Abstract

Campus loans have become a part of the lives of Chinese college students. While such loans are convenient for students, they can also create considerable difficulties. In the context of unbalanced economic development between Western and Eastern China, this study aimed to understand the factors affecting the campus loan behaviors of college students in Western China. A sample of 568 undergraduate and graduate students from four universities in Western China was taken as the research object. Binary logistic regression and orderly logistic regression were used to study campus loan consumption factors. Students without state-subsidized loans were found to have stronger campus loan consumption intention and higher loan amounts, and recreational consumption was the main loan purpose. The factors affecting campus loan consumption included students’ family structure, parents’ education level, peer students’ consumption status, grade level, relationship status, and ability to assess loan risk. Based on the findings, suggestions are made for managing campus loan behavior from the perspectives of the individual, family, school, and government. This study can provide guidance for standardizing campus loans and adjusting college students’ consumption attitudes and behaviors.

Introduction

In China, the campus loan (also known as an online loan for college students) is a special type of credit provided to college students by lending institutions to cover students’ studies, living expenses, and other financial needs. Campus loans arose based on both a rising demand for loans by students and the emergence of online loan platforms. The student loans outside of China have mainly used to examine tuition assistance for students from low-income families. This is fundamentally different from the type of “consumer loan” discussed in this study. Strictly speaking, this type of “campus loan” is not found outside of China.

State-subsidized student loans are loans from Chinese banks intended to assist college students from poor families. These loans are led by the government and are jointly operated by banks, educational administrative departments, and colleges and universities. State-subsidized student loans began in 1986 in China with small loans administered by colleges and universities, which were required to be paid off before graduation (Shen & Li, 2003). With increased enrollment in higher education and expanded economic development, in 1999, the government reformed higher education financing, establishing a loan repayment period of 4 years after graduation. However, as a result of high loan thresholds, an imperfect credit investigation system, and the increased social mobility of college students, there were many defaults, which were ultimately repaid by the government.

The Development of Campus Loans

In 2004, China Guangfa Bank started to issue credit cards to college students. This opened the door to credit consumption by college students, and the market rapidly expanded. However, the resulting spike in bad debt prompted the China Banking Regulatory Commission to suspend the issuance of commercial credit cards to college students. The lending market subsequently filled the resulting financial gap. Later, in 2013, with the rise of online financial consumption, college students’ strong online loan consumption potential attracted many online loan platforms to promote their services on campuses.

These “campus loans” have had both positive and negative effects. On the positive side, online lending products such as Jingdong IOUs and Ant Credit Pay have filled the lending gap for college students while also promoting the development of financial technology in China. Moreover, the high efficiency of the loan platforms, which involve simple approval procedures, fast repayment, and low thresholds, makes it easy for college students to borrow money.

Meanwhile, regarding the negative effects, legislation currently lags behind the development of campus loans, and regulations are therefore relatively loose for campus loan platforms. Moreover, the credit investigation system is imperfect, and college students generally lack financial knowledge and experience. As a result of inadequate supervision, diverse forms of business have emerged, giving rise to intense competition, which has hindered the reasonable development of the campus loan business. In the past few years, 66% of online loan platforms have either closed or have become problematic (He & Jia, 2018). Meanwhile, students easily fall into a debt trap. Loan platforms sometimes adopt malicious practices, including high interest rates on very large loans; some even threaten students’ lives and their information security.

In response to such problems, in April 2016, the Ministry of Education of China and the China Banking Regulatory Commission issued the Notice on Strengthening Risk Prevention and Education Guidance for Bad Online Lending on Campus. This was followed in 2017 by the Notice on Further Strengthening the Standardized Management of Campus Loans. These measures aimed to strengthen the regulation of campus loan platforms, adjust students’ concepts of consumption, and gradually contain the rising trend of problematic campus loans.

Nevertheless, online loan consumption has expanded drastically among college students. According to a 2019 report by Nielsen (China’s Youth Debt Status Report), 86.6% of young Chinese were using online loans, and 44.5% were materially indebted. Moreover, the 2017 China Online Lending Industry Research Report by iResearch projected that the number of online loan users in China would exceed 300 million in 2020. As shown in Figure 1, the number of online loan users in China is expected to continue to grow at an average annual rate of more than 10%. Furthermore, according to the 2017 Consumer Life Report of Young People by Ant Check Later (one of China’s largest online loan platforms), the post-1990s generation of college students accounted for 47.25% of the total number of online loan users, and nearly 40% chose online loans as their preferred method of payment.

2013 to 2020 online loan user scale in China.

Campus loans began to draw widespread attention in 2016 when a student in Henan Province committed suicide because he was unable to repay a 600,000 yuan loan. In another incident that year, it was discovered that multiple female college students were offered loans in exchange for nude photos. Victims of the scheme included students from 25 universities. Most came from economically underdeveloped third- or fourth-tier cities, and many were from rural areas.

Such problems highlight the need to further study the factors affecting the campus loan behaviors of college students in economically underdeveloped areas in Western China. Such work can help to provide suggestions for constraining illegal campus loans. While many studies have investigated the factors affecting college students’ online loan behaviors, this study specifically focused on students in Western China. In this way, this study aims to help promote benign consumption among college students. It also has reference value for families, governments, and universities.

The rest of this article is organized as follows. The next section reviews the relevant literature. The third section describes the data sources, while the fourth section explains the methods. Then, the results are presented and analyzed. The last two sections discuss and conclude the study.

Literature Review

In recent years, domestic researchers have investigated campus loans from multiple perspectives. Di (2019) explored the reasons for the emergence of bad campus loans and proposed corresponding countermeasures. Based on 486 questionnaires administered at six universities, Zhang and Yu (2018) analyzed the status of campus loans and their associated problems, as well as students’ coping strategies. Lv et al. (2018) analyzed campus loans at universities in Shandong Province and proposed risk-reduction measures based on synergies among the government, universities, enterprises, and families. Meanwhile, some researchers have proposed using strict legal regulation to curb the bad loan situation. Wu (2017), for example, proposed ways of using legislation and law enforcement to solve the problem of campus loans. Li and Zhao (2017), meanwhile, examined the educational guidance and risk-prevention mechanisms of campus loans.

Other studies have analyzed the factors affecting campus loans. Based on a survey of college students in Henan Province, Yang & Wang (2019) found that campus loan behavior was influenced, in decreasing order from strong to weak, by personal behavior, lifestyle, and consumption desire. Meanwhile, based on a survey of 286 college students from four universities in Beijing, Hao et al. (2019) found that campus loan demand was positively related to years of schooling, monthly living expenses, financial support from the university, and consumption preferences. However, parents’ level of education, college major, and advertisements were found to have negative effects on campus loans.

Although the campus loan has no precise equivalent outside of China, credit card use has a much longer history in Western countries than in China. Therefore, this study also considered nondomestic research on credit card consumption, credit card debt, and student consumption psychology and behavior. Such studies have important reference value for the present research.

Regarding research on students’ credit behaviors, Danes and Hira (1987) found that student characteristics (e.g., gender, grade, income, marital status) significantly affected credit behaviors. For example, students with better financial knowledge had stronger control over their use of credit cards. Senior-level students tended to use credit cards more frequently, and those with more work experiences had higher credit card utilization as well. Based on 784 sample data, Santos et al. (2016) found that female college students’ financial confidence affected their credit card behavior. Hancock et al. (2013) found that students’ credit card behaviors were mainly influenced by their parents’ financial knowledge, work experience, attitudes toward credit cards, and personality, thus highlighting the important role of families in credit behavior.

Other studies have explored the factors affecting students’ credit card debt. Robb and Sharpe (2009) found that educational background was directly proportional to debt scale, and students with financial knowledge were more tolerant of debt. The authors noted that students must accept a certain amount of debt to maintain a certain lifestyle. J. F. Wang and Wallendorf (2005) explored the reasons for overdraft consumption among American college students, the influencing factors, and solutions to the problem. They found that college students’ overdraft consumption was mainly influenced by social relations, personal values, material temptation, and peer pressure. Serido et al. (2015) found that those with greater social support were less likely to have credit card debt and that students’ financial behaviors were influenced by the financial behaviors of their parents, friends, and partners. J. J. Wang and Xiao (2010) found that compulsive buying behavior had a significantly positive effect on credit card debt among university students, while impulsive buying behavior might have also had a positive effect.

Regarding students’ consumption psychology and behavior, Penman and McNeill (2008) analyzed the credit card use and repayment attitudes of college students. They found that college students were susceptible to social pressure, and their consumption was based more on desire than need. Moreover, the external condition of loan convenience intensified impulsive debt consumption. Investigating mobile phone consumption among university students in Turkey, Acikalin and Develioglu (2009) found that purchase behaviors went beyond the scope of need and were often based on the psychological need to display social status. Hayhoe et al. (2000) found that a favorable credit attitude was positively related to the purchase of leisure goods among college students. Kiyici (2012), meanwhile, found that students who majored in education, had greater monthly stipends, and had more internet self-efficacy had positive attitudes toward and intentions to shop online. Furthermore, those who had credit cards had more familiarity with and less anxiety about internet shopping. Shim et al. (2010) found that students’ previous consumption ideas and patterns would often change during their university studies, and their subsequent consumption behaviors later in life would change accordingly. Thus, it can be said that helping college students form healthy attitudes about consumption through education and guidance is important.

Three shortcomings can be identified in the existing research. First, the research objects have been broad, mainly targeting youth groups, with few specifically studying enrolled students. Second, most studies have focused on traditional credit card lending, whereas studies on the factors affecting campus loan behavior have been rare or incomplete. Third, existing campus loan studies did not involve universities in Western China. This study therefore deepens the investigation and analysis of the factors affecting campus loans by studying college students in Western China. Specifically, this research contributes to the literature in the following ways. First, the data came from Western China, where economic development is relatively slow. Second, this study introduced factors measuring students’ socioeconomic backgrounds, such as their hometowns, whether they have state-subsidized loans, and whether students from poor families are recognized by their schools. Third, this study combined factor analysis and logistic model analysis to make the results more reliable.

Sample Data

The sample for this study included undergraduate and graduate students from LanZhou University, Northwest A&F University, GanSu Agricultural University, and Yangling Vocational and Technical College in Western China. The students were at various different stages in their studies (Year 1–4 for undergraduate students and Year 1–3 for graduate students). They came from different departments, including sciences, agriculture, engineering, economics, humanities, social sciences, and fine arts. These four universities were chosen because they are comprehensive universities, and the sample covers a wide range of students, which can improve the representativeness of the sample. Second, these four universities have a higher number of students from Western China because of their proximity to the students’ hometowns.

Questionnaire

The questionnaire has four parts. The first part covers basic information about the students, including personal and family information. The second part concerns students’ consumption status in relation to campus loans, covering aspects such as consumption structure, level, values, and channel changes. The third part covers students’ online loan use. The questions pertain to student’s knowledge of and attitudes toward campus loan products, their use of campus loans, their reasons for campus loan use, their repayment method, and their quota status. The fourth part concerns students’ understanding of campus loans, including their understanding of campus loan risks. The full questionnaire is included in the Appendix.

Basic Information About the Sample Survey

Eight hundred questionnaires were distributed at the four universities, and 568 valid ones were returned (effective rate: 71%). Table 1 shows the descriptive statistics of the valid questionnaires.

Variable Descriptive Statistics.

Note. The definition of family financial difficulties is whether recognized and registered by the university and college.

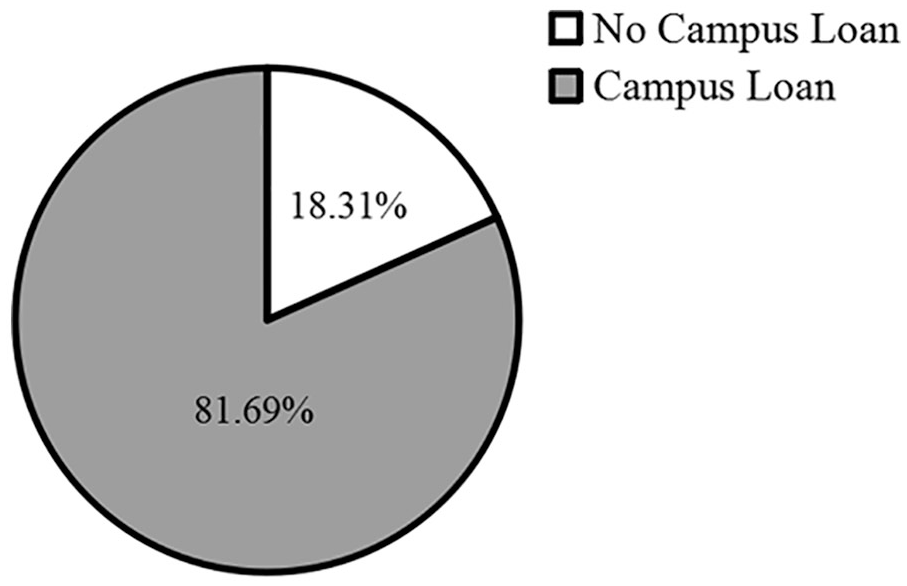

It can be seen from Table 1 that the subjects’ grades and subjects were evenly distributed. In particular, among the 568 samples, 464 students took out campus loans, accounting for 81.69% (Figure 2). A total of 252 students’ families had financial difficulties, accounting for 44.37% (Figure 3). Among the 252 students who came from poor families, 159 had state-subsidized loans, accounting for 63.10% (Figure 4).

The proportion of students with campus loan in the total sample.

The proportion of students with family financial difficulties in the total sample.

The proportion of students with state-subsidized student loan in the total sample.

Research Methods

To ensure the stability of the regression results, this study integrated the influencing factors through factor analysis. Based on the factor analysis results, stepwise regression was used to control the scope of action of the independent variables to test the regression results. Logistic regression was used in the correlation analysis. A binary logistic model is appropriate because the question of whether a student chooses a campus loan is a binary problem. Because the amount and purpose of campus loans are ordered variables, an ordered logistic model is appropriate.

Theoretical Basis and Model Construction

Logistic model

If the probability of an event is p, there are m influencing factors (independent variables):

where

Factor analysis

The basic principle of factor analysis is to group closely related variables into a common factor, and the correlation between different classes is low. Through factor analysis, the factors affecting the research problem can be integrated.

Variable Selection and Assignment

The factors for college students choosing campus loan consumption mainly include personal factors, family factors, consumption status, and risk perception. Table 2 shows the specific variables and variable assignment.

Variable Description of the Model.

Results and Analysis

Regression Analysis of the Binary Logistic Model

A binary logistic model was used to analyze the campus loan consumption intention of college students in Western China. Campus loan consumption intention is the dependent variable. The independent variables are gender, grade, subject, household registration, family financial difficulties, state-subsidized loan, single child, parents’ education, whether in a romantic relationship, monthly living expenses, monthly living expenses of peer students, and the difference between actual and expected monthly living expenses.

Factor analysis

Kaiser–Meyer–Olkin (KMO) and Bartlett tests were conducted before the factor analysis. The results were KMO = 0.747 > 0.7, and Bartlett p = .000 < .05. These results show that it is suitable for factor analysis. Table 3 shows the rotation component matrix output by SPSS. From the output results in Table 3, it can be seen that Common Factor 1 has a large load on the variables of household registration, only child, and parents’ education; this reflects the basic background of the family. Common Factor 2 has a large load on the variables of state-subsidized loan and family financial difficulties; this reflects the economic situation. Common Factor 3 has a large load on the variables of classmates’ monthly living expenses, reflecting the consumption situation. Common Factor 4 has a large load on the variables of gender and subject, reflecting students’ conceptions of consumption. Common Factor 5 has a large load on the variables of grade and students’ relationship status, which reflect the students’ stage.

The Rotated Component Matrix.

Stability test

To ensure the stability of the regression results, based on the factor analysis results, the stepwise regression method of controlling the scope of action of the independent variables was adopted to test the regression results (Table 4).

Robustness Test of Influencing Factors of Campus Loan Intention.

Significance at 10% levels. **Significance at 5% levels. ***Significance at 1% levels.

From the regression results, the eight variables of only child, parents’ education, state-subsidized loan, gender, subject, grade, relationship status, and expected living expense difference significantly affected campus loan intention. The regression results are stable.

Regression Analysis of Orderly Logistic Model

Based on the same calculation principle, to further clarify the factors affecting campus loan consumption by college students in Western China, ordered logistic regression was conducted for the 464 students who received campus loans, with the amount and purpose of the loans as the dependent variables. The regression results are shown in Tables 5 and 6.

Robustness Test of Influencing Factors of Campus Loan Amount.

Significance at 10% levels. **Significance at 5% levels. ***Significance at 1% levels.

Robustness Test of Factors Influencing the Use of Campus Loans.

Significance at 10% levels. **Significance at 5% levels. ***Significance at 1% levels.

Results and Discussion

The regression results in Table 4 indicate that eight variables had significant effects on the campus loan consumption intention of college students in Western China: only child, parents’ education, state-subsidized loan, gender, subject, grade, relationship status, and expected living expense difference.

Only child had a significant negative effect on campus loan consumption intention. It passed the significance tests of six models, with regression coefficients of −0.462 (p < .1), −0.526 (p < .05), −0.539 (p < .05), −0.605 (p < .05), −0.670 (p < .05), and −0.650 (p < .05). This indicates that the campus loan consumption intention of students from single-child families is lower. The reason could be that families with only one child are in a better economic situation than those with many children. Furthermore, results in Table 5 show that the only-child factor had a positive effect on campus loan amount; its regression coefficients were 0.379 (p < .1), 0.381 (p < .1), 0.355 (p < .1), 0.442 (p < .05), 0.421 (p < .1), 0.446 (p < .05), and 0.421 (p < .05). This means that students who are the only child have higher campus loan amounts. This may be due to their spending habits and demands. In general, although only-child students have a lower intention to take out campus loans, their loan amounts will be high when they do take out a loan.

Parents’ educational background had a significant negative effect on campus loan intention. It passed the significance tests of six models; the regression coefficients were −0.197 (p < .1), −0.269 (p < .05), −0.279 (p < .05), −0.264 (p < .05), −0.258 (p < .05), and −0.269 (p < .05). This means the higher the parents’ educational level, the lower the college students’ campus loan intention. This is consistent with Hao et al. (2019). This suggests that the higher the parents’ educational level, the stronger the family’s economic ability, which means they can basically meet their children’s consumption needs. Furthermore, Model 7 in Table 5 shows that parents’ educational level had a negative effect on campus loan amount (β = −.146; p < .1). In other words, the higher the parents’ educational levels, the lower the students’ online loan amounts. This also suggests that more educated parents pay more attention to their children’s financial management education, consumption education, and economic responsibility education. These students may therefore develop more prudent attitudes about campus loans. This is similar to Hancock et al. (2013) and Shim et al. (2010).

State-subsidized loan had a significant negative effect on campus loan intention. It passed the significance tests of five models, and its regression coefficients were −0.551 (p < .05), −0.523 (p < .1), −0.559 (p < .05), −0.680 (p < .05), and −0.620 (p < .05). This means students with state-subsidized loans are less willing to take out campus loans. This is contrary to the findings of Hao et al. (2019). This could be attributable to different study regions and different consumption concepts and behaviors among students from poor families. In Beijing and other economically developed areas, students from poor families have a greater demand for campus loans because of surrounding consumption levels, consumption concepts, or environmental temptations. However, in less developed regions such as Western China, consumption concepts are more conservative, and consumption levels are far lower than those in Central and Eastern China. Thus, students’ demands for campus loans are lower.

Furthermore, from Models 4, 5, 6, and 7 in Tables 5 and 6, it can be seen that state-subsidized loan had a significant negative effect on the amount and use of campus loans. Its regression coefficients were −0.365 (p < .1), −0.395 (p < .1), −0.403 (p < .1), −0.362 (p < .1), −0.474 (p < .01), −0.440 (p < .05), −0.453 (p < .05), −0.457 (p < .05), and −0.440 (p < .05). This means that students with state-subsidized loans have lower campus loan amounts, and they use loans to pay tuition fees and basic living expenses. This indicates that students with state-subsidized loans in Western China are more cautious about their campus loan behaviors; their consumption philosophy is oriented toward finishing their studies. In addition, Table 5 shows that the influence trend of the family economic difficulty factor is the opposite of the factor of state-subsidized loan. In other words, students from poor families have higher loan amounts, whereas those with state-subsidized loans have lower amounts. This could be attributable to respondents from poor families not applying for state-subsidized student loans.

Gender had a significant positive effect on campus loan intention; its regression coefficients were 0.544 (p < .05), 0.807 (p < .01), and 0.822 (p < .01). This means the campus loan consumption intention of male students is stronger than that of female students. Furthermore, Models 5, 6, and 7 in Table 5 and Models 3, 4, and 5 in Table 6 show that gender had a significant negative effect on the amount and purpose of campus loans. The regression coefficients were 0.356 (p < .1), 0.367 (p < .05), and 0.287 (p < .1) and 0.256 (p < .1), 0.264 (p < .1), and 0.231 (p < .1), respectively. This suggests that male students have higher loan amounts and are more inclined to spend money on things like video games, pop culture consumption, and entrepreneurship. This could be because male students need extra funds to spend on costly products rather than basic consumption, such as mobile phones, game equipment, and other electronics. This result is similar to Davies and Lea (1995). Another possible explanation is that, due to the influence of traditional Chinese culture, male students might be more anxious about achieving success than female students and therefore need more financial support.

Subject had a significant positive effect on campus loan intention; its regression coefficients in Models 4, 5, and 6 in Table 4 were 0.277 (p < .05), 0.217 (p < .1), and 0.205 (p < .1), respectively. Specifically, science students < agriculture students < engineering students < economy students < liberal arts students < arts students. Table 5 also shows that subject had a significant positive effect on campus loan use; the regression coefficients were 0.163 (p < .1), 0.163 (p < .1), and 0.185 (p < .05). In terms of the amount of campus loans, science students < agriculture students < engineering students < economy students < liberal arts students < arts students. This is consistent with the results for the loan intention factor. This could be because students from poor families in Western China are more likely to choose majors such as agriculture, science, and engineering, with lower tuition fees and better job prospects. In that case, they are less willing to apply for campus loans and have lower loan amounts. This is the opposite of the findings in Hao et al. (2019).

Grade had a significant positive effect on campus loan intention; its regression coefficients were 0.360 (p < .01) and 0.379 (p < .01). This indicates that the higher the grade, the stronger the campus loan intention. Furthermore, Table 6 shows that grade had a significant positive effect on campus loan amount; its regression coefficients were 0.289 (p < .01), 0.290 (p < .01), 0.294 (p < .01), and 0.285 (p < .01). This shows that the higher the grade level, the higher the loan amount. We can assume that senior students’ consumption psychology and behavior tend to be more mature and stable. They require more financial support because of their social lives and other personal needs. This is similar to Hao et al. (2019), J. J. Wang and Xiao (2010), and Baum (2016).

Students’ relationship status had a positive effect on campus loan intention; its regression coefficients were 0.860 (p < .01) and 0.850 (p < .01). This means students who are in a romantic relationship are more likely to choose campus loans. This may be because students in romantic relationships are more prone to impulsive consumption, resulting in additional consumption beyond basic daily consumption. In addition, influenced by traditional Chinese concepts and vanity psychology, men are expected to pay for dating expenses. To some extent, this further supports the finding that male students are more likely to take out campus loans.

The difference between actual and expected living expenses had a positive effect on campus loan intention; its regression coefficient was 0.770 (p < .01). This shows that the greater the difference between actual and expected living expenses, the stronger the intention to take out a campus loan. This may be because actual living expenses can only meet daily basic consumption needs. Once they adopt a consumption psychology of keeping up with others, they will have higher living standard requirements (e.g., for electronic products, cosmetics, or clothing). This finding is similar to that of J. J. Wang and Xiao (2010).

Furthermore, Table 5 shows that monthly living expenses and peers’ monthly living expenses had a significant positive effect on campus loan amount. The regression coefficients were 0.359 (p < .01), 0.310 (p < .01), 0.300 (p < .01), 0.284 (p < .01), 0.320 (p < .01), 0.233 (p < .05), 0.309 (p < .01), 0.293 (p < .05), 0.297 (p < .05), and 0.292 (p < .05). This means the higher the monthly living expenses of students and their peers, the higher the loan amount. This result aligns with the findings in Lachance (2012) and Penman and McNeill (2008) regarding the influence of peers on consumer choices and behaviors.

Repayment mode had a significant positive effect on campus loan amount. Table 5 shows that the regression coefficient was β = .774, p < .05. Estimated repayment ability had a significant negative effect on loan amount; the regression coefficient was β = −.525, p < .1. That is, the more clearly the campus loan repayment method is understood, the higher the campus loan amount; the loan amount is also higher for students who do not clearly estimate their repayment ability. We suggest that students’ risk perceptions of campus loans lead to the polarized trend in campus loan amounts. On one hand, if students can fully evaluate their repayment abilities and rationally use credit, they will undertake rational consumption. On the other hand, if they do not understand the risks of campus loans and cannot correctly evaluate their repayment ability, they will engage in blind loan consumption, more easily leading to a debt trap.

In addition, Tables 4, 5, and 6 show that household registration had no effect on college students’ campus loans. This suggests that it is not the urban or rural environment that affects students’ campus loan use. Rather, it is affected by consumption habits, family economic conditions, parents’ education, and risk cognition.

Conclusion

This study found that the main factors affecting the campus loan behaviors of college students in Western China were students’ consumption status, family circumstances, personal characteristics, and ability to evaluate risk.

Regarding students’ consumption status, in general, as the loan amount increases, the purpose of the loan gradually changes basic consumption to recreational consumption. Students without state-subsidized loans are more likely to use campus loans and with higher amounts. Furthermore, the greater the difference between actual and expected costs of living, the stronger the willingness to use campus loans. Also, the higher the monthly cost of living for students and their peers, the higher the campus loan amount.

Regarding students’ family circumstances, a non-only child is more likely to take out campus loans. However, once an only child chooses to use a campus loan, the loan amount is higher. Furthermore, the higher the parents’ education, the lower the student’s willingness to use a campus loan and the lower the loan amount.

With regard to students’ personal characteristics, males are more willing to take out campus loans than females, and the loan amount is higher. Males are more inclined to spend money on games, idle consumption, and business. This is also consistent with the conclusion that male students in a relationship are more likely to choose campus loans (in traditional Chinese culture, males in relationships are more inclined to pay dating expenses).

Regarding students’ ability to evaluate risk, students who understand risks, such as the means of repayment, have higher loan amounts. Meanwhile, those who do not understand risks and do not clearly consider their repayment ability have higher campus loan amounts.

Implications and Suggestions

This study’s findings suggest that the campus loan is a double-edged sword. On one hand, it meets students’ needs by providing necessary financial support. On the other hand, due to its rapid development and potential risks, there are considerable hazards for students. Based on the survey results, we can make suggestions for individuals, families, schools, and governments.

From the perspective of students, their consumption behaviors are closely related to their campus loan behaviors. In the questionnaire, 70.69% of students chose a repayment method that deducted from the next month’s living expenses. Regarding campus loan use, online shopping accounted for 57.97%, in which clothing consumption accounted for 55.02%. This suggests that while college students have no repayment ability, they tend to spend more than they can afford. The findings also indicated that student consumption is greatly influenced by other students around them. They tend to follow trends and compare themselves with others. Therefore, given the convenience of campus loans, they can hardly resist the temptation.

Furthermore, only 0.87% of students believed their learning level had improved after taking out a campus loan. Meanwhile, 42.26% indicated improvements in terms of basic living, entertainment consumption, social life, and financial management concepts. However, 48.15% of students said their lives had not significantly changed after taking out a campus loan. This is similar to Joensen and Mattana (2017), who found that loans had no significant effects on dropout rates and graduation rates.

In light of the above, we suggest the following: First, students should pursue self-education, cultivate good consumption habits, and not let marketing “define” their lives. Second, it is necessary to strengthen the awareness of campus loan risks, establish awareness of privacy protection, and pay attention to personal information security. Third, it is necessary to strengthen legal awareness and integrity concept, learn to treat campus loans rationally, and clearly understand the law and how to protect rights and interests after getting into a debt trap.

Regarding families, family education and economic status are closely related to students’ campus loan behaviors. In the questionnaire question “why you have never used campus loan products,” 49.04% of students indicated they have adequate funds and no need to use campus loans and 27.88% of students indicated they are influenced by their parents’ educational concepts. Therefore, parents should seek to be good role models in daily life. They should also aim to cultivate good concepts regarding consumption, financial management, and risk awareness.

From the perspective of colleges, there is a serious lack of online loan education for students. In response to the question “Does your university take measures regarding the phenomenon of online loans?” only 6.25% of students said their schools offered relevant financial courses. Meanwhile, 28.45% said there were no such measures in their schools, and 36.21% said their schools provided lectures on online loan safety. Finance-related courses are typically only offered to economic management majors, whereas students in other majors do not receive much education regarding financial risk. Although there are reports warning about online loans, there is a lack of targeted guidance and education for students. Colleges and universities should therefore aim to provide basic knowledge regarding finance and law. They should also guide students to adjust their consumption attitudes and habits and improve students’ understanding of rules and laws. In addition, colleges and universities should establish access and supervision mechanisms to strengthen the standardized management of campus loans. For example, online loan platforms entering campuses should specify the qualifications of their employees. Meanwhile, schools should strictly examine and supervise lectures and advertising related to credit to keep students from receiving false and misleading information.

Meanwhile, colleges and universities currently only offer state-subsidized loans to students from poor families. This fails to meet the personalized and diversified financial needs of students seeking a better life in the context of China’s current socioeconomic development. Therefore, in terms of financial aid, colleges and universities should broaden the types of financial aid offered by providing differentiated and diversified services to students based on their needs and actual conditions. This can include establishing start-up funds for students who want to start their own businesses. The purpose is to keep college students from seeking out online loans and then falling into a debt trap.

With regard to government, government departments should play a stronger role in campus loan regulation and publicity. In the questionnaire question “What do you think is the most urgently needed measure for the campus loan phenomenon,” 51.08% of students said the government should strengthen supervision and further regulate the campus loan market. It was found that students knew little about the Notice on Strengthening Campus Bad Network Lending Risk Prevention and Education Guidance, issued by the Chinese Ministry of Education and the China Banking Regulatory Commission. They were also unaware of the Interim Measures for the Management of Business Activities of Online Lending Information Intermediaries. The government is currently in the early stage of developing legal supervision regarding campus loans (the contract signing and contract fulfillment of campus loan are only the loan relationship between the platform promoters and college students without effective supervision). Therefore, it is suggested that the government should establish a long-term mechanism for establishing laws related to campus loans. Furthermore, new laws should be enacted to refine the special provisions in the field of campus finance. The government should stipulate the procedures for campus loans, including auditing, lending, and receiving procedures. It should also establish and improve the benign competition mechanism in the field of campus finance. Finally, the government should improve judicial relief, set up a campus loan dispute hotline, and establish channels for mediation and arbitration related to campus loan disputes. Such support can address the difficulty of providing evidence, the high costs, and the long time periods. In this way, the government can more effectively protect the rights and interests of college students.

Footnotes

Appendix

An Investigation of College Student’ online loan Consumption.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research and/or authorship of this article.