial educational leaders and economists, financial literacy has a considerable impact on economic stability (Arrondel et al., 2014). As speculations from this study, it is hypothesized that there are numerous implications for financial education programs for the financial literacy of generation Zs in China.

For generation Zs to take advantage of opportunities for economic stability, financial literacy is becoming increasingly necessary through financial planning. Generation Zs who are knowledgeable about financial matters is more likely to meet the needs of employers in the labor market (Hogarth, 2006). But for them to prosper and grow, they must have a fundamental understanding of economic principles like inflation and compound interest Gaisina and Kaidarova (2017). An individual’s finances can make educated judgments and analyze the advantages and disadvantages of numerous investment possibilities that are available to them if they have better levels of financial literacy (Boon et al., 2011). As stated by Agarwal et al. (2015). people who are aware of their finances, and knowledgeable in financial education are better able to make good financial decisions for themselves and their families, resulting in greater financial stability and well-being.

Alternatively, long-running discussions have taken place among academics as well as representatives of business organizations and governmental agencies over the last few decades about financial instability and financial (Adam et al., 2017). Scholars have many times demonstrated the strong link between financial education and financial literacy, and this topic has been widely discussed. However, higher education stakeholders in financial education must enhance public awareness about the threat of generation Zs financial lack of education, personal instability, and the potential impact of accumulating personal debts on their lives and family (Tjiptono et al., 2020). When it comes to saving, investing, inflation, and asset diversification, an informed and financially literate person will know all of these things and more. Vice, versa this is not the case for those who are ignorant and not financially literate. In addition, studies should identify and understand the components and measures that contribute to financial stability (Kirchmayer & Fratričová, 2020).

Literature Review

Ideas about financial education and financial literacy can be redefined through the use of theories, which can be applied to a wide range of subjects. As mentioned earlier, Gen Z is the newest generation, born between 1997 and 2012. They are currently between 9 and 24 years old (nearly 68 million in the U.S.) (Tjiptono et al., 2020). From literature reviews, financial literacy is regarded as a skill that is jointly developed with multiple aspects, including learning how to manage one’s money, understanding how the money system works, and being able to make wise financial decisions—not just saving money but also investing, borrowing, compounding interest, etc. The ability to understand these topics is one of the most important and challenging aspects of Aulia and Baskoro (2019). Given that these topics are not only basic financial knowledge but also extremely diverse, there isn’t an exact set of traits or skills that can be said to be particular for every individual. Ultimately, this is why financial literacy cannot be defined by a single characteristic (Lingyan et al., 2021).

Impact of Financial Education on Financial Literacy

Financial literacy can be developed through various learning techniques and resources to promote the effective functioning of money management systems (Zhu, 2021). Lessons are taught about money in classrooms and at home through books, television shows, and short videos. For many people, the most commonly used financial research methods include going online to learn about investments and credit cards. Students need to understand that there are risks associated with the use of these products and that the person teaching them is knowledgeable of the process (Zhu, 2019).

The potential link between financial education and Financial literacy can be achieved by learning and applying the habits of saving and investing wisely to meet basic requirements (such as personal expenses, housing, and health care). As a result, the teaching of financial education for Gen Z mainly attempts to improve financial literacy to help avoid negative impact on personal income and wealth (Ghasarma et al., 2017). With the increasing use of smartphones to access personal finance information, tablets or e-readers have also become increasingly popular devices for financial literacy classes. However, it is noted that the use of advanced technologies for learning about financial concepts does not necessarily guarantee improved learning results.

Students too can also be taught about finance through personal experience and practice (Hyranek & Misota, 2019). For example, children can often be taught by watching their parents or guardians manage expenses and make decisions. Children can also observe their parents’ spending habits and learn from them. It is also possible for a student to apply what they have learned in school to real-life situations while they are learning concepts online, in a classroom, or through observation (Naufaldi & Baskoro, 2019).

Understanding personal finance and budgeting in financial education share many similarities with the financial planning industry. It is for this reason that insurance, unit trusts, and estate planning are well-suited for the vast majority of citizens to support personal financial literacy (Huston, 2012). With the help of banks, they have also been playing their part in educating generation Zs about financial literacy with financial planning and introduction to financial products such as loans, credit cards, and other financial investment tools (Gamst-Klaussen et al., 2019). Financial planning and financial education can help guide families to purchase homes, and cars and save for education or retirement funds. Because most economies are bank-based, economic stability and growth are often used interchangeably with financial planning or financial literacy (Lusardi, 2015).

On the other hand, financial education has been approached through a one-size-fits-all approach, but studies show that this teaching style can negatively impact learning. Most people learn better in different ways. Therefore, teachers need to create a personalized learning plan for their students to best help them (Aulia & Baskoro, 2019; Birkenmaier & Fu, 2020).

Financial literacy is measured in part by how well people can take care of their finances and make informed decisions about how to manage their money. For people to be able to do so, they must have a certain knowledge of the topic related to finance, such as understanding basic concepts of economics and making wise financial decisions (Gamst-Klaussen et al., 2019). According to various scholars in financial education, the most challenging aspect of financial literacy is that it is a complex topic that requires an understanding of a variety of subjects (Zhu, 2021). There is a difference between financial literacy and financial capability—one does not automatically lead to the other. There are over 30 areas in which financial literacy is measured (A. S. Ghadwan et al., 2022; Park & Martin, 2022). However, financial literacy can be evaluated using multiple techniques. The way finance ideas are taught in school or at home can also drive students’ interest and participation in learning. For example, financial literacy about saving money is measured by how well people understand the role of savings and debt in their financial situation. In order to measure financial literacy about spending money, one must look at how well people understand the relationship between income, expenditures and assets (Jia et al., 2021).

Therefore, it can be said that financial literacy is important for all individuals in decision-making. This is particularly important for those who are younger, as decisions made now can impact their future financial situations (Park & Martin, 2022; Zhu, 2021). For example, if a student begins receiving loans from the government now and does not pay them off, they can face large problems as an adult when it comes time to make decisions about buying a car, getting married, starting a family, and more. People with lower levels of financial literacy also tend to experience higher interest rates on bank accounts and credit cards because they do not have the financial qualifications that lenders find attractive (Zhu, 2021). Vice versa, individuals who have high levels of financial literacy act differently in certain situations. They use different strategies than low-literate people when managing money. For example, they are more likely to spend down their savings and use automatic payments. They also keep track of their money and know how to budget it effectively. On the other hand, low-literate people tend to spend more of their money than they have, save less, and have difficulty managing cash flow (Gamst-Klaussen et al., 2019; Hyranek & Misota, 2019).

Financial literacy levels are also related to a person’s income levels, often called lifestyle or consumption patterns. Consumption patterns affect personal financial decisions because they determine what a person consumes and how much they save for future purchases. A study found that there are classes of consumption patterns based on household income. These consumption patterns are difficult to change because they are deeply ingrained in our cultural identities as well as our political systems (Durisova et al., 2019; Naufaldi & Baskoro, 2019). For example, the idea that high-income earners should invest large amounts of money in stocks because they have so much money to invest is a concept that many people believe in. On the other hand, this idea of wealth-based investment makes it difficult for lower-income societies to participate in the stock market because they cannot afford to invest as much money as those with higher incomes (Birkenmaier & Fu, 2020; A. S. Ghadwan et al., 2022). The way savings and debt are described can affect an individual’s behavior concerning their finances (Jia et al., 2021).

Challenges to Financial Literacy

Many challenges affect financial literacy levels. These challenges can be internal or external. Internal distractions include emotions like fear, greed, or anxiety that make it difficult for adults to maintain an objective stance on their finances. External distractions include the media and financial institutions (such as banks) that focus on specific products and services (Park & Martin, 2022; Zhu, 2019). For example, there is media influence that comes from selling products for retirement savings. Retirement funds provided through employers generally have high management fees that are paid to financial institutions. Many people are unaware that this is happening and as a result, they lose a significant portion of their earnings to these fees. In contrast, when people invest money on their own, they can choose not to pay commission fees to financial institutions and instead choose index funds that do not require paying management fees (Gamst-Klaussen et al., 2019; Park & Martin, 2022). The media often fails to mention the high level of management fees associated with retirement accounts provided through employers which may be one reason why many people do not understand how it works (Birkenmaier & Fu, 2020).

Institutions can hinder a person’s ability to make informed decisions about their finances. For example, a study found that 17% of college students had no idea how credit cards work because they were not knowledgeable about how credit works. Financial institutions spend money marketing themselves to individuals and claim they are looking out for the best interests of these individuals to gain business (Wang et al., 2011). In reality, many sometimes hide information or push people into products that may not be right for them. It is also possible that institutions are manipulating people’s decisions by giving them false information such as telling them they are less prone to bankruptcy if they have a credit card rather than a debit card (Borzekowski et al., 2008; Stavins, 2020).

The media also plays a large role in influencing adults’ financial literacy levels. This is especially true concerning advertising and marketing campaigns. Studies show that the images associated with certain products and services influence adults’ decision-making more than actual product and service characteristics. In other words, the brand is more important than the product or service itself (Manuel Otero-Lopez et al., 2021; Reisch et al., 2004). For example, when comparing two products of smartphones, people choose the pair that has a familiar brand name rather than a brand name they are unfamiliar with even if both items are equally good products (Gracia Rodriguez-Brito et al., 2021).

Overall, the media has a big effect on people’s financial literacy levels. The media campaigns for products and services have been designed to attract our attention and make people believe that they will miss out on an opportunity if they fail to act right away (Manuel Otero-Lopez et al., 2021). In many cases, these media campaigns are simply an influence that leads people to part with their money. Despite all these external factors, people can still improve their financial literacy levels (Lingyan et al., 2021).

Problem Statement

In 2009, it was estimated that 1.9 billion adults around the world had no financial knowledge whatsoever. This situation is especially alarming because there are many misconceptions among those who do have financial knowledge, such as they feel there is a “right” way to save money. As a result of this lack of financial literacy and financial management skills, two-thirds (66%) of all personal bankruptcies in the United States occur among people with a college education or higher (Stavins, 2020; Wang et al., 2011).

Financial education is an area where many generation Z’s lack experience and perhaps knowledge, skills, and attitudes. Their vulnerability to a downturn in the economy is, therefore, greater than before. According to research and data, Generation Z lacks basic financial literacy and is accumulating debt at an alarming rate (Keeter, 2020). Providing Generation Z with resources like financial planning, counseling, and instruction is a sound investment. If students aren’t exposed to financial education, they may not be able to make sensible financial decisions (Ang et al., 2022). Generation Z who finds themselves in a vulnerable financial situation as a result of increasing debt can choose from a wide range of debt management solutions. However, not many of them are well acquainted with financial planners. As a result of the current economic climate from the COVID-19 pandemic, students may feel anxious and depressed. Many of them are becoming concerned about their student loans, or even their early career finances. According to scholars, financial stress is just one of several causes of stress among minority college students who make up part of Generation Zs (Cyfert et al., 2021). Debt and financial stress can have a severe impact on pupils’ academic performance and subsequently life. Generation Zs who have graduated from college and cannot find full-time or even part-time jobs are sometimes compelled to drop out of school early. Both of these have a detrimental effect on the percentage of Generation Zs who remain in school after their first year. Some Generation Zs’ graduation date may be delayed if he or she has to reduce the number of courses he or she takes due to budgetary constraints (Khan et al., 2020).

Purpose of the Study

Generation Z, often known as the post-millennial generation, refers to those born between 1997 and 2012 This indicates that Generation Z will be between the ages of 11 and 26 in 2023 (Dimock, 2023) They are also the demographic group that comes after Millennials and before Generation Alpha (Brunjes, 2023). Scholars have highlighted that when financial education program is formally delivered in higher education institutions for this group of generations, there could be numerous research possibilities to uncover the state, impacts, and challenges for Generation Zs (Miller & Mills, 2019). However, there is a preliminary need to explore, identify and explain the existing body of knowledge on financial education about Generation Zs. As such, nine research questions are listed as follows:

Based on bibliometric analysis of the data mined from the Web of Science, what is the knowledge base of financial education in China?

Based on bibliometric analysis of the data mined from Web of Science, what are the Impact factors on financial literacy among Generation Zs in China in China?

Based on bibliometric analysis of the data mined from the Web of Science, what does the body of knowledge reveals on “Challenges” or “Strategies” of financial literacy among Generation Zs in China in China?

Based on the same data mined from the Web of Science, what is the pattern of bibliographic coupling based on universities?

Based on the same data mined from the Web of Science, what is the pattern of bibliographic coupling based on authors?

Based on the same data mined from the Web of Science, what is the pattern of bibliographic coupling based on sources of journals?

Based on content analysis of contemporary articles, what is the state of financial education among Generation Zs in China?

Based on content analysis of contemporary articles, which aspects of financial education impact the level of financial literacy among Generation Zs in China?

Based on content analysis of contemporary articles, what are the improvements to address the challenges regarding financial education to improve the level of financial literacy among Generation Zs in China?

To explain further, this study examines the knowledge base of Generation Z concerning their financial literacy and education. In recent years, many youths in China have fallen victim to high credit card debts and uncontrolled spending. Similar to other parts of the world, many members of China’s Generation Z have become victims of excessive credit card bills and reckless spending (Bloomberg, 2019; Nguyen, 2022). According to one survey, Generation Z in China spends 13% of their family income, compared to 4% in France and Germany. This is most likely because Gen Z has taken to debt in a manner that their more thrifty parents did not (Huifeng, 2021). As inflation sets in, Generation Z is amassing credit card debt almost three times faster than the rest of the population (Nguyen, 2022). In June of last year, some members of Generation Z owed a smartphone app more than 10,000 yuan ($1,500) (Bloomberg News, 2019). This has fueled fears that adolescent debt may ruin China’s luxury market (Achim, 2021). Therefore, this prompts more studies regarding their understanding and habits in personal money management.

As the information presented above is obtained and cited from reliable financial reports and news, there is a lack of evidence coming from researched databases like the Web of Science. Hence this study is carried out through bibliometric and content analysis to understand what is out there in the body of knowledge. Alternatively, this study is an approach to theoretical and methodological triangulation regarding this subject (Denzin, 1971).

Methodology

Bibliometric analysis is a quantitative analytic technique that uses mathematical and statistical techniques to assess the interdependence and influence of research constituents (Aria & Cuccurullo, 2017; Donthu et al., 2021). Alternatively, there is the application of statistical tools to analyze published documents such as books, papers, and other publications, particularly those with scientific content, is known as bibliometric analysis (Donthu et al., 2021). Vos viewer is one of the many bibliometric analysis tools that analyze and display bibliographic data (Lee et al., 2020; van Eck & Waltman, 2010). It works with data from Scopus, Web of Science, PubMed, and other databases (Tomar et al., 2021). It is used to measure the academic quality of journals or writers objectively using statistical approaches such as citation analysis (Wang et al., 2021). In recent times, scholars use bibliometric analysis to untangle the links between scientific domains and discover trends in research topics (Rani et al., 2022).

In other examples, the bibliometric analysis may be used to examine patterns in a researcher’s research, give evidence for a researcher’s or area of study’s effect, and deconstruct the structure and dynamics of scientific fields (Elder, 2023). Bibliometrics is often used to evaluate the use of certain approaches, techniques, or subjects in a given field. Citation analysis, co-citation analysis, co-word analysis, and network analysis are all common bibliometric analysis techniques (Biscaro & Giupponi, 2014; Donthu et al., 2021). These methods may be used to find prominent authors, publications, and subjects in a certain field. In other words, bibliometric analysis is useful for analyzing patterns when studying books, papers, and other publications (Donthu et al., 2021). Bibliometric analysis may also be used to assess the significance of research publications in a certain area or topic (Wang et al., 2021), or evaluate the academic quality of journals or authors by tracking measures with citations, co-citations, and impact factors(Elder, 2023; Rani et al., 2022).

This study uses the bibliometric and content analysis approach whereby the researcher shall explore the contexts of higher education institutions in China, and unearth any information on how they implement financial education programs to impact the financial literacy of Generation Z. More particularly, content analysis from the academic database will be conducted on selected high-impact articles from the Web of Science about the keywords that portray the direction of this study. Efforts are also taken to map out the need for future studies and to evaluate the criteria of participants’ selection, location, and other usefulness of this study to enhance financial education among tertiary students in higher education.

In the first part of the methodology, the researcher will conduct a bibliometric analysis using Vosviewer. The selection of keywords to extract data is shown in Table 1.

Keywords for Search From the Web of Science Database.

In the second part of the methodology, the researcher will conduct a content analysis using by reading and extracting information from top articles and prominent authors related to the key research areas. The findings from both bibliometric and content analysis are presented in the next section.

Discussions on Findings

Part 1: Bibliometric Analysis

1. Based on bibliometric analysis of the data mined from the Web of Science, what is the knowledge base of financial education in China?

The first step to investigate: (a) the knowledge base of financial education in China has yielded 56,121 results from the Web of Science Core Collection. From the total, the researcher downloaded the top 1,000 articles for Bibliometric analysis in Vosviewer. The criteria of bibliometric analysis are refined and shown in the following figures.

Bibliometric analysis revealed the following information that helped the researcher to narrow down the research inquiry before conducting content analysis. This process is vital for the researcher to scoop and explore information (in the form of keywords) from the last 5 years’ publications about the subject in the body of knowledge, identifying the direction, trends of publications, and key authors who publish in the field of financial education and literacy. The criteria of bibliometric analysis are refined and shown in the following Table 1.

With the selection of choices from Vos viewer, 310 sources met the requirement of having at least five occurrences of a keyword from the Web of Science.

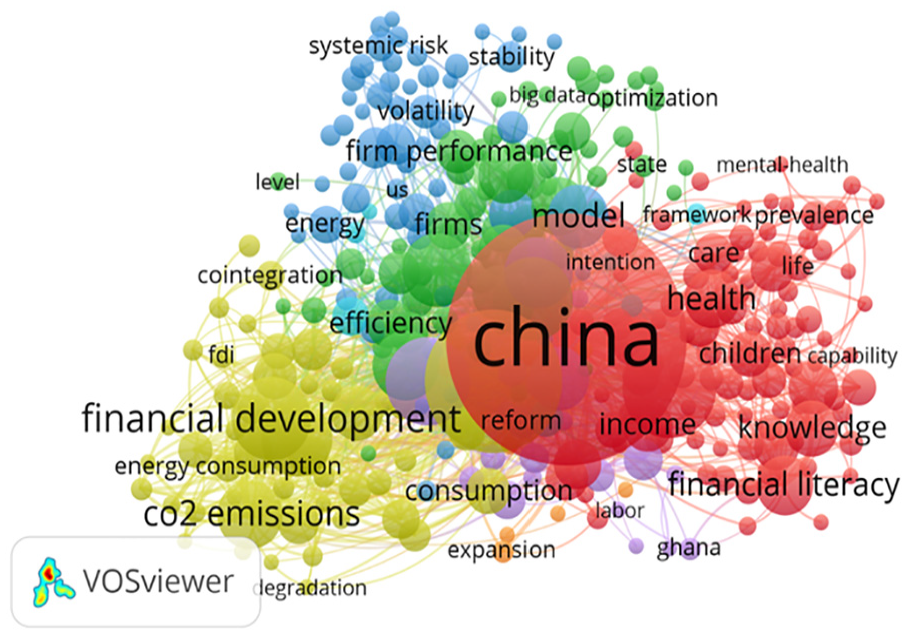

The result of the Bibliographic network visualization is shown in Figure 1.

Bibliographic network visualization for “Financial education in China” showing co-occurrence with “all keywords” as a unit of analysis.

Subsequently, Figure 2 is presented Bibliographic density visualization to reveal the prominent keywords more clearly as found on the Web of Science.

Bibliographic density visualization of “Financial education in China” showing co-occurrence with “all keywords” as a unit of analysis.

As an explanation, it is clear from the bibliometric analysis that financial education in China has overlapping fields with environmental science, healthcare, energy, and economics. As this study is related to personal finance, the keywords of financial literacy and financial development are quite substantial when compared to other keywords. Hence there is evidence from China that this is trending and accumulating in the knowledge base of the Web of Science.

Impact Factors on Financial Literacy

2. Based on bibliometric analysis of the data mined from Web of Science, what are the Impact factors on financial literacy among Generation Zs in China in China?

The second step in the bibliometric analysis is to investigate: (b) the Impact factors on financial literacy among Generation Zs in China has yielded 56,135 results from the Web of Science Core Collection. From the total, the researcher downloaded the top 1,000 articles for Bibliometric analysis in Vosviewer. The criteria of bibliometric analysis are refined and shown in the following Table 2.

Key Settings in Vosviewer for Analysis of Co-occurrence With “all Keywords” as Unit of Analysis for “Impact Factors on Financial Literacy.”

With the selection of choices from Vos viewer, the similar 310 sources met the requirement of having at least five occurrences of a keyword from the Web of Science.

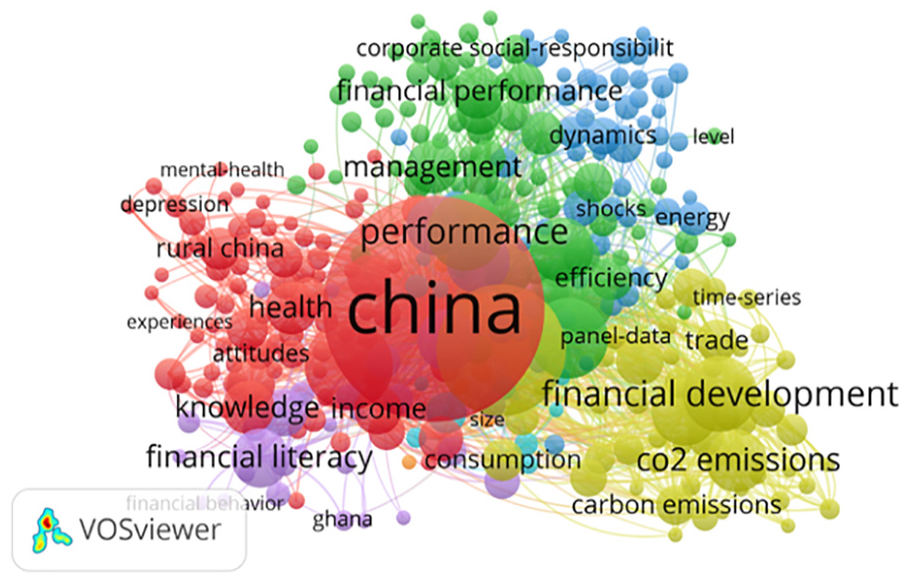

The result of the network analysis is shown in Figure 3.

Bibliographic network visualization showing “Impact factors on financial literacy.”

Subsequently, Figure 4 is presented to reveal the prominent keywords clearly as found on the Web of Science.

Bibliographic density visualization showing “Impact factors on financial literacy.”

As an explanation, it is clear from the bibliometric analysis that impact factors on financial literacy in China are studied along with their impact /on environmental science, healthcare, energy, and economics. As this study is related to personal finance, the keywords of financial literacy and financial development are quite substantial when compared to other keywords. It is also shown that the relationship between financial education and financial literacy is well documented. Hence there is evidence from China that this is trending and accumulating in the knowledge base of the Web of Science.

“Challenges” OR “Strategies” in Financial Education and Financial Literacy Among Generation Zs

3. Based on bibliometric analysis of the data mined from the Web of Science, what does the body of knowledge reveals on “Challenges” or “Strategies” of financial literacy among Generation Zs in China in China?

Lastly, the final step in the bibliometric analysis is to investigate “strategies” or “challenges” in financial education and financial literacy among Generation Zs in has yielded 56,135 results from the Web of Science Core Collection. From the total, the researcher downloaded the top 1,000 articles for Bibliometric analysis in Vosviewer. The criteria of bibliometric analysis are refined and shown in the following Table 3.

Key Settings in Vosviewer for Analysis of Co-occurrence With “All Keywords” as Unit of Analysis for “Financial Education in China” OR “Impact Factors to Financial Literacy” OR [“Challenges” OR “Strategies”].

With the selection of choices from Vos viewer, 309 sources met the requirement of having at least five occurrences of a keyword from the Web of Science.

The result of the network analysis is shown in Figure 5.

Bibliographic network visualization showing “Financial education in China” OR “Impact factors to financial literacy” OR [“Challenges” OR “Strategies”].

Subsequently, Figure 6 is presented to reveal the prominent keywords clearly as found on the Web of Science.

Bibliographic density visualization showing “Financial education in China” OR “Impact factors to financial literacy” OR [“Challenges” OR “Strategies”].

As an explanation, it is obvious from the bibliometric analysis on strategies and challenges to financial literacy in China are researched together with its influence on and from environmental science, healthcare, energy, and economics. There are emerging studies related to the phenomenon of Covid-19, inequality, higher education, adolescents, and rural China.

When compared to the other keywords, the terms “inequality,” “financial literacy” and “higher education” have significant visibility in this bibliometric analysis since it is focused on aspects of personal finance. Like the earlier analysis, it is also shown that a well-documented link exists between the two concepts of financial education and financial literacy. As a result, data is coming from China indicating that this is becoming more prevalent and expanding in the Web of Science’s knowledge base.

Bibliographic Coupling Based on Universities

4. Based on the same data mined from the Web of Science, what is the pattern of bibliographic coupling based on universities?

More efforts were also conducted by the researcher in the bibliometric analysis to investigate conceptual and social structure in the body of knowledge. With the data downloaded from the web of science, the researcher refines the search to uncover the co-occurrence of keywords and collaboration between scholars from various universities. As a result, the following Table 4 shows the findings that would later usher the researcher into selecting the right articles for content analysis.

Key Settings in Vosviewer for Analysis of Bibliographic Coupling Based on Universities.

With the selection of choices from Vos Viewer, Figure 7 shows the universities that produced knowledge based on Bibliographic coupling based on universities.

Bibliographic network visualization showing bibliographic coupling based on universities.

Subsequently, Figure 8 is presented to reveal the name of the universities more clearly.

Bibliographic density visualization showing bibliographic coupling based on universities.

As a brief explanation, the bibliometric analysis using bibliographic coupling based on universities has revealed that Southwestern University of Finance And Economics, Peking University, and Renmin University are prominent organizations that published subjects of financial education concerning other fields of studies.

Bibliographic Coupling Based on Authors

5. Based on the same data mined from the Web of Science, what is the pattern of bibliographic coupling based on authors?

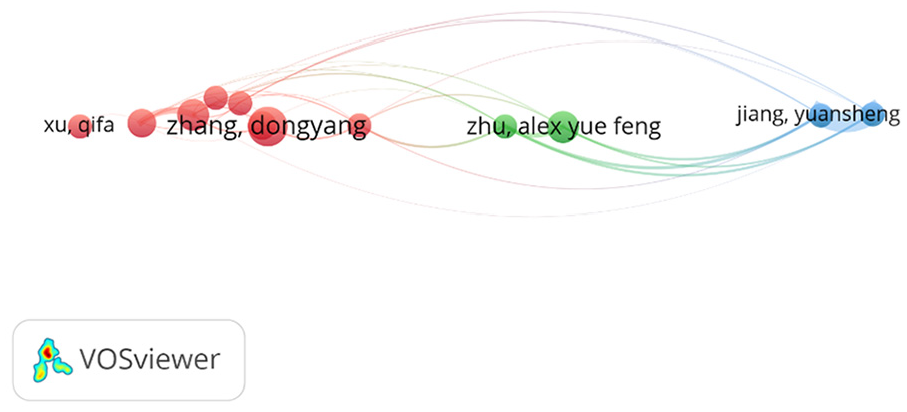

Bibliometric analysis is also conducted by the researcher to investigate bibliometric coupling in the body of knowledge. With the data downloaded from the web of science, the researcher refines the search to uncover the collaboration between scholars in China. As a result, the following Figure 9 show the findings that would later usher the researcher into selecting the right articles for content analysis.

Analysis of Bibliographic coupling based on authors.

With the selection of choices from Vos viewer, 12 authors met the requirement of having at least five documents per author from the bibliographic coupling analysis as shown in Table 5.

Key Settings in Vosviewer for the Setting of Thresholds for Analysis of Bibliographic Coupling Based on Authors.

The names of the authors are also shown in the next Figure 10.

Search results from bibliographic coupling based on authors.

The result of the network analysis is shown in Figure 11.

Bibliographic network visualization showing bibliographic coupling based on authors.

Subsequently, Figure 12 is presented to reveal the authors’ names and their network linkages.

Bibliographic density visualization showing bibliographic coupling based on authors.

With further analysis, it was found that scholar Alex Yue Feng Zhu (Lingnan University, Hong Kong, China) specializes in aspects of personal finance education, financial counseling, and youth studies, while Zhang Zongyang (Beihang University, China) specializes in topics related to green finance, sustainable growth, and corporate governance. Xu Qifa (Hefei University of Technology, China) specializes in studies related to financial risks and investments, financial institutions, investor sentiments, and market volatility. Jiang Yuan sheng (College of Economics, Sichuan Agricultural University, Chengdu, China) specializes in studies related to economics, finance, and the impact on agriculture and the environment. Between these four scholars, it is evident that studies conducted by Alex Yue Feng Zhu from Lingnan University, Hong Kong have the relevance and information that would provide the researcher with the continuity for study, and in the context of China, especially in the topic of personal financial education and literacy.

Bibliographic Coupling Based on Sources of Journals

6. Based on the same data mined from the Web of Science, what is the pattern of bibliographic coupling based on sources of journals?

As the last process of bibliometric analysis, the data downloaded from the web of science prompted the researcher to refine the search by examining the sources of publications. As a result, Table 6 show the key settings in Vosviewer for analysis of Bibliographic coupling based on Journal Sources.

Key Settings in Vosviewer for Analysis of Bibliographic Coupling Based on Journal Sources.

With the selection of choices from Vos viewer, 37 sources met the requirement of having at least five documents per source from the bibliographic coupling analysis.

The result of the network analysis is shown in Figure 13.

Bibliographic network visualization showing Journal Sources.

Subsequently, Figure 14 is presented to reveal the items more clearly.

Bibliographic density visualization showing Journal Sources.

As noticed from the density visualization, the journals that publish on the topic of finance are likely to be Sage Open, Education and Urban Society, and Frontiers in Psychology. The rest of the journals are concerning areas of environmental sustainability, economics, and other technical finance. This analysis has also indicated the potential journals for future publications for this study.

Part 2: Content Analysis

7. Based on content analysis of contemporary articles, what is the state of financial education among Generation Zs in China?

Following the process of bibliometric analysis, the researcher then conducted content analysis on the related papers that describes and explains the state of financial education and literacy in China. With the identification of key authors who wrote in this area, the researcher dives into their writing and highlights the findings of their research about each of the purposes in this paper. As such, the discussion in the following sections will be done according to the coherence and flow of the research objectives.

State of Financial Education Among Generation Zs in China

The bibliometric analysis has led to the identification of articles and Chinese scholars in the field, who have identified the gap between teens’ and young adults’ objective and subjective financial education. Zhu (2021) identifies four levels of financial literacy in a group of teenagers in China: (a) financial literacy overconfidence; (b) financial literacy under confidence; (c) financial literacy competence; and financial (d) literacy naivete. A total of 330 students from six middle schools in Hong Kong, the majority of whom were in the 10th or 11th grades, participated in the survey. According to the findings, adolescents who have an inflated perception of their level of financial literacy are more likely to take financial risks and have a stronger sense of financial control. A randomized controlled experiment was carried out to determine whether or not the gap that exists between individuals’ subjective and objective financial knowledge may be bridged via the use of financial education. Following the implementation of the financial education intervention, there was a significant rise in underconfidence; however, there was no discernible shift in any of the other three categories. Scholars posited that it is common for young people as well as adults to have an exaggerated sense of their level of financial knowledge. Therefore, financial counselors and educators may utilize the findings to assist teenagers in becoming more financially involved (Zhu, 2021).

In addition, recent assessments conducted by scholars have shown that the degree of financial literacy among younger generations is insufficient. Young people need to get financial education while they are still in secondary school since this is the environment in which young people’s financial literacy may be developed most organically. On the other hand, there is a dearth of empirical evidence from randomized research that evaluates the impact of financial education on students in secondary school (Zhu & Chou, 2018a).

As a summary for the first research question, it is evident that existing evidence from China has shown that the state of financial education is still in the infancy stage, and this calls for more local evidence in other parts of China (Durisova et al., 2019; Park & Martin, 2022). As most studies are concentrated in the southern parts of China, the researcher selects and justifies a study to be conducted elsewhere in China, so that it builds on the body of knowledge. On the other hand, the researcher now identifies those efforts that have been carried out previously to label the different levels of financial literacy and thus can be used as a concept to evaluate and measure any financial education intervention so that generation Zs can improve from the level of under confidence to at least confidence level (Birkenmaier & Fu, 2020).

Aspects of Financial Education That Impact the Level of Financial Literacy Among Generation Zs in China

8. Based on content analysis of contemporary articles, which aspects of financial education impact the level of financial literacy among Generation Zs in China?

In the second research question, the researcher carries out content analysis (aided by the bibliometric analysis) to identify the aspects of financial education that would impact financial literacy among Generation Zs. Alongside, it was found that learner characteristics also contribute to the effects of financial literacy. For example, one study was done to determine if the structure of developing adolescents’ financial capacity is comparable to that of developing college students’ capacity and whether adolescence, as opposed to college age, is the better age for objective financial knowledge to trigger the positive cycle of developing adolescents’ financial capacity. The research has also investigated if developing adolescents’ financial capacity is like developing college students’ capacity. The development of financial capability was analyzed using structural equation modeling in their research, which was carried out with the use of a convenience sample consisting of 967 secondary school students from five different schools in Hong Kong. According to scholars, adolescents’ subjective and objective financial information may both be integrated into financial self-beliefs, but only one or the other is necessary. As a direct result, these self-beliefs impact the way they handle their money. The influence of objective financial information on one’s financial self-beliefs was substantially larger for teenagers, even though it had a rather moderate impact on college students. The process of increasing one’s financial capability for teens follows a blueprint that is quite similar to that of college students. Ultimately, when compared to the age of college students, adolescence is the optimal time to acquire objective financial information to begin the process of positively enhancing one’s financial potential (Zhu & Chou, 2018b).

Another study (Zhu, 2019), highlighted that the financial risk tolerance (FRT) of teens is just as important as that of adults; nevertheless, not enough study has been done on the issue in the published literature. Within the scope of his study, factors such as demographic, socioeconomic, psychological, and cognitive variables of Hong Kong adolescents that are associated with FRT have been researched and studied. According to the findings of a survey that was carried out on adolescents, factors such as family income, future orientation, perceived Chinese reading skills, and subjective financial knowledge were found to be positively associated with financial risk tolerance (FRT), whereas financial education experience was found to be negatively associated with FRT. As such, building confidence in one’s knowledge, abilities, and the future may be a more effective strategy for encouraging adolescents who come from poor families to take financial risks when deciding on significant life paths than would be focusing on improving one’s objective cognition. These findings suggest that building confidence in one’s knowledge, abilities, and the future may be more effective than improving objective cognition.

Alternatively Zhu and Chou (2018a) investigated through a phone survey of 958 workers in Hong Kong who were between the ages of 25 and 64 the relationship between retirement savings, needs estimation, and the amount of self-reported private retirement savings amassed by working-age adults in Hong Kong, China. More specifically, this investigation focused on the role that retirement saving needs estimation plays as a mediator between the clarity of retirement goals and the amount of private retirement savings. The scholars found that the estimation of retirement saving needs was associated with the savings of individuals over the age of 44; in addition, it mediated the association between retirement goal clarity and self-reported private retirement savings. Their results give theoretical additions to existing conceptual frameworks for financial planning, as well as policy consequences.

In summary for the second research question, it is evident that existing evidence from China has shown that financial education should aim to build confidence in one’s knowledge, and abilities and the future may be a more effective strategy for improving adolescents’ financial literacy (Aulia & Baskoro, 2019; A. Ghadwan et al., 2022; Naufaldi & Baskoro, 2019). In addition, China’s academic research suggests that teenagers’ subjective and objective financial knowledge may both be incorporated into their financial self-beliefs, and it has a direct bearing on the way people manage their financial resources. Financial education is an important aspect to shape one’s financial goals clearly so that one can plan financially for the future (Zhu et al., 2021).

Improvements to Address the Challenges Regarding Financial Education to Improve the Level of Financial Literacy Among Generation Zs in China

9. Based on content analysis of contemporary articles, what are the improvements to address the challenges regarding financial education to improve the level of financial literacy among Generation Zs in China?

Scholars in China have also highlighted that a multi-faceted concept, financial literacy includes not just information but also attitudes, habits, and overall well-being about one’s financial situation. One vital finding from China is that increasing the level of financial literacy among young people enables these individuals to attain financial autonomy and break the cycle of generational poverty. The researchers conducted a randomized study with 270 Hong Kong secondary school kids who were in the equivalent of the ninth grade in the United States. The results of structural equation modeling (SEM) demonstrated that objective financial knowledge, financial attitudinal variables, and financial well-being variables could converge into the latent construct of financial literacy. On the other hand, all financial behavioral variables converged into another latent construct that was referred to as financial behavior. It is important to note that the two latent constructs were not significantly correlated with one another. The findings of the SEM also showed that the scholars’ financial education program greatly enhanced financial literacy, but in the short run, it did not have a meaningful influence on financial behavior. These results complement the research that has already been done on financial literacy by allowing for a more precise assessment and describing the near-term consequences of financial interventions in young people while they are in the teenage stage (Zhu et al., 2021).

In summary of the last (or the education research question, it is notable to highlight those strategies of improvement and interventions in financial education should have clear measurable concepts and dimensions so that more information could be unearthed to understand the real state of financial literacy of youths in China. As Generation Z is also prominent in China’s socio-demographic composition and background due to a lack of study about them, they are a potential population for a continuation of study for future research (Lingyan et al., 2021; Wang et al., 2011).

Discussion

In contemporary times, financial education has gained significant importance owing to the intricate nature of the current financial system (Brausch, 2018). This is particularly relevant for the new generation, such as Generation Zs in China, who are at the nascent stages of their financial expedition. The exploration of current condition of financial literacy among this unique generation investigates how giving financial education might favorably affect their degree of knowledge in this subject (Stolper & Walter, 2017). Additionally, this study has also delved into plausible solutions aimed at mitigating challenges associated with financial education.

As shown from the bibliometric analysis, the current status of financial literacy in China is currently at a nascent stage, with only a few empirical studies available to assess its influence on secondary school students (Goyal & Kumar, 2021). Despite certain Chinese schools introducing financial education as part of their curriculum, there exists a significant gap in the knowledge of young individuals since many institutions do not provide this instruction (Szymkowiak et al., 2021). Moreover, the educational system in China prioritizes academic accomplishments over essential life skills like financial literacy. Also, a considerable number of Chinese youths are deficient in the essential knowledge and competencies required to proficiently handle their financial matters (Ho & Lee, 2020). Consequently, they may experience monetary distress, increasing the likelihood of making imprudent financial choices or being exploited by dubious financial service providers.

From recent studies, the subject of financial education has indicated that providing financial education to young individuals can yield favorable outcomes in terms of their financial behavior (Lusardi (2019). Nevertheless, it is imperative to acknowledge that the influence of financial education is not consistent across all cases. The efficacy of initiatives aimed at financial education can be influenced by a range of elements such as the caliber and applicability of the curriculum, how it is delivered, and the characteristics of the target audience (Kaiser et al., 2022).

As implications from this study, future improvements are needed to confront the obstacles pertaining to financial education. For example, it is imperative to possess a distinct and quantifiable comprehension of the principles and aspects that constitute financial literacy. This approach will lead to a more accurate evaluation of the efficacy of financial education initiatives as well as appropriate allocation of resources (Compen et al., 2019). Furthermore, financial education interventions should be tailored for their intended audience. For example, integrating financial education into diverse academic subjects, such as mathematics or economics, could be a promising avenue for enhancing financial literacy. This approach would offer a comprehensive perspective on financial matters and guarantee that students receive consistent exposure to financial concepts across their educational journey. Moreover, it is also imperative to conduct regular evaluations of financial education interventions to ascertain their efficiency and assess the need for any modifications. This evaluation process should be extended over a prolonged period to determine the enduring influence of financial education on the youth (Zhu et al., 2021).

In a nutshell, this current research was conducted to explore and describe the knowledge base regarding the financial literacy of Generation Zs in China. Despite the increasing significance of financial education further investigation is required to gain a more comprehensive understanding of the financial knowledge, attitudes, and behaviors of this age group (Lambert et al., 2022). Also, it is imperative to conduct further research with regards to determining the most efficacious strategies for imparting financial knowledge to individuals belonging to Generation Z. This entails identifying the delivery modality that yields the highest impact, the key financial concepts that necessitate coverage, and devising tailored financial education interventions that cater to the distinct requirements of various demographic cohorts (De Jesus, 2020).

Limitations of Study

As mentioned earlier in the methodology, bibliometric analysis is a quantitative approach to assessing the output of authors or publications, although it has limits in terms of analysis. For example, bibliometric measures such as the h-index or the number of times a work has been referenced give one kind of insight into the reach and impact of work, but they are not always precise and complete owing to how research is conducted and how academic publication works (York University Libraries, 2023). Furthermore, measurements may be manipulated or abused by researchers to falsely overestimate their impact (The Open University, 2023). Furthermore, research has indicated that it takes at least 2 to 3 years after publication for manuscripts to gather enough citations for bibliometric indicators to be reliable (Belter, 2015). Also, the metrics discriminate between what is and is not referenced, rather than what is necessary of high quality (The Open University, 2023; UCL, 2018).

In this study, the authors do not include the analysis of the h-index or manipulate the impact readings because datasets from the Web of Science were taken in-situ. Alternatively, the datasets were downloaded beyond 3 years (2018–2022) to address the said weakness above. Nevertheless, this study considered all publications that are found in the body of knowledge as important to point out the patterns and directions of research across multi-disciplines. In addition to the said limitations of bibliometric analysis, the authors have to scope the entries of the key word(s) in Web of Science thoughtfully that fall within the context of Generation Z in China but are not limited to a particular field of study. While this study acknowledged that no amount of key words will ever be sufficient to cover the subject of investigation, the authors complimented this weakness by depending on content analysis on several highly cited papers, as the other method of inquiry to support the visuals that are produced from the bibliometric analysis. As a result, it is hoped that the existing body of knowledge can be further understood on the recent trends and direction of research in the context of China.

In a summary, this study has yielded evidence from the body of knowledge regarding the link between financial education and financial literacy in recent years (2018–2022). When compared with earlier empirical evidence around the world, it is clear that both subjects have received inadequate attention during the last decade (Lusardi, 2019; Mitchell & Lusardi, 2015). This is shown by poor levels of financial literacy across nations, which are linked to inefficient spending and financial planning, as well as costly borrowing (Lusardi, 2019). Financial fragility and a lack of understanding of the underlying linkages between literacy, education, and behavior have been cited as major contributors to this problem (Centeno, 2022; Hii et al., 2022; Hung et al., 2009).

In terms of the study context, financial education is critical for China’s Generation Z, since they have the lowest financial literacy of any generation (University George Washington, 2021). This lack of financial knowledge may lead to bad judgments on money management and investing. According to Chinese research, financial literacy has a considerable impact on the portfolio diversification of family wealth (Peng et al., 2022).

In China, Generation Z has distinct ideals and attitudes about money from earlier generations. They are more inclined to lead green and healthy lives and are less concerned with cost when making purchases (Yu, 2022). Traditional Chinese culture, on the other hand, continues to play a significant part in their upbringing and education, which might impact their views about money (Wong, 2021). Therefore, Generation Z in China must obtain proper financial education so that they can make educated financial choices. This will enable them to construct a solid financial future and make the most use of their resources.

Conclusions

Financial literacy is crucial for the fiscal stability of young individuals, including those belonging to Generation Z in China. Nevertheless, the progress of financial education in China is still at a nascent stage that requires further investigation and enhancements in the implementation and execution of financial education programs. Although it can enhance financial acumen, financial education cannot solely overcome systematic hindrances obstructing financial literacy. This study was carried out to explore and explain the patterns of data from the body of knowledge, mainly from the Web of Science using bibliometric analysis. Before starting the process of analysis, a literature review was conducted to set the stage for this analysis by examining two broad topics: (a) the Impact of Financial Education on Financial literacy on Gen Z; and (b) Challenges to financial literacy among Gen Z. It is reasoned that the exploration in this area would help readers to understand the scope of our studies that is to address personal financial planning through improvements of financial education and literacy among Gen Z. Hereafter, the problem statement was presented to usher in the need for bibliometric and content analysis to investigate if the body of knowledge is heading toward this direction. If it did not, then it is evident that there is a gap for future research. In terms of purpose and methods are chosen, it is hoped that readers may understand that it is not exhaustive and that this study posits the first need in this research design should concentrate on the body of knowledge concerning the context of the study.

From the bibliometric and content analysis, this paper has highlighted that financial education and financial literacy have received insufficient attention in the existing body of research since it has been under-researched. The relationship between the two concepts needs to be ascertained for future research, especially when concerning the dimensions within financial education, and other personal or environmental factors that could affect this relationship (Kim & Stebbins, 2021). In terms of the significance and impact of this study, young people need to get financial education while they are still in secondary school since this setting is the atmosphere in which young people’s financial literacy may be developed in the most organic manner (A. S. Ghadwan et al., 2022). Other factors that should be considered in future studies should consist of demographic, socioeconomic, psychological, and cognitive variables that are associated with financial risk tolerance (FRT) (Zhu, 2019).

In conclusion, the explanation of examples and recommendations to explain between financial education and financial literacy among Generation Zs has been presented as an overview in this proposal with the facilitation of bibliometric and content analysis. Exploring financial service providers and the perspectives of their Generation Zs consumers have provided further benefits and solutions from this research for stakeholders and policymakers (Mondres, 2019). Other studies have speculated reported that people who participate in a financial education program are more likely to have the knowledge and abilities to deal with their financial challenges (Hafni et al., 2020). As such, faculties that teach financial education, academic research, and financial literacy awareness can readily be included into future programs after this study.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.