Abstract

Women’s empowerment (WE) is one of the main challenges to economic development in African countries. Scholars have criticized national development initiatives to focus on well-being issues and treat women as the passive beneficiaries of welfare-enhancing assistance. This study uses panel fully modified least square and vector error correction model to investigate the impact of interactive effects of WE and financial development (FD) on employment and economic growth based on the World Bank income group as follows: upper-middle-income countries (UMIC), lower-middle-income countries (LMIC), and low-income countries (LIC). The findings show that the interactive effects of WE and FD on output and employment is not significant in the long run in LMIC and LIC. Despite the significance of these interactive effects in UMIC, the coefficient is less than one. Also, the causality result in the UMIC shows feedback between WE and economic growth. And that FD has a direct influence on growth in LMIC, while WE has a direct influence on employment in LIC.

Introduction

The empowerment of women ensures that women have the same rights as men and are not oppressed in respect of their societal benefits. It is also a vital issue related to improving aggregate welfare. Economic growth is encouraged if women continue to thrive and quickly enhance their educational level, job training, and skills (King & Mason, 2001; Mcilongo & Strydom, 2021). Women’s empowerment has received a great deal of attention recently and it is widely regarded as a critical development investment for countries (Kaffenberger & Pritchett, 2021).

The Millenium Development Goal (MDG) Goal 3 encourages nations to promote gender equality and women’s empowerment through education as a practical strategy to address poverty, hunger and disease in order to achieve sustainable development. Women’s empowerment (WE) is critical to the health and progress of families and countries. Women can attain their tremendous potential when living in a safe and productive environment. They can contribute their abilities to the labor force, while also achieving other parental goals. A similar objective was stressed by the Sustainable Development Goal (SDG) Goal 4, which emphasizes the importance of quality education. According to the SDG report there has been remarkable successes of female schooling in African countries. However, more effort is needed to reduce the disparities between genders. The notion that education is one of the most efficient factors for sustainable development is reaffirmed by achieving inclusive and high-quality education for everyone.

In addition, South Africa’s National Development Plan (NDP) 2030 considers child development a high priority and emphasizes the need to promote educational quality to improve the long-term opportunities of future generations; highlighting the importance of diverting resources toward ensuring that all children are adequately cared for and get sufficient emotional, cognitive and physical growth at a young age. Similarly, the African region has shown a strong commitment to gender equality and women’s empowerment. Almost all countries have ratified the convention on eliminating all forms of discrimination against women. Furthermore, the African Union’s Protocol on the rights of women in Africa has been adopted by more than half of the Union’s member States. Yet, despite all these efforts, women remain disempowered and gender inequalities persist in developing economies, especially in African countries (Lecoutere, 2017; Netnou & Strydom, 2020; The World Bank, 2012).

Female entrepreneurs receive a disproportionately small amount of funding compared to their male counterparts. In comparison to male entrepreneurs, women entrepreneurs have limited access to information, education, training, credit and networks, which affects economic growth and employment. The lack of female representation in the financial investment decision-making process is one of the most frequently cited reasons for this disparity (Groza et al., 2020; Handaragama & Kusakabe, 2021). Consequently, in international law and policy, the right to education has been recognized as a “multiplier right,” allowing right-holders to exercise a wide range of human rights when fully realized (Wodon et al., 2018). Therefore, women empowered by education can increase their standard of living, access to information and investment opportunities. And this also serves as a springboard for women’s advancement in various fields. Hence, it is presumed to be a fundamental tool that women should be given to fulfill their role as contributing members of society (Engida, 2021; Mbukanma & Strydom, 2021; Tomasevski, 2003). The connection between education and economic growth has been established in the literature (Kaffenberger & Pritchett, 2021; Monteils, 2002). Education directly impacts economic growth because it is a crucial determinant or component of human capital and has an indirect impact by influencing production factors and total factor productivity.

African countries are a combination of low- and middle-income countries however, in most countries irrespective of income level, gender disparity regarding empowerment through education is notable (Lecoutere, 2017; The World Bank, 2012). Although, economic growth, poverty reduction and political accountability have all improved dramatically in middle-upper income African economies, a combination of economic reform and political change sparked the turnaround. Regardless of the challenges and risks that the countries of “upper-medium-income economies in Africa” face, they appear to be on the right track. A vast array of empirical and theoretical literature has documented linkages between financial development (FD), economic growth, employment, and empowerment (Abubakar et al., 2015; Engida, 2021; Friedman, 2016; Groza et al., 2020; Handaragama & Kusakabe, 2021; Obadiaru et al., 2018; Todaro & Smith, 2003). Most of these studies demonstrate that financial development has a positive impact on economic growth and employment in two ways: first, by increasing the savings rate, which, in turn, will increase the level of investment and capital accumulation; and secondly, by improving the efficient allocation of investment, thereby increasing investment economic growth and employment in the long run (Asaleye et al., 2020; Levine, 1997). However, the empirical literature has given little attention to the importance of women’s empowerment and its connection to financial development to promote economic growth and employment.

Previous studies relating to women’s empowerment have focused on the implication of financial decision making, business networks, entrepreneurs, and mentors (Groza et al., 2020; Handaragama & Kusakabe, 2021; Kochar et al., 2022; Mbukanma & Strydom, 2022; Rink & Barros, 2021; Sell & Minot, 2018; Strydom & Fourie, 2018). In addition, other empirical works analyzed social media effects, managing diversity, cooperative societies, and reforms (Bonilla et al., 2017; Inegbedion et al., 2020; Lecoutere, 2017; Luppicini & Saleh, 2017; Reichel, 2020; Topal, 2019). However, few examine the effect of education and improvement on life, gender bias, and globalization (Guinée, 2014; Kaffenberger & Pritchett, 2021; Kucera & Milberg, 2000; Martinez & Rambaud, 2019; Neumayer & de Soysa, 2011). Therefore, the main objective of this research, which distinguishes it from previous studies, is to investigate the interactive impact of WE and FD on economic growth and employment in selected African countries based on the level of income by the World Bank 2022 fiscal year (i.e., the upper-middle-income, the lower-middle-income, and low-income countries). The specific objectives are as follows:

To analyze the long-run effect of WE and FD on economic growth.

To investigate the long-run impact of WE and FD on employment.

To examine the causal relationship between WE, FD, employment, and economic growth in selected African countries.

The hypotheses for this study are stated in null form as follows: there are no significant long run effects of WE and FD on economic growth; there is no significant long-run impact of WE and FD on employment; Finally, there is no significant causal relationship between WE, FD, employment, and economic growth in selected African countries.

The rest of this paper is structured as follows: Section 2 presents the literature review; Section 3 describes the method employed, which involves the model specification and analysis techniques to achieve the study’s objectives; Section 4 presents the main results and the discussion of the results; and Section 5 concludes the paper.

Literature Review

First, in the conceptualization of WE and education, WE has received theoretical attention. It is described as “one of the major challenges in development for many nations today” (Engida, 2021; Isaacs et al., 2022). A. Sen (1999) criticized pervious national development initiatives for being focussed on well-being issues and for treating women as “passive beneficiaries of welfare-enhancing assistance.” This perspective has also been shared in recent studies by Demartini (2019), Bayeh (2016), and G. Sen (2016). These researchers acknowledging women as active agents of change who can affect change independently. Women’s empowerment is about acquiring agency and voice by women. Together with A. Sen (1999) conceptions of capacities (the sum of resources and education as a precondition to the agency; i.e., the conditions under which individuals make choices) and functioning (the modes of being and doing), these claims emphasize the centrality of individual agency. Also, Kabeer (2000) recognizes three levels of empowerment: the “deeper” level, or knowledge of interlinkages such as the interaction of class, social position and sex or race; the intermediate level, or an understanding of institutional rules and assets; and the immediate level, or the set of financial activities, agency and achievements. As a result, Kabeer’s (2000) idea corrects the propensity to debate empowerment at the superficial and intermediate levels, while ignoring deeper cause and effect links. The scholar’s definition of empowerment considers the requirement for follow-up action. According to whom—Kabeer (2000) empowerment is “the extension of people’s ability to make strategic decisions in situations where the ability was previously denied to them.” Education can significantly influence the development of such “ability.” This paper focuses on education as a means of women’s empowerment.

Secondly, there is no consensus on theoretically transmission channels between economic growth, FD, employment and WE. Studies have emphasized that standpoint for economic development mainstream is to eliminate poverty through the creation of employment and social inequity by first focusing on increasing the growth rate and investment. (Asaleye et al., 2017; Coccia, 2019; Oloni et al., 2017; Todaro & Smith, 2003); after which, everything else will fall into place. According to this theory, increases in production and financial development will have “trickle-down” effects on education, literacy, health conditions, agency and equality. On the other hand, Friedman (2016) and Preiss (2015) stressed a market-oriented approach to inequalities, in which economic arrangements determine power distribution and concentration. As the focus of this study, WE is envisaged as a means to improve female life skills that are likely to increase their ability to be more productive and earn a higher income, to save and to invest (promoting financial development). So, according to Friedman (2016) and Preiss (2015), there is a link between improved life skills and increased earning power, rather than the other way around. Despite the diversity in the transmission channels, both theories show the linkages and the importance of empowerment and FD to promote economic growth and employment.

Empirically, two main channels, among others, are identified in which financial development affects the economy. The first is the causal impact channel (Asaleye et al., 2018; Campbell & Asaleye, 2016; Desbordes & Wei, 2017). The second is the long impact channel (Asaleye Adama & Ogunjobi, 2018; Shaikh et al., 2017). Based on this, the objective of this study is structured to investigate the long-run and the causal effect on WE and FD on employment and economic growth. However, studies on the impact of FD and WE on economic growth and employment are scanty. Mtar and Belazreg (2023) show that there is negative relationship between trade openness and economic growth in 11 European countries. Also, Baert et al. (2022) reported that there is positive relationship between school enrollment and employment. Asaleye and Strydom (2022) also reported that human capital via secondary enrollment promote economic growth. A survey by Kochar et al. (2022) discovered that community investment funds significantly impact on women’s decision-making and intra-household allocations in India. Women’s education has long been regarded as one of the best investments in development, according to Kaffenberger and Pritchett (2021). The authors show that the association between women’s education and life outcomes is much more significant than the standard estimates of gains from schooling alone. According to Handaragama and Kusakabe (2021), looked at how business associations can help and empower women entrepreneurs. They documented that women’s participation, on the other hand, is limited to low-level positions, preventing women from reaping many of the potential benefits of financial development.

Furthermore, Rink and Barros (2021) report that households in which women are empowered spend more on welfare-enhancing goods, such as food, but are less likely to have savings left at the end of the month; this, in the long run, tends to affect their financial investment decisions. A study by Luppicini and Saleh (2017) stressed the need for women to be empowered financially. Likewise, the findings of Kucera and Milberg (2000) show that gender bias does not exist but presume that female participation may improve financial development. In a similar study, Neumayer and de Soysa (2011) concluded that there is consistent evidence for the spillover effects on women’s empowerment via trade links, except in low-income countries. A study by Martinez and Rambaud (2019) shows that the presence of more women on boards of directors is linked to improved financial development performance of companies. In addition, Bonilla et al. (2017) showed that social cash transfer helped women control household investment and emergency savings, which increased their financial empowerment and economic growth. More so, Guinée (2014) argued that, while education has the potential to be an influential empowering factor, it cannot be considered in isolation of the social influences and intimate relationships that are so important in women’s lives.

Consequently, Reichel (2020) concluded that there is gender equity bias; men are more engaged at all levels of the project design than women. Likewise, Groza et al. (2020) reported that female backers support internal and external social ties more than male backers when deciding which projects to support. Also, Topal (2019) stressed that women’s empowerment increases economic integration, economic growth and employment; while a study by Sell and Minot (2018) pointed out that education is associated with higher employment rates. Finally, Lecoutere (2017) reported that women’s empowerment can be boosted by being a member of cooperative since this positively impacts on economic well-being, increases economic growth, knowledge and the adoption of agronomic practices, specifically by women.

The measurement of financial development has been discussed extensively in the literature. Cihak et al. (2013) choose the credit to private sector to GDP ratio and, for the depth of financial markets, stock market capitalization plus outstanding domestic private debt instruments as a percentage of GDP. Although different metrics have been attributed to financial development, these are some of the most often used financial system measurements. In addition, a measure of broad money (M2 or M3) is used to indicate financial development (Abubakar et al., 2015). Other notable measurements include the domestic credit-to-GDP ratio, commercial bank credit-to-GDP ratio, and financial sector liquid liabilities-to-GDP ratio (Ahlin & Pang, 2008; Benhabib & Spiegel, 2000). In this paper, we use three measures for financial development indicators: private credit as a percentage of GDP, the ratio of liquid liabilities to GDP and, finally, domestic credit to the private sector as a percentage of GDP. On the linkage or interactive of FD and WE, economic growth may be influenced by FD and the level of education used to promote the empowerment of women. However, an interacting influence from WE and FD might also be hypothesized. For example, the risk-taking abilities of individuals may grow as women’s empowerment via education accelerates, increasing investment demand and loan demand. A higher level of financial development is more likely to promote investment in some sort of enterprise by acquiring a loan. As a result, the combined benefits WE and finance on economic growth and employment may be more significant than their separate contributions.

From the foregoing, increased investments in education and FD could have catalytic and multiplier effects on the lives of women and girls, including future generations, which may increase economic growth and employment levels. Therefore, the primary goal of this study is to add to the literature by examining the interaction of WE and FD on employment and economic growth in African countries based on the evidence obtained from the limited studies above and the diverse nature of the theoretical perspective.

Method

Theoretical Framework

The theoretical framework of this study takes its base from the neoclassical growth model, with emphasis on investment in human capital as a vital input in the production process. Hence, the production function can be given as:

In Equation 1, PG is the economic growth, AC is the augmented variable used in production, EM and CA are employment and the capital inputs used in production respectively.

In Equation 2, let

Financial development and human capital variable (measured by women’s education attainment—women’s empowerment) are added to Equation 3 and results to:

Where “fd” and “we” represent financial development and women’s empowerment respectively. In order to achieve the objectives of this paper, we normalized on economic growth and employment variables to establish two equations as follows:

So, in this case, there are two dependent variables, namely economic growth and employment. Likewise, the interactive term between FD and WE was introduced given by

Model Specification and Technique of Analysis

The control variables considered in this study, based on their importance established in empirical literature, are exchange rate, consumer price index (CPI) and trade openness (Asaleye et al., 2018, 2021; Nchofoung, 2022). Following the model by Asaleye et al. (2018), with slight adjustment to meet the objective of this study, Equations 5 and 6 are given as:

In Equations 7 and 8, “ex,”“cp,” and “to” represent exchange rate, CPI and trade openness, respectively. The model is estimated using panel fully modified least square (FMOLS). Equations 7 and 8 will involve carrying out four separate analyses, as earlier mentioned: an aggregate model for all the sub-Sahara Africa countries used in this study and separate analyses for upper-middle-, lower-middle-, and low-income countries based on the World Bank income groups.

We solve the possibility of spurious regressions with panel cointegration and panel unit root tests. We examine the order of integration of the variables and if they are non-stationary. In the presence of cointegrated variables, a linear combination of the non-stationary variables is stationary. Various tests have been started in the literature to test the unit root and the most common are Levin et al. (2002) (LLC) and Im et al. (2003) (IPS). Following the test outline by Levin et al. (2002) given as:

In Equation 9, the time is defined by

Likewise, using the IPS test, individual effects, time trends and common time impacts for heterogeneous panels are all possible (Im et al., 2003). The test is based on individual Augmented Dickey-Fuller (ADF) regressions in a dynamic panel framework and permits variability across units. The equation is different from (9). Then, after the panel unit root, we test for the presence of cointegration.

As mentioned earlier, we explore FMOLS to estimate the long-run behavior of economic growth and employment equations. The Panel FMOLS is computed by simply considering an n-dimensional I (1) process, as illustrated in

The error term

Where

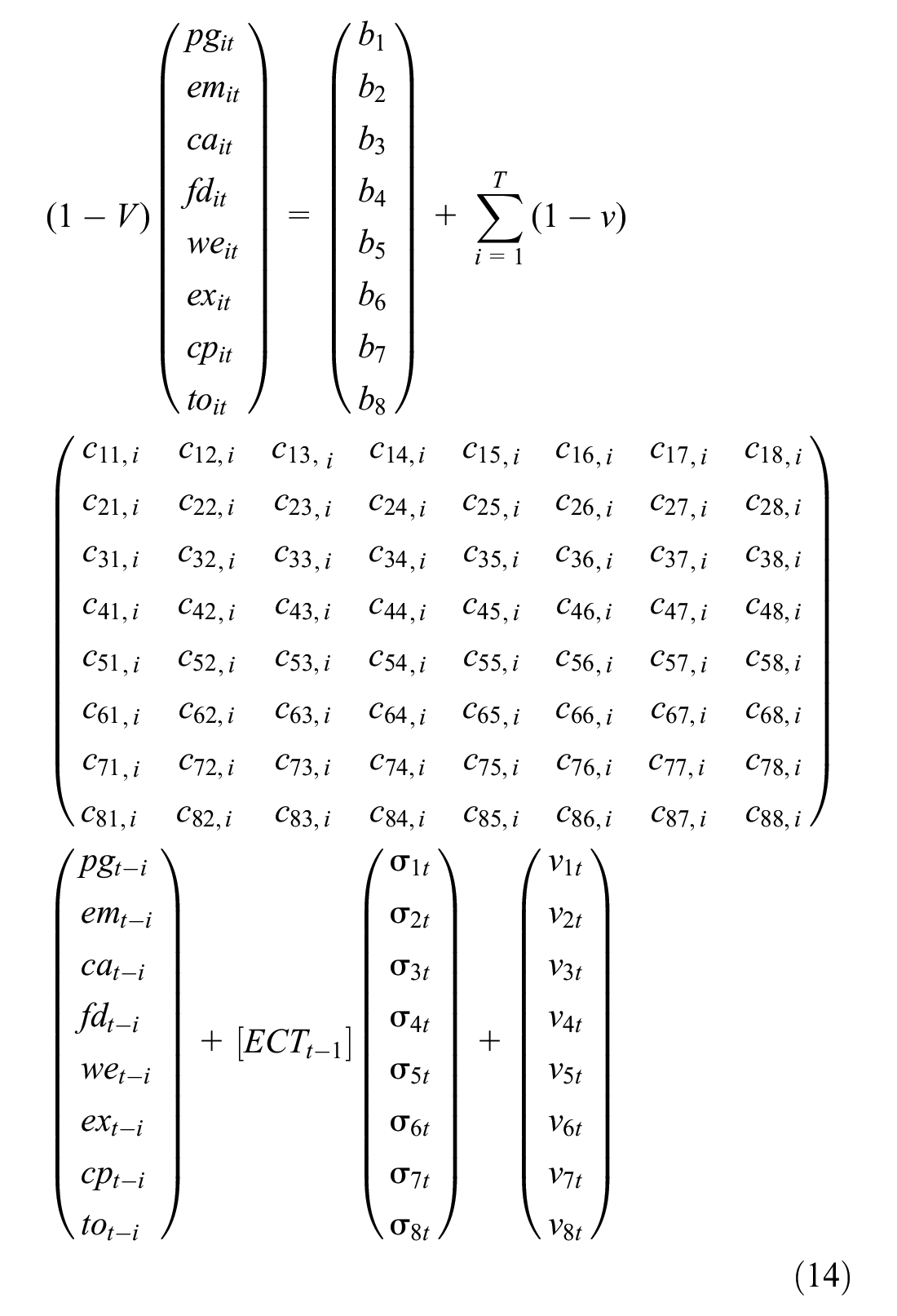

Finally, using the panel vector error correction model (VECM), we establish the causal link between the variables as follows:

In Equation 14, the differenced term is

Data Measurement, Sources, and A Prior Expectations

This study involves an analysis of the impact of interactions of WE and FD on economic growth and employment in 21 selected African counties, which are divided into three regions based on World Bank income group. The upper-middle-income countries comprises of Botswana, Gabon, Mauritius, Namibia, South Africa, Equatorial Guinea, and Libya. The lower-middle-income countries include Cameroun, Ghana, Mauritania, Nigeria, Senegal, Eswatini, and Tanzania. Finally, countries in the category of low-income economies are Rwanda, Niger, Malawi, Mozambique, Mali, Lesotho, and Ethiopia. The period of the study covers 1992 to 2020 because of the availability of data. The source of data and measurement are presented in Table 1.

Data Measurement and A Prior Expectation.

Source. Authors’ computation.

A Prior Expectations

Economic growth/employment and the exchange rate are likely to have a negative or positive relationship. The impact of currency depreciation on employment and economic growth is assumed to be either positive or negative. Devaluation weakens the currency compared to its international counterparts, making exports cheaper in the foreign market, promoting long-term export sales and improving the balance of payments. The rise in exports and decrease in imports will increase growth. The profit from exportation acts as a stimulant, causing the labor market to improve. On the other hand, currency depreciation due to “negative anticipation” may result in cost-push inflationary pressure. In the short-run, demand for imported goods may also be price-elastic. If a country relies on raw material imports, devaluation will result in poorer output and employment because of weaker competitiveness.

According to theory, the CPI and employment positively connect. The Phillips curve demonstrates how the unemployment rate and inflation rate are linked. The link between economic growth/employment and capital is predicted to be positive; this is supported by the growth model, which indicates a positive relationship between output and capital; an increase in capital-driven production would boost employment over time. The effect of trade openness on economic growth and employment depends on the level of competitiveness. In terms of the new trade theory (NTT), if countries have a high degree of competitiveness compared to their counterparts, they will reap benefits from trade. However, if they do not, trade will worsen the economy, negatively affecting economic growth and employment. Financial development and women’s empowerment are expected to positively impact growth and employment. The control variables used in this study are exchange rate, consumer price index and trade openness; the rationale for inclusion is based on the relevance as shown in empirical literature (Ogundipe et al., 2019; Friedman, 2016; Kabeer, 2000; Popoola et al., 2019; A. Sen, 1999; Todaro & Smith, 2003).

Results and Interpretation

Preliminary Test

The preliminary test in this study involves descriptive statistics, the unit root test and the cointegration test. Table 2 presents the descriptive statistics of the aggregate model variables (which comprises the upper- middle-income countries, lower-middle-income, and low-income countries) and separate for upper-middle-income countries, lower-middle-income countries and low-income countries from 1992 to 2020. In the aggregate model, gross capital formation (ca) has the highest mean value, maximum at 507.95 and minimum at −76.31. The standard deviation is 33.27. WE measured by female secondary school enrolling has a mean value of 1.65 and a standard deviation of 0.07. The financial indicators (fd_1 and fd_2) variables have the lowest values, with approximately 1.17%. In the upper- middle -income countries group, economic growth (pg) has the highest mean value of 5.4%, with a standard deviation of 17.0.

Descriptive Statistics.

Source. Author’s computation.

The financial indicators, domestic credit to the private sector by financial corporations (fd_1) and domestic credit to the private sector by banks (fd_2), have mean values of 1.38 and 1.41 with a standard deviation of 0.41 and 0.46, respectively. Likewise, in the lower-middle-income countries group, the economic growth (pg) is 4.07%, with a standard deviation of 3.21. On the other hand, the financial indicators, domestic credit to the private sector by financial corporations (fd_1) and domestic credit to the private sector by banks (fd_2), have mean values of 1.08 and 1.07, a standard deviation of 0.32 and 0.31, respectively. Finally, in the low-income countries group, economic growth (pg) is 5.58% with a standard deviation of 4.82. On the other hand, the financial indicators, domestic credit to the private sector by financial corporations (fd_1) and domestic credit to the private sector by banks (fd_2), have mean values of 1.04 and 1.06, a standard deviation of 0.24 and 0.23, respectively.

In conclusion, the upper-middle-income countries group has the highest mean value for WE, followed by the lower-medium-income and low-income countries. In addition, the mean values of the FD indicators follow the same tread. However, the low-income countries have the highest mean value of 1.85%, followed by lower-middle-income countries with 1.75%. The mean value of upper-middle-income countries stands at 1.65%.

Table 3 shows the results of the unit root test. This study employed three different unit testing types for robustness and for ensuring that the unit root tests are free of bias: Levin, Lin, and Chu; Im, Pesaran, and Shin; and ADF-Fisher test. The unit root analysis also involved two stages, first with constant (C) and second with intercept and tread (I&T). At levels, most variables are not stationary at 5% significance except for WE for Levin, Lin, and Chu. However, all the variables are stationary at first differencing at 5% significance level. After confirming that all variables are integrated at order one, the cointegration test is performed. The Johansen-Fisher panel cointegration test and Kao residual cointegration test are used to analyze the cointegration of variables. Table 4 shows the results of the panel cointegration for all four models. The null hypothesis is that the variables have no cointegration. Given the outcome of the finding, the results suggest that this null hypothesis cannot be accepted, with the significance at 5%. The findings revealed that economic growth, WE, gross capital formation, employment, FD indicators, CPI, exchange rate, and trade openness have a long-term relationship. This finding is in line with previous studies, such as Asaleye and Strydom (2022), Popoola et al. (2019), and Lawal et al. (2016). Based on this conclusion, we estimate the model’s long-run equation.

Unit Root Test Result for Aggregate Model.

Source. Authors’ computation.

Panel Cointegration Test.

Source. Authors’ computation.

and **, and show significance @ 1% and 5%, respectively.

Evaluation of Hypotheses

Evaluation of Hypothesis 1

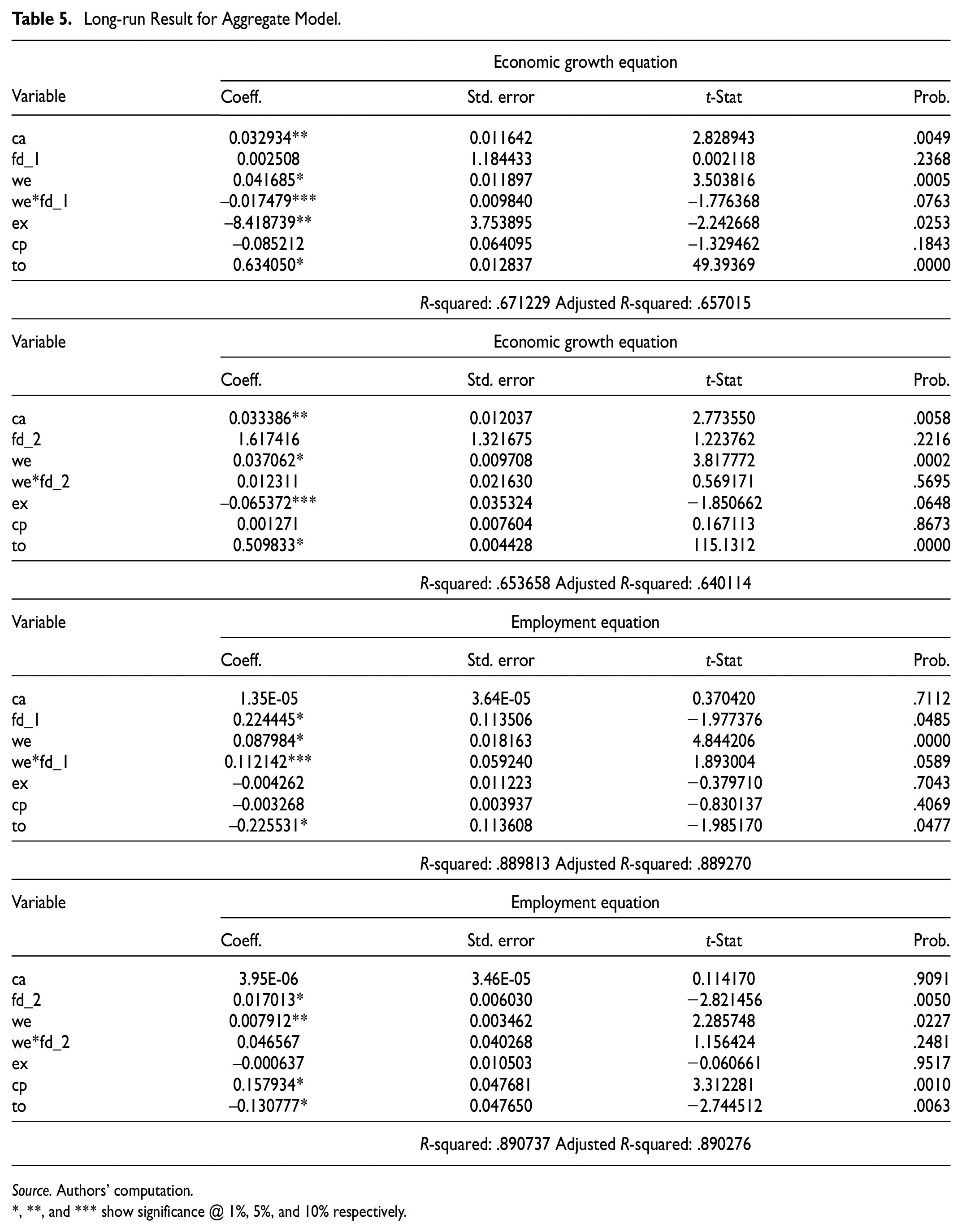

The null hypothesis is that there are no significant long effects of WE and FD on economic growth; this hypothesis is rejected because evidence from the result in Tables 5 and 6 shows that WE and FD have long-run effects on economic growth in the four models considered in this study, that is the aggregate group of income countries (AGIC), upper-middle income countries (UMIC), lower-middle income countries (LMIC), and low-income countries (LIC). The discussion of the result is given below.

Long-run Result for Aggregate Model.

Source. Authors’ computation.

**, and *** show significance @ 1%, 5%, and 10% respectively.

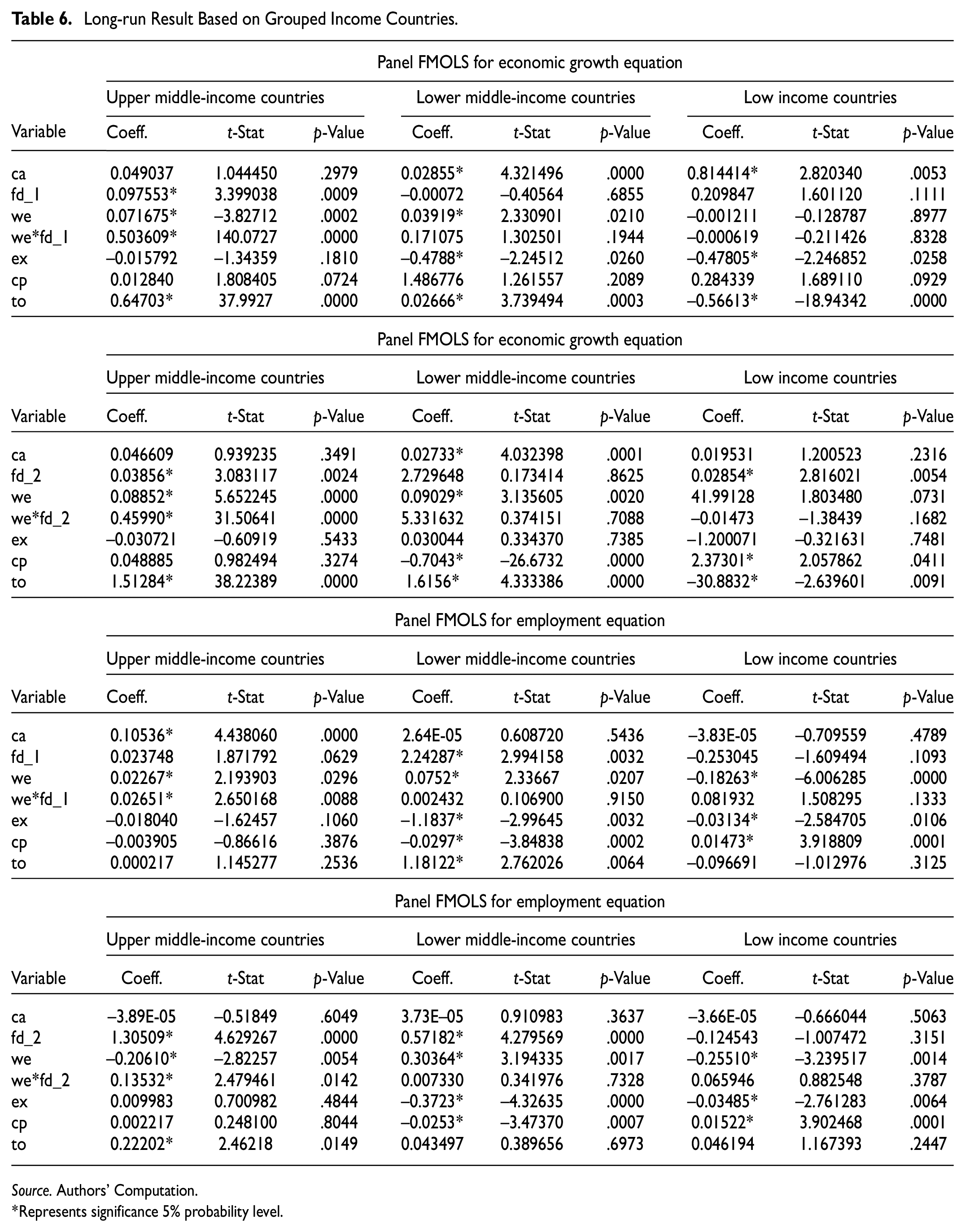

Long-run Result Based on Grouped Income Countries.

Source. Authors’ Computation.

Represents significance 5% probability level.

Aggregate Group of Income Countries (AGIC)

The long run of the first model (all categories of income countries) is presented in Table 5. Using the baseline of 5% significance level, the economic growth equation interactive with the first and second FD indicators shows that capital, WE and trade openness are positively related with the dependent variable; this finding contradict the study by Mtar and Belazreg (2023), who document negative relationship between trade openness and economic growth in 11 European countries. The exchange rate has a negative relationship with economic growth at 5% significance level in the first growth equation (i.e., the first interactive FD indicator) and at 10% significance level in the second equation (i.e., interactive with the second FD indicator). Both FD indicators are not statistically significant with economic growth. The first FD indicator interactive with WE negatively affect growth, while the second is not statistically significant; however, this outcome contradicts the study of Kochar et al. (2022).

The long-run result based on the categories of the income countries is presented in Table 6 and the baseline of 5% significance is used.

Upper-Middle Income Countries (UMIC)

The economic growth equation interactive with first and second FD indicators shows that FD, WE, interactives of WE with FD indicators and trade openness are positively related to the dependent variable. Likewise, the CPI is positively related to employment at 10% in the first FD interactive and not statistically significant in the second. The Phillips curve demonstrates employment rate and inflation rate has positive correlation, a moderate inflation rate is needed to promote growth. Likewise, gross capital formation and exchange rate are not statistically significant; the outcome of the result is not in line with the theoretical prediction of this study. One of the reasons for this result may be due to low rate of investment in the region.

Lower-Middle Income Countries (LMIC)

The economic growth equation for both interactive models shows that capital, WE, and trade openness are positively related to the dependent variable. On the other hand, FD indicators, the interactive of WE and FD indicators are not statistically significant. However, the exchange rate negatively affects employment in the first interactive model but is insignificant in the second. Also, in the second interactive model, the CPI is negatively related to the dependent variable.

Low-Income Countries (LIC)

In the economic growth equation first interactive model, gross fixed capital formation has a positive relationship to the dependent variable, while exchange rate and trade openness have a negative relationship to the dependent variable. FD indicators, WE and interactive of WE with FD indicators and consumer price are not statistically significant. In the second interactive model for the economic growth equation, the FD indicator is positively related to growth. In comparison, the CPI and trade openness are negatively related to economic growth. Gross capital formation, WE, interactive of FD and WE, and exchange rate are not significant with economic growth.

Evaluation of Hypothesis 2

The null hypothesis is that there is no significant long-run impact of WE and FD on employment; this hypothesis is rejected because evidence from the result in Tables 5 and 6 shows that WE and FD have long-run effects on employment in the four models considered in this study, that is, the aggregate group of income countries (AGIC), upper-middle income countries (UMIC), lower-middle income countries (LMIC), and low-income countries (LIC). The discussion of the result is given below.

Aggregate Group of Income Countries (AGIC)

In Table 5, the employment equation interactive with the first and second FD indicators depicts that FD indicators and WE are positively related to employment. At the same time, trade openness is negatively related to employment. Capital and exchange rate are not statistically significant. Although the first FD indicator interactive with WE has a negative relationship to employment, at 10% significance level, the second is not statistically significant. In conclusion, evidence from the results indicate that WE promote economic growth and employment in the AGIC. These findings are in line with studies of Baert et al. (2022), Kaffenberger and Pritchett (2021), Abubakar et al. (2015), and Benhabib and Spiegel (2000). Despite this positive relationship, the coefficient of WE on employment and economic growth is very low (less than 1%). However, FD indicators are not statistically significant. The findings contradict the studies by Asaleye et al. (2018) and Lawal et al. (2016).

The long-run result based on the categories of the income countries is presented in Table 6 and the baseline of 5% significance is used.

Upper-Middle Income Countries (UMIC)

The employment equation interactive with first and second FD indicators depicts that WE and the interactive of WE with FD are positively related to employment. In contrast, the exchange rate and CPI are not statistically significant. However, gross capital formation is positively related to employment in the first interactive model, while not significant in the second interactive model. Likewise, trade openness is positively related to employment in the second interactive model, while not significant in the first interactive model.

Lower-Middle Income Countries (LMIC)

The employment equation interactive with the first and second FD indicators depicts that FD indicators and WE are positively related to the dependent variable. In contrast, the exchange rate and CPI are negatively related to the dependent variable. Gross capital formation and the interactive of WE with FD indicators are not statistically significant. Trade openness has a positive relationship with employment in the first interactive model but negative in the second interactive model.

Low-Income Countries (LIC)

The employment equation interactive with the first and second FD indicators depicts that WE and the exchange rate have a negative relationship to the dependent variable. At the same time, the CPI has a positive connection to employment. Gross capital formation, FD indicators, WE interactive with FD and trade openness are not statistically significant with employment.

The overall conclusion in the UMIC and LMIC shows that women’s empowerment through secondary school enrollment can promote long-run growth and employment. These findings are in line with studies by Asaleye and Strydom (2022), Engida (2021), Guinée (2014), and Kaffenberger and Pritchett (2021), who stressed the benefits of adequate investment in the futures of women. However, the non-significance of WE on economic growth and employment in the LIC needs to be given adequate attention. Although theoretically, Todaro and Smith (2003) emphasize that an increase in production and FD will have “trickle-down” effects on education, literacy, health conditions, agency and equality. In addition, Friedman (2016) pointed out the need for linkages between empowerment and FD to promote growth and employment. The insignificance of FD indicators on employment and economic growth in the LIC, might be the reason for the insignificance of the interactive of WE and FD on growth and employment in the group.

Likewise, in the LMIC, the interactive of WE and FD to promote output and employment is not statistically significant in the long run. While in the UMIC, despite the significance of the interactive of WE and FD to promote output and employment, the coefficient is less than one. Various authors have stressed the benefits of FD and WE on the economy (Bonilla et al., 2017; Groza et al., 2020; Handaragama & Kusakabe, 2021; Kochar et al., 2022; Martinez & Rambaud, 2019; Netnou & Strydom, 2020; Rink & Barros, 2021).

Evaluation of Hypothesis 3

The null hypothesis is that there is no significant causal relationship between WE, FD, employment, and economic growth in selected African countries; this hypothesis is rejected because evidence from the result in Table 7 shows a causal relationship between WE, FD, employment, and economic growth in selected African countries. The discussion of the result is given below.

Panel Causality Result.

Source. Authors’ Computation.

Indicates significant at 5% level.

In causality test between “A” and “B,” we can have four results as follows: Bi-directional relationship, which is called feedback. It means that A and B granger cause each other. A can cause B, and at the same time, B can cause A; Secondly, Unidirectional relationship from A to B, meaning it is A that is causing B; thirdly, unidirectional relationship from B to A, meaning it is B that is causing A. Finally, independences—that is A is not causing B, and B is not causing A.

The panel causality result is presented in Table 7. The short-run causality in the aggregate model shows unidirectional causality running from WE to both FD indicators; this aligns with the findings of Mtar and Belazreg (2023). There is a bidirectional relationship between WE and economic growth in the upper-medium-income countries; this result indicates that there is feedback with the two variables. An attempt to improve WE will promote economic growth and vice versa. There is a unidirectional relationship from the FD indicators to growth in the lower-medium-income countries, which means that FD has a direct influence on economic growth. Finally, in low-income countries, there is a unidirectional relationship from WE to employment, which indicates that WE has a direct influence on employment.

In respect of the joint long-run causality, when economic growth is used as a dependent variable in the aggregate model, upper-medium-income countries and lower-medium-income countries, there is the presence of causality. Likewise, there is joint long-run causality when WE is used as a dependent variable in upper-medium-income countries and when the FD indicators are used as a dependent variable in lower-medium-income countries.

Conclusion and Policy Recommendations

Summary of the Work

This study investigates the interactive effects of women’s empowerment and financial development on employment and economic growth in African economies. The justification of this study is based on the challenges of women’s empowerment, especially in African economies where most national development initiatives focus on well-being issues and treat women as “passive beneficiaries of welfare-enhancing assistance”; coupled with limited studies on the implications of women’s empowerment and financial development on growth and employment, with the diverse nature of the theoretical perspectives. The results from this study are some of the first in study of financial development and women’s employment on economic growth and employment.

Theoretically, there is no consensus on the transmission channels between economic growth, financial development, employment and women’s empowerment. One perspective provided by scholars emphasized increasing economic growth and investment; after which, everything else will fall into place. Another viewpoint of scholars encourages linkages between improved life skills and increased earning power, rather than the other way around. However, despite the diversity in the transmission channels, both theories state the importance of empowerment and financial development to promote growth and employment. Empirically, two main channels, among others, are identified in which financial development affects the economy, the causal and long impacts. Given this, the study examines the long-run interactive effects of women’s empowerment and financial development on growth and employment in selected African countries. The casual analysis is carried out on selected variables. The investigations involve four categories, that is, the African economies are divided into three regions based on the World Bank income groups and the aggregate model, which comprises all the countries in the regions.

The main findings are as follows: panel unit root tests at different levels and first differences, confirming that all of the variables in the study are non-stationary at the level but stationary at the first difference. After confirming that all variables are integrated at order one, the cointegration test is performed. The long-run result shows that women’s empowerment through secondary school enrollment promotes long-run economic growth and employment in upper-medium-income countries and lower-medium-income countries. However, the result depicts the non-significance of women’s empowerment on economic growth and employment in the low-income countries. Likewise, the interactive of women’s empowerment and financial development to promote output and employment is not statistically significant in the long run in the lower-medium-income countries and the low-income countries. While in the upper-medium-income counties, despite the significance of the interactive of women’s empowerment and financial development to promote output and employment, the multitude was less than 1. The panel causality result in the upper-medium-income countries shows indicates that there is feedback between women employment and economic growth; an attempt to improve women’s empowerment will promote economic growth and vice versa. In addition, the unidirectional relationship from the financial development indicators to economic growth in the lower-medium-income countries means that financial development has a direct influence on growth, while in low-income countries, it indicates that women’s empowerment has a direct influence on employment.

Recommendations

Investments in education to empower women with interactive financial development could be catalytic. The multiplier effects on the lives of women and girls, including future generations in increasing economic growth and employment levels, are inevitable, as stressed by MDG. To this end, this study suggests recommendations to improve the situation. The present study recommends that the government implement policy to strengthen the financial sector, given the outcome on economic growth and employment in upper-medium-income economies. Thus, sufficiently sustaining economic growth requires improvement in women’s empowerment, as noted by the MDGs Goal 3 and SDG Goal 4. To optimize the impact of women’s empowerment on the economy, especially in Lower Medium Income and low-income economies, the educational system must be restructured with the incentive to promote women’s empowerment. A higher level of financial development is more likely to encourage investment via access to capital. As a result, the combined benefits of women’s empowerment and finance on economic growth and employment may be more significant than their separate contributions. So, there is a need to position the countries to encourage women’s empowerment and be mindful of creating comprehensive policies that create awareness for women to participate in financial decisions to increase economic growth and employment levels.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.