Abstract

In this paper, the Mainland-Hong Kong Stock (MHKS) Connect Program is used as a quasi-natural experience to study the relationship between foreign institutional investors and environmental innovation. Using the sample of the Chinese mainland A-Share market industrial firms from 2012 to 2019 and Difference-In-Difference model, we find a promoting effect of the foreign institutional investors on the mainland firms’ environmental innovation. The mediating effect tests prove that foreign institutional investors inspire environmental innovation through monitoring channel (supervising the environmental innovation), insurance channel (tolerating innovation failures) and knowledge spillover channel. It is noteworthy that only firms in the regions of high innovation capacity benefit from the knowledge spillover channel. Our study implies that environmental innovation can benefit from the opening-up of the stock market if it can attract foreign institutional investors who fulfill the roles of monitoring, insurance and knowledge spillover.

Keywords

Introduction

Environmental pollution concerns have increased worldwide in the past few years (Y. Zhang et al., 2018). With the development of the economy, the utilization of natural resources is gradually growing (Albort-Morant et al., 2016; Hancevic, 2016; Hui et al., 2021). However, the increased utilization of natural resources harms the environment and the ecological carrying capacity (Asadi et al., 2020). To realize the green and sustainable development, China is actively participating in global environmental governance and promoting research and development (R&D) and innovation.

The concept of Environmental, Social, and Governance (ESG) responsible investment, which can avoid environmental and governance risks, has been pursued by global investors since the United Nations’ Principles for Responsible Investment (UN PRI). Professional investors are more willing to invest in firms with good ESG responsibility (M. Wang & Chen, 2017). Foreign institutional investors tend to consider the long-term interests of firms, pay more attention to ESG performance, and show strong ESG investment preference in the Chinese A-share market (F. Z. Zhou et al., 2021). The liberalization of the Chinese stock market aims to increase the opportunities for high-quality overseas capital to invest in the mainland firms. It may be an opportunity to promote environmental innovation in Chinese firms.

The implementation of the Mainland-Hong Kong Stock Connect Program (hereafter called the MHKS Connect Program) marks the successful interconnection of the stock exchanges in Shanghai, Shenzhen, and Hong Kong. The original intention of the interconnection was to attract mature foreign investors from the developed capital market, promote value investment, and standardize the market mechanism. Though domestic investors and the Chinese government attach great importance to the MHKS Connect Program, there is not much literature on how the liberalization policy affects the environmental innovation behaviors of the Mainland firms. Existing research has mostly chosen the single policy of the Shanghai-Hong Kong Stock Connect as a quasi-natural experiment, which makes the results subject to confounding effects (T. L. Zhong & Lu, 2018; K. Zhong et al., 2018). Some research takes the capital markets of multiple countries as the research objects (Bekaert et al., 2005; Luong et al., 2017). Due to the lack of appropriate exogenous policy shocks, they are challenged by the potential endogenous problems and get different research results on the same subject. For example, Gupta and Yuan (2009) believe that stock market liberalization can ease firms’ financing constraints. D. Li et al. (2011) show that the liberalization can promote the introduction of foreign advanced technology and improve firms’ risk tolerance and corporate governance. They all contribute to enhancing the innovation capability of firms. Some scholars believe that the stability of the capital market will be affected by the “Herd Behavior” caused by the stock market liberalization (Bae et al., 2004). The distributed implementation of the MHKS Connect Program has provided a relatively clean experimental environment for the research on the liberalization of the Chinese stock market (Huang et al., 2020). The Shanghai-Hong Kong Stock Connect lifted the trading restrictions on some mainland stocks at the end of 2014, and the Shenzhen-Hong Kong Stock Connect lifted the trading restrictions at the end of 2016. The step-by-step implementation of these two systems provides an exogenous research scene for academic research.

This paper takes Chinese A-share market industrial firms from 2012 to 2019 as samples and the implementation of the MHKS Connect Program as a quasi-natural experiment. Using a Difference-In-Difference approach, it explores the mechanisms through which foreign institutional investment following the stock market liberalization affects environmental innovation. This research will shed light on the foreign institutional investors’ role in promoting environmental innovation activities. Although Chinese firms have achieved substantial progress in innovation quantity, there is still much space for the improvement of innovation quality (Yuan & Xiang, 2018). With the reduction of restrictions on foreign investment in the Chinese mainland capital market, foreign investors have gradually acquired the ability to influence the Chinese domestic capital market. It is necessary to investigate foreign investors’ role in promoting mainland firms’ environmental innovation.

This paper aims at investigating the relationship between stock market liberalization and environmental innovation and explore the channels through which foreign institutional investors changes firms’ innovation activities because it is essential for both the development of Chinese financial market and the green transformation of Chinese economy. The first marginal contribution is that this paper evaluates the role of the foreign institutional investors in inspiring environmental innovation. The industrialization and economic growth of developing countries are restricted to environment and resources. Green environmental innovation is an important and effective way to give attention to both the economic growth and the environment protection. This research provides the evidence that stock market liberalization is an important channel to attract high-quality investment that push forward industrial upgrades and green transformation.

Secondly, this research investigates the underlying mechanisms through which foreign institutional investors contribute to environmental innovation. Our findings reveal that foreign institutional investors can promote environmental innovation through supervising the environmental innovation activities, tolerating innovation failures, and bringing knowledge spillover into the investee firms. Value investors with ESG investment philosophy can fulfill these mechanisms. For developing countries whose stock market is not yet ripe for opening-up, cultivating value and ESG investment philosophy in their domestic investors will benefit their environmental innovation. The valuable implications we get from this study is elaborated in the conclusion part. For China, the experience is the bedrock for further opening-up and liberalization of the stock market. For other developing countries, China’s experience may be used for reference.

Thirdly, the study mitigates confounding effects and reduces the interference of endogenous problems based on the step-by-step implementation of the MHKS Connect Program. Study on Chinese stock market mostly starts with the single Hong Kong-Shanghai stock connect, which will simultaneously lead to the interference of other influencing factors. Study on other countries do not choose exogenous policies, which will disturb the research by the differences between different capital markets. The MHKS Connect Program contains an exogenous policy (Shanghai/Shenzhen-Hong Kong Stock Connect) and a single country (China). These two elements help address the existing literature on the choice of their exogenous policy.

The rest of the paper includes five parts: section “Literature Review” is literature review; section “Research Hypotheses” develops the research hypotheses; section “Data and Method” presents the data and empirical strategies; section “Results and Discussion” presents empirical results and discussions; section “Conclusions and Implications” summarizes the findings and implications. Figure 1 lay out the organization of this paper.

The organization of the research.

Literature Review

This paper mainly involves three aspects: the economic effects of the stock market liberalization, the influencing factors of firms’ environmental innovation, and the effect of stock market liberalization on innovation.

Economic Effects of Stock Market Liberalization

There are positive and negative opinions on the economic effects of stock market liberalization. The stock market liberalization has attracted many foreign rational value investors into emerging capital markets such as China (Y. S. Chen et al., 2019). Rational value investors benefit the stock market in several ways. They can help reduce heterogeneous fluctuations in stock prices and improve the stability of stock markets (K. Zhong et al., 2018). They can promote the integration of company-specific information into stock prices to improve the information content of stock prices (T. L. Zhong & Lu, 2018). They can also enhance the worth of non-financial information, improve corporate investment efficiency, corporate governance structures and governance effectiveness (Bekaert, 2000; Y. S. Chen & Huang, 2019; Lian et al., 2019a, b). However, some scholars believe that liberalizing capital markets in emerging economies is challenging (Ji & Zang, 2019; L. Lei et al., 2018; Lv & Wan, 2017). For example, foreign investors may have short-term speculation (Choe et al., 2005), and ignore the company’s long-term value (Callen & Fang, 2013; Choe et al., 2005). The “hot money” effect will lead foreign investors to pursue higher short-term returns, thus ignoring firms’ long-term value (Brennan & Cao, 1997). Due to the time and cost of supervision, professional managers’ inaction cannot be effectively supervised (Zhu & Yi, 2020).

Influencing Factors of Firms’ Environmental Innovation

There are many explanations for environmental innovation. Carrion-Flores and Innes (2010) think it emphasizes resource conservation and environmental improvement. According to Dai et al. (2015), J. Y. Li et al. (2019), and Xiao et al. (2021) environmental innovation is a green sustainable development activity focusing on ecological performance. For He et al. (2018) and X. Q. Wang and Ning (2020) environmental innovation is an innovative movement that considers social responsibility and economic development. Similarly, ecological innovation is a strategic activity with traditional innovation characteristics to solve ecological problems and promote rational allocation of resources (Rennings, 2000; Yu et al., 2020). Most existing studies discuss the influencing factors of ecological innovation from the perspective of government environmental regulation. For example, the pilot emissions trading policy has helped some pilot firms realize ecological innovation (Qi et al., 2018). The combination of government ecological regulation and subsidies has promoted environmental innovation (Li, 2021). The emission charging and information disclosure mechanism have “pushed” firms’ environmental innovation (Z. Chen et al., 2021; Q. Y. Li & Xiao, 2021; X. Q. Wang et al., 2020). Unlike these views, Z. Chen et al. (2021) believe that the “Weak Porter hypothesis” fails to realize in the Chinese current carbon trading market. The Carbon Emissions Trading Pilot Policy has reduced the proportion of green patents. Other factors such as ecological awareness, education level, and employment background of executives (Peng & Wei, 2015), Knowledge coupling and redundant resources (Yu et al., 2019), Corporate governance (F. Z. Wang & Chen, 2018), technological capability (S. Y. Lei et al., 2014), and policy uncertainty (Hu et al., 2023; W. Zhou et al., 2022) can also influence environmental innovation.

The Effect of Stock Market Liberalization on Firms’ Innovation

There is a specific correlation between liberalization and firms’ innovation. Scholars generally believe that the stock market liberalization has significantly improved firms’ innovation. Some scholars have found that the MHKS Connect Program improves firms’ innovation. Ma et al. (2019) test three mechanisms through which liberalization affects the R&D scale by the mediating effect model. These mechanisms reduce credit dependence, improve external supervision and total factor productivity. With a quasi-natural experiment, Huang et al. (2020) also conclude that liberalization is conducive to firms’ innovation. The alleviation of information asymmetry and improvement of environmental awareness are two plausible mechanisms to promote environmental innovation (T. T. Li et al., 2022; Sha et al., 2022). Research on the trading system of the Shanghai-Hong Kong stock connection show that the Hong Kong-Shanghai stock connection has significantly improved the innovation level of the target firms. R. S. Feng and Wen (2019) find that the Hong Kong-Shanghai Stock Connect promotes the innovation of Chinese state-owned firms by reducing financing constraints and improving stock liquidity. Zhu and Yi (2020) found the intermediary role and regulatory effect of alleviating professional managers’ professional anxiety in the Shanghai-Hong Kong Stock Connect promoting firms’ innovation. Y. Liu and Zang (2021) draw similar conclusions based on the analysis of firms’ heterogeneity. Reducing financing constraints and information disclosure quality are also proved to be channels through which capital market liberalization promotes green innovation in China (G. F. Feng et al., 2022).

Other scholars analyzed the positive effect of institutional investors on firms’ innovation based on their shareholding. The Qualified Foreign Institutional Investor (QFII) can promote firms’ innovation by improving the information content of stock prices, reducing the sensitivity of executive compensation to short-term corporate performance and signal effect (J. C. Jiang et al., 2021; Tan & Yang, 2020). The characteristics of industry and executive positions play a regulatory role in QFII's impact on firms’ innovation (Zheng & Zhu, 2019). Pressure-resistant institutional investors will push firms to engage in substantial environmental innovation (J. Li & Yu, 2022). In addition, Y. Zhang et al. (2017) find that IPO can encourage firms’ innovation by easing financing constraints and promoting the construction of talented teams. Hsu et al. (2014) selected the capital markets of several countries as research samples. They found that the stock market development can positively affect firms’ innovation performance more than bank credit.

To sum up, foreign investors are the main body of research on stock market liberalization. Research on Chinese stock market is mainly about their impact on stock price fluctuation, enterprise investment efficiency, corporate governance, and natural economic development. Foreign scholars tend to take the global capital market as the research scenario. The research on the factors of firms’ environmental innovation is mainly about government environmental regulation. There are rare topics about how capital market liberalization affects firms’ environmental innovation. With the gradual popularization of ESG’s concept of responsible investment and the low-carbon goal of China, it is necessary to do further investigation on the relationship between capital market liberalization and environmental innovation so as to providence experience for green and sustainable development.

Research Hypotheses

The Connect Program, Foreign Investors, and Environmental Innovation

Many countries have liberalized their capital markets and relaxed the conditions for foreign investors to enter their domestic capital market as so to promote the reform of domestic financial system (Lian et al, 2019a; Zou et al., 2019). China has made considerable progress in liberalizing its capital market. The Shanghai-Shenzhen-Hong Kong Stock Connect has enabled the interconnection of the capital markets from Mainland to Hong Kong (Luo & Wu, 2018). It is an essential step toward the two-way liberalization and improving the investor structure of the Chinese stock market. Since establishing the Chinese B-share market in 1992, the Chinese stock market has been liberalized mainly by the dual institutional arrangements under the QFII/RMB Qualified Foreign Institutional Investor (RQFII) framework and the MHKS Connect Program (X. F. Yang, 2021). China has lifted the restrictions on the investment quota of QFII and RQFII, which increases the importance of foreign institutional investors in Chinese capital market.

Mature investors from developed capital markets can convey the value investment concept to emerging capital markets (Y. S. Chen et al., 2019). The foreign investors who invest in China’s A-share market through the MHKS Connect Program are value investors, and pronouncedly promote mainland firms’ green innovation (T. T. Li et al., 2022). Scholars generally believe that QFII has improved the innovation output. The Chinese government has formulated environmental regulation policies to protect the environment. Carrying out environmental innovation becomes an important way to fulfill corporate social responsibility and environmental regulation (X. Q. Wang & Ning, 2020). Firms can obtain long-term and stable profits through “risk compensation” (B. Liu & Wang, 2021; D. Zhang & Vigne, 2021). As the shareholders of Chinese mainland firms, foreign institutional investors may also realize the importance of environmental responsibility and pay attention to both conventional financial indicators and ecological issues (He et al., 2018). Thus, foreign institutional investors may promote the environmental performance of the investee firms (Ahmad et al., 2021). It leads to our first hypothesis:

Monitoring Channel

The principal-agent problem reduces the willingness of corporate managers to innovate (Zhu & Yi, 2020) and triggers moral hazards (Y. Liu & Zang, 2021). Study on the Chinese listed high-tech companies reveals that the great power of CEO negatively is negatively related to firms’ innovation performance (X. Zhong et al., 2021). Firms’ innovation may be hindered by principal-agent problem, as the top managers pay more attention to their personal interests and miss out on promising investment projects. On the one hand, innovation needs managers to devote much effort and pay more private costs (X. Y. Jiang et al., 2019). On the other hand, innovation failure risks their human capital (P. Wright et al., 1996). These factors will discourage the managers from implementing environmental innovation. To mitigate the hindrances, companies must introduce more effective monitoring mechanisms to ensure that innovation activities are carried out correctly (Bernstein, 2015).

Foreign institutional investors, are believed to have a higher willingness corporate governance capacity (J. C. Jiang et al., 2021; J. L. Yang et al., 2018) and improve firms’ investment efficiency and value (Salehi et al., 2022), especially those from developed market because institutional qualities at the national level can shape firm level sustainable activities (Al-Mamun & Seamer, 2022; Rahi et al., 2023). They can play an influential role in monitoring opportunistic behavior (Aggarwal et al., 2011; Gillan & Starks, 2003). Aggarwal et al. (2011) find that the “voting with feet” behavior of foreign institutional investors improved corporate governance and restrained the opportunistic behavior. Gillan and Starks (2003) suggest that foreign institutional investors can act as firm supervisors. They can participate in the firms’ decision-making activities and actively intervene in the value creation process. In addition, investors from developed capital markets usually have rich investment experience. They can obtain stable returns through reasonable valuation and have few connections with Chinese mainland firms (Gillan & Starks, 2003). These characteristics make them act as a better supervisor to discipline inefficient investment behavior (e.g., management short-sightedness). Therefore, foreign investors can regulate opportunistic and short-sighted corporate management. It leads to our second hypothesis:

Insurance Channel

The Chinese stock market has many short-term investors (Li & Tu, 2015) who are more concerned with short-term corporate performance. These investors are keen to follow subtle changes in the stock market and trade with high frequency, which can easily cause stock price volatility. Frequent trading by short-term investors enhances stock liquidity, and better stock liquidity further increases short-term performance pressure on corporate executives (Fang et al., 2014). In the face of short-term performance pressure, corporate managers may selectively abandon environmental innovation to ensure short-term performance. The study on institutional investors of the Chinese market shows that the site visits of the institutional investors who are sensitive for short-term performance will induce firms to lower their innovation quality to cater to investors (J. Li & Yu, 2022). Such institutional investors have low tolerance for innovation failures. In China, environmental policy uncertainty is another factor that inhibit corporate green investment (Hu et al., 2023) and increase corporate performance pressure. Chinese mainland firms need investors who are more tolerant to ensure their investment decisions are not distorted by short-term interests.

Sophisticated investors from developed capital markets can not only use their superior information gathering and processing skills to enhance the information content of share prices (T. L. Zhong & Lu, 2018) but also guide mainland investors back to value investment (Y. S. Chen et al., 2019). Investors who uphold the concept of value investment imply that they will make investment decisions based on the long-term value of companies. This characteristic will help alleviate short-term speculation and increase tolerance for poor short-term performance, which is necessary for motivating innovation (Ederer & Manso, 2013; Manso, 2011). Compared to domestic institutional investors, foreign institutional investors have a more diversified international portfolio and show more tolerance for the risk of failure in innovative projects (Grinblat & Keloharju, 2000). It implies that managers of Mainland Chinese companies can gain incentives to innovate and alleviate short-term performance pressure. It leads to our third hypothesis:

Knowledge Spillover Channel

The dynamic flow of knowledge and innovation requires business networks (D. T. Wright & Burns, 1998). Foreign institutional investors can use business networks to facilitate knowledge dissemination and information exchange between domestic and foreign investors, thus promoting corporate innovation (Faleye et al., 2014; Luong et al., 2017). Knowledge spillovers involve multiple types of stakeholders. Foreign institutional investors can act as a bridge for managers, investors, and even other stakeholders of domestic and foreign firms to share knowledge (Luong et al., 2017). They integrate various types of information through business networks to facilitate the flow of resources and improve the firm’s efficiency. This behavior can also reduce the cost of knowledge spillovers and improve the environmental innovation capability.

In addition, foreign institutional investors promote cross-border M&As alleviate information asymmetry (Ferreira et al.,2010). The knowledge spillover from these cross-border investment behaviors further promotes innovation activities of host country firms (Guadalupe et al., 2012). J. F. Zhang et al. (2017) find that international technology spillovers promote independent innovation in Chinese high-tech industries. Foreign institutional investors can fully exploit the value of business networks, impart advanced ideas from developed capital markets to domestic investors and bring technology and markets through cross-border M&As. Similarly, the Chinese stock market liberalization may also enhance the environmental awareness of management and produce technology spillover effect, thus improving environmental protection technology development (Sha et al., 2022). It leads to our fourth hypothesis:

Figure 2 illustrates the three channels through which foreign institutional investors affect the investee firms’ environmental innovation.

Main research hypotheses.

Data and Method

Data Source

This paper uses a Difference-in-Difference approach to examine the relationship between stock market liberalization and firms’ environmental innovation. Since environmental innovation mainly concentrates on non-financial sectors, this article selects Chinese A-share industrial firms from 2012 to 2019 as samples. The paper uses the sample firms that join the MHKS Connect Program as the treatment group and the firms that do not enter the program as control group. We exclude the samples that meet the following conditions: (a) financial and insurance companies; (b) companies treated as S.T. during the sample period; (c) companies with missing key variables, resulting in a final sample of 12,365 observations.

The patents that we use to measure environmental innovation and other firm specific data are from China Stock Market & Accounting Research Database (CSMAR) and Wind Database. The patent classification numbers are from the China Research Data Service Centre (CNRDS) and matched with the “Green List of International Patent Classification” issued by the World Intellectual Property Organization (WIPO). Thus, we divide the patents into non-green patents and green patents. All continuous variables except dummy variables are winsorized at 1% (99%) to avoid extreme values. The statistical and regression software used in this paper is stata16.

Definition and Measurement of Variables

Green patents consist of green invention patents and green utility model patents. Among them, invention patents are more technological than others (Z. Y. Sun & Qi, 2021) and can substantially affect technological progress (W. Li et al., 2016). They are rigorous in granting conditions, application process, and protection regulations (W. X. Cai et al., 2019). Therefore, we select lnGreenPatent1 as a proxy variable for environmental innovation. lnGreenPatent1 is calculated as the natural logarithm of total number of green invention patents plus 1 to eliminate the problem of right-skewed distribution. Considering the long period of environmental innovation activities and the lag between the granting and acquisition of patents, lnGreenPatent1 in period t+1 is used to measure firms’ environmental innovation in period t.

The Shanghai-Hong Kong Stock Connect and Shenzhen-Hong Kong Stock Connect took place on 17th November 2014 and 5th December 2016, respectively. The policy intervention Firms that are on list of the MHKS Connect Program get the chance to be invested by foreign institutional investors. They are classified into the treatment group. When the variable Treat equals 1, indicating that the corresponding sample firms participate the MHKS Connect Program and are identified as invested by foreign institutional investors. Otherwise, Treat equals 0 and the corresponding sample firms are in control group. Post represents the policy occurrence point-in-time variable. It equals 1 for the time after the introduction of the MHKS Connect Program and 0 for the time before the introduction of the MHKS Connect Program. DID represents the interaction term of Treat and Post (Treat*Post).

The economic characteristics of firms can affect environmental innovation. Referring to Q. Y. Chen et al. (2017) and Lian et al. (2019a), the control variables include Top1, Debt, TobinQ, Tang, Itang, Roa, Size, and lnage. Table 1 illustrates the variables and their definitions.

Definition and Measurement of Variables.

Empirical Strategy

To investigated the relationship between foreign institutional investors and environmental innovation (hypothesis 1), we estimate the following model (1) by referring to Bertrand and Mullainathan (2003):

Where i represents firm; t represents year; Control includes all the control variables Top1, Debt, TobinQ, Tang, Itang, Roa, Size, and lnage, and

To verify hypotheses 2 and 4, we use the mediating effect model referring to of Wen and Ye (2014). With regard to the monitoring channel in hypothesis 2, excess turnover rate (TRUN) is adopted to measure the degree of information asymmetry referring to Zhu and Yi (2020). Stock turnover rate can reflect the investor horizon, and is usually negatively related to the latter (R. Liu & Chen, 2006). It can also reflect the degree of market manipulation. Given the information advantage, corporate management can influence the judgment of outside investors through surplus management (Tan & Xia, 2011). A lower turnover rate implies improvement of investment horizon and effective mitigation of opportunistic behavior, which can be considered as a signal of the effectiveness of foreign investors’ monitoring and participation in corporate governance. Thus, we get the following mediating effect model for hypothesis 2:

Where, the coefficient α1 predicates the significance of the mediating effect. If the coefficient β1 and the coefficient γ2 are significantly negative, the mediating effect is significant. In addition, if the coefficient γ1 is significantly positive, it shows that investment horizon and opportunistic behavior caused by information asymmetry act as partial mediators.

For the knowledge spillover channel in hypothesis 4, we also use the mediating effect model illustrated with Equations 2–4. The mediating variable is TFP. Since it is difficult to measure knowledge spillover directly, we use total factor productivity (TFP) to measure technological progress (W. Y. Cai & Chen, 2010). The increase in TFP of firms helps to increase their R&D investment (Ma et al., 2019), and R&D investment activities are closely related to firms’ innovation capability. In addition, institutional investors’ knowledge spillover effect embodies a shift from high-innovation capacity areas to low-innovation capacity areas (Q. Zhang & Wang, 2019). In this regard, we classify firms into two groups: firms in regions with high innovation capacity (high innovation region) and firms in regions with low innovation capacity (low innovation region).

Where, lnPay is the logarithmic total compensation of the top three executives. Return on net assets (Roe) measures firm performance (C. L. Sun et al., 2021). A significantly negative coefficient β2 on the multiplicative term DID*Roe indicates that executive compensation’s sensitivity to firms’ performance decreases significantly after participating the MHKS Connect Program.

Results and Discussion

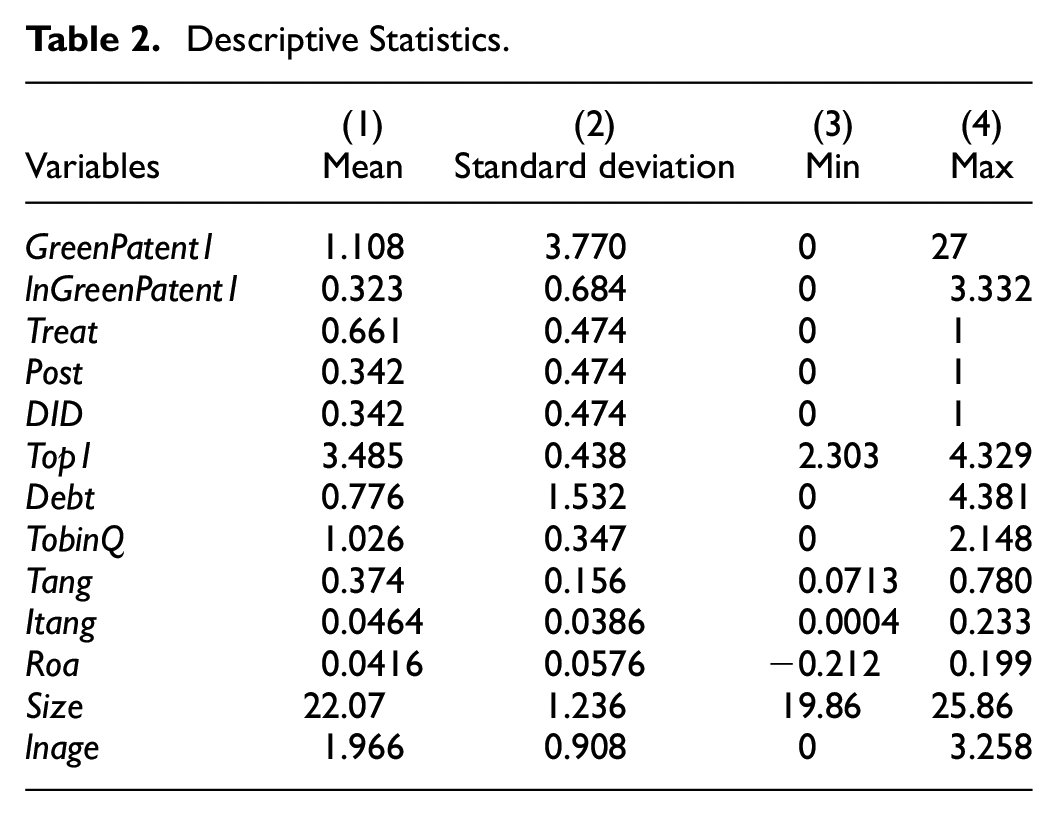

Descriptive Statistics

The descriptive statistics of the main variables are in Table 2. The mean of GreenPatent1 in the same year is 1.108. The minimum and maximum values of GreenPatent1 in the same year are 0 and 27 which shows a great difference in the level of environmental innovation among the sample companies. The mean value of the explanatory variable lnGreenPatent1 is 0.323. The standard deviation is 0.684, which shows that after the logarithmic treatment, the distribution of the explanatory variable lnGreenPatent1 is less discrete and closer to a normal distribution. In addition, the mean value of Treat*Post (DID) is 0.342, which shows that the targeted firms’ observations accounted for 34.2% of the total sample after implementing the Mainland-Hong Kong Stock Connect Program.

Descriptive Statistics.

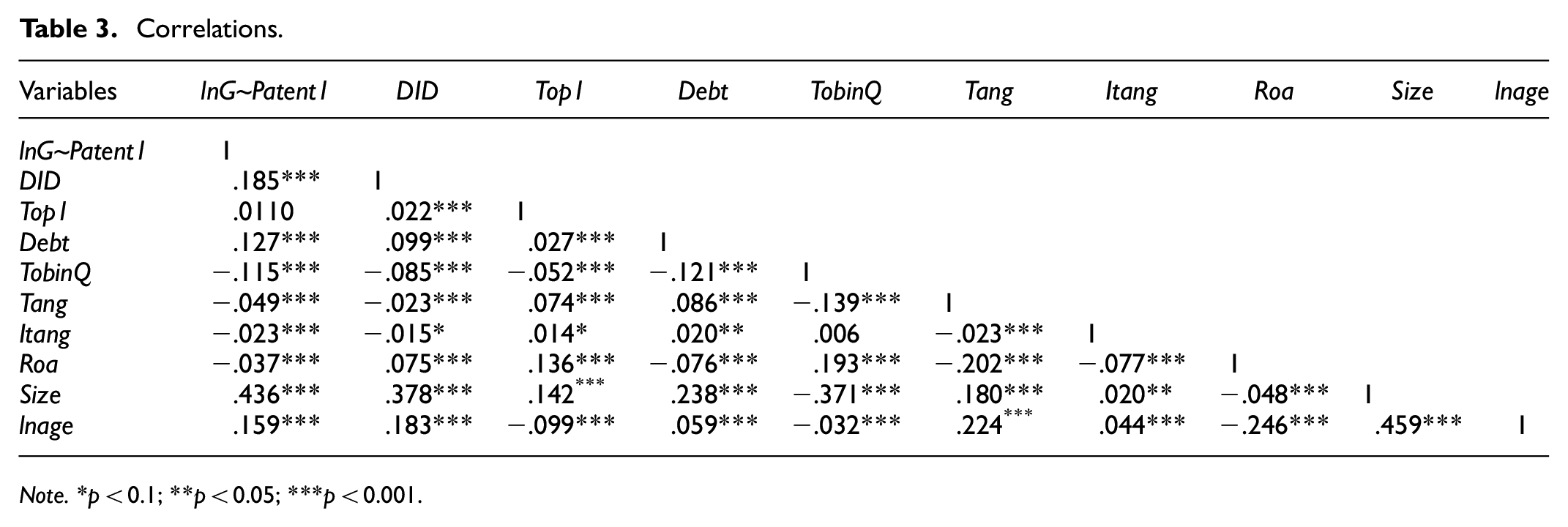

The correlation coefficient matrix of the main variables is in Table 3. The correlation coefficient on Treat*Post (DID) and lnGreenPatent1 are positive, implying that the liberalization of the MHKS Connect Program may promote firms’ environmental innovation. Most of the remaining variables showed significant correlations with lnGreenPatent1, which shows that these control variables are appropriate. Meanwhile, all of the correlation coefficients are less than .5. It means there is no multicollinearity problem in the model.

Correlations.

Note.*p < 0.1; **p < 0.05; ***p < 0.001.

Parallel Trend Test

We should take a parallel trend test before using the Difference-In-Difference method. Figure 3 shows after the implementation of the MHKS Connect Program, the parallel trend between the treatment and control group samples was no longer significant. Before the sample firms entered the MHKS Connect Program, none of the estimated coefficients was significant. After they entered, the estimated coefficients were all significantly positive. The parallel trend assumption was satisfied.

Parallel trend test.

Baseline Regression Results and Robustness tests

The baseline regression results from running empirical model (1) are reported in Table 4. For the result in column (1), we did not use any control variables except firm and year fixed effects, the coefficient on DID (Treat*Post) is significantly positive at the 1% level. After using control variables in column (2), the coefficient on DID is still significantly positive at the 1% level. The results indicate that the green invention patents increase significantly after firms participated the MHKS Connect Program, because they got the chance to be invested by foreign institutional investor. Thus, hypothesis 1 is verified. In addition, the coefficient estimate of the variable control Size is significantly positive at the 1% level. Expanding firms’ size helps increase the number of green invention patents.

Baseline Regression Results.

Note.*p < .1; **p < .05; ***p < .01. In the parentheses is the t-value.

We conducted a few more tests to ensure our results are robust. First, we advanced the implementation year of the MHKS Connect trading system by 3 years to take a placebo test. Assuming that the launch time of the Shanghai-Hong Kong Stock Connect was 2011, and Shenzhen-Hong Kong Stock Connect was 2013, we redefined the time dummy variable post, and the regression analysis was re-run. The result in column (1) of Table 5 show that the coefficient on DID (Treat*Post) is insignificant, which further excludes other influencing factors between groups from interfering with the result and proves the robustness of the baseline regression results.

Robustness tests.

Note.*p < .1; **p < .05; ***p < .01. In the parentheses is the t-value.

Second, the above empirical analysis measures firms’ environmental innovation with the natural logarithm of the total number of green invention patents lnGreenPatent1. We replaced lnGreenPatent1 with lnGreenPatent2 (the natural logarithm of the total number of green patents that include green invention patents ang green utility model patents) and lnGreenpatent3 (the natural logarithm of the number of green utility model patent). In columns (2) and (3) of Table 5, the regression results with the new dependent variables reveal that the coefficients on DID (Treat*Post) are all significantly positive at the 1% level, similar to the baseline results.

Third, we construct two research samples: (a) Using firms on the list of the Shanghai-Hong Kong Stock Connect as treatment group and excluding the Shenzhen firms from the original sample; (b) Using firms on the list of the Shenzhen-Hong Kong Stock Connect as the treatment group and excluding the Shanghai firms from the original sample. The results of the tests are in columns (4) and (5) of Table 5. The coefficients on DID (Treat*Post) is significantly positive at the 1% level. The results for both groups are similar to the baseline findings.

Fourth, it is likely that the treatment group has some differences from the control group that may disturb the results. We use the propensity score matching method (PSM) to address the endogeneity problem brought about by sample selection. The control variables in model (1) are used as the matching variables, and the matching radius is set 0.05 to match each firm in the treatment and control groups. The test result is in column (6) of Table 5. The coefficient on DID (Treat*Post) is significantly positive at the 5% level, demonstrating the results’ robustness.

Economic Mechanisms Tests

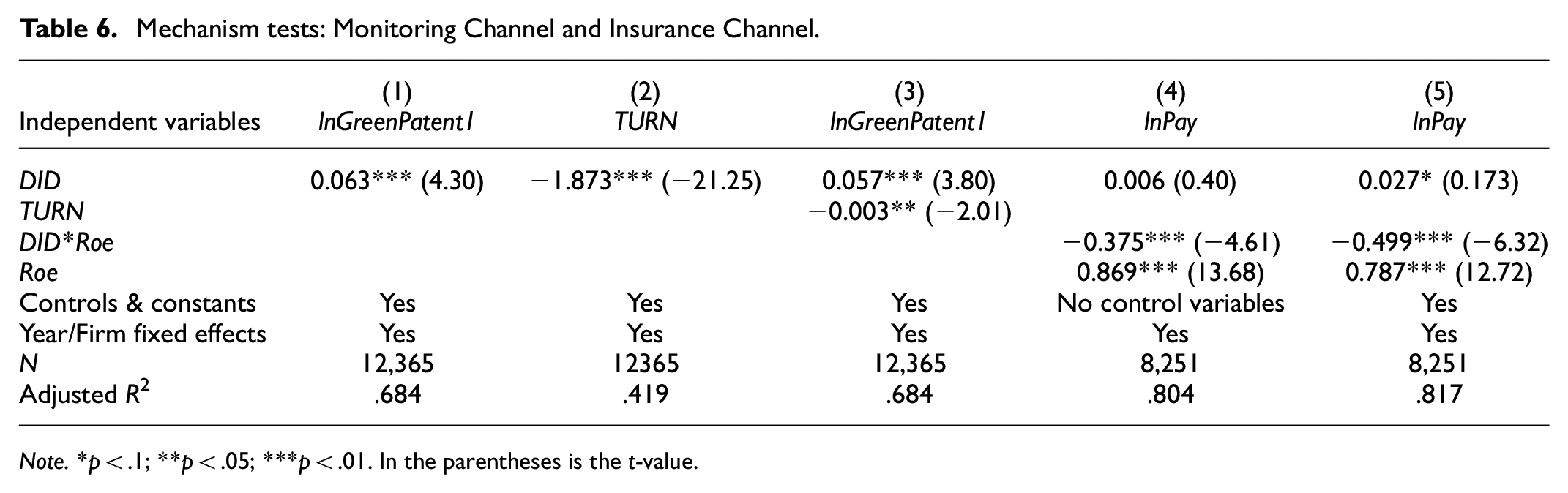

The results of the mediation effect tests for the monitoring channel are reported in the first three columns of Table 6. In column (2), the results show that the coefficient on TRUN is significantly negative, indicating that the excess stock turnover rate decreased after introducing the MHKS Connect Program. The existence of foreign institutional investors helps regulate the short-sighted and opportunistic behaviors. In column (3), the coefficient on RRUN is significantly negative, meaning the decrease in the excess stock turnover rate can promote firms’ environmental innovation. After controlling for the mediating variable TRUN, the coefficient on DID is significantly positive. Hypothesis 2 is verified that foreign institutional investors can promote environmental innovation by monitoring corporate management behavior.

Mechanism tests: Monitoring Channel and Insurance Channel.

Note.*p < .1; **p < .05; ***p < .01. In the parentheses is the t-value.

The results based on Equation 5 for insurance channel are reported in the column (4) and (5) in Table 6. In Column (4), the control variables are not included in the regression. The coefficients on Roe are significantly positive at the 1% level, demonstrating the positive relationship between corporate performance and executive compensation. The coefficients on the interaction term of DID and Roe are negative and significant at the 1% level, indicating that the sensitivity of corporate executives to short-term corporate performance significantly decreases after the introduction of the MHKS Connect Program policy. With the decrease in the sensitivity of corporate executives to short-term corporate performance, the likelihood of abandoning environmental-friendly activities due to short-term performance pressure also decreases. Therefore, the tolerance of innovation failures by foreign institutional investors will strengthen corporate executives’ willingness to engage in environmental innovation.

Table 7 presents the results of the mediating effect of knowledge spillover channel. The first three columns are for sub-sample of high innovation region. The rest three columns are for sub-sample of low innovation region. With regard to high innovation region, our results show that DID has a significantly positive effect on TFP, indicating that participating the MHKS Connect Program foreign improves firms’ technological level in high innovation region. In column (3), the coefficient on lnGreenPatent1 is significantly positive after controlling the mediating variable TFP. The coefficient on TFP is not significant. Following Wen and Ye (2014), we adopted the Bootstrap method (1,000 sampling). The confidence interval after the trial does not contain 0 (the confidence interval ranges from 0.2327 to 0.2844), indicating that the mediating effect of the mediating variable TFP was verified. For the low innovation region, we reran the mediating effect model. However, there are no significant coefficients on lnGreenPatent1 or TFP. The knowledge spillover channel is not found in firms of low innovation region. The hypothesis 4 that foreign institutional investors can improve environmental innovation by facilitating knowledge spillover is partially verified.

Mechanism Tests: Knowledge Spillover Channel.

Note.*p < .1; **p < .05; ***p < .01. In the parentheses is the t-value.

Conclusions and Implications

The liberalization of the stock market is a major ongoing financial reform by the Chinese government. Meanwhile, green and sustainable development has become an important economic and social issue. Using financial means to promote environmental innovation is necessary and plausible since the importance of finance for innovation and technological progress has been proved by many studies (Al Mamun et al., 2018; Fleiter et al., 2012; Xue & Wang, 2021). In this paper, we examine the impact of foreign institutional investment on the environmental innovation of the Chinese A-share market industrial firms using the implementation of the MHKS Connect Program as a quasi-natural experiment and DID model. The main findings are as follows.

Firms that participated the MHKS Connect Program do more environmental innovation measured with green invention patents. The MHKS Connect Program cancelled the restriction on foreign investors’ investing in Chinese mainland firms. Firms that participated the program got the chance to attract more foreign institutional investors. Foreign institutional investors with value and ESG investment philosophy can inspiring environmental innovation. We also investigated three mechanisms through which foreign institutional investors promote the environmental innovation of the mainland firms, and the findings are listed in the next two paragraphs.

Foreign institutional investors can promote firms’ environmental innovation through monitoring channel and insurance channel. Previous studies have proved that foreign institutional investors can improve corporate governance, monitoring opportunistic behavior (J. C. Jiang et al., 2021; J. L. Yang et al., 2018), and sheltering corporate executives from the pressure of innovation failure (Aggarwal et al., 2011; Gillan & Starks, 2003). Our empirical investigations based on the mediating effect model reveal that these characteristics of foreign institutional investors play a positive role in promoting environmental innovation.

Knowledge spillover channel is another mechanism through which foreign institutional investors would promote the environmental innovation of the firms in the MHKS Connect Program. However, only firms in the regions with high innovation capacity can benefit from the knowledge spillover channel.

This study has important implications in theory and practice. First, the stock market liberalization is not only an important part of the financial market development, it is also be utilized to benefit the real economy, such as the environmental innovation that is essential for green transformation. Therefore, we should keep pushing forward the financial market opening-up and perfect the investment industrial policies to attract foreign institutional investors with ESG and value investment philosophy, which would help the capital market play its role in promoting environmental innovation.

Second, the mainland firms should strengthen their innovative capacity, and the local governments should also make greater efforts to improve regional innovation environment, because macro level factors can affect micro activities (Al-Mamun & Seamer, 2022; Rahi et al., 2023). Our findings have shown that firms in regions with high innovation capacity can benefit from the MHKS Connect Program through knowledge spillover.

Third, though our findings show that foreign institutional investor can promote the environmental innovation three monitor and insurance channels, it is not the exclusive ability of the foreign institutional investors. The domestic investors can also play such a role, as long as they strengthen their role in corporate governance, pay more attention to the long-term investment value and ESG investment.

There are several potential limitations of this study that can be addressed in future research. First, we identify foreign institutional investors by the fact of participating the MHKS Connect Program. We are able to quantify the foreign institutional investment. However, we believe that the more foreign institutional investors invest, the greater their impact is. There may be a threshold for the foreign institutional investment to promote environmental innovation. Further analysis can investigate the impact of foreign institutional investors using more detailed investment data if it is available.

Second, we are able to identify the origin of the foreign institutional investors as the data is not available. Investors from different foreign markets may differ in investment styles. For example, investors from countries that attach much importance to environment protection have higher environment protection awareness, thus, more likely to support environmental innovation as noted by Al-Mamun and Seamer (2022) and Rahi et al. (2023). Investors from technologically developed countries have more experience in identifying the value of innovation. They may do better in knowledge spillover and tolerance for innovation failures. Such heterogenous features of the foreign institutional investors should be taken into consideration in the future studies.

Footnotes

Acknowledgements

We would like to acknowledge the helpful and valuable comments from the anonymous referees. All errors are our own.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by Philosophy and Social Science Fund Project of Anhui Province (granted numbers: AHSKY2020D36)

Data Availability Statement

Data is available on request.