Abstract

Existing literature on relationship between financial development (FD) and economic growth (EG) has presented dichotomous observations: a linear relationship by many of the studies and yet an inverted U-shaped relationship observed by number of renowned researchers. Most of the studies used narrow measures like credit to GDP growth ratio for measurement of financial development. Moreover, many of the researches have taken only the post-Global Financial Crisis data or neglected the data pre-1990s and most of the researches related to developing countries are on single-country data. Therefore, this relationship requires re-estimation to arrive at some conclusive results. This paper explores the relationship between financial development and economic for both developed and developing countries based on broader measures of financial development (financial access, financial depth, and financial efficiency). Panel Corrected Standard Error regression model is used to evaluate the relationship for 23 developed and 35 developing countries. Our results observe contrasting facts for developed and developing countries. For developed countries, we observed an inverted U-shaped relationship between FD and EG. The contributing sub-components of FD are financial depth and efficiency. However, financial access is observed to have a U-shaped relationship. However, for developing countries, we don’t observe an inverted U-shaped relationship but linear relationship between FD and EG. The contributing sub-components are financial depth and financial efficiency.

Keywords

Introduction

Financial development has indeed been established as one of the most significant contributors to the economic growth (Schumpeter, 1911). Miller (1998, p. 14) remarks that “financial markets’ contribution to economic growth is a proposition almost too obvious for serious discussion.” Financial development leads to the reduction in the cost of financing from external sources and this contributes to the increase in economic growth (Rajan & Zingales, 1998). Levine (2003) further emphasis that more finance would relate to more growth. Financial system development provides choices for liquidity management to firms and can also assist in long-term investments, which eventually reduces the volatility of price, investment and growth. In addition, it stimulates the acquisition and dissemination of information thereby facilitating the process of risk diversification and providing assistance in resource mobilization (Aghion et al., 2010). Taking a sample of sub-Saharan African countries, Ustarz and Fanta (2021) observed that financial development has a positive effect on growth of agriculture and service sectors, but a U-shaped relationship exists for industrial development in these countries.

However, recent studies also show that beyond a certain threshold, the increase in financial deepening leads to the reduction of growth. This phenomenon is called as the “too-much-finance effect” (Rajan, 2005). Financial development unfavourably impacts the economic growth irrespective of the income-group the country belongs to Cheng et al. (2021). Cheng et al. (2021), however, also observed a greater negative effect of increased financial development on growth in the developed economies. Arcand et al. (2012) point out toward non-linearities caused by financial depth. They observed that financial development exerts the negative influence on output growth when the private sector credit becomes equal to or more than 100% of gross-domestic-product (GDP). Aizenman et al. (2015) also find that finance increases growth, but not beyond a threshold point. They also show finance having heterogeneous effects across the sectors of economy.

Many explanations have been proposed for the weakening of the finance-growth nexus, particularly at high levels of financial depth. Cheng et al. (2021) have observed that irrespective of income-level of the countries, financial development negatively affects the economic growth. Though, this negative effect is higher in the high-income countries as compared to middle-income or low-income countries. Cecchetti and Kharroubi (2015) observe negative effects of rapid expansion of finance on allocative efficiency and that it results in crowding out of human capital away from the real sector to rapidly expanded financial sector. A study by Dabla-Norris et al. (2015), while observing the trend of pre-Global Financial Crisis 2008 also suggests a shift of resources in advanced countries from productive sectors of the economy to the financial sector. High-income countries may reach a point at which financial depth no longer contributes to increasing the efficiency of investment (De Gregorio & Guidotti, 1995). Rajan (2005) highlights the dangers of financial development that leads to large and complicated financial systems, which could end up in a “catastrophic meltdown.”Gennaioli et al. (2012) show that financial innovation can increase financial fragility even in the absence of leverage when neglected tail risk is present. Further, the financial fiasco of the Global Financial Crisis 2008 raised questions on raison deter of its genesis. Legitimately, the question also comes on what might have been different for developing and developed countries, as the crisis, per se, largely hit the developed countries. This question becomes increasingly important for the policy makers in the background of divergent views of researchers presented in our discussion so far.

A reasonable number of studies have explored the role of mediating variables on the relationship between finance and growth. These mediating variables have been observed by these researchers as conditions for positive correlation. Among these variables are the thresholds of factors like inflation (Rousseau & Wachtel, 2002; Yilmazkuday, 2011), per capital income and trade openness (Yilmazkuday, 2011), financial policies (Ang, 2008), culture (Stulz & Williamson, 2003), financial openness (Law, 2009), quality of institutions (Law & Azman-Saini, 2012; Law et al., 2013; Law et al., 2017), political institutions (Girma & Shortland, 2008; Huang et al., 2010; Roe & Siegel, 2011), ownership structure of financial institutions (Andrianova et al., 2008; La Porta et al., 2002), financial policies (Abiad & Mody, 2005; Ang, 2008), legal structure and system (La Porta et al., 1997, 1998), and remittances (Demirgüç-Kunt et al., 2011).

This study contributes to the literature in the following ways. First, most of the earlier studies have used a narrow measure of financial development that is, private sector credit as a percentage of the gross domestic product and/or the ratio of stock market capitalization to the gross domestic product (Abdul Bahri et al., 2018; Arcand et al., 2012; Cecchetti & Kharroubi, 2012; 2015; Dabla-Norris & Srivisal, 2013; Deidda & Fattouh, 2002; Law & Singh, 2008; 2014; Rajan & Zingales, 1998). However, recent literature suggests that financial development is a multidimensional phenomenon, and hence requires a move from the usage of single indicator proxies to measure it (Aizenman et al., 2015; Čihák et al., 2012). Financial institution and financial markets define the backbone of financial sectors’ institutional infrastructure. A broader measure of financial development encompassing both financial institutions and financial markets that are based on financial depth, access, and efficiency may, therefore, be more appropriate to examine any relationship involving financial development (Sahay et al., 2015; Svirydzenka,2016). This study uses this broader measure instead of a narrow single proxy measure of development of financial institutions and financial markets. This study would be able to clearly identify as to which sub-component of financial development is responsible for non-monotone relationship between financial development and economic growth. Once, it is identified whether depth, access, and/or efficiency of financial institutions and/or financial markets is contributing positively economic growth, the macro-economic policy makers shall be able to focus those elements for enhanced economic growth. At the same time macro-prudential policy makers shall have a clear view of risks associated with which elements of financial development are needed to be managed. Since, both developing and developed countries are being explored separately, the policy makers for both stream of countries may have clear understanding of this relationship according to their peculiar institutional infra-structures and economic dynamics. Using such a measure also helps in analysing the role played by the individual components that is, financial depth, financial access, and/or financial efficiency. Second, most of the recent studies, especially the post-global financial crisis (2008) is focused either on developing countries or a single country (Abdul Bahri et al., 2018; Karagol et al., 2022; Oro & Alagidede, 2019; Sahay et al., 2015). In this regard, ignoring advanced economies can be counterproductive especially keeping the fact in mind that the global financial crisis originated from advanced economies where financial institutions and markets are well developed. Third, most of the previous research which studied this relation in developing countries utilize a single country setting and their results either lack in consistency or are ambiguous (Akpan et al., 2017; Atindéhou et al., 2005; Karagol et al., 2022; Nkoro & Uko, 2013; Oro & Alagidede, 2019). Onyinye et al. (2023) in a most recent country-specific study has concluded that financial inclusion and financial development has a significant positive relationship with EG in Nigeria.

This suggests the re-examination of finance-growth nexus in developing countries’ context to reach a conclusion convincing enough to be used for policy makers and other stakeholders. Fourth, majority of the studies have considered a limited time span that is, since 1995. Similarly, analysis employing most of the post-Global Financial Crisis has focused on a limited span of data from post-global financial crisis (Abdul Bahri et al., 2018). Extending the sample period from 1980 to 2020 may provide additional insights into financial development-growth literature. This study, therefore, has taken the data from 1980 to 2020.

The remainder structure of this study is as follows: first part reviews the literature to identify the gaps to be filled in this area of research, second part covers the research methodology, in third part we give the empirical results, this followed by part four drawing the conclusions for macroprudential policy formulators.

Literature Review

This research paper first reviews the theoretical literature on finance-growth relationship with a focus on research questions/objectives of our research. Later, it reviews empirical literature related to financial development leading to economic growth, then moves to the empirical literature with added rigor to systematically establish the robustness of this observation. Finally, concluding by a possible menu of factors leading to the introduction of vulnerabilities during the process of higher levels of financial development. The last part of the paper shall present the potential avenues for further exploration in future.

Impact of Finance on Economic Growth: Theoretical Literature

Two well-known hypotheses, demand-following and supply-leading, have explained the relationship between financial development and growth. Direction of the relationship has been under observation; demand-following hypothesis suggesting the direction of relationship from economic growth to financial development, whereas the supply-leading hypothesis suggesting a direction of causation from financial development toward economic growth (Patrick, 1966). An expansion in real economic activity results in growth of finance due to subsequent increase in demand for financial sector services. This is what Robinson (1952, p. 86) describes as “where enterprise leads, finance follows.”Ang (2008) more recently observes that its economic growth leading to financial development instead of the later leading to the former. On the other hand, there is this proposition that financial development promotes economic growth (Calderón & Liu, 2002; Levine et al., 2002; McKinnon, 1973; Shaw, 1973).

Theoretical underpinnings of finance-growth relationship however, have also been pointing out the negative impact of increased financial development. This negative effect is what literature refers to as “too much finance effect.” This opened up a whole new set of exploration of non-monotone relationship between financial development and economic growth. Literature talks about both the financial as well as social costs associated with financial sectors expanding beyond certain threshold. The probable social costs associated with largely expanded financial sectors have been evaluated by Kindleberger (1978), Minsky (1974), and Tobin (1984). Minsky (1974) hypothesis suggests that over a period of time financial depth may divert resources from real sectors of the economy into speculative and eventually destabilizing risky financial investments. Kindleberger (1978) suggested that financial deepening process may lead to macroeconomic volatility. His work extensively refers to financial instability leading to financial manias. His worries revolved around his understanding that large financial system may lead to creation of such financial instruments which may not only be useless but also harmful in case they allow speculative activity to take over the legitimate financial activity. in that case, he argued, the benefits of price discovery and liquidity risk management would be offset. Tobin (1984) also considered this aspect and even went a step forward to suggest a transaction tax (lately known as “Tobin Tax”) to curb the tendencies of using financial instruments for pure speculation.

Rajan (2005) was amongst the pioneers who presented the non-linearities created by “too-much-finance effect” in a structured discussion on possible reason. His argument suggested that longer the financial systems sustain, higher is the burden of expectations and demands placed on them. This financial deepening process leads to adding complexities and accumulation of vulnerabilities in the system. These complexities and accumulated vulnerabilities may eventually lead to chain reaction of unexpected events resulting in economic meltdown.

Impact of Finance over Economic Growth: Empirical Literature

Positive Effect of Financial Development on Economic Growth

Goldsmith (1969) was amongst the first to empirically establish a positive correlation between economic growth in the long-run and the size of financial sector. The increase in efficiency due to financial development is the channel through which the growth is impacted (Bencivenga & Smith, 1991; Greenwood & Jovanovich, 1990). However, Goldsmith (1969) established that there is a positive relationship between these two variables, he did not establish the fact that one causes the other or vice versa.

There is a positive linear relationship between financial development and economic growth (Onyinye et al., 2023; Ustarz & Fanta, 2021). However, in a recent study Wen et al. (2021) also observed a positive linear relationship between FD, EG and poverty alleviation but only in the short-run. Ekanayake and Thaver (2021) also observed a direct and strong relationship between FD and EG in the developing countries. Musabeh et al. (2020) have observed a positive effect of FD on EG in country-level analysis. They observed that out of the sample of four countries, the most energetic impact of FD on EG was observed in Turkey when compared to Poland, Hungary, and Brazil.

A substantial and growing portion of literature provides evidence that financial institutions (like insurance companies and banks) and financial markets (such as stock markets, derivative markets, and bond markets) significantly influence, economic development, economic stability, and poverty alleviation (Levine, 2005). The obligor screening process of the banks leads toward efficient allocation of resources to make the businesses capable of creating opportunities, and hence result in fostering economic growth. Various deposit products of banks and other financial institutions allow mobilization of savings by providing a wide menu of risk-return scenarios. The monitoring process of banks also contributes toward making the managers of firms to behave in a disciplined way. Moreover, high risk and return projects’ investments are also facilitated by the risk diversification enabled by bond, derivatives, and equity markets. Chu (2020), while investigating the impact of financial structure on economic development observes that financial development increases economic development at advanced stages of financial development in a financial market driven system. She also observes that in systems where financial development is skewed heavily toward stock market excessive development viz-a-viz banking sector, the increased financial development may prove to be detrimental toward the economic growth.

A large number of researchers have reviewed the process through which the deepening of financial sector positively impacts economic growth (Ang, 2008; Bassanini et al., 2001; Beck & Levine, 2004; Bekaert et al., 2005; Bertocco, 2008; Demetriades & Hussein, 1996; Edison et al., 2002; Kemal et al., 2007; Leahy et al., 2001; Mavrotas & Son, 2006; Rousseau & Vuthipadadorn, 2005). Perera and Paudal (2009) observe that a positive relationship exists between financial depth and economic growth among firms in Sri Lanka. Using data from Pakistan for the period 1975 to 2008, Jalil and Feridun (2011) observed a strong relationship between the deepening of financial sector and economic growth. The same relationship was observed by Anwar and Nguyen (2011) in Vietnam. Shen et al. (2018) observed that banking sector development influence on per capita GDP growth becomes positive from negative in case the outliers are controlled. Whereas there is a positive impact of financial markets development on GDP growth no matter if outliers are controlled or not.

Financial sector development leads to creation of enabling environment in which all the related stakeholders are benefited through provision of opportunities to unleash their potential (Beck et al., 2008). Belley and Lochner (2007) empirical research show parental investment increasing in children education as a result of greater access to private credit. It has also been observed that improved financial systems provide better access of funds to the collateral constrained small enterprises and contribute to formation of new promising firms (Kerr & Nanda, 2009). There is enough growing evidence available to suggest that financial development intensifies competition, boosts economic growth, and accelerates demand for labour. Bigger benefits of growth and poverty reduction are channelized to the firms/individuals at lower end of income distribution (Beck et al., 2007; Beck et al., 2010).

For a considerable period, there was no attention paid to explore the causality and direction of relationship between FD and EG. King and Levine (1993) renewed the relevant research on this topic. Using the data form 1960 to 1989, they observed size of financial sector being the predictor of economic growth, productivity growth, and investment. They even used the control variables trade openness, government consumption, and school enrolment.

Rajan and Zingales (1998) used data of various industrial sectors across the countries and established a causal relationship from financial deepening to economic growth. Levine continued his research on the same lines as adopted in King and Levine (1993) and along with his co-authors tested different variables and econometric techniques. Levine and Zervos (1998) showed that GDP growth can be predicted by stock market liquidity. Beck et al. (2000) and Levine et al. (2000) established that financial deepening leads to economic growth. Beck et al. (2000) showed financial depth leads to economic growth.

Financial depth (as measured by domestic private credit and financial liquid liabilities) has positive relationship with economic growth (Levine et al., 2000). Demirgüc-Kunt and Levine (2008) show that economies having better-developed financial system have shown the tendency to develop fast in the long-run. Some other researches explored various mechanisms through which financial sector can positively impact the economic growth (Aghion et al., 2005; Bencivenga & Smith, 1991; Levine, 1991; Obstfeld, 1994). While analyzing the data from developing countries of South Asia, it was observed that financial institutions and financial markets’ development positively relates with economic growth (Bibi & Sumaira, 2022). Usman et al. (2022) have, on the other hand, observed that FD strongly influences the economic growth in middle-income countries as compared to low-income countries where this effect is the weakest. They also observed a negative relationship between financial development and economic growth. Guru and Yadav (2019) used credit-to-deposit ratio and domestic credit to private sector as proxy for Banking sector development and stock market development and observed that financial development stimulates economic growth and the financial institutions and financial markets’ development complement each other in this process.

In this backdrop of cost-benefit discussion for larger financial sectors, Loayza and Ranciere (2006) estimated short and long run impact exerted by financial intermediation on economic growth. They show that long-run positive correlation exists between output growth and financial intermediation. However, in the short-run they observed a negative relationship between the two variables. Karagol et al. (2022) employed Toda-Yamamoto Fisher test on data from North African countries to check causality from financial deepening to economic growth and found no causal relationship between the two. Rahman et al. (2020) while studying finance-growth-nexus, for data 1980 to 2017, in Pakistan confirmed Schumpeter (1911) stance of financial development enhancing economic growth. Haque (2020) assessed financial development’s contribution toward private sector growth. They observed positive effect of financial development on trade openness, economic growth, and government expenditures. Le et al. (2023) observe North-South R&D and technology spill overs improve the total-factor productivity of developing countries. They observe a larger impact of financial institutions-based R&D spill over on total productivity as compared to financial markets-based counterpart. Haibo et al. (2023) find that long-term economic benefits of FD can only be achieved if economic volatility is contained within acceptable limits in low- and medium-income countries.

Too-Much-Finance Effect?

Although, literature on financial development and economic growth nexus yielding positive results is well-established. However, if the system does not perform its functions properly, they may negatively impact economic growth, reduce economic opportunities, and introduce volatility leading to destabilization of various degrees. For example, poor selection of borrowers, and passing on the collected funds to politically connected cronies does not allow the finance to be channelized to optimum utilization. It even does not allow the entrepreneurial ideas to be converted into economic realities. The loose monitoring of borrowing firms also leads to the funds being used on non-productive activities by the managers of the borrowing firms. Therefore, the other side of the picture is also the talk of the research which largely revolves around exploring the reasons for financial fiascos and crises. A small proportion of the research is available with regards to the aspect of exploring the non-linearities of finance and growth nexus. The following portion of our literature review presents these researches.

Demetriades et al. (2023) observed that private credit negatively affects economic growth. Rahman et al. (2020) used Markov Switching methodology to observe relationship between FD and EG in various growth regimes. They observed that FD has contributed negatively to EG in low and high economic growth regimes. Rousseau and Wachtel (2011) observed the results which got recognition as “vanishing effect.” These authors observed that view of increased financial depth, measured by credit to GDP ratio, having positive effect on economic growth is less than robust if post-1990 data is used. They suggested that this effect may be caused by financial crises resulted by increased financial depth. Beck et al. (2012) found another explanation for “vanishing effect.” They found a statistically significant relationship between enterprise credit and economic growth but the opposite held true for household credit in their research.

Haiss et al. (2016) findings were consistent with Rousseau and Wachtel (2011) vanishing effect. They took data from 1990 to 2009 for 30 European countries. They attribute the conclusions to procyclical credit cycles and structural changes in the banking system. Pagano and Pica (2012) also referred to higher level of development negatively affecting economic growth. De Gregorio and Guidotti (1995) empirically observe that high income countries might have reached a threshold where financial deepening is no longer contributing to increase in investment efficiency. Molyneux and Forbes (1995) finds that in most European countries large finance sectors are correlated to small number of large banks which breeds inefficiencies due to anticompetitive policies and collusion.

Arcand et al. (2015) and Cecchetti and Kharroubi (2012) however, provide a different explanation for “vanishing effect.” They check if financial depth has decreasing returns after achieving a certain deepening threshold. In 2011, Jean Louis Arcand, Enrico Berkes, and Ugo Panizza first circulated their IMF paper titled “Too Much Finance?” (Arcand et al., 2015). This paper concluded that relationship between financial depth and growth becomes non-linear when private credit enters the range 80% to 100% of GDP. They also establish that too-much-finance effect is not being driven by financial crises, poor institutions, or macro-economic volatility. They also conclude non-existence of vanishing effect in their quadratic specification. This effect may be due to models not allowing for non-monotonicity which suffer from omitted variable bias. Aizenman et al. (2015) show that growth increases as a result of financial development but only to a certain point. While examining sectoral data of 41 countries, they find a heterogenous impact on growth across the sectors. Cave et al. (2020) observed a negative linear relationship between FID and EG. However, for FMD they observe a non-linear relationship with EG.

There are number of research papers which established a U-shaped inverted correlation between financial deepening and growth (Cecchetti & Kharroubi, 2012; Cournède & Denk, 2015; Eugster, 2014; Law & Singh, 2014; Mbome, 2016; Pagano, 2012; Sahay et al., 2015). Cecchetti and Kharroubi (2015) shows that financial development may disproportionately benefit high low productivity but high collateral offering projects. Thus, this exogenous increase in financial depth results in decrease in total factor productivity growth.

However, Cline (2015a b) opines that this view established by so many researchers is just statistical artifact. They show that if economic growth is regressed over R&D Technicians, doctors, and telephones, these yields coefficients implying the same inverted U-shaped relationship for these variables with economic growth as for that of financial depth and economic growth. Arcand et al. (2015) rebuts Cline’s criticism of “too-much-finance effect” being just statistical artifact. Their first argument shows that simple mode taken by him does not present quadratic term in growth-finance relationship being negative. Rather it only shows that sign of the linear term is opposite to the quadratic term. Cline assumed that linear term being positive implies a negative sign for quadratic term. An implicit assumption, therefore, cannot be construed to be a proof. second and more important, they derive normally estimated equation in finance-growth literature by using assumptions of Cline’s model and setting quadratic term equals zero. Resultantly, they find linear term becomes negative. This result contradicts findings of literature related to finance-growth relationship. This leads them to conclusion that either main assumptions of Cline’s model are correct which necessarily mean that pre-2011 linear models used are wrong or assumptions taken by Cline are wrong.

Researchers also found other explanations. Deidda and Fattouh (2002, 2008) observed that during the financial reforms process of transition from a largely bank-based system to market-based system, the traditional positive relationship between financial depth and growth gets reversed. Deidda and Fattouh (2002) worked on heterogeneity across the countries and show that relationship between financial depth and growth is non-monotone. While financial depth has insignificant impact on growth in countries with low levels of financial depth, it has significant positive affect on economic growth in countries with high levels of financial depth. Rioja and Valev (2004) also show the non-monotone relationship by taking panel of 72 countries across three regions. Their results also corroborate with (Deidda & Fattouh, 2002).

An explanation of negative effect of financial depth on growth is also sought by the researchers who worked on impact of state-owned banks on economy. Khwaja and Mian (2005) show that firms connected to political elite get preferential treatment by state owned banks in Pakistan. This, according to them, annually costs 1.9% of GDP. Korner and Schnabel (2010) also worked on data from 1970 to 2007 to observe the impact of state ownership of banks on growth. They show that low institutional capacity and lower levels of financial deepening led to negative contribution of state-owned banks toward economic growth. Khan and Senhadji (2000) and Khan et al. (2001), using a big sample for cross-country study of relationship between financial deepening and inflation show in the first paper, a threshold beyond which inflation results in significant slowdown in growth. In second paper, they uncover a threshold beyond which financial deepening is impeded by inflation. Gennaioli et al. (2012) describe financial innovation may increase the financial fragility due to financial innovation in case the tail risk is neglected.

Hypotheses

The empirical literature provides evidence of both a positive and a negative influence of development of the financial sector on economic growth. Therefore, this study proposes a non-linear effect of financial development on economic growth. Under this non-linear relationship, the economic development boosts economic growth in the initial phase. However, after a certain level, additional economic development may suppress the economic growth. The hypotheses are as follows:

H1: There is a non-linear relationship between financial development and economic growth.

H2: There is a non-linear relationship between financial development and economic growth in developing countries.

Theoretical Model

In line with its research objectives, this study focuses on observing the impact of financial development on economic growth, by approximating financial development through two composite indices. The two composite indices are financial institutions’ development (FI) and financial markets’ development (FM). The composite indices are sub-divided into three sub-measures for each of the index. The sub-measures are financial depth (Depth), financial access (Access), and financial efficiency (Efficiency). The measures for financial development also include a composite index indicating the overall financial development of an economy (Composite), a composite index for measuring financial development of financial institutions (Composite FI), and a composite index measuring financial development of financial market (Composite FM). Consequently, nine different measures, identifying the different aspects of financial markets and institutions, are used in this study. Figure 1 below provides the hypothesized model.

Theoretical model.

Research Methodology

Sample and Data

Panel data from 1980 to 2020 for 23 developed and 35 developing countries is used for the study. The data sources are World Development Indicators of the World Bank GDI and the Global Economy.com. Since the data has a panel structure having 58 countries data across number of variables and time-series of 40 years, we have used the statistical software Stata SE 15 for data science.

Empirical Model

The empirical model of the study is represented by the equation below.

where, EG represents the dependent variable that is the economic growth for country “j” at time “t,”FD refers to financial development and FD2 is the quadratic term of financial development. Other symbols are interpreted as follows: γ0 is the country fixed effect, γ1 is the coefficient on relevant financial development indicators, γ2 is the coefficient on squared terms of relevant financial development indicator, X is the coefficients on control variables, ε is the error term of the model, and the subscripts j and t refer to the variable corresponding to country j in time t.

The above Equation tests the non-linear relationship between financial development (FD) and economic growth (ED) as hypothesized in Hypothesis 1 and Hypothesis 2. A negative coefficient on the quadratic term of FD (

Variables’ Measurement

Economic growth is the dependent variable of this study. Following earlier studies (Arcand et al., 2012; Beck & Levine, 2004), economic growth is measured as average of GDP per capita growth. The measurement proxies of financial development adopted from Sahay et al. (2015). The components of financial institutions development and financial markets development are shown in Figure 2.

Components of financial development (Sahay et al., 2015).

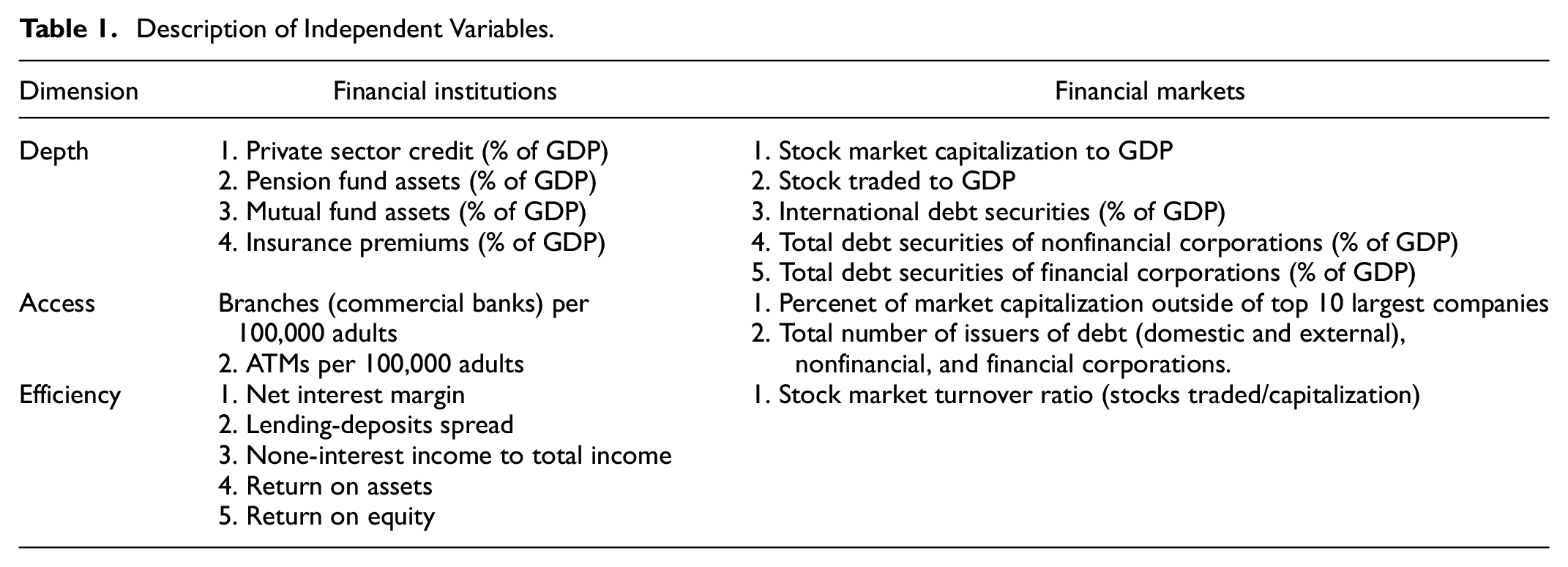

Table 1 shows the variables used to measure the financial depth, access and efficiency for financial institutions and financial markets. Following earlier studies such as Beck and Levine (2004) and Sahay et al. (2015), this study includes several country-level variables to control for heterogeneity across panels. Among the control variables are foreign direct investment, inflation, level of education, public consumption, trade openness, and gross capital inflow.

Description of Independent Variables.

Data Estimation Method

Ignoring cross-sectional dependence/correlation while estimating panel models may lead to severe bias in statistical results (Hoechle, 2007). A number of researchers have suggested the use of Panel Corrected Standard Error (PCSE) being a robust approach to address the problem of autocorrelation, cross-sectional dependence, and heteroskedasticity (Bailey & Katz, 2011; Bai et al., 2020; Wooldridge, 2010; Sundjo & Aziseh, 2018). Some recent studies have considered use of PCSE estimator due to it providing good fit for the data characterized by issues like autocorrelation and heteroskedasticity (Pais-Magalhaes et al., 2022). According to Anton and Nucu (2020), “panels corrected standard errors model” is beneficial to decrease the existence of autocorrelation, cross sectional dependence and heteroskedastic in the panel data. This approach is also in line with (Beck & Katz, 1995).

Additional Testing

We have adopted an additional measure of testing Generalized Methods-of-Movement estimator (GMM) method. Roodman (2006) observes when data feature large number of countries relative to time period, GMM difference estimator as proposed by Arellano and Bond (1991) and the GMM system estimator by Arellano and Bover (1995) and Blundell and Bond (1998) are more efficient. These two estimators are specifically used to explore micro-panel datasets (Eberhardt, 2012). Wide range of current literature has applied these techniques to macro-panel data, including relationship of FD and EG (Abdul Bahri et al., 2018; Arcand et al, 2012; Beck & Levine, 2004; Law & Singh, 2014; Sahay et al., 2015). GMM testing shall allow us to take care of the issue of endogeneity.

Results and Discussions

Descriptive Statistics, Correlation, and Diagnostic Testing

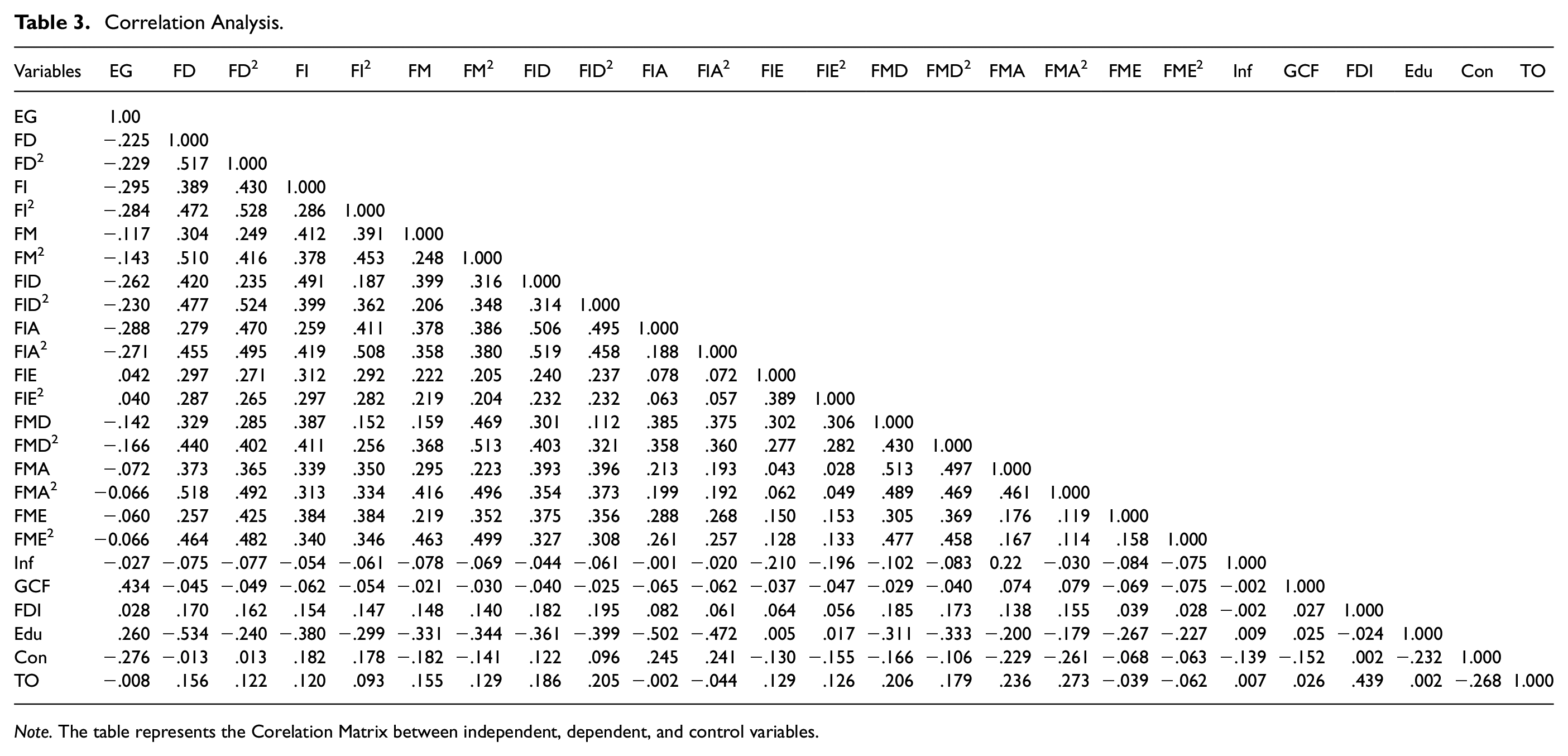

Our discussion here starts with the examination of descriptive statistics in Table 2 and cross correlation of variables in Table 3. We observe from Table 2 that our data on most of the variables has volatility that is less than average, as the standard deviations for most of them are lesser than their respective means. In Table 3, we see that all the variables in this study are partially correlated and hence, there is no issue of multicollinearity.

Descriptive Statistics.

Note. The above table shows the descriptive statistics representing the variables. Tales of distribution of dependent and independent variables are winsorized at 1% and 99% level of confidence. Economic growth (EG) is measured by growth per capital real GDP, Financial Development (FD) is calculated vide an index of Financial Institutions’ Development (FI) and Financial Markets’ Development (FM). Both FI and FM are further calculated vide decomposition into Financial Institution Access (FIA), Financial Institution Depth (FID), Financial Institution Efficiency (FIE), Financial Markets Access (FMA), Financial Markets Depth (FMD), Financial Markets Efficiency (FME). FD2, FI2, FM2, FID2, FIA2, FIE2, FMD2, FMA2, and FME2 are the quadratic terms for the variables described in the previous sentence. Control variables used are inflation, foreign direct investment (FDI), education (secondary level education), consumption (public consumption), and Trade Openness (TO).

Correlation Analysis.

Note. The table represents the Corelation Matrix between independent, dependent, and control variables.

Financial Development and Economic Growth

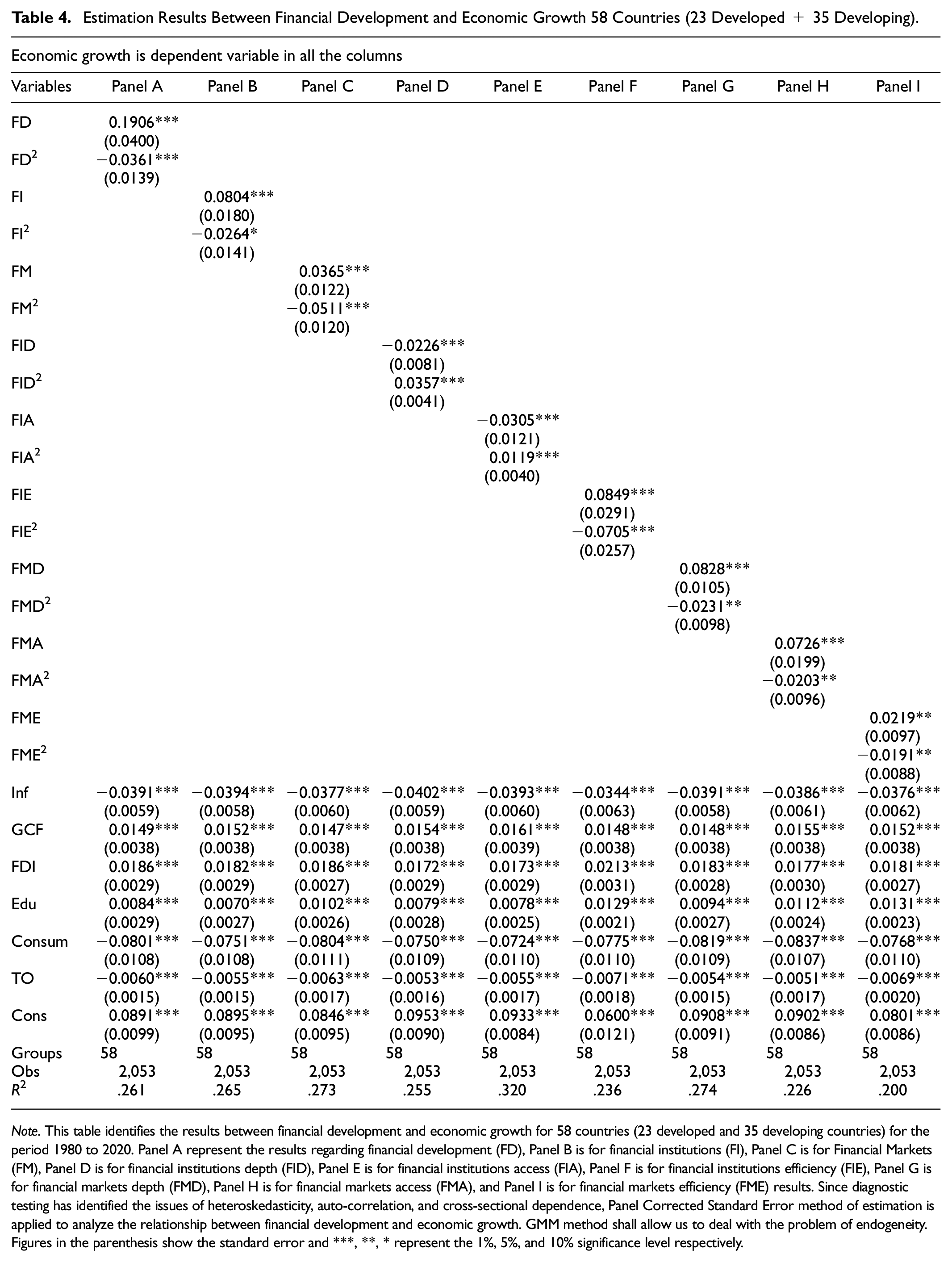

Table 4 tabulates the results of the hypothesized relationships between financial development and economic growth. According to Table 4, the results for the overall data of 58 countries show that FD and EG has an inverted U-shaped relationship. The linear term (γ1) is positive, showing that there is an increase in EG in the initial stages of FD. But as the FD keeps increasing, the economic growth slows down. The quadratic term of FD (γ2) has the negative sign showing that the EG goes down at the higher levels of FD.

Estimation Results Between Financial Development and Economic Growth 58 Countries (23 Developed + 35 Developing).

Note. This table identifies the results between financial development and economic growth for 58 countries (23 developed and 35 developing countries) for the period 1980 to 2020. Panel A represent the results regarding financial development (FD), Panel B is for financial institutions (FI), Panel C is for Financial Markets (FM), Panel D is for financial institutions depth (FID), Panel E is for financial institutions access (FIA), Panel F is for financial institutions efficiency (FIE), Panel G is for financial markets depth (FMD), Panel H is for financial markets access (FMA), and Panel I is for financial markets efficiency (FME) results. Since diagnostic testing has identified the issues of heteroskedasticity, auto-correlation, and cross-sectional dependence, Panel Corrected Standard Error method of estimation is applied to analyze the relationship between financial development and economic growth. GMM method shall allow us to deal with the problem of endogeneity. Figures in the parenthesis show the standard error and ***, **, * represent the 1%, 5%, and 10% significance level respectively.

For Panel A, the quadratic term of FD has a negative coefficient of −0.0361 with significant level of 5%. Our results are in line with the “vanishing effect” of Rousseau and Wachtel (2011) and the inverted U-shaped relationship concluded by prior studies (Cecchetti & Kharroubi, 2012; Cheng et al., 2021; Eugster, 2014; Philippon & Reshef, 2012, 2013; Samargandi et al., 2015). Sahay et al. (2015) also observed a significant bell-shaped relationship between FD and EG, indicating that the marginal returns for EG starts diminishing at the higher levels of FD. Arcand et al. (2015) also reached the same conclusion that FD increases EG, but the effects weaken at higher levels of FD, and eventually become negative.

Results for Panel B and Panel C of Table 4 provide an explanation that both the financial institutions’ development (FI) and financial markets’ development (FM) have non-monotone relationships with EG with 5% significance level of their quadratic terms. Thus, in contrast to some studies which do not find financial markets development to be significant in contributing toward long-run decline in EG, our research shows that financial markets development also contributes to this non-monotonous relationship for our dataset of developed and developing countries. A possible explanation to this may be found in the research of Law and Singh (2014) and Samargandi et al. (2015). They attribute this to the inefficiency of derivative market where the financial flow is not channelled in productive manner. Subsequently, the resultant high liquidity without adequate control and monitoring may cause the “finance curse” or chains to support the “too much finance harm growth” propositions.

There are interesting results when we analyze the components of FD that contribute toward the major results. For results on analysis using the consolidated data of 58 countries, the development of financial institutions (FI) and financial markets (FM) are shown to have an inverted U-shaped relationship with EG. For financial institutions’ development, the results are consistent with (Arcand et al., 2012; Sahay et al., 2015). However, for financial markets’ development, the results are diverged from the conclusions of Sahay et al. (2015). Nevertheless, the results are logical as at the larger levels of development of financial markets, the risk-taking appetite is higher and more exotic financial instruments are available. The complex structure of the instruments allows the risks to be hidden in the complexities and higher levels of leverage.

However, the depth (FID) and access (FIA) of financial institutions’ development are both shown to be significant, and thus conclude that the increased levels of depth and access of the development of financial institutions are contributing toward larger economic growth. Whereas for the depth (FMD) of financial market’s development, the results are similar to FID, that the increased levels of FM depth explain an increase in the economic development. The results are in contrast with the research that associate the negative impacts of the excess financial depth on growth to excessive banks’ competition (Law & Singh, 2014) and the increase in financial sector without a corresponding increase in financial intermediation (Beck et al., 2014).

Results of additional testing using GMM method of estimation confirms are results for Panel A. Table 7 tabulates the GMM results of the hypothesized relationships between financial development and economic growth for 58 countries. According to Table 5, the results for the overall data of 58 countries show that FD and EG have an inverted U-shaped relationship. The linear term (γ1) is positive, showing that there is an increase in EG in the initial stages of FD. But as the FD keeps increasing, the economic growth slows down. The GMM results also confirm the sub-component results, using the consolidated data of 58 countries, the development of financial institutions (FI) and financial markets (FM) are shown to have an inverted U-shaped relationship with EG. Therefore, we have conclusive evidence that the results of PCSE method of estimation are reliable.

Estimation Results Between Economic Growth and Financial Development.

The results for the analysis using the dataset of 23 developed countries are shown in Table 6. For the developed countries, the results are generally in line with the previous research. It shows inverted U-shaped relationships for FD, FI, FM, FID, FIE, and FME with EG (Cecchetti & Kharroubi, 2012; Cheng et al., 2021; Eugster, 2014; Philippon & Reshef, 2012, 2013; Rousseau & Wachtel, 2002; Samargandi et al., 2015). All things considered, the results for the “too much finance effect,” as indicated by an inverted U-shaped relationship between financial depth and growth, are corroborated by a large number of papers (Arcand et al., 2012; Cecchetti & Kharroubi, 2012; Cournède & Denk, 2015; Eugster, 2014; Kindleberger, 1996; Law & Singh, 2014; Minsky, 1974; Mbome, 2016; Pagano, 2012; Sahay et al., 2015).

Estimation Results Between Financial Development and Economic Growth (Developed Countries).

A possible explanation is provided by Rajan (2005), that discussed on the dangers of financial development. He suggested that the presence of a large and complicated financial system had increased the probability of a “catastrophic meltdown.” He argues that longer sustaining financial systems increases the perception of reliability thereby increasing the demands being placed on the services provided by such systems. In such case, further deepening results in creation of complex products resulting in vulnerabilities for the financial system.

For developed countries, most of the sub-components that is, FI, FM, FID, FIE, FMD, and FME of FD are showing IUS relationship. However, an interesting result is that financial access components (FIA and FMA) for both banking institutions and financial markets are showing a U-shaped relationship. These results entail that further financial access can lead to higher levels of EG at higher levels of FD in developed countries.

However, our results for developing countries in Table 7 are opposite to what we see in the panels of collective or developed countries. There is a positive linear relationship observed for FD and EG in developing countries, which entails a likelihood of low level of financial development and a room for increase in FD that would lead to the increased EG in developing countries. Our results in this regard are the same as observed by Demirgüc-Kunt and Levine (2008). There is a vast literature showing the benefits that accrue to countries in which the financial development is greater. Kpodar et al. (2019) found that the development of banking system for the low-income countries acts to increase the shock absorption capacity in those countries, but this shock-absorbing role diminishes with economies growing richer. This argument provides one of the possible explanations to our result of linear relationship between FD and EG for developing countries. Botev et al. (2019) also did not find support for the “too-much finance” hypothesis for developing countries.

Estimation Results Between Financial Development and Economic Growth (Developing Countries).

For developing countries, the observations on the components of FI and FM present the possible explanations. FI has a positive impact on EG at higher levels of FI. The positively contributing sub-components of FD in the developing countries’ case are FI depth, efficiency, and FM depth. The relationship on FD and growth for developing countries has been corroborated by several empirical research (Akpan et al., 2017; Botev et al., 2019; Deidda & Fattouh, 2002; Rioja & Valev, 2004). Some researchers found this relationship non-linear but U-shaped which necessarily denies the “too-much-finance” argument for the developing countries (Oro & Alagidede, 2019). Karagol et al. (2022) even argued of no causality from FD to EG.

Conclusions

Keeping in view the objectives of our research, the following conclusions are drawn based on the results and discussions. First, a positive association between financial institutions’ development and economic growth for developing countries entail that macro-economic policy makers need to focus on increasing the banking sector development especially with focus on the sub components of financial depth and financial efficiency. On the other hand, macro-prudential policy makers need to put in place the mechanism to manage the risks associated with enhanced banking-sector led financial development. Our conclusion that the hypothesis of non-linear relationship between financial development and economic growth is not accepted for developing countries has also been corroborated by many researchers (Akpan et al., 2017; Botev et al., 2019; Deidda & Fattouh, 2002; Rioja & Valev, 2004). Some researchers found this relationship non-linear but U-shaped, which also necessarily denies the “too-much-finance” argument for the developing countries (Oro & Alagidede, 2019). Hence, the policy-making institutions, both at domestic and international levels, need to rethink that whenever they have to formulate the policies related to financial development, they need to consider the aspect of dealing with the different dynamics of the developed and developing economies. They need to understand that the set of opportunities in developing countries may be a recipe for disaster in developed countries and vice versa.

Second, financial development and economic growth have an inverted U-shaped relationship for developed countries. Interestingly, both the sub-components of financial depth that is, financial institutions depth (FID) and financial markets depth (FMD) are the contributory elements toward this IUS association. Macro-economic policy makers therefore, needs to focus on coming up with a bi-pronged strategy in developed countries; one, risks leading to negative consequences of FID and FMD needs to be managed, two focus may be on developing financial access and financial efficiency sub-components as they have positive association with economic growth even at higher levels of financial development. Our finding of financial depth having IUS relationship with EG for developed countries is corroborated by the broader results of researches conducted by Arcand et al., 2012, Cecchetti and Kharroubi, 2012, Cournède and Denk, 2015, Eugster, 2014, Kindleberger, 1978, Law and Singh, 2014, Minsky, 1974, Mbome, 2016, and Pagano, 2012. However, for developing countries, financial depth is contributing to higher levels of growth as the financial depth increases. Therefore, the policy makers have to see this aspect in relation to their countries’ perspectives prior to the execution of a particular policy.

Third important conclusion of our research is that single-proxy measures like credit-to-GDP growth or market-capitalization-to-GDP growth for financial development are not conclusive enough to draw inferences. Once the financial development is further decomposed into the sub-components of banking development (financial institutions development and financial markets development), the sub-components are to be separately analysed for their respective roles. These two dimensions of financial development are further analysed for their drivers that is, financial access, depth, and efficiency as is done in this research by using the approach illustrated by Sahay et al. (2015). Hence, improved understandings may be achieved. For example, our results provide interesting insights while observing these sub-components. For developing countries, the analysis on components of FI and FM may prove useful for the policy makers to focus their efforts on components having positive linear relationship with EG. FI has a positive impact on EG at higher levels of FI and the contributing components of FI are financial institutions’ depth and efficiency. Similarly, for financial markets, efficiency contributes to growth at higher levels of efficiency. This conclusion is in line with the ones observed by some other researchers (Akpan et al., 2017; Bibi & Sumaira, 2022; Botev et al., 2019; Rahman et al., 2020; Rioja & Valev, 2004). Non-linear but U-shaped relationship found by certain researchers also points at the positive impact on economic growth at higher levels of efficiency (Oro & Alagidede, 2019). Similarly, though inverted U-shaped relationship between FD and EG is observed for developed countries, an interesting result observed is that financial institutions’ access and financial markets’ access are showing a U-shaped relationship. The findings entail that further financial access can lead to higher levels of EG at higher levels of FD in developed countries. This may also be an important insight for policy makers.

Fourth, owing to the different financial dynamics and structure of developing and developed countries, we need to evaluate the countries separately. The results shown by the collective set of data of 58 developing and developed countries are different when we tested the developed and developing countries separately. For the developed countries, there is an inverted U-shaped relationship between FD and EG, which is in line with many previous research (Arcand et al., 2012; Cecchetti & Kharroubi, 2012; Cournède & Denk, 2015; Eugster, 2014; Kindleberger, 1978; Law & Singh, 2014; Mbome, 2016; Minsky, 1974; Pagano, 2012; Rajan, 2005; Sahay et al., 2015). However, for developing countries, these generalizations cannot hold true as our research observes a positive linear relationship between FD and EG for the developing countries. Our research observes that establishing the nature of relationship between economic growth and financial development is critical for policy formulation to ensure sustainable economic growth in countries. The differences in financial intermediation mechanisms, structures, and decision-making patterns between the developed and developing countries warrant detailed research on the economic growth for each of these group of countries. Empirical study of Xu and Gui (2021) has observed that neglect of interactions between financial institutions and financial markets may lead to biased estimations. We have not examined these interactions per se. Future researchers may also look at this aspect.

The conclusions may be summarized further to conclude that higher levels of financialization adds certain anomalies which either slows down or adversely affect the economic growth in developed countries. These anomalies include movement of funds from real sectors of the economy toward the speculative activities, shift in human talent from real sector to more rewarding financial sector, increase of operational and financial risk due to financial engineering and innovative complex financial contracts. However, the higher levels of financialization impacts the economic growth positively. The underlying reason seems to be the overall level of financial development characterized by less developed financial markets operating on basis financial contracts.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data is available at The Global Economy.com