Abstract

Issuing government debt is an important means to ensure economic growth and maintain social stability. Based on the panel data of Chinese cities from 2011 to 2019, this paper analyzes the impact of local government implicit debts on the economic growth of Chinese cities and the internal mechanism. The research has reached the following main conclusions: Firstly, local government implicit debts have a significant inhibitory effect on the economic growth of Chinese cities, which has been verified in both the first-term model and the second-term model. Moreover, after replacing the core explanatory variables, adjusting the sample size, and conducting robustness tests such as the lag period, this inhibitory effect remains significant. Secondly, at the same debt level, cities with low GDP, non-resource-based cities and cities in non-eastern regions have more limited fiscal space when achieving maximum economic growth. These regions are confronted with more severe debt burdens and economic growth bottlenecks. Finally, both the level of financial development and fiscal transparency can significantly and negatively regulate the inhibitory effect of local government implicit debts on economic growth. Among them, the regulatory role of fiscal transparency is particularly prominent, reflecting its key role in improving government fiscal management and enhancing market trust. Based on this, this paper suggests enhancing local fiscal transparency and debt management, optimizing the financing structure of local government debts to improve financing efficiency, and implementing differentiated policies in accordance with local conditions to promote coordinated regional economic development.

Keywords

Introduction

Against the backdrop of continuously intensifying downward pressure on the economy and sluggish growth in fiscal revenue, it has become a common practice for local governments to use debt financing to fill fiscal gaps, maintain basic public services and economic growth. Local government debts include explicit debts and implicit debts. Explicit debts are direct liabilities that are clearly stipulated by law and incorporated into budget management, with high transparency and controlled scale. Implicit debt refers to the debt that local governments borrow directly or indirectly with fiscal funds or by illegally providing guarantees outside the legal debt budget. It is characterized by strong concealment, high interest rates, and a high risk of triggering regional financial risks (You, 2024). Due to the constraints of the Budget Law on local government financing, local governments widely rely on financing platforms for borrowing, generating a large amount of hidden debts. Especially after the implementation of the “4 trillion yuan” investment plan, the scale of local government implicit debts represented by financing platform debts has continued to expand, showing explosive growth (Ma et al., 2024). The issue of local government debt in China has three notable characteristics. First, compared with the explicit debts within the budget, the implicit debts in local government debts are larger in scale and more prominent in risk. They mainly include debts borrowed by financing platform companies (urban investment companies; such as loans, bonds, non-standard financing, etc.), non-standard PPP projects, and contingent debts formed by government procurement of services (Fan et al., 2025). Secondly, as an important component of local government debt, implicit debt is not included in budget management and is usually not reflected in the government’s public financial statements. However, local governments need to undertake certain repayment or rescue responsibilities, and its potential risks and scale cannot be ignored (Liao et al., 2025); Thirdly, the spatial distribution of local government implicit debts is unbalanced. Although the overall government debt risk in China is controllable, considering the huge differences in economic and fiscal conditions among regions in China, the risk of local government implicit debts in some regions is more prominent and has a greater impact on the stable development of the economy and society (Wen et al., 2024). Clarifying the specific impact of local government implicit debts on the economic growth of Chinese cities will help various regions address the problem of implicit debts in a targeted manner on the basis of stable economic operation. If implicit debt drives economic growth, then when resolving the issue of implicit debt as a whole, more attention should be paid to “stabilizing growth.” If implicit debt restrains economic growth, then when resolving the issue of implicit debt as a whole, more attention should be paid to “preventing risks.”

Existing research results show that, compared with explicit debt, the implicit debt of local governments has a more profound and complex impact on economic growth. Hong et al. (2023) pointed out that hidden debts are mainly realized through local government financing platforms, financing state-owned enterprises and other innovative financing tools, etc (Hong et al., 2023). These financing forms are usually not within the formal budget of the government, resulting in the “concealment” effect of government debts. This implicit debt model enables the government to circumvent fiscal audits and debt reviews. Information asymmetry and regulatory loopholes have led to the risk of implicit debt being far greater than that of explicit debt, and its repayment capacity is difficult to predict. Song et al. (2025) pointed out that the impact of implicit debt on local economies is mainly reflected in fiscal pressure and the limitation of public investment capacity (Song et al., 2025). With the continuous accumulation of hidden debts, the fiscal burden on local governments has gradually increased. Especially for local economies that rely on land transfer income and local government financing platforms, this debt model often leads to excessive tension in fiscal resources. Cai et al. (2024) also pointed out that under the circumstances of increasing fiscal pressure, local governments’ investment in infrastructure construction, social services, and public investment is insufficient (Cai et al., 2024). Thus, this debt model is not conducive to the sustainable development of the local economy and may lead to a decline in the quality of economic growth and an imbalance in regional development. Chen et al. (2024) also pointed out that the repayment pressure of implicit debts often forms a vicious cycle through debt financing. In the context of economic growth slowdown and fiscal revenue decline, local governments find it difficult to rely on traditional fiscal revenue to repay debts and instead rely on new debts for repayment. Such a debt snowball effect increases the vulnerability of the local economy. Furthermore, X. Yang et al. (2024) pointed out that implicit debt also restrains the innovation ability and long-term development of local governments (X. Yang et al., 2024). Against the backdrop of a slowing economic growth, the debt pressure faced by local governments has forced them to invest more funds in high-debt and low-return projects, while neglecting investment in technological innovation, industrial upgrading and economic structure adjustment. Therefore, the excessive accumulation of hidden debts is not merely a matter of local fiscal risk, but also a hidden danger that affects regional economic competitiveness and long-term development.

Different regions show significant heterogeneity when dealing with the issue of implicit local government debts, a phenomenon mainly reflected in multiple aspects such as economic scale, resource-based cities, and geographical location. Firstly, economic scale, as a core indicator for measuring a city’s economic strength, directly affects the fiscal revenue level and debt repayment capacity of local governments (Leite & De Bacco, 2024). Luo et al. (2023) pointed out that cities with a larger economic scale, due to their relatively solid industrial foundation and abundant fiscal revenue, can obtain relatively stable sources of funds through taxation, land transfer and other means, and the problem of hidden debt is relatively mild (Luo et al., 2023) . These cities can make use of local government financing platforms and diversified financial tools to meet public investment demands while maintaining the controllability and rationality of debt. However, He and Chen (2023) also pointed out that with the acceleration of urbanization and the sharp increase in the demand for public infrastructure, although some economically developed cities have a strong debt repayment capacity, the scale of their implicit debts has also been continuously expanding, and the debt structure has become increasingly complex, especially through indirect financing through local government financing platforms (He & Chen, 2023). This makes the management and early warning of debt risks even more difficult; Secondly, as an important component of the local economy, the economic growth of resource-based cities largely depends on the development and utilization of natural resources (Y. P. Zhang et al., 2025). However, the economic model of resource-based cities has long been based on resource consumption and has relatively weak innovation capabilities. With the depletion of resources or fluctuations in the resource market, resource-based cities are confronted with the dual pressure of industrial structure transformation and the shift in economic growth drivers. Song (2021) pointed out that in order to address the challenges brought about by economic transformation, many resource-based cities rely on large-scale infrastructure construction and investment, and finance through local government implicit debts (Song, 2021). This way of relying on debt financing may bring about certain economic growth, but with the accumulation of debt and the increase of fiscal pressure, the hidden debt problem of resource-based cities may become a bottleneck restricting their sustainable economic development. Especially when resource prices fluctuate or market demand declines, the increase in debt burden often exacerbates the fiscal predicament of local governments, which may lead to a slowdown in economic growth or even the outbreak of a debt crisis. Finally, the eastern region, as the most economically developed area in China, has long played the role of an engine driving the country’s economic growth. Due to their superior geographical location and solid economic foundation, cities in the eastern region enjoy significant advantages in terms of local fiscal revenue, industrial development and innovation capabilities (Jiang & Zhao, 2025). However, with the development of the economy, especially the acceleration of urbanization, cities in the eastern region are facing an increasing demand for infrastructure construction and pressure on social public services. Li and Chen (2025) pointed out that in order to meet these demands, local governments often finance through implicit debts to promote urban construction and regional development (Li & Chen, 2025). Although cities in the eastern region generally have a strong debt repayment capacity, the rapid growth of debt and the complexity of the debt structure have exposed these areas to a relatively high debt risk. To sum up, the issue of local government implicit debts shows obvious heterogeneity in the urban economy of China. The economic scale, the transformation of resource-based cities and the particularity of the eastern region jointly act on the formation and expansion of local debts. For different types of cities, implicit debt is not only an important tool for promoting economic development, but also may become a potential risk to sustainable economic growth.

However, the existing research still has certain deficiencies: Firstly, there is a lack of systematic studies on the impact of the “scale” of implicit debt. Most of the existing literature focuses on the proportion or structural characteristics of implicit debt in local government debt and the role of economic growth. However, research on the absolute scale of implicit debt is still relatively scarce. Therefore, existing research has failed to fully reveal the long-term impact of the absolute scale of implicit debt on economic development. Secondly, the regulatory role of the external institutional environment on the economic effect of implicit debt is ignored. Existing research often focuses on analyzing the impact of implicit debt itself on economic growth, while less exploring the regulatory role of the external institutional environment. Although some studies have pointed out the impact of fiscal transparency and the development of financial markets on the economy, there is a lack of in-depth analysis of how these external variables regulate the economic effects of implicit debt. Finally, the nonlinear relationship between the scale of implicit debt and economic growth was not fully considered. Most existing studies regard the relationship between the scale of implicit debt and economic growth as a linear one, ignoring its possible nonlinear effects. Although some studies have explored the relationship between debt and economic growth, few have used quadratic term models to reveal the complex mechanism by which the scale of implicit debt affects economic growth.

Based on this, the possible marginal contributions of this paper are as follows: First, from the perspective of the “scale” of implicit debt, this paper systematically studies the nonlinear impact of implicit debt on regional economic growth. Most of the existing literature focuses on the impact of the proportion or structural characteristics of implicit debt in local government debt on economic growth. However, research on the absolute scale of implicit debt is still relatively scarce, especially in terms of the specific consequences of debt of different scales on economic growth, where there is a lack of systematic evidence. Secondly, this paper introduces the development level of the financial market and fiscal transparency as moderating variables, revealing the moderating path of the external institutional environment on the economic effect of implicit debt. Among them, the regulatory role of fiscal transparency is particularly prominent, demonstrating its significance in improving government fiscal management and enhancing market trust. Thirdly, in this study, the quadratic form of the explanatory variable is introduced for analysis, revealing the nonlinear impact of the scale of implicit debt on economic growth. This approach expands the understanding of the effect of implicit debt and further verifies the complex influence mechanism of the scale of implicit debt on economic growth at different levels. Through this innovative analytical framework, this paper not only enriches the theoretical perspective of implicit debt research, but also provides new ideas for future related research.

Theoretical Analysis and Research Hypotheses

Direct Effect Analysis

The fiscal multiplier effect is an important concept in Keynesian economics, referring to the fact that the government can trigger multiple times the growth of economic activities through fiscal policies such as increasing spending or reducing taxes (Qi et al., 2025). Local governments’ financing through hidden debt, especially in infrastructure construction and public investment, often can stimulate aggregate demand and boost GDP growth in the short term. During an economic recession or downturn, the consumption and investment demands of the private sector are insufficient. The government can fill this gap by increasing fiscal spending. The fiscal multiplier effect indicates that when the government increases its spending, it not only directly affects economic growth but also further promotes economic activities through multiple reverse cycles. The government’s expenditure not only directly provides funds for construction projects, public services, and other fields, but also indirectly drives the demand of related industries through wage payments, material procurement and other means, thereby encouraging more enterprises to increase production, expand investment, and provide job opportunities for workers. The incremental demand brought about by such expenditures ultimately boosts the output level of the entire economy through a circular effect (Liu & Wang, 2025).

Local governments can achieve rapid economic growth through the fiscal multiplier effect by increasing implicit debts and conducting large-scale infrastructure construction. The construction industry, manufacturing, and related service industries have all benefited from government investment, driving up employment and tax revenue, and promoting the total social demand (Wan et al., 2024). Therefore, in the initial stage, the government’s debt input often manifests as a positive economic stimulus, promoting economic activities, and growth. However, as debts continue to accumulate, the fiscal conditions of local governments gradually come under pressure, and the burden of hidden debts begins to rise. Ciaffi et al. (2024) pointed out that although the increase in initial fiscal expenditure would bring about a positive growth effect, with the aggravation of the debt burden, the promoting effect of fiscal expenditure on economic growth would gradually decrease and might even reverse (Ciaffi et al., 2024). When debt reaches a certain level, the government has to allocate more fiscal resources to debt repayment and reduce spending in other areas such as social welfare, public services, and education. The reduction in investment in these areas will affect overall social demand and subsequently lead to a slowdown in economic growth. Ma and Lv (2021) also pointed out that long-term debt accumulation may also lead to market concerns about government credit, thereby affecting private investment and consumption (Ma & Lv, 2021). According to the theory of the fiscal multiplier effect, when debt is too high, the market’s expectations for the government’s fiscal health may become pessimistic, leading to an increase in capital costs, difficulties for enterprises in financing, a decrease in the investment willingness of the private sector, and possible suppression of consumer demand. Liu (2022) also pointed out that local governments may need to raise taxes to repay debts, which will further squeeze the consumption and investment space of the private sector, forming a vicious circle (Liu, 2022). Therefore, local government hidden debts have promoted economic growth in the short term through the fiscal multiplier effect. However, as the debt burden increases, the stimulating effect of fiscal expenditure on the economy gradually weakens or even reverses, and the inhibitory effect on the economy emerges, presenting an inverted U-shaped effect.

However, the negative effects of local government’s hidden debts in China’s urban economy have gradually emerged. Firstly, the increase in fiscal pressure has weakened investment in public services and development. Yue and Liu (2025) pointed out that in some second-tier cities such as Shenyang and Changchun, due to heavy debt burdens, local governments have to cut public investment in order to repay debts, resulting in insufficient allocation of educational and medical resources and a decline in the quality of social services (Yue & Liu, 2025). This kind of fiscal pressure directly affects the consumption confidence and living standards of local residents, thereby indirectly suppressing the growth of the local consumer market and the endogenous driving force of the economy. Secondly, the reliance on the real estate market has intensified, and the economic structure is single. Local governments promote economic growth through land transfer income and borrowing from financing platforms, especially in cities that rely on real estate development. The implicit accumulation of debt is closely related to the real estate market. Many local governments have increased fiscal revenue and promoted rapid urban economic growth through large-scale infrastructure construction and land development. However, over-reliance on the real estate market may lead to a local economy being overly simplistic and lacking diversified economic support. With the fluctuations in the real estate market, the instability of local government fiscal revenue increases. If the real estate market declines, the land transfer income of local governments will drop significantly, and the pressure of debt repayment will increase, thereby restricting the sustainable growth of the urban economy (Y. J. Yang et al., 2025); Furthermore, the rising financing costs have curbed corporate investment. Another significant consequence of the accumulation of local government implicit debts is the increase in financing costs. When the debt burden is too heavy, the credit rating of local governments may decline, which in turn leads to an increase in their financing costs. These rising costs not only affect the government’s fund-raising but may also be passed on to local enterprises, dampening their willingness to invest. Faced with high financing costs, enterprises often choose to postpone or reduce investment, especially in high-risk innovative projects and infrastructure construction, which affects the transformation and upgrading of the economy (L. W. Li et al., 2022); Finally, implicit debts affect the fiscal autonomy of local governments. Local governments often fail to make effective economic decisions independently in the face of implicit debts, as debt repayment consumes a large amount of fiscal resources (Rong et al., 2023). This means that when local governments implement economic development plans, they may be constrained by debt repayment pressure and find it difficult to carry out large-scale economic structural adjustment and industrial optimization and upgrading. With the increase in local debt levels, the government’s fiscal autonomy and regulatory capacity have gradually been weakened, resulting in an inability to effectively deal with the downward pressure on the economy and ultimately suppressing the potential for economic growth. Therefore, this paper proposes Hypothesis 1:

Mechanism of Action Analysis

This article mainly explores whether the level of urban financial development and fiscal transparency in China can regulate the inhibitory effect of local government implicit debts on economic growth. On the one hand, the development of the financial system can provide local governments with more financing options, improve the debt structure, and thereby alleviate fiscal pressure. The improvement of the financial system enables local governments to obtain lower-cost funds through diversified financing channels (such as bank loans, bond issuance, etc.), thereby supporting economic growth. Q. J. Zhang and Wei (2025) pointed out that when local government debt burdens are heavy, through mature financial markets, local governments can refinance at lower interest rates, avoiding further suppression of the economy by high-cost debts (Q. J. Zhang & Wei, 2025). Meanwhile, Yan et al. (2025) also pointed out that the deepening of the financial market has provided local governments with a broader range of financing options, reducing their reliance on land finance and short-term borrowing, which has effectively alleviated the pressure of hidden debts (Yan et al., 2025). Therefore, cities with a higher level of financial development can usually manage local government implicit debts better and reduce their negative impact on economic growth. However, the volatility and unpredictability of the financial market may lead to unstable financing costs, which limits the ability of local governments to rely on the financial market. Especially when the debt burden of local governments is too heavy, even if the financial market can provide more financing channels, excessive debt will still have a suppressing effect on the economy (J. M. Li et al., 2024).

On the other hand, fiscal transparency, as an important component of local government fiscal management, can more effectively and negatively regulate the inhibitory effect of local government implicit debts on economic growth. Fiscal transparency refers to the extent to which a government discloses information such as its fiscal revenue, expenditure, and debt. High transparency helps to improve the traceability of government debt, reduce information asymmetry in debt management, enhance market trust in the government, and thereby promote the sense of responsibility and standardization of local governments in debt management (Y. H. Li et al., 2024). The improvement of fiscal transparency can reduce the expansion of local government fiscal deficits and debts, thereby helping to alleviate the inhibitory effect of debts on economic growth. By enhancing fiscal transparency, local governments can not only strengthen the effective allocation of fiscal resources but also improve the sustainability of debt repayment, which to a certain extent reduces the burden of hidden debts on the economy (Wan, 2025). Therefore, fiscal transparency can effectively restrain the debt expansion of local governments by strengthening social supervision and enhancing the responsibility and standardization of government debt management, and to a certain extent, alleviate the negative impact of debt on economic growth. Based on the above analysis, this paper proposes the following research hypotheses:

Model Construction and Data Explanation

Model Construction

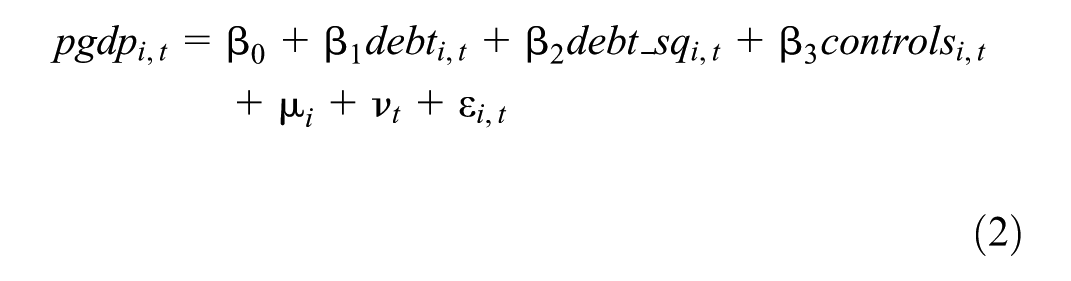

To study the impact of local government implicit debts on economic growth, referring to existing literature (Ma & Lv, 2021), this paper conducts an empirical test by constructing model (1). At the same time, considering that special bonds share certain similar characteristics with local government implicit debts and have a “U” -shaped relationship with economic growth, it is possible that there is also a “U” -shaped relationship between local government implicit debts and economic growth. Based on the theoretical analysis above, this paper introduces the quadratic term of implicit debt and constructs model (2) to test the nonlinear impact of implicit debt expansion on economic growth. The panel data model is established as follows:

Among them, i represents a prefecture-level city, t represents a year, pgdp represents the growth rate of per capita real GDP, debt represents the level of local hidden debt, and μiνtεi,t represents the fixed effect of the city, the fixed effect of time, and the random error term. If debt_sq in Equation 2 is significantly non-zero, and debt_sq is equal to 0 or not significant, it indicates that there is only a linear relationship between local government implicit debt and economic growth. If debt_sq is significantly not 0, it indicates that there is a nonlinear relationship between local government implicit debt and economic growth. When β 1 > 0, local government implicit debt and economic growth present a “U” -shaped relationship. When β 1 < 0, the implicit debt of local governments and economic growth show an inverted “U” shape relationship. The controlsi,t represents other factors that affect the economic growth rate as control variables of the model to alleviate model bias caused by omitted variables.

Compared with the first-term model, the quadratic parabolic model has obvious advantages in describing the impact of local government hidden debts on economic growth. The single-term model assumes that there is a linear relationship between local government hidden debt and economic growth, that is, the increase in debt always has the same impact on economic growth. However, this assumption overly simplifies the actual situation, ignoring the accumulation effect of debt and its nonlinear impact on economic growth. The introduction of the quadratic parabola can, on the one hand, reveal the inverted U-shaped relationship between local government debt and economic growth. That is, within a certain range, debt growth can promote economic growth, but excessive debt begins to have a negative impact on economic growth (Li & Chen, 2025); On the other hand, through the introduction of quadratic terms, the model can precisely capture the inflection point of economic growth caused by debt burden, helping us identify the critical interval of debt levels (Ma & Lv, 2021). Under the current debt situation in China, the debts of many cities have reached this critical range, leading to a slowdown in their economic growth.

Data Description

The explained variable: Per capita real GDP growth rate. This paper measures the level of economic growth by using the per capita real GDP growth rate (Li & Pu, 2024). Per capita real GDP is calculated based on the nominal GDP, GDP deflator and permanent resident population of each prefecture-level city over the years, with 2010 as the base period. Then, the logarithmic difference of the per capita real GDP is taken to obtain the growth rate of per capita real GDP.

Explanatory variable: The level of local government implicit debt. Referring to the practice of Cai et al. (2024), local debt includes explicit debt and contingent debt (Cai et al., 2024). Contingent debt consists of the total amount of state-owned debt of state-owned enterprises and the balance of urban investment bonds issued by local financing platforms. State-owned debt of state-owned enterprises is mainly used for the development of state-owned enterprises themselves and changes little. In this paper, the balance of urban investment bonds is adopted to measure the level of implicit debt of local governments. The balance of local government investment bonds this year =(the amount of newly issued local government investment bonds this year—the amount of local government investment bonds due this year) + the balance of local government investment bonds from the previous year. Another measure that takes the proportion of the balance of urban investment bonds to GDP as the core explanatory variable is used for robustness tests.

Refer to the existing literature (Chen & Wang, 2019; Wang & Zhang, 2023), the following six control variables were selected: (a) Digital infrastructure is calculated based on the number of mobile phone users per 100 people; (b) Structural high-level classification divides GDP into three parts based on the three industries. The proportion of the added value of each part in GDP is regarded as a component of the spatial vector, thereby forming a set of three-dimensional vectors. Then, the angles between these three-dimensional vectors and the vectors of industries arranged from low to high levels are calculated respectively. Finally, the formula for industrial structural high-level classification is defined, as shown in Equation 3. (c) Fixed asset investment is measured by the ratio of the total fixed asset investment of the whole society to GDP. (d) The level of urbanization is measured by the proportion of the built-up area of towns to the total area of the region. (e) Fiscal decentralization is measured by the proportion of fiscal expenditure of prefecture-level cities in the total fiscal expenditure of the province. (f) The fiscal gap is measured by the proportion of the difference between fiscal expenditure and revenue to GDP.

Moderating variables: To further examine the impact of the level of financial development and fiscal transparency on the relationship between local government implicit debts and economic growth, this paper selects the level of financial development and fiscal transparency as moderating variables for verification and analysis. The level of financial development is measured by the proportion of the balance of various loans of financial institutions at the end of the year to GDP (Q. J. Zhang & Wei, 2025); The fiscal transparency is measured by the index of fiscal transparency of prefecture-level cities in China as per the “Research Report on Fiscal Transparency of Municipal Governments in China” released by the School of Public Policy and Management of Tsinghua University (Y. H. Li et al., 2024).

Data Sources and Descriptive Statistics

Considering the availability of data and the difficulty in identifying the impact brought by the COVID-19 pandemic, this paper selects panel data from 286 cities in China from 2011 to 2019 as samples. The data of urban investment bonds in this article is from the Wind database, and observations with completely repetitive content have been excluded based on “bond abbreviation” and “bond name.” Other data are from the “China Urban Statistical Yearbook,” statistical annual reports of some prefecture-level cities, and the “Research Report on the Fiscal Transparency of Municipal Governments in China,” Descriptive statistics of each variable are shown in Table 1.

Descriptive Statistics of Variables.

Meanwhile, this paper also conducted correlation tests on the main variables. The specific results are shown in Figure 1. On the one hand, the results of the correlation test of the main variables are all numerically lower than the critical value of 0.800, indicating that the linear relationship between the relevant variables in the model is weak, and thus the problem of multicollinearity is not obvious. Because the low correlation makes the explanatory power among each variable more independent and the regression coefficient estimation stable, in this case, the multicollinearity problem can be reasonably ignored and the model analysis can continue (Duan et al., 2022); On the other hand, most of the main variables are significant, that is, the selected variables are valid and can provide meaningful information for modeling. This further lays the foundation for the empirical analysis in the next section.

Correlation analysis of main variables.

Empirical Testing and Analysis

The Impact of the Scale of Local Government Implicit Debt on Economic Growth

To explore the impact of local government implicit debt scale on economic growth, this paper estimates based on models (1) and (2) using a bidirectional fixed effects model. The results are shown in Table 2. Among them, columns (1), (3), and (5) are the regression results based on model (1), without including the secondary term of local government implicit debt. Column (3) controls more urban fixed effects compared to column (1), and column (5) controls more annual fixed effects compared to column (3). Columns (2), (4), and (6) are the regression results based on model (2), with the secondary term of local government implicit debt added. Column (4) has more control over the urban fixed effect compared to column (2), and column (6) has more control over the annual fixed effect compared to column (4).

Regression Results of the Impact of Local Government Hidden Debt on Economic Growth.

Note. *, **, and *** indicate that the results are significant at the level of 10%, 5%, and 1% respectively. The values in parentheses are t-values.

According to the results in Table 2, the regression coefficients of the core explanatory variables in columns (1), (3), and (5) are all negative. Except for column (3) which is significant considering the urban fixed effect, the other two columns are not significant, indicating that local government implicit debt has a negative impact on economic growth. Firstly, if the fixed effects of time and cities are not controlled, there may be a bias of omitted variables. Especially in different regions of China, there may be significant differences in economic cycles, fiscal conditions and debt problems. Under such circumstances, it may be impossible to fully identify the true relationship between local government implicit debts and economic growth, thus leading to insignificant regression results (Song et al., 2025). Secondly, after controlling for urban fixed effects, the actual impact of local government implicit debts can be captured more accurately (Chen et al., 2024). The regression result was significantly negative, indicating that after excluding the heterogeneous factors at the urban level, the negative correlation between implicit debt and economic growth became more definite. The economic foundations and governance capabilities of different cities vary greatly, and the debt burdens of local governments differ among different cities. This may lead to significant differences in the relationship between debt and economic growth. Finally, when both the time effect and the urban effect are controlled simultaneously, the reason why the regression results are not significant might be that the relationship between implicit debt and economic growth is greatly influenced by the dynamic changes of time and region. The time-lag effect of changes in the economic cycle and policy adjustments may have a complex impact on the relationship between debt and economic growth. The implicit debt of local governments may stimulate the economy in the short term, but in the long run, the burden of debt gradually accumulates and eventually shows a negative impact (X. Yang et al., 2024). Therefore, after controlling for more time and urban effects, the model may fail to capture the complex impact of implicit debt at different times and in different regions, resulting in the regression coefficients no longer being significant.

Based on the theoretical analysis in this paper, there may be an inverted “U” -shaped relationship between the scale of local government implicit debt and economic growth. Therefore, based on Model (2), a re-regression was conducted and it was found that the coefficients of the primary term of the core explanatory variables in columns (2), (4), and (6) were all significantly negative, and the coefficients of the secondary term were also significantly negative. This indicates that there is an inverted “U” -shaped relationship between local government implicit debt and economic growth, and the symmetry axes are all smaller than the minimum value of debt in Table 1, which is 0. This indicates that the increase in local government’s hidden debts has significantly curbed urban economic growth. The existing data are all on the right side of the inverted U-shaped curve, suggesting that the current debt level has exceeded the optimal range for economic growth and is in a negatively affected area. The excessive expansion of debt has forced local governments’ financial resources to be used for debt repayment instead of being effectively invested in areas that promote long-term growth (Duan et al., 2022). Further debt increases may also trigger financial risks, raise financing costs, and limit other potential economic development opportunities, verifying Hypothesis 1 of this paper.

Robustness Test

Considering that issues such as variable measurement errors, sample selection, and endogeneity may have adverse effects on the research conclusions during the empirical analysis process, in order to verify the reliability of the above conclusions, this paper conducts a robustness test on the above benchmark regression results.

Firstly, replace the explained variable. The explained variable in this paper is the growth rate of per capita real GDP to capture the dynamic changes in economic growth of each city. However, given that the growth rate of per capita real GDP may be affected by short-term fluctuation factors, this could lead to a misjudgment of the long-term economic growth trend. Therefore, in order to enhance the robustness of the results and eliminate the interference of short-term fluctuations on the results, this paper further introduces the per capita GDP level as a substitute variable for robustness tests. Per capita GDP, as a long-term indicator for measuring the level of economic development, can not only effectively control the impact brought about by differences in population size and total economy among different cities, but also reflect the overall economic welfare level of residents in a region (Liao et al., 2025). By conducting robustness tests using per capita GDP, we can further verify whether the inhibitory effect of local government hidden debts on economic growth is universal and consistent. The specific regression results are shown in columns (1) and (2) of Table 3. The results still indicate that the increase in local government hidden debts significantly inhibits the economic growth of Chinese cities.

Robustness Test.

Note. *, **, and *** indicate that the results are significant at the level of 10%, 5%, and 1% respectively. The values in parentheses are t-values.

Secondly, replace the explanatory variable. This article selects the debt balance as the measurement indicator of the implicit debt of local governments. However, as an absolute value, the debt balance fails to fully take into account the differences in economic aggregate among different cities, which may lead to distorted assessment of the debt burden, especially in cities with significant differences in economic scale. Therefore, in order to enhance the reliability and comparability of the empirical results, we further introduced the debt-to-GDP ratio as an alternative indicator for robustness tests. The debt-to-GDP ratio, as a relative indicator, can effectively eliminate the interference of differences in urban economic scale, making the measurement of debt levels more accurate. This ratio not only reflects the relative relationship between local government debt and economic output, but also can more intuitively demonstrate the pressure of debt burden (Luo et al., 2023). Therefore, using the debt-to-GDP ratio can more clearly reveal the potential restrictive effect of local government implicit debt on economic growth, especially among cities with different economic levels, which can provide more consistent and comparable analysis results. The specific regression results are shown in columns (3) and (4) of Table 3. The increase in local government implicit debts has significantly suppressed the growth of urban economies in China.

Furthermore, delete extreme data. Considering that first-tier cities such as Beijing, Tianjin, Shanghai, Chongqing, Hangzhou, and Shenzhen, as well as some special economic zones, may have significant differences in terms of economic scale, fiscal policies and debt structure, the debt levels and economic growth characteristics of these cities may differ greatly from those of other cities. This further affects the estimation results of the impact of local government implicit debts on economic growth (Wang & Zhang, 2023). Therefore, in order to eliminate the possible bias that the particularity of these cities may cause to the analysis results, this paper decides to remove them from the sample and conduct a robustness test. This elimination treatment enables the research to more accurately reflect the impact of local government implicit debts on the economic growth of small and medium-sized cities in China, without being disturbed by extreme values. The specific regression results are shown in columns (5) and (6) of Table 3. Even after excluding the above-mentioned cities, the results still indicate that the increase in local government implicit debts has significantly suppressed the economic growth of Chinese cities. This further supports research Hypothesis 1.

Finally, consider the issue of endogeneity. Endogeneity problems usually stem from the bidirectional nature of causality, that is, local government hidden debts may not only affect the economic growth of Chinese cities, but also the changes in the economic growth of Chinese cities may in turn affect local government hidden debts. In this case, if this interaction is not taken into account, the estimates in the model may be biased, thereby affecting the judgment of policy effects. The introduction of the lag period can capture the dynamic characteristics of changes in urban economic growth in China. The impact of local government’s hidden debts often does not manifest immediately but takes some time to become apparent in the economic growth of Chinese cities (Ma & Lv, 2021). In addition, the economic growth of Chinese cities in previous periods may also affect the economic growth of Chinese cities in the current period. Therefore, by introducing a lag period, the research in this paper can identify the delayed effect of policy effects and avoid misjudgment caused by short-term fluctuations in independent variables. This method not only enhances the robustness of the model and its applicability in different scenarios, but also helps to reveal the long-term accumulation effect of local government hidden debt (Liu, 2022). The specific estimation results are shown in Table 4. The lagging first and second phases of local government hidden debts have significantly suppressed urban economic growth. Moreover, the p-values of the Sargan test in these four columns are all greater than .1, indicating that all instrumental variables are valid. The results of the endogeneity test further confirmed research Hypothesis 1.

Endogeneity Test.

Note. *, **, and *** indicate that the results are significant at the level of 10%, 5%, and 1% respectively. The values in parentheses are t-values.

Heterogeneity Test

This article conducts heterogeneity tests from three aspects: economic development level, whether it belongs to a resource-based city, and whether it belongs to the eastern region.

Firstly, the differences in economic development levels may lead to the impact of local government hidden debts on the urban economy of China. Cities with high GDP usually have more diversified and stable economic structures, and their fiscal revenue and resource allocation capabilities are stronger. Therefore, although these cities are also under pressure from local government hidden debts, their relatively mature economic systems and strong debt management capabilities enable the negative effects of the debt burden to be absorbed and alleviated to a certain extent (Leite & De Bacco, 2024). On the contrary, cities with low GDP, due to their relatively lagging economic development, relatively single economic structure, and weak debt management capabilities, have a lower economic pressure-bearing capacity when confronted with local government implicit debts, and the inhibitory effect of debt burden on economic growth is more significant (He & Chen, 2023). Therefore, in this paper, 2,574 Chinese cities are ranked in ascending order, with the top 20% being high-GDP cities and the bottom 20% being low-GDP cities. The specific results are shown in columns (1) and (2) of Table 5 below. Local government hidden debts significantly inhibit the economic growth of Chinese cities, and the symmetry axis of low-GDP cities is lower than that of high-GDP cities. This means that at the same debt level, the fiscal space for low-GDP cities to achieve maximum economic growth is more limited, indicating that their debt levels are more likely to exceed the optimal range, thereby leading to efficiency losses. This also reveals the non-linear relationship between implicit debt and economic growth, and intensifies the structural risks faced by “fiscally weak markets” during the process of debt expansion.

Heterogeneity Test.

Note. *, **, and *** indicate that the results are significant at the level of 10%, 5%, and 1% respectively. The values in parentheses are t-values.

Secondly, based on the degree of dependence on resources, in accordance with the “Notice on the National Sustainable Development Plan for Resource-based Cities (2013–2020),” this paper classifies 286 Chinese cities into resource-based cities and non-resource-based cities. Resource-based cities rely on the exploitation and processing of natural resources as the main economic pillar and usually have a single economic structure. And it is highly sensitive to fluctuations in resource prices. In this case, although resource-based cities may generate certain fiscal revenue in the short term due to resource development, the economic model that relies on a single resource for a long time makes their fiscal and tax foundation relatively fragile, making it difficult for them to maintain a high level of fiscal elasticity in the face of an increase in hidden debt, etc (Y. P. Zhang et al., 2025). The specific results are shown in columns (3) and (4) of Table 5 above. The hidden debts of local governments have significantly inhibited the economic growth of Chinese cities, and the symmetry axis of non-resource-based cities is lower than that of resource-based cities. This means that at the same debt level, the maximization space for economic growth in non-resource-based cities is relatively small. Perhaps due to its constraints on structural issues such as resource depletion and environmental pollution, the accumulation of its debt is more likely to exceed the optimal debt range, resulting in significant losses to economic growth.

Finally, based on geographical location classification, Chinese cities are divided into eastern region cities and non-eastern region cities. As the core area of China’s economy, eastern region cities usually have a more diversified industrial structure, stronger economic resilience and higher fiscal revenue levels. Furthermore, the eastern region is often at the forefront of foreign capital inflow, technological innovation and industrial upgrading, which enables local governments to have more policy tools and market channels to deal with debt issues (Jiang & Zhao, 2025). On the contrary, cities in non-eastern regions, due to their relatively lagging economic development, single industrial structure, limited fiscal revenue, and high debt dependence, often lack effective economic transformation and debt management mechanisms (Li & Chen, 2025). The specific results are shown in columns (5) and (6) of Table 5 above. The hidden debts of local governments have significantly suppressed the economic growth of Chinese cities, and the symmetry axis of cities in non-eastern regions is lower than that of cities in eastern regions. This means that the economic growth of cities in non-eastern regions, under a relatively high debt level, shows a lower growth space. This indicates that the debt levels of these cities may have approached or exceeded their optimal debt range, leading to diminishing marginal effects.

Further Analysis

There is an inhibitory relationship between local government implicit debt and urban economic growth in China. To study its specific mechanism of action, this paper examines it from the aspects of financial development level and fiscal transparency. Referring to the existing literature (Yan et al., 2025), when conducting the moderating effect analysis on the level of financial development, the interaction terms between the primary term of implicit debt level and the level of financial development and the secondary term of implicit debt level and the level of financial development are added. When conducting the moderating effect analysis on fiscal transparency, add the interaction terms between the primary term of implicit debt level and fiscal transparency, as well as the secondary term of implicit debt level and fiscal transparency. The specific model is as follows:

In Model (4), fdl represents the level of financial development, and in Model (5), ftscore represents fiscal transparency. The meanings of other parts are the same as those in Model (2). If β 5 and β 6 in the model are significantly non-zero, causing the turning point to drift or the curve shape to change, it indicates that the moderating effect exists. Table 6 shows the regression results with the level of financial development as the moderating variable, where columns (1) and (3) do not include the quadratic terms of the core explanatory variable.

Regression Results of the Moderating Effect of Financial Development Levels.

Note. *, **, and *** indicate that the results are significant at the level of 10%, 5%, and 1% respectively. The values in parentheses are t-values.

According to the results in Table 6, the results in columns (1) and (3) indicate that the level of financial development and fiscal transparency promote the economic growth of Chinese cities. Moreover, the interaction coefficients of both columns are significantly positive, suggesting that both the level of financial development and fiscal transparency can negatively regulate the inhibitory effect of local government hidden debts on economic growth. On the one hand, the improvement of financial development levels has provided local governments with more financing channels and more efficient capital allocation mechanisms. When the financial market becomes more mature and the banking system more complete, local governments can raise funds through various means such as the bond market, rather than relying solely on implicit debts. This diversified financing approach can effectively disperse debt risks, reduce local governments’ reliance on implicit debts, and thereby alleviate the inhibitory effect of debt on economic growth (Q. J. Zhang & Wei, 2025); On the other hand, the improvement of fiscal transparency means that local governments are more open and transparent in terms of fiscal revenue and expenditure, debt management, etc., which helps enhance the market’s trust in the fiscal situation of local governments (J. M. Li et al., 2024). When local governments can clearly and transparently present their fiscal conditions and debt risks, the financial market and the public can better assess and respond to these risks, avoiding the blind expansion of hidden debts. This transparency helps to promote more rational and sustainable fiscal policies and reduce economic risks brought about by hidden debts.

The interactive results of columns (2) and (4) further indicate that both the level of financial development and fiscal transparency can negatively moderate the inhibitory effect of local government hidden debts on economic growth, and the negative moderating effect of fiscal transparency is stronger. This indicates that the improvement of fiscal transparency has more effectively alleviated the negative impact of implicit debt on economic growth than financial development, strengthened the predictability of the government’s financial situation and market trust, and thereby optimized the trajectory of economic growth to a certain extent. This reinforcing effect mainly stems from its improvement of the openness and information symmetry of local government finances (Y. H. Li et al., 2024). Enhancing fiscal transparency means that the government’s fiscal situation, debt level and spending decisions will be more open and transparent, which will help the market, investors and the public form more rational expectations. When the financial situation of local governments can be clearly presented, the sustainability of debt expansion is subject to more regulation and social supervision. Local governments will be more cautious in financing, avoiding excessive accumulation of hidden debts (Wan, 2025). Therefore, fiscal transparency directly affects the management level of government debt by increasing the transparency and accessibility of information, and thereby strengthens its positive regulatory effect on economic growth. Confirmed research Hypothesis 2.

Meanwhile, the symmetry axes of both are less than −9.4604 in Table 2, indicating that the negative moderating effects of financial development and fiscal transparency have significant nonlinear characteristics on the impact of local government implicit debts on economic growth. With the improvement of these two variables, the inhibitory effect of local government implicit debt on economic growth gradually weakens, but its marginal effect shows a decreasing trend after a certain threshold. A lower value of the symmetry axis indicates that after controlling for the moderating effects of financial development and fiscal transparency, the inhibitory effect of implicit debt on economic growth has not been completely eliminated but has tended to stabilize, suggesting that even in the context of improved financial environment and fiscal transparency, the burden of local government debt still has a certain economic inhibitory effect.

Conclusions, Policy Recommendations, and Limitations

Conclusions

Based on the analysis of the impact of local government implicit debts on the economic growth of Chinese cities, and combining the level of financial development and fiscal transparency as moderating variables, this paper systematically examines the mechanism of implicit debts on economic growth. The research has reached the following main conclusions: Firstly, local government implicit debts have a significant inhibitory effect on the economic growth of Chinese cities, which has been verified in both the first-term model and the second-term model. Moreover, after replacing the core explanatory variables, adjusting the sample size, and conducting robustness tests such as lag periods, this inhibitory effect remains significant. Secondly, at the same debt level, cities with low GDP, non-resource-based cities and cities in non-eastern regions have more limited fiscal space when achieving maximum economic growth, indicating that these regions are facing more severe debt burdens and economic growth bottlenecks. Finally, the improvement of financial development levels and fiscal transparency can significantly and negatively regulate the inhibitory effect of local government implicit debts on economic growth. Among them, the regulatory role of fiscal transparency is particularly prominent, reflecting its key role in improving government fiscal management and enhancing market trust.

Policy Recommendations

Based on the above conclusions, this paper puts forward the following suggestions:

First of all, enhance local fiscal transparency and debt management. First, establish and improve the mechanism for making local government debts public and transparent. It is suggested that the government further improve the local government debt information disclosure system, promote comprehensive, timely and accurate fiscal information disclosure, especially the transparent management of hidden debts. By formulating specific laws and regulations, local governments are required to issue debt reports on a quarterly and annual basis, and third-party audits of the report contents should be strengthened. This can effectively reduce the potential risks of hidden debts, enhance the government’s fiscal management capabilities, and increase the market’s trust in local governments. Second, promote the auditing and accountability mechanism for local government debts. All levels of government should conduct regular debt risk assessments and introduce independent auditing institutions to review local government debts. For cities with hidden debt risks, a risk early warning mechanism should be implemented. If debt issues are identified, timely countermeasures should be taken, responsibilities should be clearly defined, and it should be ensured that local governments bear clear responsibilities for the burden and repayment of debts. Third, establish a transparent fiscal performance evaluation system. Regularly assess the fiscal expenditure, debt utilization and economic growth effects of local governments, and make the assessment results public. Transparent assessment of local government fiscal performance can enhance the financial constraints of local governments, prompt them to plan their debts more reasonably, and help increase the trust of society and the market in local fiscal management.

Secondly, optimize the debt financing structure of local governments and enhance financing efficiency. First, encourage local governments to rely on diversified financing channels. In addition to traditional bank loans and fiscal bond financing, it is suggested that local governments be encouraged to issue various financing tools such as local government special bonds and asset securitization products through the capital market to reduce reliance on hidden debts and enhance the transparency and sustainability of financing. Especially in regions with rapid economic development and strong financial resources, the scale of debt and financing structure can be regulated through moderate debt marketization. Second, establish and improve the market-based assessment mechanism for local debts. Local governments should conduct market-based pricing of debts through credit rating systems and enhance the role of market mechanisms in debt financing. For regions with relatively high debt levels, credit ratings should be adopted to gradually reduce the financing costs of implicit debts, and financing instruments should be priced based on debt risks to enhance the marketization level of debt management. Third, strengthen the cooperation mechanism between local governments and financial institutions. Establish a long-term cooperation mechanism between local governments, commercial banks and investment institutions to provide more stable and low-cost financing channels for local economic development. Meanwhile, a risk-sharing mechanism for local government financing should be established to ensure that the risks of financial institutions in areas such as loans and bond investments can be reasonably evaluated and managed.

Finally, implement differentiated policies in accordance with local conditions to promote coordinated regional economic development. First, increase fiscal support for cities with low GDP and resource-based cities. For cities with low GDP and resource-based cities, the government should increase the intensity of fiscal transfer payments, alleviate the fiscal pressure on local governments by supplementing fiscal revenue, and reduce the debt burden. Meanwhile, local governments should be guided to gradually achieve stable growth in fiscal revenue and reduce reliance on debt by promoting industrial upgrading and diversifying the economic structure. Second, implement differentiated policies for regional economies. Formulate differentiated economic support policies based on the economic development levels of different regions. For instance, in the developed eastern coastal areas, the scale of debt can be adjusted through market-oriented means to promote local fiscal self-sufficiency. For the central and western regions and resource-based cities, efforts should be made to optimize the industrial structure and enhance the level of technological innovation to help these regions get out of the debt predicament and promote sustainable economic development. Third, promote regional integration and infrastructure connectivity. By strengthening regional economic cooperation and promoting the connectivity and sharing of infrastructure, the economic vitality of underdeveloped regions can be enhanced. The government can encourage local governments and enterprises to jointly invest in public infrastructure construction through the approach of “guiding funds + policy support,” improve the local economic foundation, enhance the coordination of economic development among regions, and reduce the fiscal pressure caused by regional debt differences.

Limitations

First, the breadth and depth of sample selection are insufficient. Although this study adopted the overall data of Chinese cities for analysis, it failed to delve into the level of specific enterprises, especially as there might be significant differences in the sensitivity of different types of enterprises to local government implicit debts. For instance, state-owned enterprises and private enterprises may differ in their capacity to bear government debt burdens, access to resources and financing channels. Future research can further refine the sample from the enterprise level, analyze how enterprises of different scales, natures and industries are affected by local government implicit debts, and thereby reveal more detailed mechanisms of action. This refinement will help to understand more accurately the transmission path of implicit debt to economic growth.

Second, the complexity of the mechanism of action needs to be expanded. Although this article proposes the level of financial development and fiscal transparency as moderating variables, the exploration of their mechanisms of action is still rather simplistic. Local government implicit debts may affect economic growth through various channels, including the impact of government debts on local investment efficiency, resource allocation, and the stability of local financial markets. Future research should examine these multi-dimensional mechanisms of action more systematically, especially the impact of local debt on the efficiency of resource allocation, innovation capacity, employment structure, and industrial structure adjustment, etc. This can provide a more comprehensive and in-depth analytical framework, revealing how implicit debts affect economic growth through various channels.

Third, the diversity of perspectives on economic growth is insufficient. This study analyzes the impact of local government implicit debts on urban economic growth from a macro perspective, but fails to further refine the different dimensions of economic growth. For instance, local government implicit debts may have different impacts on short-term and long-term economic growth, and their mechanisms and transmission effects may also change over time. Furthermore, the differences in economic development levels, industrial structures and policy backgrounds among various regions may lead to heterogeneity in the impact of implicit debts on economic growth. Future research can adopt multi-level economic growth models, taking into account dimensions such as long-term growth, structural growth, and productivity growth, thereby providing a more detailed explanation for the diverse impacts of implicit debt on economic growth.

Footnotes

Acknowledgements

We would like to express our sincere gratitude to the funding organization. We appreciate the insightful comments and suggestions provided by the anonymous reviewers.

Ethical Considerations

This study did not involve human participants or animal subjects and therefore did not require ethical approval.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by China Ministry of Education’s Humanities and Social Sciences Project “Research on the Impact of External Shocks on Local Fiscal Sustainability and Underlying Mechanisms” (23YJC790201).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data used to support the findings of this study are available from the corresponding author upon request.